IPO note | IT Consulting & Software

September 9, 2016

L&T Technology Services Limited

SUBSCRIBE

Issue Open: September 12, 2016

Issue competitively priced - Subscribe

Issue Close: September 15, 2016

IPO note

Company background: L&T Technology Services Limited (LTTS) is subsidiary of

Issue Details

Engineering giant, L&T and was incorporated in Jun-2012. Post transfer of

Product Engineering Services (PES) and Integrated Engineering Services (IES)

Face Value: `2

division and 2 acquisitions in 2014-15, LTTS emerged as leading pure play

Present Eq. Paid up Capital: `20.3cr

Engineering Research & Development (ER&D) player. Zinnov recognizes LTTS in

“leadership zone” in 8 Industry verticals (Industrial Automation, Construction and

Fresh Issue: 0.0cr Shares

Heavy Machinery, Medical Devices, Aerospace, Automotive, Rail and Marine,

Offer for Sale: 1.04cr Shares

Telecom, Energy and Utilities) & 2 horizontal offerings (Embedded Systems and

Mechanical). LTTS has 12 Global Delivery Centres (GDCs), 27 sales offices

Post Eq. Paid up Capital: `20.3cr

globally and 31 Labs in India. As of Jun-2016, LTTS has 9,419 Engineers from

Issue size (amount): `884-894.4cr

9 nationalities serving 200+ customers, including >50 of Fortune 500 customers.

Positives: (1) LTTS, a leading global pure-play ER&D company is likely to benefit

Price Band: `850-860

from (a) under-penetration, (b) expected increase in India’s market share in

Lot Size: 16 shares and in multiple there-of

outsourced ER&D space, and (c) strong 13% industry CAGR during FY2015-20E,

Post-issue implied mkt. cap:

(2) pursue multi-pronged growth strategy, which includes (a) Focus on key

`8,643.7cr- 8,745.4cr

Segments, Verticals and Geographies, (b) mine existing customers and add new

Promoters holding Pre-Issue: 100.0%

customers, (c) Focus on Solutions-oriented Engineering services, (d) continued

Promoters holding Post-Issue: 89.8%

investment towards innovation labs, (e) pursue selective acquisitions, (f) Attract

and retain employees, and (3) Operational levers (improvement in Utilization,

better onshore-offshore mix) to aid margin expansion, and (4) strong historical

financial performance.

Book Building

Risks & Concerns: (1) LTTS could lose business volumes if large clients set-up their

QIBs

50% of issue

own captive R&D centers, (2) LTTS is dependent to large extent on limited clients.

Non-Institutional

15% of issue

Loss of a major client could impact the revenues of LTTS.

Valuation: LTTS trades at 21.0x FY2016 EPS at upper-end of issue price band. On

Retail

35% of issue

considering (1) strong growth potential of LTTS, which is ahead of some of the

industry peers, coupled with (2) 38%+ RoE levels in FY2016, (3) FY2015-16

average cash flow from operations of `446cr, (4) strong ~64% dividend payout

Post Issue Shareholding Pattern

(translating to ~4% dividend yield), we are of view that LTTS stock has the

potential to trade at premium to the peers. However, if we consider the average

Promoters Group

89.8

of the 3 peers, then LTTS stock has been priced at 19% discount. Given that the

DIIs/FIIs/Public & Others

10.2

LTTS IPO has been priced at discount, we advise SUBSCRIBE.

Key Financial

Y/E March (` cr)

FY15

FY16

Net Sales

2,619

3,067

% chg

17.1

Net Profit

311

417

% chg

33.8

EBITDA (%)

15.2

17.0

EPS (`)

31

41

P/E (x)

28.1

21.0

P/BV (x)

8.3

8.0

RoE (%)

29.6

38.9

RoCE (%)

33.3

42.2

Yellapu Santosh

EV/Sales (x)

1.8

2.2

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

11.6

12.8

Source: Company, Angel Research; Note: Considered Upper price band of ` 860/share; For EPS

and other valuation purposes, we have considered 10.2cr shares o/s

Please refer to important disclosures at the end of this report

1

L&T Technology Services | IPO note

Issue Details

LTTS is offering 1.04cr equity shares of `2 each via book building route in price

band of `850-860/share, entirely comprising offer for sale by current promoters

L&T.

Exhibit 1: Shareholding Pattern

Pre-Issue

Post-Issue

Particulars

No. of Shares

(%)

No. of Shares

(%)

Promoter Group

101,690,392 100.0

91,290,392

89.8

Retail & HNI Investors

0

0.0

5,200,000

5.1

Institutional Investors

0

0.0

5,200,000

5.1

Source: Company, Angel Research

Objects of the Offer

Objects of the Offer are to achieve benefits of listing equity shares on stock

exchanges and to carry out the offer for sale. Listing of equity shares will

enhance LTTS’s brand name and provide liquidity to existing shareholders.

The listing will also provide a public market for the equity shares in India.

