3QFY2016 Result Update | Banking

January 29, 2016

ICICI Bank

ACCUMULATE

CMP

`230

Performance Highlights

Target Price

`254

Particulars (` cr)

3QFY16 2QFY16

% chg (qoq)

3QFY15

% chg (yoy)

Investment Period

12 Months

NII

5,453

5,251

3.8

4,812

13.3

Pre-prov. profit

6,560

5,158

27.2

5,037

30.2

Stock Info

PAT

3,018

3,030

(0.4)

2,889

4.5

Sector

Banking

Source: Company, Angel Research

Market Cap (` cr)

1,33,742

ICICI Bank reported a disappointing set of results for 3QFY2016. Though

Beta

1.4

operating numbers remained decent, a sharp increase in slippages was the key

52 Week High / Low

383/216

negative during the quarter. The bank booked profit of `1,243cr on sale of 4%

Avg. Daily Volume

1,28,17,908

stake in its life insurance business during the quarter.

Face Value (`)

2

BSE Sensex

24,871

Healthy growth in advances, backed by retail loans: During 3QFY2016, the

Nifty

7,564

bank’s advances grew by 15.8% yoy (6.1% qoq), aided by healthy retail loan book

Reuters Code

ICBK.NS

growth of 24% yoy. Personal loans and home loans were the main drivers leading

Bloomberg Code

ICICIBC@IN

to the growth in the retail loan book. Retail contribution to total loans increased to

43.8% as compared to 40.9% in 3QFY2015. The corporate book grew 10.2% yoy.

NII grew by 13.3% yoy to `5,453cr, largely in line with our expectation. Due to

Shareholding Pattern (%)

high slippages, the bank took provision of `2,844cr vs `980cr in 3QFY2015, up

by 190% yoy. However, proceeds from the stake sale in its life insurance business

Promoters

NA

helped the reported PAT grow by 4.5% yoy to `3,018cr.

MF / Banks / Indian Fls

24.3

Pick up in deposits growth: Deposits growth picked up, growing by 14.6% yoy

FII / NRIs / OCBs

67.3

compared to 9.3% yoy growth reported in 2QFY2016. CASA deposits also

Indian Public / Others

8.4

accelerated, growing by 17.7% yoy, resulting in an improvement in the CASA ratio

by 120bp yoy to 45.2%. The Reported NIM improved marginally by 1bp qoq to

3.53%, with domestic NIM at 3.86% as compared to 3.84% in 2QFY2016.

Abs. (%)

3m

1yr

3yr

Asset quality deteriorates sharply: Slippages went up sharply to

`6,544cr

(annualized slippage ratio at 6.8%) vs `2,242cr in 2QFY16 (annualized slippage

Sensex

(7.3)

(16.2)

24.4

ratio of 2.3%), with slippage from restructuring at `1,355cr. 2/3rd of the slippages

ICICI Bank

(15.2)

(39.4)

(4.2)

during the quarter came from the RBI highlighted accounts, with a large steel

account being classified as NPA. The GNPA ratio increased by 95bp sequentially

to 4.72%, whereas the NNPA ratio rose 63bp qoq to 2.28%. The bank refinanced

3-year price chart

~`450cr under the 5:25 scheme and SDR worth `1,670cr. It expects SDR of

450

`700cr and 5:25 of `1,200cr in 4QFY2016. The Management has guided at

400

350

similar level of slippages in 4QFY2016 as well. Outstanding restructured loans

300

came down to `11,294cr at the end of 3QFY2016 vs `11,868cr in 2QFY2016.

250

Outlook and valuation: At the current market price, the bank’s core banking

200

150

business (after adjusting `67/share towards the value of subsidiaries) is trading at

100

1.1x FY2017E ABV. The stock has corrected in the last one quarter due to concerns

50

over deteriorating asset quality. Though pain in asset quality is likely to persist in

0

the quarters to come, we believe the current valuations adequately factor in the

relatively higher stressed assets in the bank’s books. We recommend an

Accumulate rating on the stock, with a revised target price of `254.

