2QFY2016 Result Update | Infrastructure

November 16, 2015

IL&FS Transportation Networks

NEUTRAL

CMP

`89

Performance Highlights

Target Price

-

Quarterly highlights - Consolidated

Y/E March (` cr)

2QFY16 1QFY16 2QFY15

% chg (yoy)

% chg (qoq)

Investment Period

-

Net sales

1,872

1,644

1,502

24.7

13.8

EBITDA

659

530

616

7.1

24.3

Stock Info

Reported PAT

69

3

99

(30.1)

nmf

Source: Company, Angel Research; nmf- Not Meaningful

Sector

Infrastructure

IL&FS Transportation Networks (ITNL)’ consolidated revenues for 2QFY2016

Market Cap (` cr)

2,941

were up 24.7% yoy to `1,872cr, reflecting a 38.7% increase in Construction

Net debt (` cr)

22,736

business income to `1,223cr. During the quarter, ITNL’s revenues benefitted from

Beta

1.0

`135.6cr of compensation claim. On adjusting for the same, adj. revenues were

52 Week High / Low

223/84

up 15.6% yoy to `1,736cr. Higher contribution from the low margin Construction

business led to a 578bp yoy decline in EBITDA margin to 35.2%. Despite a 7.1%

Avg. Daily Volume

68,265

yoy EBITDA growth, higher interest and depreciation expenses led to a 30.1%

Face Value (`)

10

decline in PAT to `69cr. On adjusting for compensation claims, ITNL would have

BSE Sensex

25,611

reported adj. losses of `66cr.

Nifty

7,762

ITNL reported an order backlog of `15,023cr at 2QFY2016-end, which gives

revenue visibility for the construction segment for over the next 36 months.

Reuters Code

ILFT.BO

Bloomberg Code

ILFT@IN

The consolidated debt stood at `26,213cr, reflecting a D/E ratio of 4.5x (vs. D/E

ratio of 3.7x at 2QFY2015-end, when debt stood at `21,177cr).

ITNL’s incremental equity requirement towards BOT projects for the next 2-3

Shareholding Pattern (%)

years is at ~`495cr. 8 of the ongoing BOT projects are expected to report Date

Promoters

70.8

of Completion (CoD) in the next 12 months, in-turn contributing to FY2016-17E

MF / Banks / Indian Fls

2.5

Toll/ Annuity Income.

FII / NRIs / OCBs

7.9

Outlook and Valuation: Despite ITNL’s robust order backlog and strong

execution capabilities, we are concerned about its higher consol. D/E ratio, which

Indian Public / Others

18.8

is eating into profits. Even though ITNL successfully raised `740cr through the

rights issue recently, we sense this would not be enough to address the Balance

Abs. (%)

3m

1yr

3yr

sheet concerns, and we believe more needs to be done. The Management

continues to pursue strategic initiatives which should lead to debt reduction;

Sensex

(8.8)

(8.7)

38.6

however, we believe containing debt within comfortable levels would take more

ITNL

(23.5)

(51.0)

(49.1)

time than is being anticipated by the Management. This could possibly lead to

continued pressure on the stock. To capture high leverage and delays in strategic

initiatives, we revise down our estimates. We now expect ITNL to report 18.3%

3-Year Daily Price Chart

top-line and negative 17.6% bottom-line (owing to higher interest expenses)

300

CAGR during FY2015-17E. Using SoTP based valuation methodology, we arrive

250

at FY2017E based price target of `97. Given the limited upside potential from

200

the current levels, we maintain our Neutral rating on the stock.

150

Key financials (Consolidated)

100

Y/E March (` cr)

FY13

FY14

FY15E

FY16E

FY17E

50

Net Sales

6,645

6,587

6,304

7,360

8,825

% chg

(0.9)

(4.3)

16.8

19.9

0

Net Profit

520

463

444

218

301

% chg

(11.0)

(4.2)

(50.8)

38.1

EBITDA (%)

27.7

28.7

30.8

34.0

35.9

Source: Company, Angel Research

EPS (`)

29

19

14

7

9

P/E (x)

3.0

4.8

6.2

13.5

9.8

P/BV (x)

0.5

0.4

0.4

0.4

0.4

RoE (%)

14.9

10.6

7.5

3.2

3.7

RoCE (%)

9.7

8.3

6.7

7.3

7.9

Yellapu Santosh

EV/Sales (x)

2.4

3.1

4.0

3.8

3.6

022 - 3935 7800 Ext: 6828

EV/EBITDA (x)

8.5

10.8

12.8

11.0

10.1

Source: Company, Angel Research; CMP as of 13 Nov, 2015

Please refer to important disclosures at the end of this report

1

ITNL | 2QFY2016 Result Update

Exhibit 1: Quarterly Performance (Consolidated)