September 9, 2016

2

L&T Technology Services | IPO note

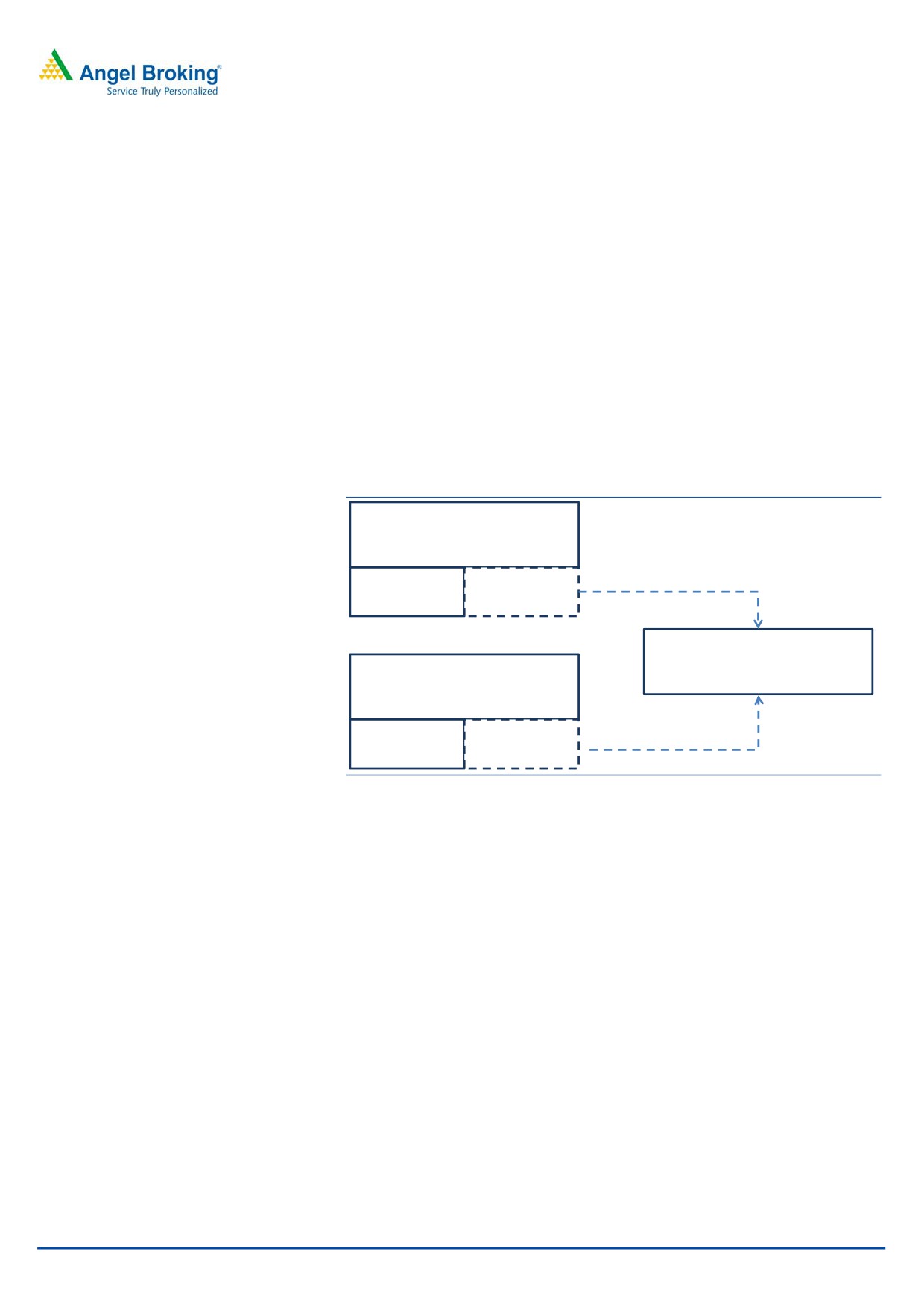

About the Company

LTTS, subsidiary of Engineering giant, L&T was incorporated in Jun-2012.

Thereafter in Jan-2014, Product Engineering Services (PES) division was transferred

from L&T Infotech (LTIL) to LTTS. In Apr-2014, Integrated Engineering Services (IES)

division was transferred from the parent to LTTS. As part of restructuring, LTTS

brought together engineers with domain expertise in product and process industry

from IES and PES to create specialized talent pool in ER&D services. In FY2015,

LTTS acquired majority of equity of TSIPL, a company engaged in the business of,

software development, IT consulting, software evaluation, design, implementation,

research and training in relation to computer software. Further, in FY2015, LTTS

also acquired certain of assets and liabilities of Dell Product and Process

Innovation Services, Engineering services division of Dell U.S.A., and also acquired

its operations in India from Dell India.

Exhibit 2: L&T Background

Larsen & Toubro Ltd.

Transferred in

Apr-2014

Others

IES

L&T Technology Services

L&T Infotech Ltd.

Transferred in

Others

PES

Jan-2014

Source: Company, Angel Research

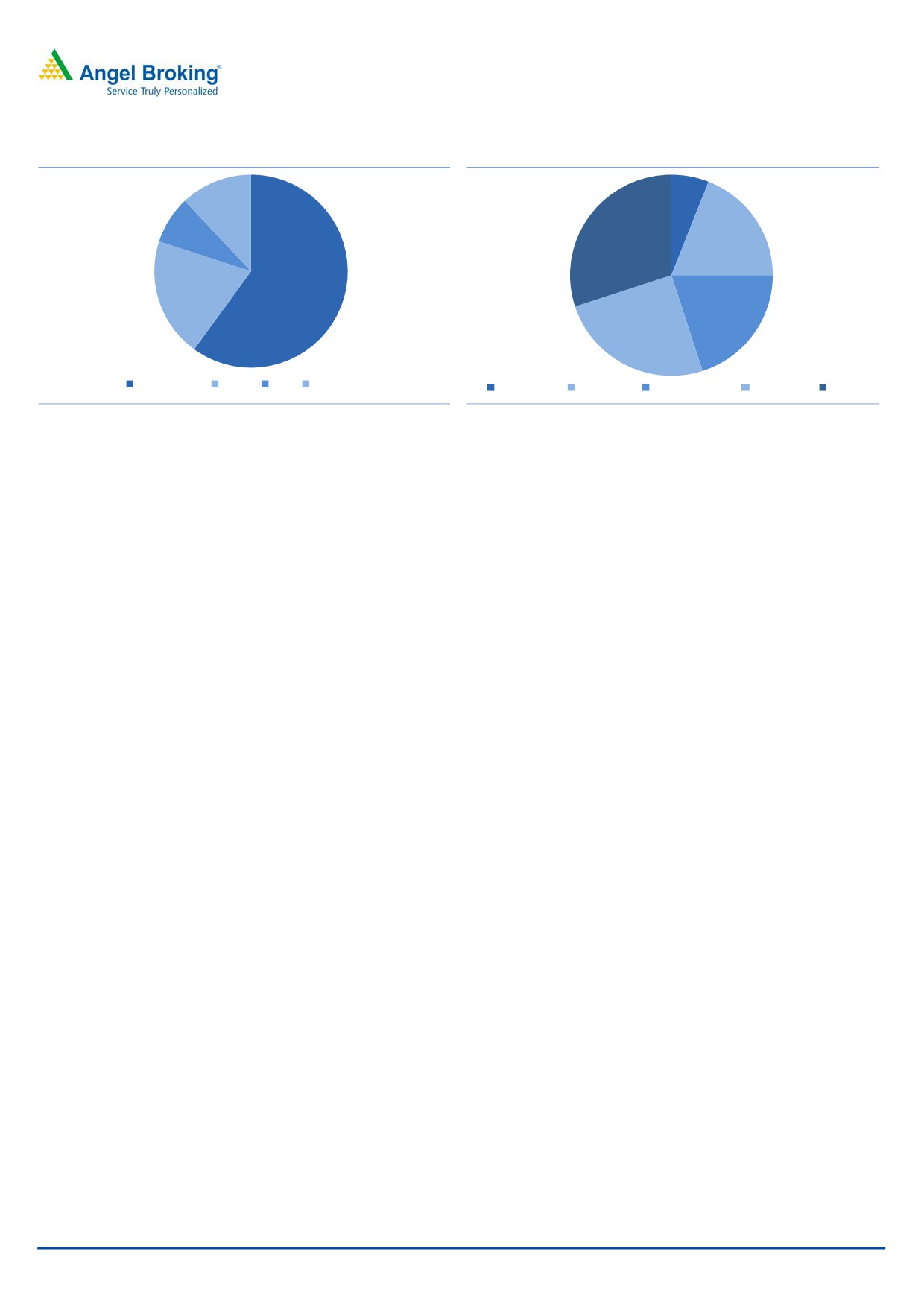

If we look at FY2016 region-wise revenue split then 80% of LTTS revenues were

from North America and Europe (NA- 60%, Europe- 20%), 2 large regions of

corporate ER&D spend. These 2 regions a/c’ed for 73+% of $1,007bn corporate

ER&D services spend in 2015.

