Initiating coverage | Infrastructure

July 10, 2015

KNR Constructions

NEUTRAL

CMP

`593

Road laid for a sustainable drive….

Target Price

`582

Recent order inflows provide revenue growth visibility: KNR Constructions (KNR) is

Investment Period

12 Months

a specialist Roads & Highways EPC player. Over the last 4 months, KNR has

reported `2,591cr of order wins (excludes `555cr of Chittagong order win), which

Stock Info

is significantly higher than `950cr of order inflows in FY2015. Management has

Sector

Infrastructure

guided for another `750cr of order wins for remaining part of FY2016E. These

Market Cap (` cr)

1,668

order wins from the road vertical, take the 1QFY2016 unexecuted order book to

Net debt (` cr)

72

`3,356cr. This would result in order book / last twelve month (LTM) sales ratio at

Beta

1.3

1QFY2016 to be at 3.8x, which is higher than order book / LTM ratio of 1.2x at

52 Week High / Low

618/200

4QFY2015-end. With award momentum in road vertical to continue, we expect

KNR to report 5.4x growth in its order book to `5,450cr by FY2017E. Taking into

Avg. Daily Volume

8,722

account its past execution track record and average execution cycle of 24-36

Face Value (`)

10

months, we expect KNR to report strong top-line growth over FY2015-17E.

BSE Sensex

27,574

Nifty

8,329

New orders won amidst low competition: KNR has impressed us by prudently

Reuters Code

KNRL.BO

selecting projects, mainly in southern India, where it has strong foothold. Notably,

Bloomberg Code

KNRC@IN

recent order wins by KNR have come amidst low competition (2-3 bidders for

each project), when compared to higher competition witnessed across other NHAI

bids (5 to 8 bidders for each project). Recent order wins have been entirely from

Shareholding Pattern (%)

southern India (except the M.P. order which was won in Jul-2015), where KNR has

Promoters

65.5

aggregate mines as well as majority of its idly lying construction equipments. This

MF / Banks / Indian Fls

20.8

in our view would enable KNR to attain synergy in its operations and continue to

FII / NRIs / OCBs

0.9

post higher EBITDA margins.

Indian Public / Others

12.9

Comfortable Balance Sheet: KNR is one of the few Road EPC players with low D/E

ratio of 0.2x (FY2015), whereas peers are having D/E ratio of over 1.0x.

Abs. (%)

3m 1yr 3yr

Valuation: Improved order book outlook, strong earnings growth potential, and

comfortable Balance Sheet, strengthen our view that KNR would continue to trade

Sensex

(4.5)

8.7

58.5

at rich valuations. Announcement of recent order wins, have supported the KNR’s

KNR

30.3

152.1

380.7

stock price run up, which is up 30% in last 3 months. On valuing the standalone

entity at 14.0x our FY2017E EPS of `37, and adding up free cash flow to equity

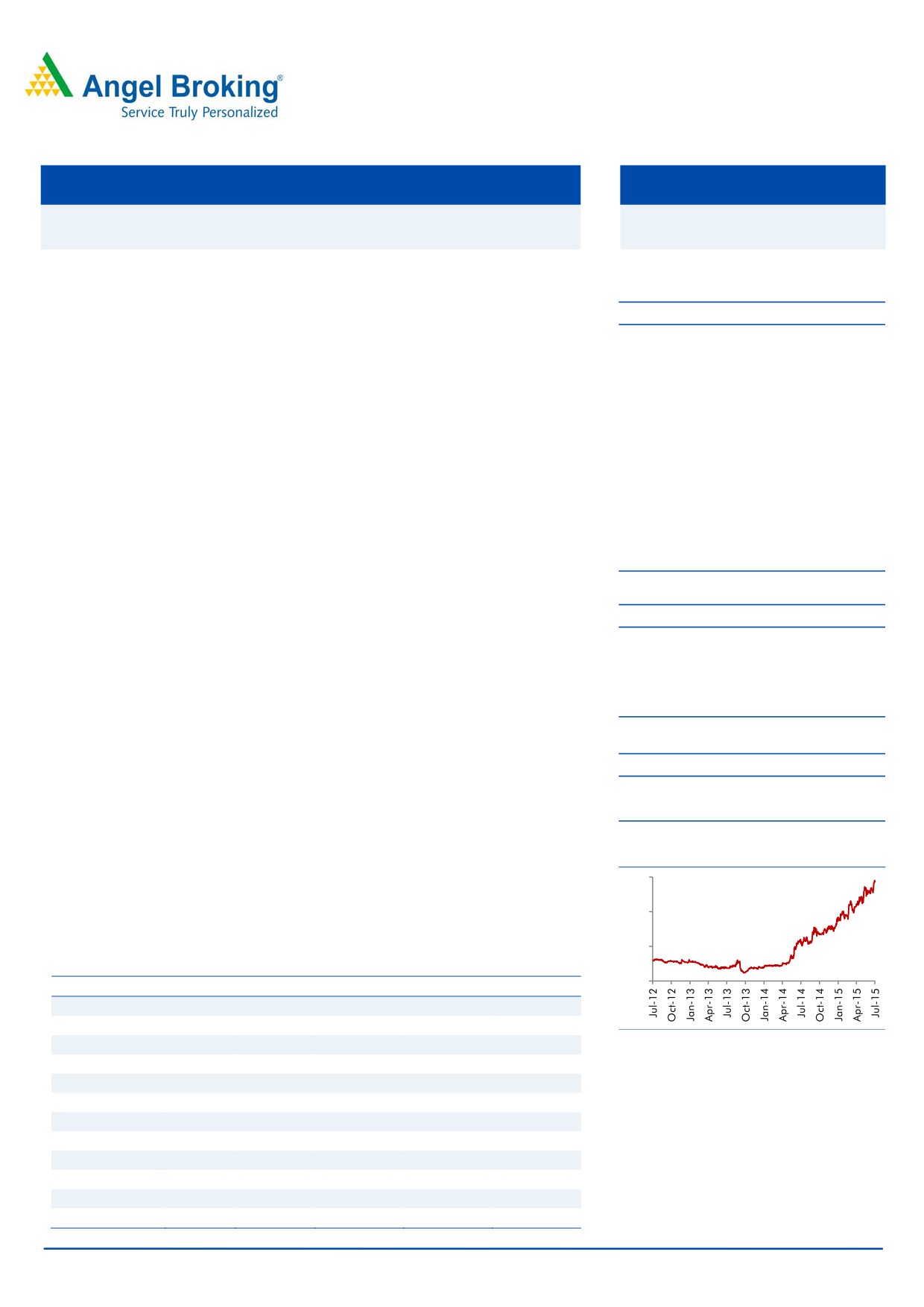

3 year price chart

shareholders value for its Kerala based BOT project, we arrive at FY2017E sum-

600

of-the-parts (SoTP) based price target of `582/share, implying that the KNR stock

400

is close to its fair value. We initiate coverage on KNR Constructions with a Neutral

rating, given that all the positives have been captured in the stock price.

