2QFY2016 Result Update | Cement

November 5, 2015

JK Cement

BUY

CMP

`647

Performance Highlights

Target Price

`744

Quarterly results (Standalone)

Investment Period

12 Months

Y/E March (` cr)

2QFY2016

2QFY2015

% chg yoy 1QFY2016

% chg qoq

Net Sales

868

828

4.8

811

7.1

Stock Info

EBITDA

106

88

21.4

84

26.1

Sector

Cement

EBITDA margin

12.3

10.6

167bp

10.4

185bp

Market Cap (` cr)

4,524

Net Profit

14

32

(57.5)

0

8473.7

Source: Company, Angel Research

Net debt (` cr)

1,700

Beta

0.7

JK Cement (JKCem)’s 2QFY2016 reported numbers have come in better than our

52 Week High / Low

754 / 546

estimates. The company’s net sales grew by 4.8% yoy to `867.9cr (above our

Avg. Daily Volume

52,455

estimate of `832.2cr). The company’s blended sales volume increased by 2.8%

Face Value (`)

10

yoy, led by 4.3% yoy growth in the white cement (including putty) business.

BSE Sensex

26,553

Blended realization/tonne, at `4,743, increased 2.0/6.3% yoy/qoq during the

Nifty

8,040

quarter (above our estimate of `4,596). The EBITDA increased by 21.4% yoy to

Reuters Code

JKCE.BO

`106.4cr, which is above our estimate of `97.1cr. The EBITDA/tonne improved by

Bloomberg Code

JKCE IN

18.1% yoy to `581 and is above our estimate of `536. The Net profit declined

57.5% yoy to `13.7cr, on account of higher depreciation and interest expenses.

Shareholding Pattern (%)

EBITDA margin at 12.3%, up 167bp yoy: For 2QFY2016, JKCem posted a

Promoters

67.0

marginal 4.8% yoy increase in its top-line to `867.9cr. The EBITDA came in at

`106.4cr, an increase of 21.4% yoy (above our estimate of `97.1cr). The EBITDA

MF / Banks / Indian Fls

14.0

margin at 12.3% is above our estimate of 10.8%, led by better than expected

FII / NRIs / OCBs

11.0

realization and flat operating costs. The operating cost/tonne remained flat yoy at

Indian Public / Others

8.1

`4,161. The EBITDA/tonne came in at `581, up by 18.1% yoy, due to increase in

realization and flat operating costs.

Abs.(%)

3m 1yr 3yr

Outlook and valuation: Going ahead, we expect the company to witness

Sensex

(5.4)

(4.7)

41.5

moderation in demand and impact on profitability. The Management has also

JK Cement

(2.8)

(1.9)

128.6

reduced its grey cement volume guidance from 7.5mt to 6.5mt for FY16 due to

soft demand. We forecast top-line to grow at a CAGR of 18.4% and EBIDTA to

grow at CAGR of 33.3% over FY2015-17E. At the current market price, the stock

3-year price chart

900

trades at 7.8x FY2017E EV/EBIDTA and EV/tonne of $96 on FY2017E blended

800

capacity. We maintain our Buy rating on the stock with a target price of `744

700

based on 8.0x grey cement and 9.5x white cement FY2017 EV/EBIDTA.

600

Key Financials

500

400

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

300

Net Sales

2,904

2,782

3,337

3,661

4,613

200

% chg

1442.9

(421.8)

1998.1

971.2

2597.8

100

Net Profit

234

97

157

128

297

% chg

26.1

(58.5)

61.7

(18.5)

132.0

EPS (`)

33

14

22

18

42

Source: Company, Angel Research

P/E (x)

19.4

46.6

28.8

35.4

15.3

P/BV (x)

2.7

2.6

2.7

2.6

2.3

RoE (%)

16.9

6.4

9.8

7.5

16.0

RoCE (%)

13.3

5.8

6.9

8.3

13.6

Shrenik C. Gujrathi

EV/Sales (x)

