IPO Note | Financials

Oct 05, 2017

MAS Financials Services Ltd

SUBSCRIBE

sue Open: Oct 06, 2017

Is

On the track to excel

Issue Close: Oct 10, 2017

MAS Financial Services (MAS) is a Gujarat based NBFC, which is two decades

old. It primarily lends to Micro Enterprises (ME) and SME, which contribute 60%

and 23% of its AUM respectively. Company’s business and financing is in five

Issue Details

categories i.e. micro-enterprise loan, SME loans, two wheeler loans, commercial

Face Value: `10

vehicle loans and housing loans. Company’s AUM has grown at healthy 33.4%

Present Eq. Paid up Capital: `91.5cr

CAGR over FY2013-17 with strong asset quality (GNPA -1.1%, NNPA -0.9%).

Expanding offerings to support AUM growth: MAS had begun its journey with a

Offer for Sale: **0.49cr Shares

clear focus to ME and gradually expanded its offerings to two wheeler & CV

segments for its existing client. FY2012 onwards, MAS commenced lending to

Fresh issue: `233cr

SME and Housing loan, which is growing at a very healthy rate. To leverage

Post Eq. Paid up Capital: `96.5cr

existing client base and network further it has extended loans to the agricultural

input and equipment segment.

Issue size (amount): *`457cr -**460 cr

Fairly strong AUM growth at 33.4% CAGR over FY2013-17: Focused approach

towards asset financing, ability to find out gaps and the underserved sections of

Price Band: `456-459

the micro enterprise SME, Vehicle Finance, segments has helped the company to

Lot Size: 32 shares and in multiple

achieve a strong 33.4% CAGR in AUM over FY2013-17.

thereafter

Healthy return ratios: MAS has reported average ROE/ROA of 27.9%/3.2% over

Post-issue implied mkt. cap: *`2,492cr

last 5 years. Higher return ratios are largely driven by lower Cost to Income(C/I)

- **`2,508cr

(33.5%) and lower provisioning expenses. C/I has declined from 43.7% in

Promoters holding Pre-Issue: 80.7%

FY2013 to 33.5% in FY2017, and we believe C/I would continue to decline

Promoters holding Post-Issue: 73.2%

further.

Strong asset quality; sufficient CAR to support growth: Robust credit assessment

*Calculated on lower price band

process and clever understanding of targeted market has helped to keep GNPA at

** Calculated on upper price band

1% over last 5 years. As on 1QFY2018, CAR stood at 23.8% and post IPO CAR

Book Building

would further increase. With strong internal capital generation ability, present

high CAR and IPO proceeds would not require MAS to dilute equity for high

QIBs

50% of issue

growth in near future.

Non-Institutional

15% of issue

High valuations underpinned by high growth potential and profitability: Close

Retail

35% of issue

peers, Capital First and Shriram City Union Finance are trading at ~3x FY2017

book, however both the companies report moderate ROE of 11%. At the upper

end of the price band, MAS is valued at 6.85x of FY2017 book value (Pre-IPO)

Post Issue Shareholding Patter

and on post dilution basis at 4.1x of Book value. Although valuations are on the

Promoters

73%

higher side, looking at the strong and sustainable growth and ROE prospects of

the company, we recommend a Subscribe to the issue.

Others

27%

Key Financials

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

NII

71

90

105

136

172

YoY Growth (%)

-

27

16

30

27

PAT

27

33

40

51

69

YoY Growth (%)

-

19

23

27

35

EPS

6

7

8

10

14

Book Value

21

26

32

37

67

P/E

83

70

57

45

33

P/BV

21

18

14

12

7

Jaikishan J Parmar

ROE (%)

26

28

28

30

27

+022 39357600, Extn: 6810

ROA (%)

3

3

3

3

3

Source: RHP, Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band d

Please refer to important disclosures at the end of this report

1

MAS Financials Services Ltd | IPO Note

Company Background

MAS Fin Ser is a Gujarat-headquartered NBFC with more than two decades of

business operations and as of June 30, 2017, it operated across six States and the

NCT of Delhi. The financing activity are primarily focused on middle and low

income customer segments, and include five principal categories: (i) micro-

enterprise loans; (ii) SME loans; (iii) two-wheeler loans; (iv) Commercial Vehicle

loans (which include new and used commercial vehicle loans, used car loans and

tractor loans); and (v) housing loans.