200

Key Financials (Standalone)

0

Y/E March (` cr)

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Net Sales

689

837

876

915

1,479

% chg

(8.1)

21.5

4.7

4.5

61.6

Net Profit

52

61

73

57

105

Source: Company, Angel Research

% chg

(1.2)

17.0

19.7

(21.7)

82.9

EBITDA (%)

16.4

15.3

14.4

14.3

13.9

EPS (`)

18.5

21.7

26.0

20.3

37.2

P/E (x)

32.0

27.4

22.8

29.2

15.9

P/BV (x)

3.7

3.2

2.9

2.7

2.3

RoE (%)

12.1

12.6

13.5

9.6

15.6

RoCE (%)

16.0

15.4

13.8

12.2

19.3

Yellapu Santosh

EV/Sales (x)

2.5

2.1

2.0

1.9

1.2

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

14.8

13.6

13.8

13.5

8.8

Source: Company, Angel Research; Note: CMP as of July 9, 2015

Please refer to important disclosures at the end of this report

1

Initiating coverage | KNR Constructions

Investment Argument

Government’s increased focus on Infra sector

In order to revive the economy, the government has been increasingly focusing on

the infrastructure sector, in recent times. Sub-sectors like Roads & Highways, Water

& Water Treatment, and Urban Infrastructure, have caught the government’s

attention as well.

The National Highways Authority of India (NHAI) spent ~`21,000cr in FY2015.

NHAI has set an ambitious target of spending ~`75,000cr in FY2016 (a 3-fold

increase). Of the incremental NHAI spending, ~`55,000cr would be funded

through higher budgetary allocation (~`15,000cr) and borrowings (~`40,000cr).

Also, Ministry of Road Transport & Highways (MoRTH) has set an ambitious target

to award ~12,000km (including NHAI’s target of ~9,000km) of road projects in

FY2016 itself. Again, three-fourths of these projects, expected to be awarded in

FY2016, are engineering, procurement & construction (EPC) projects. On the back

of sharp revival in EPC Road award activity, we expect Road EPC players, including

KNR, to benefit. Recent order wins by KNR further strengthen our view that the

company is well positioned to continue reporting order inflows, going forward.

