2QFY2016 Result Update | Infrastructure

November 16, 2015

KNR Constructions

BUY

CMP

`580

Performance Highlights

Target Price

`673

Investment Period

12 Months

Quarterly highlights - Standalone

Y/E March (` cr)

2QFY16 1QFY16 2QFY15

% chg (yoy)

% chg (qoq)

Stock Info

Net sales

213

175

170

24.9

21.8

Sector

Infrastructure

EBITDA

35

28

30

15.6

24.6

Market Cap (` cr)

1,630

Adj. PAT

22

15

14

59.4

48.0

Net debt (` cr)

72

Source: Company, Angel Research

Beta

1.2

52 Week High / Low

625/274

KNR Constructions (KNR) reported strong set of 2QFY2016 numbers. On the

Avg. Daily Volume

3,229

top-line (standalone) front, it reported 24.9% yoy increase to `213cr (ahead of

Face Value (`)

10

our estimate of `189cr). EBITDA and PAT numbers were ahead of our estimate at

BSE Sensex

25,611

`35cr and `22cr, respectively (v/s our estimate of `27cr and `11cr, respectively).

Nifty

7,762

PAT numbers during the quarter benefitted from prior period tax refunds and

Reuters Code

KNRL.BO

interest on such tax refunds to the tune of `33cr. On adjusting for the same, Adj.

Bloomberg Code

KNRC@IN

PAT of KNR was at `22cr, reflecting an impressive 10.5% Adj. PAT margin.

Shareholding Pattern (%)

KNR’s order book as of 2QFY2016 stands at ~`3,665cr, which gives strong

Promoters

60.8

revenue visibility for over the next few quarters.

MF / Banks / Indian Fls

25.5

FII / NRIs / OCBs

1.7

Valuation: Improved order book, ramp-up in recently won projects, strong

Indian Public / Others

12.1

earnings growth potential, and comfortable Balance Sheet, strengthen our view

that KNR would continue to trade at rich valuations. On valuing the standalone

entity at 15.0x our FY2017E EPS of `38.6, and adding value for its Kerala &

Abs. (%)

3m 1yr 3yr

Sensex

(8.8)

(8.7)

38.6

Muzaffarpur BOT projects, we arrive at FY2017E sum-of-the-parts (SoTP) based

KNR

8.8

104.8

447.5

price target of `673/share, implying 16% upside from the current levels. Given

the upside in the stock, we upgrade our rating to Buy.