Notably, Top 100 spenders contributed 66% of G500 ER&D spend and LTTS’ key

global customers include 43 of the top 100 global ER&D spenders.

LTTS mainly operates in

5 key Industry segments, namely, Transportation,

Industrial Products, Telecom and Hi-tech, Process Industry and Medical Devices,

each represent significant component of G500 ER&D spend.

50% of FY2016 revenues were derived from Industrial Products, Process Industry

and Medical Devices. These segments represent $205bn of the G500 ER&D spend

and have low penetration by India based third-party ER&D service providers, which

gives LTTS competitive advantage.

September 9, 2016

3

L&T Technology Services | IPO note

Exhibit 3: Segment-wise FY2016 revenue mix

Exhibit 4: Industry-wise FY2016 revenue mix

6%

12%

30%

8%

19%

20%

60%

20%

25%

North America Europe India Rest of World

Med. Devices Process Eng. Telecom & Hitech Ind. Products

Transport.

Source: Company, Angel Research

Source: Company, Angel Research

LTTS is considered as one of the world’s leading global pure play ER&D Services

Company. As an ER&D service provider, LTTS offers design, development solutions

throughout product development chain, provides solutions in areas of Mechanical

and Manufacturing Engineering, Embedded Systems, Software Engineering and

Process Engineering. For “new” technologies, LTTS provides services and solutions

in areas of Product Lifecycle Management (PLM), Engineering Analytics, Power

Electronics, M2M connectivity and IoT.

LTTS has invested in IoT, digital technologies (smart products, smart services, smart

manufacturing, smart operations) and Lab Infrastructure to strengthen its position

in these areas. Key decision makers of LTTS customers belong to Engineering/

Product Development/ R&D departments, which tend to have distinct budgets,

where industry domain knowledge and focus on R&D is highly critical in the choice

of outsourcing ER&D service provider. LTTS is of the view that customers value it as

pure-play services provider focused solely on ER&D services, giving them edge

over generalist IT service providers who also provide ER&D services.

LTTS is recognized by Zinnov in “leadership zone” in 8 Industry verticals (Industrial

Automation, Construction and Heavy Machinery, Medical Devices, Aerospace,

Automotive, Rail and Marine, Telecom, Energy and Utilities) & 2 horizontal

offerings (Embedded Systems and Mechanical). LTTS is ranked “high” by ARC

Advisory Group for deep capabilities in Consumer IoT, Industrial IoT, and Smart

Manufacturing.

LTTS currently has 12 Global Delivery Centres (GDCs) in India and overseas,

27 Sales offices in India, North America, Europe, Middle East and Asia and

31 Labs in India. LTTS has filed 35 proprietary patents, 134 patents have been

filed by our customers along with our employees. As of Jun-2016, LTTS has 9,419

Engineers from 9 nationalities serving 200+ customers, including more than 50 of

the Fortune 500 customers.