Particulars (` cr)

2QFY16

1QFY16

% chg (qoq) 2QFY15

% chg (yoy) 1HFY16

1HFY15

% chg (yoy)

Net Sales

1,872

1,644

13.8

1,502

24.7

3,516

2,922

20.4

Total Expenditure

1,213

1,114

8.8

886

36.9

2,327

1,886

23.4

Cost of materials consumed

67

72

(6.9)

34

96.1

138

60

130.0

Construction Contract Cost

709

677

4.8

499

41.9

1,386

1,124

23.3

Employee benefits Expense

126

109

15.7

118

6.1

234

231

1.2

Other Expenses

311

257

21.1

234

33.1

569

471

20.8

EBITDA

659

530

24.3

616

7.1

1,189

1,036

14.9

EBIDTA %

35.2

32.2

41.0

33.8

35.4

Depreciation

59

58

2.4

43

37.2

117

91

29.0

EBIT

600

472

27.0

572

4.8

1,072

945

13.5

Interest and Financial Charges

585

560

4.6

494

18.4

1,145

946

20.9

Other Income

88

93

(6.0)

71

23.0

181

299

(39.5)

PBT before Exceptional Items

103

6

nmf

150

(31.5)

109

298

(63.5)

Exceptional Items

0

0

0

0

0

PBT after Exceptional Items

103

6

nmf

150

(31.5)

109

298

(63.5)

Tax Expenses/ (credit) (note)

48

15

221.0

62

(21.7)

63

81

(22.3)

% of PBT

47.0

244.8

41.1

58.2

27.4

PAT

54

(9)

nmf

88

(38.3)

45

216

(79.0)

Share of profit of Associates (net)

1

(1)

nmf

3

nmf

0

4

nmf

Loss/ (Profit) to Minority Interest

(14)

(13)

nmf

(8)

nmf

(26)

(17)

nmf

PAT after MI, profit share of Associates

69

3

nmf

99

(30.1)

72

237

(69.6)

PAT %

3.7

0.2

6.6

2.0

8.1

Dil. EPS

1.84

0.84

119.0

3.20

(42.5)

1.00

8.01

(87.5)

Source: Company, Angel Research; Note: nmf- Not Meaningful

Consolidated Business Review

Execution during the quarter gains momentum

Led by stronger execution, ITNL reported a 24.7% yoy increase in its consolidated

revenues to `1,872cr.

Construction segment revenues during the quarter reported a 38.7% yoy increase

to

`1,223cr. Construction revenues booked during the quarter include

compensation claim of `135.6cr; adjusting for the same, the segment’s revenues

grew 23.4% yoy. Construction segment revenues during the quarter were booked

from SBEL, CNTL, and BAEL projects.

Elsamex reported 5.0% yoy increase in revenues to `239cr, during the quarter.

This is against the previous quarter’s 6.2% yoy revenue de-growth (owing to forex

loss).

Notably, Toll/ Annuity business reported a 14.6% yoy increase in revenues to

`358cr.

Also, during the quarter, ITNL reported a 103.7% yoy increase in fee income on

account of higher fee bookings from ACEL, FSEL, KNCEL and GRBDCL projects.

On adjusting for compensation claim of `135.6cr, 2QFY2016 adj. revenues grew

15.6% yoy to `1,736cr.