Source: Company, Angel Research

Key financials (Standalone)

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

Vaibhav Agrawal

NII

16,476

19,040

21,301

24,365

022 - 3935 7800 Ext: 6808

% chg

18.8

15.6

11.9

14.4

Net profit

9,810

11,045

12,238

14,220

% chg

17.8

12.6

10.8

16.2

Siddharth Purohit

NIM (%)

3.2

3.3

3.3

3.3

022 - 3935 7800 Ext: 6872

EPS (`)

17.0

18.9

21.0

24.4

P/E (x)

13.5

12.2

11.0

9.4

P/ABV (x)

1.9

2.0

1.8

1.6

Chintan Shah

RoA (%)

1.6

1.6

1.5

1.6

022 - 4000 3600 Ext: 6828

RoE (%)

14.9

14.8

14.4

14.7

Source: Company, Angel Research; Note: CMP as of January 29, 2015

Please refer to important disclosures at the end of this report

1

ICICI Bank | 3QFY2016 Result Update

Exhibit 1: 3QFY2016 performance (Standalone)

Particulars (` cr)

3QFY16

2QFY16

% chg (qoq)

3QFY15

% chg (yoy)

FY2015

FY2014

% chg

Interest earned

13,346

13,099

1.9

12,435

7.3

49,091

44,178

11.1

- on Advances / Bills

9,863

9,665

2.1

9,032

9.2

35,631

31,428

13.4

- on investments

2,652

2,661

(0.3)

3,012

(11.9)

11,945

11,557

3.4

- on balance with RBI & others

36

31

15.1

53

(31.8)

195

200

(2.4)

- on others

795

741

7.2

338

134.9

1,320

993

32.9

Interest Expended

7,893

7,847

0.6

7,624

3.5

30,052

27,703

8.5

Net Interest Income

5,453

5,251

3.8

4,812

13.3

19,040

16,476

15.6

Other income

4,217

3,007

40.2

3,092

36.4

12,176

10,428

16.8

Other income excl. treasury

2,775

2,785

(0.4)

2,649

4.8

10,482

9,412

11.4

- Fee income

2,262

2,235

1.2

2,110

7.2

8,286

7,758

6.8

- Treasury income

1,442

222

549.5

443

225.5

1,694

1,016

66.7

- Others

513

550

(6.7)

538

(4.6)

2,196

1,654

32.8

Operating income

9,670

8,259

17.1

7,903

22.4

31,216

26,903

16.0

Operating expenses

3,110

3,100

0.3

2,866

8.5

11,496

10,309

11.5

- Employee expenses

1,140

1,213

(6.0)

1,118

2.0

4,750

4,220

12.6

- Other Opex

1,970

1,888

4.3

1,749

12.6

6,746

6,089

10.8

Pre-provision Profit

6,560

5,158

27.2

5,037

30.2

19,720

16,595

18.8

Provisions & Contingencies

2,844

942

201.9

980

190.3

3,900

2,626

48.5

PBT

3,716

4,216

(11.9)

4,057

(8.4)

15,820

13,968

13.3

Provision for Tax

698

1,186

(41.2)

1,168

(40.3)

4,645

4,158

11.7

PAT

3,018

3,030

(0.4)

2,889

4.5

11,175

9,810

13.9

Effective Tax Rate (%)

18.8

28.1

(936)bp

28.8

(1002)bp

29.4

29.8

(41)bp

Source: Company, Angel Research

January 29, 2016

2

ICICI Bank | 3QFY2016 Result Update

Exhibit 2: 3QFY2016 performance analysis (Standalone)

Particulars

3QFY16 2QFY16

% chg (qoq) 3QFY15

% chg (yoy)

Balance sheet

Advances (` cr)

4,34,800

4,09,693

6.1

3,75,345

15.8

Deposits (` cr)

4,07,314

3,84,618

5.9

3,55,340

14.6

Credit-to-Deposit Ratio (%)

106.7

106.5

23bp

105.6

112bp

Current deposits (` cr)

57,181

49,504

15.5

45,916

24.5

Saving deposits (` cr)

1,26,918

1,23,985

2.4

1,10,533

14.8

CASA deposits (` cr)

1,84,099

1,73,489

6.1

1,56,449

17.7

CASA ratio (%)

45.2

45.1

9bp

44.0

117bp

CAR (%)

15.8

16.2

(38)bp

17.6

(180)bp

Tier 1 CAR (%)

11.8

12.1

(30)bp

13.0

(117)bp

Profitability Ratios (%)

Reported NIM

3.52

3.54

(2)bp

3.42

10bp

Cost-to-income ratio

32.2

37.5

(538)bp

36.3

(411)bp

Asset quality

Gross NPAs (` cr)

21,356

16,006

33.4

13,231

61.4

Gross NPAs (%)

4.7

3.8

95bp

3.4

132bp

Net NPAs (` cr)

10,014

6,828

46.7

4,773

109.8

Net NPAs (%)

2.3

1.7

63bp

1.3

101bp

Provision Coverage Ratio (%)

53.2

57.4

(420)bp

63.5

(1030)bp

Slippage ratio (%)

6.8

2.3

444bp

2.7

406bps

Provision exps. to avg. adv (%)

