Company Update | Infrastructure

April 4, 2016

MBL Infrastructures

BUY

CMP

`154

Wins projects worth `2,126cr

Target Price

`285

MBL Infrastructures (MBL) reported having won 2 NHAI road projects worth

Investment Period

12 Months

`2,126cr on Hybrid Annuity model.

Stock Info

The first project entails 4-laning of Chutmultpur-Ganeshpur section of NH-72A to

Sector

Infrastructure

Roorkee-Chutmalpur-Gagalheri section of NH-73, covering a stretch of 53.3kms.

Market Cap (` cr)

638

MBL won this project at a bid price of `942cr, against the NHAI base price of

Net debt (` cr)

987

`809.88cr. This Hybrid Annuity project is a 15-year project, which includes 730

Beta

1.0

days of construction period.

52 Week High / Low

320/116

The second project covers 4-laning of Gagalheri-Saharanpur-Yamunanagar

Avg. Daily Volume

122,396

Face Value (`)

10

section of NH-73, covering a 51.455kms stretch. MBL won this project at a bid

price of `1,184cr, against NHAI base price of `1,009.36cr. This Hybrid Annuity

BSE Sensex

25,270

Nifty

7,713

project is a 15-year project, which includes 730 days of construction period.

Reuters Code

MBLI.BO

For both the projects, Sadbhav Engineering was the second lowest bidder.

Bloomberg Code

MBL@IN

MBL’s unexecuted order book as of 3QFY2016 stood at ~`4,748cr (order book

[OB] to LTM revenues at ~2.0x). With these 2 project wins, we now expect MBL to

Shareholding Pattern (%)

end FY2016 with OB to LTM sales ratio of ~2.8x, indicating better revenue

Promoters

46.7

visibility.

MF / Banks / Indian Fls

31.2

Outlook and valuation: MBL’s stock price has corrected by ~50% in the last 12

FII / NRIs / OCBs

6.6

months period owing to order book concerns. For FY2016, MBL has surpassed its

Indian Public / Others

15.6

order inflow guidance of `2,500cr. Considering the strong roads & highways bid

pipeline and MBL’s strong market positioning, we are optimistic that MBL has a

Abs. (%)

3m 1yr 3yr

fair chance of attaining its order inflow guidance of `2,800cr for FY2017E. Post

the recent order wins, concern over its order book get allayed up to certain

Sensex

(3.4)

(10.6)

32.7

extent. Also 3 of its BOT projects are expected to commence operations in

MBL

(31.5)

(50.4)

110.1

FY2016-17E, which should lead to initiation of debt repayment cycle at SPV level.

All these positives shaping-up comfort us that the stock is poised to get re-rated.