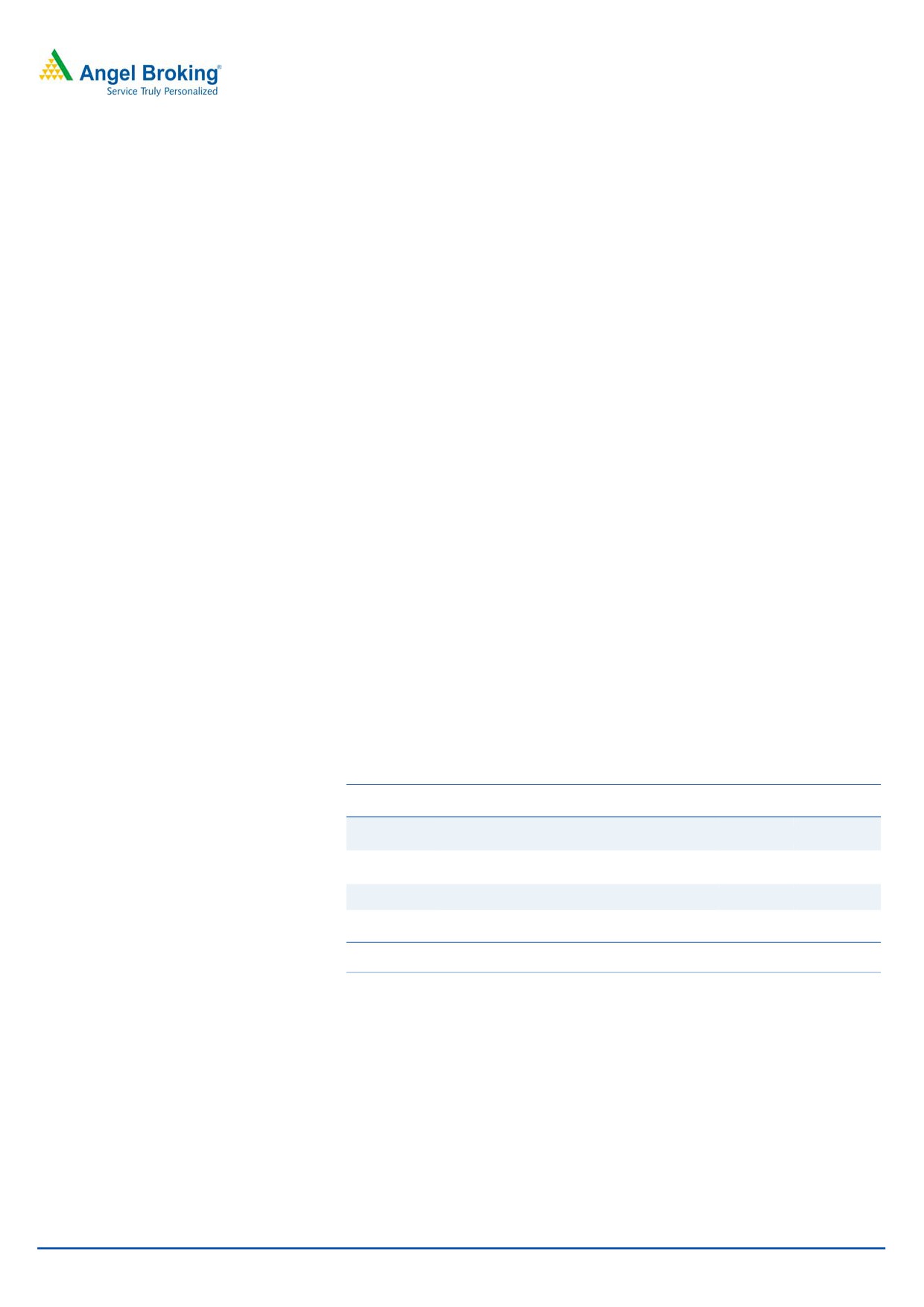

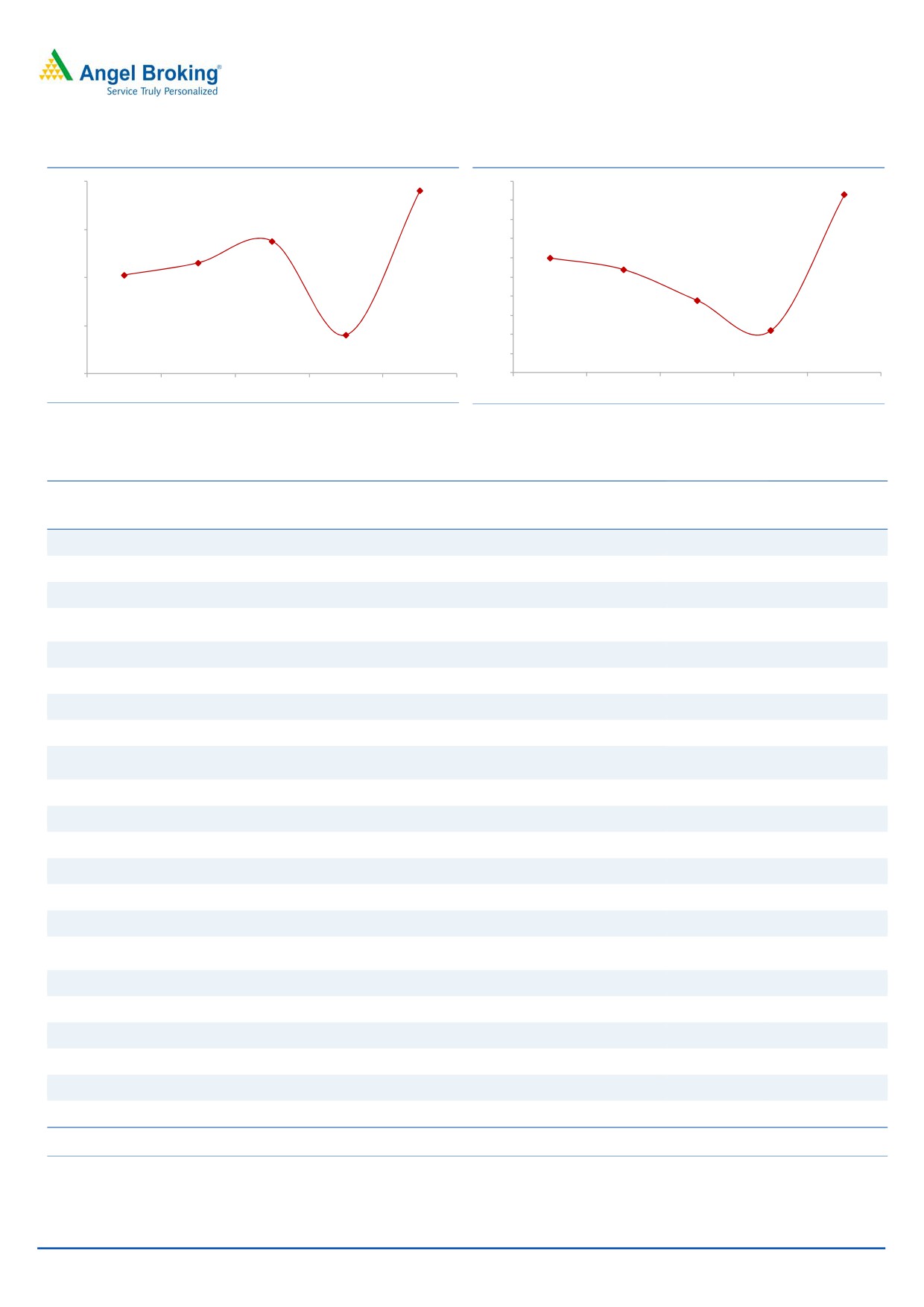

Order Book grows 3.3x, gives better revenue visibility….

KNR, in the last 4 months, has announced large ticket project wins mainly from the

Roads & Highways EPC space. To-date in FY2016, KNR reported `2,591cr worth

of project wins (excludes `515cr Chittagong Ring Road project), thereby taking the

order backlog at 1QFY2015E to `3,356cr (vs `1,010cr in 4QFY2015), which gives

better revenue visibility for FY2016-17E. The order book of the company in the last

1 quarter has grown by 3.3x, which is impressive.

Exhibit 1: Details of recently won EPC Road projects

Announced

Project Value

Project Details

Stake (%)

On

(` cr)

Upgradation of 3 road stretches across Tamil

13-Apr-15

100%

729

Nadu

2/4 laning of the Madurai- Ramanathapuram

17-Apr-15

100%

937

section (115 kms, NH-49)

14-May-15

4-laning of Kazhakkottam-Mukkola (NH-47)

100%

669

Widen/ Reconstruct 3 road stretches across

8-Jul-15

100%

256

different locations within Madhya Pradesh

Total

2,591

Source: Company, Angel Research

NHAI is expected to award ~20,000km of road projects during FY2016-18E. Of

this, the target for FY2016E is of ~9,000km (~3,000km of EPC+~2,000km of

BOT+~4,000km of Hybrid). KNR’s Management has highlighted that it intends to

bid only for Road EPC projects. Also, the Management has set its sight on 25-30

EPC Road tenders worth `14,000-16,000cr, which are likely to be up for bids, in

few months time from now. In line with the Management’s expectation, we are

optimistic that KNR would report order wins of ~`750cr in the remaining part of

FY2016E. We expect KNR’s order inflow growth momentum to continue going

forward. In FY2017E, we expect KNR to report `3,500cr worth of project wins

across verticals.

July 10, 2015

2

Initiating coverage | KNR Constructions

Accordingly we expect the order book to report 132.3% CAGR during FY2015-

17E. KNR’s unexecuted order book stands at `3,356cr, which gives revenue

visibility for 24+ months.

Exhibit 2: Order Inflow to gain pace...

Exhibit 3: Execution to pick-up, as order book grows...

4,000

6,000

1.0x

3,500

0.9x

0.9x

5,000

0.8x

3,000

0.7x

2,500

4,000

0.7x

0.6x

2,000

3,000

0.5x

0.5x

1,500

0.4x

0.4x

0.4x

2,000

0.3x

1,000

0.3x

0.2x

500

0.2x

1,000

0.1x

0

FY11

FY12

FY13

FY14

FY15

FY16E FY17E

0

0.0x

(500)

FY11

FY12

FY13

FY14

FY15

FY16E FY17E

(1,000)

OB (` cr)

Execution Rate (x)

Source: Company, Angel Research

Source: Company, Angel Research

KNR to report good set of EBITDA margins…

We remain impressed by KNR, given its strategy to prudently select projects, mainly

in southern India, where it has strong foothold. Notably, recent order wins by KNR

have come amidst low competition (2-3 bidders for each project), when compared

to higher competition witnessed across other NHAI bids (5 to 8 bidders seen across

projects). Recent order wins have been entirely from southern India (except the

M.P. order which was won in Jul-2015), where KNR has aggregate mines as well

as majority of its idly lying construction equipments. This would enable KNR to

attain synergy in its operations and continue to post higher EBITDA margins.

Exhibit 4: 15.9% Avg. EBITDA % during FY2011-15

Exhibit 5: Peers’ margins below KNR’s...

20.0

20.0

17.1

16.1

18.0

Avg. EBITDA Margins (FY2011-15)- 15.9

14.7

15.0

13.4

10.7

16.0

12.1

12.4

12.0

10.9

14.0

9.7

8.7

9.3

10.0

12.0

10.0

4.0

8.0

5.0

6.0

0.2

4.0

0.0

FY11

FY12

FY13

FY14

FY15

2.0

15.3

17.8

16.8

15.1

14.4

14.4

13.9

(2.1)

0.0

(5.0)

FY11

FY12

FY13

FY14

FY15

FY16E

FY17E

MBL Ahluwalia

J Kumar

Source: Company, Angel Research

Source: Company, Angel Research

KNR, during FY2011-15, reported EBITDA margin in the range of 14.4-17.8%

(average of 15.9%). Except for J Kumar’s FY2014 and FY2015 EBITDA margins,

KNR’s margins during FY2011-15 have been ahead of the industry peers (MBL

Infrastructures, Ahluwalia Contracts and J Kumar). In our view, (1) higher asset

turnover ratio (vs. industry peers), (2) acquisition of aggregate mines closer to

projects under execution, (3) receipt of early completion bonus for some of the

projects, and (4) minimal dependency on sub-contracting, helped the company

report over 14% EBITDA margins during FY2011-15.

