Initiating Coverage | Banks

March 31, 2017

Karur Vysya Bank

BUY

CMP

`110

Easing troubles to pave way for growth

Target Price

`140

Karur Vysya Bank (KVB) is one of the oldest private sector banks with strong presence in

Investment Period

12 Months

the Southern parts of India. More than 53% of KVB’s 706 branches are located in

Tamil Nadu, however it is gradually branching out in other parts of India also.

Stock Info

Sector

Banks

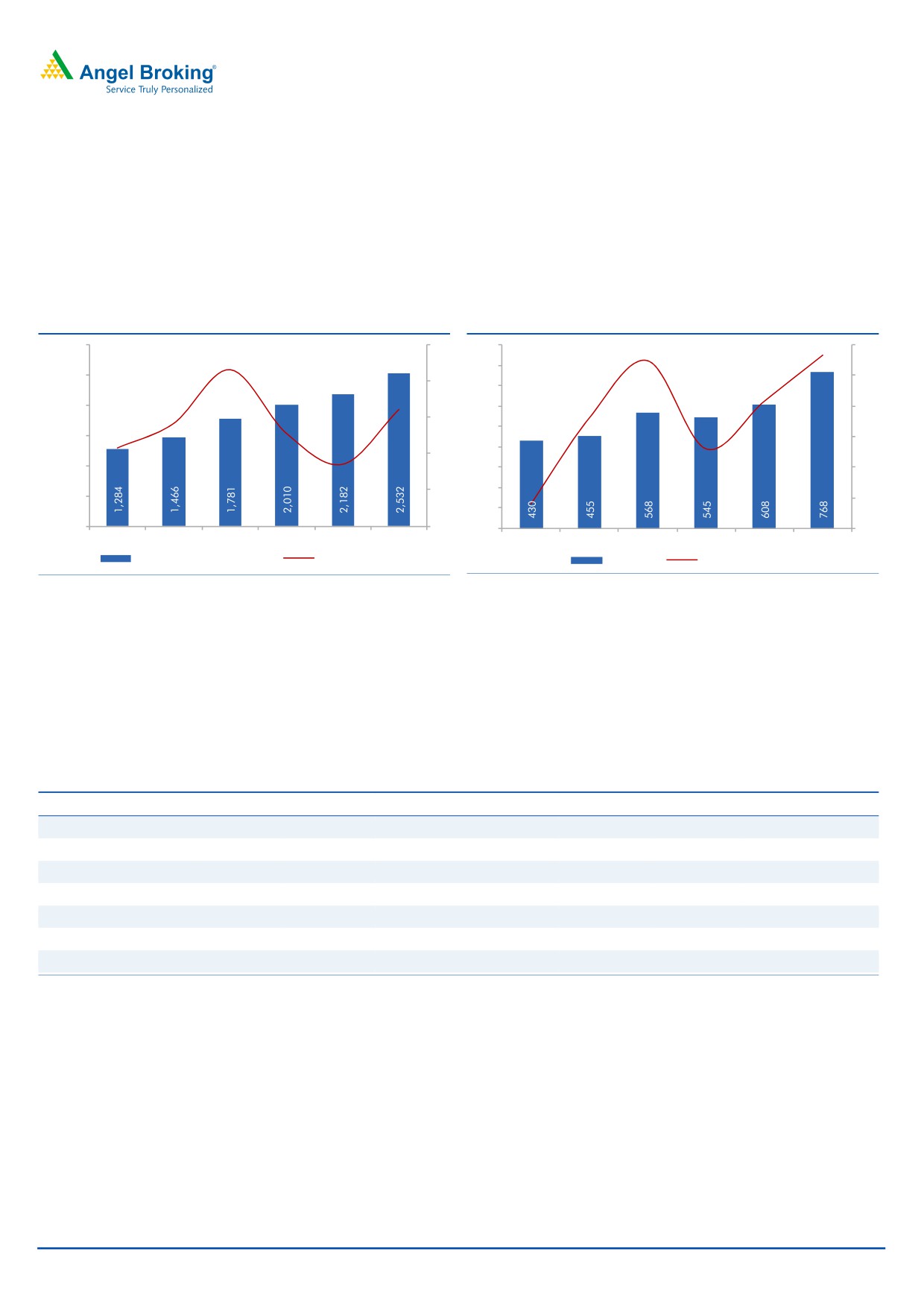

Loan growth trajectory should pick up: KVB’s loan book reported a healthy CAGR

of 17% over FY2011-16. However, FY2017 has been a lackluster year so far with loan

Market Cap (` cr)

6,730

growth of only 3.3%. Nevertheless, we expect the growth trajectory to pick up from

Beta

0.5

FY2018 onwards. While the bank is still largely dependent upon corporate loans for its

52 Week High / Low

112/80

growth, it has been scaling up its presence in the retail loans segment gradually. Retail

Avg. Daily Volume

150,460

as a % of total loans has gone up to 16% at the end of 3QFY17 as compared to 8% in

FY2012, and this is likely to see further improvement in the years to come.

Face Value (`)

2

BSE Sensex

29,647

Fairly stable deposit growth further boosted by demonetization: KVB’s deposits

have reported a healthy 15.2% CAGR over FY2011-16. The growth in deposits

Nifty

9,174

got a further boost owing to demonetization. During demonetization the bank

Reuters Code

KARU.BO

received strong flows in the low cost CASA base and the share of CASA in total

Bloomberg Code

KVB@IN

deposits thus went up to 30.8% at the end of 3QFY2017 v/s 23.3% in FY2016

end. Though incrementally the growth in CASA could taper down, we expect

overall deposits to grow at a CAGR of 9% over FY2017-19.

Shareholding Pattern (%)

Asset quality issues to subside gradually: KVB had maintained a fairly stable asset

Promoters

2.1

quality in a challenging economic environment, however prolonged slowdown in the

MF / Banks / Indian Fls

28.9

core sector took a toll on its asset quality and GNPAs went up from 1.30% (FY2016)

FII / NRIs / OCBs

19.8

to 2.66% at the end of 3QFY2017, while NNPAs went up to 1.68% v/s 0.55% over

Indian Public / Others

49.3

the same period. We expect NPAs issues to subside in the quarters to come.

Moderate credit costs will lead to earnings pick up and gradual recovery in RoE:

Historically KVB had maintained a moderate credit cost of 40-45 bps, which

Abs.(%)

3m 1yr 3yr

jumped in FY2014/15 to 130/133 bps. However, it has moderated subsequently

Sensex

11.3

17.0

32.7

and we expect this to further moderate to 70 bps by FY2019. Lower incremental

KVB

35.0

28.6

52.1

slippages, pick up in business growth and moderate credit cost should help

earnings to grow by 12% & 26 % in FY2018 &19 respectively.

