IPO Note | Pharmaceuticals

December 3, 2016

Laurus Labs Limited

NEUTRAL

sue Open: December 06, 2016

Is

IPO Note - Valuations expensive; Neutral

Issue Close: December 08, 2016

Laurus Labs is a Hyderabad based company engaged in manufacturing of Active

Pharma Ingredients (API). Company derives 80% of its revenues from exports

Issue Details

while rest comes from the domestic markets. Its client base features companies

Face Value: `10

like Cipla, Natco, Mylan, etc. API is its largest segment which contributes 92% of

Present Eq. Paid up Capital: `98.7cr

the revenues while rest 8% comes from its Synthesis and Ingredients business.

(September 2016)

Investment rationale - 1) Company operates its API business model with a niche

Offer for Sale: 2.41cr Shares

focus on select therapeutic segments. This makes it a specialist API manufacturer

Fresh issue: *70.4 lakh -**70.1 lakh

shares

in a few therapeutic segments. 2) Laurus intends to enter in the US market with its

own products in FY2019E which is a right strategy considering most domestic

Post Eq. Paid up Capital: `105.8cr

pharma companies currently derive significant revenues from the US market. 3)

Issue size (amount): *`1,327cr -**1,332

Promoters strong entrepreneurial capability which is reflected in Laurus’ top line

cr (Up to `12.5cr of this offer is

reserved for employees)

CAGR of ~40% since inception 4) Company spends ~4-5% of sales on R&D

Price Band: `426-428

which may see a healthy product pipeline in future.

Lot Size: 35 shares and in multiple

Investment concerns - 1) Large portion (62%) of its business comes from supply of

thereafter

Anti Retroviral (ARV) APIs to pharma companies. These pharma companies

Post-issue implied mkt. cap:

receive contracts through competitive tenders every 3 years from govt. agencies

*`4,506.6cr - **`4,526.4cr

and one of its customers (Aspen) has indicted of lower prices of ARV tenders. We

Promoters holding Pre-Issue: 32.8%

believe that ARV is a volume based competitive business with no significant

Promoters holding Post-Issue: 30.6%

pricing power 2) Company has high client concentration risk with a top 10 and

top 3 clients contributing 80% and 40% of revenues respectively. 3) Laurus

*Calculated on lower price band

operates a low margin business with high working capital requirement and low

** Calculated on upper price band

asset turnover ratio which has impacted its return ratios. 4) Its current capacity

Book Building

utilization is at ~70% and company is undertaking capex to add new API facility

in CY2017 which may weaken its return ratios going ahead.

QIBs

50% of issue

Valuations and outlook: On FY2016’s PAT of `133.3cr, the issue, at its upper

Non-Institutional

15% of issue

band, is priced at P/E of 32x which looks expensive. Accounting for FY2017E PAT,

Retail

35% of issue

the valuation still looks high at P/E of 28x. We believe that this kind of valuation is

commanded by domestic pharma companies who have branded formulations

business, healthy product pipeline and strong return ratios. Considering Laurus’

Post Issue Shareholding Patter

1) high client concentration, 2) low pricing power 3) asset heavy model and 4)

Promoters Group

30.6

high valuation, we rate this IPO as Neutral.

DIIs/FIIs/Public & Others

69.4

Key Financials

Y/E March (` cr)

FY2014

FY2015

FY2016

1HFY17

Net Sales

1,160

1,327

1,784

930

% chg

14.4

34.5

-

Net Profit

97

68

133

77

% chg

(29.9)

95.3

-

OPM (%)

18.0

15.1

20.9

21.2

EPS (`)

9.8

6.9

13.4

7.6

P/E (x)

43.5

61.8

31.9

-

P/BV (x)

11.8

5.9

5.0

-

RoE (%)

27.1

9.4

15.6

-

RoCE (%)

20.5

9.5

15.6

-

Shrikant Akolkar

EV/Sales (x)

4.1

3.7

2.9

-

+91 22 39357800 Ext: 6846

EV/EBITDA (x)

