Initiating Coverage | Auto Ancillary

November 23, 2015

Jamna Auto Industries

ACCUMULATE

CMP

`234

Play on MHCV upcycyle

Target Price

`258

Jamna Auto Industries (JAI) is engaged in the manufacturing of suspension

Investment Period

12 Months

products for commercial vehicles viz leaf springs and lift axles. It is the market

leader in the MHCV OEM springs commanding market share of about 60%, while

Stock Info

it has a 15% share in the aftermarket springs segment.

Sector

Auto Ancillary

Recovery in OEM segment coupled with aftermarket focus to drive growth

Market Cap (` cr)

890

The MHCV industry is clearly in an upcycle and is poised to grow at 16% CAGR

Net Debt (` cr)

54

over the FY2015-2018 period. This would be on account of economic pick-up

Beta

1.1

leading to uptick in freight, huge pent up demand due to low base (industry had

52 Week High / Low

275 / 130

halved over FY2013-2014 period), and improving profitability of the fleet

Avg. Daily Volume

4,346

operators on account of firm freight rates and decline in diesel prices. The

Face Value (`)

10

industry is likely to reach pre-slowdown levels by FY2018. Apart from growth in

BSE Sensex

25,868

the springs segment, JAI is witnessing robust demand for lift axles used in multi

axle vehicles (JAI commenced supplies to market leader Ashok Leyland). JAI is

Nifty

7,857

also in negotiation with high-end bus manufacturers for supplies of air suspension

Reuters Code

JMNA.BO

systems. We expect the share of new products to inch up from 4% of revenues in

Bloomberg Code

JMNA@IN

FY2015 to 7% by FY2018. We expect JAI to clock 14% revenue CAGR over the

next three years.

Shareholding Pattern (%)

Operating leverage, raw material localization and new products to

Promoters

43.8

augment margins

MF / Banks / Indian Fls

1.9

JAI would reap benefits of operating leverage on account of healthy double-digit

top-line growth. Steep reduction in crude prices due to slowdown would lower the

FII / NRIs / OCBs

1.0

power and fuel costs which account for 7% of the top-line. Further, increasing

Indian Public / Others

53.3

share of high margin products such as parabolic leaf springs and lift axles (new

products’ share would go up from 22% currently to about 30% by FY2018) would

also augment margins for the company. We estimate JAI’s operating margins to

Abs. (%)

3m 1yr 3yr

improve by 130bp over the next three years.

Sensex

(6.3)

(7.8)

41.1

JMNA

6.6

60.0

127.9

Outlook and valuation: JAI’s top-line is estimated to grow at 14% CAGR on

account of uptick in the MHCV OEM segment and ramp up of new products, ie

parabolic leaf springs and lift axles. Further, operating leverage coupled with a

3-Year Daily price chart

better product mix and savings on energy costs would enhance margins. We

300

expect JAI’s earnings to grow at a CAGR of 35% over FY2015-2018. JAI’s return

250

ratios are also estimated to improve on account of margin expansion, better working

200

capital management and lower gearing. We initiate coverage on JAI with an

150

Accumulate rating and target price of `258 (based on 15x FY2018E earnings).

100

Key financials

50

Y/E March (` cr)

FY2015

FY2016E

FY2017E

FY2018E

0

Net sales

1,095

1,292

1,486

1,620

% chg

31.4

18.0

15.0

9.0

Net profit (Adj.)

29

48

60

68

Source: Company, Angel Research

% chg

NA

64.5

25.3

14.9

EBITDA margin (%)

8.6

9.3

9.8

9.9

EPS (`)

7.3

12.0

15.0

17.2

P/E (x)

32.2

19.6

15.6

13.6

P/BV (x)

4.7

4.0

3.4

2.9

RoE (%)

14.7

20.7

21.8

21.3

RoCE (%)

23.2

25.1

27.1

27.3

Bharat Gianani

EV/Sales (x)

0.9

0.8

0.7

0.6

022-39357800 Ext: 6817

EV/EBITDA (x)