1.7

0.6

109bp

0.6

104bp

Source: Company, Angel Research

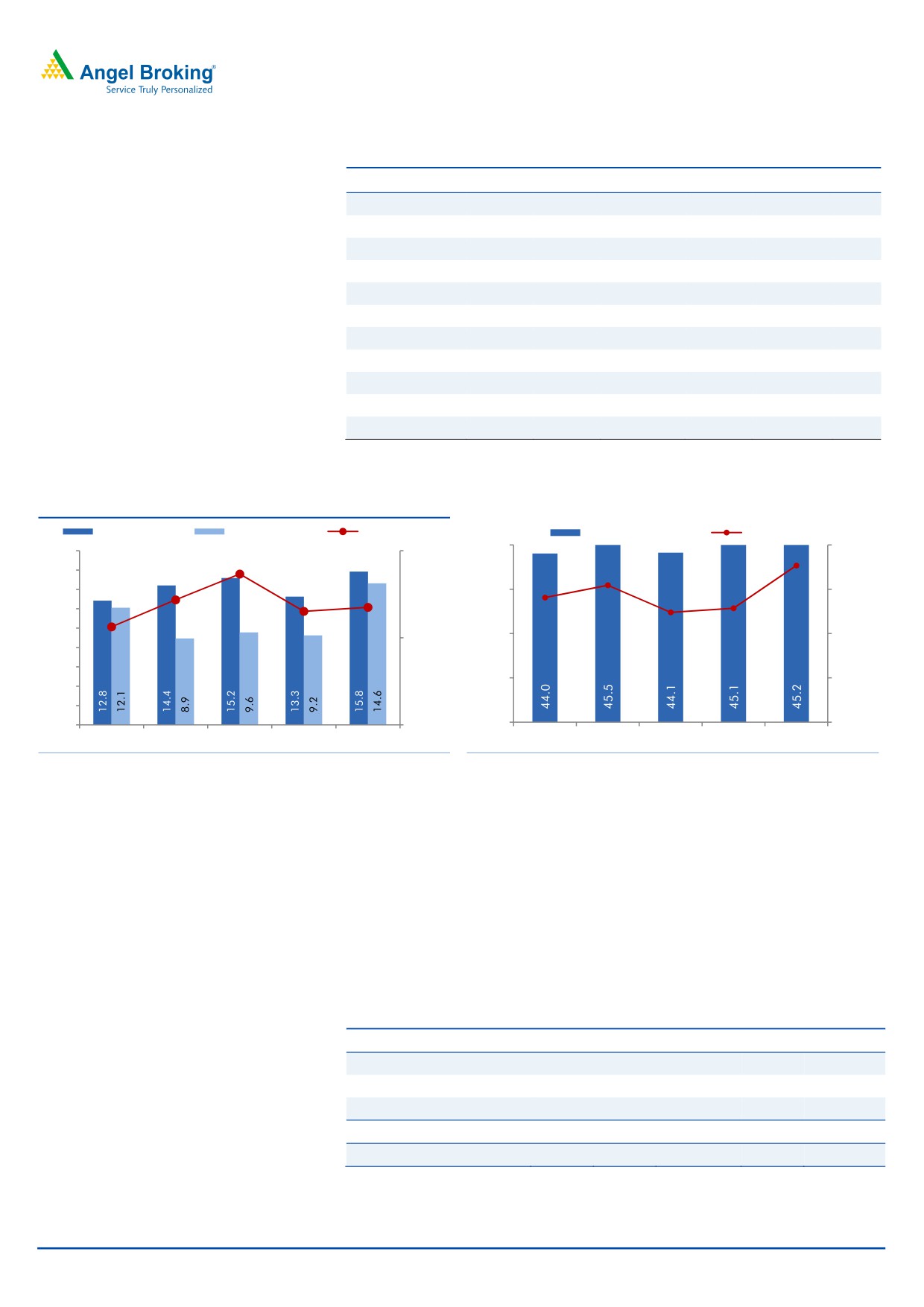

Healthy growth in advances, backed by retail loans

During 3QFY2016, the bank’s advances grew by 15.8% yoy (6.1% qoq), aided by

healthy retail loan book growth of 24% yoy. The main drivers leading to the

growth in the retail loan book were Personal loans and Home loans. Retail

contribution to total loans, increased to 43.8% as compared to 40.9% in 3QFY15.

The corporate book grew 10.2% yoy. NII grew by 13.3% yoy to `5,453 cr largely

in line with expectations. Due to high slippages the bank took provision of

`2,844cr vs `980cr in 3QFY15, up by 190%. However, proceeds from stake sale

in Life Insurance business helped reporting PAT growth of 4.5% to `3,018 cr.