22.5

24.5

13.8

-

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Laurus labs | IPO Note

Company background

Laurus Labs is an Active pharma ingredient (API) oriented leading research and

development driven pharmaceutical company in India. Company sells its products

in 32 countries and has 5 manufacturing capacities. Its clients are well known

names from the pharma industry such as Aspen Pharmacare, Aurobindo Pharma,

Cipla, Mylan, NATCO Pharma, Strides Shasun, etc. Top 10 / top 3 clients

contribute 80% / 30% of total revenues. Company has four business segments

namely Generics - APIs, Generics - FDFs (finished dosage forms), Synthesis and

Ingredients. API business contributes 92% of total revenues while company is yet to

record revenues in its FDF business. Synthesis business contributes 5% of total

revenues and rest 3% come from Ingredients Business. In its API business,

company has focus on Anti-retro Viral APIs (ARV), Oncology APIs (anti-cancer) and

Hepatitis-C APIs.

Company intends to move in formulations business and has made significant

investments in new facilities for the same. It has filed 2 ANDAs and expects to

generate revenues in the next two years (FY-2019E). Company currently operates

kilo lab (capacity of 4.6KL) and three manufacturing facilities (aggregate capacity

of 1,833.6 KL) in Visakhapatnam. Of these, 2 facilities manufacture APIs and

ingredients and third facility manufactures APIs and FDFs. Company through

acquisition of Sriam Labs, operates two other manufacturing facilities in Bibinagar

and Visakhapatnam for the manufacturing of APIs and intermediates. Company is

process of setting up two additional manufacturing facilities in Visakhapatnam of

which one will operational in December 2016 while construction will begin at the

other facility in CY2017.