10.4

8.4

7.0

6.2

Source: Company, Angel Research; CMP as on Nov 20, 2015

Please refer to important disclosures at the end of this report

1

Jamna Auto Industries | Initiating Coverage

Investment Arguments

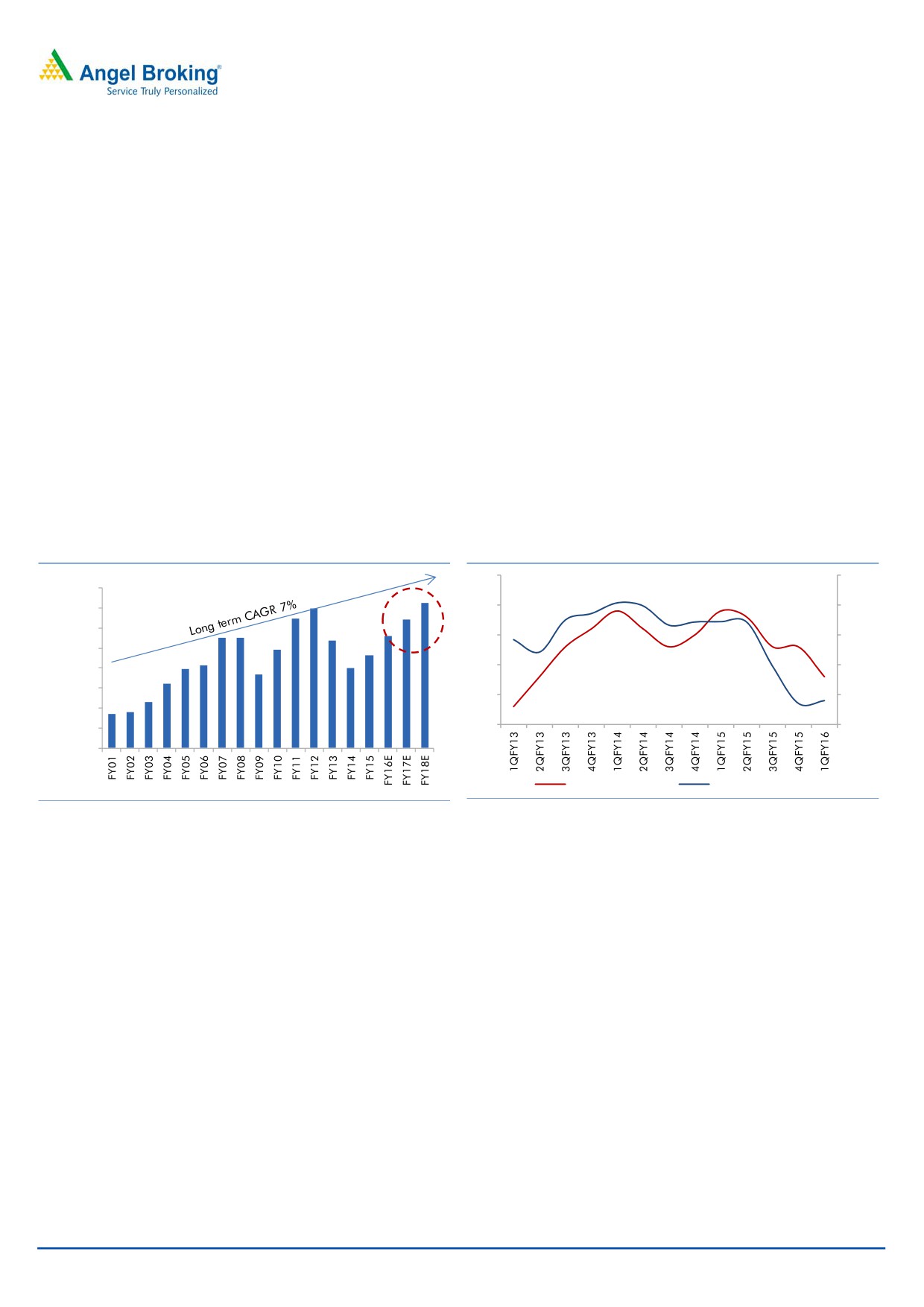

MHCV industry in upcycle; expect 16% CAGR over FY2015-18

After two consecutive years of double-digit dip, the MHCV industry resurged

strongly in FY2015, reporting a healthy growth of 17%. Policy actions by the

government led to economic recovery. Further, government actions in terms of

clearing stalled projects, increased infrastructure activity, and resumption of mining

have further boosted MHCV sales. Also, improvement in fleet operators’

profitability due to firm freight rates and reduction in diesel prices have also

boosted demand. Huge pent up demand due to severe slowdown in FY2013/14

coupled with economic revival has stoked demand.

The MHCV industry is clearly in an upcycle and we expect the industry to maintain

double-digit growth momentum and clock 16% CAGR over FY2015-2018 period.

Given the pace of recovery, the MHCV segment should reach pre-slowdown levels

(levels seen in FY2012) by FY2018. JAI derives about 70% of its revenues from the

MHCV OEM segment and would be a beneficiary of the strong demand.

Exhibit 1: MHCV industry trend

Exhibit 2: Trend in freight rates and diesel prices

2.5

30.0

400,000

Implied

2.0

20.0

350,000

CAGR 16%

300,000

1.5

10.0

250,000

200,000

1.0

0.0

150,000

0.5

(10.0)

100,000

0.0

(20.0)

50,000

0

Freight Growth (%)

Diesel Price growth (%)