1.9

1.9

1.9

1.7

1.3

022-39357800 Extn: 6872

EV/EBITDA (x)

9.8

14.9

14.2

11.5

7.8

Source: Company, Angel Research; Note: CMP as of November 4, 2015

Please refer to important disclosures at the end of this report

1

JK Cement | 2QFY2016 Result Update

Exhibit 1: Quarterly Performance (Standalone)

Y/E March (` cr)

2QFY2016

2QFY2015

% Chg

1QFY2016

% Chg

1HFY2016

1HFY2015

% Chg

Net sales

868

828

4.8

811

7.1

1,679

1,629

3.0

Net raw-material costs

178

161

10.4

155

14.6

340

291

16.7

(% of sales)

20.5

19.4

19.1

20.2

17.9

Power & fuel

194

198

(1.9)

179

8.6

372

392

(4.9)

(% of sales)

22.3

23.9

22.0

22.2

24.1

Staff costs

57

49

16.7

60

(4.9)

117

97

20.2

(% of sales)

6.5

5.9

7.4

6.9

6.0

Freight & forwarding

180

179

0.2

178

1.2

357

357

0.1

(% of sales)

20.7

21.7

21.9

21.3

21.9

Other expenses

153

153

(0.2)

155

(1.3)

308

306

0.9

(% of sales)

17.6

18.5

19.1

18.4

18.8

EBITDA

106

88

21.4

84

26.1

191

186

2.5

EBITDA margin

12.3

10.6

167bp

10.4

185bp

11.4

11.4

(6bp)

Interest

69

46

49.5

66

4.2

135

87

56.4

Depreciation

38

30

29.0

37

4.5

75

58

28.7

Other income

15

16

(6.9)

17

(14.2)

32

32

1.7

PBT (excl. Exp. Items)

14

28

(49.7)

(1)

13

73

(82.4)

Exp. Item

0

0

0

-

-

PBT (incl. Exp. Items)

14

28

(49.7)

(1)

13

73

(82.4)

Provision for taxation

0

(5)

(1.3)

(1)

3

(% of PBT)

1.9

(16)

114.4

(7.8)

3.8

Adjusted PAT

137

323

(57.5)

2

8,473.7

14

70

(80.3)

PATM

1.6

3.9

(232bp)

0.0

156bp

0.8

4.3

(349bp)

EPS (`)

