2QFY2016 Result Update | Oil&Gas

November 5, 2015

Indian Oil Corporation

ACCUMULATE

CMP

`410

Performance Highlights

Target Price

`455

Standalone (` cr)

2QFY16

2QFY15

yoy (%)

1QFY16

qoq%

Investment Period

12 months

Total Revenue

85,385

1,11,664

(23.5)

1,01,307

(15.7)

EBITDA

695

(356)

(295.1)

10,101

(93.1)

Stock Info

Margin (%)

0.8

(0.3)

113bp

10.0

(916)bp

Sector

Oil&Gas

Reported PAT

(329)

(898)

(63.4)

6,436

0.0

Market Cap (` cr)

99,607

Source: Company, Angel Research

Net Debt (` cr)

48,349

Indian Oil Corporation (IOCL)’s 2QFY2016 revenue came in 2.4% ahead of our

Beta

0.7

estimate at `85,385cr, led by a 5.8% yoy increase in product sales volumes to

52 Week High / Low

465 / 307

19.07MMT as against 18.03MMT in 2QFY2015. Refining throughput increased

Avg. Daily Volume

8,69,14,736

2.1% to 13.68MMT as against 13.41MMT in 2QFY2015, while total throughput

Face Value (`)

10

increased 5% yoy to 19.98MMT as against 19.04MMT in 2QFY2015. Revenue

BSE Sensex

26,553

however declined 24% yoy on account of lower price realisations. The EBITDA at

Nifty

8,040

`695cr was much lower than our expectation of `3,714cr, owing to lower than

Reuters Code

IOC.BO

expected refining margins and high inventory losses. Refining margin at $0.9/bbl

Bloomberg Code

IOCL IN

was much lower than our expectation and compared to $10.8/bbl as in

1QFY2016. This was largely on account of reduced spreads and adventitious loss

of `1,197cr. We expect the impact from inventory losses to reduce going forward

Shareholding Pattern (%)

and profit to stabilise as crude prices stabilise at current levels.

Promoters

58.6

MF / Banks / Indian Fls

13.6

The commissioning of its state-of-the-art 15MMTPA coastal refinery at Paradip is

FII / NRIs / OCBs

3.3

expected to be fully operational in an integrated manner by Dec 2015. With its

Indian Public / Others

24.6

commissioning, IOCL’s refining capacity is set to increase by

~23% to

80.7MMTPA from the current capacity of 65.7MMTPA.

Outlook and valuation

Abs. (%)

3m 1yr

3yr

IOC is currently trading at an EV/EBITDA multiple of 5.4x its FY2017E EBITDA

Sensex

(5.4)

(4.7)

41.6

and 8.4x FY2017E EPS of `48.7. Lower oil prices resulting in significant reduction

IOCL

(3.5)

12.4

56.7

in under recoveries, expected improvements in refining margins and IOCL’s reach

make it a structural play on the refining sector. We apply a 6x multiple on its

3-year price chart

FY2017E EBITDA to arrive at our price target of `455 and retain our Accumulate

520

rating on the stock.

470

420

Key financials (Consolidated)

370

320

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

270

Net sales

4,66,837

4,94,528

4,49,509

3,59,607

4,02,760

220

170

% chg

12.9

5.9

(9.1)

(20.0)

12.0

120

Adj. net profit

4,427

5,976

3,753

10,308

11,831

70

% chg

(58.5)

35.0

(37.2)

174.6

14.8

Adj. EPS (`)

18.2

24.6

15.5

42.5

48.7

OPM (%)

3.0

3.5

2.3

5.9

6.1

Source: Company, Angel Research

P/E (x)

22.4

14.0

20.3

9.7

8.4

P/BV (x)

1.6

1.5

1.4

1.3

1.1

RoE (%)

5.9

10.6

7.1

14.1

14.3

RoCE (%)

5.5

6.8

3.6

11.6

12.7

Rahul Dholam

EV/Sales (x)

0.4

0.4

0.3

0.4

0.3

Tel: 022- 3935 7800 Ext: 6847

EV/EBIDTA

12.4

10.3

13.4

6.6

5.4

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Indian Oil Corporation | 2QFY2016 Result Update