September 9, 2016

4

L&T Technology Services | IPO note

Investment rationale

ER&D is a large and growing market…

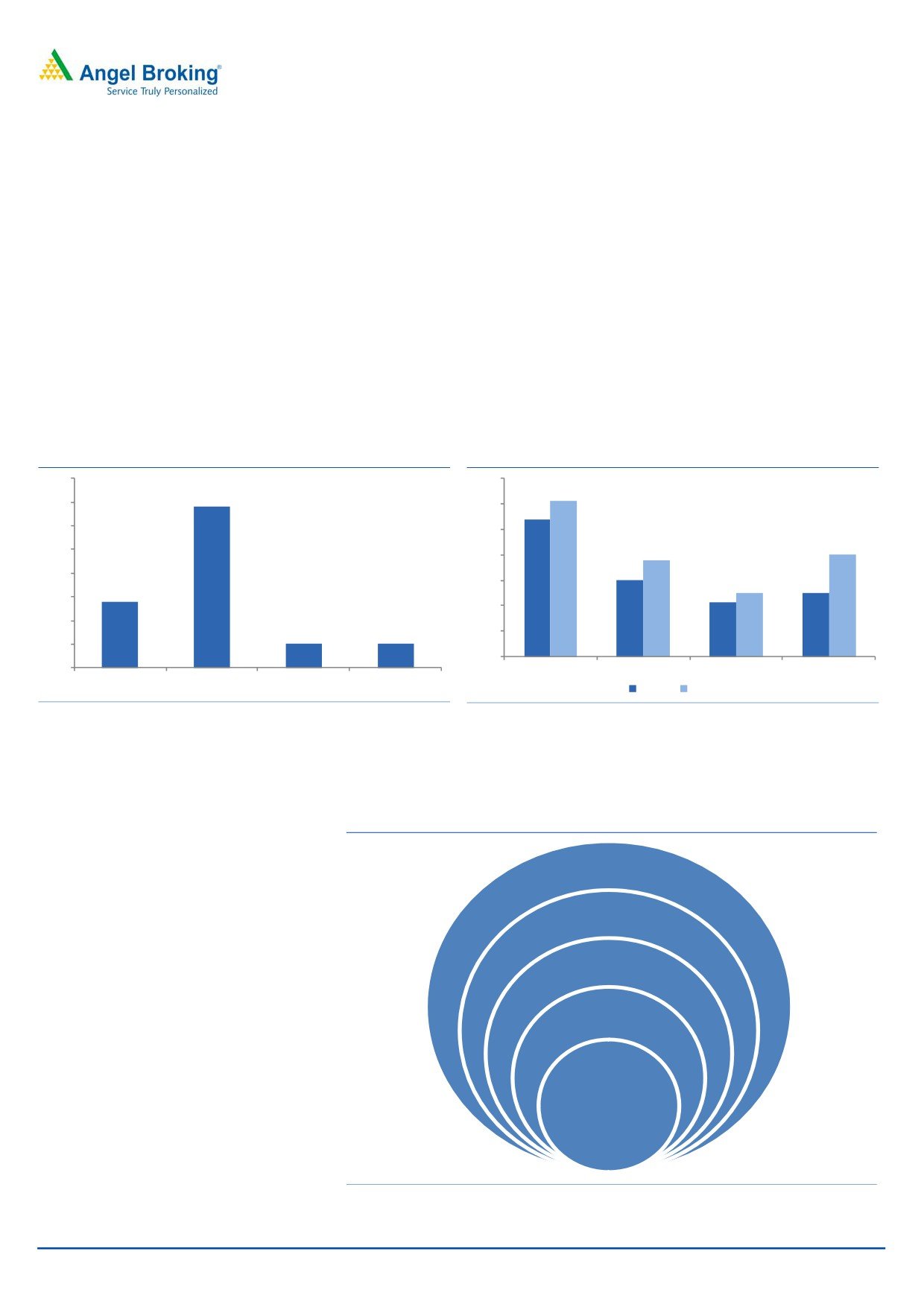

We see huge opportunity for Indian Engineering Research & Development (ER&D)

business going forward, on the back of (1) under-penetration seen (as only

2% of global ER&D is outsourced against 14% in IT Services and 34% in BPM) and

(2) India’s 22% market share of outsourced ER&D portion (against 61% in IT

Services and 38% in BPM). Zinnov Consulting highlights that India addresses

40% of the total outsourced Internet of Things (IoT) Technology market and

globally the IoT market is expected to grow at 16% CAGR during FY2016-21 to

$253bn. Value addition by Indian vendors and exposure to IoT and Analytics have

increased value proposition for the Indian vendors.

Exhibit 5: Share of sourcing in the global spend (%)

Exhibit 6: India's share in global sourcing (%)

40%

70%

61%

34%

35%

60%

54%

50%

30%

40%

25%

38%

40%

30%

20%

30%

25%

25%

14%

21%

15%

20%

10%

5%

5%

10%

5%

0%

0%

IT Services

BPM

ER&D

IOT

IT Services

BPM

ER&D

IOT

FY2013

FY2015

Source: Company, Zinnov. NASSCOM, Angel Research

Source: Company, Zinnov. NASSCOM, Angel Research

As per Zinnov only 2% of $1,007bn of Corporate ER&D spend is being addressed

from India, indicating huge growth potential. Zinnov identifies that of the $365bn

Exhibit 7: Large untapped market

Corporate ER&D spend

$1,007bn

G500 ER&D apend

$614bn

Addressable Engi.

Oustsourcing

$365bn

Global

addressed

market $67bn

Market

addressed from

India $20bn

Source: Company, Zinnov, Angel Research

September 9, 2016

5

L&T Technology Services | IPO note

of addressable engineering outsourcing potential, $215bn is from Product Eng.

Services & $150bn is from Process Eng. Services. Notably, of the $67bn global

addressable market, $36bn is related to Service Providers and $31bn is related to

Global in-house Centres. Within the $20bn identified Indian market opportunity,

$7.8bn is for Indian Service Providers.

Following are some of the advantages Indian Service Providers have over global

peers:

(1) Diversified range of service offerings across verticals (unlike

European/NA/ Chinese players who are specialized in Automotive, Aerospace,

Software, Internet, Telecom and Energy), (2) Skilled offering at low blended billing

rates of $40-50k/year (vs. $70-110k/year in NA & Europe).

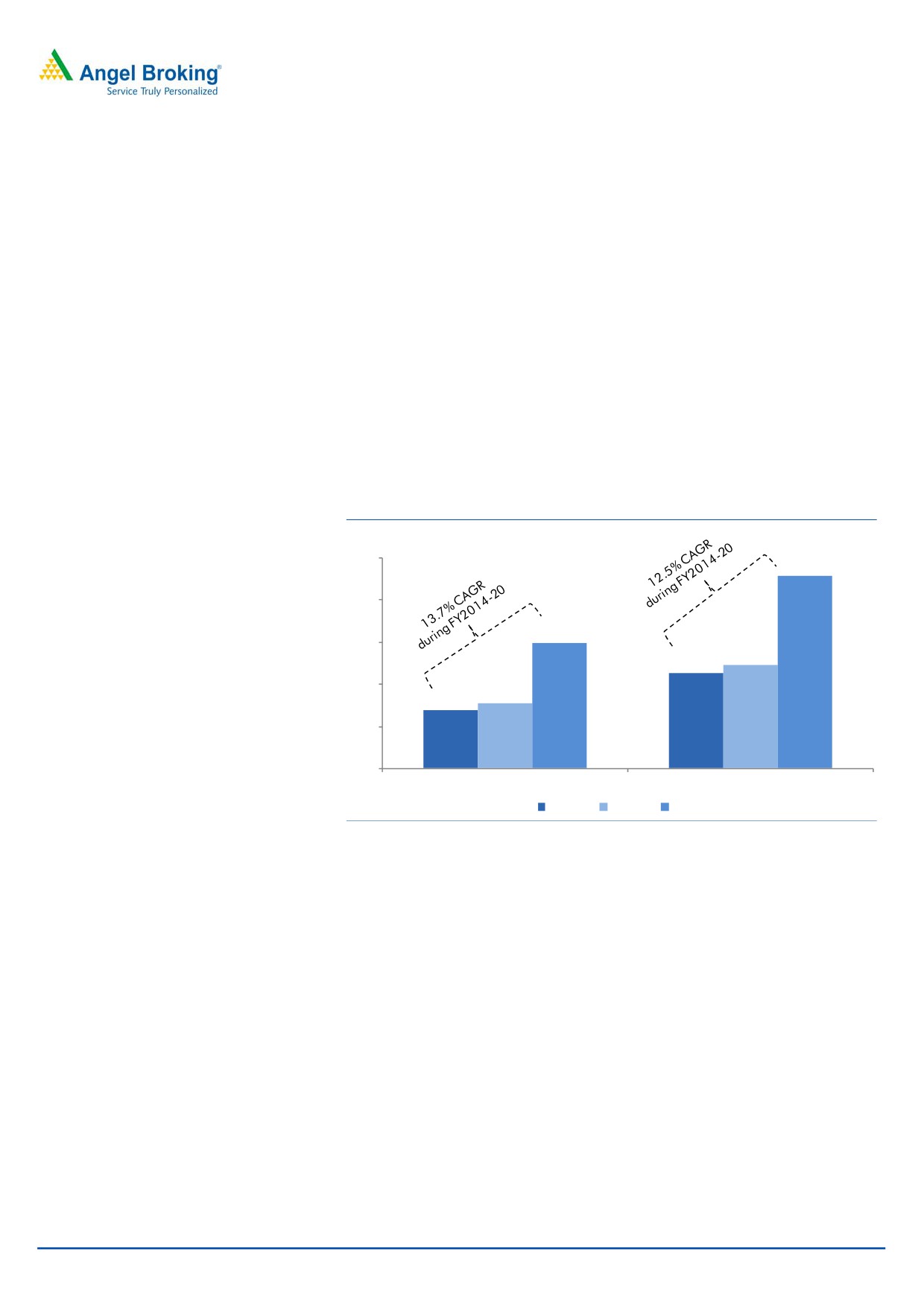

Indian ER&D market is expected to report 13% CAGR during FY2015-20E to

$38bn. Within Indian ER&D space, Service Providers are likely to report 13.7%

CAGR during FY2014-20 to $14.9bn, faster than 12.5% CAGR expected from

In-house R&D centers during the same time period.