As of Q4FY17 and Q1FY18, the company’s AUM was `3,332.6cr and `3,451.7

cr, respectively. AUM increased at a CAGR of 33.4% from `1,053.2cr as of FY13

to `3,332.6cr as of FY17. As of June 30, 2017 MAS had more than 500,000

active loan accounts, across more than 3,165 Customer Locations in six States and

the NCT of Delhi, served through our 121 branches.

Exhibit 1: Business Segments

ME

SME Two Wheeler

CV Housing

AUM (` Cr )

1,984.86

763.84

285.39

122.06

3,332.57

% of AUM

60

23

9

4

5

Average Ticket Size

`36,000

`55lacs

`43,000

`1.5lacs

`14lacs

4 Yr CAGR

32

138

6

3

44

Loan Tenure

36 Months

-

36 Months

60 Months 240 Months

Source: RHP, Angel Research

Key Management Personnel

Mr. Kamlesh Chimanlal Gandhi is Chairman & Managing Director (Founder of

MAS). He received the higher secondary school examination certificate from the

Gujarat Secondary Education Board, Gandhinagar in 1983. He has over 21 years

of experience in the financial services sector.

Mr. Mukesh Chimanlal Gandhi is a whole-time Director and Chief Financial

Officer of the Company. He has been associated with the Company since May 25,

1995. He holds bachelor’s and master’s degrees in commerce from Gujarat

University. He is also the chairman of the Gujarat Finance Company Association

and a director of the Finance Industry Development Council.

Darshana Saumil Pandya is an executive Director of the Company. She has been

associated with the Company since June 1, 1996. She holds a bachelor’s degree

in commerce from Gujarat University. Presently, she also holds the position of the

Chief Operating Officer of the Company.

Oct 05, 2017

2

MAS Financials Services Ltd | IPO Note

Issue details

This IPO is a mix of OFS and issue of fresh shares. The issue would constitute fresh

issue worth of `233cr and OFS worth of `227cr. OFS largely would offer exit to

early investors namely FMO, DEG & Sarva Capital.

Exhibit 2: Pre and Post-IPO shareholding pattern

No of shares

No of shares

%

%

(Pre-issue)

(Post-issue)

Promoter

3,99,96,975

80.7

3,99,96,975

73.2

Investor/Public

95,72,239

19.3

1,46,48,491

26.8

4,95,69,214

100.0

5,46,45,466

100.0

Source: RHP Note: Calculated on upper price band

Objects of the offer

To achieve benefits of listing equity shares on stock exchanges and to carry out

the offer for sale. Listing of equity shares will enhance MAS’ brand name and

provide liquidity to existing shareholders.

The Company would utilise the proceeds from the Fresh Issue towards

augmenting its capital base to meet future capital requirements.

Oct 05, 2017

3

MAS Financials Services Ltd | IPO Note

Expanding offerings to support AUM growth: MAS has begun its journey with a

clear focus to ME and gradually expanded its offering in two wheeler & CV to

existing client. FY12 onwards MAS has commence lending to SME and Housing

loan, which is growing at a very healthy rate. To Leverage existing client base and

network further it has extended loans to the agricultural input and equipment

segment.

Exhibit 3: Segmental Gross AUM (` Cr )

FY13

FY14

FY15

FY16

FY17

CAGR FY13-17

ME

651

948

1,386

1,735

1,985

32%

YoY Growth %

46

46

25

14

SME

24

75

215

429

764

138%

YoY Growth %

214

185

100

78

Two Wheeler

227

229

240

258

285

6%

YoY Growth %

1

5

7

11

CV

110

139

164

144

122

3%

YoY Growth %

26

18

-12

-15

Housing Loan

41

65

94

135

176

44%

YoY Growth %

60

44

43

31

Total AUM

1,053

1,743

2,354

2,820

3,421

33%

YoY Growth %

66

35

20

21

Source: RHP

We believe ME & SME would continue to support advance growth going forward.

However, housing finance and newly ventured segment i.e. farm loan would

propel loan growth going forward. It intends to offer loans to farmers to acquire

accessories, implements and tractors in collaboration with dealers, manufacturers

and distributors as sourcing intermediaries. The proximity of these sourcing

intermediaries with farmers enables them to generate quality leads for MAS.

