Initiating coverage | Auto Ancillary

December 18, 2017

Menon Bearings Limited

BUY

CMP

`91.5

To benefit from CV recovery

Target Price

`114.3

Menon Bearings Limited (MBL) is a 4-decades old company operating in the

Investment Period

12 Months

business of engine bearings, Bushes, thrust washers, and aluminum die-castings.

Its 70% revenue comes from bearings segment while rest 30% comes from aluminum die-

Stock Info

castings. Exports contribute ~35% of revenue.

Sector

Auto Ancillary

Recovery in the CV volumes positive for MBL: MBL makes engine bearings, bushes

Market Cap (` cr)

515

and thrust washers for commercial vehicles (CV). Bearings business represents

Net Debt (` cr)

5

55% of its total sales, where it caters only to CVs. On that backdrop, the recovery

Beta

1.3

in the CV sales is going to be positive for MBL. Company claims that the bearings

52 Week High / Low

102/60

business has certain entry barriers, hence its customer base is sticky in nature.

Avg. Daily Volume

12,488

Capacity augmentation to cater incremental demand: With the revival in the CVs

Face Value (`)

1

and tractors, MBL is expecting a strong traction in its revenue and is in process of

BSE Sensex

33,463

increasing its bearings capacity by 30-35% over next one year. Moreover,

Nifty

10,333

company is targeting increase in its wallet share with most of its customers.

Reuters Code

MEN IN

Aluminum die-casting and exports business de-risking operations: We like MBL’s

Bloomberg Code

MENO NS

de-risking strategy by diversifying business in Aluminum die casting and exports.

The die casting business has strong clientele like Honeywell, whereas in exports its

Shareholding Pattern (%)

clients are Cummins, John Deere, etc. The aluminum die casting business is

expected to grow at a faster rate (~2x over next two years) due to the new

Promoters

74.7

contracts, particularly Honeywell. The growing exports are expected to boost the

MF / Banks / Indian Fls

0.0

margins from current 27% to ~28-29% over next three years.

FII / NRIs / OCBs

0.0

Outlook and valuation: We expect MBL to report net revenue/PAT CAGR of

Indian Public / Others

25.3

15.0%/17.8% respectively over FY2017-20E due to recovery in CV volumes,

addition of clients, increasing wallet share and rising aluminum die casting and

Abs. (%)

3m 1yr

3yr

exports business. We expect MBL to continue report EBITDA margins between 28-

29% and ROE of 27-29% during this period. We also expect company to pay

Sensex

4.0

26.2

22.3

dividend at 30-40% payouts. At the CMP of `92, the stock trades at a P/E of 16x

Menon Bearings

5.2

29.4

238.8

its FY2020E EPS of

`5.7. We initiate coverage on the stock with a Buy

recommendation and Target Price of `114 based on 20x FY20E EPS, indicating

Price Chart

an upside of 25% from the current levels.

120

Key Financials (Consolidated)

90

Y/E March (`cr)

FY16

FY17

FY18E

FY19E

FY20E

60

Net Sales

111

124

139

162

188

% chg

7.9

11.0

12.0

17.0

16.0

30

Net Profit

15

19

23

27

32

0

% chg

28.8

29.2

18.6

19.2

17.7

OPM (%)

26.0

27.0

28.0

29.0

29.0

EPS (Rs)

2.7

3.4

4.1

4.9

5.7

P/E (x)

34.5

26.7

22.5

18.9

16.0

Source: Company, Angel Research

P/BV (x)

9.9

8.0

6.5

5.4

4.4

RoE (%)

28.6

30.0

29.0

28.4

27.6

RoCE (%)

38.0

33.0

34.4

35.1

35.1

EV/Sales (x)

4.7

4.2

3.7

3.1

2.6

Shrikant Akolkar

EV/EBITDA (x)