Exhibit 1: 2QFY2016 performance (Standalone)

(` cr)

2QFY16

2QFY15

yoy%

1QFY16

qoq%

FY2015

FY2014

yoy%

Net Sales

85,115

1,11,305

(23.5)

1,01,009

(15.7)

4,32,330

4,54,985

(5.0)

Other Operating Income

270

359

(24.8)

298

(9.4)

17,178

39,543

(56.6)

Total Revenue

85,385

1,11,664

(23.5)

1,01,307

(15.7)

4,49,509

4,94,528

(9.1)

Material Expenses

74,233

1,02,676

(27.7)

81,889

(9.3)

3,99,121

4,32,808

(7.8)

% of net sales

86.9

92.0

80.8

88.8

87.5

Employee Cost

1,628

1,576

3.3

2,362

(31.1)

7,662

7,137

7.4

% of net sales

1.9

1.4

2.3

1.7

1.4

Other Expenses

8,829

7,768

13.7

6,956

26.9

32,189

37,490

(14.1)

% of net sales

10.3

7.0

6.9

7.2

7.6

Total expenditure

84,690

1,12,020

(24.4)

91,206

(7.1)

4,38,973

4,77,435

(8.1)

% of net sales

99.2

100.3

90.0

97.7

96.5

EBITDA

695

(356)

10,101

(93.1)

10,536

17,094

(38.4)

Margin (%)

0.8

-0.3

10.0

(916bp)

2.3

3.5

(264bp)

Interest

729

1,039

(29.8)

592

23.2

4,175

5,948

(29.8)

Depreciation

1,129

730

54.6

1,143

(1.3)

5,219

6,360

(17.9)

Other income

1,003

847

18.3

835

20.1

5,872

5,192

13.1

Exceptional items

0

0

0

0

0

Profit before tax

(160)

(1,278)

9,200

7,014

9,978

(29.7)

% of net sales

(0.2)

(1.1)

9.1

1.6

2.0

Tax

169

(380)

2,764

2,143

3,011

(28.8)

% of PBT

NM

29.7

30.0

30.5

30.2

Net Profit

(329)

(898)

6,436

4,872

6,967

(30.1)

Adj Net Profit

(326)

(1,289)

6,105

3,753

5,976

(37.2)

Source: Company, Angel Research

Exhibit 2: Standalone - 2QFY2016 Actual vs. estimates

(` cr)

Actual

Estimates

Variation (%)

Revenue

85,385

83,364

2.4

EBITDA

695

3,714

(81.3)

EBITDA margin (%)

0.8

4.5

(364bp)

Net Profit

(329)