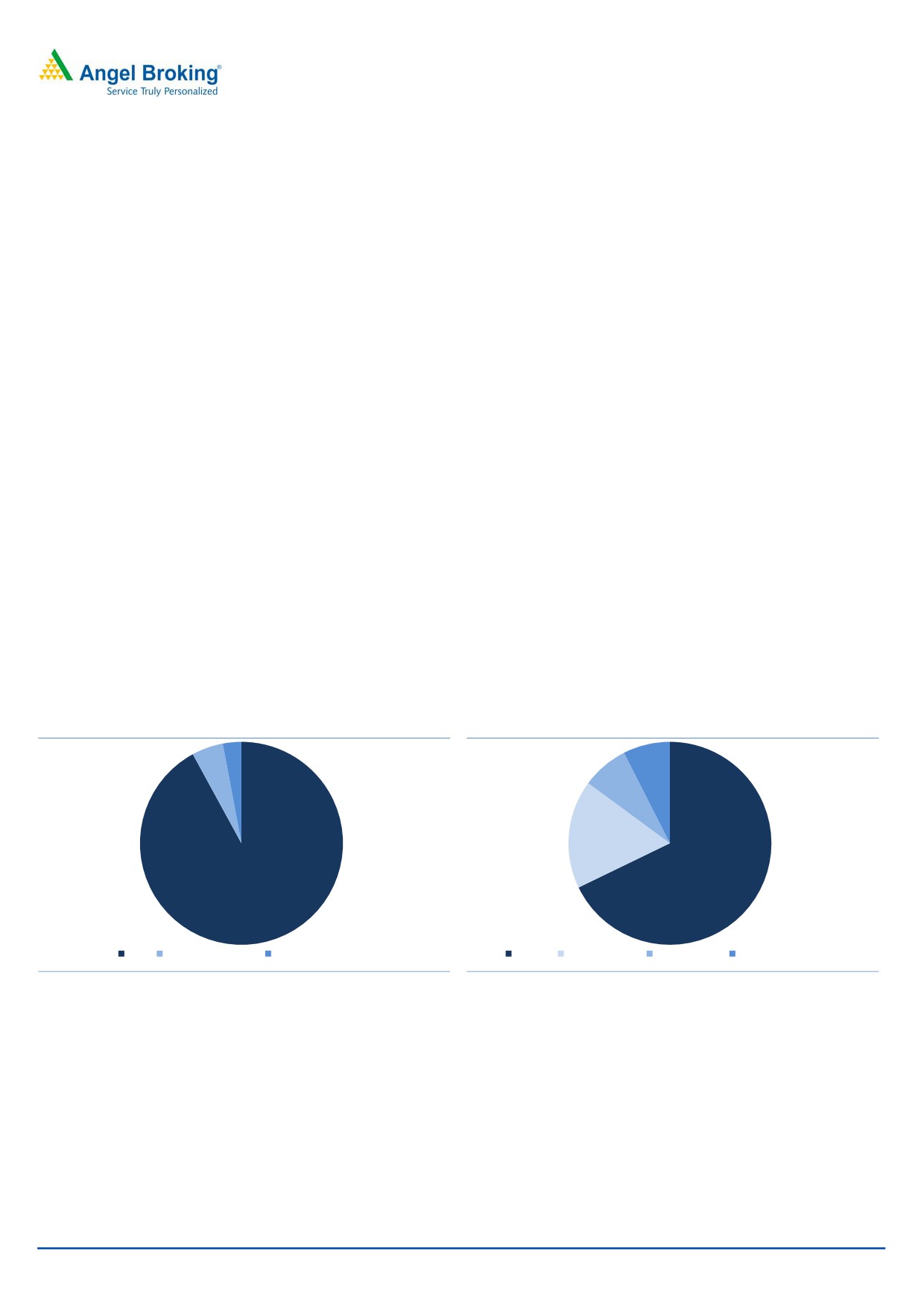

Exhibit 1: Revenue mix (%)

Exhibit 2: API mix (%)

3.0%

5%

7.5%

7.4%

67.8%

17.3%

92%

API

Synthesis business

Ingredients Business

ARV

Hepatitis C

Oncology

Other therapeutic areas

Source: Company, Angel Research

Source: Company, Angel Research

December 3, 2016

2

Laurus labs | IPO Note

Issue details

Through this IPO, some existing shareholders (Aptuit, Bluewater, FIL Capital

Management and Fidelity India Principals) are selling their stake in the company.

Aptuit is selling its entire shareholding while other shareholders are selling their

partial stake.

Company is also raising `300cr by selling fresh shares which will be used to repay

its debt and for general corporate purpose.

Exhibit 3: Pre and Post-IPO shareholding of selling shareholders

Selling shareholders

Pre-issue shares held

Percentage of pre-issue capital

Post issue

Percentage of post- issue capital

Aptuit

9,040,240

9.15%

0

0.00%

Bluewater

29,989,596

30.37%

20,989,596

19.85%

FIL Capital Management

18,265,612

18.50%

12,237,612

11.57%

Fidelity India Principals

118,752

0.12%

79,552

0.08%

Total

57,414,200

58.14%

33,306,760

31.49%

Source: Company, Angel Research

Objects of the offer

Achieve the benefits of listing of the equity shares on the stock exchanges

Pre-payment of term loans

General corporate purposes

December 3, 2016

3

Laurus labs | IPO Note

Investment Rationale

Operating in niche API segments: Laurus labs operates in a niche API segment with

focus on Anti Retroviral (ARV), Hepatitis C and Oncology therapeutics segment. API

segment contributes 92% of its total revenues. Within API segment, ARV is the

largest segment which contributes 68% of the total API segment’s revenues while

rest of the segment revenues come from Hepatitis C and Oncology APIs.

ARV segment has shown a 2 year CAGR of 16% from FY2014-FY2016. This is

mainly due to the increased Anti Retroviral therapies in the African region and

increase in number of patients undergoing treatment. At the end of 2015, ~17

million people were receiving Anti Retroviral therapy of the total 36.7 million

people living with HIV globally, representing approximately 46% of the total HIV

population. Company believes that there are near term opportunities for the US

and European markets.

The company also makes APIs for Hepatitis C which has exhibited strong growth

rates. The prevalence of Hepatitis C is mostly seen in the South Asia and North

Africa which makes nearly

80% of global Hepatitis C burden. Laurus has

arrangement to manufacture and sell Hepatitis C APIs with NATCO, who

commands a 38.5% share of the Indian Hepatitis C market. Company also has

agreement with Gilead Sciences and Bristol-Myers for Hepatitis C API supply in the

international markets.

In the Oncology API, its portfolio consists of 15 active DMFs and supplies

Oncology APIs to global generic multinational pharmaceutical companies.

Globally, Oncology is one of the largest therapeutic segments and is expected to

grow ~7% to 8% between 2015 and 2020E to reach a value of US$152 billion.