17.9

15.5

13.2

10.7

9.0

022 - 3935 7800 Ext: 6846

Source: Company, Angel Research; Note: as CMP of Dec 15, 2017

Please refer to important disclosures at the end of this report

1

Initiating coverage | Menon Bearings

Menon Bearings at a glance

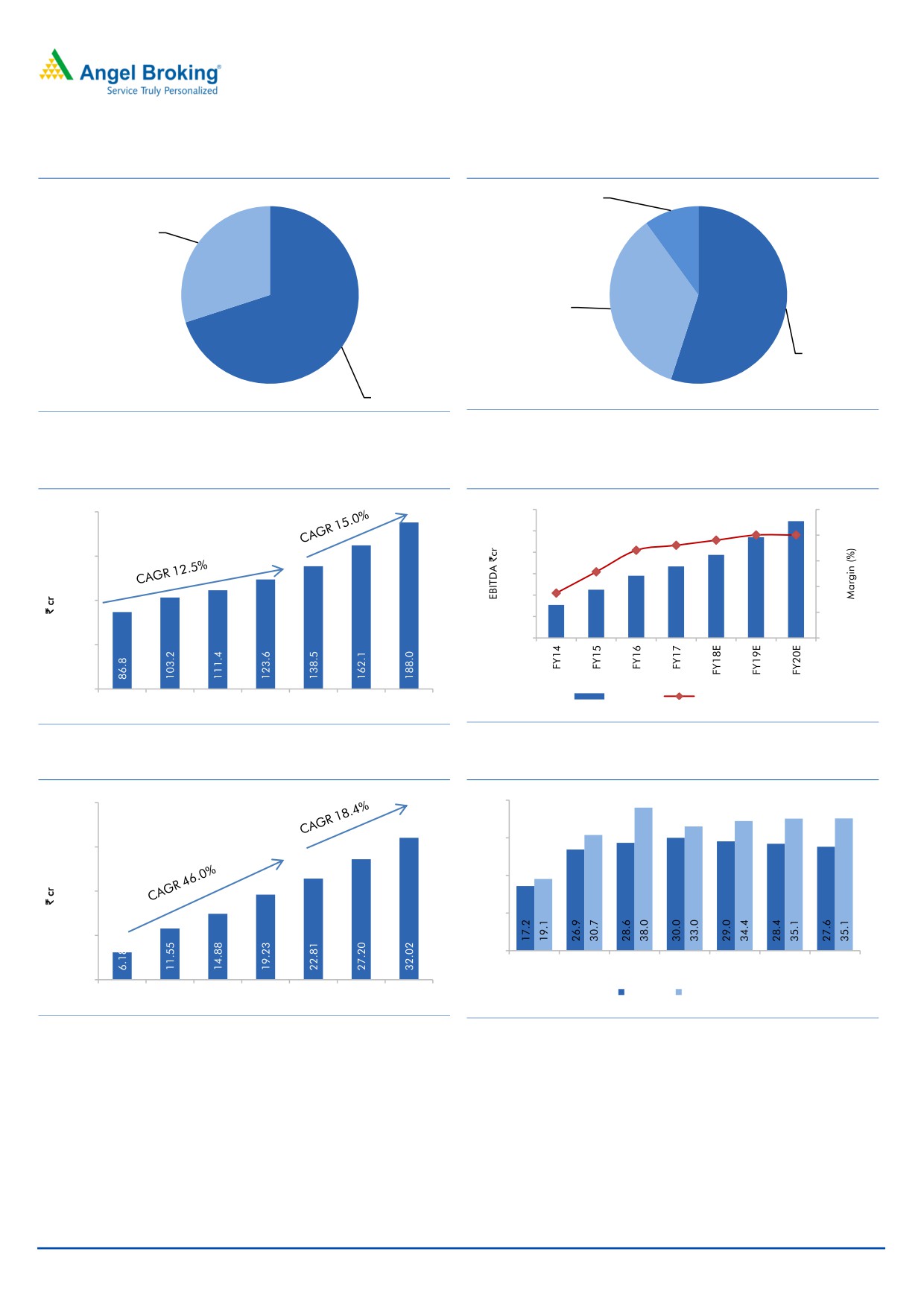

Exhibit 1: Bearings is the largest segment

Exhibit 2: OEMs contribute 55% of the revenue

Aftermarket,

Aftermarket,

10.0%.0%

Aluminum die

castings, 30%

Exports, 35.0%

OEMs, 55.0%

Bearings, 70%

Source: Company, Angel Research

Source: Company, Angel Research

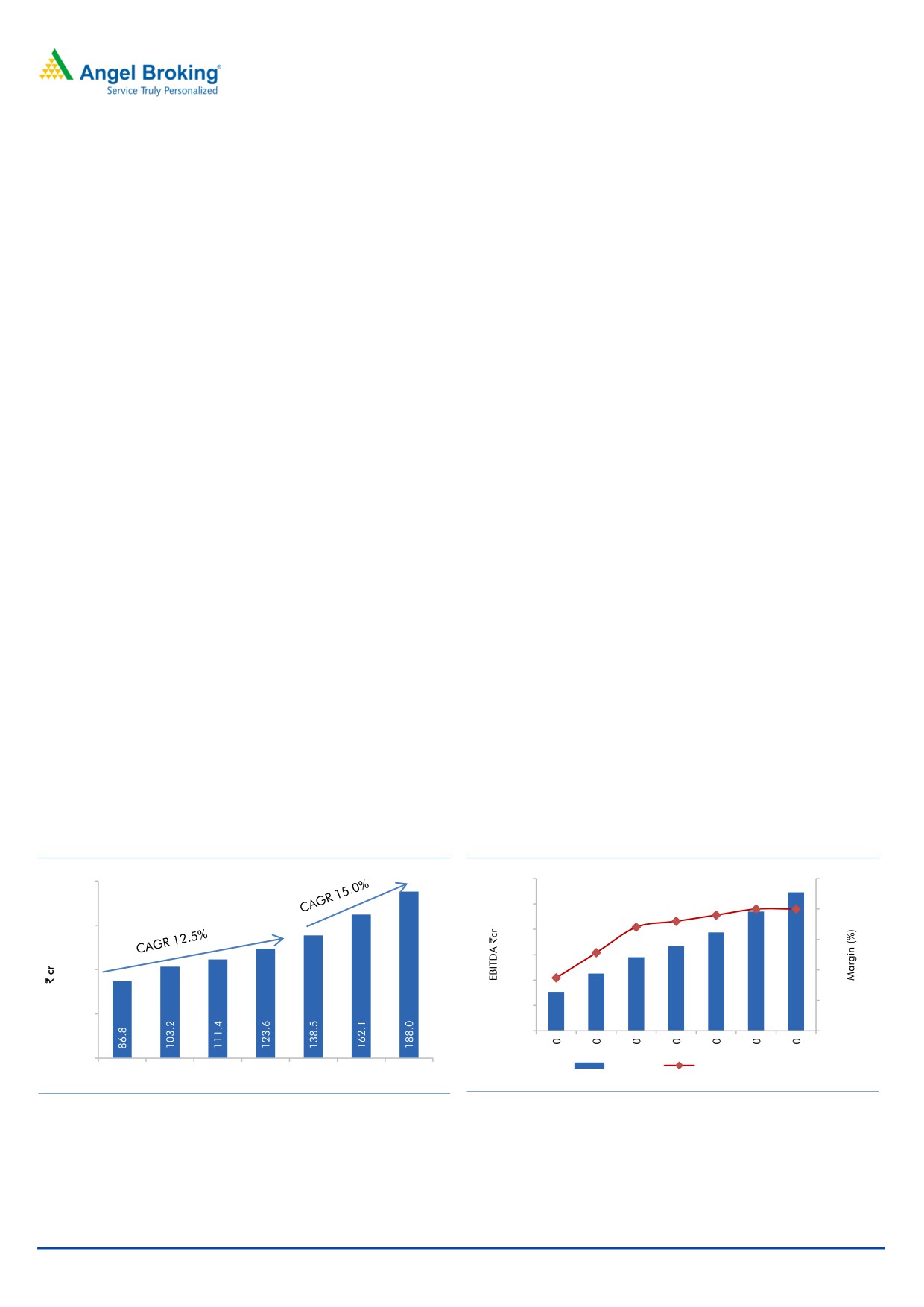

Exhibit 3: 15% revenue CAGR over next three years

Exhibit 4: Margin profile sustainable

200.0

60.0

29.0

34

29.0

28.0

50.0

27.0

29

26.0

150.0

40.0

21.8

24

30.0

17.7

19

20.0

100.0