1,614

NM

Source: Company, Angel Research

Result highlights

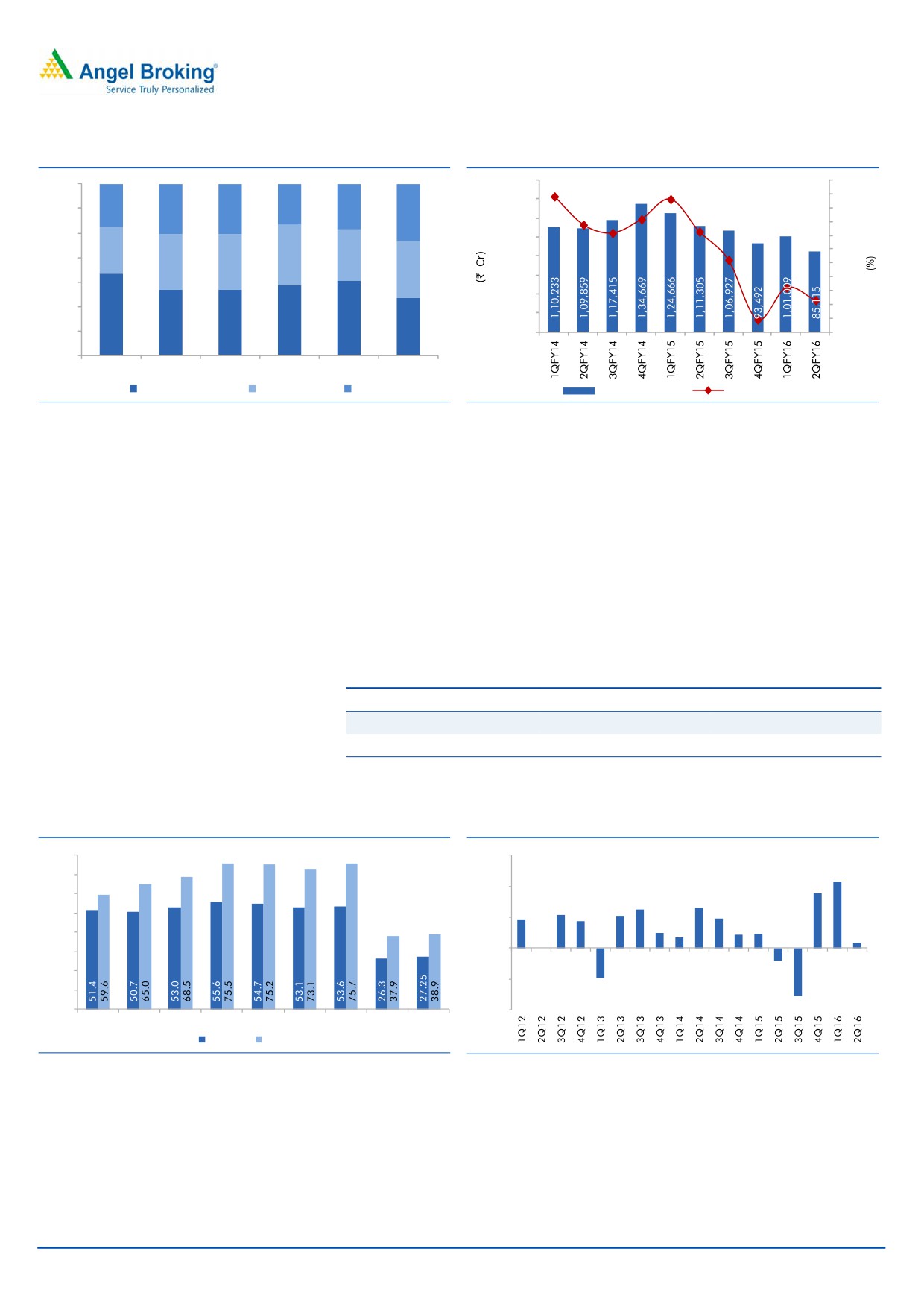

Revenue growth in line with expectation

IOCL’s 2QFY2016 revenue came in 2.4% ahead of estimate at `85,385, led by a

5.8% increase in product sales volumes to 19.07MMT as against 18.03MMT in

2QFY2015. Refining throughput increased

2.1% to

13.68MMT as against

13.41MMT in 2QFY2015, while total throughput increased 5% to 19.98MMT as

against 19.04MMT in 2QFY2015. Revenue however declined 24% yoy on account

of lower price realisations.

November 5, 2015

2

Indian Oil Corporation | 2QFY2016 Result Update

Exhibit 3: Revenue mix

Exhibit 4: :Lower realisations impact revenue

20

1,60,000

100%

15

1,40,000

3.5%

3.4%

3.7%

98%

4.1%

4.0%

4.7%

10

1,20,000

5

96%

1,00,000

0

3.9%

-5

94%

4.9%

4.2%

80,000

4.6%

4.6%

-10

4.6%

60,000

-15

92%

40,000

-20

90%

-25

93%

20,000

92%

-30

91%

91%

92%

88%

91%

-

-35

86%

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Petroleum Revenue

Petrochemicals

Other Revenue

Net Sales (` Cr)

yoy change (%)

Source: Company, Angel Research

Source: Company, Angel Research

EBITDA decline led by inventory losses

IOCL reported an EBITDA of `695cr, much lower than our expectation of

`3,714cr, owing to lower than expected refining margins and high inventory

losses. Refining margin at $0.9/bbl was much lower than our expectation and

compared to $10.8/bbl as in 1QFY2016. This was largely on account of reduced

spreads and adventitious loss of `1,197cr. We expect the impact from inventory

losses to reduce going forward and profit to stabilise as crude prices stabilise at

current levels.