July 10, 2015

3

Initiating coverage | KNR Constructions

Exhibit 6: Construction & Mining Equip. Portfolio...

Exhibit 7: Projects completed ahead of schedule...

(As of 4QFY2015)

Qty.

Sch. Time

Act. Comp

Tippers

531

Bijapur-Hungund

910

582

Excavators

125

Hyderabad-Ramagundam

1,440

1,219

Compactors

60

Karimnagar-Kamareddy

450

343

Concrete Mixers & Pumps

45

Hyderabad-Chanda

365

364

Loaders

38

Siricilla-Siddipet

365

364

Pavers

33

Narsapur-Aswaraopet

365

364

Crushers

14

Source: Company, Angel Research

Graders

31

Tractors

31

Cranes

31

Tankers

28

Transit Mixers

24

Rollers

18

Batching & Mixing

21

Breakers

13

Hot Mix Plant

11

Drillers

12

Dozers

9

Wet Mix Plant

9

Drum Mix Plant

7

Source: Company, Angel Research

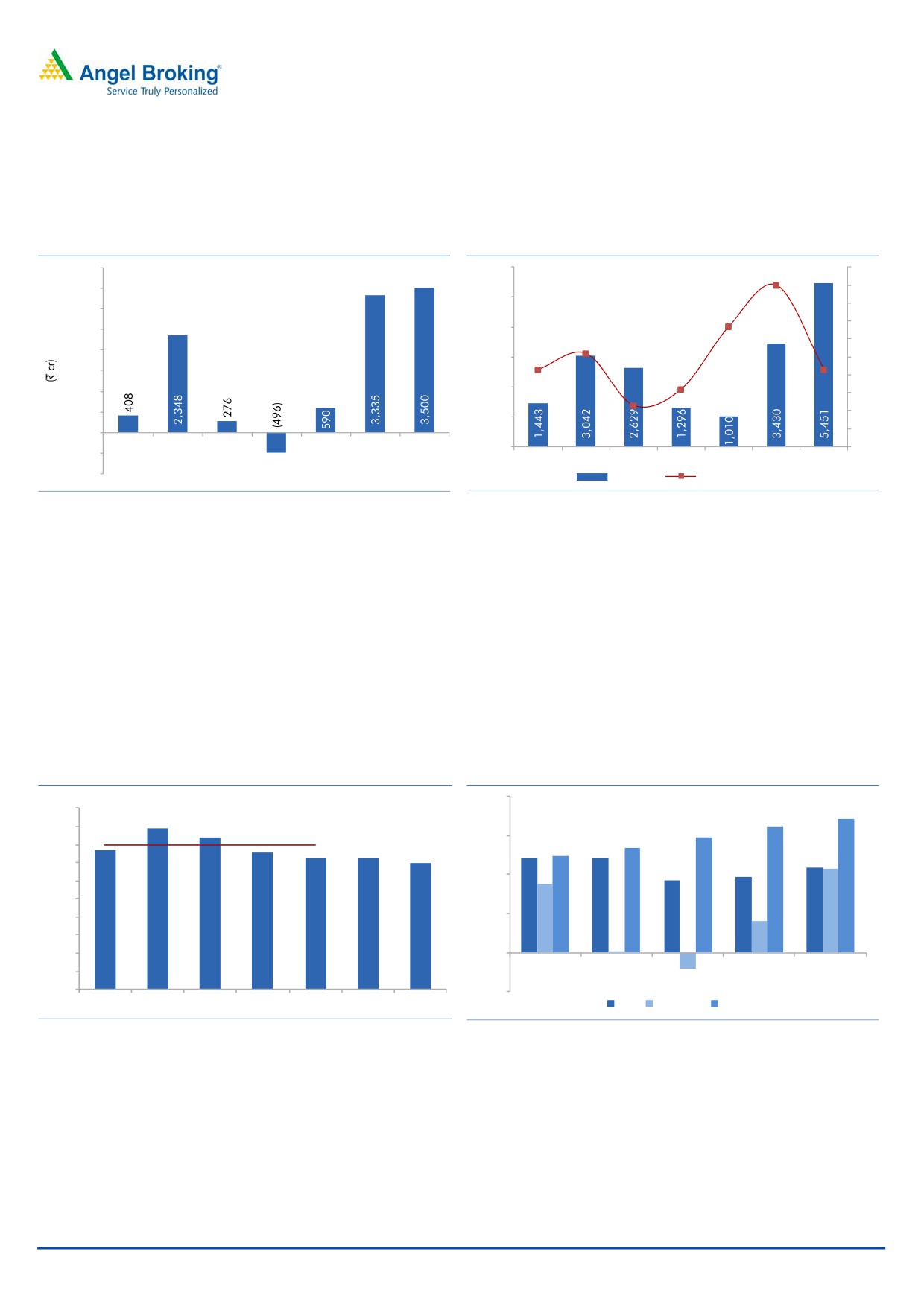

During FY2014-15, KNR invested in various types of construction equipments (P&M

gross block at FY2015-end stood at `448cr), this coupled with decline in yoy order

book, resulted in decline in equipment utilization to ~50% as of FY2015-end.

Despite such lower utilization, KNR’s asset turnover was at 1.6x, slightly below the

peers’ average of 1.7x.

Exhibit 8: Industry Peers’ Asset Turnover Ratio (x)

2.5

2.0

Average- 1.7x

1.5

1.0

0.5

1.0

1.9

2.1

1.6

0.0

MBL

Ahluwalia

J Kumar

KNR

Source: Company, Angel Research

These investments towards construction and mining equipments have helped KNR

become self sufficient, and build cushion against rising operating costs.

July 10, 2015

4

Initiating coverage | KNR Constructions

KNR has always focused on backward integration by sourcing aggregates from its

mines, for road projects under execution. Currently, KNR has 4 captive quarrying

mines, 14 crusher units (with daily crushing capacity of 15-20 lakh metric tonne)

and 21 Batching & Mixing plants, in close proximity to its projects under execution.

This helps KNR control its costs as sourcing of raw materials from captive quarrying

mines are 30-40% cheaper than those procured from open market. Also, KNR has

tie-ups with BPCL, HPCL, IOC, and MRPL to source bitumen, which is a core

consumable in a Road project.

KNR currently prefers to use more of its resources and depend lesser on sub-

contracting for getting a given project executed. Management indicated that given

the recent large ticket project wins, it would be left with no option but to increase its

dependency on sub-contracting works. For the outstanding order book, KNR would

incur ~`500cr worth of sub-contracting expenses (excluding the recently won MP

order, where KNR intends to depend majorly on sub-contracting).

Also, over the years, KNR has built a strong execution track record. The above

table (Exhibit 7) clearly highlights that a few of the projects have been completed

ahead of schedule, thereby making KNR eligible for early completion bonus.

Considering all the above mentioned levers, shift in strategies, when coupled with

our assumption that KNR may not receive any early completion bonus for projects,

we estimate 14.4% and 13.9% EBITDA margins for FY2016E and FY2017E,

respectively.

