IPO Note | Financial Services

Oct 7, 2017

Indian Energy Exchange

SUBSCRIBESUBSCRIBE

Powering up for the future of electricity trading

Issue Open: Oct 9, 2017

Issue Close: Oct 11, 2017

Indian Energy Exchange (IEX) is the dominant exchange in India for trading

electricity in the country. It has a market share of over ~98% of the volumes in the

power exchange industry.

Issue Details

Low market penetration allows for significant growth potential: As on FY17,

Face Value: `10

3.6% of electricity generation in India was traded on power exchanges. This is

Present Eq. Paid up Capital: `3.03cr

much lower than global power exchanges, which typically have 30-70% of

traded volumes. This leaves the power market lots of room to grow.

O ffer for Sale: **0.60cr Shares

Migration of electricity markets to exchanges: Electricity on IEX trades at a

lower price than the bilateral price (`2.5 per kWh on IEX Vs `3.5 per kWh

Fresh issue:

-

bilateral price in FY17). The price difference has ranged between `0.8 to `1.4

per kWh over the past four years. The consistently lower pricing that IEX offers

Post Eq. Paid up Capital: `3.03cr

results in power procurement cost optimization for distribution companies and

Issue size (amount): *`998cr -**1000

large consumers.

cr

Capacity addition in Renewable Energy Sources (RES): Under the Central

Electricity Authority’s (CEA) 13th plan, 100 gW of capacity addition is to take

Price Band: `1645-1650

place in the Renewable Energy segment. This would bring the total of solar

Lot Size: 9 shares and in multiple

and wind energy capacity installed to 100 and 60 gW respectively. Due to

thereafter

seasonality and variability in the generation of solar and wind energy, these

Post-issue implied mkt. cap: *`4984cr

new power generators would depend on the power exchanges to provide

**`5000cr

access to short-term electricity markets.

Enforcement of Renewable Purchase Obligation (RPO) to provide boost to

Promoters holding Pre-Issue: -

trading in REC segment: the central government has targeted 17% share of

Promoters holding Post-Issue: -

renewable power by 2019. However, many states are still laggards in regards

to their RPO targets. In order to address this deficit, trading of Renewable

*Calculated on lower price band

Energy Certificates (REC) is likely to see increased participation.

** Calculated on upper price band

High Dividend Payout: The company has a policy to payout more than 50%

of net profits as dividend. Due to strong cash generation, the company is

Book Building

likely to maintain the dividend payout similar to the payout (80%) in FY17.

QIBs

50% of issu

Outlook & Valuation: IEX is likely to continue its current growth trajectory as

the short-term electricity market would continue its migration away from other

Non-Institutional

15% of issu

platforms and to the exchanges. The company is also likely to sustain its

Retail

35% of issu

position as the dominant market player. The company is also likely to benefit

from long-term industry trends as the Indian power market moves towards

global standards. The company has an ROE of 30.8% Vs 7.4% for Multi-

Post Issue Shareholding Patte

commodity Exchange (MCX), based on FY18 annualized earnings. At the

upper end of the price band, the pre issue P/E multiples works out be 40.9x

Promoters

0%

of FY2018 annualized EPS or IEX,Vs 51.5x of FY2018 annualized EPS for

Others

100%

MCX. We recommend ‘SUBSCRIBE’ on the issue for a mid-to-long term

period.

Key Financial

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

Net Sales

153

145

175

204

% chg

26%

-5%

21%

17%

Net Profit

92

90

100

114

% chg

9.9

-2.1

11.5

13.2

EBITDA (%)

74.8%

71.9%

71.5%

70.3%

Noel Vaz

EPS (Rs)

30.3

29.7

33.1

37.5

P/E (x)

54

56

50

44

+022 39357600, Extn: 6847

P/BV (x)

20

21

18

18

RoE (%)

53

55

54

63

RoCE (%)

44

42

45

51

EV/EBITDA

41

44

37

31

PlSource: RHP, Angel Research; Note: Valuation ratios based on pre-issue outstanding sharesrt

and at upper end of the price band

1

Indian Energy Exchange | IPO Note

Company background

Indian Energy Exchange (IEX) is the largest power trading exchange in India. For

the past five years, it has more than 90% market share of the exchange-traded

volumes of electricity in India. The balance of the exchange-traded volumes are

transacted on the Power Exchange India Ltd (PXIL), which is its main competitor.