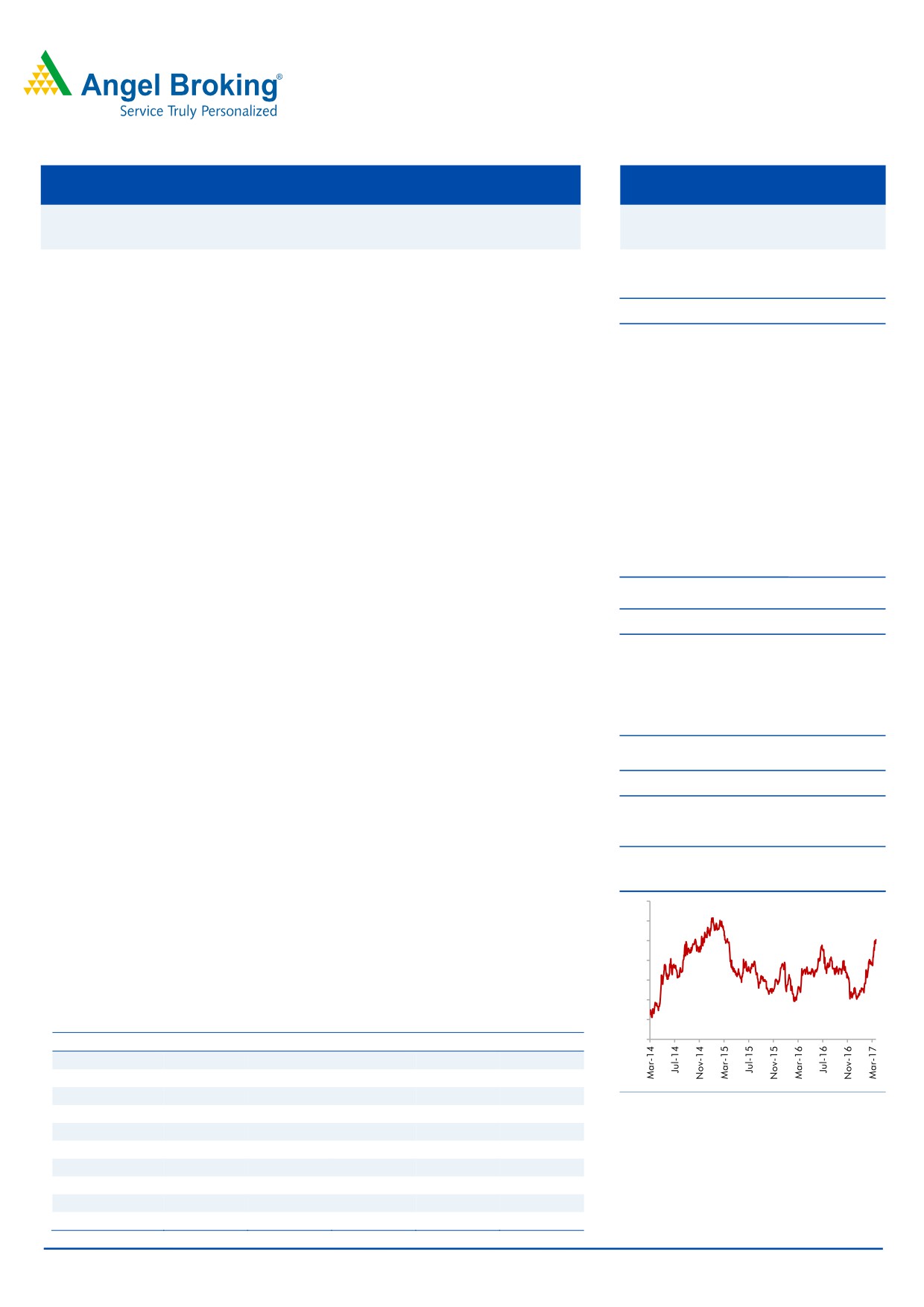

3-year price chart

Outlook and valuation: KVB’s earnings were impacted due to higher provisions

130

and lower business growth, however, we expect gradual recovery on both the

120

fronts going ahead. While in FY2018 we expect earnings recovery to be visible,

110

sharp growth is expected in FY2019. At the CMP the stock is trading at 1.1x it’s

100

FY2019 BV. We have valued the stock at 1.4x its FY2019E BV and recommend

90

BUY with a Target Price of `140 over the next 12 months.

80

70

Key financials (Standalone)

60

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

FY2019E

NII

1,466

1,781

2,010

2,182

2,532

% chg

14.2

21.5

12.8

8.6

16.1

Net profit

455

568

545

608

768

Source: Company, Angel Research

% chg

6.0

24.7

(4.0)

11.5

26.5

NIM (%)

2.8

3.2

3.3

3.2

3.4

EPS (`)

7.5

9.3

8.9

10.0

12.6

P/E (x)

14.7

11.8

12.3

11.0

8.7

P/ABV (x)

1.6

1.5

1.3

1.2

1.1

Siddharth Purohit

RoA (%)

0.9

1.0

0.9

0.9

1.0

022 - 3935 7800 Ext: 6828

RoE (%)