30% & 20% Revenue & PAT CAGR, respectively, during FY15-17E

KNR reported 2.3% top-line CAGR during FY2011-14, owing to weak order inflow

scenario. However, with uptick in award activity and recent order wins, coupled

with average execution cycle of ~24-36 months, we expect KNR to report a strong

30% revenue CAGR during FY2015-17E to `1,479cr.

During FY2011-15, KNR reported EBITDA margins in the range of 14.4%-17.8%

and PAT margins in the range of 7.0%-8.3%. Assuming (1) KNR would not get any

early completion bonus for its ongoing projects and (2) increase its dependency on

sub-contracting, we model 52bp EBITDA margin decline from 14.4% in FY2015 to

13.9% in FY2017E. Higher interest expenses (owing to stretch in working capital

cycle) and higher tax rate assumption (in FY2016-17E) would restrict the entire

benefits of EBITDA growth from flowing down to PAT level. Management clarified

that it is availing tax benefits u/s 80IA. We have assumed 15.0% and 21.0% tax

rate for FY2016E and FY2017E, respectively. As a result, we have estimated

restricted PAT CAGR of 20% over FY2015-17E to `105cr. PAT margins would

decline by 126bp to 7.1% in FY2017E.

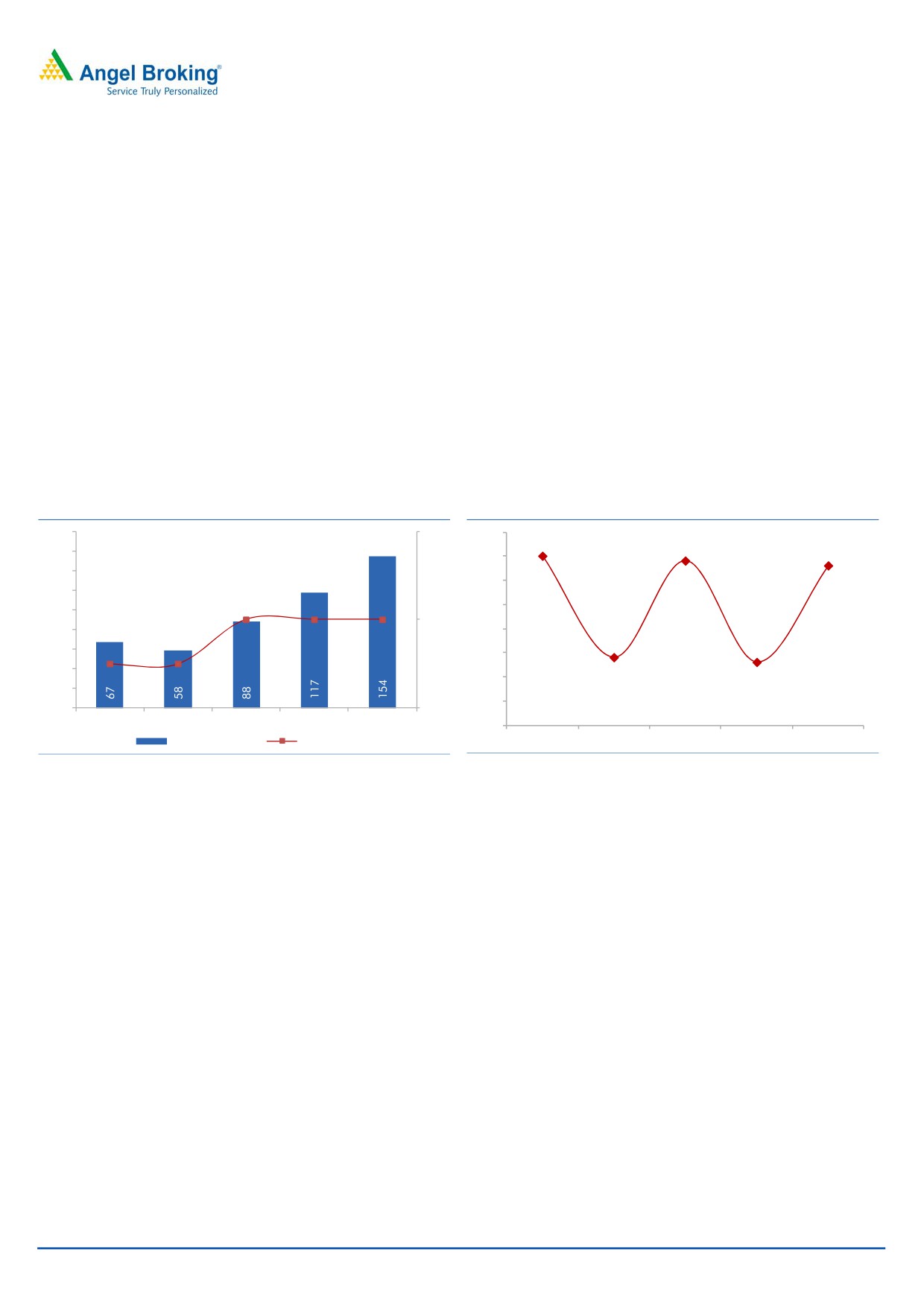

Comfortable Gearing ratio

KNR over the years has been prudently managing its overall capital requirements.

It has maintained lower D/E ratio (in the range of 0.1x-0.2x during FY2011-14E),

owing to (1) positive cash flow generation from operations (reported average cash

flows of `87cr during FY2011-14), and (2) shorter working capital cycle.

We sense that the company has been disciplined in maintaining attractive payment

terms with its suppliers, and has been prompt in collections from its clients. Picking

July 10, 2015

5

Initiating coverage | KNR Constructions

up large ticket projects from bigger players, which have all clearances in place, at

attractive margins, has helped the company report positive cash flows and shorter

working capital.

KNR is vying to enter the bigger league, where it intends to bid directly for State

PWDs and NHAI based road projects as against it earlier bidding for larger ticket

EPC road projects from larger construction players. This would result in the order

book mix shifting towards State PWDs and NHAI based road projects. On this

account, we now expect stretch in Receivables cycle (to increase from 74 days in

FY2015 to 99 days in FY2017E), which in turn should lead to stretch in the

working capital cycle. Accordingly, we expect the working capital days to increase

from 59 days in FY2015 to 80 days in FY2017E.

Considering strong profitability growth, despite stretch in the WC cycle, we expect

KNR to report positive cash flow from operations to the tune of `118cr during

FY2015-17E and maintain its D/E ratio at 0.2x by FY2017E.

Exhibit 9: Standalone Debt and D/E ratio

Exhibit 10: Standalone Interest Coverage ratio (x)

180

0.4x

7.5x

7.0x

6.9x

160

6.8x

7.0x

140

6.5x

120

6.0x

100

0.2x

0.2x

80

0.2x

0.2x

5.5x

4.9x

60

4.8x

5.0x

0.1x

0.1x

40

4.5x

20

4.0x

0

0.0x

FY13

FY14

FY15

FY16E

FY17E

3.5x

Std. Debt (` cr)

D/E ratio (x)

FY13

FY14

FY15

FY16E

FY17E

Source: Company, Angel Research

Source: Company, Angel Research

Prudent BOT bidding, Kerala BOT to commence in FY2016E

KNR is one of the few listed players in the infra space, which has stayed away from

the BOT space. It started a few years ago with 2 BOT Annuity projects as minority

partner (40% stake) in a JV (partnering Patel Engineering). On commencement of

Annuity receipts, KNR, along with its JV partner, went ahead and raised `900cr as

securitization proceeds, thereby almost freeing its equity from these 2 projects.