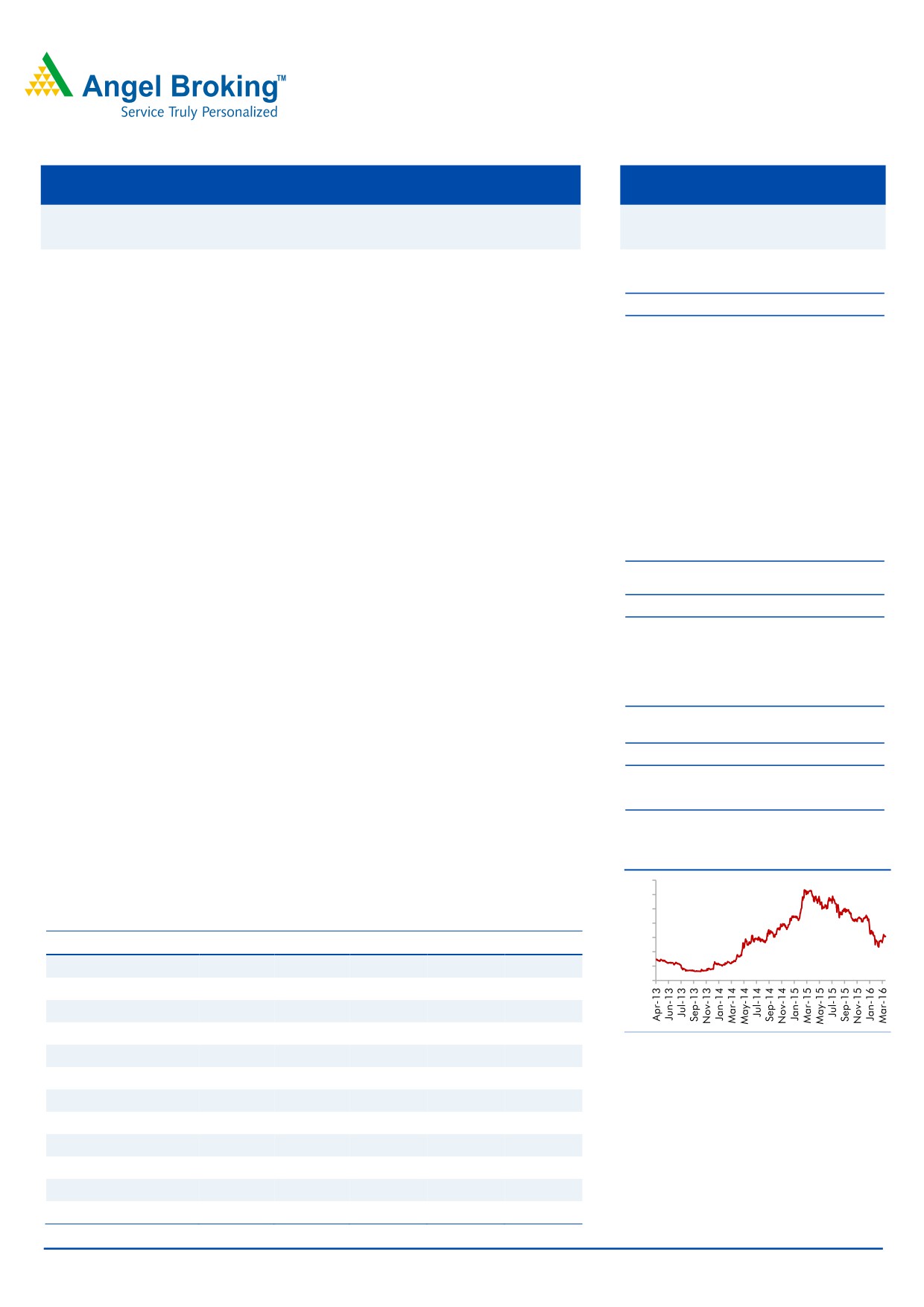

3-Year Daily Price Chart

Using SoTP based valuation methodology we arrive at FY2017E based price

350

target of `285. Given the upside potential, we maintain our Buy on the stock.

300

250

Key financials (Consolidated)

200

150

Y/E March (` cr)

FY13

FY14

FY15P

FY16E

FY17E

100

Net Sales

1,355

1,766

1,962

2,313

2,797

50

0

% chg

30.3

11.1

17.9

21.0

Net Profit

57

77

82

80

84

% chg

35.9

6.0

(2.1)

5.0

Source: Company, Angel Research

EBITDA (%)

10.6

10.7

12.1

12.2

14.6

EPS (`)

32

44

39

19

20

P/E (x)

4.8

3.5

3.9

8.0

7.6

P/BV (x)

0.7

0.6

0.5

0.8

0.8

RoE (%)

15.2

17.8

14.5

11.3

10.6

RoCE (%)

14.6

15.6

14.9

12.1

13.9

Yellapu Santosh

EV/Sales (x)

0.6

0.6

0.7

1.0

0.9

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

5.8

5.2

5.5

8.0

6.0

Source: Company, Angel Research; CMP as of April 1, 2016

Please refer to important disclosures at the end of this report

1

MBL Infrastructures | Company Update

Profit and Loss Statement (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Net Sales

1,355

1,766

1,962

2,313

2,797

% Chg

30.3

11.1

17.9

21.0

Total Expenditure

1,212

1,578

1,725

2,031

2,389

Cost of Materials Consumed

954

1,376

1,517

1,777

2,089

Direct Labour, Sub-Contracts

180

118

84

138

161

Employee benefits Expense

23

27

37

36

41

Other Expenses

55

57

87

79

98

EBITDA

143

188

237

282

408

% Chg

31.2

25.9

19.0

44.8

EBIDTA %

10.6

10.7

12.1

12.2

14.6

Depreciation

11

14

20

33

57

EBIT

132

174

217

249

351

% Chg

31.6

24.5

14.8

41.1

Interest and Financial Charges

58

75

101

140

246

Other Income

2

4

3

3

3

PBT

76

103

119

111

108

Tax

20

26

37

31

39

% of PBT

25.7

25.2

31.3

28.1

35.6

PAT before Exceptional item

57

77

82

80

70

Exceptional item

0

0

0

0

0

PAT before Minority Interest

57

77

82

80

70

Minority Interest

0

0

0

0

(14)