Deposits growth picked up

Deposits growth picked up in 3QFY16 growing by 14.6% yoy compared to 9.2%

growth reported in 2QFY16. CASA deposits also accelerated growing by 17.7%

yoy, resulting in improvement in CASA ratio by 120bp yoy to 45.2%. The Reported

NIM improved marginally by by 1bp qoq to 3.53%, with domestic NIM at 3.86%

as compared to 3.84% in 2QFY2016. Fee income reported a modest growth of

7.2% yoy.

January 29, 2016

3

ICICI Bank | 3QFY2016 Result Update

Exhibit 3: Retail lending supports Loan Growth

Particulars (` cr)

3QFY16

2QFY16

% chg (qoq) 3QFY15

% chg (yoy) % total

Domestic Corporate

1,25,222

1,16,353

7.6

1,08,850

15.0

28.4

Overseas branches

99,134

95,458

3.9

96,464

2.8

23.3

SME

20,001

17,617

13.5

16,515

21.1

4.3

Retail Total

1,90,442

1,80,265

5.6

1,53,516

24.1

44.0

-Home

1,04,553

99,326

5.3

84,434

23.8

55.1

-Vehicle loans

33,708

32,267

4.5

28,708

17.4

17.9

-Others

27,805

25,778

7.9

21,953

26.7

14.3

-Banking business

10,093

10,095

(0.0)

8,136

24.1

5.6

-Credit cards

5,142

4,507

14.1

3,838

34.0

2.5

-Personal loans

9,141

8,292

10.2

6,448

41.8

4.6

Total advances

4,34,800

4,09,693

6.1

3,75,345

15.8

100.0

Source: Company, Angel Research

Exhibit 4: Retail segment supports Advances growth

Exhibit 5: CASA ratio rises, CASA deposits up 17.7% yoy

Adv. yoy growth

Dep. yoy growth

CDR (%, RHS)

CASA ratio (%)