14

10.0

0.0

9

50.0

0.0

EBITDA

EBITDA margins

FY14

FY15

FY16

FY17 FY18E FY19E FY20E

Source: Company, Angel Research

Source: Company, Angel Research

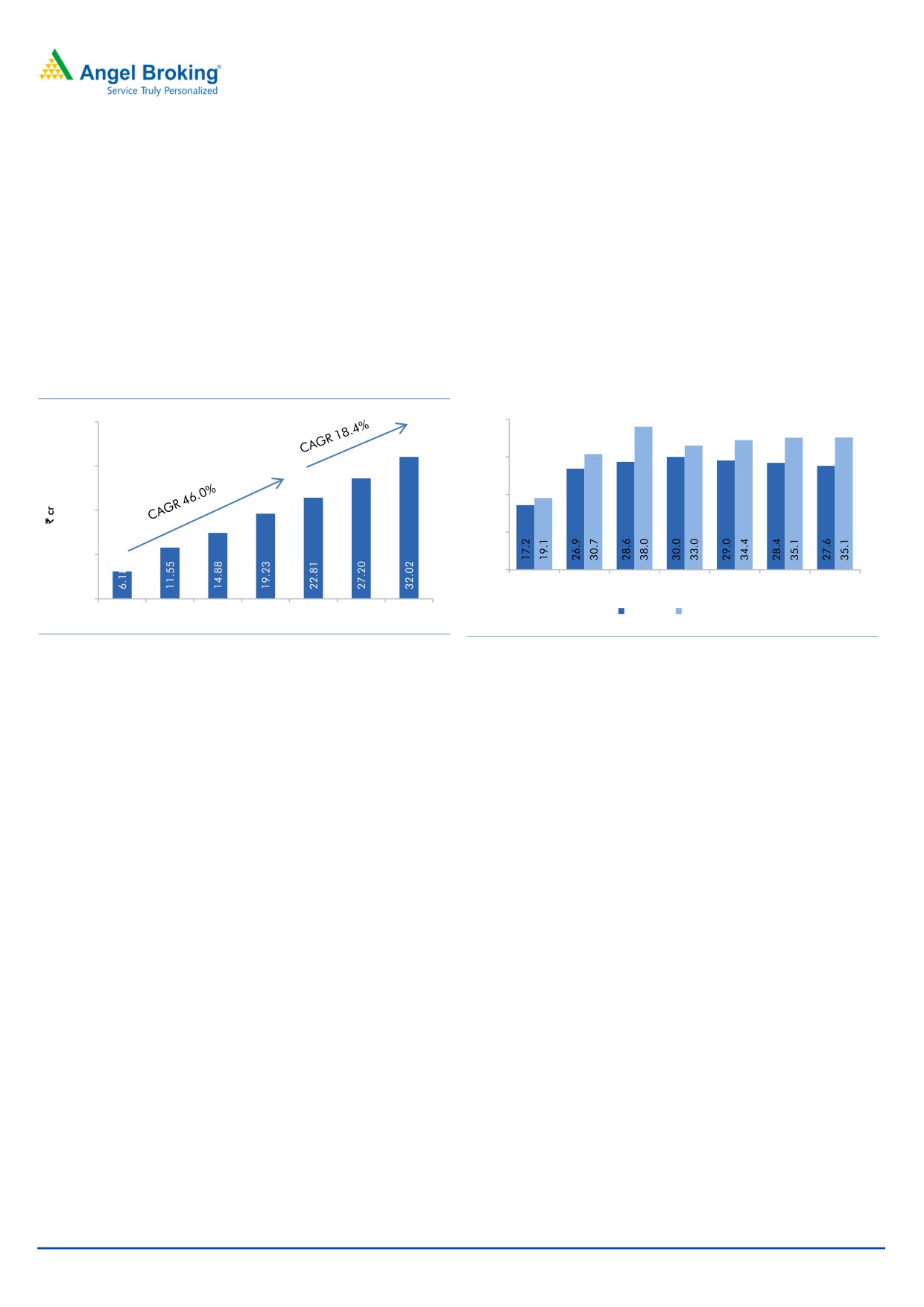

Exhibit 5: 18.4% PAT CAGR over next three years

Exhibit 6: Sticky model allows ROE/ROCE expansion

40.00

40.0

30.0

30.00

20.0

20.00

10.0

10.00

0.0

FY14

FY15

FY16

FY17

FY18E FY19E FY20E

0.00

FY14

FY15

FY16

FY17 FY18E FY19E FY20E

ROE (%) ROCE (%)

Source: Company, Angel Research

Source: Company, Angel Research

December 18, 2017

2

Initiating coverage | Endurance Technologies

About company

Menon Bearings Limited (MBL) is engaged in the manufacturing of bi-metal engine

bearings; bushes and thrust washers for light and heavy automobile engines; two

wheeler engines, and compressors for refrigerators, air conditioners and others. It

also offers aluminum die casting components. Company exports its products to the

United States, the United Kingdom, Italy, France, China, Mexico and Brazil, among

others

Its product portfolio includes following

Bearing products - bearings for connecting rods, bearings for crank shafts,

flanged bearings and tri-metal bearings.

Bushes - truncated bushes for connecting rods; ball indented bushes; bushes

for connecting rods; cam shafts; rock shafts, and rocker arms.

Thrust washers - washers with thrust face contours and ring type thrust

washers.

Aluminum products - engine components, gear case covers, clutch assembly,

cylinder heads for automobile engines, break parts, engine parts, portable

tools and fuel pump parts.