12.0

12.9

11.2

11.4

13.2

Source: Company, Angel Research; Note: CMP as of March 30, 2017

Please refer to important disclosures at the end of this report

1

Karur Vysya Bank | Initiating Coverage

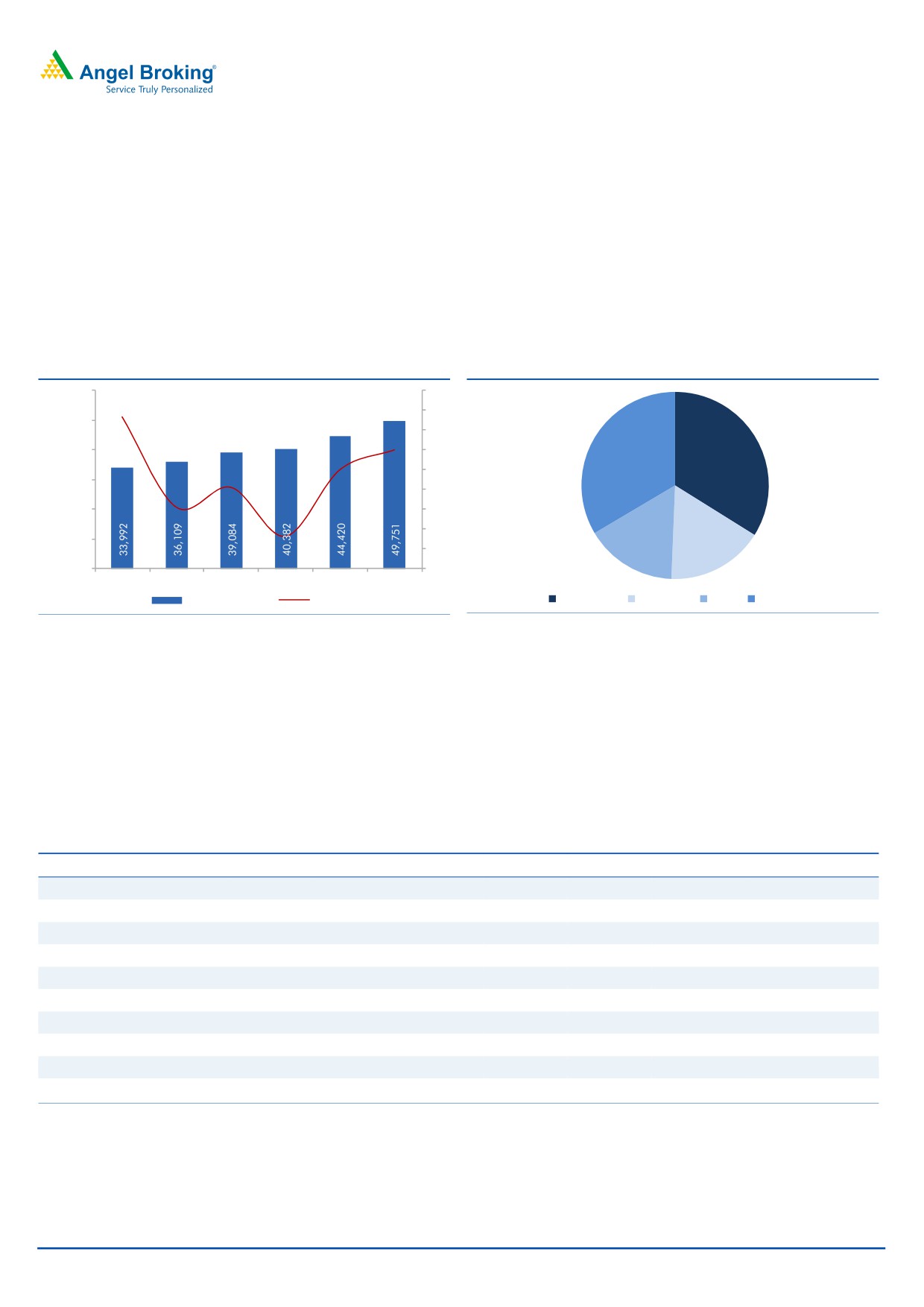

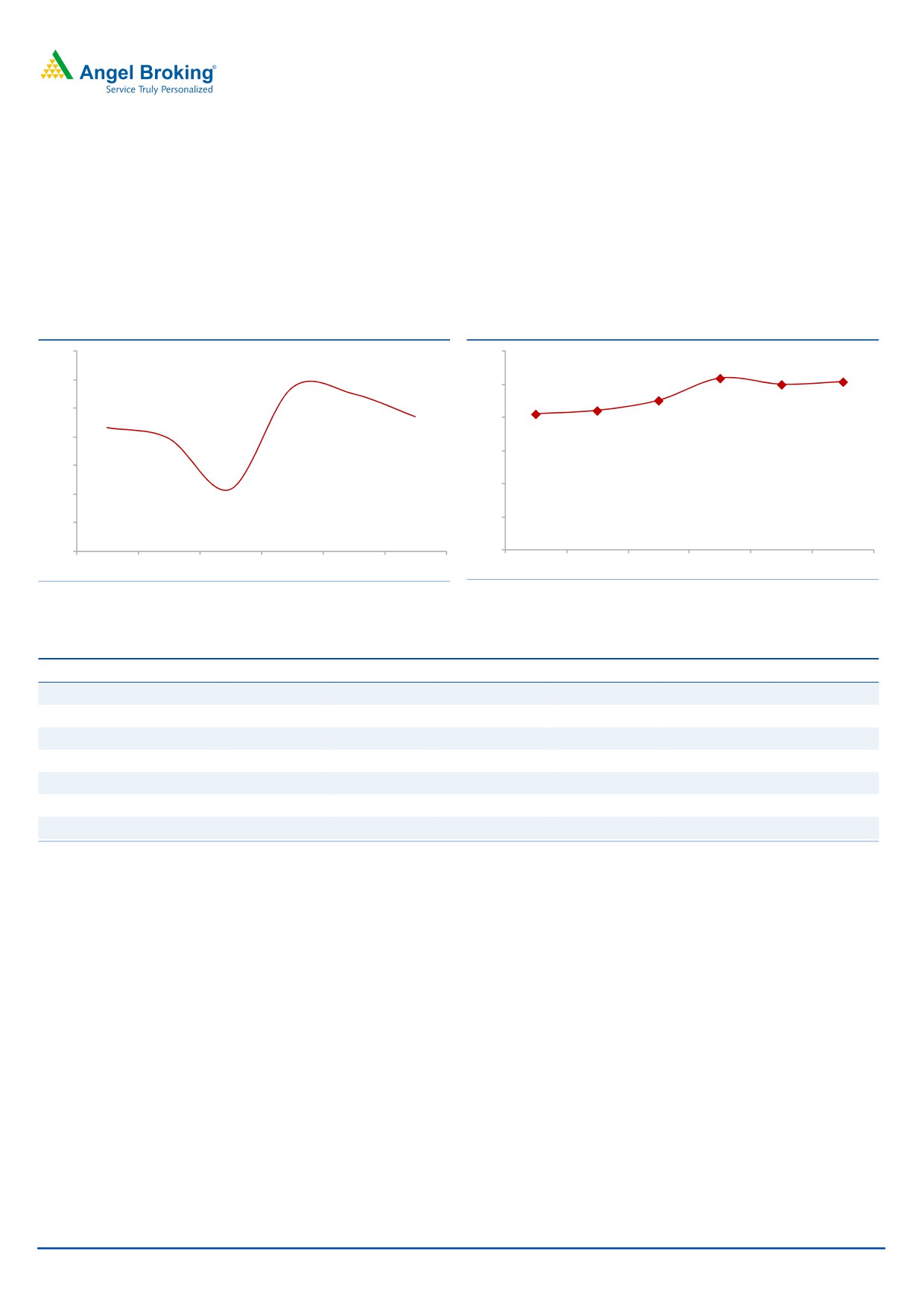

Loan growth remained moderate over the last few years,

likely to see revival from FY2018

KVB’s loan book reported a healthy CAGR of 17% over FY2011-16. However,

FY2017 has been a lackluster year so far with loan growth of only 3.3%. Too much

reliance on the corporate side has impacted the growth of the bank in the recent

quarters, as incremental demand from corporate segment has been muted due to

the lack of fresh capex. Further, looking at the stress in asset quality, the

management has further slowed down the loan book expansion.

Exhibit 1: Loan growth has remained moderate

Exhibit 2: Loan Bifurcation Segmemnt wise %

60,000

18

16

50,000

15.3

14

12.0

40,000

12

34%

34%

10.0

10

30,000

8.2

8

20,000

6.2

6

4

10,000

3.3

2

16%

17%

-

0

FY14

FY15

FY16

FY17E

FY18E

FY19E

Advances (` cr)

Growth (%)

Commercial

Agriculture

Retail

Corporates

Source: Company, Angel Research

Source: Company, Angel Research

While the bank is still largely dependent upon corporate loans for its growth, it has

been scaling up its presence in the retail loans segment gradually. Retail as a % of

total loans has gone up to 16% at the end of 3QFY17 as compared to 8% in

FY2012, and this is likely to see further improvement in the years to come. Further,

political instability in its home state Tamil Nadu also had been one of the key

reasons for the lack of credit growth, however with stability in Government now,

investments should revive, leading to better credit off take.

Exhibit 3: Advances Bifurcation Segment Wise

Segment Wise (` Cr)

FY12

FY13

FY14

FY15

FY16

3QFY17

CAGR 12-16 (%)

Advances

23,949

29,480

33,992

36,691

39,476

38,460

13.3

Commercial

8,231

9,513

11,217

11,774

12,764

13,035

11.6

Agriculture

3,807

5,386

6,119

6,240

7,032

6,442

16.6

Retail

1,976

3,502

4,079

5,274

5,918

6,093

31.6

Corporates

10,191

11,079

12,577

13,402

13,764

12,890

7.8

Segment Wise (%)

Commercial

34

32

33

32

32

34

Agriculture

16

18

18

17

18

17

Retail

8

12

12

14

15

16

Corporate

43

38

37

37

35

34

Source: Company, Angel Research

March 31, 2017

2

Karur Vysya Bank | Initiating Coverage

Exhibit 4: Advances Category Wise (` Cr )

FY12

FY13

FY14

FY15

FY16

3QFY17

CAGR 12-16 (%)

Manufacturing Sector

9,390

10,260

12,026

12,558

13,688

12,627

9.9

Jewel Loan

5,200

7,798

8,006

7,060

6,282

6,094

4.8

Personal Loan Segment

3,077

3,745

4,141

4,743

5,310

5,364

14.6

Trading

2,576

4,035

3,909

4,812

5,771

5,783

22.3

Bills

1,292

1,558

2,112

2,010

1,352

1,118

1.1

NBFC

1,255

1,116

833

968

975

1,041

(6.1)

Other Exposure

1,415

1,194

3,399

4,540

6,076

6,433

44.0

Total Advances

24,205

29,706

34,426

36,691

39,454

38,460

13.0

Source: Company, Angel Research

Exhibit 5: Manufacturing Sector Break Up (` Cr)

FY12

FY13

FY14

FY15

FY16

3QFY17

CAGR 12-16 (%)

Textiles

1,777

2,057

2,595

2,771

3,515

3,423

18.6

Infrastructure

2,984

2,948

3,164

3,422

3,354

2,751

3.0

Food Processing

863

1,010

1,134

1,317

1,282

1,302

10.4

Basic Metal & Metal Products

1,154

1,438

1,597

1,459

1,225

1,247

1.5

Chemicals & Chemicals Products

494

473

719

641

720

488

9.9

All Engineering

270

386

424

499

433

441

12.5

Transport Equipments

256

214

313

380

368

393

9.5

Cement & Cement Products

95

92

91

81

375

379

41.0

Gems & Jewellery

217

252

366

378

342

371

12.0

Other Industries

1,280

1,390

1,623

1,610

2,019

1,832

12.1

Total Industry Exposure

9,390

10,260

12,026

12,558

13,633

12,627

9.8

Source: Company, Angel Research

KVB has a strong presence in the Textile belt of Coimbatore-Karur-Tirupur region

and has strong relationships with the local textile manufactuers. Textile loans

account for ~27% of the bank’s manufcaturing sector loan book and ~9% of the

total loan book, and has reported a 18.6% CAGR over FY2012-16. In the near

term the Indian textile manufcaturers are seeing some moderation in growth due

to the overall slow down in the developed countries, which are their export

destinations. However, Indian textile industry remains quite competitive and is likley

to bounce back, which should aid the loan growth for the bank.

Exhibit 6: Comparative Loan Book (` Cr)

Company

FY11

FY12

FY13

FY14

FY15

FY16

CAGR 5Yr (%)