2.0

4.6

0.0

2.0

1.0

Source: Company, Angel Research

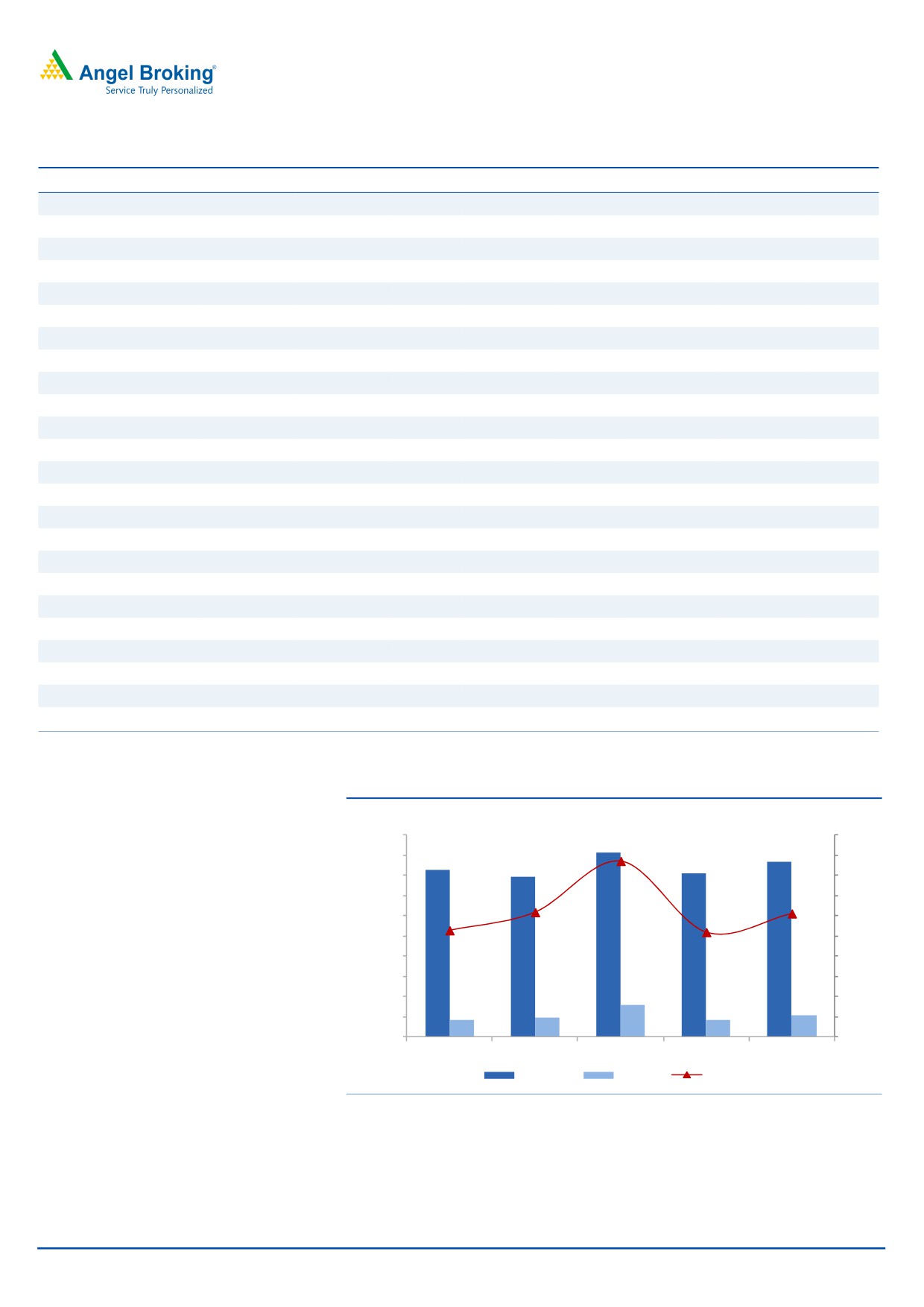

Exhibit 2: Financial performance

(` cr)

(%)

