4QFY2016 Result Update | FMCG

May 23, 2016

ITC

BUY

CMP

`330

Performance Highlights

Target Price

`380

Quarterly result (Standalone)

Investment Period

12 Months

(` cr)

4QFY16

4QFY15

% chg

3QFY16

% qoq

Revenue

10,169

9,293

9.4

9,177

10.8

Stock Info

Sector

FMCG

EBITDA

3,687

3,243

13.7

3,605

2.3

Market Cap (` cr)

2,65,518

OPM (%)

36.3

34.9

136bp

39.3

(303bp)

Net Debt (` cr)

-15,928

PAT

2,495

2,361

5.7

2,653

(5.9)

Beta

0.8

Source: Company, Angel Research

52 Week High / Low

360/268

ITC posted a healthy set of numbers for 4QFY2016, both on the top-line and the

Avg. Daily Volume

6,90,195

bottom-line front. The top-line was strong due to higher growth in Cigarettes &

Face Value (`)

1

Agri businesses; however, higher taxes slightly dragged down the overall

BSE Sensex

25,302

profitability of the company.

Nifty

7,750

Reuters Code

ITC.BO

Key highlights: ITC’s net sales for the quarter grew by 9.4% yoy to `10,169cr. The

Bloomberg Code

ITC@IN

Cigarettes business posted a 10.2% yoy growth in net sales to `4,639cr, aided by

price hikes, which enabled an 11.5% yoy growth in the segment’s EBIT. The

FMCG (Others) business posted a 5.4% yoy growth in net sales to `2,704cr, and

Shareholding Pattern (%)

an EBIT level profit of `71cr. Further, the Paperboards and Packaging division

Promoters

0.0

posted a growth of 3.0% yoy and 6.5% yoy in revenue and EBIT, respectively. The

MF / Banks / Indian Fls

38.7

Hotels business posted a 4.8% yoy growth in its top-line, while it reported a flat

FII / NRIs / OCBs

51.2

growth at the EBIT level. The Agri business posted a strong growth of 26.5% yoy

Indian Public / Others

10.1

in revenue, while its EBIT grew by 6.1% on a yoy basis. Overall, the company’s

OPM expanded by 136bp yoy to 36.3%, owing to reduction in overall operating

Abs. (%)

3m

1yr

3yr

expenses.

Sensex

6.7

(9.1)

25.8

Outlook and valuation: We expect ITC to report a top-line and bottom-line CAGR

ITC

8.2

(0.8)

6.9

of 8.3% and 9.3% respectively over FY2016-18E. At the current market price, the

stock is trading at 22.6x FY2018E EPS. We recommend a Buy on the stock with a

3-year price chart

target price of `380.

410

390

Key financials (Standalone)

370

Y/E March (` cr)

FY2015

FY2016E

FY2017E

FY2018E

350

330

Net Sales

36,507

36,837

39,726

43,194

310

% chg

9.8

0.9

7.8

8.7

290

270

Net Profit (Adj)

9,608

9,845

10,844

11,754

250

% chg

9.4

2.5

10.2

8.4

EBITDA (%)

36.9

38.7

38.8

38.8

Source: Company, Angel Research

EPS (`)

11.9

12.2

13.5

14.6

P/E (x)

27.6

27.0

24.5

22.6

P/BV (x)

8.7

7.5

6.6

5.8

RoE (%)

31.3

27.8

26.9

25.7

RoCE (%)

40.6

37.3

35.4

33.8

Amarjeet S Maurya

EV/Sales (x)

6.8

6.7

6.2

5.6

022 - 3935 7800 Ext: 6831

EV/EBITDA (x)

18.5

17.3

15.9

14.6

Source: Company, Angel Research; Note: CMP as of May 20, 2016

Please refer to important disclosures at the end of this report

1

ITC | 4QFY2016 Result Update

Exhibit 1: Quarterly performance (Standalone)

Y/E March (` cr)

4QFY16

4QFY15

% yoy

3QFY16

%qoq

FY2016

FY2015

% chg

Net Sales

10,169

9,293

9.4

9,177

10.8

36,837

36,507

0.9

Consumption of RM

3,980

3,662

8.7

3,336

19.3

13,703

14,672

(6.6)

(% of Sales)

39.14

39.40

36.35

37.2

40.2

Staff Costs

465

454

2.4

450

3.5

1,884

1,780

5.8

(% of Sales)

4.6

4.9

4.9

5.1

4.9

Other Expenses

2,037

1,934

5.3

1,786

14.0

7,013

6,582

6.5

(% of Sales)