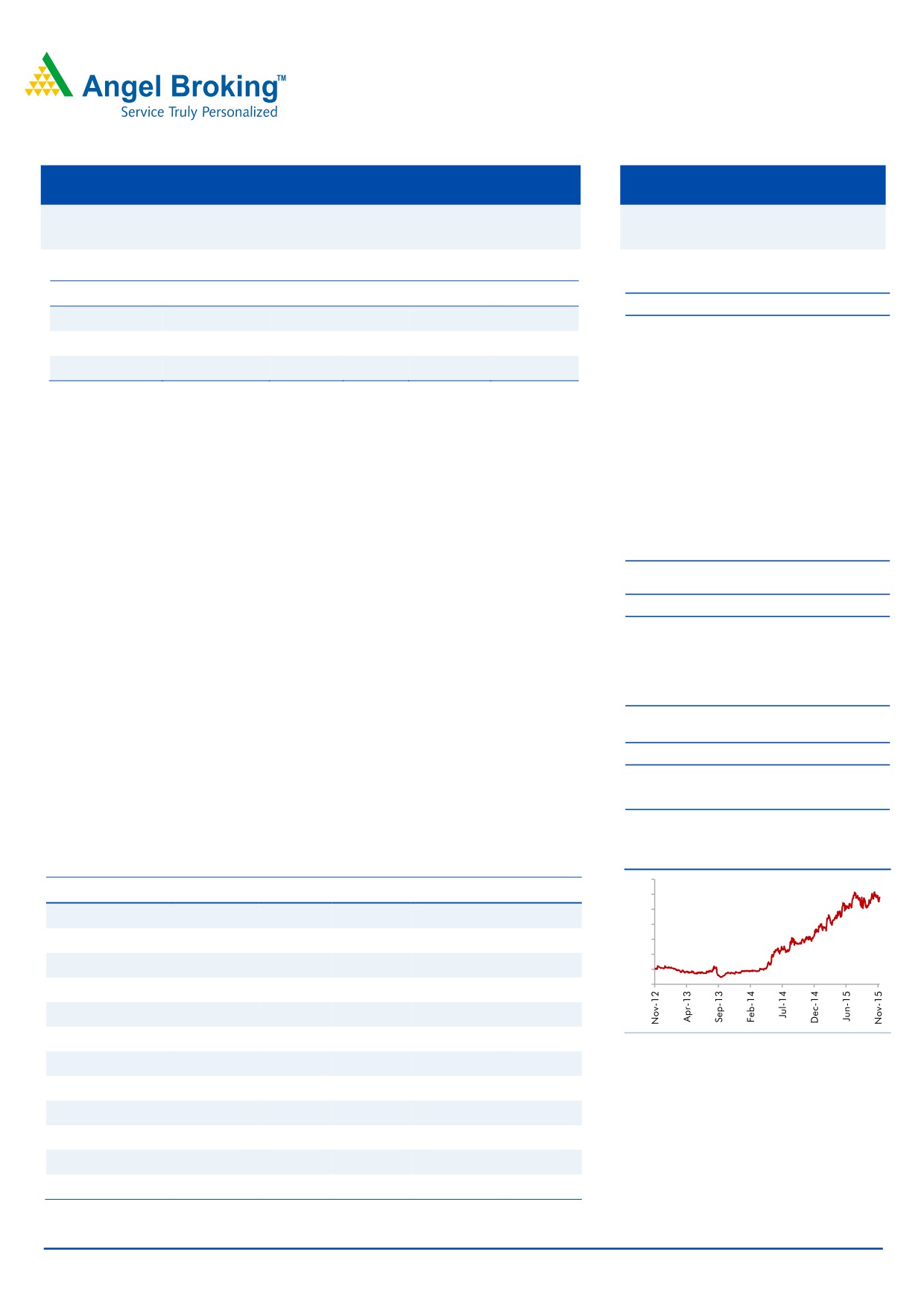

3-Year Daily Price Chart

Key financials (Standalone)

700

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

600

500

Net Sales

689

837

876

937

1,470

400

% chg

(8.1)

21.5

4.7

7.0

56.8

300

200

Net Profit

52

61

73

94

109

100

0

% chg

(1.2)

17.0

19.7

28.9

15.4

EBITDA (%)

16.4

15.3

14.4

14.3

14.0

EPS (`)

18.5

21.7

26.0

33.5

38.6

Source: Company, Angel Research

P/E (x)

31.3

26.7

22.3

17.3

15.0

P/BV (x)

3.6

3.2

2.9

2.5

2.2

RoE (%)

12.1

12.6

13.5

15.4

15.4

RoCE (%)

16.0

15.4

13.8

13.8

19.1

EV/Sales (x)

2.4

2.0

1.9

1.8

1.2

Yellapu Santosh

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

14.5

13.3

13.5

12.6

8.4

Source: Company, Angel Research; CMP as of November 13, 2015

Please refer to important disclosures at the end of this report

1

KNR Constructions | 2QFY2016 Result Update

Exhibit 1: Quarterly Performance (Standalone)

Particulars (` cr)

2QFY16

1QFY16

% chg (qoq) 2QFY15

% chg (yoy) 1HFY16 1HFY15

% chg (yoy)

Net Sales

213

175

21.8

170

24.9

387

407

(4.8)

Total Expenditure

178

147

21.2

140

26.9

324

345

(6.1)

Cost of materials consumed

66

84

(21.2)

58

13.8

150

152

(1.0)

Sub-Cont., Spreading & Assort. Exp.

78

34

127.4

55

42.6

112

134

(16.2)

Employee benefits Expense

12

10

17.3

9

29.8

21

17

22.7

Other Expenses

22

19

19.3

18

20.7

41

43

(4.2)

EBITDA

35

28

24.6

30

15.6

62.9

61.2

2.8

EBIDTA %

16.4

16.0

17.7

16.2

15.0

Depreciation

11

11

2.3

13

(18.5)

21

29

(25.4)

EBIT

24

17

38.0

17

42.3

42

33

27.5

Interest and Fin. Charges

3

3

36.0

3

6.6

6

6

(3.6)

Other Income

12

2

462.5

2

406.0

14

5

170.5

PBT before Exceptional Items

33

17

92.1

16

103.9

50

32

57.6

Exceptional Items

0

0

0

0

0

PBT after Exceptional Items

33

17

92.1

16

103.9

50

32

Tax

(23)