yoy Growth

45.0

20.0

18.0

110.0

108.7

16.0

15.5

107.2

14.1

14.0

106.7

40.0

12.9

17.7

15.0

106.5

12.4

12.0

105.6

10.0

35.0

10.0

105.0

8.0

6.0

30.0

5.0

4.0

2.0

-

100.0

25.0

-

3QFY15

4QFY15

1QFY16

2QFY16

3QFY16

3QFY15

4QFY15

1QFY16

2QFY16

3QFY16

Source: Company, Angel Research

Source: Company, Angel Research

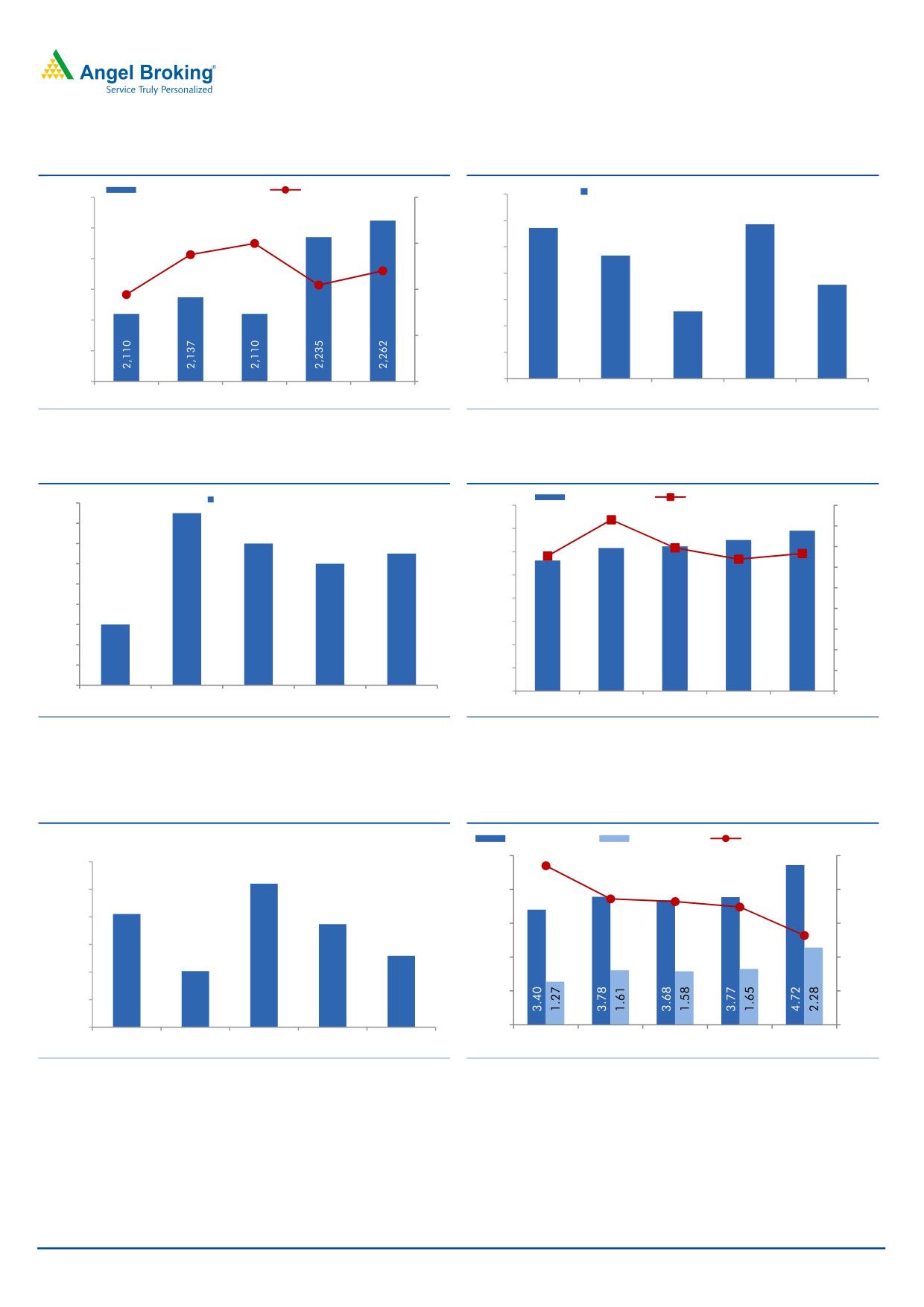

Muted growth in fee income

The core fee income growth remained muted up by only 7.2% yoy. The bank

booked profit of `1,243cr on sale of 4% stake in its life insurance business during

the quarter. Excluding this onetime gain the non interest income would have

declined by 3.9% yoy. However, the bank is likely to get approval from the

concerned authorities for balance 2% stake sale in Life Insurance business and 9%

stake sales in its General Insurance business, which might flow in the coming

quarters.

Exhibit 6: ‘Treasury Income’ aides non-interest income performance

Particulars (` cr)

3QFY16 2QFY16

% chg (qoq) 3QFY15

% chg (yoy)

Fee income

2,262

2,235

1.2

2,110

7.2

Treasury

1,442

222

549.5

443

225.5

Others

513

550

(6.7)

538

(4.6)

Non-interest income

4,217

3,007

40.2

3,091

36.4

Non-int. income excl. treasury

2,775

2,785

(0.4)

2,648

4.8

Source: Company, Angel Research

January 29, 2016

4

ICICI Bank | 3QFY2016 Result Update

Exhibit 7: Fee income growth at 7.2% yoy

Exhibit 8: Share of fee income

Fee Income (` cr)

yoy growth (%, RHS)

Fee income to average assets (%)

2,300

12.0

1.4

9.0

1.4

1.4

1.4

2,250

8.3

9.0

1.4

1.4

2,200

7.2

5.7

6.3

1.3

1.3

2,150

6.0

1.3

1.3

2,100

1.3

3.0

2,050

1.3

2,000

-

1.3

3QFY15

4QFY15

1QFY16

2QFY16

3QFY16

3QFY15

4QFY15

1QFY16

2QFY16

3QFY16

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 9: NIM improves marginally on qoq basis

Exhibit 10: NII growth trends

NIM (Reported, %)

NII (` cr)

YoY growth (%, RHS)

3.58

6,000

18.0

3.56

16.0

5,500

3.54

14.0

5,000

3.52

16.6

13.9

12.0

13.1

13.3

4,500

12.8

3.50

10.0

4,000

3.48

8.0

3.46

3,500

6.0

3.44

3,000

4.0

3.42

2,500

3.46

3.57

3.54

3.52

3.53

2.0

3.40

2,000

-

3QFY15

4QFY15

1QFY16

2QFY16

3QFY16

3QFY15

4QFY15

1QFY16

2QFY16

3QFY16

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 11: O/s Restructured book declines qoq

Exhibit 12: Asset quality during the quarter

(` cr)

Gross NPAs (%)

Net NPAs (%)

Coverage ratio (%, RHS)