The company has 4 products that it offers: Day Ahead Market (DAM), Term Ahead

Market (TAM), Renewable Energy Certificate (REC). The company also soon began

trading in Energy Savings Certificates (ESCerts) from

26 Sept.

2017. The

company’s primary revenue is from earning transaction charges of `20 per mWh

on the traded volume on the exchange. The company also earns a good amount

of interest on interest free deposits collected from exchange members.

IEX primary focus is on the short-term electricity market. At present, the short-term

electricity market is 10.3% of the total traded volumes of the electricity market. Of

the short-term market, 34.5% is traded on power exchanges. The short-term

trading market consists of Inter-state trading Licenses, Power exchanges, Deviation

Settlement Mechanism (DSM), and Direct Bilateral. Market share of volumes traded

on exchanges has gone from 10.9% in FY10 to 34.5% in FY17 (in the short-term

electricity market).

Exhibit 1: Business Volumes by product category for IEX

FY 13

FY 14

FY 15

FY 16

FY 17

DAM (in kWh)

22,346

28,923

28,124

33,956

39,783

TAM (in kWh)

481

345

222

330

744

REC (in mln units)

1.99

1.32

1.55

3.14

4.62

Source: Company, Angel Research, RHP

The company is a professionally managed entity with no promoter group or

subsidiaries. In August 2016, the company received three ISO Certifications - ISO

9001:2008 for quality management, ISO 27001:2013 for information security

management and ISO 14001:2004 for environment management. The Council of

Power utilities recognized IEX as the ‘Leader in Power Market Development’ in

2015 and was awarded the ‘Exchange of the Year’ Award by Power Business View

in 2014.

As of August 31, 2017, the company had over 5,900 participants registered on

their exchange of which over

3,200 participants were active. Over

4,300

registered participants were eligible to trade electricity contracts and over 4,000

registered participants were eligible to trade RECs. The trading participants

registered to trade electricity contracts are located across 29 states and 5 union

territories, and include 50 distribution companies, over 400 electricity generators

and over 3,900 open access consumers. The activities of the company are subject

to regulation from Central Regulatory Electricity Commission (CERC).

Oct 7, 2017

2

Indian Energy Exchange | IPO Note

Exhibit 2: Market share of IEX in exchange traded electricity

FY 13

FY 14

FY 15

FY 16

FY 17

IEX

95.0%

91.5%

92.1%

93.7%

94.8%

PXIL

5.0%

8.5%

7.9%

6.3%

5.2%

Source: Company, Angel Research, RHP

Issue Details

This IPO is an OFS and with no issue of fresh shares. The issue constitutes of an

OFS worth `1000cr. The OFS would offer exit to the institutional investors in IEX.

The two largest sellers are Multiples Private Equity and Tata Power. Multiples

Private Equity and Tata Power currently hold 13.3% and 4.34% of the pre-Offer

Equity Share capital of the company respectively.

Exhibit 3: Pre and Post-IPO shareholding pattern

No of shares (Pre-issue)

% No of shares (Post-issue)

%

Promoter

-

-

-

-

Public

3,03,28,624 100%

3,03,28,624

100%

3,03,28,624 100%

3,03,28,624

100%

Source: RHP, Angel Research

Objects of the offer

To get the benefits of listing the equity shares on the stock exchange

To carry out sale of upto 6,065,009 Equity Shares of existing shareholders

Key Management Personnel

Dinesh K. Mehrotra is the Chairman of the company. He has worked for LIC for

over 35 years and last held the position of Chairman of the company. He also

holds directorships across multiple boards such as Tata Steel and UTI Asset

Management. He has been with the company for over two years.

Satyanarayan Goel is the Managing Director and CEO of the company. He has

over 38 years of experience working in the power sector. He was previously the

Director of Marketing and Operations at PTC and was associated with NTPC for

over 29 years. He is responsible for the company’s overall business operations.

Rohit Bajaj is the Vice President, Business Development. He has over 23 years of

experience in the energy domain. He was previously the Head of Business at NETS

Ltd.

Oct 7, 2017

3

Indian Energy Exchange | IPO Note

Investment Rationale

Low market penetration allows for significant growth potential

As on FY17, only 3.6% of power generated in India was traded on exchanges.

This is much lower than global power markets, where exchange volumes

account for 30-70% of the volume of power generated. As Indian energy

markets develop and mature, the participation on electricity exchanges is

going to converge with global level.