2

2

(20)

(2)

% of PBT

(68.7)

12.1

13.3

(41.1)

(6.6)

PAT

55

15

268.7

14

296.9

70.4

33.7

108.5

Adj. PAT

22

15

48.0

14

59.4

37

34

10.4

Adj. PAT %

10.5

8.6

8.2

9.6

8.3

Dil. EPS

19.68

5.34

268.5

4.96

296.8

25.02

12.00

108.5

Source: Company, Angel Research

Standalone Business Review

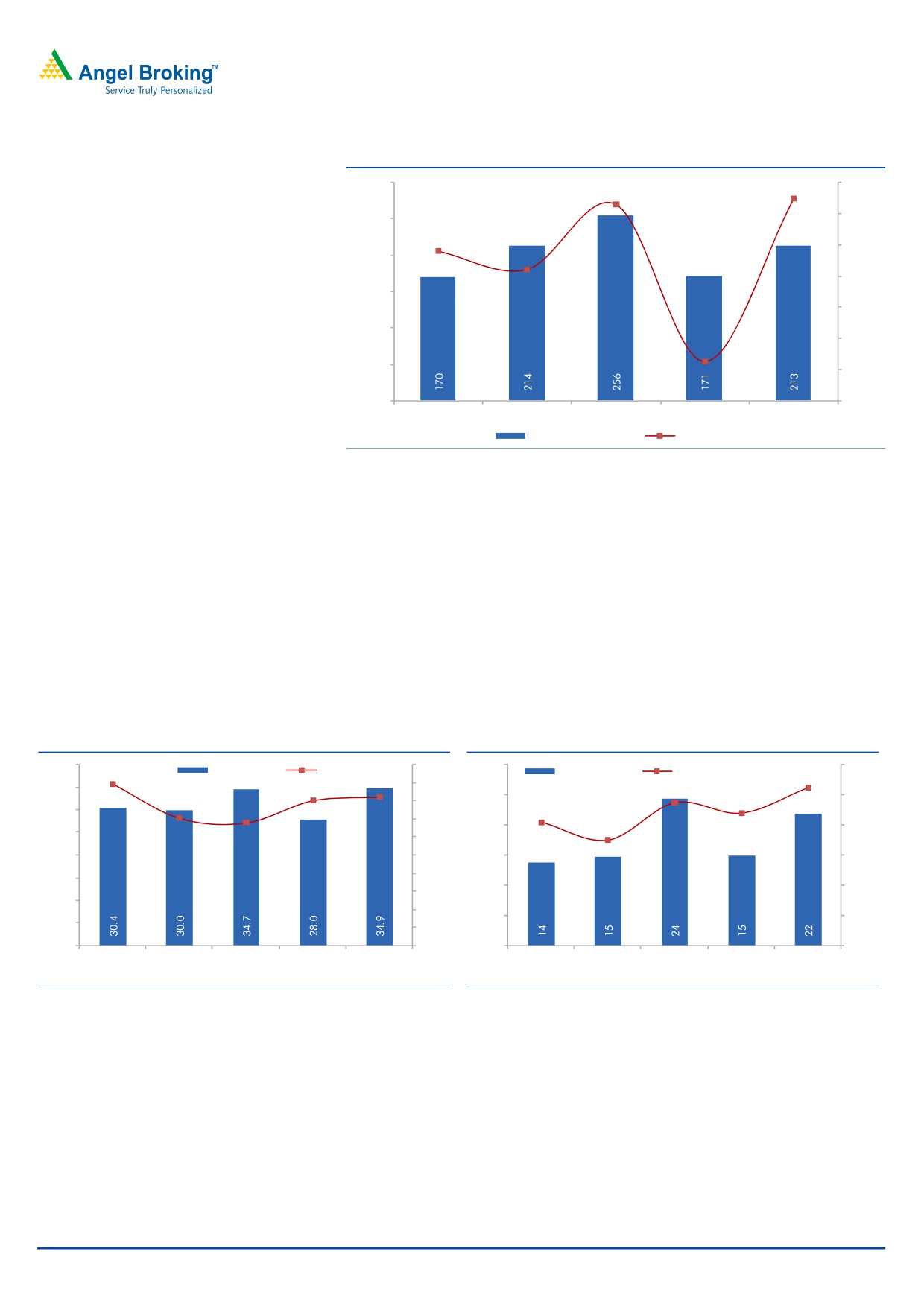

Revenues grow 24.9% yoy

Strong execution led to 24.9%/21.8% yoy/qoq revenue growth in 2QFY2016 to

`213cr. Reported revenues were ahead of our estimate of `189cr. Execution of

Madhya Pradesh (Chindwara-Linga-Umarnala-Saoner, Dabra-Bhitarwar-Harsi

projects) and Andhra Pradesh projects contributed to strong revenues during the

quarter.