5.00

65.0

13,000

12,604

63.5

58.6

58.2

12,500

4.00

57.4

60.0

12,052

11,868

12,000

53.2

3.00

55.0

11,500

11,294

11,017

2.00

50.0

11,000

1.00

45.0

10,500

10,000

-

40.0

3QFY15

4QFY15

1QFY16

2QFY16

3QFY16

3QFY15

4QFY15

1QFY16

2QFY16

3QFY16

Source: Company, Angel Research

Source: Company, Angel Research

Asset Quality deteriorated sharply

Slippages went up sharply to `6,544cr (annualized slippage ratio at 6.8%) as

compared to `2,242cr in the sequential previous quarter (annualized slippage

ratio at 2.3%), with slippage from restructuring at `1,355 cr. 2/3 rd of the

slippages during the quarter came from the RBI highlighted accounts, with a large

January 29, 2016

5

ICICI Bank | 3QFY2016 Result Update

steel account being classified as NPA. The Gross NPA ratio increased 95bp

sequentially to 4.72%, whereas the Net NPA rose 63bp qoq to 2.28%. The bank

refinanced ~`450cr under the 5:25 scheme and SDR worth `1,670cr and expects

SDR of `700cr and 5:25 of `1,200cr in 4QFY16 and the management has guided

for similar level of slippages in 4QFY16 as well. Outstanding restructured loans

came down to `11,294cr at the end of 3QFY16 vs `11,868cr in 2QFY16.

Overview of performance of subsidiaries

ICICI Bank’s consolidated net profit for 3QFY2016 declined by 4.55% yoy to

`3,122cr. The consolidated reported RoE came in at 13.5% for 3QFY2016 as

compared to 15.5% in 3QFY2015.

ICICI Bank’s overseas subsidiary, ICICI Bank UK’s earnings remained flat yoy

during 3QFY2016 while ICICI Bank Canada’s earnings increased 88% yoy.

ICICI Prudential AMC reported a PAT of `82cr for 3QFY2016 as compared to

a PAT of `67cr for 3QFY2015.

ICICI Lombard General Insurance reported a 26% decline in PAT at `130 cr

for 3QFY2016, as against `176cr in 3QFY2015 whereas ICICI Home Finance

reported a PAT of `40 cr for 3QFY2016 as against a PAT of `50 cr in

3QFY2015. Earnings for ICICI Securities came in at `55cr for 3QFY2016

compared to `76 cr.

Exhibit 13: Performance of subsidiaries

Subsidiary

Parameter

3QFY16

3QFY15

% chg

FY2015

FY2014

% chg

ICICI Bank UK

PAT (USD mn)

6.1

6.1

-

18.3

25.2

(27.4)

ICICI Bank Canada

PAT (CAD mn)

5.4

3.0

80.0

33.7

48.3

(30.2)

ICICI Home Finance

PAT (` cr)

40

50

(19.4)

198.0

223.0

(11.2)

ICICI Prudential Life Insurance

APE (` cr)

1,259

1,290

(2.4)

4,744.0

3,444.0

37.7

NBP (` cr)

174

147

18.4

532.0

427.0

24.6

NBP margin (%)

14

11

21.1

11

12

-

AuM (` cr)

1,01,731

94,593

7.5

1,00,183

80,597

24.3

ICICI Lombard General Insurance

Gross Premium (` cr)

2,072

1,708

21.3

6,914

7,134

(3.1)

PAT (` cr)

130

176

(26.1)

536

511

4.9

ICICI Securities

PAT (` cr)

55

76

(27.6)

294

91

223.1

ICICI Securities PD

PAT (` cr)

63

75

(16.0)

217

132

64.4

ICICI Venture

PAT (` cr)

(9)

5

(280.0)

1

33

(97.0)

ICICI Prudential AMC

PAT (` cr)

82

67

22.4

247

183

35.0

Source: Company, Angel Research

Outlook and Valuation

At the current market price, the bank’s core banking business (after adjusting

`67/share towards the value of subsidiaries) is trading at 1.1x FY2017E ABV. The

stock has corrected in the last one quarter due to concerns over deteriorating asset

quality. Though pain in asset quality is likely to persist in the quarters to come, we

believe the current valuations adequately factor in the relatively higher stressed

assets in the bank’s books. We recommend an Accumulate rating on the stock,

with a revised target price of `254.

January 29, 2016

6

ICICI Bank | 3QFY2016 Result Update

Exhibit 14: SOTP valuation summary

Particulars

Target multiple

Value/share (`)

ICICI Bank

1.1x FY2017E ABV

187

Life Insurance

34.0x FY2017E NBP

33

General Insurance

32x FY2014 PAT

17

Others (Home Fin, AMC, VC, Securities

18

PD and Overseas subsidiaries)

SOTP value

254

Source: Angel Research

Exhibit 15: Recommendation summary

CMP

Tgt. Price

Upside

FY2017E

FY2017E

FY2017E

FY15-17E

FY2017E

FY2017E

Company

Reco.