20.0

20.8

19.5

19.0

18.0

Total Expenditure

6,482

6,050

7.1

5,572

16.3

22,599

23,034

(1.9)

Operating Profit

3,687

3,243

13.7

3,605

2.3

14,238

13,474

5.7

OPM

36.3

34.9

136

39.3

(303)

38.7

36.9

174.5

Interest

12

16

(20.9)

16

(23.7)

49

57

(14.4)

Depreciation & Amortization

255

250

2.1

263

(2.9)

1,034

962

7.6

Other Income

412

370

11.1

678

(39.3)

1,804

1,543

16.9

PBT (excl. Extraordinary Items)

3,832

3,348

14.4

4,004

(4.3)

14,958

13,998

6.9

Extraordinary Income/(Expense)

-

-

-

-

PBT (incl. Extraordinary Items)

3,832

3,348

14.4

4,004

(4.3)

14,958

13,998

6.9

(% of Sales)

37.7

36.0

43.6

40.6

38.3

Provision for Taxation

1,336

987

35.4

1,352

(1.1)

5,114

4,390

16.5

(% of PBT)

34.9

29.5

33.8

34.2

31.4

Reported PAT

2,495

2,361

5.7

2,653

(5.9)

9,845

9,608

2.5

PATM

25

25

29

27

26

EPS (`)

3.1

2.9

5.7

3.3

(5.9)

12.3

12.0

2.5

Source: Company, Angel Research

May 23, 2016

2

ITC | 4QFY2016 Result Update

Top-line remains healthy

ITC’s net sales for the quarter grew by 9.4% yoy to `10,169cr. The Cigarettes

business posted a 10.2% yoy growth in net sales to `4,639cr, aided by price hikes,

which enabled an 11.5% yoy growth in the segment’s EBIT. The FMCG (Others)

business posted a 5.4% yoy growth in net sales to `2,704cr, and an EBIT level

profit of `71cr. Further, the Paperboards and Packaging division posted a growth

of 3.0% yoy and 6.5% yoy in revenue and EBIT, respectively. The Hotels business

posted a 4.8% yoy growth in its top-line, while it reported a flat growth at the EBIT

level. The Agri business posted a strong growth of 26.5% yoy in revenue, while its

EBIT grew by 6.1% on a yoy basis.