November 16, 2015

2

KNR Constructions | 2QFY2016 Result Update

Exhibit 2: Quarterly Revenues

300

24.9

30

23.1

20

250

10

200

2.2

(8.1%)

0

150

(10)

100

(20)

(27.6)

50

(30)

0

(40)

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

Revenues (` cr)

yoy growth (%)

Source: Company, Angel Research

EBITDA margin declines by 132bp yoy to 16.4%

KNR reported an EBITDA of `35cr ahead of our estimate of `27cr. Reported

EBITDA margins of the company were at 16.4%, lower than year ago levels of

17.7% (reflecting 132bp yoy decline). Decline in yoy EBITDA margin was on

account of 42.6% increase in sub-contracting and spreading and assorting

expenses to `78cr (accounted for 36.7% of 2QFY2016 sales) and 29.8% increase

in employee expenses to `12cr. Completion of Chindwara road project where

payments were received on revised quotations led to better EBITDA margins in

2QFY2016.

Exhibit 3: EBITDA margins decline to 16.4%

Exhibit 4: Adj. PAT Margin at 10.5% for the quarter

40

20

30

12

17.8

EBITDA (` cr)

EBITDA Margin (%)

Adj. PAT (` cr)

Adj. PAT Margin (%)

10.5

35

16.0

18

9.5

25

8.8

10

16

30

13.6

8.2

16.4

14

20

7.0

8

25

14.1

12

20

10

15

6

8

15

10

4

6

10

4

5

2

5

2

0

0

0

0

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

Source: Company, Angel Research

Source: Company, Angel Research

Adj. PAT margin expands to 10.5%

The company reported PAT of `55cr, ahead of our estimate of `11cr. Reported

PAT margins of the company were at 26%, ahead of year ago levels of 8.2%.

During the quarter the company reported tax refunds related to prior periods (for

FY2009-12) to the tune of `25.8cr. Also, `5.8cr of interest on income tax refunds

was reported in 2QFY2016 (under other income). On adjusting for these

2 transactions, adj. PAT of the company were at `22cr (reflecting Adj. PAT margins

of 10.5%).