November 16, 2015

2

ITNL | 2QFY2016 Result Update

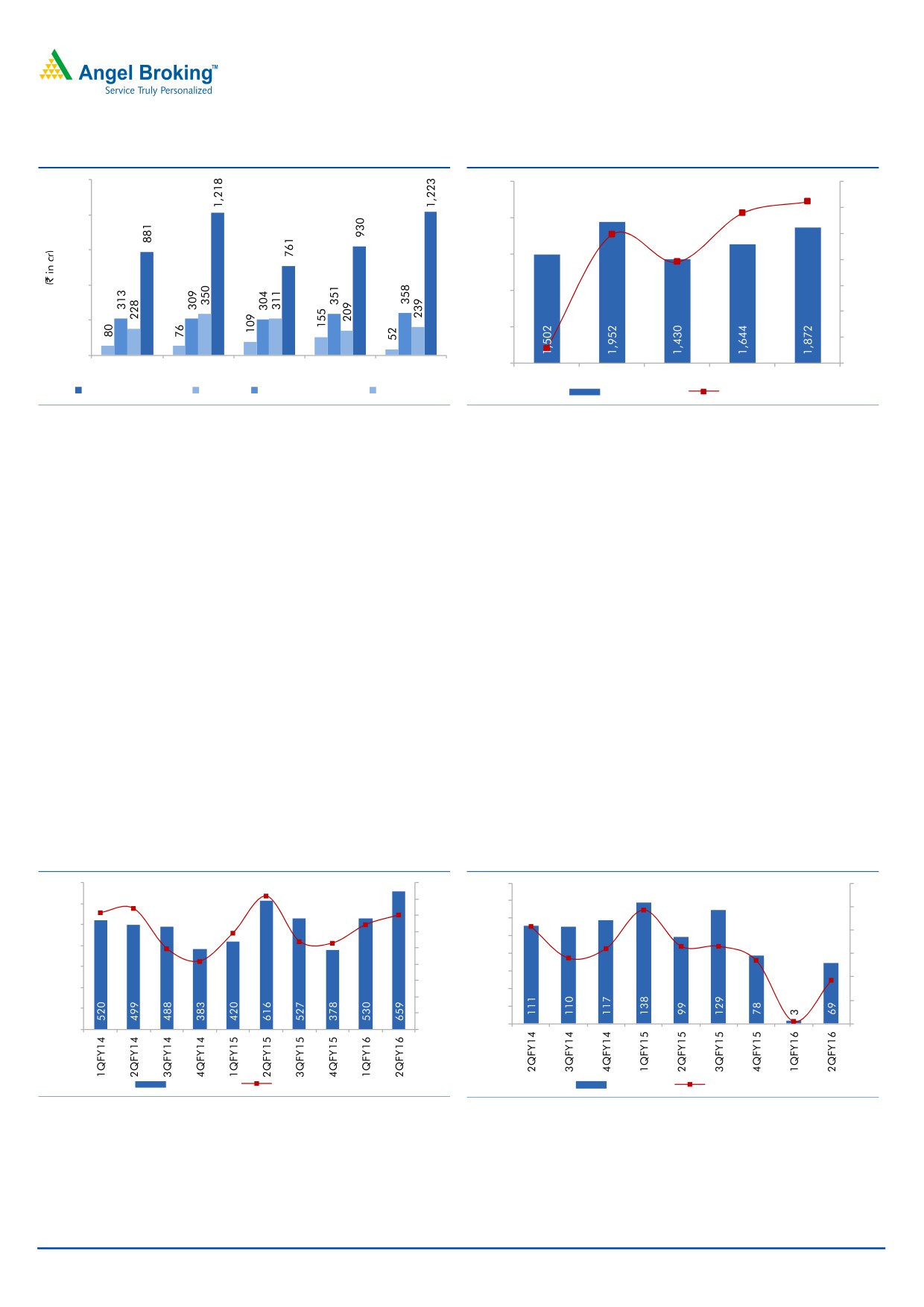

Exhibit 2: Quarterly Income Split

Exhibit 3: Quarterly Net Revenue movement

1,500

2,500

40

24.7

15.8

20

1,200

2,000

0

900

(0.7)

1,500

(20)

(21.8)

600

(40)

1,000

(60)

300

500

(88.8)

(80)

0

0

(100)

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Construction Income Elsamex

Toll/ Annuity Income Other Income

Net Income (` cr)

yoy change (%)

Source: Company, Angel Research

Source: Company, Angel Research

Commencement of Moradabad-Bareilly (MBEL) and Warora Chandrapur

(WCBTRL) BOT-Toll projects contributed to 14.6% yoy increase in 2QFY2016 Toll

income. The quarter’s Toll & Annuity Income also benefitted from

(1)

25.8%

increase in toll income from Barwa Adda (to avg. per day toll of `0.15cr),

(2) 22.6% increase in toll income from Baleshwar-Kharagpur (to avg. per day toll

of `0.15cr), (3) 13.6% increase in toll income from Ahmedabad Mehsana (to avg.

per day toll of `0.22cr) and (4) 13.0% increase in toll income from Pune-Solapur

(to avg. per day toll of `0.20cr). These 4 BOT-Toll projects together contributed

16% of the total 2QFY2016 toll income.

EBITDA margins decline to 35.2%

Shift in revenue mix, where higher contribution of the low margin Construction

business was seen during the quarter, led to 578bp yoy EBITDA margin contraction

to 35.2%. On adjusting for compensation claim, the EBITDA margin of the

company in 2QFY2016 stood at 28%. EBITDA margin contraction on a yoy basis

was owing to a 23.4% rise in material expenses which grew 96.1% (to `67cr), and

with Construction expenses growing 41.9% (to `709cr).