KNR, during the down-cycle, pursued 1 BOT project in order to maintain its

business. In FY2013, KNR won its first 100% BOT-Toll project across the 54km

Walayar-Vadakkancheery stretch (in Kerala). KNR is expected to finish EPC works

by Sep-2015 (vs scheduled completion date in Dec-2015). This project is already

partially operational, with tolling across entire stretch to start in 2HFY2016E.

At the backdrop of recent order wins, Management indicated that the company is

not interested in adding any further BOT projects to its portfolio, unless the BOT

project conservatively generates internal threshold IRR of 18-20%.

July 10, 2015

6

Initiating coverage | KNR Constructions

Update on BOT Projects

KNR has a portfolio of 3 BOT Road projects, with 2 of them operational and the

3rd being partially operational (to be fully operational by Sep-15).

Exhibit 11: Details of the 3 BOT Projects

Particulars

PKIL

PKHIL

KNRWTPL

Islamnagar-

Stretch

AP/Karnataka border-Avathi

Walayar-Vadakkancheery

Nagpur-Hyderabad section

Project Type

BOT- Annuity

BOT- Annuity

BOT- Toll

State

Karnataka

Telangana

Kerala

Length (kms)

60

53

54

Status

Operational

Operational

Partly Operational

Concession Period

20 years

20 years

20 years

KNR's stake

40%

40%

100%

Concession Agreement Date

Apr-06

Mar-07

May-13

TPC (` in cr)

442

592

900

EPC (` in cr)

350

518

790

Debt (` in cr)

334

484

500

Equity (` in cr)

37

49

135

Grant (` in cr)

0

0

265

Traffic Growth Assumption:

1-5 years

NA

NA

7%

6-10 years

NA

NA

5%

10 years and there-after

NA

NA

0%

Source: Company, Angel Research; Note: NA- Not Applicable

Patel Infra led JV has securitized both the Annuity projects. As a result, we sense

that value for equity shareholders post securitization from these BOT projects is not

material, hence, we excluded these 2 BOT projects from our valuation exercise.

The 3rd BOT-Toll project across Walayar-Vadakkancheery is partly operational

(93% of EPC work is complete). The Management expects the remaining 7% of the

stretch to be complete by Sep-2015. KNR is currently doing `11lakh/day of tolling

vs the Management’s expectation of `14lakh/day (for the partly operating stretch).

Protests by locals, to address local infrastructure surrounding the road stretch,

disrupted operations for a few days and thereafter rains contributed to lower toll.

Post the rainy season, once the entire stretch gets operational, the Management

expects daily toll collection to catch-up and reach expected levels of ~`14lakh/day

(for already operational stretch). On a whole, once the entire road stretch gets fully

operational, we model `75cr of toll vs the Management’s guidance of `78cr for

FY2017E.

July 10, 2015

7

Initiating coverage | KNR Constructions

Outlook & Valuation

Outlook

KNR in our view enjoys (1) strong execution track record, (2) better cost structure

(reflected in the form of better EBITDA & PAT margins in comparison to its peers),

(3) shorter working capital cycle, (4) low leverage (since FY2011, D/E ratio has

been ~0.2x), (5) ability to generate positive cash flow from operations (generated

avg. cash flow from operations to the tune of `87cr during FY2011-14), and

(6) superior RoEs (12.1-17.1% range during FY2011-14). All these indicators point

at KNR’s superior earnings quality and strengthen our view that KNR would

continue to trade at rich valuations.

For valuation purposes, we have valued KNR using Sum-Of-The-Parts method.

KNR’s EPC business (standalone entity) is valued at FY2017E P/E multiple, whereas

only 1 of the 3 BOT projects has been valued using “Free Cash flow to Equity

holders” method. We have excluded 2 Annuity BOT projects, where KNR has 40%

stake in the JVs with Patel Engineering, as both these projects are securitized.

Value of Core EPC business

Considering (1) 3.3x order backlog of `3,356cr (at 1QFY2016-end), which gives

revenue visibility for 24+ months, (2) strong balance sheet (FY2015 D/E at 0.2x),

(3) strong 20% earnings CAGR during FY2015-17E, and (4) RoE expansion

scenario (from 13.5% in FY2015 to 15.6% by FY2017E), we assign 14.0x P/E

multiple to our FY2017E EPS estimate of `37/share, arrive at standalone business

value of `521/share.

Exhibit 12: Sum-of-the-Parts based Valuation Table

FY17E Std. PAT

Target

Target Value

Value/ share

% of

Particulars

Segment

Basis

(` cr)

Multiple

(` cr)

(`)

SoTP

KNR's EPC business

Construction

105

14.0

1,464

521

90

P/E of 14x

Total

105

1,464

521

90

Disounted FCFE

Project

Adj. FCFE

Value/ share

% of

Particulars

Proj. Type

Basis

(` cr)

Stake

Value (` cr)

(`)

SoTP

Road BOT projects

Walayar-Vadakkancheery BOT Proj.

Toll

171

100%

171

61

10

Ke of 16%

Total

171

171

61

10

Grand Total

1,800

582

100

Upside/ (Downside)

(2%)

CMP

593

Source: Company, Angel Research

July 10, 2015

8

Initiating coverage | KNR Constructions

Value of BOT projects

BOT projects have been valued using “Free Cash flow to Equity holders” method.

The Walayar-Vadakkancheery BOT Project is partly operational and expected to be

fully operational by Sep-2015. We have valued this BOT projects using 16%

discounting rate to arrive at FCFE per share value of `61/share (10% of SOTP

value of the company).

Business Value

On combining the value of EPC business and BOT projects, we arrive at a

combined business value of `582/share, reflecting all positives being captured in

the stock price. We initiate coverage on KNR Constructions with a Neutral rating

and price target of `582/share.

Risks to our Estimates

Any change in KNR’s taxation policy or adverse ruling by Tax department could act

as risk to our TP and rating.

KNR is highly dependent on roads vertical (accounts for ~95% of the order book).

Delays in award activity, unfavorable changes in the policy framework, could affect

our outlook on KNR.

Delays in execution (vs our estimates) could be a risk to our rating.

July 10, 2015

9

Initiating coverage | KNR Constructions

Company Overview

About the company

KNR is a Hyderabad based 20+ year old company having executed ~5,888kms

of road projects across 12+ states in India. Over the years, KNR has executed

Roads & Highways, Irrigation, and Bridges & Flyover projects. KNR also has a

quarrying division, which ensures timely supply of stone aggregates at project

locations. KNR over the years has evolved from a smaller sized Roads & Highways-

Engineering Procurement and Construction (EPC) player to a large one by

executing projects timely and building its qualification criterion. As of now, KNR

has executed projects for a diversified range of clients namely, NHAI, KSHIP,

MPRDCL, UPSHA, EIL, Sadbhav Engineering and GMR, amongst others.

In addition to the EPC business, KNR has 3 Build Operate Transfer (BOT) projects

in its kitty, with 2 of them operational and the 3rd one partly operational (to be fully

operational by Sep-15).