Exhibit 7: Marquee customers in the portfolio

Source: Company, Angel Research

Key Management Personnel

Mr. R D Dixit - Chairman and Managing Director

Mr. Dixit is associated with Menon Group for more than 50 years. He is currently

CMD of Menon bearings and also holds directorship in Menon Pistons Limited. He

is a Bachelor of Mechanical Engineering and has been with MBL since 1992.

Mr. Nitin Menon - Vice chairman and Joint Managing Director

He is a promoter of the company associated with the MBL since 1995. He has

experience in running businesses in automobile, agriculture and allied sectors. He

has a degree in Commerce.

December 18, 2017

3

Initiating coverage | Endurance Technologies

Investment Rationale

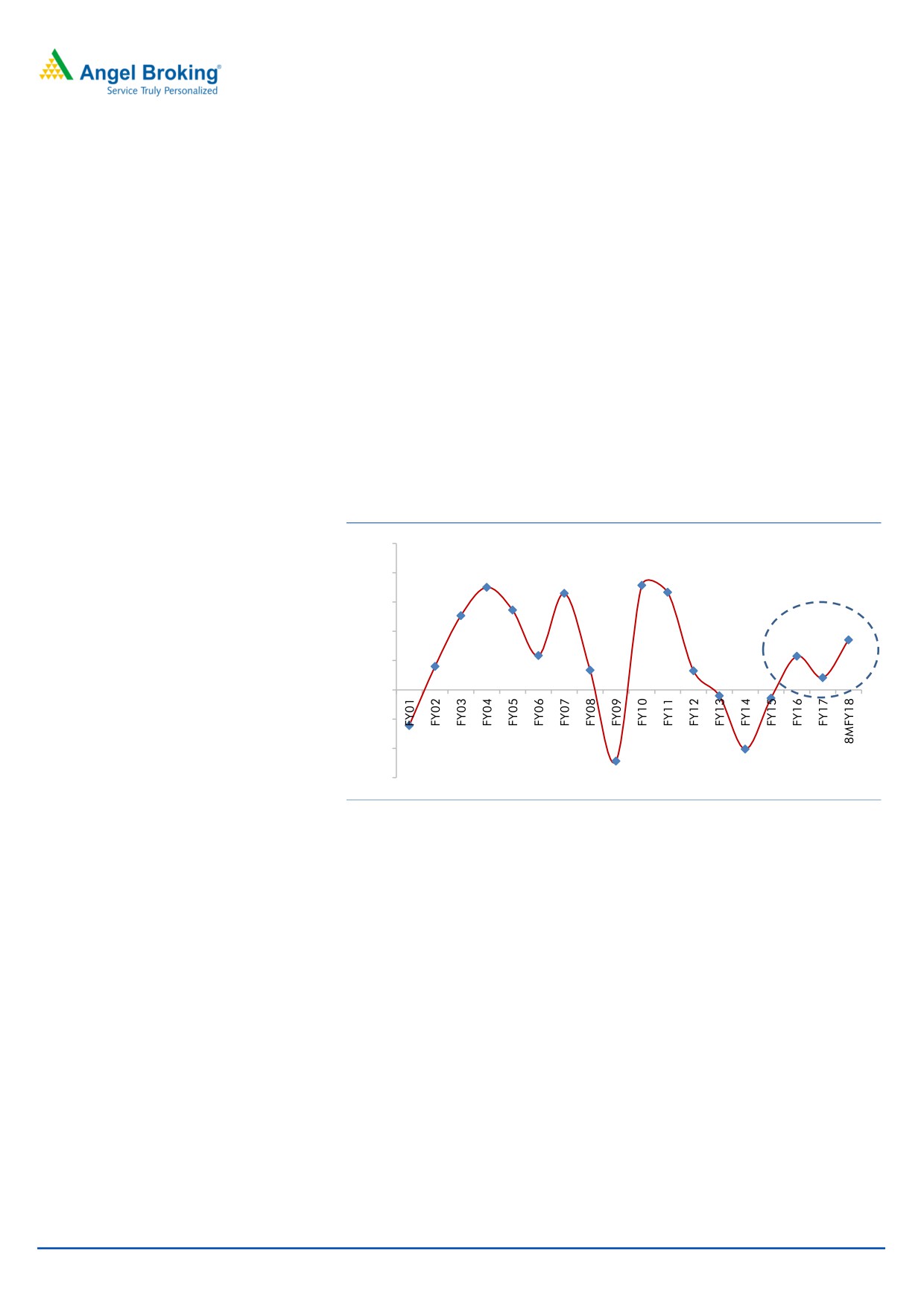

CV market recovery to be positive for Menon Bearings: After the slump of three

years (FY13 to FY15), the domestic CV volumes have been recovering since FY16.