Exhibit 4: EBITDA margins decline to 35.2%

Exhibit 5: PAT margins decline to 3.7%

700

35.9

41.0

45

160

12

37.2

9.7

35.2

40

140

8.3

600

10

29.6

26.5

32.2

35

120

500

27.0

24.8

20.9

30

6.4

6.6

6.6

8

100

400

25

5.6

5.4

80

3.7

6

300

20

60

15

4

200

40

10

0.2

2

100

20

5

0

0

0

0

EBITDA (` cr)

EBITDA Margin (%)

PAT (` cr)

PAT Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

November 16, 2015

3

ITNL | 2QFY2016 Result Update

Higher interest & depreciation exp. led to yoy PAT decline

Despite 7.1% yoy EBITDA growth, the reported PAT declined sharply from `99cr in

2QFY2015 to `69cr in 2QFY2016, mainly on account of higher interest (up 18.4%

yoy to `585cr) and depreciation (up 37.2% yoy to `59cr) expenses. PAT margins

declined from 6.6% in 2QFY2015 to 3.7% in 2QFY2016. On adjusting for

compensation claim, ITNL incurred losses of `66cr. Further, increase in yoy interest

expense is owing to draw-down of already sanctioned debts towards the projects

under construction. Increase in yoy depreciation expense is due to commencement

of operations at MBEL, WCBTRL, and some of the check-posts at MPBCDCL.

Strong Order backlog of `15,023cr gives better revenue visibility

ITNL at 2QFY2016-end reported an order backlog of `15,023cr, which gives

revenue visibility for the Construction segment for over the next 36 months.

Exhibit 6: Order Book

Exhibit 7: Order Book Split at 2QFY2016-end (in %)

18,000

Non-Road

16,000

Projects, 7%

14,000

12,000

10,000

8,000

Non-NHAI

6,000

Road , 33%

4,000

NHAI, 60%

2,000

0

Source: Company, Angel Research

Source: Company, Angel Research

ITNL to-date in FY2016 has reported 4 BOT project order wins. These include:

4-laning of 141kms stretch between Fagne-Gujarat/ Maharashtra Border

(Package-III, NH-6) on BOT (Toll) basis.

4-laning of 194kms stretch between Amravati-Chikhli (Package-I, NH-6)

on BOT (Toll) basis.

6-laning of 23.5kms stretch between Ranchi Ring Road, section VII from

Kathitanr to Karma on BOT basis.

Upgrade 2 road projects, (i) Bandri-Jaruwakheda, Nirtala-Mandi-Bamora

and Damoh-Hindoriya-Patera section covering 76.23 kms, (ii) Pachawali-

Rannod, Rannod-Pichhore, Bhasula-Chainpur, Vijaypur-Dhanrawad and

Ashok Nagar-Thubon section on performance based contract.

Also, ITNL indicated healthy bid-pipeline of

~`15,018cr, with a major

~`11,569cr of it being at RFQ stage. Notably, ~66% of the bid pipeline

highlighted by the company is from NHAI.

November 16, 2015

4

ITNL | 2QFY2016 Result Update

Exhibit 8: 1QFY2016E Bid Pipeline details

Particular (` cr)

RFP Stage

RFQ Stage

NHAI Projects

3,170

6,748

State Highway Projects

280

4,821

MoRTH Projects

0

0

NHAI EPC Projects

0

0

Metro Transportation Corp. Project

0

0

Total Bid Pipeline

3,450

11,569

Source: Company, Angel Research

Update on BOT Projects

ITNL in YTDFY2016 has reported receipt of Provisional Completion Certificate

(CC)/ Commercial Operations Date (CoD) for 8 stretches of the MP Border check

post project, including, (1) Sagar-Lalitpur Border check post, (2) Nawgaon-Jhansi

Checkpost (S-4) Border check post, (3) Venkatnagar (SS-2) Border check post, (4)

Sendhwa-Khetia Border check post, (5) Ujjain-Jhalawar Border check post, (6)

Balaghat-Gondia Border check post. With these stretches getting operational, the

total count of operational stretches has gone up to 2 Central Control Facility and

19 Border Checkpost (of the total 20 check posts).

SBHL has received provisional completion certificate as on Oct 10, 2015. JSEL has

applied for Completion Certificate.

Financial Health of the company

ITNL reported consolidated debt of `26,213cr, reflecting D/E ratio of 4.5x (vs. D/E

ratio of 3.7x at 2QFY2015-end with debt of `21,177cr). ~5% surge in qoq D/E

ratio is owing to draw-down of already sanctioned debt towards projects under

construction.