Exhibit 4: Market share of Power exchanges by country

Nordic

India

France

Belgium UK

Germany Austria

countries

3%

23%

29%

53%

53%

53%

91%

Source: Company, Angel Research, RHP

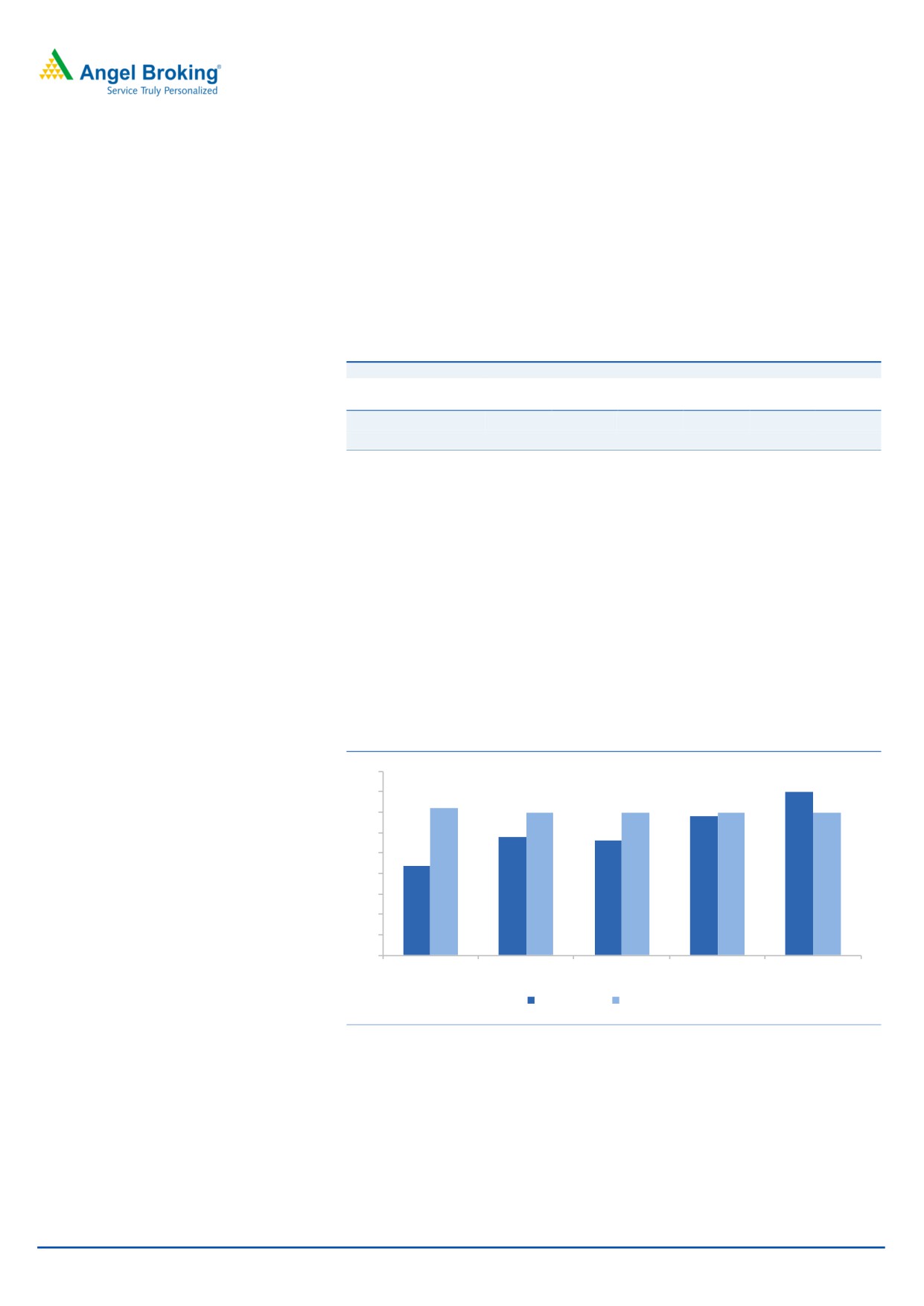

Migration of short-term energy market towards exchanges

IEX is the leading power exchange and a leader in volumes in the short-term

power market. It has a dominant market share in the DAM, TAM and REC segment

of the market. The company has steadily gained market share against other

participants in the short-term market. IEX has gained market share due to its

superior execution, cost optimization and transparent price discovery.