1000

20.0

911

17.5

868

900

828

18.0

797

811

800

16.0

700

14.0

600

12.4

10.4

12.3

12.0

10.6

500

10.0

400

8.0

300

6.0

159

200

4.0

99

106

88

84

100

2.0

0

0.0

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Net sales

EBITDA

EBITDAM

Source: Company, Angel Research

November 5, 2015

2

JK Cement | 2QFY2016 Result Update

Performance highlights

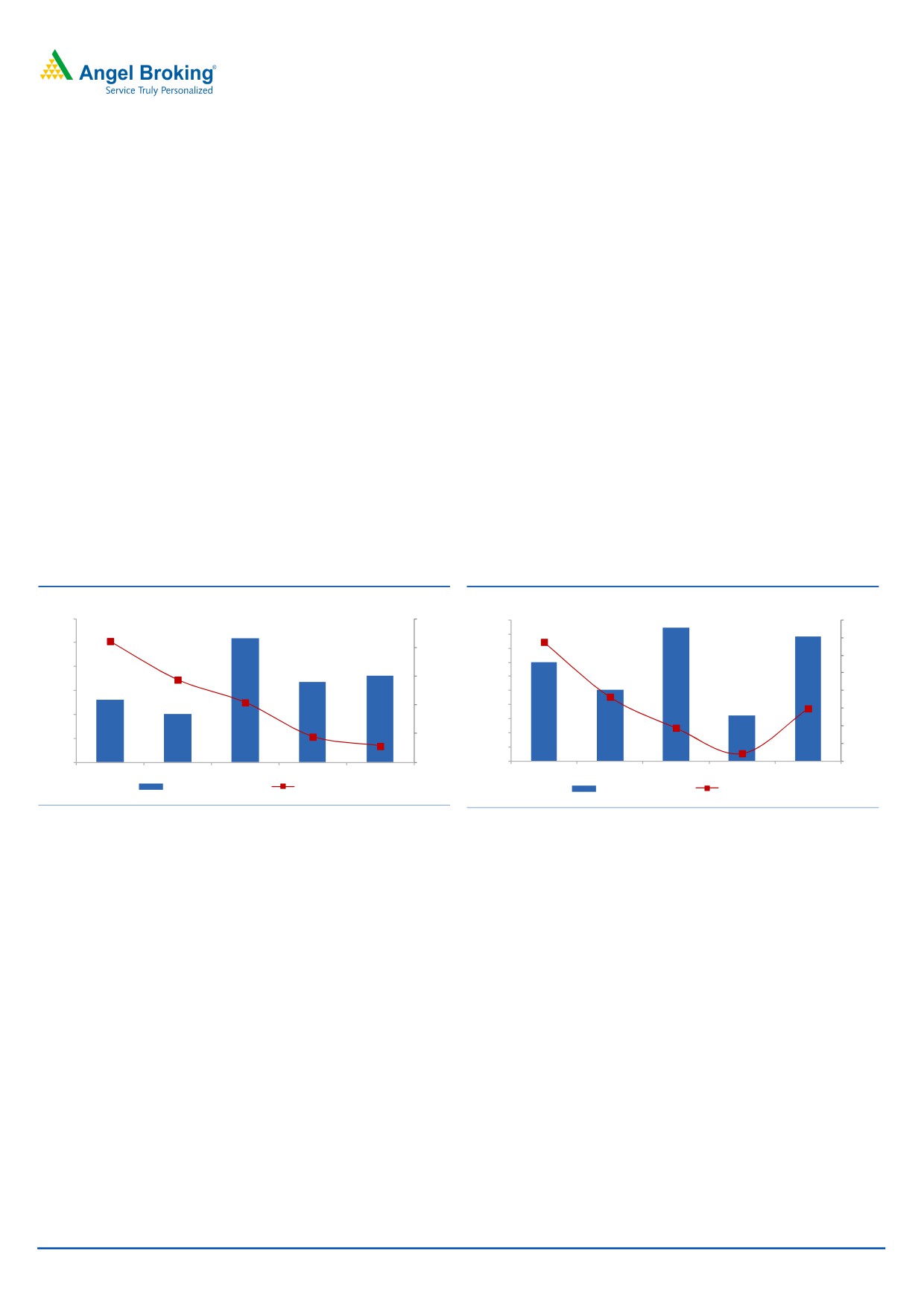

Top-line up 4.8% yoy

For 2QFY2016, JKCem posted a 4.8% yoy increase in its top-line to `867.9cr,

which is above our estimate of `832.2cr. Blended cement volumes rose by 2.8%

yoy to 1.8mn tonne (in line with our estimate), while blended realization/tonne

increased by 2.0/6.3% yoy/qoq to `4,743 (above our estimate of `4,596).

Revenue from grey cement improved by 3.4% yoy to `605cr, led by 2.8% yoy

volume growth, while realization/tonne remained flat at `3806. Muted volume

growth was due to weak demand in the North while demand pressures in

Maharashtra

((JKCem sells

60% of its south based plant’s production in

Maharashtra) impacted volumes in the South. White cement volume increased by

4.3% yoy to 0.24mn, mainly led the putty segment, which grew by 21.4% yoy to

0.12mn tonne during the quarter as against 0.13mn tonne in 2QFY2015. White

cement realization/tonne improved by 3.9% yoy to `10,934. Going forward, we

expect blended cement volume to grow at a CAGR of 12.8% over FY2015-17E.

We expect grey cement volumes to grow at a CAGR of 13.9% and white cement

volumes to grow at a CAGR of 4.3% over FY2015-2017E.