KVB

17,814

23,949

29,480

33,992

36,109

39,084

17.0

LVB

8,094

10,189

11,703

12,889

16,352

19,644

19.4

Federal Bank

31,953

37,756

44,097

43,436

51,285

58,090

12.7

City Union Bank

9,255

12,137

15,246

16,097

17,966

21,057

17.9

Karnataka Bank

17,348

20,721

25,208

28,345

31,680

33,902

14.3

DCB

4,271

5,284

6,586

8,140

10,465

12,921

24.8

South Indian Bank

20,489

27,281

31,816

36,230

37,392

41,086

14.9

Source: Company, Angel Research

March 31, 2017

3

Karur Vysya Bank | Initiating Coverage

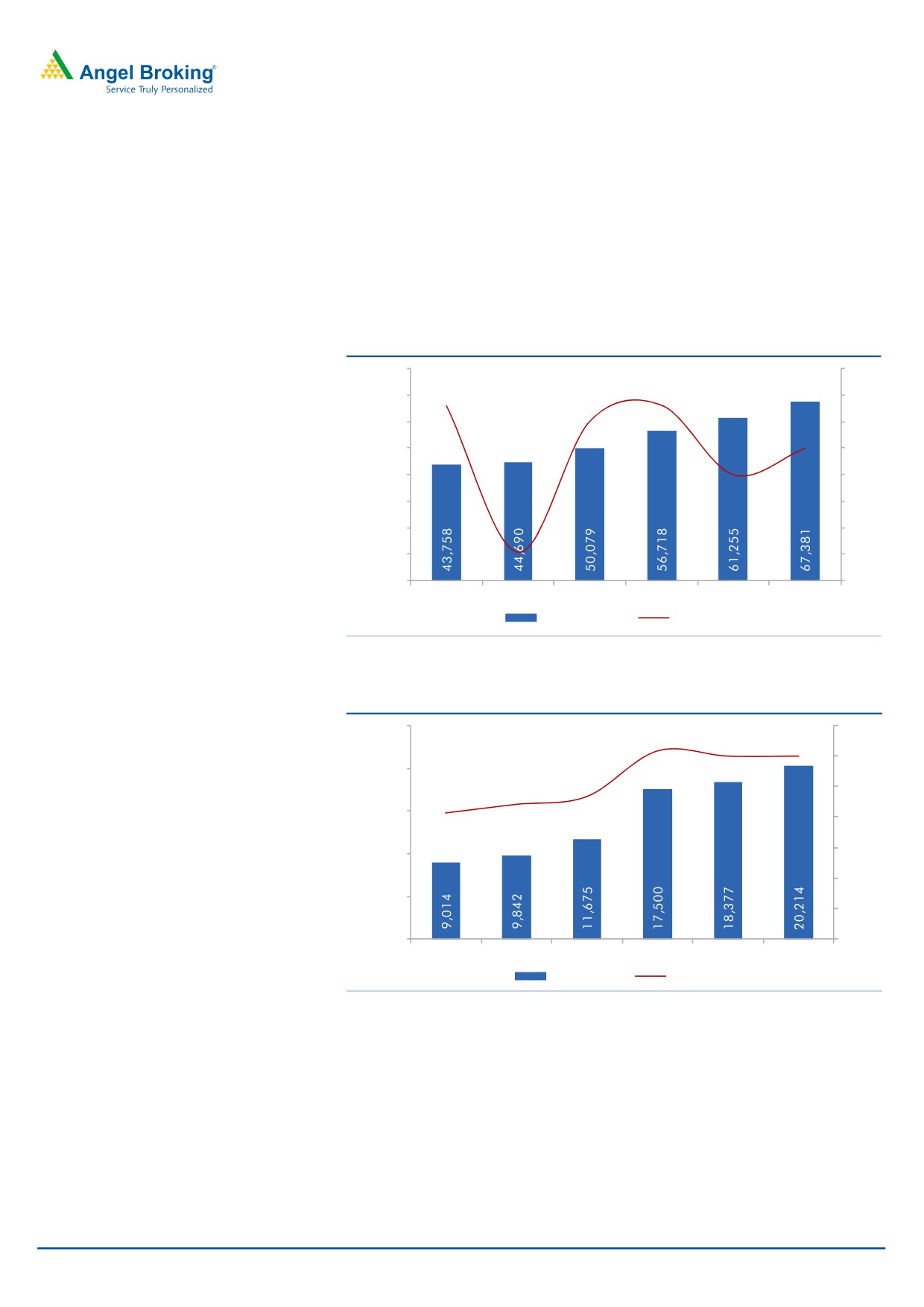

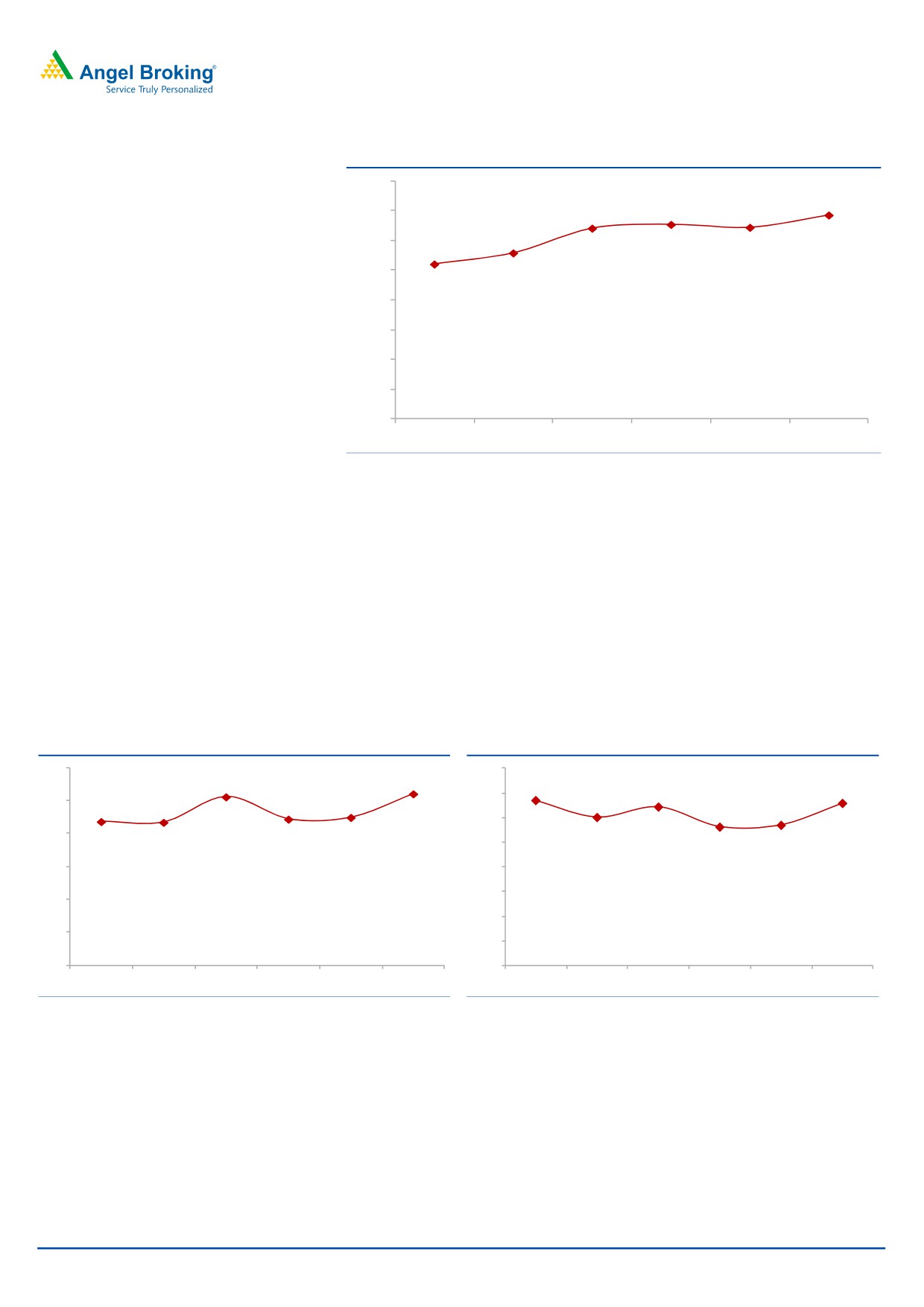

Fairly stable deposit growth further boosted by demonetization

KVB’s deposits have reported a healthy 15.2% CAGR over FY2011-16. The growth in

deposits got a further boost owing to demonetization. During demonetization the bank

received strong flows in the low cost CASA base and the share of CASA in total

deposits thus went up to 30.8% at the end of 3QFY2017 v/s 23.3% in FY2016 end.

Though incrementally the growth in CASA could taper down, we expect

overall

deposits to grow at a CAGR of 9% over FY2017-19.