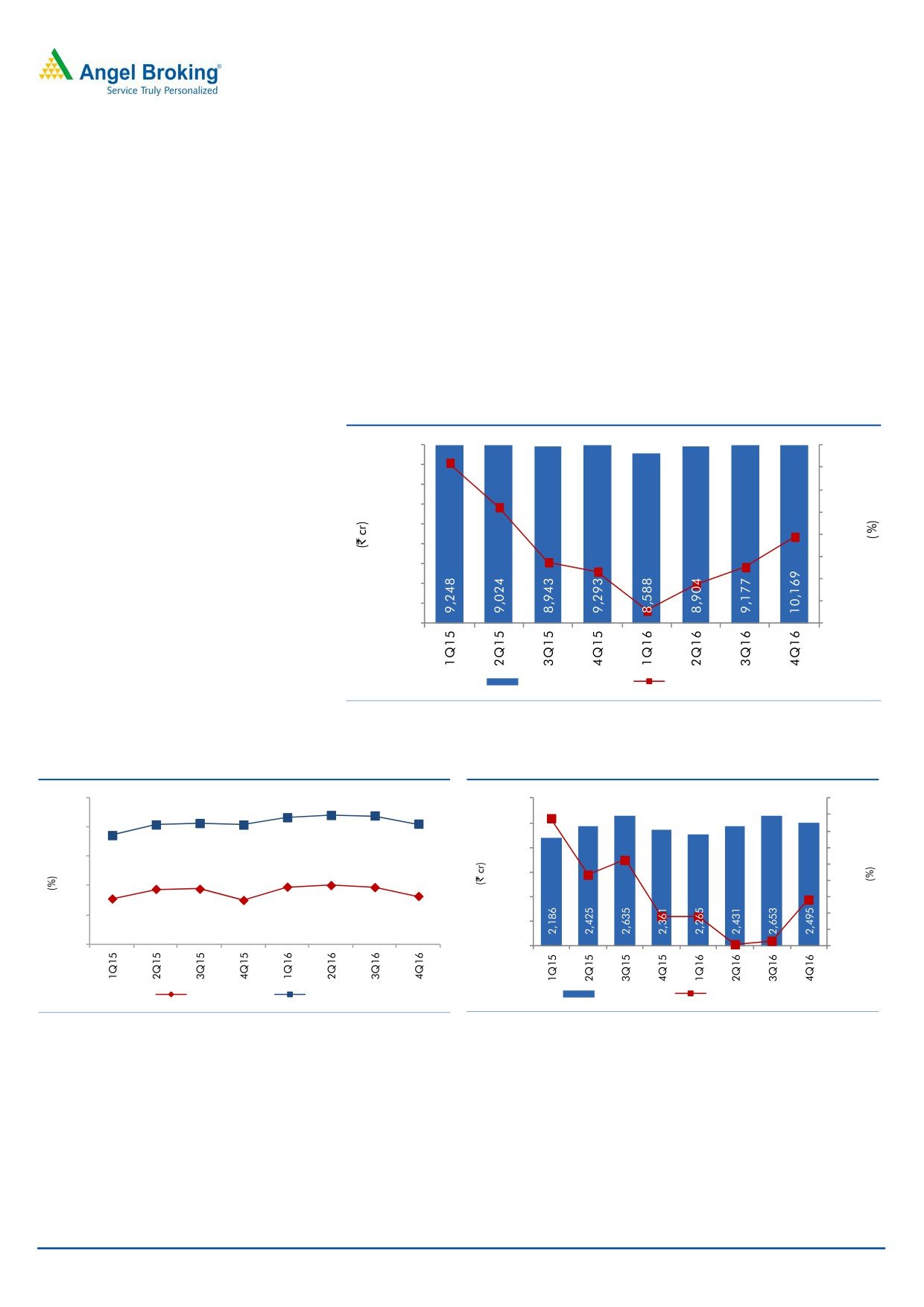

Exhibit 2: Top-line grows 9.4% yoy

9,000

30.0

8,000

25.0

7,000

20.0

6,000

15.0

5,000

10.0

4,000

5.0

3,000

-

2,000

1,000

(5.0)

-

(10.0)

Top-line (LHS)

yoy growth (RHS)

Source: Company, Angel Research

Exhibit 3: OPM increases by 136bp yoy to 36.3%

Exhibit 4: Earnings grow 5.7% yoy

70

63.1

63.9

63.7

3,000

15.6

18.0

60.6

61.1

60.6

60.9

57

16.0

2,500

60

14.0

10.5

2,000

5.7

12.0

50

8.7

10.0

38.7

38.7

39.4

40.0

39.3

1,500

35.4

34.9

36.3

8.0

40

3.6

0.3

3.7

0.7

1,000

6.0

30

4.0

500

2.0

20

-

-

OPM

Gross margin

PAT (LHS)

yoy growth (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

Operating profit up 13.7% yoy

The company reported an operating profit of `3,687cr for 4QFY2016, up

13.7% yoy. Further, the company’s OPM expanded by 136bp yoy to 36.3%, owing

to reduction in overall operating expenses.

May 23, 2016

3

ITC | 4QFY2016 Result Update

Exhibit 5: Segment-wise performance (Standalone)

Y/E Mar (` cr)

4QFY16

4QFY15

% yoy 3QFY16

% qoq FY2016 FY2015

% chg

Net Income

Cigarettes

4639

4211

10.2

4380

5.9

17486

16805

4.1

Others

2704

2567

5.4

2478

9.1

9704

9011

7.7

Hotels

363

346

4.8

345

5.1

1286

1187

8.4

Agri Business

1806

1428

26.5

1481

22.0

7457

8380

(11.0)

Paperboards & Packaging

1238

1203

3.0

1260

(1.7)

5017

4974

0.9

PBIT

Cigarettes

3019

2706

11.5

2984

1.2

11752

11196

5.0

Others

71

49

46.0

19

277.8

71

34

106.9

Hotels

43

42

1.5

26

65.1

56

49

13.5

Agri Business

174

164

6.1

231

(24.6)

934

904

3.3

Paperboards & Packaging

203

191

6.5

241

(15.8)

908

921

(1.5)

PBIT Margin (%)

Cigarettes

65.1

64.3

68.1

67.2

66.6

Others

2.6

1.9

0.8

0.7

0.4

Hotels

11.8

12.1

7.5

4.3

4.1

Agri Business

9.7

11.5

15.6

12.5

10.8

Paperboards & Packaging

16.4

15.8

19.1

18.1

18.5

Source: Company, Angel Research

May 23, 2016

4

ITC | 4QFY2016 Result Update

Investment rationale

Cigarettes business to enjoy strong pricing power: We believe ITC’s cigarettes

business is well poised to continue to post a healthy profit growth over

FY2016-18E due to its strong pricing power and improvement in volume

growth.