November 16, 2015

3

KNR Constructions | 2QFY2016 Result Update

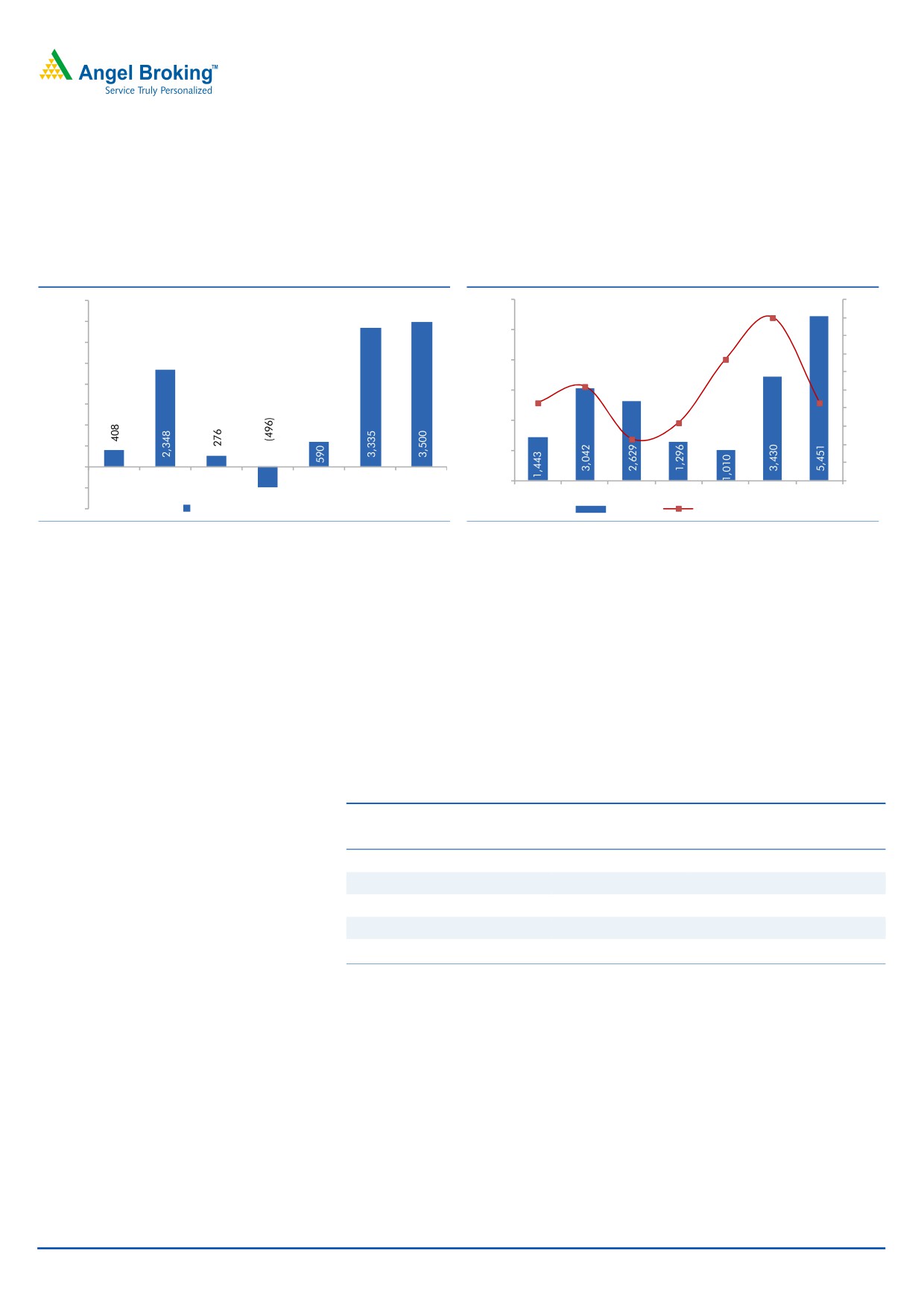

Strong Order Inflow seen during YTD FY2016

Year-to-date in FY2016, KNR has reported `2,591cr of order wins, which is

significantly higher than `950cr of order inflows in FY2015. Management has

guided for another `750cr-1,000cr of order wins for remaining part of FY2016E.

Exhibit 5: Order Inflows to see uptrend

Exhibit 6: Order Book gives better revenue visibility

4,000

6,000

1.0x

0.4x

3,500

0.9x

5,000

0.9x

0.8x

3,000

0.7x

0.7x

2,500

4,000

0.5x

0.2x

0.6x

2,000

3,000

0.4x

0.5x

1,500

0.3x

0.4x

2,000

1,000

0.3x

500

0.2x

1,000

0.1x

0

FY11

FY12

FY13

FY14

FY15

FY16E

FY17E

0

0.0x

(500)

FY11

FY12

FY13

FY14

FY15

FY16E FY17E

(1,000)

Order Inflows (` cr)

OB (` cr)

Execution Rate (x)

Source: Company, Angel Research

Source: Company, Angel Research

Recent order wins from road vertical take the 2QFY2016 Order book to `3,665cr.

This has resulted in 2QFY2016 order book / last twelve month (LTM) sales ratio at

4.3x (vs 1.2x as of 4QFY2015-end). The current order book gives strong revenue

visibility for the next few quarters.

Revision of Earnings Estimate

On considering better than expected execution in 2QFY2016, 1HFY2016 EBITDA

margins, tax refund related to earlier period, we revise our FY2016-17E estimates.