Exhibit 3: Blended Cement Volume Trend

Exhibit 4: Blended Realization Trend

(mn

tn)

(%)

(`/tonne)

(%)

1.95

25.0

4,800

4,772

12.0

1.91

4,743

21.1

4,750

10.0

1.90

9.5

20.0

4,700

4,651

8.0

1.85

1.83

4,650

14.4

6.0

1.82

15.0

4,600

1.80

1.78

4,550

4,552

4.0

10.4

3.3

1.75

10.0

4,500

4,462

2.0

2.0

1.75

4,450

4.4

(0.2)

0.0

5.0

4,400

1.70

-2.0

2.8

4,350

(3.1)

1.65

0.0

4,300

-4.0

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Blended sales volume

% change (yoy)

Blended Realization

% change (yoy)

Source: Company, Angel Research

Source: Company, Angel Research

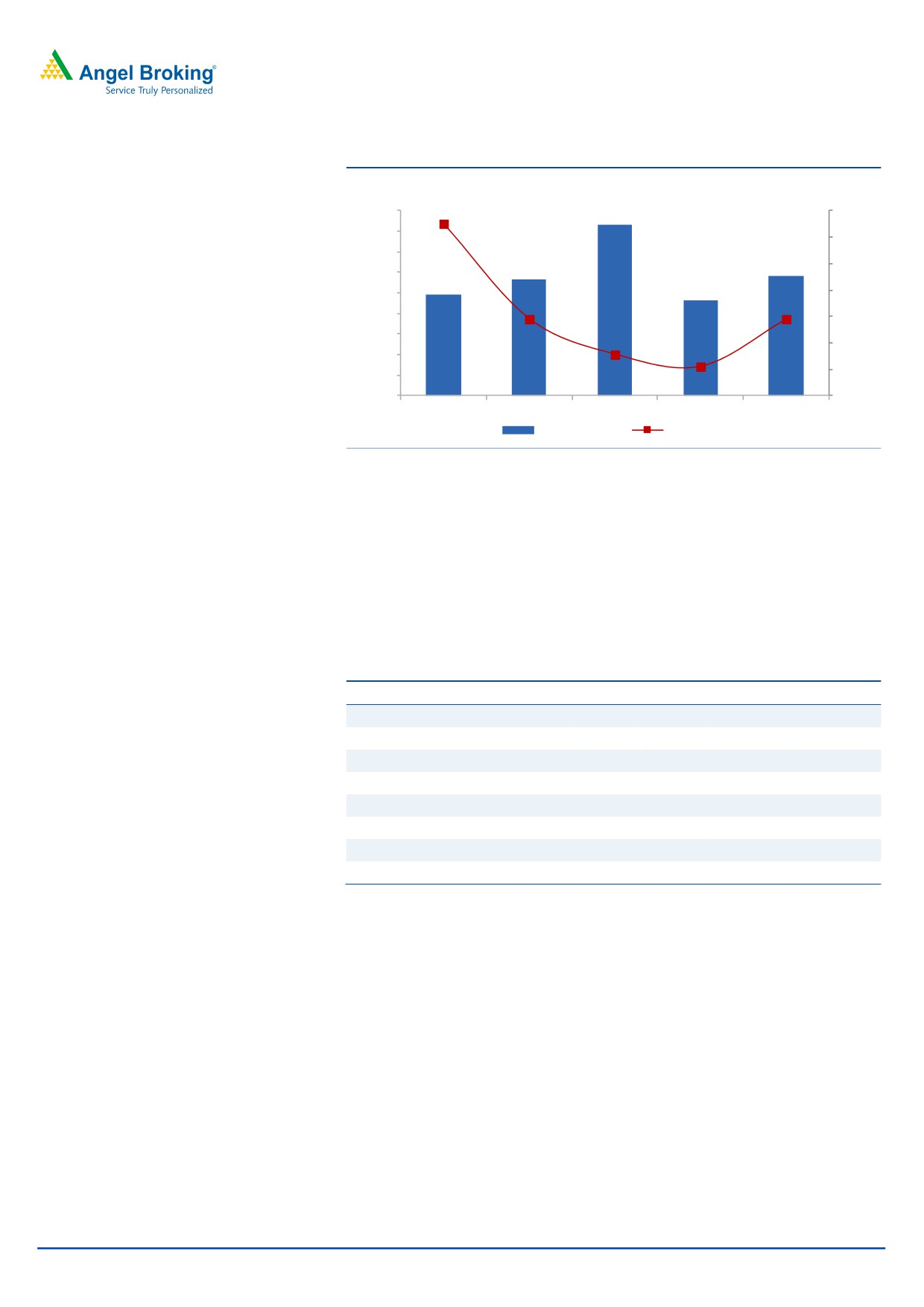

EBITDA margin improved by 167bp yoy to 12.3%

The EBITDA margin for the quarter improved by 167bp yoy to 12.3% on account

of higher realization and flat operating expenses. The company’s operating cost/

tonne remained flat yoy to `4,161, due to fall in power & fuel and freight

expenses. Thus, the blended EBITDA/tonne rose by 18.1% yoy to `581. However,

on a segmental basis, grey cement EBIDTA increased by 45.9% yoy to `40.2cr.

EBITDA/tonne increased by 42.3% yoy to `253. White cement EBIDTA grew by

10.1% yoy and came in at `66.2cr. EBIDTA/tonne for white cement grew by 5.6%

yoy to `2,758, during the quarter.

November 5, 2015

3

JK Cement | 2QFY2016 Result Update

Exhibit 5: Blended EBITDA/tonne trend

(%)

(`/tonne)

900

833

100.0

90.3

800

80.0

700

581

60.0

564

600

492

465

40.0

500

400

20.0

18.0

18.1

300

0.0

200

(8.8)

(17.9)

(20.0)

100

0

(40.0)

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

EBITDA/tonne

% change (yoy)