Power equipment, hybrid seeds penetration, and higher usage of bio-pesticides

and bio-fertilisers will drive growth close to 15% in FY2017 and over 10%

thereafter, compared to a single digit growth for most large sub segments in Fiscal

2016. (Source: CRISIL Agri Report, 2016)

Agricultural finance segment had a market size of `8.8 trillion in FY2016. The

expectation of good monsoons is expected to increase demand for agriculture

credit. A growth of 13-15% is expected going ahead in agricultural financing in

India.

Oct 05, 2017

4

MAS Financials Services Ltd | IPO Note

Fairly strong AUM growth at 33.4% CAGR over FY2013-17: Focused approach

towards asset financing, the ability to find out gaps and the underserved sections

of the micro enterprise SME, Vehicle Finance segments has helped the company to

achieve a strong 33.4% CAGR in AUM over FY2013-17.

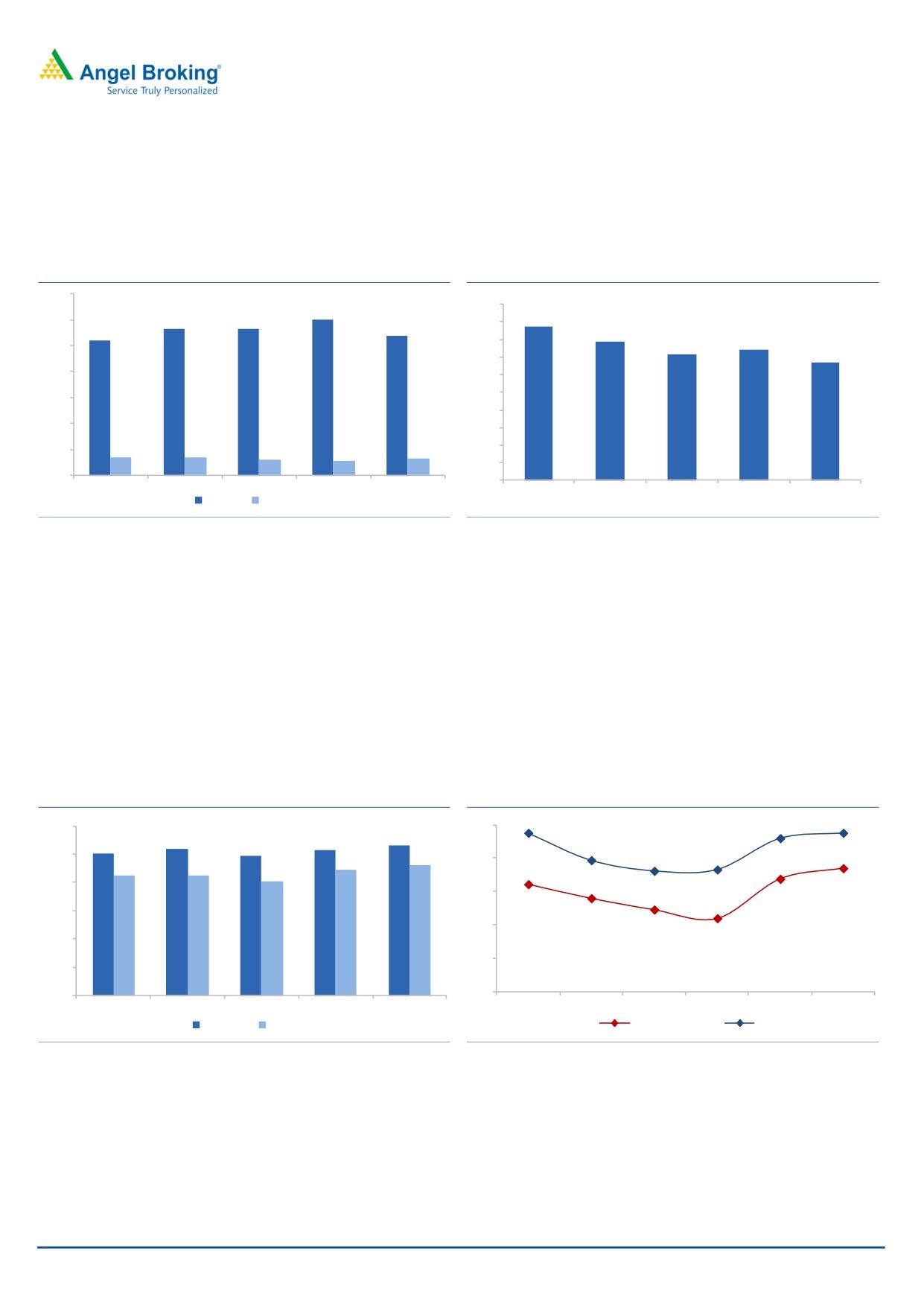

Exhibit 4: Loan Book Composition (%) FY17

Exhibit 5: AUM Growth Trend

3,500

44

50

45

4%

3,000

38

5%

40

2,500

35

9%

ME

29

30

2,000

23

SME

25

Two Wheeler

1,500

20

23%

60%

CV

1,000

15

10

Housing

500

5

1,053

1,456

2,100

2,700

3,333

0

0

FY13

FY14

FY15

FY16

FY17

AUM

% Growth YoY

Source: RHP

Source: RHP

Micro-financing is aimed at aiding the under-privileged in undertaking economic

activity, smoothening consumption and mitigating vulnerability to income shocks

(in times of illness and natural disasters), thereby increasing their savings. Focused

players like MAS, have been able to grow their book at healthy rate by catering to

these segments. Additionally, NBFCs have been gaining market share in the

growing credit market in India.

Oct 05, 2017

5

MAS Financials Services Ltd | IPO Note

Healthy return ratios: MAS has reported average ROE/ROA of 27.9%/3.2% over

last 5 years. Higher return ratios are largely driven by lower Cost to Income(C/I)

(33.5%) and lower provisioning expenses. C/I has declined from 43.7% in FY2013

to 33.5% in FY2017, and we believe C/I would continue to decline further.

Exhibit 6: consistently delivering strong returns

Exhibit 7: Cost to Income ratio (%)

35

30

50

28

28

30

27

45

26

40

25

35

20

30

25

15

20

10

15

3.4

3.4

3.0

3.3

10

2.9

5

5

44