Exhibit 9: Consolidated Debt & D/E Ratio

30,000

5

4.5

4.1

4.2

5

25,000

3.8

3.7

4

3.5

4

20,000

3

15,000

3

2

10,000

2

1

5,000

1

0

0

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Debt (` cr)

D/E (x)

Source: Company, Angel Research

ITNL reported interest coverage ratio at 1.2x (vs 1.3x reported in 2QFY2015). Such

lower interest coverage ratio is owing to longer gestation of BOT projects executed

and many of them being under the investment phase.

November 16, 2015

5

ITNL | 2QFY2016 Result Update

As of 2QFY2016-end, ITNL needs `495cr as equity investment towards BOT

projects in its pipeline (to-date equity invested in BOT projects stands at

~`5,218cr). In addition, new project wins (where FC is yet to be done), would

further add to the above-mentioned equity requirements.

The Management is working on the following strategic initiatives to raise equity for

BOT projects in the pipeline, (1) raise preference equity (passed board resolution

to raise `750cr), (2) sell stake in some of the operational BOT projects, and (3)

securitize some of the operating BOT projects.

Even though ITNL’s Management indicated that these initiatives would unfold by

Mar-2016, we expect possible delays in some of the targeted events unfolding. In

Nov-2015, ITNL successfully raised

`740cr through a Rights issue. The

Management highlighted that money raised from the rights issue would be majorly

used towards debt repayment. On considering the Management’s strategic

initiatives, and debt draw-down plan for SPVs, we expect debt to continue to be at

current levels by FY2016-end. Despite the fund raising exercise, we sense that ITNL

would experience near-term pain, as high leverage would continue to eat into their

profitability. On the whole, we expect a majority of the funding issues to be

addressed in FY2017E, thereby leading to alleviation in Balance Sheet stress,

going forward.

Future Funding requirements

ITNL’s Management highlighted that additional equity requirement towards

existing BOT projects are to the tune of ~`495cr (majorly to be invested in next 2-

3 years).

8 of the ongoing BOT projects are expected to get Date of Completion (CoD) in

the next 12 months, thereby adding to the Toll/ Annuity income in FY2016/2017E.

Exhibit 10: BOT Projects Scheduled CoD

BOT Projects

Scheduled CoD

BAEL

Sep-2016

TRDCL III

Nov-2015

CNTL

May-2016

MPBCDCL

Jan-2016

RIDCOR III

Jun-2016

SBEL

Nov-2015

KSEL

Aug-2016

KNC

Nov-2016

Source: Company, Angel Research

Outlook & Valuation

A major part of the `740cr raised through the Rights issue recently, would be

majorly used towards debt repayment. Considering (1) equity requirements of

`495cr towards existing projects (currently being met through the standalone entity

debt), (2) additional financing requirements towards recently won projects, and (3)

8 more projects expected to commence operations in the next 12 months, there

probably exists requirement for incremental debt as well as equity requirements.

November 16, 2015

6

ITNL | 2QFY2016 Result Update

Anticipating future funding requirements, ITNL in its recent board meeting passed

resolution to (1) increase the borrowing limits of the company (from `9,000cr to

`11,000cr), and (2) allow issuance of `750cr of preference shares. Considering

projects in the pipeline and their current funding requirements (unless the strategic

initiatives highlighted by the Management gain traction), the company should

continue to face near term funding issues, which will continue to keep the balance

sheet under stress. On capturing the impact of the recent rights issue, we increase

our FY2016/17E PAT estimates by 541.2% and 142.7%, respectively.

Exhibit 11: Earnings Revision

FY2016E

FY2017E

Y/E March (` cr)

Old

New Chg (%)

Old

New Chg (%)

Net Sales

7,360

7,360

0.0

8,825

8,825

0.0

EBITDA

2,503

2,503

0.0

3,168

3,168

0.0

EBITDA Margins (%)

34.0

34.0

35.9

35.9

PAT

34

218

541.2

124

301

142.7

PAT Margins (%)

0.5

3.0

1.4

3.4

Source: Angel Research

Maintain Neutral view on ITNL with revised price target of `97

Despite ITNL’s robust order backlog and strong execution capabilities, we are

concerned about its higher consol. D/E ratio, which is eating into profits. Even

though money raised from the rights issue has been used to repay debt, new

projects would require debt funding, which should again lead to increase in debt

levels. The Management is working on strategic initiatives to reduce debt, which in

our view could take a few quarters to materialize. Till then, ITNL’s profitability

would be impacted due to higher interest expenses, given their levered balance

sheet status.

With more visibility from the order book, we view that any news flow on order wins

would not lead to upward re-rating of the stock. It is more of actions taken by the

Management in de-levering the balance sheet which should lead to upwards re-

rating of the stock. Till the time more visibility comes on the Balance Sheet de-

leveraging process, we expect the stock to remain under pressure.