Exhibit 5: Refining Margins

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

IOC Refining Margin

2.3

(2)

(7.7)

8.8

10.8

0.9

Singapore GRM ($ / bbl)

5.8

4.8

6.3

8.6

8.0

6.3

Source: Company, Angel Research

Exhibit 6: Throughput volumes remain stable

Exhibit 7: Weak refining margins this quarter

15.0

80.0

10.8

70.0

8.8

10.0

60.0

6.6

6.2

5.3

5.2

4.7

4.3

4.8

50.0

5.0

2.4

1.7

2.2

2.3

40.0

0.9

0.0

0.0

30.0

20.0

(2.0)

(5.0)

10.0

(4.8)

-

(10.0)

(7.7)

FY09

FY10

FY11

FY12

FY13

FY14

FY15

1H15

1H16

Refineries Pipelines

Source: Company, Angel Research

Source: Company, Angel Research

November 5, 2015

3

Indian Oil Corporation | 2QFY2016 Result Update

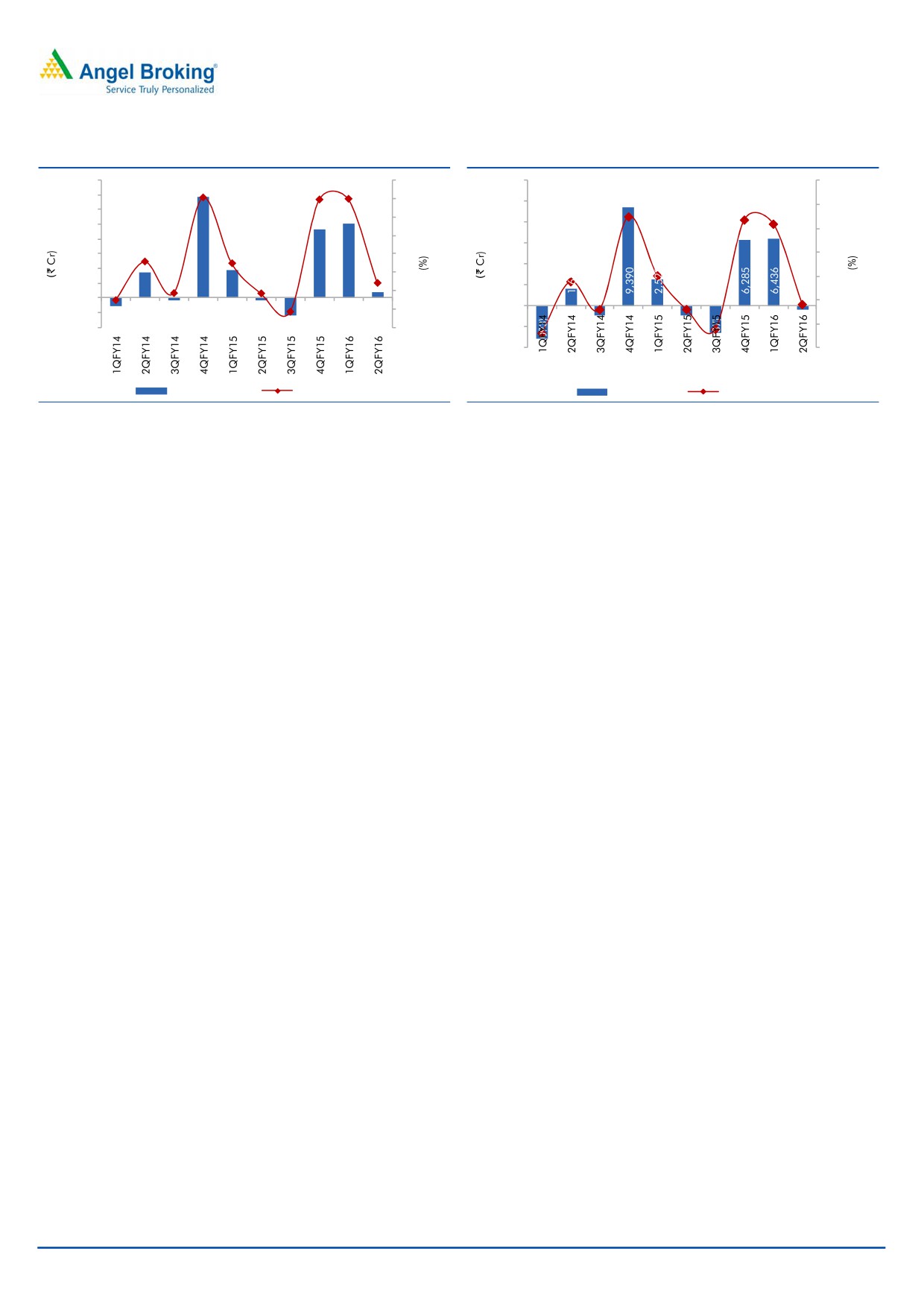

Exhibit 8: EBITDA margin declines to 0.8%

Exhibit 9: Net loss led by inventory losses

16,000

12

12,000

10

14,000

10

10,000

8

12,000

8

10,000

8,000

6

8,000

6

6,000

6,000

4

4

4,000

4,000

2

2

2,000

2,000

0

-

0

-2

-

(2,000)

(4,000)

-4

(2,000)

-2

(4,000)

-4

EBITDA (` Cr)

Margin (%)

PAT (` Cr)

Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

November 5, 2015

4

Indian Oil Corporation | 2QFY2016 Result Update

Investment arguments

Lower oil prices and government reforms transform OMCs into

structural plays

Lower oil prices coupled with oil & gas reforms are resulting in reduced net under

recoveries, higher margins and lower working capital requirements for oil

marketing companies (OMCs). Brent crude oil prices have declined significantly

over the last one year and this has resulted in significant reduction in gross under

recoveries. Gross under recoveries stood at a mere `4,793cr in the first half of this

fiscal as against `27,543cr in 1HFY2015. We expect oil prices to remain near

current levels, with pressure from US shale suppliers changing the dynamics of the

global oil industry. This will help the OMCs to keep their net under recoveries to a

minimum, enabling stable profitability.