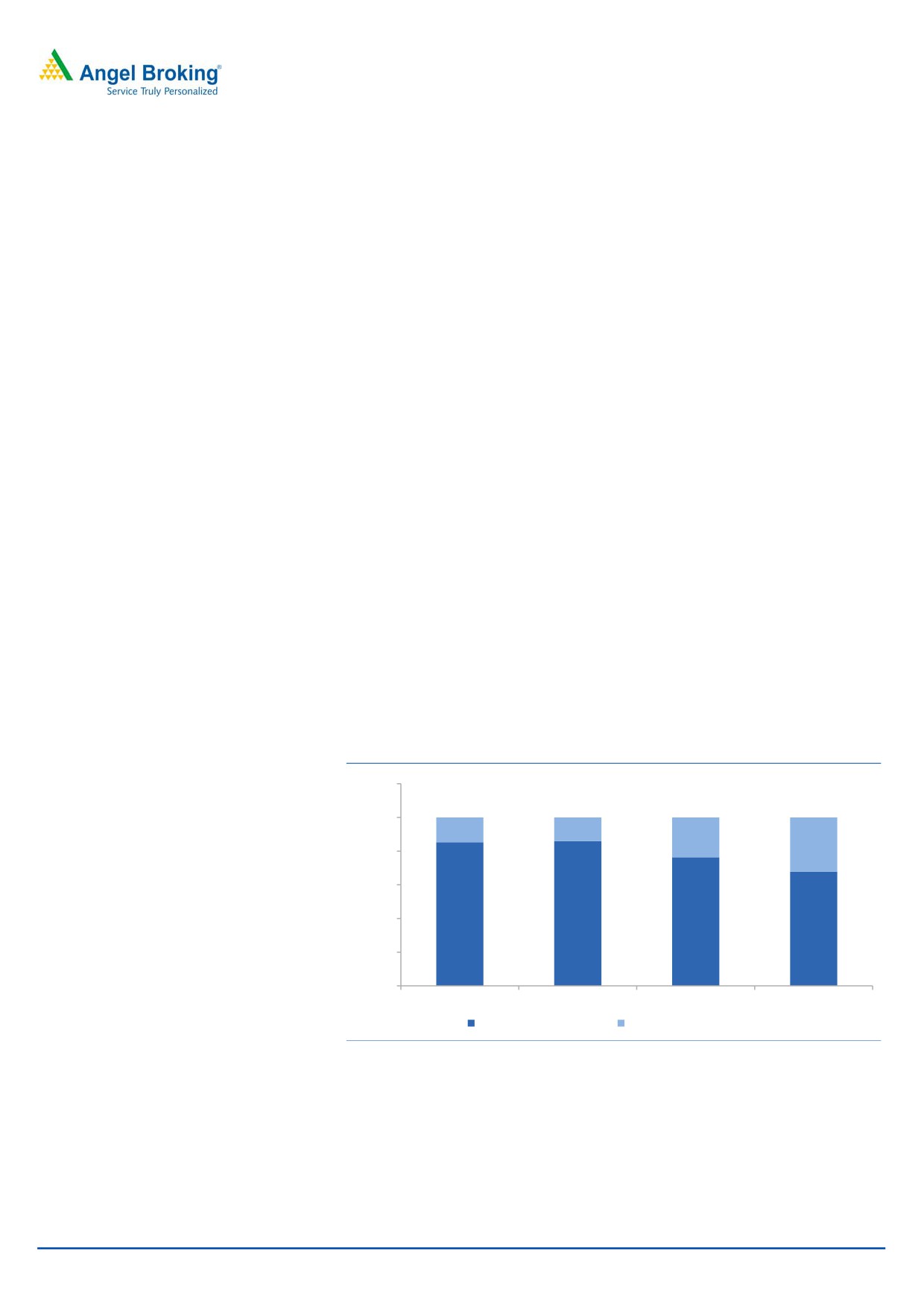

Exhibit 4: API business mix has changed over the years

120.0

100.0

14.7

14.0

23.6

32.2

80.0

60.0

85.3

86.0

40.0

76.4

67.8

20.0

0.0

FY2014

FY2015

FY2016

1HFY17E

ARV Therapeutic Area

Others Therapeutic Areas

Source: Company, Angel Research

December 3, 2016

4

Laurus labs | IPO Note

Possible formulations foray, but too early to price in: Company intends to move in

the formulations business and has started to research on possible ANDAs that it

may file and launch in future. As of now, company has 2 ANDAs filed and it

expects to receive USFDA approval in FY2018E and a possible launch in FY2019E.