Exhibit 8: Service Providers to report 13.7% CAGR during FY2014-20

25

22.9

20

14.9

15

12.3

11.3

10

7.8

6.9

5

0

Service Providers

In-house R&D Centres

FY2014

FY2015

FY2020

Source: Company, Zinnov, Angel Research

LTTS, a leading global pure-play ER&D player…

LTTS in last 3 years has emerged as one of the largest pure-play ER&D players in

India with a delivery model having strong offshore presence in India. LTTS has built

a global delivery model, with ~80% of its revenues booked from 2 of the largest

global markets, i.e. US and Europe.

Despite having presence across diversified verticals, strong market positioning

across low competitive verticals like, Industrial, Process has helped the company

scale operations, which can be seen from their FY2016 turn-over of `3,067cr, and

manpower of 9,419 Engineers who are serving 200+ customers.

September 9, 2016

6

L&T Technology Services | IPO note

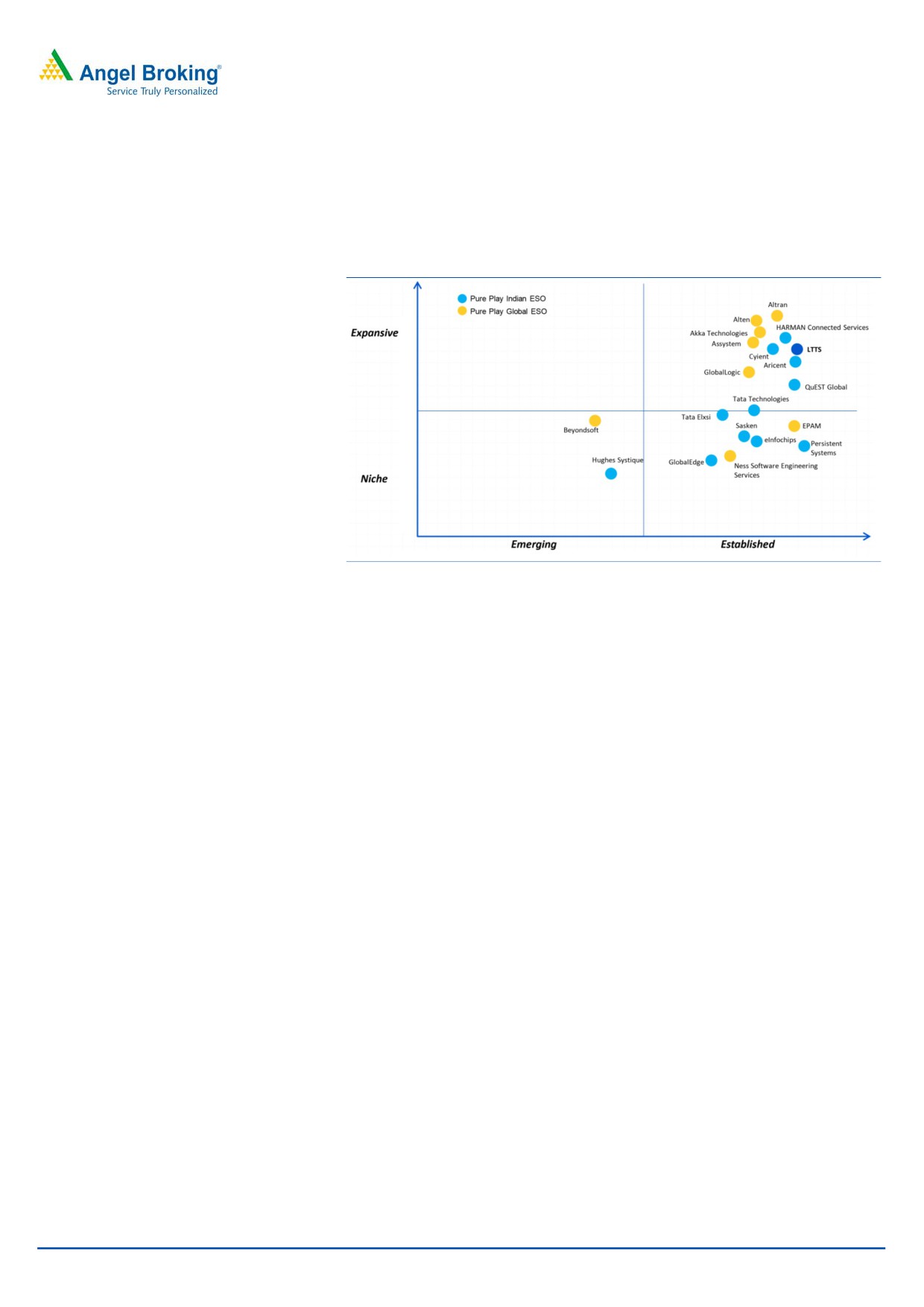

Zinnov in its 2015 report, has recognized LTTS in “leadership zone” in 8 Industry

verticals (Industrial Automation, Construction and Heavy Machinery, Medical

Devices, Aerospace, Automotive, Rail and Marine, Telecom, Energy & Utilities) and

2 horizontal Service offerings (Embedded systems and Mechanical).

Exhibit 9: Leading global pure-play ER&D company

Source: Company, Zinnov, Angel Research

LTTS end-to-end engineering expertise backed by its parent's engineering heritage

of 75+ years provides it with competitive edge over other ER&D players. Strong

parentage has helped (1) LTTS in attracting and retaining quality talent (reported

lower than industry attrition of 12-13%), (2) benefit from parents global network in

exploring business opportunities and getting direct access to senior decision

makers in potential end customers (~95% of business is repeat business).