Exhibit 10: Under recoveries almost eliminated

FY10

FY11

FY12

FY13

FY14

FY15

1H15

1H16

Gross Under Recovery

25,879

43,112

75,127

85,793

72,938

39,758

27,543

4,793

Sharing:

Upstream discount

7,548

16,704

29,619

31,967

34,674

23,597

17,205

1,340

Budgetary Support

15,172

22,605

45,486

53,278

37,182

14,960

9,161

3,448

Net Under Recovery

3,159

3,803

22

548

1,083

1,201

1,177

4

% of Gross Under Recovery

12.2%

8.8%

0.0%

0.6%

1.5%

3.0%

4.3%

0.1%

Source: Company, Angel Research

IOCL’s net under recoveries have also reduced, led by oil sector reforms such as

auto fuel deregulation and direct benefit transfer for LPG subsidies. Net under

recoveries for IOCL have reduced from ~12% in FY2010 to 3% in FY2015 and

0.1% in 1HFY2016. With oil prices under pressure, political interference to

regulate prices of auto fuels will remain low. We also expect stable oil prices to

minimize inventory losses going forward.

Paradip refinery to drive refining segment revenues

IOCL began the commissioning of its state-of-the-art 15 MMTPA coastal refinery at

Paradip in March 2015. The refinery is expected to be fully operational in an

integrated manner by Dec 2015. With its commissioning, IOCL’s refining capacity

is set to increase by

~23% to 80.7MMTPA from the current capacity of

65.7MMTPA. We expect throughput and refining revenues to increase in line with

increase in capacity.

The refinery, built at a cost of more than US$5bn, is one of the most modern

refineries in the world and categorized among the best refineries worldwide across

major performance parameters such as distillate yield, complexity factor and

energy consumption. With a nelson complexity of 12.2, it is designed to process a

broad range of crude, including heavy and high sulfur heavy crudes, along with

the capability to produce futuristic Euro-V standard fuels. Led by the increase in

marketing and refining margins, we expect IOCL to report a 380bp improvement

in EBITDA margin over FY2015-FY2017E.