As of 1QFY2015-end, KNR had an order book of ~`3,356cr, which gives revenue

visibility for 24+ months. The Roads & Highways vertical accounts for ~95% of the

order book. The order book is currently being executed across 7 states.

Employees

KNR has strength of 700+ employees, led by proven Management team. Majorly,

150+ of them are experienced engineers; ~250 are equipment operators and

~175 Admin and Office staff.

The company follows a lean team structure while executing its projects across

different locations, thereby leading to quicker decision making and execution. This

can be seen from their better margin profile.

Exhibit 13: Employee Split (functionality-wise)

Project Eng., 13%

Admin. & Office

Site Supervision,

staff, 25%

5%

Site Engineers,

22%

Equipment

Operators, 35%

Source: Company, Angel Research

July 10, 2015

10

Initiating coverage | KNR Constructions

Exhibits

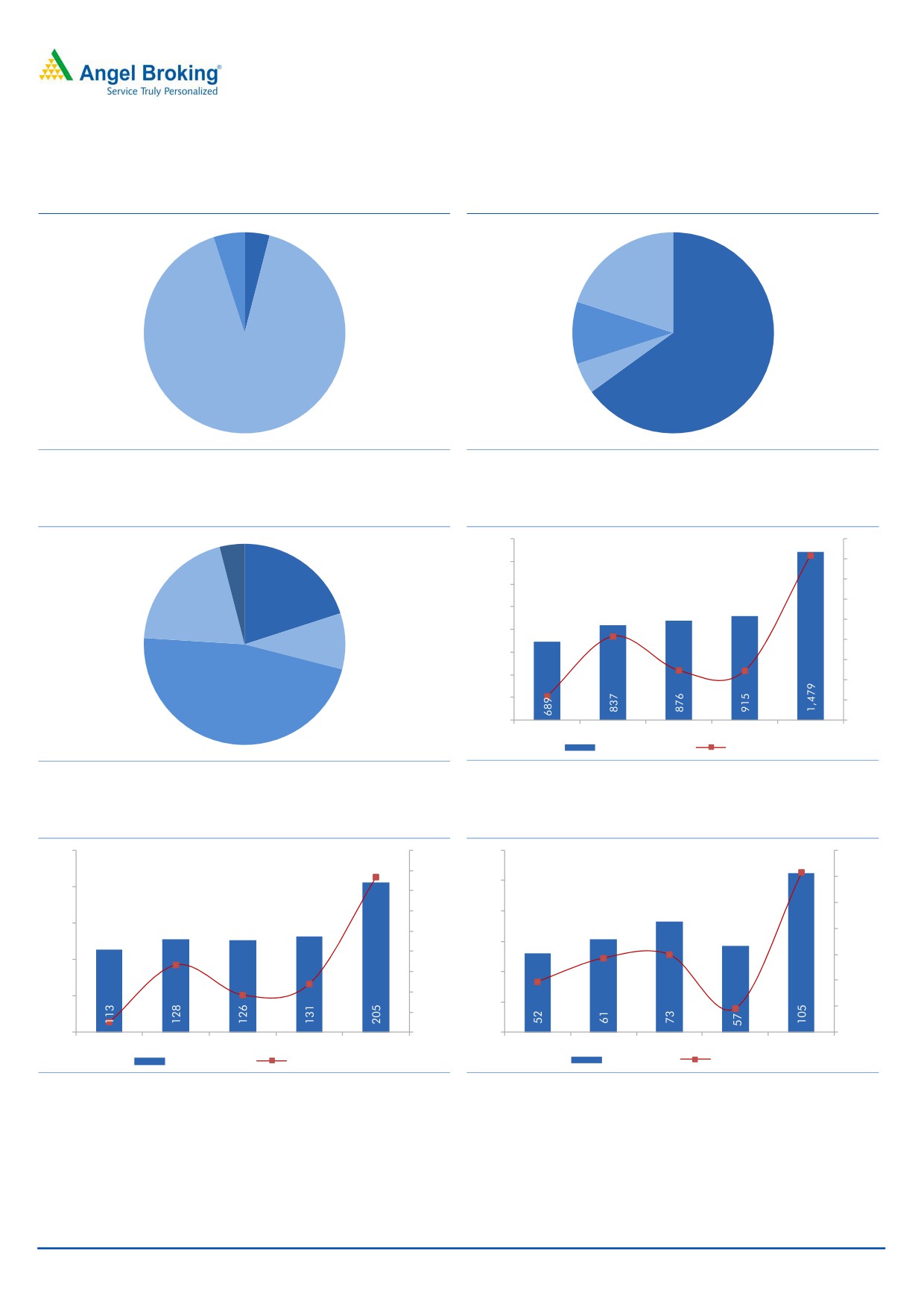

Exhibit 14: Order Book split- Vertical-wise

Exhibit 15: Order Book split- Region-wise

Roads &

Irrigation,

5%

Highways

(non-Captive),

4%

International,

20%

North, 10%

South, 65%

Roads &

Highways

East, 5%

(Captive), 91%

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 16: Order Book split- Client-wise

Exhibit 17: 30% Revenue CAGR during FY2015-17E

1,600

70

Captive, 4%

61.6

1,400

60

50

1,200

Central Govt.,

40

International,

20%

1,000

20%

30

800

21.5

20

Pvt. Co's, 9%

600

10

4.7

4.5

400

0

(8.1)

State Govt.,

200

(10)

47%

0

(20)

FY13

FY14

FY15

FY16E

FY17E

Revenues (` cr)

yoy growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 18: 28% EBITDA CAGR during FY2015-17E

Exhibit 19: 20% PAT CAGR during FY2015-17E

250

70.0

120

100.0

82.9

56.7

60.0

80.0

100

200

50.0

60.0

40.0

80

150

30.0

40.0

60

20.0

19.7

20.0

100

13.3

17.0

10.0

40

3.9

(1.2)

0.0

(1.6)

50

0.0

20

(20.0)

(10.0)

(21.9)

(14.9)

0

(20.0)

0

(40.0)

FY13

FY14

FY15

FY16E

FY17E

FY13

FY14

FY15

FY16E

FY17E

EBITDA (` cr)

yoy growth (%)

PAT (` cr)

yoy growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

July 10, 2015

11

Initiating coverage | KNR Constructions

Exhibit 20: Return on Equity (%)

Exhibit 21: Return on Capital Employed (%)

16.0

15.6

20.0

19.3

19.0

18.0

14.0

13.5

17.0

16.0

12.6

12.1

16.0

15.4

12.0

15.0

13.8

14.0

13.0

12.2

9.6

10.0

12.0

11.0

8.0

10.0

FY13

FY14

FY15

FY16E

FY17E

FY13

FY14

FY15

FY16E

FY17E

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 22: List of Ongoing projects

KNR share-

Unexecuted

Project details

Contract Val.

Val. (` in cr)

(` in cr)

3 road stretches across M.P.