LTTS, to pursue Multi-pronged growth strategy…

LTTS has been carved out of L&T’s IES and L&T Infotech’s PES division in 2014. If

we just take segmental revenues from both entities, before LTTS was carved out,

then LTTS reported 23.1% revenue CAGR during FY2013-16 to `3,066cr. This

growth is after reducing `111cr of revenues in FY2016 for some non-performing

accounts. LTTS is pursuing multi-pronged growth approach, which in our view

could possibly drive the earnings growth, going forward.

LTTS is pursuing multi-pronged growth strategy, which includes (a) Focus on

key Segments, Verticals and Geographies, (b) mine existing customers and

add new customers, (c) Focus on Solutions-oriented Engineering services, (d)

continued investment towards innovation labs, (e) pursue selective acquisitions,

and (f) Attract and retain employees

Focus on key Segments, Verticals and Geographies

LTTS focuses to pursue growth strategies to expand its market share across key

segments, verticals, geographies and solutions.

Currently LTTS is focusing on (1) Automotive (reported under Transportation) and

(2) all verticals categorized under Industrial Products, Consumer Electronics and

Product software (forms part of Telecom, Hi-tech) segment.

September 9, 2016

7

L&T Technology Services | IPO note

In Automotive vertical, LTTS would focus on software-based engineering solutions,

which will supplement its traditional strength in Auto-mechanics area. Area which

LTTS intends to expand in Automotive space include, Telematics, Advance

driver assist systems, V2X communication (includes vehicle-to-vehicle and

vehicle-to-infrastructure intelligent control and connectivity systems), Green

Technologies (hybrid vehicles, battery management systems), Infotainment and

Body electronics.

In Industrial products segment, LTTS plans to expand its offerings in IoT-enabled

smart products, Renewable Energy space with focus on storage, Grid connectivity,

Energy efficiency for Buildings. In Customer Electronics vertical, LTTS would focus

on Wearables, Connected Homes (Smart Homes), Camera and Security devices.

Geographically LTTS would continue to focus on North America and Europe, which

happen to be the 2 largest markets. Also, LTTS is working on setting-up Labs/

Development Centres in close proximity to its customers' offices. LTTS is keen to

focus on Austria, Switzerland markets and also establish a Delivery centre at East

Europe. LTTS is also keen to expand its operations in Japan, as number of its

existing and prospective Automotive customers are based in Japan.

Mine existing customers, develop new Customer relationships

Top 20 customers of LTTS contributed ~54% of FY2016 revenues (vs. ~56% in

FY2015). LTTS boasts to serve 43 of top 100 global ER&D spenders, representing

66% of G500 ER&D corporate spending budget (Source: Zinnov). This indicates

huge opportunity awaiting for the pure play ER&D companies.

Exhibit 10: Sourcing share in global spend (%)

Exhibit 11: Customer Concentration details...

No. of

No. of

Customer Revenue

Customers-

Customers-

Customer Concentration

FY2016

FY2015

($ mn)

FY2016

FY2015

20+

3

2

New customers added

36

8

10-20

8

8

Revenue from new customers (%)

5.4

1.3

5-10

17

16

Repeat business (%)

94.6

98.7

>1-5

44

41

Source: Company, Zinnov. NASSCOM, Angel Research

Source: Company, Zinnov. NASSCOM, Angel Research

Over the next few years, Top 100 ER&D spending is expected to grow in to a large

market opportunity for LTTS. With majority of LTTS clients belonging to the

sub-$5mn category (61% of the clients as of FY16), there exists scope for increase

in client mining, which could contribute to the long-term growth of LTTS. Also,

36 of these total 72 clients added in FY2016, contributed only 5.4% of the total

FY2016 revenues of `3,067cr.

LTTS is implementing a “T30:A3” model, whereby top customer a/c’s (contributing

in $10mn revenue bracket) have been identified under T30 model and are

developing relationships with adjacent customers, which are identified under A3

model (those with potential to be scaled to $5mn of yearly revenues). Here, LTTS is

identifying potential opportunities from within the same verticals and engage them

in cross-selling of solutions. Further, LTTS seeks to provide value-added solutions

by leveraging its in-depth industry expertise and then expanding the breadth of

services offered to them beyond those in the initial engagement.

September 9, 2016

8

L&T Technology Services | IPO note

Also LTTS aims to leverage its employee’s domain expertise in different services to

offer their customers multiple services and solutions under single engagement. For

example, one of their strategies is to structure large, long term deals with

customers, with defined time periods for execution. These deals would help the

company to improve their productivity and provide better revenue visibility.

Focus on Solutions-oriented Engineering services…

Based on its experience of having served clients in Digital Engineering, Mobile

Internet, IoT (IIoT, mBIoT), Knowledge Automation, Advanced Robotics,

Autonomous and near-autonomous Vehicles, Energy efficiency and Imaging and

Video solutions space, the company as a natural progression is building its

portfolio of Solutions-Oriented Engineering Services across verticals.

A logical extension of their strategy in our view is to develop industry-specific use

cases and then customize these solutions as per specific individual customer

requirements. In order to achieve this goal, LTTS is already in the process of

building and strengthening its alliances with the technology companies.

Higher investment towards Innovation labs…

LTTS has been continuously investing in innovation labs since its establishment and

currently has 31 such labs (located in Bengaluru, Mumbai, Mysore, Vadodara and

Chennai). LTTS also intends increase the scope of its existing labs by adding

space/ equipment to its existing labs to broaden their capabilities and address

customer needs. LTTS has highlighted that it would continue to invest towards the

innovation labs, which would help them provide competitive advantage to its

peers.

Expand business through selective acquisitions…

LTTS has pursued the inorganic growth strategy to grow its business. To-date it has

done 2 acquisitions. In Jun-2014, LTTS acquired 74% stake in TSIPL (Indian

subsidiary of Thales) to further strengthen its expertise in Transportation segment,

especially in the embedded avionics. Thereafter in Jul-2014, LTTS acquired certain

assets and liabilities of Dell India and in Nov-2014, acquired certain assets and

liabilities of Dell USA, which added 3 delivery centers in US to LTTS’s portfolio.

These acquisitions strengthened LTTS’s global ER&D position in Transportation

segment, widened the reach through local delivery centers and enhanced the

talent pool with addition of 200+ engineers to the workforce.

LTTS has further indicated that it would pursue selective acquisitions, strategic

alliances that provide it access to better infrastructure, industry knowledge,

technology expertise, geographical reach and allows it to expand to their vertical

offerings and customer base.

LTTS also intends to pursue acquisitions outside India in order to expand their

global footprint by leveraging low cost offshore delivery model and move greater

portion of their work offshore to India.