While the demonetisation in Nov-16 and BSIII to BSIV transition in April-17

affected the CV sales in FY17, the growth has come back in FY18, reflected in the

double-digit growth in 2QFY18. We continue to see strong CV volumes going

ahead due to Government’s thrust to create road infrastructure and build ~1.2cr

affordable houses by FY2022E.

On the back of strengthening of the rural economy and two nearly normal seasons

of monsoon, the demand for tractors has also come back on track. While this

remains a seasonal phenomenon, it should be noted that it has come back after

two seasons of draught prior two years. With the rising food grain production and

MSP hikes this year, we believe rural economy is expected to remain strong which

is expected to keep the tractor demand on the growth trajectory.

Exhibit 8: Recovery in the CV volumes

50%

35%

36%

40%

33%

33%

27%

25%

30%

17%

20%

12%

12%

8%

7%

7%

10%

4%

-2%

-3%

0%

-10%

-20%

-12%

-20%

-30%

-24%

Source: SIAM, Angel Research

Menon Bearings - Diversified business with marquee clients: Menon bearings is a

diversified auto ancillary, making engine bearings for the CVs/tractors and high

pressure aluminum die casting for non auto clients. The company earlier had only

bearings business which it diversified by moving in the high pressure die casting

business and exports.

In the bearings business company has customers like Tata Motors, Cummins, John

Deere, Greaves Cotton, M&M, Federal Mogul, while in the Die casting business its

customers are Honeywell, Gabriel, Royal Enfield, Mahindra and Mahindra, Tata

Motors, etc. The company has seen strong traction in the die casting business

which now contributes about 30% of the business. The exports business has been

doing well due to the strong order book from its overseas clients, contributing

~35% of the total revenue. The pie of exports has been increasing which also de-

risks its business from the volatility in the domestic CV business.

The customer concentration risk remains low for the company as no single OEM

contributes more than 7-8% of its revenue. Considering that CVs follow a

December 18, 2017

4

Initiating coverage | Endurance Technologies

particular business cycle, MBL is less dependent on a single OEM for revenue

generation.

Increasing wallet share with existing customers: While the company has diversified

customer base, its wallet share with its major customers is also increasing. For

example, share of business with Tata Motors is currently at 35-40% which is

expected to grow to ~55% going ahead. The share of business with John Deere is

also expected to grow going forward. Share with Honeywell is ~35-40% which is

also expected to rise going ahead, given that company is very bullish on its

business with Honeywell. MBL is also expecting to add more clients and in

anticipation of high growth in the bearings business, company is expanding its

manufacturing capacity.

Capacity augmentation to cater incremental demand: With the revival in the

commercial vehicles and tractors, MBL is expecting strong growth traction in its

revenue and is in process of increasing its bearings capacity by 30-35% over next

one year. The aluminum die casting business is expected to grow at a faster rate

(~2x over next two years) due to the new contracts, which includes business from

Honeywell on which MBL is extremely bullish. Similarly, company is targeting to

increase its wallet share with most of its customers.

Strong track record in growth and profitability: Owing to stickiness of clients and

diversified business model, MBL has achieved a topline CAGR of 12.5% between

FY14-FY17. Due to strict control, control, timely raw material sourcing, increasing

exports business and well integrated facilities, MBL has also seen improvement in

EBITDA margins from 22% in FY14 to 27% in FY17. We believe that MBL can

deliver top line CAGR of 15% due to improved outlook of CV business. We are

also positive on the margins as exports business is expected to grow further and

company is delivering economies of scale due to 1) entry barrier due to the long

time span required to validate the bearings and 2) strong expertise in the business.

We forecast average 29% EBITDA margins during our forecast period and

bottomline CAGR of 17.8% between FY18E-FY20E.

Exhibit 9: 15% revenue CAGR over next three years

Exhibit 10: Margin profile sustainable

200.0

60.0

34

29.0

29.0

28.0

50.0

27.0

26.0

29

150.0

40.0

21.8

24

30.0

17.7

100.0

19

20.0

14

10.0

50.0

0.0

9

0.0

EBITDA

EBITDA margins

FY14

FY15

FY16

FY17 FY18E FY19E FY20E

Source: Company, Angel Research

Source: Company, Angel Research

Strong balance sheet with healthy return ratios: The lower capex requirement has

led MBL to maintain a lean balance sheet with debt to equity ratio of 0.34x. It has

a cash of `17cr, while debt stands at `23.3cr. The balance sheet is expected to

December 18, 2017

5

Initiating coverage | Endurance Technologies

remain healthy as company does not plan to raise more debt, with additional

capex requirement of ~`20cr to be largely funded using internal accruals and

existing cash. Working capital cycle has been between 80-90 days, in line with

the industry peers (~90-100 days).