256

256

4-laning of Kazhakkottam-Mukkola (NH-47)

669

669

2/4 laning of Madurai-Ramanathapuram (NH-49)

937

937

Upgrade Kanchipuram-Vandavasi Road & Upgrade Sdras-Chengalpattu-

185

185

Kancheeepuram-Arakonam-Thiruthani Road (SH-116)

Upgrade Arcot Villupuram (SH-4)

320

320

Upgrade Malliyakarai-Rasipuram-Thiruchengode-Erode Road (SH-79)

224

224

Chittagong Outer Ring Road

0

0

RoB at Davanagere-Channagiri Road

40

40

2 Flyovers at Dr. Nanjappa Road & Chinnaswamy Road, along with

146

106

pedestrian subway at Gandhipuram Area

2-laning of Penchalakona-Yerpedu section (NH-565)

201

173

4-laning of Walayar-Vadakkancheery (NH-47)

848

83

2-laning of Gobuk-Mariyang-Sijhon Nallah

99

64

Upgrade Magadi-Koratgere (NH-48/SH-3)

126

66

RoB at Gadag bypass between Benkanakatti-Gadag stations on Hubli-Gadag section

23

22

Upgrade Shelvadi-Mundargi (Dharwad & Gadag Districts)

136

39

Construct bridge across Tungabhadra River between

35

18

Kadebagilu Bukkasagar, Koppal District

RoB at Ramdurga-Badami Road

29

29

Construct bridge between Bhagyanagar-Yatnatti Road, Koppal District

84

32

Shankarasamudaram Balancing Resorvoir

156

62

Construct ROB at Battala Bazaar, Warangal

28

21

DLRB construction across Manjeera River, Medak District

21

8

2 to 4 laning of East Coast Road, in Chennai

46

41

Total Order Book

5,339

3,512

Source: Company, Angel Research; Note: OB numbers are unadjusted for works executed during 1QFY2016

July 10, 2015

12

Initiating coverage | KNR Constructions

Profit and Loss Statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Net Sales

689

837

876

915

1,479

% Chg

(8.1)

21.5

4.7

4.5

61.6

Total Expenditure

576

709

750

784

1,274

Cost of Raw Materials Consumed

202

291

337

353

564

Sub-Contracting Expenses

274

282

260

290

489

Employee benefits Expense

30

35

38

38

55

Other Expenses

70

101

115

104

167

EBITDA

113

128

126

131

205

% Chg

(14.9)

13.3

(1.6)

3.9

56.7

EBIDTA %

16.4

15.3

14.4

14.4

13.9

Depreciation

56

57

54

57

62

EBIT

57

71

72

74

143

% Chg

(29.6)

23.5

1.7

2.2

94.6

Interest and Financial Charges

11

17

12

18

23

Other Income

21

13

13

12

12

PBT

67

67

72

67

132

Tax

15

6

(1)

10

28

% of PBT

22.2

8.8

(1.0)

15.0

21.0

PAT before Exceptional item

52

61

73

57

105

Exceptional item

0

0

0

0

0

PAT

52

61

73

57

105

% Chg

(1.2)

17.0

19.7

(21.7)

82.9

PAT %

7.6

7.3

8.3

6.2

7.1

Basic EPS

18.5

21.7

26.0

20.3

37.2

Diluted EPS

18.5

21.7

26.0

20.3

37.2

% Chg

(1.2)

16.9

19.8

(21.7)

82.9

July 10, 2015

13

Initiating coverage | KNR Constructions

Balance Sheet (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Sources of Funds

Equity Capital

28

28

28

28

28

Reserves Total

428

485

541

594

691

Networth

456

513

569

622

719

Total Debt

67

58

88

117

154

Other Long-term Liabilities

138

100

69

85

95

Deferred Tax Liability

0

0

0

0

0

Total Liabilities

661

671

726

823

968

Application of Funds

Gross Block

508

525

543

577

616

Accumulated Depreciation

218

262

316

373

435

Net Block

290

264

227

204

181

Capital WIP

4

0

0

0

0

Investments

48

40

32

85

89

Current Assets

Inventories

30

34

36

36

60

Sundry Debtors

121

117

177

221

401

Cash and Bank Balance

7

11

16

6

9

Loans & Advances

328

229

241

334

527

Current Liabilities

293

283

277

349

588

Net Current Assets

194

108

192

248

410

Other Assets

125

259

276

285

287

Total Assets

661

671

726

823

968

July 10, 2015

14

Initiating coverage | KNR Constructions

Cash Flow Statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15P

FY16E

FY17E

Profit before tax

67

67

72

67

132

Depreciation

56

57

54

57

62

Change in Working Capital

(106)

16

(98)

(58)

(149)

Interest & Financial Charges

11

16

12

22

36

Direct taxes paid

(27)

(24)

(22)

(24)

(46)

Cash Flow from Operations

1

133

18

65

35

(Inc)/ Dec in Fixed Assets

(38)

(25)

(16)

(28)

(37)

(Inc)/ Dec in Investments & Int. recd.

(20)

(55)

(9)

(55)

(4)

Cash Flow from Investing

(58)

(80)

(25)

(82)

(42)

Issue/ (Buy Back) of Equity

0

0

0

0

0

Inc./ (Dec.) in Loans

71

(32)

36

30

41

Dividend Paid (Incl. Tax)

(3)

(3)

(6)

(4)

(8)

Interest Expenses

(11)

(17)

(12)

(18)

(23)

Cash Flow from Financing

57

(52)

18

8

10

Inc./(Dec.) in Cash

(0)

1

12

(10)

3

Opening Cash balances

4

3

4

16

6

Closing Cash balances

3

4

16

6

9

July 10, 2015

15

Initiating coverage | KNR Constructions

Key Ratios

Y/E March

FY13

FY14

FY15

FY16E

FY17E

Valuation Ratio (x)

P/E (on FDEPS)

32.0

27.4

22.8

29.2

15.9

P/CEPS

15.5

14.1

13.1

14.6

10.0

Dividend yield (%)

0.0

0.0

0.0

0.0

0.0

EV/Sales

2.5

2.1

2.0

1.9

1.2

EV/EBITDA

14.8

13.6

13.8

13.5

8.8

EV / Total Assets

3.3

2.6

2.6

2.4

2.2

Per Share Data (`)

EPS (Basic)

18.5

21.7

26.0

20.3

37.2

EPS (fully diluted)

18.5

21.7

26.0

20.3

37.2

Cash EPS

38.3

42.0

45.2

40.7

59.2

DPS

1.0

1.0

1.7

1.3

2.4

Book Value

162

183

202

221

256

Returns (%)

RoCE (Pre-tax)

16.0

15.4

13.8

12.2

19.3

Angel RoIC (Pre-tax)

15.0

14.7

12.9

11.5

17.8

RoE

12.1

12.6

13.5

9.6

15.6

Turnover ratios (x)

Asset Turnover (Gross Block) (x)

1.4

1.6

1.6

1.6

2.5

Inventory / Sales (days)

16

15

15

15

15

Receivables (days)

64

51

74

88

99

Payables (days)

56

34

29

31

34

WC days

24

32

59

72

80

Leverage Ratios (x)

D/E ratio (x)

0.1

0.1

0.2

0.2

0.2

Interest Coverage Ratio (x)

7.0

4.9

6.9

4.8

6.8

July 10, 2015

16

Initiating coverage | KNR Constructions

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

KNR Constructions

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

July 10, 2015

17