LTTS at FY2016-end is sitting on Debt of `195.5cr, reflecting Debt/Equity ratio of

0.2x. During FY2015-16, LTTS generated `822cr of Cash flow from operations.

Considering BS strength, cash generating potential from the current business, LTTS

September 9, 2016

9

L&T Technology Services | IPO note

is well positioned to pursue mid to small size acquisitions, without putting much of

stress on the balance sheet.

Attract, retain highly-skilled employees…

As of Jun-2016, LTTS has 9,419 Engineers with average age of 31 years,

serving 200+ customers. LTTS runs various programs and has been proactive

in attracting, retaining quality talent (reported lower than industry attrition of

12-13%).

Company pursuing multi-pronged growth strategy augurs well for its long-term

growth prospects.

Operational levers to aid Margin expansion…

We sense LTTS has multiple operating levers, which could aid its margin

expansion, going forward.

Exhibit 12: Utilization rates on uptrend...

Exhibit 13: Onshore-Offshore mix to improve...

78%

76%

76%

74%

47%

72%

71%

53%

70%

70%

68%

66%

FY15

FY16

1QFY17

Onsite

Offsite

Source: Company, Angel Research

Source: Company, Angel Research

Revenues from 36 clients added contributed just 5.4% to FY2016 revenues,

indicating that there exists possibility for further client mining from these newly

acquired customers. As a result, we expect Utilization rates in next few quarters to

improve from the 76% reported in 1QFY2017.

At FY2016-end, LTTS reported onshore-offshore mix of 53%:47%. With company

focusing on more of client mining, and maturity in the processes to be attained

going forward from these projects, there again exists possibility of favourable

movement in the onshore-offshore mix.

Further, LTTS has drawn strategy to focus on Solutions Oriented Engineering

services approach. As a result, it could focus on cross-selling existing offerings to

newer customers with some customization (as per requirement). This strategy in the

long-run would aid in gradual margin expansion.

Another margin expansion lever, LTTS has in its kitty is focus on the fast growing,

low competition verticals, like Industrial Products, Process Engineering, and

Medical Devices. Usually billing rates across these segment tend to stand higher

than other verticals, where more competition exists. Favourable shift in the mix

towards high billing and margin business could aid LTTS’s margin expansion

strategy in the long-run.

September 9, 2016

10

L&T Technology Services | IPO note

Strong Financials and Balance Sheet Strength…

LTTS reported 17.1% yoy top-line growth in FY2016, driven by higher repeat

business. Shift in business mix (higher contribution from the high margin business),

improvement in yoy utilization rates (from 69.5% in FY2015 to 71.4% in FY2016)

and better onshore-offshore mix (from 48%:52% in FY2015 to 47%:53% in

FY2016) helped the company report 174 bps improvement in its EBITDA margins

to 17% in FY2016.

We expect such strong performance to continue on the back of LTTS’s leadership

position in the higher growth ER&D verticals, and operating levers to continue to

aid the margin expansion.

LTTS has an unlevered balance sheet as of FY2016, given their D/E ratio at 0.2x

(with debt o/s at `195cr). LTTS in last 2 years generated cash flow from operations

to the tune of `822cr (average for FY2015-16 at `411cr). Comfortable balance

sheet, strong cash flow generating potential of the business suggests that LTTS

could go ahead with small to mid size strategic acquisitions.

Exhibit 14: Strong Cash Flow from Operations potential

Exhibit 15: Impressive RoEs...

70

700

600

59.1

600

60

50

500

42.0

38.9

400

40

291

29.6

300

30

200

20

103

109

10

100

0

0

FY15

FY16

FY15

FY16

Net Debt

CFO

RoE RoCE

Source: Company, Angel Research

Source: Company, Angel Research

Risks & Concerns

1. For large clients willing to set-up their own captive R&D centers could act as a

big threat to company’s business. This could also lead to loss of business.

2. LTTS is dependent to large extent on limited number of customers. On loss of

a major client, LTTS could see decline in the company’s revenues.

September 9, 2016

11

L&T Technology Services | IPO note

Outlook and Valuation

LTTS reported 17.1% yoy top-line growth in FY2016, driven by higher repeat

business. LTTS is pursuing multi-pronged growth strategy of (1) focusing on key

segments, verticals and geographies, (2) mining the existing customers, add new

customers, (3) Focus on Solutions-oriented engineering, (4) continued investment

towards innovation labs, (5) expand business through selective acquisitions, and

(6) retain skilled employees, all augur well for long-term growth prospects of the

company. LTTS on the back of its leadership position in the high growth ER&D

space should be able to report strong revenue growth, going forward.

Continued shift in business mix (with high contribution from high margin business),

likely improvement in yoy utilization rates, better onshore-offshore mix should help

LTTS continue to report EBITDA margin expansion.

For comparison purposes, we have considered Tata Elexsi, Geometric, and Cyient.

Tata Elexsi generates >70% of revenues from Embedded product development

and the remaining from Systems Integration, Industrial design, Visual Effects and

Animation business (this segment’s contribution to the total revenues over the years

has been declining). Tata Elexsi is highly dependent on Transportation vertical,

especially Automotives segment. During FY2014-16, Tata Elexsi reported 18.0%

top-line CAGR to `1,075cr. High contribution from high margin Embedded

product development segment, better onshore-offshore mix helped the company

report 210bps EBITDA margin improvement during the same period to 23.0% and

46.4% PAT CAGR to `155cr.

Exhibit 16: Peer group comparison

Sales

Adj. PAT

Rev. CAGR PAT CAGR

EBITDA %

PAT %

RoE %

P/E

FY15

FY16

FY15

FY16

(FY14-16)

(FY14-16)

FY15

FY16

FY15

FY16

FY15

FY16

FY16

LTTS

2,619

3,067

311

417

20.0%

NA

15.2

17.0

11.9

13.6

29.6

38.9

21.0

Tata Elexsi

849

1,075

102

155

18.0%

46.4%

20.9

23.0

12.0

14.4

36.0

40.1

46.9

Geometric

1,105

1,234

55

105

6.1%

51.0%

12.1

14.3

5.0

8.5

13.5

22.2

14.4

Cyient

2,736

3,096

353

333

18.4%

11.9%

13.9

13.3

12.9

10.8

19.2

17.4

16.2

Average

15.6

16.9

10.0

11.2

22.9

26.6

25.8

Source: Company, Angel Research; Note: NA - Not available

Geometric offers a portfolio of Global Engineering Services, Product Lifecycle

Management (PLM) Solutions, Embedded System Solutions, and Digital Technology

Solutions. Software services a/c for >60% of revenues, with remaining from

Engineering Services. Geometric is pre-dominantly focused on 3 verticals namely,

Automotive, Industrial Heavy Equipment and Aerospace and Defense. During

FY2014-16, Geometric reported 6.1% top-line CAGR to `1,234cr. Shift in business

mix towards high realization areas, improvement in utilization, helped Geometric

report 224bps EBITDA margin expansion during the same period to 14.3% and

report 51% PAT CAGR to `105cr.