The strong balance sheet coupled with healthy business has led MBL put a strong

return profile. ROE has consistently improved from 17.2% in FY14 to 30.% in

FY17. Return on Invested Capital has improved from ~22.0% in FY14 to 43.4% in

FY17. We expect MBL to continue report EBITDA margins between 28-29% and

ROE of 27-29% over FY18E-FY20E.

Exhibit 11: 18.4% PAT CAGR over next three years

Exhibit 12: Further headroom for ROE/ROCE expansion

40.00

40.0

30.0

30.00

20.0

20.00

10.0

10.00

0.0

FY14

FY15

FY16

FY17

FY18E FY19E FY20E

0.00

FY14

FY15

FY16

FY17 FY18E FY19E FY20E

ROE (%) ROCE (%)

Source: Company, Angel Research

Source: Company, Angel Research

Outlook and valuation

We expect MBL to report net revenue/PAT CAGR of 15.0%/17.8% respectively over

FY2017-20E due to recovery in CV volumes, addition of clients, increasing wallet

share and rising aluminum die casting and exports business. We expect MBL to

continue report EBITDA margins between 28-29% and ROE of 27-29% during this

period. We also expect company to pay dividend at 30-40% payouts. At the CMP

of `92, the stock trades at a P/E of 16x its FY2020E EPS of `5.7. We initiate

coverage on the stock with a Buy recommendation and Target Price of `114 based

on 20x FY20E EPS, indicating an upside of 25% from the current levels.

December 18, 2017

6

Initiating coverage | Endurance Technologies

Income statement

Y/E March (` cr)

FY16

FY17

FY18E

FY19E

FY20E

Total operating income

111

124

139

162

188

% chg

7.9

11.0

12.0

17.0

16.0

Total Expenditure

82

90

100

115

133

Cost of Materials

38

42

48

53

62

Personnel

8

9

11

13

15

Others Expenses

36

39

41

49

56

EBITDA

29

33

39

47

55

% chg

28.6

15.1

16.2

21.2

16.0

(% of Net Sales)

26.0

27.0

28.0

29.0

29.0

Depreciation& Amort.

5

5

4

6

6

EBIT

24

28

34

41

48

% chg

33.3

15.7

21.9

19.3

17.5

(% of Net Sales)

21.9

22.9

24.9

25.3

25.7

Interest & other Charges

2

1

1

1

1

Other Income

1

1

1

1

1

(% of PBT)

2.3

2.1

3.0

2.5

2.1

Share in profit of Ass.

-

-

-

-

-

Recurring PBT

23

28

34

41

48

% chg

40.2

18.7

22.8

19.5

17.7

Prior Period & Extra. Exp.

-

-

-

-

-

PBT (reported)

23

28

34

41

48

Tax

8

8

11

13

16

(% of PBT)

36.2

30.5

32.9

33.0

33.0

PAT (reported)

15

19

23

27

32

Add: Share of earnings of ass.

-

-

-

-

-

Less: Minority interest (MI)

-

-

-

-

-

PAT after MI (reported)

15

19

23

27

32

ADJ. PAT

15

19

23

27

32

% chg

28.8

29.2

18.6

19.2

17.7

(% of Net Sales)

13.4

15.6

16.5

16.8

17.0

Basic EPS (`)

2.7

3.4

4.1

4.9

5.7

Fully Diluted EPS (`)

2.7

3.4

4.1

4.9

5.7

% chg

28.8

29.2

18.6

19.2

17.7

December 18, 2017

7

Initiating coverage | Endurance Technologies

Balance sheet

Y/E March (` cr)