Non-cigarettes businesses to register healthy growth over FY2016-18E: While

cigarettes remain the main profit center for the company, investments in

the non-cigarettes businesses such as FMCG, Hotels and Paperboards have

given the company a foothold in the respective businesses. We expect these

businesses to play a major role in driving the company’s long-term growth.

Outlook and valuation

We expect ITC to report a top-line and bottom-line CAGR of 8.3% and 9.3%

respectively over FY2016-18E. At the current market price, the stock is trading at

22.6x FY2018E EPS. We recommend a Buy on the stock with a target price of

`380.

Company Background

ITC is a diversified conglomerate, present across various categories - Cigarettes

(41% of revenue); Hotels (3% of revenue); Paperboards and Packaging (13% of

revenue); Agri-business (22% of revenue); and other FMCG (branded apparel,

personal care, stationery, safety matches and specialty papers [21% of revenue])

businesses. Although ITC is a market leader in the cigarettes category, it is rapidly

gaining market share even in its evolving businesses of packaged foods and

confectionery, branded apparel, personal care and stationery.

May 23, 2016

5

ITC | 4QFY2016 Result Update

Profit and loss statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

FY18E

Total operating income

29,901

33,239

36,507

36,837

39,726

43,194

% chg

18.9

11.2

9.8

0.9

7.8

8.7

Total Expenditure

19,274

20,784

23,034

22,599

24,312

26,435

Cost of Materials

12,066

13,156

14,672

13,703

14,619

15,766

Personnel

1,387

1,608

1,780

1,884

2,066

2,289

Others

5,821

6,019

6,582

7,013

7,627

8,380

EBITDA

10,628

12,455

13,474

14,238

15,414

16,759

% chg

20.1

17.2

8.2

5.7

8.3

8.7

(% of Net Sales)

35.5

37.5

36.9

38.7

38.8

38.8

Depreciation& Amortisation

796

900

962

1,034

1,123

1,256

EBIT

9,832

11,555

12,512

13,204

14,290

15,503

% chg

20.6

17.5

8.3

5.5

8.2

8.5

(% of Net Sales)

32.9

34.8

34.3

35.8

36.0

35.9

Interest & other Charges

86

3

57

49

55

60

Other Income

939

1,107

1,543

1,804

1,950

2,100

(% of PBT)

8.8

8.7

11.0

12.1

12.0

12.0

Share in profit of Associates

-

-

-

-

-

-

Recurring PBT

10,684

12,659

13,998

14,958

16,185

17,543

% chg

20.1

18.5

10.6

6.9

8.2

8.4

Extraordinary Expense/(Inc.)

-

-

-

-

-

-

PBT (reported)

10,684

12,659

13,998

14,958

16,185

17,543

Tax

3,266

3,874

4,390

5,114

5,341

5,789

(% of PBT)

30.6

30.6

31.4

34.2

33.0

33.0

PAT (reported)

7,418

8,785

9,608

9,845

10,844

11,754

Add: Share of associates

-

-

-

-

-

-

ADJ. PAT

7,418

8,785

9,608

9,845

10,844

11,754

% chg

20.4

18.4

9.4

2.5

10.2

8.4

(% of Net Sales)

24.8

26.4

26.3

26.7

27.3

27.2

Basic EPS (`)

9.2

10.9

11.9

12.2

13.5

14.6

Fully Diluted EPS (`)

9.2

10.9

11.9

12.2

13.5

14.6

% chg

20.4

18.4

9.4

2.5

10.2

8.4

May 23, 2016

6

ITC | 4QFY2016 Result Update

Balance Sheet (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E FY17E FY18E