November 5, 2015

5

Indian Oil Corporation | 2QFY2016 Result Update

Outlook and valuation

IOC is currently trading at an EV/EBITDA multiple of 5.4x its FY2017E EBITDA and

8.4x FY2017E EPS of `48.7. Lower oil prices resulting in significant reduction in

under recoveries, expected improvements in refining margins and IOCL’s reach

make it a structural play on the refining sector. We apply a 6x multiple on its

FY2017E EBITDA to arrive at our price target of `455 and retain our Accumulate

rating on the stock.

Exhibit 11: Valuation

` Cr

FY2017E Consolidated EBITDA

24,707

Multiple (x)

6

Total EV

1,48,243

Net Debt

50,084

Investments (0.8x BV)

12,855

Minority Interest

993

Equity Value

1,10,021

Target Price

455

Source: Company, Angel Research

Company background

Incorporated in 1959, Indian Oil Corporation Ltd (IOCL) is India’s leading oil

refiner with a capacity of 65.7MMTPA (31% market share). It is also the country’s

largest oil marketing company with a 42% market share and a pipeline network of

over 11,000km. IOCL is a ‘Maharatna’ company and is ranked 96th in the Fortune

Global 500 Company rankings.

November 5, 2015

6

Indian Oil Corporation | 2QFY2016 Result Update

Profit & loss statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

Net Sales

4,66,837

4,94,528

4,49,509

3,59,607

4,02,760

% chg

12.9

5.9

(9.1)

(20.0)

12.0

Total Expenditure

4,52,945

4,77,435

4,38,973

3,38,266

3,78,053

Net Raw Materials

4,14,541

4,32,808

3,99,121

3,06,385

3,42,346

Other Mfg costs

30,620

37,490

32,189

25,751

28,841

Personnel

7,784

7,137

7,662

6,130

6,866

Other

-

-

-

-

-

EBITDA

13,892

17,094

10,536

21,341

24,707

% chg

17.8

23.0

(38.4)

102.6

15.8

(% of Net Sales)

3.0

3.5

2.3

5.9

6.1

Depreciation& Amort.

5,692

6,360

5,219

6,050

7,050

EBIT

8,201

10,734

5,317

15,291

17,657

% chg

26.4

30.9

(50.5)

187.6

15.5

(% of Net Sales)

1.8

2.2

1.2

4.3

4.4

Interest & other Charges

7,165

5,948

4,175

3,489

3,618

Other Income

3,468

5,192

5,872

3,523

3,558

Share in profit of Asso.

-

-

-

-

-

Profit before tax

4,504

9,978

7,014

15,325

17,598

% chg

12.7

121.5

(29.7)

118.5

14.8

Tax

877

3,011

2,143

5,057

5,807

(% of PBT)

19.5

30.2

30.5

33.0

33.0

PAT (reported)

3,627

6,967

4,872

10,268

11,791

Minority Interest

(822)

(119)

(40)

(40)

(40)

Net Profit

4,449

7,086

4,912

10,308

11,831

Adjusted Profit

4,427

5,976

3,753

10,308

11,831

% chg

(58.5)

35.0

(37.2)

174.6

14.8

(% of Net Sales)