39

36

37

34

-

0

FY13

FY14

FY15

FY16

FY17

FY13

FY14

FY15

FY16

FY17

ROE (%) ROA (%)

Source: RHP

Source: RHP

Strong asset quality; sufficient CAR to support growth: Robust credit assessment

process and clever understanding of targeted market has helped the company to

keep GNPA at 1% over last 5 years. The Company has been strategically

expanding its footprint after understanding targeted market in detail. Presently, it

has very strong foothold in Gujarat & Maharashtra. As on 1QFY2018, CAR stood

at 23.8% and post IPO, CAR would further increase. With strong internal capital

generation ability, present high CAR and IPO proceeds, MAS would be able to

grow without dilution in the near term.

Exhibit 8: Robust Asset Quality

Exhibit 9: Capital Adequacy Ratio

1.2

25

23

1.0

1.0

1.1

1.0

1.0

23.8

19.7

23.8

1.0

0.9

18.1

18.3

0.9

20

0.9

0.9

0.8

0.8

18.5

15

16.9

16.1

0.6

14

10

12.3

0.4

11

5

0.2

0

-

FY13

FY14

FY15

FY16

FY17

Q1FY18

FY13

FY14

FY15

FY16

FY17

GNPA (%) NPA (%)

CRAR Tier -1(%)

CRAR (%)

Source: RHP

Source: RHP

Oct 05, 2017

6

MAS Financials Services Ltd | IPO Note

Outlook & Valuation

High valuations underpinned by high growth potential and profitability: Close

peers, Capital First and Shriram City Union Finance are trading at ~3x FY2017

book, however both the companies report moderate ROE of 11%. At the upper

end of the price band, MAS is valued at 6.85x of FY2017 book value (Pre-IPO)

and on post dilution basis at 4.1x of Book value. Although valuations are on the

higher side, looking at the strong and sustainable growth and ROE prospects of

the company, we recommend a Subscribe to the issue.

Exhibit 10: Relative comparison

Adv Growth

EPS Growth

Company

GNPA

NPA

ROE

ROA

P/B

PE

FY13-17

FY13-17

MAS

37.0

26.0

1.1

0.9

26.9

3.3

6.9

33.2

Capital First

27.0

40.0

1.7

1.0

11.9

1.6

3.1

22.9

Shriram City Union Finance

10.0

1.0

6.7

1.8

11.7

2.6

2.7

24.4

Source: Company, Angel Research, Valuation are based on FY17 numbers

Key risk

Risky Borrower

MAS’ operations involve transactions with relatively high risk borrowers. Any

default from the customers could adversely affect the business, results of

operations and financial condition.