Source: SIAM, Angel Research

Source: SIAM, Angel Research

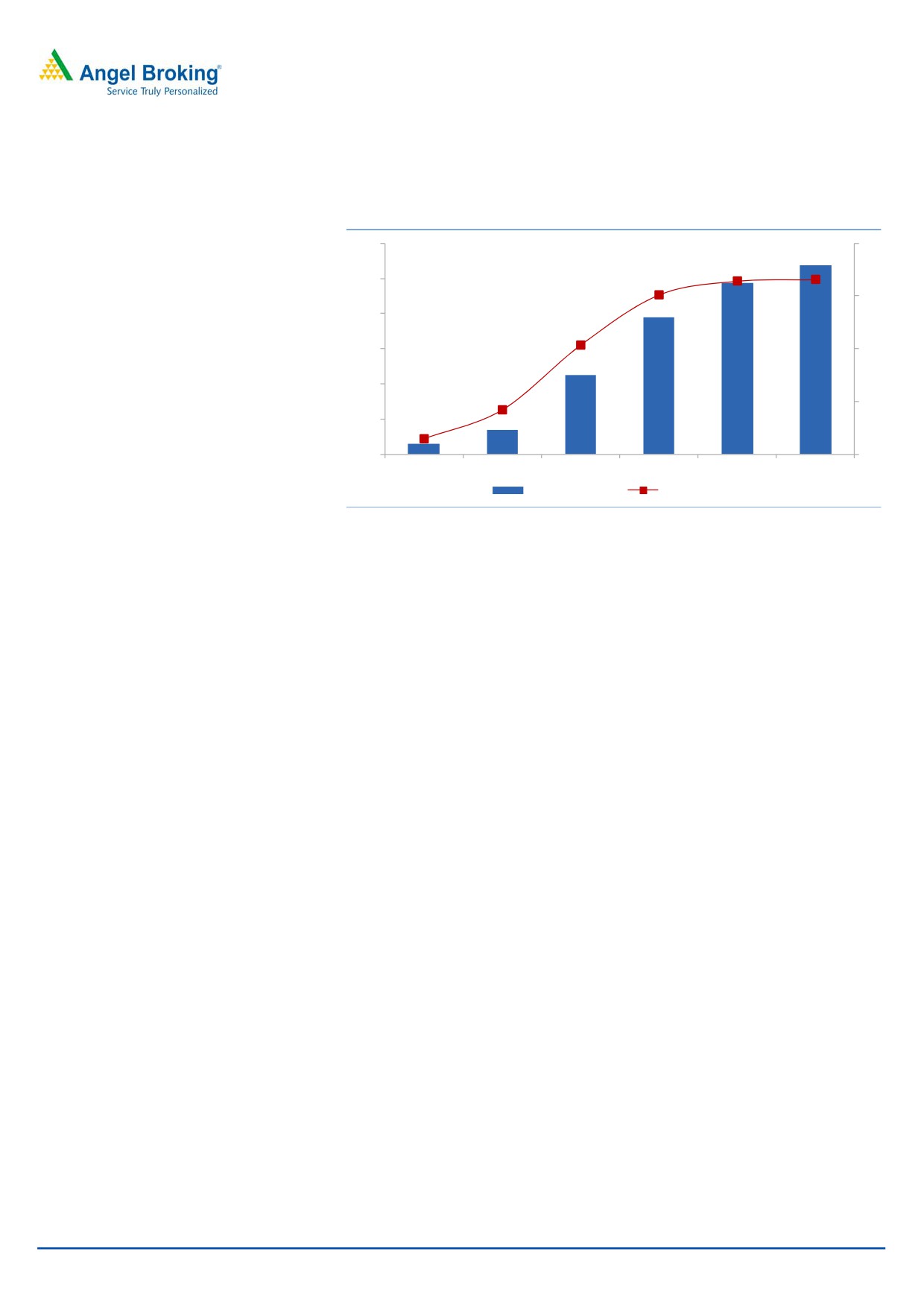

New product launches to boost top-line

Under the “Lakshya” initiative, JAI is aiming for 33% revenue contribution from

new products. JAI is focusing on new products such as parabolic leaf springs, lift

axles and air suspension systems. JAI has been a pioneer in introducing parabolic

springs (currently holds 95% market share) which are more strong as compared to

conventional springs and offer more driving comfort. The penetration of parabolic

springs currently stands at 18% and is expected to reach 25% levels over the next

three years.

JAI aims to be a leader in automobile suspension solutions. It aims to be a full

suspension system provider and has expanded its product profile. In 2013, JAI

ventured into manufacturing of lift axles and air suspensions with technological

collaboration with Ridewell Corporation, USA. JAI successfully commenced

supplies of lift axles to Ashok Leyland in FY2013 and is in negotiation with other

OEMs. The share of lift axles in the overall revenues increased to 4% in FY2015.

Similarly, JAI is also negotiating with SML Isuzu for commencing supplies of air

November 23, 2015

2

Jamna Auto Industries | Initiating Coverage

suspension systems. We expect the share of new products to improve from 22% to

30% by FY2018.

Exhibit 3: Lift axles

120

8

100

6

80

60

4

40

2

20

0

0

FY13

FY14

FY15

FY16E

FY17E

FY18E

Lift axle (` cr)