Exhibit 5: IEX volumes Vs Trader volumes in DAM & TAM segment

45

40

40

36

35

35

34

35

35

35

29

28

30

25

22

20

15

10

5

0

FY 13

FY 14

FY 15

FY 16

FY 17

IEX Volume

Trader Volume

Source: Company, Angel Research, RHP

Oct 7, 2017

4

Indian Energy Exchange | IPO Note

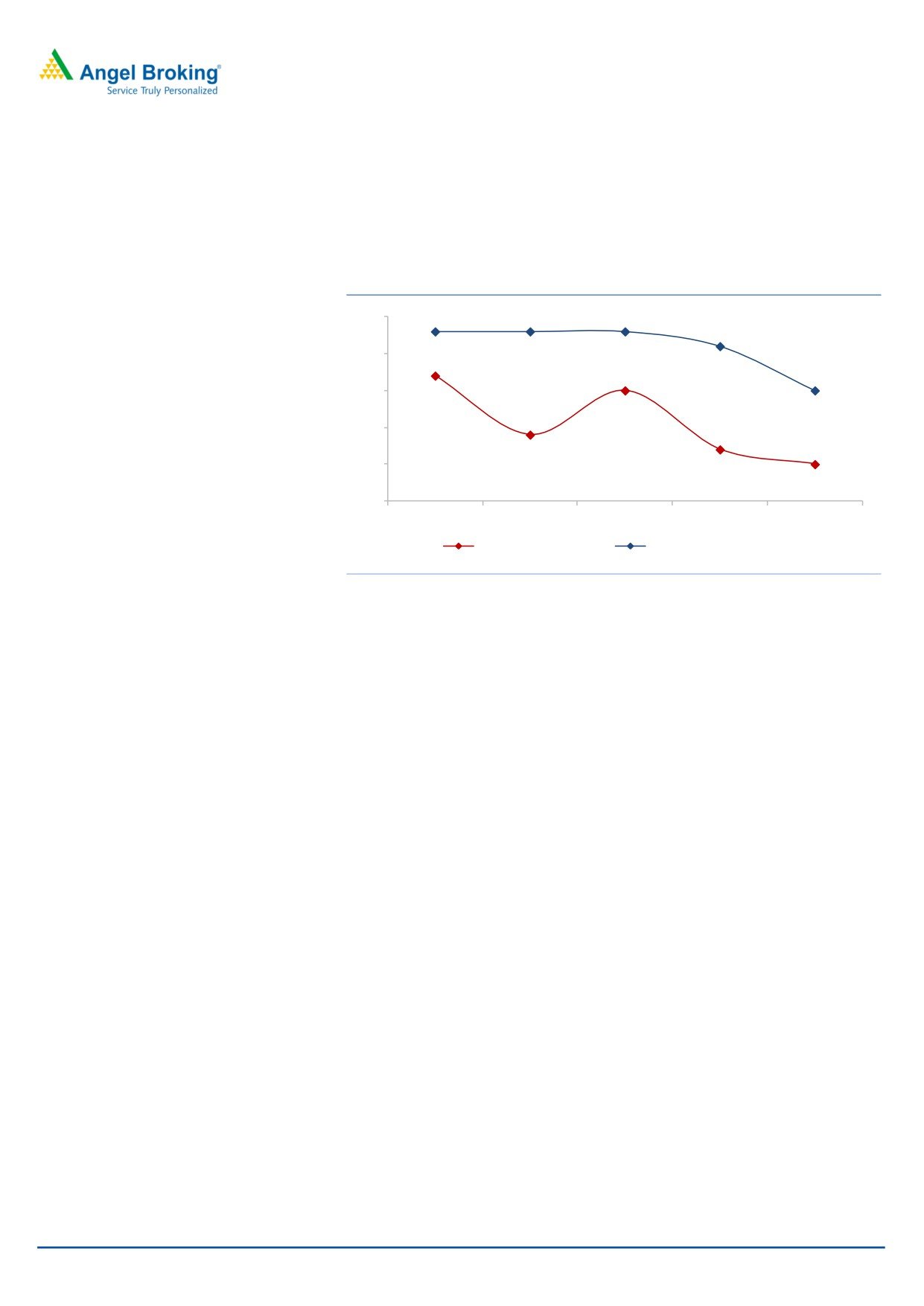

This superior price discovery has resulted in IEX prices being consistently lower than

dealer prices. This trend is likely to remain as markets get deeper with better

participation and improved transmission infrastructure.