We have used sum-of-the-parts (SOTP) valuation method to arrive at a target price

for ITNL. Considering increase in leverage, we have valued the construction

business at an EV/EBITDA of 4x FY2017E EBITDA, and the BOT projects (inclusive

of YuHe Expressway & Metro Rail) on FCFE basis at a Cost of Equity of 16%. Also,

we have valued Elsamex, and their Surface Transportation Projects (other than

road projects) using P/BV multiple. On adding up all the projects’ value, we arrive

at a SOTP-based target price of `97. Given that all the positives are captured in

the current stock price, we maintain our NEUTRAL rating on stock.

November 16, 2015

7

ITNL | 2QFY2016 Result Update

Exhibit 12: Derivation of SOTP-based target price for ITNL (FY2017E)

FY17E Std.

Target

Target

Value/

% of

Particulars

Segment

Basis

EBITDA (` cr)

Multiple

Value (` cr)

share (`)

SoTP

ITNL's construction business

Construction

747

4

2,987

91

93.3

EV/EBITDA of 4x

Total

2,987

91

93.3

Discounted

Project

Adj. FCFE

Value/

% of

Particulars

Proj. Type

Basis

FCFE (` cr)

Stake

Value (` cr)

share (`)

SoTP

Road BOT projects

Noida Toll Bridge

Toll

552

25%

138

4

4.3

NPV at CoE of 16%

Gujarat Toll Roads

Toll

770

42%

323

10

10.1

NPV at CoE of 16%

West Gujarat Expressway

Toll

197

100%

197

9

9.6

NPV at CoE of 16%

RIDCOR Phase-I & II

Toll

1,683

50%

842

26

26.3

NPV at CoE of 16%

Beawar-Gomti

Toll

400

100%

400

12

12.5

NPV at CoE of 16%

Pune Sholapur

Toll

59

100%

59

2

1.8

NPV at CoE of 16%

Moradabad Bareilly

Toll

840

100%

840

26

26.2

NPV at CoE of 16%

Chandrapur Warora

Toll

273

35%

96

3

3.0

NPV at CoE of 16%

Narkatpally Addanki

Toll

289

50%

144

4

4.5

NPV at CoE of 16%

Kiratpur Ner-Chowk

Toll

1,073

100%

1,073

33

33.5

NPV at CoE of 16%

Sikar Bikaner

Toll

200

100%

200

6

6.3

NPV at CoE of 16%

Baleshwar Kharagpur

Toll

13

100%

13

0

0.4

NPV at CoE of 16%

North Karnataka Expressway

Annuity

163

94%

153

5

4.8

NPV at CoE of 16%

Thiruvananthapuram Phase - I & II

Annuity

(7)

50%

(4)

(0)

(0.1)

NPV at CoE of 16%

AP Expressway

Annuity

(2)

100%

(2)

(0)

(0.1)

NPV at CoE of 16%

Hyderabad Ring Road

Annuity

124

26%

32

1

1.0

NPV at CoE of 16%

East Hyderabad Expressway

Annuity

88

74%

65

2

2.0

NPV at CoE of 16%

Hazaribagh Ranchi Expressway

Annuity

110

74%

81

2

2.5

NPV at CoE of 16%

Jharkhand roads Ph-I & II

Annuity

679

100%

679

21

21.2

NPV at CoE of 16%

Chenani Nashri

Annuity

793

100%

793

24

24.8

NPV at CoE of 16%

Jorabat Shillong

Annuity

237

50%

118

4

3.7

NPV at CoE of 16%

Total

8,642

6,350

193

198.3

Elsamax

295

1.0

295

9

9.2

Valued at 1x its BV

YuHe Expressway

Toll

177

49%

87

3

2.7

NPV at CoE of 16%

Vansh Nimay Infraprojects

16

1.0

16

0

0.5

Valued at 1x its BV

Metro Rail Gurgaon

FCFE

326

59%

194

6

6.0

NPV at CoE of 16%

MP Entry Point project

203

51%

103

3

3.2

Valued at 1x its BV

Other Investments

145

1.0

145

4

4.5

Valued at 1x its BV

Net Debt- FY2016E

(6,975)

(212)

(217.9)

Standalone Net Debt

Grand Total

3,201

97

100.0

No. of shares

33

Upside

9%

CMP

89

Source: Company, Angel Research

November 16, 2015

8

ITNL | 2QFY2016 Result Update

Investment arguments

Market leader in the growing BOT space: ITNL is a surface transport player, with

an established track record of successfully bidding, developing and operating road

BOT projects on a commercial basis. ITNL was one of the first movers in the road

development segment. The company bagged Noida Toll bridge project in 1998.