Exhibit 7: Deposit growth has been fairly strong

80,000

16.0

13.2

13.3

70,000

14.0

12.1

60,000

12.0

10.0

50,000

10.0

8.0

40,000

8.0

30,000

6.0

20,000

4.0

2.1

10,000

2.0

-

0.0

FY14

FY15

FY16

FY17E

FY18E

FY19E

Deposits (` cr)

Growth (%)

Source: Company, Angel Research

Exhibit 8: Deposits got a boost backed by CASA

25,000

35.0

30.9

30.0

30.0

30.0

20,000

23.3

22.0

25.0

20.6

15,000

20.0

15.0

10,000

10.0

5,000

5.0

-

-

FY14

FY15

FY16

FY17E

FY18E

FY19E

CASA (` cr)

CASA (%)

Source: Company, Angel Research

March 31, 2017

4

Karur Vysya Bank | Initiating Coverage

Exhibit 9: Comparative Deposit Growth

Deposits (` Cr)

FY11

FY12

FY13

FY14

FY15

FY16

CAGR 5 Yr (%)

KVB

24,722

32,112

38,653

43,758

44,690

50,079

15.2

LVB

11,150

14,114

15,619

18,573

21,964

25,431

17.9

Federal Bank

43,015

48,937

57,615

59,731

70,825

79,172

13.0

City Union Bank

12,914

16,341

20,305

22,017

24,075

27,158

16.0

Karnataka Bank

27,336

31,608

36,056

40,583

46,009

50,488

13.1

DCB

5,610

6,336

8,364

10,325

12,609

14,926

21.6

South Indian Bank

29,721

36,501

44,262

47,491

51,912

55,721

13.4

Source: Company, Angel Research

Exhibit 10: Low Cost Deposits of comparative banks

CASA (%)

FY11

FY12

FY13

FY14

FY15

FY16

KVB

23.3

19.2

19.2

20.6

22.0

23.3

LVB

18.8

14.9

14.5

14.2

16.7

17.4

Federal Bank

26.9

27.5

0.0

30.8

30.4

32.5

City Union Bank

19.6

18.2

16.8

17.8

19.2

20.4

Karnataka Bank

24.9

24.6

24.9

25.4

24.9

26.3

DCB

35.2

32.1

27.2

25.0

23.4

23.4

South Indian Bank

21.5

19.7

18.6

20.7

20.6

22.4

Source: Company, Angel Research

March 31, 2017

5

Karur Vysya Bank | Initiating Coverage

Strong NII growth was cost dented by higher operating and

credit costs, which should normalize over the next few years

KVB’s NII has grown at 18.4% CAGR over FY2011-16 backed by a 17% CAGR in

loan book. However, FY2017 has been a year of consolidation for the bank and

we expect FY2017 to end with 12.8% growth in NII, however, we expect that it

would pick up from FY2018 onwards.

Exhibit 11: NII Growth trend

Exhibit 12: PAT growth trend

3,000

25

900

24.7

26.5

30

21.5

800

2,500

20

20

700

11.5

16.1

2,000

14.2

600

6.0

10

15

12.8

500

10.8

(4.0)

1,500

0

8.6

400

10

1,000

300

-10

5

200

(22.0)

500

-20

100

-

0

0

-30

FY14

FY15

FY16

FY17E

FY18E

FY19E

FY14

FY15

FY16

FY17E

FY18E

FY19E

Net Interest Income (` cr)

YoY Growth (%)

PAT (` cr)

YoY Growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

As shown in the below table KVB’s NII growth has been quite robust reporting

18.4% CAGR over FY2011-16 and is very much comparable to its peers. However,

as mentioned earlier higher operating costs and credit costs took a toll on the

earnings growth of the bank, which has reported a CAGR of 6.4% over the same

period. However, with credit cost coming under control we expect the bank’s

bottom-line growth to outpace the NII growth over the next two years.

Exhibit 13: Comparative NII Growth

NII (` Cr)

FY11

FY12

FY13

FY14

FY15

FY16

CAGR 5 Yr (%)

KVB

767

917

1,158

1,284

1,466

1,781

18.4

LVB

365

371

392

486

527

645

12.1

Federal Bank

1,747

1,953

1,975

2,229

2,380

2,504

7.5

City Union Bank

420

500

624

759

807

981

18.5

Karnataka Bank

612

744

904

1,056

1,169

1,303

16.3

DCB

189

228

284

368

508

620

26.8

South Indian Bank

791

1,022

1,281

1,399

1,366

1,510

13.8

Source: Company, Angel Research

March 31, 2017

6

Karur Vysya Bank | Initiating Coverage

Asset quality issues to subside gradually

KVB had maintained a fairly stable asset quality in a challenging economic

environment, however, prolonged slowdown in the core sectors took a toll on its

asset quality. The bank’s large dependence upon corporates and dwindling

profitability of the sectors has impacted the asset quality. Thus, the GNPAs which

were 1.30% at the end of FY2016 went up to 2.66% at the end of 3QFY2017,

while NNPAs went up to 1.68% v/s 0.55% over the same period of time. We expect

asset quality pressure to subside in the quarters to come.

Exhibit 14: GNPAs & NNPAs Ratio yearly trend (%)

3.50

3.2

3.1

3.00

2.7

2.50

1.9

2.00

1.67

1.64

1.60

1.50

1.3

1.00

0.8

0.78

0.55

0.41

0.50

0.00

FY14

FY15

FY16

FY17E

FY18E

FY19E

Gross NPAs (%)

Net NPAs (%)

Source: Company, Angel Research

Exhibit 15: Slippages (%)

3.50

3.14

3.00

2.48

2.50

2.00

2.00

1.82

1.50

1.50

1.00

0.50

0.50

0.00

FY14

FY15

FY16

FY17E

FY18E

FY19E

Source: Company, Angel Research

March 31, 2017

7

Karur Vysya Bank | Initiating Coverage

Large scale slippages and resultant higher credit cost impacted the bottom-line of

the bank. The last three quarters of FY2017 have been quite painful with

increasing slippages. However, we believe that a large part of the troubled assets

have already slipped into NPA and incremental slippages would be under control

for KVB. Further, recovery and up gradation is likely to gain momentum and this

should also aid in the overall control on the GNPA levels.

Exhibit 16: Comparable Asset quality of peer banks

GNPAs (%)

FY11

FY12

FY13

FY14

FY15

FY16

3QFY17

KVB

1.26

1.33

0.96

0.82

1.85

1.30

2.66

LVB

1.93

2.97

3.84

4.10

2.73

1.97

2.78

Federal Bank

3.49

3.35

3.44

2.70

2.04

2.84

2.77

City Union Bank

1.21

1.01

1.13

1.81

1.86

2.41

2.98

Karnataka Bank

3.97

3.27

2.51

2.92

2.95

3.44

4.30

DCB

5.86

4.40

3.18

1.69

1.76

1.51

1.55

South Indian Bank

1.11

0.97

1.36

1.19

1.71

3.77

3.98

Source: Company, Angel Research

Exhibit 17: Credit Cost (%)

Exhibit 18: PCR( %)