Exhibit 7: Earnings Revision

FY2016E

FY2017E

Y/E March (` cr)

Old

New Chg. (%)

Old

New Chg. (%)

Net Sales

915

937

2.4

1,479

1,470

(0.6)

EBITDA

131

134

2.3

205

205

0.0

EBITDA Margins (%)

14.3

14.3

13.9

14.0

PAT

57

94

64.9

105

109

3.8

PAT Margins (%)

6.2

10.0

7.1

7.4

Source: Angel Research

November 16, 2015

4

KNR Constructions | 2QFY2016 Result Update

Outlook & Valuation

Outlook

KNR in our view enjoys (1) strong execution track record, (2) better cost structure

(reflected in the form of better EBITDA & PAT margins in comparison to its peers),

(3) shorter working capital cycle, (4) low leverage (since FY2011, D/E ratio has

been ~0.2x), and (5) superior RoEs (12.1-17.1% range during FY2011-15). All

these factors indicate at KNR’s superior earnings quality, and strengthen our view

that KNR would continue to trade at rich valuations.

For valuation purposes, we have valued KNR using Sum-Of-The-Parts method.

KNR’s EPC business (standalone entity) is valued at FY2017E P/E multiple, whereas

only 1 of the 4 BOT projects has been valued using “Free Cash flow to Equity

holders” method and another one on BV basis. We have excluded 2 Annuity BOT

projects, where KNR has 40% stake in the JVs with Patel Engineering, as both these

projects are securitized.

Value of Core EPC business

Considering (1) 4.3x order backlog of `3,665cr (as of 2QFY2016-end), which

gives revenue visibility for 24+ months, (2) ramp-up in some of the recently won

projects, which gives better revenue visibility, (3) strong balance sheet (1HFY2015

D/E at 0.1x), (4) strong 22% earnings CAGR during FY2015-17E, and (5) expected

expansion in the RoE (from 13.5% in FY2015 to 15.4% by FY2017E), we assign

15.0x P/E multiple to our FY2017E EPS estimate of `38.6/share and arrive at

standalone business value of `579/share.

Exhibit 8: Sum-of-the-Parts based Valuation Table

FY17E Std. PAT

Target

Target Value

Value/ share

% of

Particulars

Segment

Basis

(` cr)

Multiple

(` cr)

(`)

SoTP

KNR's EPC business

Construction

109

15.0

1,629

579

86

P/E multiple

Total

109

1,629

579

86

Discounted

Project

Adj. FCFE

Value/ share

% of

Particulars

Proj. Type

Basis

FCFE/ BV (` cr)

Stake

Value (` cr)

(`)

SoTP

Road BOT projects

Walayar-Vadakkancheery BOT Proj.

Toll

232

100%

232

83

12

Ke of 14%

Muzaffarpur-Barauni BOT Project

Toll

30

51%

30

11

2

P/BV multiple

Total

262

262

93

14

Grand Total

1,892

673

100

Upside/ (Downside)

16%

CMP

580

Source: Company, Angel Research

November 16, 2015

5

KNR Constructions | 2QFY2016 Result Update

Value of BOT projects

BOT projects have been valued using “Free Cash flow to Equity holders” and Book

value method. The Walayar-Vadakkancheery BOT Project is operational ahead by

1 month from its scheduled CoD of Sep-2015. We have valued this BOT project

using 14% discounting rate to arrive at a FCFE of `83/share (12% of SOTP value

of the company). Also, we have added, equity value of `30cr, which KNR is

expected to infuse in Muzaffarpur-Barauni BOT project at BV to arrive at project

value of `11/share. On a whole, BOT projects contribute `93/share to our revised

price target.

Business Value

On combining the value of EPC business and BOT projects, we arrive at a

combined business value of `673/share, reflecting 16% upside in the stock price

from here-on. Accordingly, we upgrade our rating on the stock to Buy.

November 16, 2015

6

KNR Constructions | 2QFY2016 Result Update

Investment arguments

Order Book grows 3.5x, gives better revenue visibility

KNR announced large ticket project wins, mainly from the Roads & Highways EPC

space in YTD FY2016. To-date in FY2016, KNR reported `2,591cr worth of project

wins, thereby taking the order backlog to `3,665cr as of 2QFY2016-end (vs

`1,010cr in 4QFY2015-end), which gives better revenue visibility for FY2016-17E.

Exhibit 9: Details of recently won EPC Road projects

Announced

Project Value

Project Details

Stake (%)

On

(` cr)

Upgradation of 3 road stretches across Tamil

13-Apr-15

100%

729

Nadu

2/4 laning of the Madurai- Ramanathapuram

17-Apr-15

100%

937

section (115 kms, NH-49)

14-May-15

4-laning of Kazhakkottam-Mukkola (NH-47)

100%

669

Widen/ Reconstruct 3 road stretches across

8-Jul-15

100%

256

different locations within Madhya Pradesh

Total

2,591

Source: Company, Angel Research

KNR’s Management highlighted that it intends to bid only for Road EPC projects.