Since then, it has come a long way and has built sizeable portfolio currently. The

company has one of the largest BOT portfolios in India, encompassing 31 road

projects covering 14,667 lane kms spread across 16 states. Their 2QFY2016

order book at `15,023cr, gives construction segments revenue visibility for over the next

36 months.

Pan-India presence: ITNL has 31 BOT Road projects well spread across 16 states

in India. The company has decent exposure to state highways, which differentiates

it from peers. The one major advantage that state highway projects enjoy over

national highways is that they can be bundled with land, making the projects

viable. Such diversification strategy prevents the company from any fluctuation in

the revenue stream given its limited exposure to any one region or project.

Hedged revenue stream: We believe ITNL has a hedged road BOT asset portfolio

currently, as it is bifurcated into toll and annuity projects in revenue terms, thereby

reducing its dependence on traffic-related revenue inflow. Recent project win from

Kenyan BOT-Annuity project strengthens our view that going forward too, ITNL

would continue to have a balanced revenue mix of Annuity and Toll.

ITNL’s levered BS puts it in a tough spot: ITNL is currently sitting on a consol. D/E

ratio of 4.5x (reflecting debt of `26,213cr). On considering, (1) equity requirement

of `495cr towards existing BOT projects, (2) 8 BOT projects expected to commence

operations in the next 12 months, and (3) their levered Balance Sheet status, we

are of view that the growth for the company would not flow down entirely to the

PAT level, as higher interest expenses would eat into the EBITDA. Hence, till the

time more visibility emerges on the Balance Sheet de-leveraging process, we

expect the profitability to be under pressure.

Key concerns

Even though expectations are high for allocation towards Roads and Highways

vertical in the upcoming budget, any slowdown in the award activity from NHAI

could affect road-focused players such as ITNL.

ITNL has faced execution delays across few projects. Prolonged delays in project

execution beyond the time schedule could act as risk to our estimates.

BOT projects are inherently highly-levered projects. Hence, delays in the correction

of interest rates than our expectations could be a risk to our assumptions.

The Management has highlighted plans to pursue fund raising / strategic initiatives

which should materialize in the next 2-3 quarters. Any delays beyond that could

act as a risk to our estimates.

November 16, 2015

9

ITNL | 2QFY2016 Result Update

Company background

ITNL promoted by IL&FS was incorporated in Nov 2000. Over the years, ITNL

emerged as the largest Surface Transportation Infrastructure Company in Indian.

ITNL is involved in the development, operations and maintenance of surface

transportation infrastructure projects encompassing national and state highways,

roads, tunnels, flyovers and bridges. The company performs a range of project

development activities from project conceptualization to commissioning and

commencement of commercial operations. ITNL has presence in various surface

transportation sub-sectors, such as urban transportation, railways, border check

posts and parking complexes.

November 16, 2015

10

ITNL | 2QFY2016 Result Update

Profit & Loss Statement (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Net Sales

6,645

6,587

6,304

7,360

8,825

% Chg

(0.9)

(4.3)

16.8

19.9

Total Expenditure

4,807

4,697

4,362

4,858

5,657

Cost of Materials Consumed

156

227

242

221

247

Construction Contract Cost

3,423

2,984

2,599

3,202

3,733

Employee benefits Expense

382

414

459

449

525

Other Expenses

846

1,072

1,063

986

1,152

EBITDA

1,838

1,890

1,941

2,503

3,168

% Chg

2.8

2.7

28.9

26.6

EBIDTA %

27.7

28.7

30.8

34.0

35.9

Depreciation

94

151

152

238

401

EBIT

1,743

1,739

1,789

2,265

2,767

% Chg

(0.3)

2.9

26.6

22.2

Interest and Financial Charges

1,119

1,471

1,833

2,391

2,735

Other Income

144

215

525

383

306

PBT

768

483

481

256

337

Tax

227

27

80

54

78

% of PBT

29.6

5.5

16.7

21.0

23.0

PAT before Extraordinary item

541

457

400

202

260

Extraordinary item

0

0

0

0

0

PAT before Minority Interest

541

457

400

202

260

Minority Interest

(25)

1

(29)

(24)

(49)

Share of Profit/ (Loss) of Associates

5

5

15

(8)

(7)

PAT after MI, profit share from Assoc.