Unsecured Portfolio

As of June 30, 2017, the unsecured loan portfolio was `5,10cr (22% of AUM) out

of On-book AUM of `2,276.2cr. These unsecured loans present a higher risk of

loss in case of a credit default as compared to loans to customers in other asset-

backed financing products.

Oct 05, 2017

7

MAS Financials Services Ltd | IPO Note

Income Statement

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

NII

71

90

105

136

172

- YoY Growth (%)

27

16

30

27

Other Income

16

16

22

26

28

- YoY Growth (%)

1

34

20

8

Operating Income

87

106

126

162

200

- YoY Growth (%)

22

19

28

24

Operating Expenses

38

42

45

60

67

- YoY Growth (%)

10

8

32

12

Pre - Provision Profit

49

64

81

102

133

- YoY Growth (%)

31

26

26

31

Prov. & Cont.

8

15

19

24

27

- YoY Growth (%)

72

34

21

15

Profit Before Tax

41

50

62

79

106

- YoY Growth (%)

23

24

27

35

Exceptional Item

-

-

-

-

-

PBT Post Exceptional Item

41

50

62

79

106

Prov. for Taxation

13

17

21

27

37

- as a % of PBT

32

33

34

34

35

Reported PAT

27

33

41

51

69

Adj PAT

27

33

40

51

69

- YoY Growth (%)

19

23

27

35

Balance sheet

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17

Share Capital

53

59

59

59

90

Reserve & Surplus

53

68

101

124

242

Net Worth

106

128

160

183

332

Borrowings

514

723

1,031

1,308

1,264

- Growth (%)

41

43

27

(3)

Total Provisions

5

8

9

11

17

Other Liabilities

177

275

372

444

588

Total Liabilities

802

1,133

1,572

1,946

2,201

Cash and Cash equivalents

175

185

218

182

47

Investments

0

0

0

0

0

Total Loans & Advances

601

923

1,322

1,725

2,109

- Growth (%)

53

43

30

22

Fixed Assets

6

6

5

8

9

Other Assets

19

19

27

31

36

Total Assets

802

1,133

1,572

1,946

2,201

Oct 05, 2017

8

MAS Financials Services Ltd | IPO Note

Key Ratio

FY13

FY14

FY15

FY16

FY17

Profitability ratios (%)

NIMs

11.8

11.8

9.3

8.9

9.0

ROA

3.4

3.4

3.0

2.9

3.3

ROE

25.9

28.3

28.3

30.0

26.9

Cost to Income

43.7

39.4

35.8

36.9

33.5

Asset Quality (%)

Gross NPAs (cr)

104.8

151.2

208.1

279.1

352.7

Gross NPAs (AUM)

1.00

1.04

0.99

1.03

1.06

Net NPAs (cr)

89.3

122.2

170.9

239.3

305.5

Net NPAs (AUM)

0.85

0.85

0.81

0.89

0.92

Credit Cost

0.81

1.16

1.10

0.98

0.90

CAR

23.8

19.7

18.1

18.3

23.0

Tier1

16.1

14.0

12.3

11.0

16.9

Tier - 2

7.7

5.7

5.8

7.3

6.1

Per Share Data (`)

EPS

5.5

6.6

8.1

10.3

13.8

BVPS

21.4

25.8

32.3

36.9

67.0

DPS

0.5

0.8

1.3

4.3

3.2

Valuation Ratios

PER (x)

83.3

69.8

56.9

44.8

33.2

P/BVPS (x)

21.5

17.8

14.2

12.4

6.9

DuPont Analysis

NII

8.9

9.3

7.7

7.7

8.3

(-) Prov

1.1

1.5

1.4

1.3

1.3

Adj NII

7.8

7.8

6.3

6.4

7.0

Other Inc.

2.0

1.7

1.6

1.5

1.4

Total Income

9.8

9.5

7.9

7.9

8.4

Opex

4.7

4.3

3.3

3.4

3.2

PBT

5.1

5.1

4.6

4.5

5.1

Taxes

1.6

1.7

1.5

1.5

1.8

ROA

3.4

3.4

3.0

2.9

3.3

Leverage

7.6

8.3

9.4

10.3

8.1

ROE

25.9

28.3

28.3

30.0

26.9

Note- Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

Oct 05, 2017

9

MAS Financials Services Ltd | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager and investment advisor with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking

Private Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide

registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory

authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Oct 05, 2017

10