However, this in our opinion is too early to price in. We also believe that lot of

Indian companies are already present in the USA with their own front ends and

huge operational scale. We believe most pharma companies which entered in the

US market have now moved towards complex products as low value ANDAs have

seen huge competition and steep price erosion.

The company’s one of the plant has recently undergone an USFDA audit and has

received minor process related observation. While management believes that this

can be resolved in few weeks, an escalation of the same may be negative for its

US plans in near term.

High working capital requirement: Laurus has seen rise in its working capital cycle

in last two years and the same has affected its return ratios. In FY2014 company’s

working capital cycle was ~110 days which increased to ~177 days in FY2016.

Most of this has come due to the rise in the inventories. Company has said that the

cycle is expected to remain at ~180 days going ahead. In our opinion, this is at an

elevated level and may impact its future return ratios.

Recent financial performance: In the first half of the current fiscal, Laurus reported

healthy set of numbers. In H1FY2017, Laurus reported `939.6cr in revenues vs.

`1,783.8cr in FY2016. The raw material costs as percent of sales stood at 53.3%

in H1FY2017 compared to 56.5% in FY2016 indicating decline in the input costs.

EBITDA came in at `196.7cr and EBITDA margins were at 21.2% vs. 20.9% in

FY2016. Its PAT stood at `75.1cr vs. `132.6cr in FY2016 indicating company

reported strong profitability in the first half the current fiscal.