The Management maintained optimism that the company would report order wins

of ~`750cr-1,000cr in the remaining part of FY2016E. We expect KNR’s order

inflow growth momentum to continue going forward. For FY2016E/FY2017E, we

expect KNR to report `3,335cr/ `3,500cr worth of project wins across verticals.

Accordingly we expect the order book to report

132.3% CAGR during

FY2015-17E.

~30% & 22% Revenue & PAT CAGR, respectively, during

FY15-17E

KNR reported 2.3% top-line CAGR during FY2011-14, owing to a weak order

inflow scenario. However, with uptick in award activity and recent order wins,

coupled with average execution cycle of ~24-36 months, we expect KNR to report

a strong ~30% revenue CAGR during FY2015-17E to `1,479cr.

During FY2011-15, KNR reported EBITDA margins in the range of 14.4%-17.8%

and PAT margins in the range of 7.0%-8.3%. Assuming KNR would not get any

early completion bonus for its ongoing projects and that it would increase its

dependency on sub-contracting, we model 43bp EBITDA margin decline from

14.4% in FY2015 to 14.0% in FY2017E. Higher interest expenses (owing to stretch

in working capital cycle) and higher tax rate assumption (in FY2016-17E) would

restrict the entire benefits of EBITDA growth from flowing down to the PAT level.

The Management clarified that it is availing tax benefits u/s 80IA. We have

assumed 20.0% and 21.0% tax rate for FY2016E and FY2017E, respectively. As a

result, we have estimated restricted PAT CAGR of 22% over FY2015-17E to

`109cr. PAT margins would decline by 94bp to 7.4% in FY2017E.

November 16, 2015

7

KNR Constructions | 2QFY2016 Result Update

Risks & Concerns

Any change in KNR’s taxation policy or adverse ruling by Tax department

could act as risk to our target price and rating.

KNR is highly dependent on the Roads vertical (accounts for ~98% of the

order book). Delays in award activity and unfavorable changes in the policy

framework, could affect our outlook on KNR.

Delays in execution (vs our estimates) could be a risk to our rating.

Company background

KNR is a Hyderabad based 20+ year old company having executed ~5,888kms

of road projects across 12+ states in India. Over the years, KNR has executed

Roads & Highways, Irrigation, and Bridges & Flyover projects. KNR also has a

quarrying division, which ensures timely supply of stone aggregates at project

locations. KNR over the years has evolved from a smaller sized Roads & Highways-

Engineering Procurement and Construction (EPC) player to a large one by

executing projects timely and building its qualification criterion. As of now, KNR

has executed projects for a diversified range of clients namely, NHAI, KSHIP,

MPRDCL, UPSHA, EIL, Sadbhav Engineering and GMR, amongst others.

In addition to the EPC business, KNR has 4 Build Operate Transfer (BOT) projects

in its kitty, with 3 of them operational and the 4rd one soon to be operational.

As of 2QFY2016-end, KNR had an order book of ~`3,665cr, which gives revenue

visibility for next few quarters. The Roads & Highways vertical accounts for ~98%

of the order book.

November 16, 2015

8

KNR Constructions | 2QFY2016 Result Update

Profit and Loss Statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Net Sales

689

837

876

937

1,470

% Chg

(8.1)

21.5

4.7

7.0

56.8

Total Expenditure

576

709

750

803

1,264

Cost of RM Consumed

202

291

337

361

560

Sub-Contracting Expenses

274

282

260

296

485

Employee benefits Expense

30

35

38

39

54

Other Expenses

70

101

115

106

165

EBITDA

113

128

126

134

205

% Chg

(14.9)

13.3

(1.6)

6.4

53.0

EBIDTA %

16.4

15.3

14.4

14.3

14.0

Depreciation

56

57

54

57

62

EBIT

57

71

72

77

143

% Chg

(29.6)

23.5

1.7

6.6

86.6

Interest and Financial Charges

11

17

12

15

18

Other Income

21

13

13

20

12

PBT

67

67

72

81

137

Tax

15

6

(1)

(13)

29

% of PBT

22.2

8.8

(1.0)

(16.2)

21.0

PAT before Exceptional item

52

61

73

94

109

Exceptional item

0

0

0

0

0

PAT

52

61

73

94

109

% Chg

(1.2)