SOURCES OF FUNDS

Equity Share Capital

790

795

802

805

805

805

Reserves& Surplus

21,498

25,467

29,934

34,561

39,550

44,956

Shareholders Funds

22,288

26,262

30,736

35,366

40,354

45,761

Minority Interest

-

-

-

-

-

-

Total Loans

78

67

53

29

35

40

Deferred Tax Liability

1,706

1,741

2,099

2,099

2,099

2,099

Total Liabilities

24,072

28,070

32,888

37,495

42,489

47,900

APPLICATION OF FUNDS

Gross Block

16,944

18,545

21,727

25,140

28,641

32,143

Less: Acc. Depreciation

5,735

6,532

7,548

8,583

9,706

10,963

Net Block

11,209

12,013

14,178

16,557

18,935

21,181

Capital Work-in-Progress

1,488

2,296

2,114

2,114

2,114

2,114

Investments

7,060

8,823

8,405

12,854

12,854

12,854

Current Assets

14,260

16,097

19,498

19,735

22,316

26,273

Inventories

6,600

7,360

7,837

7,872

8,707

9,704

Sundry Debtors

1,163

2,165

1,722

1,615

1,524

1,657

Cash

3,615

3,289

7,589

6,565

7,716

8,865

Loans & Advances

1,154

1,803

843

1,842

2,384

3,024

Other

1,728

1,480

1,506

1,842

1,986

3,024

Current liabilities

10,448

11,604

11,775

14,234

14,199

14,989

Net Current Assets

3,812

4,494

7,722

5,501

8,117

11,284

Deferred Tax Asset

503

445

468

468

468

468

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

24,072

28,070

32,888

37,495

42,489

47,900

May 23, 2016

7

ITC | 4QFY2016 Result Update

Cash flow statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16E FY17E FY18E

Profit before tax

10,684

12,659

13,998

14,958

16,185

17,543

Depreciation

796

900

962

1,034

1,123

1,256

Change in Working Capital

(1,049)

(1,732)

30

1,280

(1,465)

(2,017)

Interest / Dividend (Net)

(580)

(767)

(1,131)

49

55

60

Direct taxes paid

(2,886)

(3,797)

(4,226)

(5,114)

(5,341)

(5,789)

Others

(255)

(300)

(324)

-

-

-

Cash Flow from Operations

6,710

6,962

9,309

12,208

10,557

11,054

(Inc.)/ Dec. in Fixed Assets

(4,324)

(4,586)

(4,402)

(12,398)

(3,501)

(3,502)

(Inc.)/ Dec. in Investments

(744)

(1,763)

418

(4,449)

-

-

Cash Flow from Investing

(3,581)

(2,823)

(4,820)

(7,949)

(3,501)

(3,502)

Issue of Equity

922

691

979

3

-

-

Inc./(Dec.) in loans

(10)

(11)

(15)

(24)

6

5

Dividend Paid (Incl. Tax)

(3,518)

(4,148)

(4,772)

(5,218)

(5,856)

(6,347)

Interest / Dividend (Net)

273

(996)

3,619

(45)

(55)

(60)

Cash Flow from Financing

(2,333)

(4,465)

(190)

(5,284)

(5,905)

(6,402)

Inc./(Dec.) in Cash

796

(326)

4,299

(1,024)

1,151

1,149

Opening Cash balances

2,819

3,615

3,289

7,589

6,565

7,716

Closing Cash balances

3,615

3,289

7,589

6,565

7,716

8,865

May 23, 2016

8

ITC | 4QFY2016 Result Update

Key ratios

Y/E March

FY13

FY14

FY15

FY16E

FY17E

FY18E

Valuation Ratio (x)

P/E (on FDEPS)

35.8

30.2

27.6

27.0

24.5

22.6

P/CEPS

32.3

27.4

25.1

24.4

22.2

20.4

P/BV

11.9

10.1

8.7

7.5

6.6

5.8

Dividend yield (%)

1.6

1.8

1.9

2.0

2.2

2.4

EV/Sales

8.5

7.6

6.8

6.7

6.2

5.6

EV/EBITDA

24.0

20.4

18.5

17.3

15.9

14.6

EV / Total Assets

7.4

6.4

5.6

4.8

4.3

3.9

Per Share Data (`)

EPS (Basic)

9.2

10.9

11.9

12.2

13.5

14.6

EPS (fully diluted)

9.2

10.9

11.9

12.2

13.5

14.6

Cash EPS

10.2

12.0

13.1

13.5

14.9

16.2

DPS

5.3

6.0

6.2

6.5

7.3

7.9

Book Value

27.6

32.6

38.1

43.9

50.1

56.8

Returns (%)

RoCE

44.0

43.9

40.6

37.3

35.4

33.8

Angel RoIC (Pre-tax)

84.1

81.3

84.6

82.6

72.1

64.4

RoE

33.3

33.5

31.3

27.8

26.9

25.7

Turnover ratios (x)

Asset Turnover

1.8

1.8

1.7

1.5

1.4

1.3

Inventory / Sales (days)

81

81

78

78

80

82

Receivables (days)

14

24

17

16

14

14

Payables (days)

24

25

22

24

26

26

Net Working capital (days)

71

79

74

70

68

70

May 23, 2016

9

ITC | 4QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

ITC

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

May 23, 2016

10