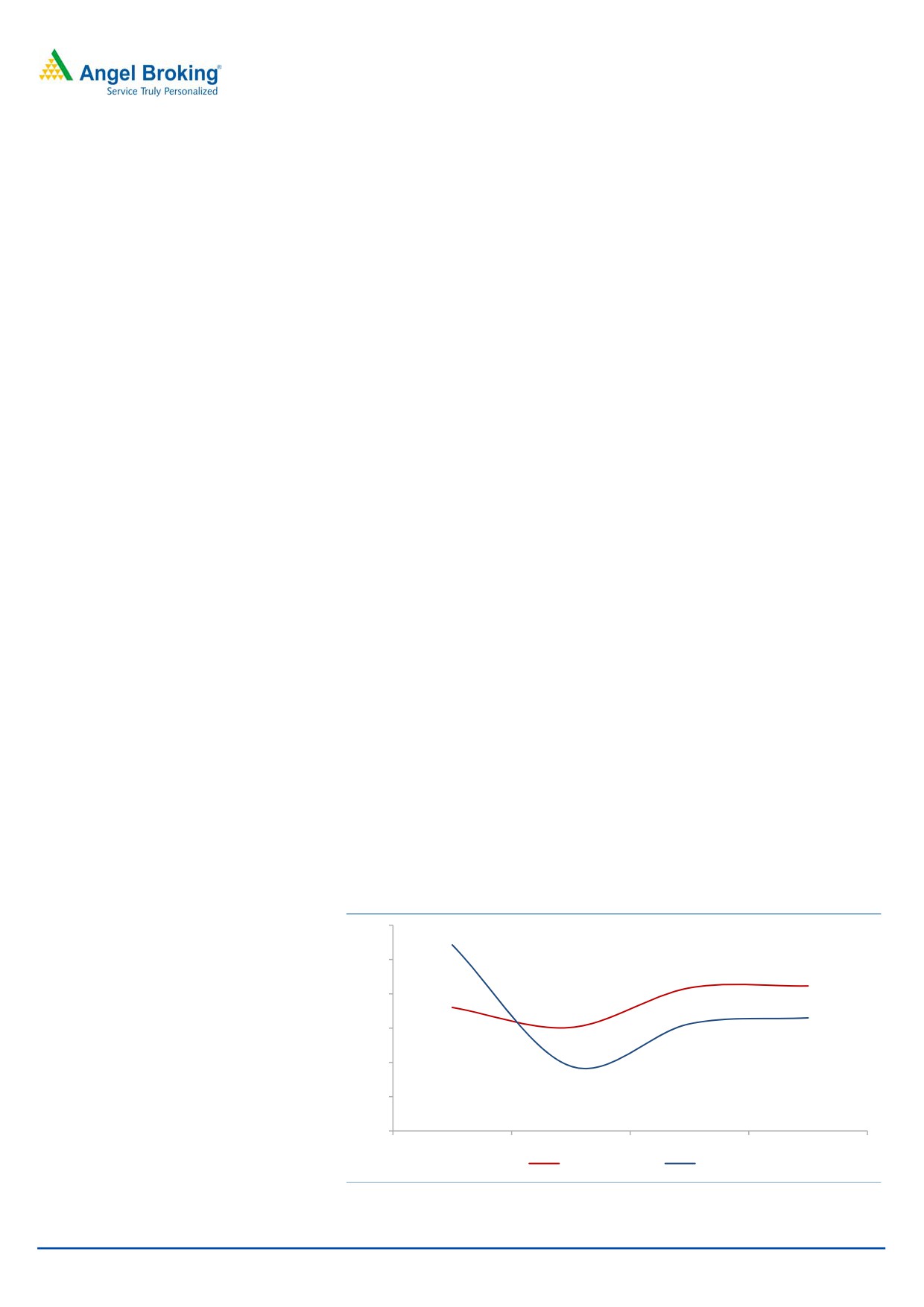

Overall, company has seen improvement in the profitability in the last three years

with EBITDA margins moving from 18.0% in FY2014 to 21.2% in H1FY2017.

Company indicates that ~20.0% EBITDA margin level is sustainable going ahead.

Its return on equity stood at 27.1% in FY2014 but decline in FY2015 to 9.4% but

has recovered to ~16% in H1FY2017.

Exhibit 5: EBITDA margins and RoE ratios since FY2014

30.0

25.0

20.0

15.0

10.0

5.0

0.0

FY2014

FY2015

FY2016

1HFY17E

EBITDA margins

RoE

Source: Company, Angel Research

December 3, 2016

5

Laurus labs | IPO Note

Outlook and Valuation:

On FY2016’s PAT of `133.3cr, the issue, at its upper band, is priced at P/E of 32x

which looks expensive. Accounting for FY2017E PAT, the valuation still looks high

at P/E of 28x. We believe that this kind of valuation is commanded by domestic

pharma companies who have branded formulations business, healthy product

pipeline and strong return ratios. Considering Laurus’ 1) high client concentration,

2) low pricing power 3) asset heavy model and 4) high valuation, we rate this IPO

as Neutral.

Upside risks

Early approval and launch of ANDAs: The increased momentum in the ANDA

filing may be positive for the company as the company will be able to start its

formulations business earlier than expected.

Improvement in working capital: If Laurus sees improvement in its working capital,

return ratios will also improve accordingly. This will be positive for the company.

December 3, 2016

6

Laurus labs | IPO Note

Income Statement

Y/E March (` cr)

FY2014

FY2015

FY2016

1HFY17

Total operating income

1,160

1,327

1,784

930

% chg

14.4

34.5

Total Expenditure

951

1,126

1,412

733

Cost of Materials

726

828

1,008

495

Personnel

104

133

190

118

Others Expenses

121

165

214

120

EBITDA

209

200

372

197

% chg

(4.2)

85.9

(47.2)

(% of Net Sales)

18.0

15.1

20.9

21.2

Depreciation& Amortisation

33

62

92

54

EBIT

176

139

280

143

% chg

(21.2)

101.9

(% of Net Sales)

15.2

10.5

15.7

15.4

Interest & other Charges

64

106

120

53

Other Income

9

34

8

12

(% of PBT)

7.3

51.2

4.5

11.9

Share in profit of Associates

-

-

-

-

Recurring PBT

121

67

168

102

% chg

(44.9)

151.7

Prior Period & Extraord Exp./(Inc.)