0.9

1.2

0.8

2.9

2.9

November 5, 2015

7

Indian Oil Corporation | 2QFY2016 Result Update

Balance sheet (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

SOURCES OF FUNDS

Equity Share Capital

2,428

2,428

2,428

2,428

2,428

Reserves & Surplus

60,609

65,485

66,404

74,789

84,697

Shareholders Funds

63,037

67,913

68,832

77,217

87,125

Minority Interest

1,262

1,171

1,073

1,033

993

Total Loans

89,671

94,916

58,154

58,154

53,154

Deferred Tax Liability

6,332

6,423

6,836

6,836

6,836

Other Long term liabilities

11,874

14,135

15,930

16,408

16,900

Total Liabilities

1,72,176

1,84,557

1,50,826

1,59,648

1,65,008

APPLICATION OF FUNDS

Gross Block

1,15,182

1,26,982

1,38,745

1,63,745

1,88,745

Less: Acc. Depreciation

48,408

54,427

59,646

65,696

72,746

Net Block

66,774

72,554

79,098

98,048

1,15,998

Capital Work-in-Progress

27,240

38,061

38,061

22,837

7,993

Goodwill

0

0

0

0

0

Investments

17,351

15,895

16,069

16,069

16,069

Current Assets

1,23,880

1,34,003

93,778

87,682

96,248

Cash

1,220

3,705

1,221

1,502

3,070

Inventory

66,758

72,505

49,917

49,686

54,038

Debtors

12,502

12,552

7,645

7,725

7,724

Other

43,400

45,241

34,995

28,769

31,415

Current liabilities

69,702

82,254

82,870

71,810

78,259

Net Current Assets

54,177

51,749

10,909

15,871

17,989

Other Assets

6,633.8

6,297.5

6,689.4

6,823.2

6,959.6

Total Assets

1,72,176

1,84,557

1,50,826

1,59,648

1,65,008

November 5, 2015

8

Indian Oil Corporation | 2QFY2016 Result Update

Cash flow statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

Profit before tax

4,504

9,978

7,014

15,325

17,598

Depreciation

5,710

6,369

5,219

6,050

7,050

Change in Working Capital

(4,453)

5,451

28,111

(10,908)

2,097

Others

4,747

4,302

14,324

10,060

1,327

Direct taxes paid

(1,169)

(1,896)

(1,730)

(5,057)

(5,807)

Cash Flow from Operations

9,339

24,204

52,939

15,469

22,265

(Inc.)/ Dec. in Fixed Assets

(12,289)

(21,424)

(11,763)

(9,776)

(10,156)

(Inc.)/ Dec. in Investments

899

931

(174)

0

0

Share of profit/ (loss) from asso.

2,096

1,899

0

0

0

Cash Flow from Investing

(9,294)

(18,594)

(11,936)

(9,776)

(10,156)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

9,668.1

5,597.5

(36,761.8)

-

(5,000.0)

Dividend Paid (Incl. Tax)

(1,492.2)

(1,850.1)

(2,549.7)

(1,923.0)

(1,923.0)

Others

(7,824.0)

(6,872.2)

(4,174.6)

(3,489.2)

(3,617.5)

Cash Flow from Financing

352

(3,125)

(43,486)

(5,412)

(10,541)

Inc./(Dec.) in Cash

398

2,485

(2,483)

281

1,568

Opening Cash balances

822

1,220

3,705

1,221

1,502

Closing Cash balances

1,220

3,705

1,221

1,502

3,070

November 5, 2015

9

Indian Oil Corporation | 2QFY2016 Result Update

Key Ratios (Consolidated)

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

Per Share Data (`)

Reported EPS

18.3

29.2

20.2

42.5

48.7

Adjusted EPS

18.2

24.6

15.5

42.5

48.7

Cash EPS

41.8

55.4

41.7

67.4

77.8

DPS

6.2

8.7

6.6

6.6

6.6

Book Value

259.6

279.7

283.5

318.0

358.8

Valuation Ratio (x)

P/E (on FDEPS)

22.4

14.0

20.3

9.7

8.4

P/CEPS

9.8

7.4

9.8

6.1

5.3

P/BV

1.6

1.5

1.4

1.3

1.1

Dividend yield (%)

1.5

2.1

1.6

1.6

1.6

EV/Sales

0.4

0.4

0.3

0.4

0.3

EV/EBITDA

12.4

10.3

13.4

6.6

5.4

EV/Total Assets

1.0

1.0

0.9

0.9

0.8

Returns (%)

ROCE

5.5

6.8

3.6

11.6

12.7

ROE

5.9

10.6

7.1

14.1

14.3

Turnover ratios (x)

Asset Turnover (Gross Block)

4.2

4.1

3.4

2.4

2.3

Inventory (days)

51.1

51.4

49.7

50.5

47.0

Receivables (days)

9.4

9.2

8.2

7.8

7.0

Payables (days)

51.2

56.1

67.0

78.5

68.0

WC cycle (ex-cash) (days)

40.0

37.3

23.4

12.2

13.3

Solvency ratios (x)

Net debt to equity

1.4

1.3

0.8

0.7

0.6

Net debt to EBITDA

1.0

1.0

1.0

1.0

0.9

Interest Coverage (EBIT / Int.)

1.1

1.8

1.3

4.4

4.9

November 5, 2015

10

Indian Oil Corporation | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Indian Oil Corporation

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 5, 2015

11