520

463

444

218

301

% Chg

(11.0)

(4.2)

(50.8)

38.1

PAT %

7.8

7.0

7.0

3.0

3.4

Diluted EPS

29

19

14

7

9

% Chg

(36.5)

(23.2)

(53.7)

38.1

November 16, 2015

11

ITNL | 2QFY2016 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16E

FY17E

Sources of Funds

Equity Capital

194

571

623

705

705

Reserves Total

3,446

4,433

5,096

6,068

6,487

Networth

3,640

5,004

5,719

6,773

7,192

Minority Interest

358

459

291

291

291

Total Debt

14,359

18,817

23,514

25,994

30,394

Deferred Tax Liability

243

199

108

108

108

Total Liabilities

18,599

24,478

29,632

33,166

37,985

Application of Funds

Gross Block

10,190

14,282

17,438

18,630

21,690

Accumulated Depreciation

580

795

947

1,185

1,587

Net Block

9,610

13,487

16,491

17,444

20,103

Capital WIP

48

50

70

60

50

Investments

687

469

663

708

743

Goodwill

523

575

581

581

581

Current Assets

Inventories

17

17

14

20

23

Sundry Debtors

752

988

1,126

1,109

1,257

Cash and Bank Balance

420

671

777

1,295

1,225

Loans, Advances & Deposits

1,417

2,076

2,377

2,660

3,045

Other Current Asset

7,105

8,782

10,838

12,510

14,362

Current Liabilities

1,991

2,655

3,323

3,240

3,424

Net Current Assets

7,720

9,879

11,808

14,353

16,488

Deferred Tax Asset

11

18

20

20

20

Total Assets

18,599

24,478

29,632

33,166

37,985

November 16, 2015

12

ITNL | 2QFY2016 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16E FY17E

Profit before tax

768

483

481

256

337

Depreciation & Amortization Exp.

109

161

164

253

417

Other non-Cash Expenses

(91)

(119)

(58)

165

(375)

Change in Working Capital & Oth. Adj.

1,320

1,522

(1,628)

(1,724)

(1,443)

Cash Generated from Operations

2,106

2,048

(1,042)

(1,050)

(1,063)

Direct taxes paid

(158)

(251)

(155)

(211)

(142)

Net Cash Flow from Operations

1,947

1,797

(1,197)

(1,261)

(1,205)

(Inc)/ Dec in Fixed Assets

(3,057)

(3,196)

(3,176)

(1,182)

(3,050)

(Inc)/ Dec in Investments

(234)

(60)

(193)

(45)

(35)

(Inc)/ Dec in Other Investing Cash Flows

(1,806)

(868)

(231)

(250)

(150)

Cash Flow from Investing

(5,097)

(4,123)

(3,600)

(1,477)

(3,235)

Issue/ (Buy Back) of Equity

0

746

525

740

0

Inc./ (Dec.) in Loans

2,813

1,509

4,697

2,480

4,400

Dividend Paid (Incl. Tax)

(91)

(94)

(116)

(110)

(175)

Other Financing Cash Flows

507

276

(144)

145

145

Cash Flow from Financing

3,230

2,437

4,963

3,255

4,370

Inc./(Dec.) in Cash

80

111

166

517

(70)

Opening Cash balance & Oth. Adj.

278

500

611

777

1,295

Closing Cash balances

358

611

777

1,295

1,225

November 16, 2015

13

ITNL | 2QFY2016 Result Update

Key Ratios (Consolidated)

Y/E March

FY13

FY14

FY15E

FY16E

FY17E

Valuation Ratio (x)

P/E (on FDEPS)

3.0

4.8

6.2

13.5

9.8

P/CEPS

2.7

3.6

4.0

6.7

4.4

Dividend yield (%)

2.1

2.7

2.4

2.1

2.5

EV/Sales

2.4

3.1

4.0

3.8

3.6

EV/EBITDA

8.5

10.8

12.8

11.0

10.1

EV / Total Assets

0.8

0.8

0.8

0.8

0.8

Per Share Data (`)

EPS (fully diluted)

29.4

18.7

14.3

6.6

9.2

Cash EPS

32.7

24.6

22.4

13.4

20.1

DPS

4.0

5.1

4.0

3.5

4.0

Book Value

187

203

232

206

219

Returns (%)

RoCE (Pre-tax)

9.7

8.3

6.7

7.3

7.9

Angel RoIC (Pre-tax)

9.7

7.3

6.1

6.9

7.4

RoE

14.9

10.6

7.5

3.2

3.7

Turnover ratios (x)

Asset Turnover (Gross Block) (X)

0.2

0.2

0.1

0.1

0.2

Inventory / Sales (days)

1

1

1

1

1

Receivables (days)

41

48

61

55

49

Payables (days)

84

90

109

95

95

Leverage Ratios (x)

D/E ratio (x)

3.9

3.8

4.1

3.8

4.2

Interest Coverage Ratio (x)

1.6

1.2

1.0

0.9

1.0

Note- nmf- Not meaningful

November 16, 2015

14

ITNL | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

ITNL

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 16, 2015

15