Cyient, one of the closest competitor to LTTS is the market leader in Engineering

Services space (accounted for >60% of revenues), especially in Aerospace and

September 9, 2016

12

L&T Technology Services | IPO note

Railways verticals. Data Transformation, Network & Operations (DNO) for

Communication Service Providers and Utilities account for remaining revenues.

During FY2014-16, Cyient reported 18.4% top-line CAGR during to `3,096cr, led

by 3 acquisitions. Revenue growth from organic business has been flat owing to

client specific issues. Pricing pressure, shift in business mix (towards low margin

business), re-investment in restructuring, acquisition of low margin business led to

61bps EBITDA margin decline during the same period to 13.3% and just 11.9%

PAT CAGR to `333cr.

LTTS fares better on all the above-mentioned metrics, given the 20.0% revenue

CAGR seen during FY2014-16, and strong earnings growth. Such strong financial

performance is driven by (1) new client additions, (2) mining of existing clients, and

(3) improvement in the utilization and onshore-offshore mix.

Again on considering Zinnov’s view of leadership position in 8 verticals, and more

operating levers in place, we are optimistic about LTTS continuing to perform

strongly, going forward (glimpse of it is already seen in the 1QFY2017 numbers,

EBITDA/ PAT margins were at 19.3%/14.8% in 1QFY2017 vs. 17.0%/13.6% in

FY2016).

On the back of strong financial performance, LTTS reported impressive RoE’s of

29.6%/38.9% for FY2015/16. This is against peers FY2016 RoE’s in the range of

13.5% (Geometric)-40.1% (Tata Elexsi).

LTTS trades at

21.0x FY2016 EPS at upper-end of issue price band. On

considering (1) strong growth potential of LTTS, which is ahead of some of the

industry peers, coupled with

(2)

38%+ RoE levels in FY2016, (3) FY2015-16

average cash flow from operations of `446cr, (4) strong ~64% dividend payout

(translating to ~4% dividend yield), we are of view that LTTS stock has the potential

to trade at premium to the peers. However, if we consider the average of the 3

peers, then LTTS stock has been priced at 19% discount. Given that the LTTS IPO

has been priced at discount, we advise SUBSCRIBE.

September 9, 2016

13

L&T Technology Services | IPO note

Profit & Loss Statement (Consolidate)

Y/E March (` cr)

FY15

FY16

Net Sales

2,619

3,067

% Chg

17.1

Total Expenditure

2,220

2,546

Operating Expenses

230

266

Employee benefits Expense

1,487

1,723

Other Expenses

503

557

EBITDA

399

520

% Chg

30.5

EBIDTA %

15.2

17.0

Depreciation

48

59

EBIT

350

462

% Chg

31.7

Interest and Financial Charges

3

2

Other Income

25

76

EBT & exceptional items

372

535

Exceptional Items

0

0

EBT

372

535

Tax Expenses

61

119

% of PBT

16.4

22.2

PAT

311

417

Minority Interest loss/ (Income)

(0)

0

PAT after MI

311

417

% Chg

33.8

PAT %

11.9

13.6

Diluted EPS

30.6

41.0

% Chg

33.8

September 9, 2016

14

L&T Technology Services | IPO note

Balance Sheet (Consolidate)

Y/E March (` cr)

FY15

FY16

Sources of Funds

Equity Capital

1,050

1,050

Reserves & Surplus

2

43

Networth

1,052

1,093

Total Debt

219

195

Deferred Tax Liabilities (net)

0

0

Other Long-term Liabilities & Prov.

7

19

Total Liabilities

1,278

1,307

Application of Funds

Gross Block

562

628

Accumulated Depreciation

61

120

Net Block

1,064

1,160

Goodwill

8

8

Investments

0

56

Current Assets

Inventories

175

147

Sundry Debtors

685

727

Cash and Bank Balance

115

86

Loans & Advances

232

234

Other Current Asset

0

0

Current Liabilities

537

614

Net Current Assets

671

581

Deferred Tax Assets

37

36

Total Assets

1,278

1,307

September 9, 2016

15

L&T Technology Services | IPO note

Cash Flow Statement (Consolidate)

Y/E March (` cr)

FY15

FY16

Profit before tax

372

535

Depreciation & Other Non-cash Charges

48

59

Change in Working Capital

(64)

151

Interest & Financial Charges

2

(1)

Direct taxes paid

(67)

(145)

Cash Flow from Operations

291

600

(Inc)/ Dec in Fixed Assets

(53)

(127)

(Inc)/ Dec in Investments & Oth. Adj.

(614)

(52)

Cash Flow from Investing

(667)

(179)

Issue/ (Buy Back) of Equity

547

0

Inc./ (Dec.) in Borrowings

170

(23)

Dividend Paid (Incl. Tax)

(250)

(358)

Interest Expenses & Oth. Adj.

(3)

(2)

Cash Flow from Financing

464

(383)

Inc./(Dec.) in Cash & forex translation

86

(29)

Opening Cash balances

29

115

Closing Cash balances

115

86

September 9, 2016

16

L&T Technology Services | IPO note

Ratio Analysis

Y/E March

FY15

FY16

Valuation Ratio (x)

Adj. P/E (on FDEPS)

28.1

21.0

Adj. P/CEPS

24.3

18.4

Dividend yield (%)

4.9

4.7

EV/Sales

1.8

2.2

EV/EBITDA

11.6

12.8

EV / Total Assets

0.4

0.6

Per Share Data (`)

Adj. EPS (fully diluted)

30.6

41.0

Cash EPS

35.4

46.8

DPS

41.8

40.3

Book Value

103

107

Returns (%)

RoCE (Pre-tax)

33.3

42.2

Angel RoIC (Pre-tax)

27.3

35.3

RoE

29.6

38.9

Turnover ratios (x)

Total Asset Turnover (x)

2.0

2.3

Inventory / Sales (days)

24

18

Receivables (days)

96

87

Payables (days)

75

73

WC (days)

45

31

Leverage Ratios (x)

D/E ratio (x)

0.2

0.2

Source: Company, Angel Research; Note: Considered Upper price band of `860/share; For EPS

and other valuation purposes, we have considered 10.2cr shares o/s

September 9, 2016

17

L&T Technology Services | IPO note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

September 9, 2016

18