(`)

(`)

(%)

P/ABV (x)

Tgt. P/ABV (x)

P/E (x)

EPS CAGR (%)

RoA (%)

RoE (%)

HDFCBk

Buy

1,049

1,262

20.3

3.2

3.8

17.2

22.4

1.9

19.7

ICICIBk*

Accumulate

230

254

10.3

1.6

1.3

9.4

13.5

1.6

14.7

YesBk

Neutral

747

-

-

1.9

2.0

10.7

20.5

1.6

19.6

AxisBk

Buy

408

494

21.0

1.7

2.0

9.4

18.4

1.8

18.9

SBI*

Accumulate

180

202

12.1

0.9

0.8

7.4

17.8

0.7

12.8

FedBk

Neutral

46

-

-

0.9

0.9

8.3

(2.9)

0.9

10.8

SIB

Neutral

19

-

-

0.7

0.7

5.6

21.6

0.7

11.6

BOB

Neutral

126

-

-

0.7

0.7

6.0

17.5

0.6

10.6

PNB

Neutral

91

-

-

0.4

0.4

3.3

28.5

0.7

12.0

BOI

Neutral

100

-

-

0.3

0.7

3.0

14.0

0.3

7.6

IndBk

Neutral

91

-

-

0.3

0.3

3.1

19.4

0.6

8.6

Vijaya Bank

Neutral

31

-

-

0.4

0.4

4.7

14.1

0.4

8.8

OBC

Neutral

112

-

-

0.2

0.3

2.5

65.5

0.5

9.4

Allahabad Bank Neutral

54

-

-

0.2

0.2

2.0

56.2

0.6

11.9

UnionBk

Neutral

130

-

-

0.4

0.3

3.3

18.1

0.6

11.4

CanBk

Neutral

194

-

-

0.3

0.2

2.8

12.0

0.6

11.2

IDBI#

Neutral

59

-

-

0.4

0.5

4.1

61.6

0.6

9.3

DenaBk

Neutral

36

-

-

0.3

0.4

3.6

45.6

0.4

7.9

Source: Company, Angel Research; Note:*Target multiples=SOTP Target Price/ABV (including subsidiaries), #Without adjusting for SASF

Company Background

ICICI Bank is India's largest private sector bank, with more than 5% market share

in credit. The bank has a pan-India extensive network of 4,156 branches and

around 13,372 ATMs. The bank has a large overseas presence (overseas loans

comprise ~23% of total loans). The bank also has market-leading subsidiaries in

life insurance, general insurance and asset management segments.

January 29, 2016

7

ICICI Bank | 3QFY2016 Result Update

Income statement (Standalone)

Y/E March (` cr)

FY12

FY13

FY14

FY15

FY16E

FY17E

Net Interest Income

10,734

13,866

16,476

19,040

21,824

25,222

- YoY Growth (%)

19.0

29.2

18.8

15.6

14.6

15.6

Other Income

7,503

8,346

10,428

12,064

13,344

15,295

- YoY Growth (%)

12.9

11.2

24.9

15.7

10.6

14.6

Operating Income

18,237

22,212

26,903

31,104

35,168

40,517

- YoY Growth (%)

16.4

21.8

21.1

15.6

13.1

15.2

Operating Expenses

7,850

9,013

10,309

11,496

12,933

14,988

- YoY Growth (%)

18.6

14.8

14.4

11.5

12.5

15.9

Pre - Provision Profit

10,386

13,199

16,595

19,608

22,235

25,529

- YoY Growth (%)

14.8

27.1

25.7

18.2

13.4

14.8

Prov. & Cont.

1,589

1,810

2,631

3,927

4,531

4,724

- YoY Growth (%)

(30.6)

13.9

45.4

49.2

15.4

4.2

Profit Before Tax

8,797

11,390

13,963

15,681

17,704

20,805

- YoY Growth (%)

30.2

29.5

22.6

12.3

12.9

17.5

Prov. for Taxation

2,332

3,064

4,153

4,636

5,225

6,125

- as a % of PBT

26.5

26.9

29.7

29.6

29.5

29.4

PAT

6,465

8,325

9,810

11,045

12,479

14,680

- YoY Growth (%)

25.5

28.8

17.8

12.6

13.0

17.6

Balance sheet (Standalone)

Y/E March (` cr)