% of revenues

Source: Company, Angel Research

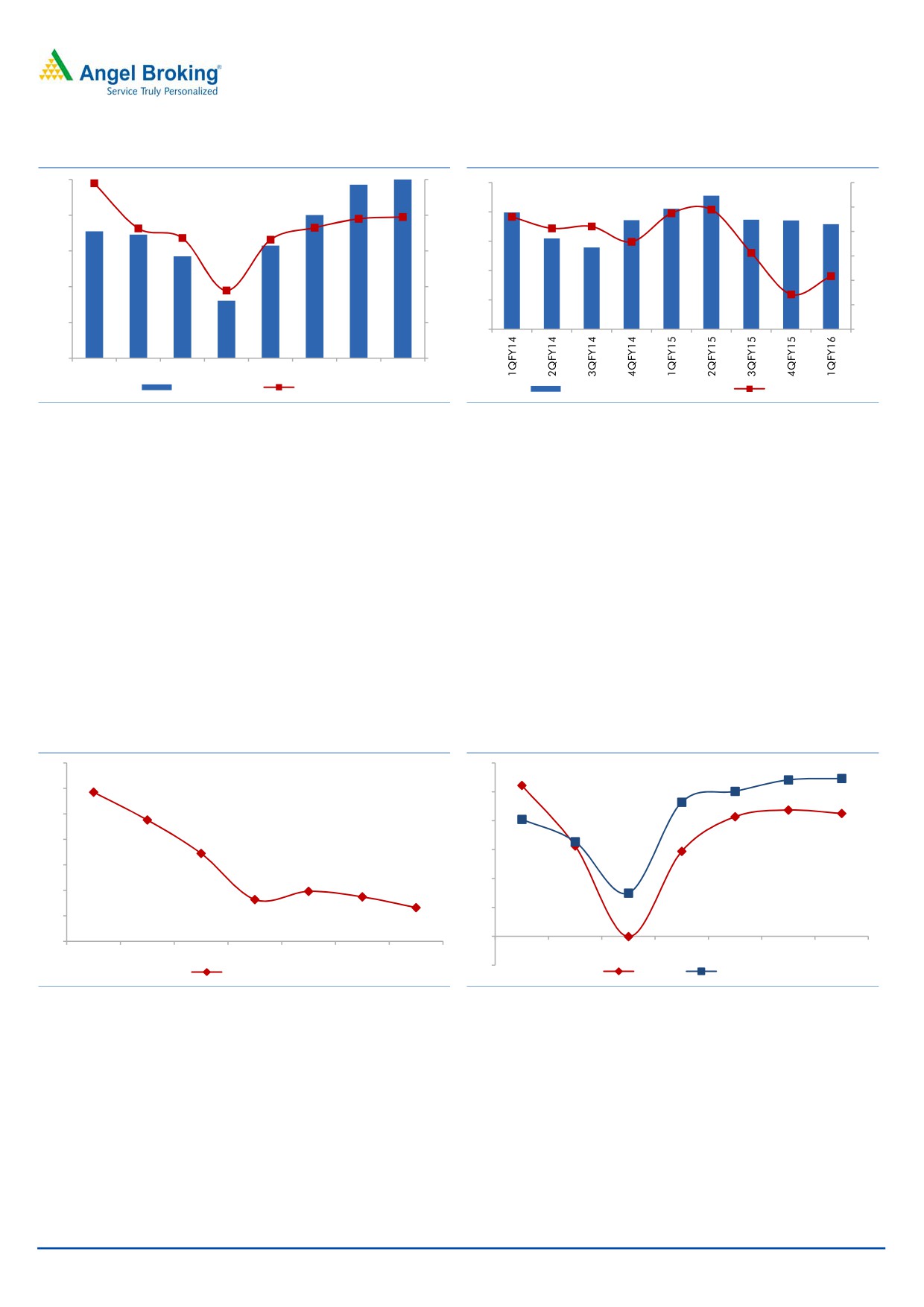

Operating leverage, lower energy prices coupled with better

product mix to improve margins

JAI’s revenues are likely to grow at 14% CAGR over the next three years owing to

steep uptrend in the MHCV OEM segment. The company is likely to draw benefits

of operating leverage due to double digit top-line growth. Also, given the slump in

oil prices due to slowdown in China, the energy cost for the company (forming

about 7% of the revenues) is likely to remain lower resulting into margin

improvement.

Also, JAI is likely to benefit from a better product mix viz lift axles and parabolic

springs. The MHCV industry is increasingly adopting technologically advanced

parabolic springs which offer more driver comfort and are long lasting as

compared to conventional springs. Parabolic springs fetch about 20% more

realisaton as well as better margins. JAI is the pioneer in introduction of parabolic

springs and already commands 95% market share. The share of parabolic springs

is likely to increase from 18% to 25% over the next three years. Also, the share of

lift axles is likely to inch up given the ramp up of supplies. We expect JAI’s margins

to improve by 130bp over the next three years.

November 23, 2015

3

Jamna Auto Industries | Initiating Coverage

Exhibit 4: EBIDTA margins to improve

Exhibit 5: Energy cost trend

150

12

25

10

9

120

10

20

8

15

90

8

7

10

6

60

6

5

5

30

4

0

4

0

2

FY11

FY12

FY13

FY14

FY15

FY16E FY17E FY18E

EBIDTA (` cr)

Margin (%)

Power and Fuel Costs (` cr)

% of sales

Source: Company, Angel Research

Source: Exchange rates, Angel Research

Margin improvement coupled with improvement in leverage to

boost return ratios

JAI’s margins are estimated to improve by 130bp from 8.6% in FY2015 to 9.9% in

FY2018. Also, JAI is following better working capital management by adopting

just-in-time approach (leading to lower inventory) and having better negotiation

terms with customers. Given the robust top-line growth coupled with improved

working capital cycle, JAI’s capital expenditure is likely to be met through internal

accruals. JAI’s debt/equity ratio is likely to remain low at 0.3x. Given the above

factors, we expect JAI’s RoCE to improve from 23.2% in FY2015 to 27.3% in

FY2018. Similarly, the RoE is estimated to improve from 14.7% in FY2015 to

21.3% in FY2018.

Exhibit 6: Capital Gearing

Exhibit 7: Return ratios

1.4

30

1.2

25

1.0

20

0.8

15

0.6

10

0.4

5

0.2

0

0.0

FY12

FY13

FY14

FY15

FY16E

FY17E

FY18E

FY12

FY13

FY14

FY15

FY16E

FY17E

FY18E

(5)

Capital Gearing

RoE (%)

RoCE (%)

Source: Company, Angel Research

Source: Company, Angel Research

Focus on Aftermarket segment to augment growth

In a bid to reduce dependence on the OEM business, JAI is focusing on the

aftermarket segment. As per industry estimates, the size of the aftermarket segment

is similar to the OEM (aftermarket size is pegged at `1200cr-1500cr). JAI’s

aftermarket revenues have grown at 15% CAGR over the FY2011-15 period. JAI is

pretty strong in the Northern and Western markets with it deriving about 70% of

the aftermarket revenues from these markets. JAI is expanding dealerships in the

Southern and the Eastern markets as well to boost revenues.

November 23, 2015

4

Jamna Auto Industries | Initiating Coverage

Further as per JAI, the unorganised players currently constitute about half of the

overall aftermarket industry. Unorganised players are mostly from the cottage

industry and do not pay taxes, leading to a price advantage. As per the

Management, the rollout of GST would virtually eliminate the pricing advantage of

the unorgainsed players. Organised players such as JAI would benefit from GST

and are likely to see market share gains.

November 23, 2015

5

Jamna Auto Industries | Initiating Coverage

Management targets

JAI has a vision to be a leader in automobile suspension solutions. To achieve this,

the Management has charted out an action plan - Lakshya 33. Lakshya 33

envisages the following:

33% revenue from new products: JAI aims to derive one-third of its revenues

from new products. JAI has successfully introduced new products viz lift axles,

air suspension systems and new generation springs.

33% revenues from new markets: The Management is aiming to derive one-

third of the revenues from new segments, viz the aftermarket segment and

exports. The company is strengthening its dealer network in Eastern and

Southern markets to boost aftermarket sales. Further, JAI is setting up a plant

in Hosur to supply to global OEMs, viz General Motors and Ford.

Lower breakeven point: JAI is aiming to lower the breakeven point to 33% of

the installed capacity. The Management aims to achieve this by focusing on

operational efficiencies and reducing fixed costs.