-

-

-

-

PBT (reported)

121

67

168

102

Tax

24

(2)

35

26

(% of PBT)

19.6

(2.3)

20.6

25.2

PAT (reported)

97

68

133

76.6

Add: Share of earnings of associate

-

0

(0)

(1.5)

Less: Minority interest (MI)

-

-

-

-

PAT after MI (reported)

97

68

133

75

ADJ. PAT

97

68

133

75

% chg

(29.7)

94.0

(% of Net Sales)

8.4

5.2

7.4

8.1

Basic EPS (`)

9.8

6.9

13.4

7.6

Fully Diluted EPS (`)

9.8

6.9

13.4

7.6

% chg

(29.7)

94.0

December 3, 2016

7

Laurus labs | IPO Note

Balance Sheet

Y/E March (` cr)

FY2014

FY2015

FY2016

1HFY17

SOURCES OF FUNDS

Equity Share Capital

78

82

82

99

Reserves& Surplus

281

640

769

830

Shareholders’ Funds

358

722

852

929

Minority Interest

-

-

-

-

Total Loans

500

735

942

859

Deferred Tax Liability

12

10

45

60

Total Liabilities

871

1,468

1,839

1,847

APPLICATION OF FUNDS

Net Block

494

795

1,079

1,052

Intangible assets

5

6

6

7

Capital Work-in-Progress

116

110

70

216

Goodwill on consolidation

0

-

-

-

Long-term loans and adv.

69

94

129

152

Investments

-

7

7

6

Other non-current assets

15

14

9

14

Current Assets

575

862

1,003

1,134

Inventories

328

475

487

521

Sundry Debtors

195

285

445

533

Cash

23

59

28

14

Loans & Advances

25

31

30

39

Other Assets

4

12

13

26

Current liabilities

403

421

464

733

Net Current Assets

172

442

539

401

Deferred Tax Asset

-

-

-

-

Mis. Exp. not written off

-

-

-

-

Total Assets

871

1,468

1,839

1,847

December 3, 2016

8

Laurus labs | IPO Note

Cash Flow Statement

Y/E March (` cr)

FY14

FY15

FY16

1H1FY17

Profit before tax

121

67

168

102

Depreciation

33

62

92

54

Change in Working Capital

(59)

(251)

(148)

(71)

Interest / Dividend (Net)

48

84

101

47

Direct taxes paid

(23)

(17)

(33)

(13)

Others

2

(9)

13

(1)

Cash Flow from Operations

121

(65)

193

119

(Inc.)/ Dec. in Fixed Assets

(309)

(383)

(337)

(177)

(Inc.)/ Dec. in Investments

(3)

(14)

12

1

Cash Flow from Investing

(312)

(397)

(325)

(176)

Issue of Equity

-

-

-

-

Inc./(Dec.) in loans

250

274

205

97

Finance costs

(51)

(84)

(103)

(47)

Others

12

315

18

8

Cash Flow from Financing

211

505

120

58

Inc./(Dec.) in Cash

21

44

(12)

1

Opening Cash balances

3

15

40

13

Closing Cash balances

23

59

28

14

December 3, 2016

9

Laurus labs | IPO Note

Key Ratios

Y/E March

FY2014

FY2015

FY2016

Valuation Ratio (x)

P/E (on FDEPS)

43.5

61.8

31.9

P/CEPS

32.5

32.6

18.8

P/BV

11.8

5.9

5.0

Dividend yield (%)

0.0

0.0

0.0

EV/Sales

4.1

3.7

2.9

EV/EBITDA

22.5

24.5

13.8

EV / Total Assets

3.69

2.59

2.23

Per Share Data (`)

EPS (Basic)

9.8

6.9

13.4

EPS (fully diluted)

9.8

6.9

13.4

Cash EPS

13.2

13.1

22.8

DPS

0.0

0.0

0.0

Book Value

36.3

73.1

86.3

Returns (%)

ROCE

20.5

9.5

15.6

Angel ROIC (Pre-tax)

21.1

10.0

15.9

ROE

27.1

9.5

15.6

Turnover ratios (x)

Asset Turnover (Net Block)

2.3

1.7

1.7

Inventory / Sales (days)

165

210

176

Receivables (days)

61

78

91

Payables (days)

114

102

90

WC cycle (ex-cash) (days)

112

186

177

December 3, 2016

10

Laurus labs | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

December 3, 2016

11