70

1.40

1.30

1.33

59

58

60

1.20

50

50

50

50

1.00

0.89

40

0.83

0.80

40

0.80

0.70

30

0.60

0.40

20

0.20

10

0.00

0

FY14

FY15

FY16

FY17E

FY18E

FY19E

FY14

FY15

FY16

FY17E

FY18E

FY19E

Source: Company, Angel Research

Source: Company, Angel Research

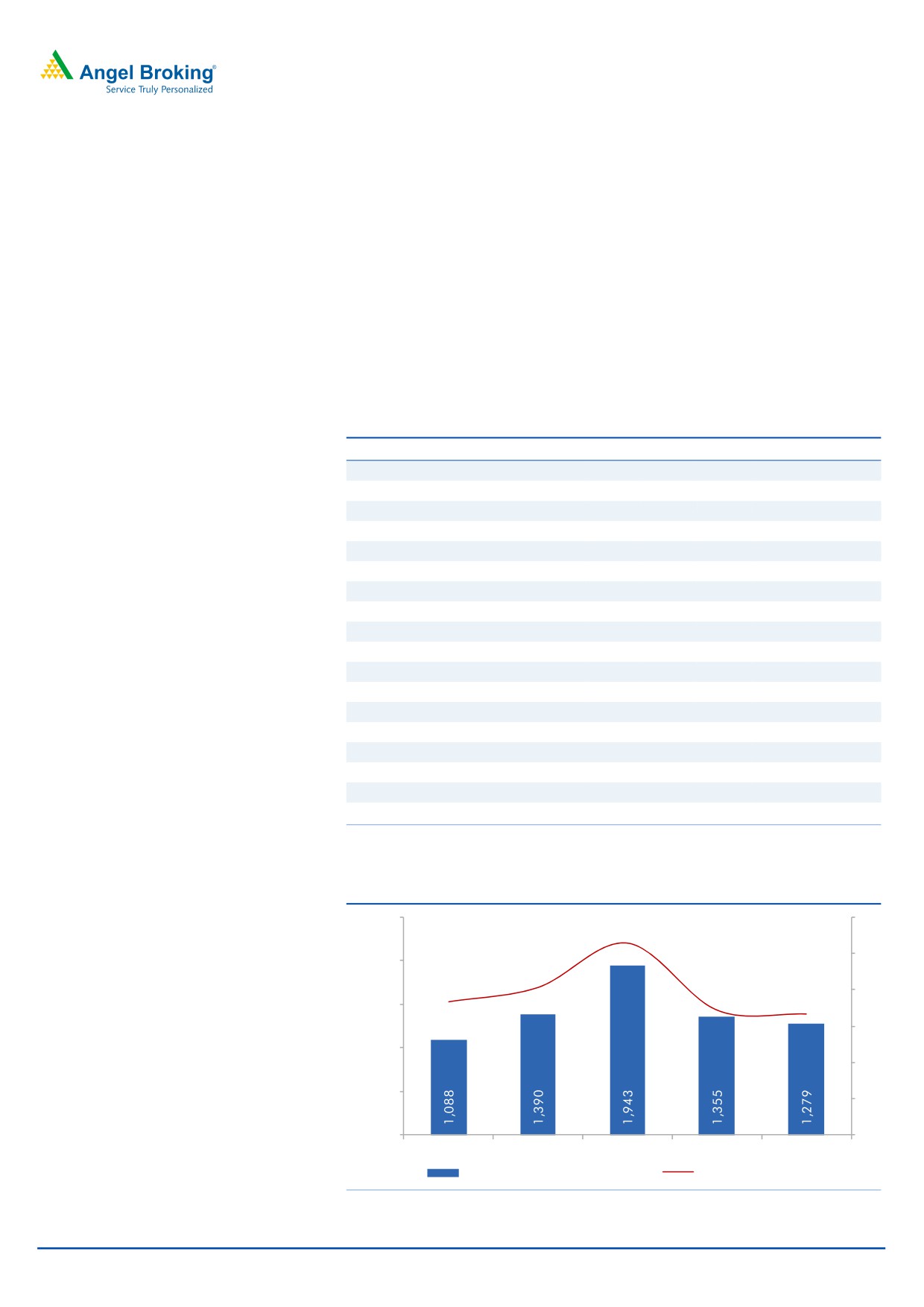

Large scale restructuring already over, incremental pain to be

minimal

KVB had to undertake a lot of restructuring in the sectors it had exposure to during

the last two years. Infrastructure and Textiles were the two large sectors where lot

of stress was witnessed by the bank. At the beginning of FY2016, the bank had an

outstanding restructured loan book of `1,943 cr, of which ~`692 cr (35% of total)

were downgraded to NPAs. Large part of this was from the commodity sector.

Accordingly, the outstanding restructured loan book had declined and it stood at

`1,279 cr (3.32% of the loan book) at the end of 3QFY2017. For KVB, large part

of the troubled assets has already been restructured and even the more

troublesome accounts have slipped into NPAs, hence we believe that incremental

stress in the form of restructuring could be minimal.

March 31, 2017

8

Karur Vysya Bank | Initiating Coverage

Large scale restructuring already over, incremental pain to be minimal

KVB had to undertake a lot of restructuring in the sectors it had exposure to during

the last two years. Infrastructure and Textiles were the two large sectors where lot

of stress was witnessed by the bank. At the beginning of FY2016, the bank had an

outstanding restructured loan book of `1,943 cr, of which ~`692 cr (35% of total)

were downgraded to NPAs. Large part of this was from the commodity sector.

Accordingly, the outstanding restructured loan book had declined and it stood at

`1,279 cr (3.32% of the loan book) at the end of 3QFY2017. For KVB, large part

of the troubled assets has already been restructured and even the more

troublesome accounts have slipped into NPAs, hence we believe that incremental

stress in the form of restructuring could be minimal.

Exhibit 19: Restructured Loan Book (` Cr)

Sector Wise Restructured Advances

FY13

FY14

FY15

FY16

Q3FY17

Infrastructure

606

599

890

807

752

Textiles

268

267

276

205

196

Food Processing

225

234

Agriculture

14

14

23

16

8

Iron & Steel

14

124

322

0

0

Real Estate

1

1

5

0

23

Others

186

386

426

102

66

Total Restructured Loans

1,088

1,390

1,943

1,355

1,279

% to Total Advances

3.66%

4.06%

5.29%

3.43%

3.32%

% to Total Restructured Advances

Infrastructure

55.7%

43.1%

45.8%

59.6%

58.8%

Textiles

24.6%

19.2%

14.2%

15.1%

15.3%

Food Processing

0.0%

0.0%

0.0%

16.6%

18.3%

Agriculture

1.3%

1.0%

1.2%

1.2%

0.6%

Iron & Steel

1.3%

8.9%

16.6%

0.0%

0.0%

Real Estate

0.1%

0.1%

0.3%

0.0%

1.8%

Others

17.1%

27.8%

21.9%

7.5%

5.2%

Total

100%

100%

100%

100%

100%

Source: Company, Angel Research

Exhibit 20: Restructured loan book (%)

2,500

6%

5.29%

5%

2,000

4.06%

3.43%

3.32%

3.66%

4%

1,500

3%

1,000

2%

500

1%

-

0%

FY13

FY14

FY15

FY16

Q3FY17

Total Restructured Loans (` cr)

% to Total Advances

Source: Company, Angel Research

March 31, 2017

9

Karur Vysya Bank | Initiating Coverage

Cost structure has come down in the last few years

Expanding the number of branches and ATMs on one hand and slowdown in

business on the other has impacted the cost structure of the bank, and hence, the

cost/income ratio of KVB has gone up. However, with maturing of new branches

and pick up in business in the existing branches, moderation in its cost/income

ratio is expected going ahead.

Exhibit 21: Cost to Income (%)

Exhibit 22: Cost to Assets (%)

60.0

3.00

2.60

2.54

57.5

2.50

58.0

57.0

2.50

2.26

2.06

2.11

55.4

56.0

54.7

2.00

53.9

54.0

1.50

52.0

50.3

1.00

50.0

0.50

48.0

46.0

0.00

FY14

FY15

FY16

FY17E

FY18E

FY19E

FY14

FY15

FY16

FY17E

FY18E

FY19E

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 23: Comparative Cost Structure

Cost / Income %

FY11

FY12

FY13

FY14

FY15

FY16

KVB

41.8

42.7

47.3

54.7

53.9

50.3

LVB

45.4

55.5

57.4

56.1

54.6

57.1

Federal Bank

36.9

39.4

44.7

47.6

50.0

56.7

City Union Bank

37.5

39.6

41.7

45.2

42.8

40.1

Karnataka Bank

60.7

52.7

51.2

56.0

53.9

53.7

DCB

71.4

74.4

68.7

62.9

58.8

58.4

South Indian Bank

46.8

48.7

47.5

50.0

56.2

56.6

Source: Company, Angel Research

Increasing share of low cost deposits and lower interest reversals

will ensure a healthy NIM going ahead

During the last quarter, the bank witnessed a drop in yield of assets coupled with a

sharp drop in the cost of funds. Backed by demonetization there was strong flow of

low cost deposits, and hence the reduction in cost. Though some part of the funds

could migrate to high cost term deposits, overall CASA could remain much

stronger than earlier for KVB, this together with lower interest reversal should help

in NIM remaining strong in the quarters to come.

March 31, 2017

10

Karur Vysya Bank | Initiating Coverage

Exhibit 24: NIM likely to see gradual upmove

4.00

3.44

3.50

3.21

3.28

3.23

2.80

3.00

2.61

2.50

2.00

1.50

1.00

0.50

0.00

FY14

FY15

FY16

FY17E

FY18E

FY19E

Source: Company, Angel Research

Return ratios hurt due to high credit cost, RoE to bounce back in

FY2018

Subdued growth in loan book on one hand and deteriorating asset quality on the

other dented the profitability of KVB in last few years. Operating expenses of the

bank grew at higher rate than the operating income, thus exerting pressure on the

cost structure of the bank. All these factors impacted the overall return ratios of the

bank, which saw a declining trend. However, over the medium term, with

moderating credit cost and cost structure, backed by better credit off take we

expect RoE to improve gradually.

Exhibit 25: ROA (%) to move up gradually

Exhibit 26: ROE to see steady improvement (%)

1.2

16.0

1.0

1.0

13.4

13.2

14.0

12.9

1.0

0.9

0.9

0.9

12.0

0.9

11.2

11.4

12.0

0.8

10.0

0.6

8.0

6.0

0.4

4.0

0.2

2.0

0.0

0.0

FY14

FY15

FY16

FY17E

FY18E

FY19E

FY14

FY15

FY16

FY17E

FY18E

FY19E

Source: Company, Angel Research;

Source: Company, Angel Research

March 31, 2017

11

Karur Vysya Bank | Initiating Coverage

In order to meet business growth capital needs to be raised

KVB has a relatively lower capital adequacy as compared to other south based

private sector banks. We feel that the bank will have to raise capital in the near

term in order to push higher growth. However, considering the bank’s strong track

record, we don’t see raising capital as a challenge for the bank.