RoCE and dividend payout of 33%: The Management aims to achieve RoCE

of 33%, led by lowering the breakeven point and a better product mix.

Further, to award shareholders, the Management would increase the dividend

payout to 33%.

November 23, 2015

6

Jamna Auto Industries | Initiating Coverage

Outlook and Valuation

JAI’s top-line is estimated to grow at a CAGR of 14% on account of uptick in the

MHCV OEM segment and ramp up of new products, ie parabolic leaf springs and

lift axles. Further, operating leverage coupled with a better product mix and

savings on energy costs would enhance margins. We expect JAI’s earnings to grow

at a CAGR of 35% over FY2015-2018. JAI’s return ratios are also estimated to

improve on account of margin expansion, better working capital management and

lower gearing. We initiate coverage on JAI with an Accumulate rating and target

price of `258 (based on 15x FY2018E earnings).

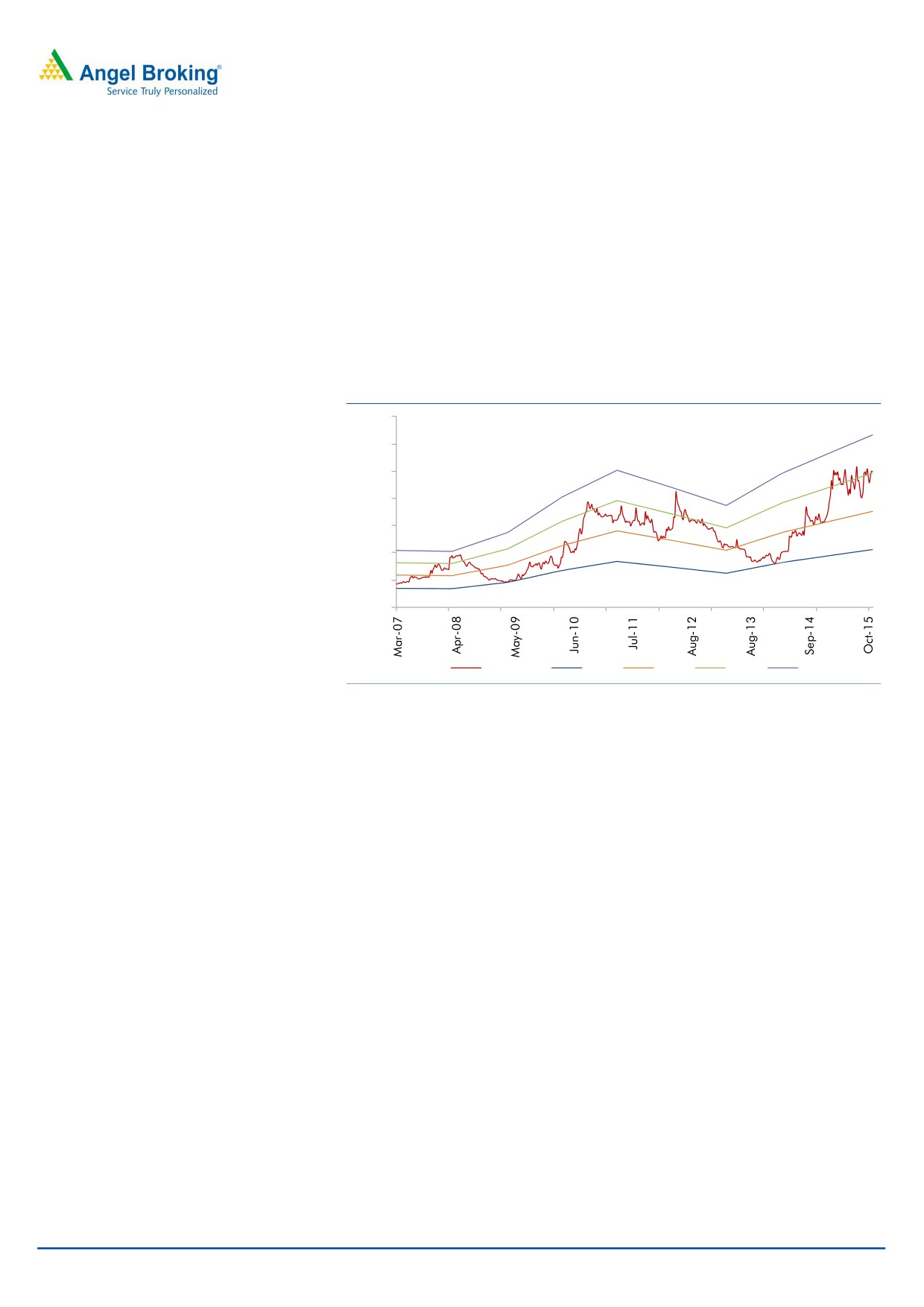

Exhibit 8: One-year forward EV/Sales band

1,400

1,200

1,000

800

600

400

200

0

EV (` cr)