Exhibit 6: Avg. prices discovered on IEX Vs dealer market

4.5

4.3

4.3

4.3

4.1

4

3.7

3.5

3.5

3.5

2.9

3

2.7

2.5

2.5

2

FY 13

FY 14

FY 15

FY 16

FY 17

IEX Price (in Rs. kWh)

Bilateral Price (in Rs. kWh)

Source: Company, Angel Research,RHP

Capacity addition in Renewable Energy Sources

By 2022, the capacity of the renewable energy segment is expected to reach

170gW from a present capacity of 58.3gW. Of this capacity, 100 gW is solar

energy while 60 gW is wind energy. Wind and solar energy generators are highly

dependent on local conditions such as the weather (in case of both) and time of

day (in case of solar).

Due to these reasons, it is likely that power generators from this segment would

rely on the short-term power market.

Enforcement of Renewable Purchase Obligation

The central government has attempted to encourage the use of renewable energy.

The government aims to encourage this by using Renewable Purchase Obligations.

Renewable Purchase Obligations

(“RPOs”), put simply, is the minimum

percentages of total power that electricity distribution companies and other

obligated entities like captive and open access consumers need to purchase from

renewable energy sources.

The ministry of power has set an ambitious RPO target of 17.0% by 2019. Of this,

6.75% should come from solar and the balance from non-solar renewable sources

such as wind, biomass etc.

However, the State Regulatory Commissions are free to set year-wise RPO targets

in their respective states as well as targets for solar and non-solar sources

separately. However, few states have been able to meet their RPO targets.

Oct 7, 2017

5

Indian Energy Exchange | IPO Note

Historically, distribution licensees have not been interested in purchasing electricity

generated from renewable energy sources, due to power generation costs as well

as a lack of local availability. Renewable energy certificates (“RECs”) were

introduced to address this mismatch so that states can meet their renewable

purchase obligations, by purchasing REC of producers from other states.

As the power ministry has still reiterated its initial target, states will now have to

increase their participation. Thus, it is likely that the participation is likely to

increase in the REC market.