Exhibit 27: Capital adequacy trend

16.0

14.6

13.6

14.0

12.6

12.2

12.0

11.7

11.8

11.9

11.3

11.3

12.0

11.0

11.1

10.0

8.0

6.0

4.0

2.0

0.0

FY14

FY15

FY16

FY17E

FY18E

FY19E

CAR (%) Tier I (%)

Source: Company, Angel Research

Exhibit 28: Comparative CAR (%) as on 31st Dec,2016

KVB

11.05

LVB

10.21

Federal Bank

12.28

City Union Bank

14.88

Karnataka Bank

13.19

DCB

13.33

South Indian Bank

11.05

Source: Company, Angel Research

March 31, 2017

12

Karur Vysya Bank | Initiating Coverage

Outlook and valuation

KVB’s earnings were impacted due to higher provisions and lower business growth,

however, we expect gradual recovery on both the fronts going ahead. While in

FY2018 we expect earnings recovery to be visible, sharp growth is expected in

FY2019. At the CMP the stock is trading at 1.1x it’s FY2019 BV. We have valued

the stock at 1.4x its FY2019E BV and recommend BUY with a Target Price of `140

over the next 12 months.

Exhibit 29: Comparative Valuation & Return ratio

P/BV

RoE%

RoA%

FY17E

FY18E

FY19E

FY17E

FY18E

FY19E

FY17E

FY18E

FY19E

KVB

1.3

1.2

1.1

11.2

11.4

13.2

0.9

0.9

1.0

LVB

1.6

1.4

1.3

11.2

12.7

15.2

0.7

0.7

0.9

Federal Bank

1.7

1.6

1.5

9.2

11.4

13.4

0.8

0.9

1.0

City Union Bank

2.6

2.3

2.0

15.1

15.7

16.4

1.5

1.5

1.6

Karnataka Bank

0.9

0.9

0.8

10.9

11.8

12.7

0.8

0.8

0.8

DCB

2.4

2.1

1.9

10.7

15.8

12.9

0.9

0.9

1.0

Source: Company, Angel Research, Note: CMP as of March 30, 2017, * other companies Consensus taken from Bloomberg,