0.3x

0.5x

0.7x

0.9x

Source: Company, Angel Research

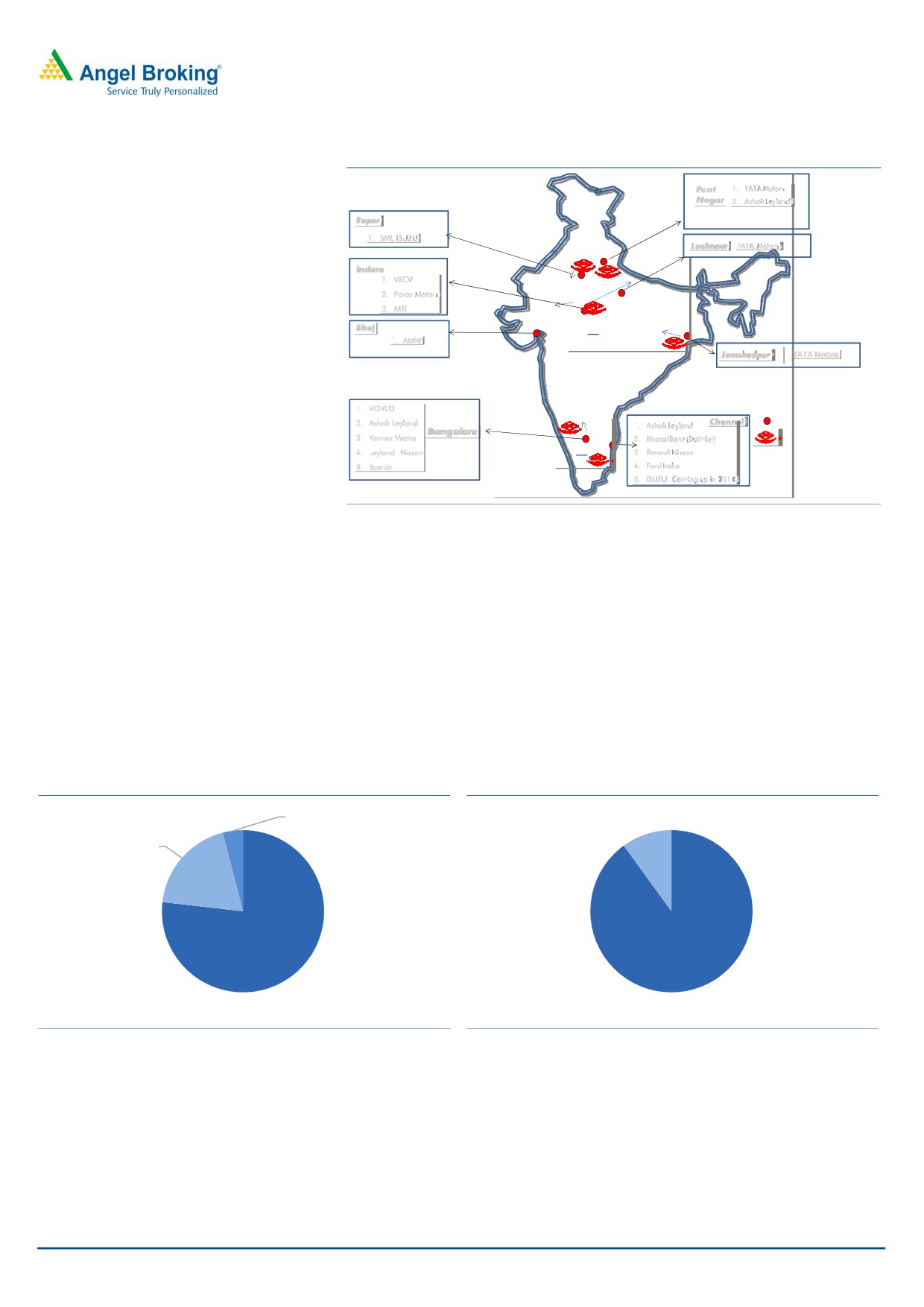

Company Background

Jamna Auto Industries Ltd is India's largest and world's third largest manufacturer

of tapered leaf springs and parabolic springs for automobiles. The company was

first to introduce parabolic springs in India. It has six strategically located

manufacturing facilities at Yamuna Nagar, Malanpur (near Gwalior), Chennai,

Jamshedpur, Hosure and Pantnagar (under subsidiary entity). The company is the

market leader with 57% market share in the Indian OEM segment and produces

over 410 modes of springs for OEMs.

November 23, 2015

7

Jamna Auto Industries | Initiating Coverage

Exhibit 9: Manufacturing footprint

Pant

1. TATA Motors

Nagar

2. Ashok Leyland

Ropar

1. SML ISUZU

Lucknow

TATA Motors

JAI - Pantnagar

Indore

1. VECV

JAI - Yam

2. Force Motors

3. MTI

JAI - Gwal

Bhuj

1. AMW

Jamshedpur

TATA Motors

1. VOVLO

JAI - Hosur

2. Ashok Leyland

1. Ashok Leyland

Chennai

M Plants

Bangalore

3. Kamaz Vectra

2. Bharat Benz (Daimler)

JAI Existing Plants

4. Leyland Nissan

ai

3. Renault Nissan

5. Scania

4. Ford India

5. ISUZU -Coming up in 2014

Source: Company, Angel Research

JAI is the domestic leader in the manufacturing of leaf springs for commercial

vehicles. It has a well established client base supplying to major domestic

customers such as Tata Motors, Ashok Leyland, Volvo Eicher Commercial Vehicles

and foreign players such as Daimler India. Springs constitute about 95% of the

company’s sales. Conventional springs contribute 77% of the revenues while the

parabolic springs account for 19%. The recently introduced lift axles constitute 4%

of the top-line. The MHCV segment contributes a major chunk of revenues for the

company, forming about 90% of the overall top-line. Besides the MHCV segment,

JAI also supplies to the LCV segment which constitutes about 10% of the revenues.