Source: Company, Angel Research

Per tonne analysis

During 2QFY2016, JKCem’s raw material cost/tonne increased by 2.0% yoy. The

power and fuel cost/tonne declined by 4.6% yoy. Freight cost/tonne also reduced,

ie by 2.6% yoy. However employee cost/tonne rose by 13.6% yoy to `311. The

total operating cost/tonne remained flat yoy to `4,161. The company’s operating

profit/tonne increased by 18.1% yoy to `581, during the quarter.

Exhibit 6: Per tonne analysis

Particulars (`/tonne)

2QFY16

2QFY15

1QFY16

yoy chg (%) qoq chg (%)

Net Realization/tone

4,743

4,651

4,462

2.0

6.3

Raw-Material* Cost/tone

970

903

853

7.4

13.8

Power and Fuel cost/tonne

1,059

1,110

983

(4.6)

7.8

Employee Cost/tone

311

274

329

13.6

(5.6)

Freight Cost/tone

982

1,008

977

(2.6)

0.5

Other Cost/tone

837

862

854

(2.9)

(2.0)

Operating costs/tone

4,161

4,159

3,997

0.1

4.1

Operating Profit/tone

581

492

465

18.1

25.2

Source: Company, Angel Research; Note Incl. Raw materials and purchase of stock in trade

Outlook and valuation

Going ahead, we expect the company to witness moderation in demand and

impact on profitability. The Management has also reduced its grey cement volume

guidance from 7.5mt to 6.5mt for FY16 due to soft demand. We forecast the

top-line to grow at a CAGR of 18.4% and EBIDTA to grow at CAGR of 33.3% over

FY2015-17E. At the current market price, the stock trades at 7.8x its FY2017E

EV/EBIDTA and at an EV/tonne of $96 on FY2017E blended capacity. We

maintain our Buy rating on the stock with a target price of `744, based on 8.0x

grey cement and 9.5x white cement FY2017E EV/EBIDTA.