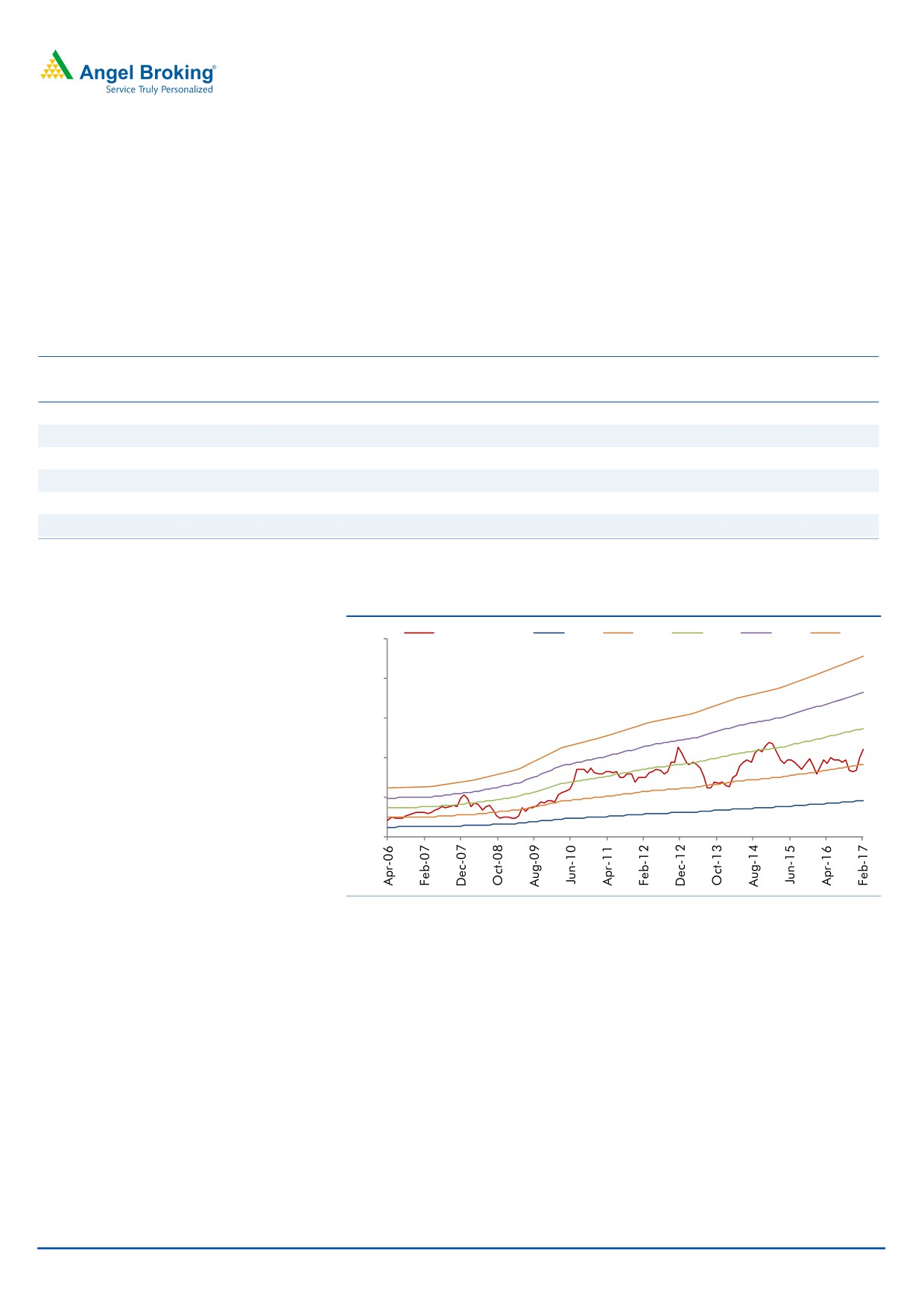

Exhibit 30: One Year Forward P/BV

Close -Unit Curr

0.5 X

1.0 X

1.5 X

2.0 X

2.5 X

250

200

150

100

50

0

Source: Company, Angel Research

March 31, 2017

13

Karur Vysya Bank | Initiating Coverage

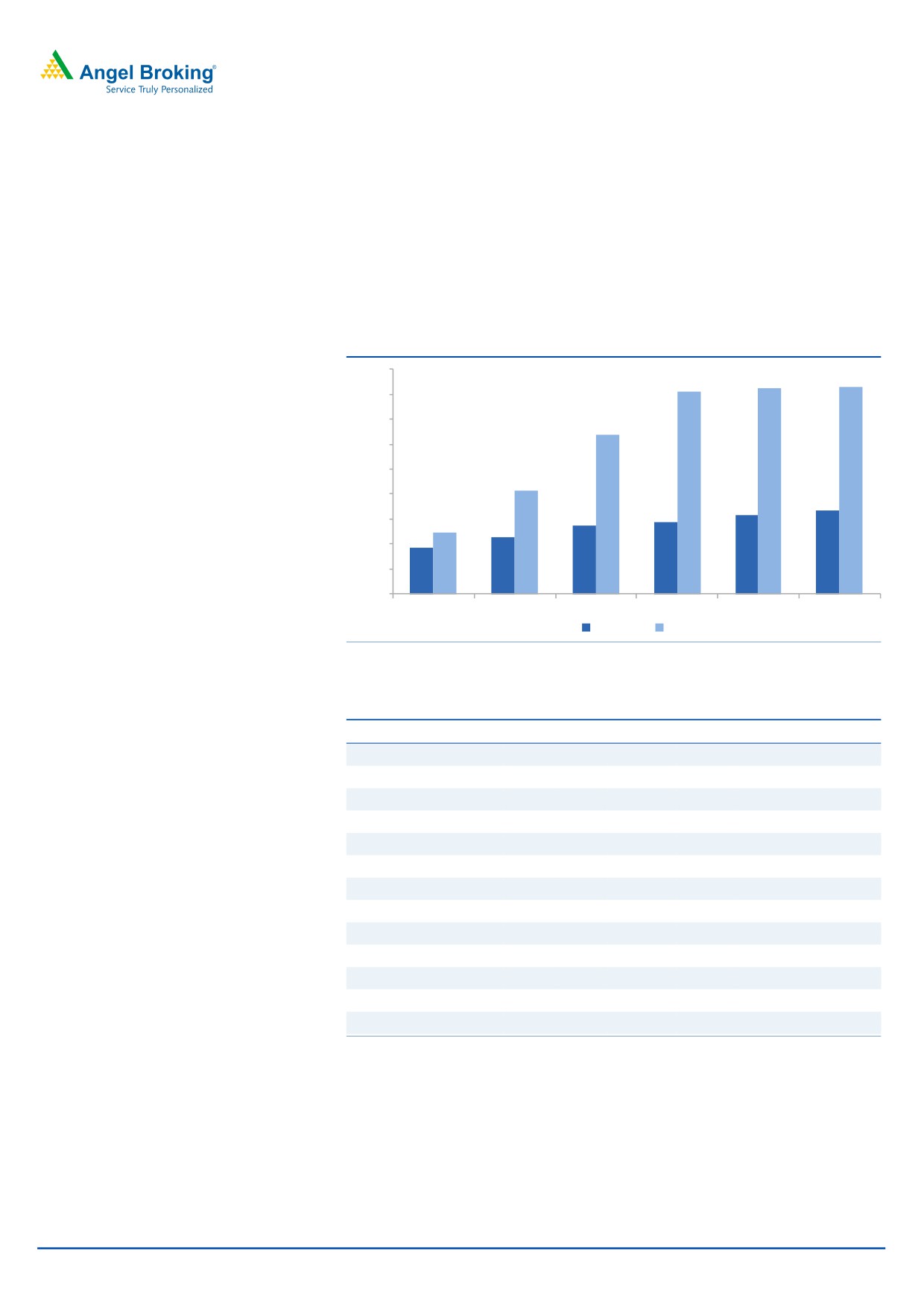

Company Background

Based out of Karur, Tamil Nadu, Karur Vysya Bank is one of the oldest private

sector banks in India. The bank has strong presence in its home state Tamil Nadu

and in other southern states of India. However, in the last few years the bank has

also been scaling up its operations in other states of India. At the end of

3QFY2017 the bank had a customer base of 6.09 million and operated through

706 branches and 1,711 ATMs.

Exhibit 31: Branch and ATM strength

1800

1,645

1,655

1,616

1600

1400

1,276

1200

1000

825

800

667

629

551

572

600

488

451

369

400

200

0

FY11

FY12

FY13

FY14

FY15

FY16

Branches

ATM

Source: Company, Angel Research

Exhibit 32: Comparative DuPont (FY2016)

KVB

LVB

Federal

CUB Karnataka

DCB

Interest Income

9.8

9.6

8.9

10.0

9.2

9.6

Interest Expenses

6.6

7.2

6.0

6.6

6.8

6.1

NII

3.2

2.4

2.9

3.3

2.4

3.5

Non Interest Income

1.3

1.1

0.9

1.4

1.0

1.3

Total Revenues

4.5

3.6

3.8

4.7

3.4

4.8

Operating Cost

2.3

2.0

2.1

1.9

1.8

2.8

PPP

2.2

1.5

1.6

2.8

1.6

2.0

Total Provisions

0.6

0.7

0.8

0.8

0.6

0.5

PreTax Profit

1.6

0.9

0.8

2.0

1.0

1.5

Tax

0.6

0.2

0.3

0.5

0.2

0.4

ROA

1.0

0.7

0.5

1.5

0.8

1.1

Leverage

12.6

16.1

10.8

10.3

15.3

10.4

RoE (%)

12.9

10.9

5.9

15.5

11.7

11.5

Source: Company, Angel Research

March 31, 2017

14

Karur Vysya Bank | Initiating Coverage

Income statement (Standalone)

Y/E March (` cr)

FY15

FY16

FY17E

FY18E

FY19E

Net Interest Income

1,466

1,781

2,010

2,182

2,532

- YoY Growth (%)

14.2

21.5

12.8

8.6

16.1

Other Income

581

707

761

783

848

- YoY Growth (%)

2.9

21.7

7.7

2.9

8.3

Operating Income

2,046

2,488

2,771

2,965

3,380

- YoY Growth (%)

10.7

21.6

11.4

7.0

14.0

Operating Expenses

1,103

1,253

1,592

1,691

1,874

- YoY Growth (%)

9.2

13.5

27.1

6.2

10.8

Pre - Provision Profit

943

1235

1179

1,274

1,506

- YoY Growth (%)

12.6

31.0

(4.6)

8.1

18.2

Prov. & Cont.

481

324

361

367

359

- YoY Growth (%)

8.6

(32.6)

11.6

1.6

(2.1)

Profit Before Tax

462

912

817

907

1147

- YoY Growth (%)

17.0

97.1

(10.3)

10.9

26.5

Prov. for Taxation

7

344

273

299

378

- as a % of PBT

1.6

37.7

33.3

33.0

33.0

PAT

455

568

545

608

768

- YoY Growth (%)

6

25

(4)

12

26

Balance sheet (Standalone)

Y/E March (` cr)

FY15

FY16

FY17E

FY18E

FY19E

Share Capital

122

122

122

122

122

Reserves & Surplus

4,124

4,451

4,997

5,426

6,002

Networth

4,246

4,573

5,119

5,548

6,124

Deposits

44,690

50,079

56,718

61,255

67,381

- Growth (%)

2.1

12.1

13.3

8.0

10.0

Borrowings

2,901

1,573

1,702

1,838

2,021

- Growth (%)

(11.9)

(45.8)

8.2

8.0

10.0

Other Liab & Prov.

1,315

1,439

1,418

1,531

1,685

Total Liabilities

53,152

57,664

64,956

70,173

77,211

Cash balances

2,693

2,529

2,836

3,063

3,369

Bank balances

56

263

1,134

613

674

Investments

12,773

13,222

15,881

17,152

18,867

Advances

36,109

39,084

40,382

44,420

49,751

- Growth (%)

6.2

8.2

3.3

10.0

12.0

Fixed Assets

411

420

462

496

546

Other Assets

1,110

2,146

4,261

4,430

4,005

Total Assets

53,152

57,664

64,956

70,173

77,211

March 31, 2017

15

Karur Vysya Bank | Initiating Coverage

Ratio analysis (Standalone)

Y/E March

FY15

FY16

FY17E

FY18E

FY19E

Profitability Ratios (%)

NIMs

2.8

3.2

3.3

3.2

3.4

Cost to Income Ratio

53.9

50.3

57.5

57.0

55.4

RoA

0.9

1.0

0.9

0.9

1.0

RoE

12.0

12.9

11.2

11.4

13.2

B/S ratios (%)

CASA Ratio

22.0

23.3

30.9

30.0

30.0

Credit/Deposit Ratio

80.8

78.0

71.2

72.5

73.8

CAR

14.6

12.2

11.8

11.9

12.0

- Tier I

13.6

11.3

11.0

11.1

11.3

Asset Quality (%)

Gross NPAs

1.9

1.3

2.7

3.2

3.1

Net NPAs

0.8

0.6

1.7

1.6

1.6

Slippages

1.8

3.1

2.5

2.0

1.5

Loan Loss Prov./Avg. Assets

1.3

0.8

0.9

0.8

0.7

Provision Coverage

59

58

40

50

50

Per Share Data (`)

EPS

7.5

9.3

8.9

10.0

12.6

BVPS

69.8

75.0

84.0

91.1

100.5

ABVPS

65.2

71.5

72.9

79.1

87.5

DPS

1.0

3.0

2.0

3.0

4.0

Valuation Ratios

PER (x)

14.7

11.8

12.3

11.0

8.7

P/BVPS(x)

1.6

1.5

1.3

1.2

1.1

P/ABVPS (x)

1.7

1.5

1.5

1.4

1.3

Dividend Yield

0.9

2.7

1.8

2.7

3.6

DuPont Analysis (%)

Interest Income

10.3

9.8

9.2

8.9

9.1

Interest Expenses

7.5

6.6

5.9

5.7

5.7

NII

2.8

3.2

3.3

3.2

3.4

Non Interest Income

1.1

1.3

1.2

1.2

1.2

Total Revenues

3.9

4.5

4.5

4.4

4.6

Operating Cost

2.1

2.3

2.6

2.5

2.5

PPP

1.8

2.2

1.9

1.9

2.0

Total Provisions

0.9

0.6

0.6

0.5

0.5

PreTax Profit

0.9

1.6

1.3

1.3

1.6

Tax

0.0

0.6

0.4

0.4

0.5

ROA

0.9

1.0

0.9

0.9

1.0

Leverage

13.8

12.6

12.7

12.7

12.6

RoE (%)

12.0

12.9

11.2

11.4

13.2

March 31, 2017

16

Karur Vysya Bank | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Karur Vysya Bank

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

March 31, 2017

17