Exhibit 10: Product breakup

Exhibit 11: Segmentwise breakup

Lift axles, 4%

Parabolic leaf

springs, 19%

LCV,

10%

Conventional

MHCV, 90%

leaf springs,

77%

Source: Company, Angel Research

Source: Company, Angel Research

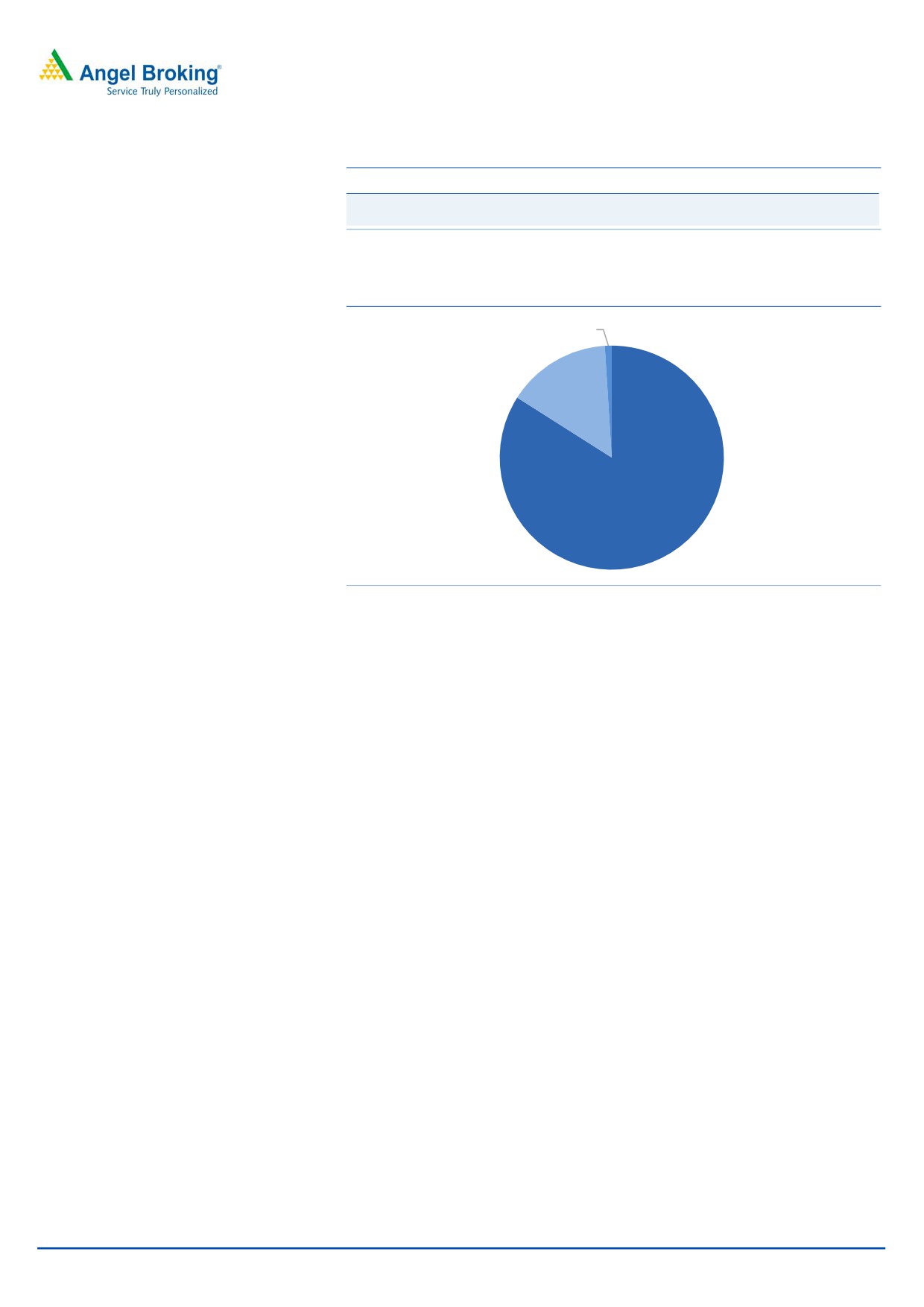

The OEM segment is the largest contributing segment, accounting for about 84%

of revenues. Aftermarket is the second largest segment constituting ~15% of the

revenues. Exports currently constitute about 1% of the overall sales.

November 23, 2015

8

Jamna Auto Industries | Initiating Coverage

Exhibit 12: Client base

Domestic customers

International customers

Tata Motors, Ashok Leyland, VECV,

Daimler India, Volvo, Renault-Nissan,

Swaraj Mazda, AMW, Mahindra & Mahindra Isuzu, Ford, General Motors

Source: Company, Angel Research

Exhibit 13: Customer segmentation

Exports, 1%

Aftermarket,

15%

OEM , 84%

Source: Company, Angel Research

November 23, 2015

9

Jamna Auto Industries | Initiating Coverage

Profit & Loss Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

FY2018E

Total operating income

980

833

1,095

1,292

1,486

1,620

% chg

(12.5)

(15.0)

31.4

18.0

15.0

9.0

Total Expenditure

895

785

1,001

1,172

1,340

1,459

Net Raw Materials

645

563

735

863

988

1,077

Personnel

60

60

69

79

89

97

Other

190

162

197

230

263

285

EBITDA

85

48

94

120

146

160

% chg

(17.6)

(43.6)

95.9

27.2

21.2

10.1

(% of Net Sales)

8.7

5.8

8.6

9.3

9.8

9.9

Depreciation & Amortisation

29

26

31

37

43

46

EBIT

59

24

65

86

106

118

% chg

(19.9)

(58.7)

168.7

31.0

23.3

11.6

(% of Net Sales)

6.0

2.9

6.0

6.6

7.1

7.3

Interest & other Charges

27

24

18

14

16

15

Other Income

2

2

2

3

3

4

PBT (recurring)

32

0

47

72

90

103

% chg

(41.2)

(99.2) 17,639.2

51.3

25.1

14.8

Extraordinary Expense/(Inc.)