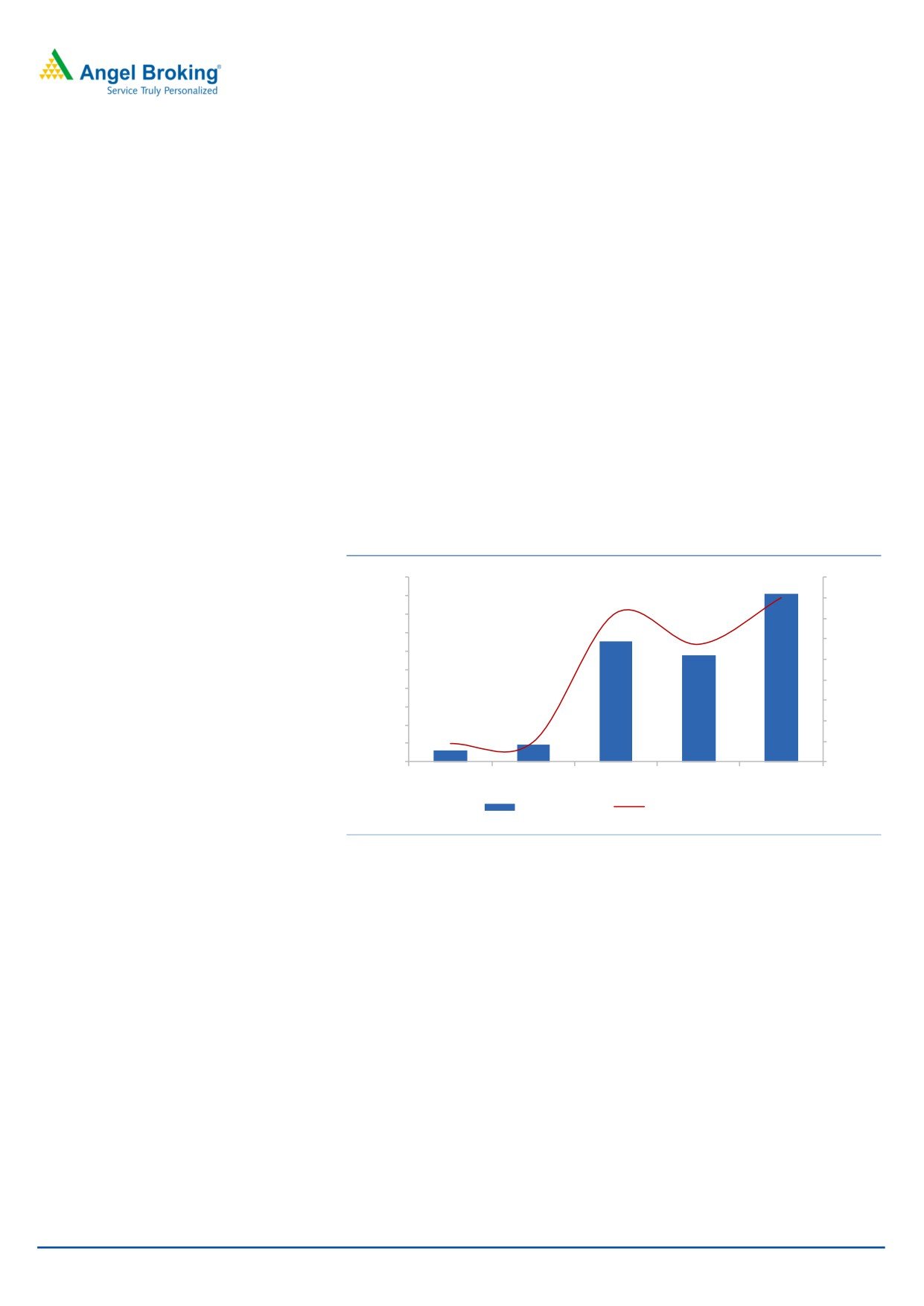

High Dividend Payout: Since FY15, the company has maintained a dividend

payout of over 50%. The company has stated that it will follow a policy to keep its

dividend payout at 50% of net profits. Given the extremely low levels of capital

required to run the business, it is quite likely that the company would keep

dividend payout as per its historical levels.

Exhibit 7: High Dividend Payout

100.0

90.0%

80.1%

90.0

80.0%

72.7%

80.0

70.0%

57.4%

70.0

60.0%

60.0

50.0%

50.0

40.0%

40.0

30.0%

30.0

9.1%

20.0%

20.0

9.9%

10.0

10.0%

-

0.0%

FY 13

FY 14

FY 15

FY 16

FY 17

Div. per share

Dividend Payout %

Source: Company, Angel Research

Oct 7, 2017

6

Indian Energy Exchange | IPO Note

Outlook & Valuation

IEX is likely to continue its current growth trajectory as the short-term electricity

market would continue its migration away from other platforms and to the

exchanges. The company is also likely to sustain its position as the dominant

market player. The company is also likely to benefit from long-term industry

trends as the Indian power market moves towards global standards. The

company has an ROE of 30.8% Vs 7.4% for Multi-commodity Exchange (MCX),

based on FY18 annualized earnings. At the upper end of the price band, the

pre issue P/E multiples works out be 40.9x of FY2018 annualized EPS or IEX,Vs

51.5x of FY2018 annualized EPS for MCX. We recommend ‘SUBSCRIBE’ on

the issue for a mid-to-long term period.

Key risks

Regulatory control on pricing

At present, the company is charging a transaction charge of `20 per mWh of

electricity traded on its platform. The power industry regulator CERC sets this

pricing and hence the company’s revenue is vulnerable to any regulation that

stipulates a reduction in the transaction charges.

Competition from other exchanges

IEX faces competition from two other platforms - PXIL and the DEEP portal (created

by the Power ministry). At present, these exchanges do not pose a significant

threat to IEX. However, this industry is still in the early phases of its development

and the situation remains quite dynamic. This is a possible outcome as platforms

like DEEP have the support of the central government. Also, there are no

regulatory barriers that prevent other competitors from entering the industry.