FY12

FY13

FY14

FY15

FY16E

FY17E

Share Capital

1,503

1,504

1,505

1,517

1,517

1,517

- Equity

1,153

1,154

1,155

1,167

1,167

1,167

- Preference

350

350

350

350

350

350

Reserve & Surplus

59,252

65,552

72,052

79,107

87,837

98,134

Deposits

2,55,500

2,92,614

3,31,914

3,61,563

4,19,413

4,94,907

- Growth (%)

13.3

14.5

13.4

8.9

16.0

18.0

Borrowings

1,02,200

1,05,329

1,14,224

1,31,467

1,45,170

1,62,894

Tier 2 Capital

37,615

39,662

40,185

40,600.0

39,585

38,595

Other Liab. & Prov.

17,577

21,307

34,762

31,875

35,926

41,302

Total Liabilities

4,73,647

5,25,968

5,94,642

6,46,129

7,29,448

8,37,349

Cash Balances

20,461

19,053

21,822

25,653

20,971

24,745

Bank Balances

15,768

22,365

19,708

16,652

21,508

24,745

Investments

1,59,560

1,71,394

1,77,022

1,86,583

2,03,977

2,19,093

Advances

2,53,728

2,90,249

3,38,703

3,87,522

4,49,526

5,30,440

- Growth (%)

17.3

14.4

16.7

14.4

16.0

18.0

Fixed Assets

4,615

4,647

4,678

4,723

5,183

5,784

Other Assets

19,515

18,261

32,709

24,997

28,284

32,541

Total Assets

4,73,647

5,25,968

5,94,642

6,46,129

7,29,448

8,37,349

- Growth (%)

17.1

11.4

13.4

8.8

13.1

15.1

January 29, 2016

8

ICICI Bank | 3QFY2016 Result Update

Ratio analysis (Standalone)

Y/E March

FY12

FY13

FY14

FY15

FY16E

FY17E

Profitability ratios (%)

NIMs

2.7

3.0

3.2

3.3

3.4

3.4

Cost to Income Ratio

43.0

40.6

38.3

37.0

36.8

37.0

RoA

1.3

1.5

1.6

1.6

1.6

1.6

RoE

12.8

14.7

14.9

14.8

14.7

15.2

B/S ratios (%)

CASA Ratio

43.5

41.9

42.9

45.5

45.9

46.2

Credit/Deposit Ratio

99.3

99.2

102.0

107.2

107.2

107.2

CAR

18.5

18.7

17.7

17.6

16.4

15.1

- Tier I

12.7

12.8

12.8

12.6

12.2

11.6

Asset Quality (%)

Gross NPAs

3.6

3.2

3.0

3.8

4.7

4.8

Net NPAs

0.7

0.8

1.0

1.6

1.9

1.7

Slippages

1.3

1.4

1.5

2.3

2.5

1.9

Loan Loss Prov. /Avg. Assets

0.2

0.3

0.4

0.5

0.6

0.5

Provision Coverage

80.4

76.8

68.6

62.5

62.5

67.5

Per Share Data (`)

EPS

11.2

14.4

17.0

18.9

21.4

25.2

ABVPS (75% cover.)

104.8

115.6

120.9

116.7

124.9

149.8

DPS

3.3

4.0

4.5

6.3

5.9

6.9

Valuation Ratios

PER (x)

24.7

19.2

16.3

14.6

13.0

11.0

P/ABVPS (x)

2.6

2.4

2.3

2.4

2.2

1.8

Dividend Yield

1.2

1.4

1.6

2.3

2.1

2.5

DuPont Analysis

NII

2.5

2.8

3.0

3.1

3.2

3.3

(-) Prov. Exp.

0.4

0.4

0.5

0.6

0.7

0.6

Adj. NII

2.1

2.5

2.5

2.5

2.6

2.7

Treasury

(0.0)

0.1

0.1

0.2

0.2

0.2

Int. Sens. Inc.

2.1

2.6

2.7

2.7

2.8

2.9

Other Inc.

1.6

1.4

1.5

1.5

1.5

1.5

Op. Inc.

3.7

4.0

4.2

4.2

4.3

4.4

Opex

1.8

1.9

1.9

1.9

1.9

1.9

PBT

1.9

2.2

2.3

2.3

2.3

2.4

Taxes

0.5

0.6

0.8

0.8

0.8

0.8

RoA

1.3

1.5

1.6

1.6

1.6

1.6

Leverage

9.6

9.6

9.6

9.5

9.4

9.4

RoE

12.8

14.7

14.9

14.8

14.7

15.2

January 29, 2016

9

ICICI Bank | 3QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

ICICI Bank

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

January 29, 2016

10