-

16

-

-

-

-

PBT (reported)

32

17

47

72

90

103

Tax

4

3

18

24

30

34

(% of PBT)

13.8

17.2

38.0

33.0

33.0

33.0

Minority Interest

0

0

0

-

-

-

Preference dividend

0

0

0

0

0

0

PAT (reported)

27

14

29

48

60

68

ADJ. PAT

27

(0)

29

48

60

68

% chg

(33.0)

NA

NA

64.5

25.3

14.9

(% of Net Sales)

2.8

(0.0)

2.6

3.7

4.0

4.2

Basic EPS (`)

6.9

3.4

7.3

12.0

15.0

17.2

Fully Diluted EPS (`)

6.9

(0.0)

7.3

12.0

15.0

17.2

% chg

(33.0)

NA

NA

64.5

25.3

14.9

November 23, 2015

10

Jamna Auto Industries | Initiating Coverage

Balance sheet statement

Y/E March (` cr)

FY2013 FY2014 FY2015 FY2016E FY2017E FY2018E

SOURCES OF FUNDS

Equity Share Capital

43

41

40

40

40

40

Reserves& Surplus

132

140

157

190

233

282

Shareholders Funds

175

182

196

230

273

322

Total Loans

166

125

64

90

95

85

Deferred Tax Liability

16

15

16

16

16

16

Other long term liab.

1

1

1

1

1

1

Long term provisions

3

3

4

5

6

8

Total Liabilities

360

326

282

342

391

432

APPLICATION OF FUNDS

Gross Block

463

467

479

579

669

729

Less: Acc. Dep.

198

208

237

274

317

363

Net Block

265

259

242

305

352

366

Capital WIP

17

2

8

3

3

3

Investments

5

0

0

0

0

0

Long Loans and adv.

39

32

39

47

53

58

Current Assets

274

245

206

243

272

322

Cash

15

14

11

8

3

14

Other

259

231

196

234

270

308

Current liabilities

241

213

214

256

291

318

Net Current Assets

32

32

(8)

(13)

(18)

4

Total Assets

360

326

282

342

391

432

November 23, 2015

11

Jamna Auto Industries | Initiating Coverage

Cash flow statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E FY2018E

Profit before tax

32

17

47

72

90

103

Depreciation

19

10

29

37

43

46

Change in Working Capital

9

(1)

37

3

(1)

(11)

Others

1

0

2

0

1

2

Direct taxes paid

(4)

(3)

(18)

(24)

(30)

(34)

Cash Flow from Operations

57

23

96

88

103

105

(Inc.)/ Dec. in Fixed Assets

(28)

11

(17)

(95)

(90)

(60)

(Inc.)/ Dec. in Investments

0

5

0

0

0

0

(Inc.)/ Dec. in Loans & Adv

2

7

(7)

(7)

(7)

(5)

Cash Flow from Investing

(26)

23

(24)

(102)

(97)

(65)

Issue of Equity

0

(2)

(2)

0

0

0

Inc./(Dec.) in loans

(17)

(41)

(61)

26

5

(10)

Dividend Paid (Incl. Tax)

(8)

(4)

(9)

(14)

(17)

(19)

Others

(1)

(1)

(4)

0

0

0

Cash Flow from Financing

(25)

(47)

(75)

11

(12)

(29)

Inc./(Dec.) in Cash

5

(1)

(3)

(2)

(6)

11

Opening Cash balances

10

15

14

11

8

3

Closing Cash balances

15

14

11

8

3

14

November 23, 2015

12

Jamna Auto Industries | Initiating Coverage

Key ratios

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

34.1

NA

32.2

19.6

15.6

13.6

P/CEPS

16.5

36.0

15.5

11.0

9.1

8.1

P/BV

5.3

5.1

4.7

4.0

3.4

2.9

Dividend yield (%)

0.9

0.4

0.9

1.5

1.8

2.1

EV/Sales

1.1

1.2

0.9

0.8

0.7

0.6

EV/EBITDA

12.6

21.6

10.4

8.4

7.0

6.2

EV / Total Assets

3.0

3.2

3.5

3.0

2.6

2.3

Per Share Data (`)

EPS (Basic)

6.9

0.0

7.3

12.0

15.0

17.2

EPS (fully diluted)

6.9

0.0

7.3

12.0

15.0

17.2

Cash EPS

14.2

6.5

15.1

21.3

25.8

28.8

DPS

2.0

1.0

2.2

3.6

4.2

4.8

Book Value

43.9

45.7

49.4

57.8

68.6

81.0

Dupont Analysis

EBIT margin

6.0

2.9

6.0

6.6

7.1

7.3

Tax retention ratio

0.9

0.8

0.6

0.7

0.7

0.7

Asset turnover (x)

2.8

2.7

4.0

3.9

3.8

3.9

ROIC (Post-tax)

14.7

6.5

15.0

17.2

18.3

18.9

Cost of Debt (Post Tax)

13.9

15.9

17.4

10.4

11.3

11.8

Leverage (x)

0.9

0.6

0.3

0.4

0.3

0.2

Operating ROE

15.4

0.6

14.3

19.7

20.6

20.5

Returns (%)

ROCE (Pre-tax)

16.4

7.5

23.2

25.1

27.1

27.3

Angel ROIC (Pre-tax)

17.1

7.8

24.1

25.7

27.3

28.2

ROE

15.6

(0.1)

14.7

20.7

21.8

21.3

Turnover ratios (x)

Asset Turnover (Gross Block)

2.1

1.8

2.3

2.2

2.2

2.2

Inventory / Sales (days)

49.0

44.1

36.4

37.0

37.0

38.0

Receivables (days)

39.8

47.5

18.8

19.0

19.0

21.0

Payables (days)

89.9

93.3

71.4

72.3

71.4

71.6

WC cycle (ex-cash) (days)

6.4

7.9

(6.2)

(6.1)

(5.2)

(2.2)

Solvency ratios (x)

Net debt to equity

0.9

0.6

0.3

0.4

0.3

0.2

Net debt to EBITDA

1.8

2.3

0.6

0.7

0.6

0.4

Interest Coverage (EBIT / Int.)

2.2

1.0

3.6

6.1

6.6

7.9

November 23, 2015

13

Jamna Auto Industries | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Jamna Auto Industries

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 23, 2015

14