17.0

19.7

28.9

15.4

PAT %

7.6

7.3

8.3

10.0

7.4

Basic EPS

18.5

21.7

26.0

33.5

38.6

Diluted EPS

18.5

21.7

26.0

33.5

38.6

% Chg

(1.2)

16.9

19.8

28.9

15.4

November 16, 2015

9

KNR Constructions | 2QFY2016 Result Update

Balance Sheet (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Sources of Funds

Equity Capital

28

28

28

28

28

Reserves Total

428

485

541

628

728

Networth

456

513

569

656

757

Total Debt

67

58

88

87

124

Other Long-term Liabilities

138

100

69

97

101

Deferred Tax Liability

0

0

0

0

0

Total Liabilities

661

671

726

840

982

Application of Funds

Gross Block

508

525

543

577

616

Accumulated Depreciation

218

262

316

373

435

Net Block

290

264

227

204

181

Capital WIP

4

0

0

0

0

Investments

48

40

32

85

89

Current Assets

Inventories

30

34

36

37

60

Sundry Debtors

121

117

177

227

399

Cash and Bank Balance

7

11

16

17

26

Loans & Advances

328

229

241

342

524

Current Liabilities

293

283

277

357

584

Net Current Assets

194

108

192

265

424

Other Assets

125

259

276

285

287

Total Assets

661

671

726

840

982

November 16, 2015

10

KNR Constructions | 2QFY2016 Result Update

Cash Flow Statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Profit before tax

67

67

72

81

137

Dep. & Other Non-cash Charges

56

57

54

57

62

Change in Working Capital

(106)

16

(98)

(53)

(147)

Interest & Financial Charges

11

16

12

48

32

Direct taxes paid

(27)

(24)

(22)

(28)

(48)

Cash Flow from Operations

1

133

18

105

36

(Inc)/ Dec in Fixed Assets

(38)

(25)

(16)

(28)

(37)

(Inc)/ Dec in Investments

(20)

(55)

(9)

(55)

(4)

Cash Flow from Investing

(58)

(80)

(25)

(82)

(42)

Issue/ (Buy Back) of Equity

0

0

0

0

0

Inc./ (Dec.) in Loans

71

(32)

36

0

41

Dividend Paid (Incl. Tax)

(3)

(3)

(6)

(7)

(8)

Net Interest Expenses

(11)

(17)

(12)

(15)

(18)

Cash Flow from Financing

57

(52)

18

(22)

14

Inc./(Dec.) in Cash

(0)

1

12

1

9

Opening Cash balances

4

3

4

16

17

Closing Cash balances

3

4

16

17

26

November 16, 2015

11

KNR Constructions | 2QFY2016 Result Update

Key Ratios (Standalone)

Y/E March

FY13

FY14

FY15

FY16E

FY17E

Valuation Ratio (x)

P/E (on FDEPS)

31.3

26.7

22.3

17.3

15.0

P/CEPS

15.1

13.8

12.8

10.8

9.6

Dividend yield (%)

0.0

0.0

0.0

0.0

0.0

EV/Sales

2.4

2.0

1.9

1.8

1.2

EV/EBITDA

14.5

13.3

13.5

12.6

8.4

EV / Total Assets

3.2

2.5

2.5

2.3

2.1

Per Share Data (`)

EPS (fully diluted)

18.5

21.7

26.0

33.5

38.6

Cash EPS

38.3

42.0

45.2

53.9

60.7

DPS

1.0

1.0

1.7

2.2

2.5

Book Value

162

183

202

233

269

Returns (%)

RoCE (Pre-tax)

16.0

15.4

13.8

13.8

19.1

Angel RoIC (Pre-tax)

15.0

14.7

12.9

13.0

17.6

RoE

12.1

12.6

13.5

15.4

15.4

Turnover ratios (x)

Asset Turnover (Gross Block) (X)

1.4

1.6

1.6

1.7

2.5

Inventory / Sales (days)

16

15

15

15

15

Receivables (days)

64

51

74

88

99

Payables (days)

56

34

29

31

34

Leverage Ratios (x)

D/E ratio (x)

0.1

0.1

0.2

0.1

0.2

Interest Coverage Ratio (x)

7.0

4.9

6.9

6.3

8.7

November 16, 2015

12

KNR Constructions | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

KNR Constructions

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

November 16, 2015

13