PAT after Minority Interest

57

77

82

80

84

% Chg

35.9

6.0

(2.1)

5.0

PAT %

4.2

4.4

4.2

3.5

3.0

Diluted EPS

32

44

39

19

20

% Chg

36.0

(10.5)

(51.1)

5.0

April 4, 2016

2

MBL Infrastructures | Company Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Sources of Funds

Equity Capital

18

18

21

41

41

Reserves Total

380

451

635

715

779

Networth

398

469

656

756

820

Total Debt

644

772

1,063

1,680

1,848

Other Long-term Liabilities

44

40

80

73

73

Minority Interest

0

32

0

0

(14)

Deferred Tax Liability

30

34

41

35

35

Total Liabilities

1,116

1,347

1,839

2,544

2,762

Application of Funds

Gross Block

248

287

351

921

1,663

Accumulated Depreciation

59

73

91

120

181

Net Block

189

214

260

801

1,482

Capital WIP

209

376

497

620

0

Investments

20

20

24

24

24

Current Assets

Inventories

`491

559

811

807

919

Sundry Debtors

253

318

395

450

544

Cash and Bank Balance

77

68

76

49

39

Loans, Advances & Deposits

72

98

88

101

104

Other Current Asset

6

8

7

6

7

Current Liabilities

208

330

379

375

417

Net Current Assets

692

721

998

1,038

1,195

Other Assets

6

16

61

61

61

Total Assets

1,116

1,347

1,839

2,544

2,762

April 4, 2016

3

MBL Infrastructures | Company Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Profit before tax

76

103

119

111

108

Depreciation

11

14

20

33

57

Change in Working Capital

(35)

(56)

(261)

(217)

(488)

Interest & Financial Charges

58

75

101

140

246

Direct taxes paid

(48)

(14)

(37)

(31)

(39)

Cash Flow from Operations

62

122

(58)

37

(115)

(Inc)/ Dec in Fixed Assets

(172)

(206)

(186)

(552)

197

(Inc)/ Dec in Investments

(20)

0

(4)

0

0

Cash Flow from Investing

(191)

(206)

(190)

(552)

197

Issue/ (Buy Back) of Equity

0

0

117

21

0

Inc./ (Dec.) in Loans

202

128

290

617

176

Dividend Paid (Incl. Tax)

(3)

(6)

(7)

(8)

(9)

Interest Expenses

(58)

(75)

(101)

(140)

(246)

Minority Interest

0

32

(32)

0

(14)

Cash Flow from Financing

142

78

267

490

(92)

Inc./(Dec.) in Cash

13

(6)

18

(26)

(11)

Opening Cash balances

50

63

57

75

49

Closing Cash balances

63

57

75

49

39

April 4, 2016

4

MBL Infrastructures | Company Update

Key Ratios (Consolidated)

Y/E March

FY13

FY14

FY15

FY16E

FY17E

Valuation Ratio (x)

P/E (on FDEPS)

4.8

3.5

3.9

8.0

7.6

P/CEPS

4.0

3.0

3.1

5.6

4.5

Dividend yield (%)

1.5

1.5

1.5

0.8

0.9

EV/Sales

0.6

0.6

0.7

1.0

0.9

EV/EBITDA

5.8

5.2

5.5

8.0

6.0

EV / Total Assets

0.8

0.7

0.7

0.9

0.9

Per Share Data (`)

EPS (fully diluted)

32.3

44.0

39.4

19.3

20.2

Cash EPS

38.7

52.0

49.1

27.3

34.0

DPS

3.0

3.0

3.1

1.6

1.9

Book Value

227.1

267.6

316.5

182.5

197.9

Returns (%)

RoCE (Pre-tax)

14.6

15.6

14.9

12.1

13.9

Angel RoIC (Pre-tax)

12.9

14.4

12.8

10.3

13.3

RoE

15.2

17.8

14.5

11.3

10.6

Turnover ratios (x)

Asset Turnover (Gross Block) (X)

0.6

0.7

0.7

0.5

0.4

Inventory / Sales (days)

127

108

127

128

113

Receivables (days)

57

59

66

67

65

Payables (days)

18

25

37

32

19

Leverage Ratios (x)

D/E ratio (x)

1.6

1.6

1.6

2.2

2.3

Interest Coverage Ratio (x)

2.3

2.4

2.2

1.8

1.4

April 4, 2016

5

MBL Infrastructures | Company Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

MBL Infrastructures

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

April 4, 2016

6