November 5, 2015

4

JK Cement | 2QFY2016 Result Update

Company Background

JK Cement is one of the leading cement producers in India with installed grey

cement capacity of 10.5mtpa (7.5mtpa capacity is located in the North region

[Rajasthan and Haryana] and the remaining 3mtpa capacity is located in the South

region [Karnataka]). JKCem is the second largest white cement producer in India

with installed capacity of 0.6mtpa. The company also has a 0.5mtpa wall putty

capacity in Gotan, Rajasthan. It also has a 0.6mtpa white cement plant in UAE to

tap the growing Middle East and African markets. JKCem was the first company to

install a captive power plant in 1987 at Rajasthan and now it has a total power

capacity of 140MW. The company sells cement under the brands of JK Cement

and JK Super Cement.

Exhibit 7: Plant Locations

Grey Cement Capacity

Plant Location

State

Region

Capacity (MTPA)

Nimbahera

Rajasthan

North

3.25

Mangrol*

Rajasthan

North

2.25

Gotan

Rajasthan

North

0.5

Jhajjar*

Haryana

North

1.5

Muddapur

Karnataka

South

3

Total Grey Cement Capacity

10.5

White Cement Capacity

Plant Location

State

Region

Capacity (MTPA)

Gotan

Rajasthan

North

0.6

UAE

0.6

Total White Cement Capacity

1.2

Source: Company, Angel Research; Note: *New capacity (1.5mtpa at each location) added during

1HFY2015.

November 5, 2015

5

JK Cement | 2QFY2016 Result Update

Profit & Loss Statement (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

Net Sales

2,904

2,782

3,337

3,661

4,613

% chg

14.4

(4.2)

20.0

9.7

26.0

Total Expenditure

2,352

2,421

2,893

3,113

3,824

Net Raw Materials

362

425

556

607

743

Power & Fuel cost

714

674

793

866

1,050

Personnel

158

168

203

205

258

Other

1,118

1,155

1,341

1,435

1,772

EBITDA

552

361

444

549

789

% chg

8.7

(34.7)

23.1

23.6

43.8

(% of Net Sales)

19.0

13.0

13.3

15.0

17.1

Depreciation&

128

134

137

180

190

Amortisation

EBIT

424

227

307

369

599

% chg

10.9

(46.5)

35.6

20.0

62.3

(% of Net Sales)

14.6

8.1

9.2

10.1

13.0

Interest & other Charges

140

153

219

268

236

Other Income

57

62

71

59

33

(% of PBT)

16.6

45.7

44.7

37.0

8.2

Recurring PBT

341

136

159

160

395

% chg

16.0

(60.0)

16.8

0.4

147.5

Extraordinary

-

-

-

-

-

Expense/(Inc.)

PBT (reported)

341

136

159

160

395

Tax

107

39

2

32

99

(% of PBT)

31.4

28.8

1.4

20.0

25.0

PAT (reported)

234

97

157

128

297

ADJ. PAT

234

97

157

128

297

% chg

26.1

(58.5)

61.7

(18.5)

132.0

(% of Net Sales)

8.0

3.5

4.7

3.5

6.4

Basic EPS (`)

33

14

22

18

42

Fully Diluted EPS (`)

33

14

22

18

42

November 5, 2015

6

JK Cement | 2QFY2016 Result Update

Balance Sheet (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

SOURCES OF FUNDS

Equity Share Capital

70

70

70

70

70

Reserves& Surplus

1,627

1,689

1,577

1,674

1,899

Shareholders Funds

1,697

1,758

1,647

1,744

1,969

Total Loans

1,272

2,320

2,422

2,242

2,042

Deferred Tax Liability

249

268

280

280

280

Other Long term liabilities

87

97

117

117

117

Total Liabilities

3,305

4,445

4,465

4,382

4,408

APPLICATION OF FUNDS

Gross Block

3,087

3,180

4,342

4,492

4,642

Less: Acc. Depreciation

722

868

1,004

1,184

1,374

Net Block

2,364

2,313

3,338

3,308

3,268

Capital Work-in-Progress

108

1,102

191

191

191

Investments

169

300

315

315

315

Current Assets

1,261

1,389

1,504

1,348

1,492

Inventories

461

542

510

551

673

Sundry Debtors

115

112

139

153

193

Cash

332

348

408

205

184

Loans & Advances

345

373

438

430

432

Other

7

14

10

10

10

Current liabilities

597

658

883

780

858

Net Current Assets

664

731

622

569

634

Total Assets

3,305

4,445

4,465

4,382

4,408

November 5, 2015

7

JK Cement | 2QFY2016 Result Update

Cash Flow Statement (Standalone)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