FY16

FY17

FY18E

FY19E

FY20E

SOURCES OF FUNDS

Equity Share Capital

5

6

6

6

6

Reserves& Surplus

47

59

73

90

110

Shareholders Funds

52

64

79

96

116

Minority Interest

-

-

-

-

-

Total Loans

12

21

21

21

21

Deferred Tax Liability

4

4

4

4

4

Other long term liabilities

-

-

-

-

-

Long-term provisions

-

-

-

-

-

Total Liabilities

68

89

104

121

141

APPLICATION OF FUNDS

Gross Block

79

87

97

108

114

Less: Acc. Depreciation

44

49

54

60

66

Net Block

35

37

43

48

48

Intangible assets

-

-

-

-

-

Capital work-in-progress

1

4

4

4

4

Non-current investments

-

-

-

-

-

Long-term loans and advances

Other non-current assets

Current Assets

44

62

71

84

106

Inventories

11

12

13

15

18

Sundry Debtors

25

29

30

36

41

Cash

5

17

24

30

44

Loans & Advances

2

3

3

3

3

Other Assets

1

1

1

1

1

Current liabilities

12

13

14

15

16

Net Current Assets

33

48

57

69

90

Deferred Tax Asset

0

0

0

0

0

Mis. Exp. not written off

-

-

-

-

-

Total Assets

68

89

104

121

141

December 18, 2017

8

Initiating coverage | Endurance Technologies

Cash flow statement

Y/E March (` cr)

FY16

FY17

FY18E FY19E FY20E

Profit before tax

23

28

34

41

48

Depreciation

5

5

4

6

6

Change in Working Capital

(9)

(4)

(1)

(6)

(7)

Interest / Dividend (Net)

2

1

1

1

1

Direct taxes paid

(8)

(8)

(11)

(13)

(16)

Others

0

(0)

-

-

-

Cash Flow from Operations

12

21

27

28

33

(Inc.)/ Dec. in Fixed Assets

(4)

(10)

(10)

(11)

(6)

(Inc.)/ Dec. in Investments

0

(0)

-

-

-

Cash Flow from Investing

(4)

(10)

(10)

(11)

(6)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

(4)

9

-

-

-

Interest paid

(2)

(1)

(1)

(1)

(1)

Dividend Paid (Incl. Tax)

(6)

(7)

(8)

(10)

(12)

Cash Flow from Financing

(12)

1

(10)

(12)

(13)

Inc./(Dec.) in Cash

(4)

12

7

6

14

Opening Cash balances

9

5

17

24

30

Closing Cash balances

5

17

24

30

44

December 18, 2017

9

Initiating coverage | Endurance Technologies

Key Ratios

Y/E March

FY16

FY17

FY18E

FY19E

FY20E

Valuation Ratio (x)

P/E (on FDEPS)

34.5

26.7

22.5

18.9

16.0

P/CEPS

26.4

21.1

18.9

15.5

13.4

P/BV

9.9

8.0

6.5

5.4

4.4

Dividend yield (%)

0.9

1.1

1.4

1.6

1.9

EV/Sales

4.7

4.2

3.7

3.1

2.6

EV/EBITDA

17.9

15.5

13.2

10.7

9.0

EV / Total Assets

8.1

6.0

5.1

4.3

3.6

Per Share Data (`)

EPS (Basic)

2.7

3.4

4.1

4.9

5.7

EPS (fully diluted)

2.7

3.4

4.1

4.9

5.7

Cash EPS

3.5

4.3

4.8

5.9

6.8

DPS

0.8

1.0

1.3

1.5

1.8

Book Value

9.3

11.4

14.0

17.1

20.7

Dupont Analysis

EBIT margin

21.9

22.9

24.9

25.3

25.7

Tax retention ratio

0.6

0.7

0.7

0.7

0.7

Asset turnover (x)

1.9

1.8

1.8

1.9

2.0

ROIC (Post-tax)

26.4

28.6

30.5

31.6

34.6

Cost of Debt (Post Tax)

0.08

0.04

0.05

0.05

0.05

Leverage (x)

0.1

0.1

(0.0)

(0.1)

(0.2)

Operating ROE

30.0

30.6

29.4

28.8

27.9

Returns (%)

ROCE

38.0

33.0

34.4

35.1

35.1

Angel ROIC (Pre-tax)

41.9

43.4

47.7

49.1

53.6

ROE

28.6

30.0

29.0

28.4

27.6

Turnover ratios (x)

Asset Turnover (Gross Block)

1.4

1.4

1.4

1.5

1.7

Inventory / Sales (days)

37

37

34

34

34

Receivables (days)

82

86

80

80

80

Payables (days)

22

24

22

21

21

WC cycle (ex-cash) (days)

98

99

92

93

93

Solvency ratios (x)

Net debt to equity

0.1

0.1

(0.0)

(0.1)

(0.2)

Net debt to EBITDA

0.2

0.1

(0.1)

(0.2)

(0.4)

Interest Coverage (EBIT / Interest)

15.0

24.1

23.3

27.8

32.6

December 18, 2017

10

Initiating coverage | Endurance Technologies

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager and Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking

Private Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide

registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory

authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Menon Bearings Limited

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

December 18, 2017

11