Oct 7, 2017

7

Indian Energy Exchange | IPO Note

Exhibit 8: Consolidated Income Statement

Y/E March (` cr)

FY14

FY15

FY16

FY17

Total operating income

153

145

175

204

% chg

25.9

(5.1)

20.9

16.5

Total Expenditure

38

41

50

61

Personnel

8

12

14

16

Others Expenses

30

29

36

45

EBITDA

114

104

125

143

% chg

8.0

(8.8)

20.3

14.5

(% of Net Sales)

74.8

71.9

71.5

70.3

Depreciation& Amortisation

3

3

3

3

EBIT

111

101

122

140

% chg

11.5

(9.3)

20.4

14.8

(% of Net Sales)

73.1

69.9

69.6

68.6

Interest & other Charges

0

0

0

0

Other Income

21

32

25

34

(% of Sales)

16.1

23.8

17.1

19.3

Share in profit of Associates

-

-

-

-

Recurring PBT

133

133

147

173

% chg

20.6

(0.3)

10.7

18.1

Tax

40.9

42.5

46.3

59.6

PAT (reported)

92

90

100

114

% chg

9.9

(2.1)

11.5

13.2

(% of Net Sales)

60.3

62.2

57.3

55.7

Basic & Fully Diluted EPS (Rs)

30.3

29.7

33.1

37.5

% chg

38.7

(2.1)

5.3

13.2

Oct 7, 2017

8

Indian Energy Exchange | IPO Note

Exhibit 9: Consolidated Balance Sheet

Y/E March (` cr)

FY14

FY15

FY16

FY17

SOURCES OF FUNDS

Equity Share Capital

30

30

30

30

Reserves& Surplus

223

210

241

245

Shareholders Funds

253

240

271

275

Minority Interest

-

-

-

-

Total Loans

3

-

-

-

Other Liab & Prov

2

1

0

-

Total Liabilities

369

406

424

552

APPLICATION OF FUNDS

Net Block

10

14

11

9

Capital Work-in-Progress

-

-

-

0

Investments

65

44

39

39

Current Assets

294

348

373

502

Inventories

-

-

-

-

Sundry Debtors

0

0

1

0

Cash

289

338

363

498

Loans & Advances

2

2

2

2

Other Assets

2

8

7

3

Current liabilities

111

165

153

277

Net Current Assets

182

183

220

225

Other Non Current Asset

-

-

0

2

Total Assets

369

406

424

552

Oct 7, 2017

9

Indian Energy Exchange | IPO Note

Exhibit 10: Consolidated Cash Flow Statement

Y/E March (`cr)

FY14

FY15

FY16

FY17

Profit before tax

133

133

147

173

Depreciation

3

3

3

3

Change in Working Capital

4

30

9

123

Interest / Dividend (Net)

(18)

(17)

(25)

(10)

Direct taxes paid

(42)

(42)

(46)

(61)

Others

(3)

(15)

(0)

(22)

Cash Flow from Operations

76

92

89

206

(Inc.)/ Dec. in Fixed Assets

(1)

(7)

(2)

(1)

(Inc.)/ Dec. in Investments

(89)

30

(21)

(19)

Cash Flow from Investing

(90)

24

(23)

(21)

Issue of Equity

0

0

0

0

Inc./(Dec.) in loans

3

(3)

0

0

Others

(11)

(103)

(70)

(110)

Cash Flow from Financing

(8)

(106)

(70)

(110)

Inc./(Dec.) in Cash

(22)

9

(4)

76

Opening Cash balances

22

0

10

6

Closing Cash balances

0

10

6

82

Exhibit 11: Key Ratios

Y/E March

FY14

FY15

FY16

FY17

Valuation Ratio (x)

P/E (on FDEPS)

54.4

55.5

49.8

44.0

P/CEPS

52.8

53.8

48.2

42.7

P/BV

19.8

20.8

18.5

18.2

Dividend yield (%)

0.2

1.3

1.2

1.8

EV/Sales

30.5

31.9

26.3

21.9

EV/EBITDA

40.7

44.4

36.7

31.1

EV / Total Assets

12.6

11.4

10.9

8.1

Per Share Data (Rs)

EPS (Basic)

30.3

29.7

33.1

37.5

EPS (fully diluted)

27.6

27.0

31.5

35.7

Cash EPS

31.2

30.7

34.2

38.6

DPS

3.0

21.6

19.0

30.0

Book Value

83.5

79.2

89.4

90.8

Returns (%)

ROCE

43.6

42.2

44.9

50.8

ROE

52.5

55.2

54.1

63.0

Turnover ratios (x)

Asset Turnover (Gross Block)

8.9

6.3

7.3

8.3

Receivables (days)

1

1

2

0

Payables (days)

69

87

123

308

Returns (%)

(68)

(86)

(121)

(307)

Oct 7, 2017

10

Indian Energy Exchange | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Oct 7, 2017

11