Profit before tax

341

136

159

160

525

Depreciation

128

134

137

180

190

Change in Working Capital

(123)

(51)

169

(149)

(87)

Less: Other income

57

62

71

59

33

Direct taxes paid

107

39

2

32

99

Cash Flow from Operations

182

117

391

99

497

(Inc)/ Decin Fixed Assets

(209)

(1,088)

(251)

(150)

(150)

(Inc)/ Dec in Investments

(158)

(130)

(15)

-

-

Other income

57

62

71

59

33

Cash Flow from Investing

(311)

(1,156)

(195)

(91)

(117)

Issue of Equity

Inc./(Dec.) in loans

84

1,078

133

(180)

(200)

Dividend Paid (Incl. Tax)

53

25

34

31

71

Others

2

(0)

235

-

129

Cash Flow from Financing

28

1,054

(136)

(211)

(401)

Inc./(Dec.) in Cash

(100)

15

60

(203)

(21)

Opening Cash balances

433

332

348

408

205

Closing Cash balances

332

348

408

205

184

November 5, 2015

8

JK Cement | 2QFY2016 Result Update

Key Ratios (Standalone)

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

19.4

46.6

28.8

35.4

15.3

P/CEPS

12.5

19.6

15.4

14.7

9.3

P/BV

2.7

2.6

2.7

2.6

2.3

Dividend yield (%)

1.0

0.5

0.6

0.6

1.3

EV/Sales

1.9

1.9

1.9

1.7

1.3

EV/EBITDA

9.8

14.9

14.2

11.5

7.8

EV / Total Assets

1.6

1.2

1.4

1.4

1.4

Per Share Data (`)

EPS (Basic)

33.4

13.9

22.4

18.3

42.4

EPS (fully diluted)

33.4

13.9

22.4

18.3

42.4

Cash EPS

51.7

33.0

42.0

44.0

69.6

DPS

6.5

3.0

4.0

3.7

8.5

Book Value

242.7

251.5

235.5

249.3

281.6

Dupont Analysis

EBIT margin

14.6

8.1

9.2

10.1

13.0

Tax retention ratio

68.6

71.2

98.6

80.0

75.0

Asset turnover (x)

1.0

0.8

0.8

0.9

1.1

ROIC (Post-tax)

10.4

4.6

7.4

7.2

10.7

Cost of Debt (Post Tax)

7.7

6.0

9.1

9.2

8.3

Leverage (x)

0.5

0.7

1.0

1.0

0.9

Operating ROE

11.7

3.5

5.8

5.1

12.8

Returns (%)

ROCE (Pre-tax)

13.3

5.8

6.9

8.3

13.6

Angel ROIC (Pre-tax)

16.2

8.4

9.8

10.2

16.2

ROE

16.9

6.4

9.8

7.5

16.0

Turnover ratios (x)

Asset Turnover (Gross Block)

1.0

0.9

0.9

0.8

1.0

Inventory / Sales (days)

52

66

58

53

48

Receivables (days)

13

15

14

15

14

Payables (days)

87

95

97

97

78

WC cycle (ex-cash) (days)

34

47

33

29

32

Solvency ratios (x)

Net debt to equity

0.5

1.0

1.0

1.0

0.8

Net debt to EBITDA

1.4

4.6

3.8

3.1

2.0

Interest Coverage (EBIT / Int.)

3.0

1.5

1.4

1.4

2.5

November 5, 2015

9

JK Cement | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

JK Cement

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 5, 2015

10