2QFY2016 Result Update | Cons. Durables

October 30, 2015

Hitachi Home & Life Solutions

NEUTRAL

CMP

`1,346

Performance Highlights

Target Price

-

Y/E March (` cr)

2QFY2016 1QFY2014

% chg (yoy) 4QFY2014 % chg (qoq)

Investment Period

-

Net sales

251

254

(1.2)

709

(64.6)

EBITDA

(5)

16.3

(128.0)

87

(105.3)

EBITDA margin (%)

(1.8)

6.4

(822)bp

12.2

(1402)bp

Stock Info

Reported PAT

(10.7)

9.1

(218.1)

46.5

(123.1)

Sector

Cons. Durable

Source: Company, Angel Research

Market Cap (` cr)

3,659

Hitachi Home & Life Solutions (India) Ltd (HHLS) reported a disappointing set of

Net Debt

134

numbers for 2QFY2016. Although the decline in the top-line is of 1.2% on a yoy

Beta

1.1

52 Week High / Low

1,745 / 551

basis to `251cr, but the same is far lower than our expectation of `320cr. HHLS

Avg. Daily Volume

25,009

reported an EBITDA loss of `4.5cr for the quarter as against a positive EBITDA of

Face Value (`)

10

`16.3cr in the same quarter last year. A jump of 387bp yoy and 398bp yoy in

BSE Sensex

26,657

raw material cost and other expenses as a percentage of sales, respectively, led to

Nifty

8,066

an 822bp yoy decline in the EBITDA margin. As a result, HHLS reported a net loss

Reuters Code

HITA.NS

of `10.7cr for the quarter as against a net profit of `9.1cr in the corresponding

Bloomberg Code

HTHL IN

quarter of the previous year.

Favorable outlook for the room AC (RAC) segment to support growth: The

domestic economy is now expected to improve, after having witnessed a phase of

Shareholding Pattern (%)

lackluster growth in the past few years. We believe that steady economic growth

Promoters

74.3

will lead to higher disposable incomes in the hands of the consumers, thus

MF / Banks / Indian Fls

7.6

triggering higher demand for room ACs. Also the company will benefit from the

FII / NRIs / OCBs

1.5

improved demand from the commercial/institutional clients for its ductable ACs.

Indian Public / Others

16.7

Strong technological support from parent: HHLS has been sourcing advanced

technology from its Japanese parent which has enabled it to launch superior

products in the Indian market. “Hitachi” enjoys a strong brand pull, which has

Abs.(%)

3m 1yr 3yr

helped the company to steadily grow its market share in India. As per HHLS, their

Sensex

(2.6)

(1.0)

44.0

market share in the room AC segment has improved from a mere 5.3% in

HHLS

(8.7)

123.7

922.4

FY2009 to 13.3% in FY2015. We expect the company to successfully leverage on

both, the technical support and brand strength, to grow in India.

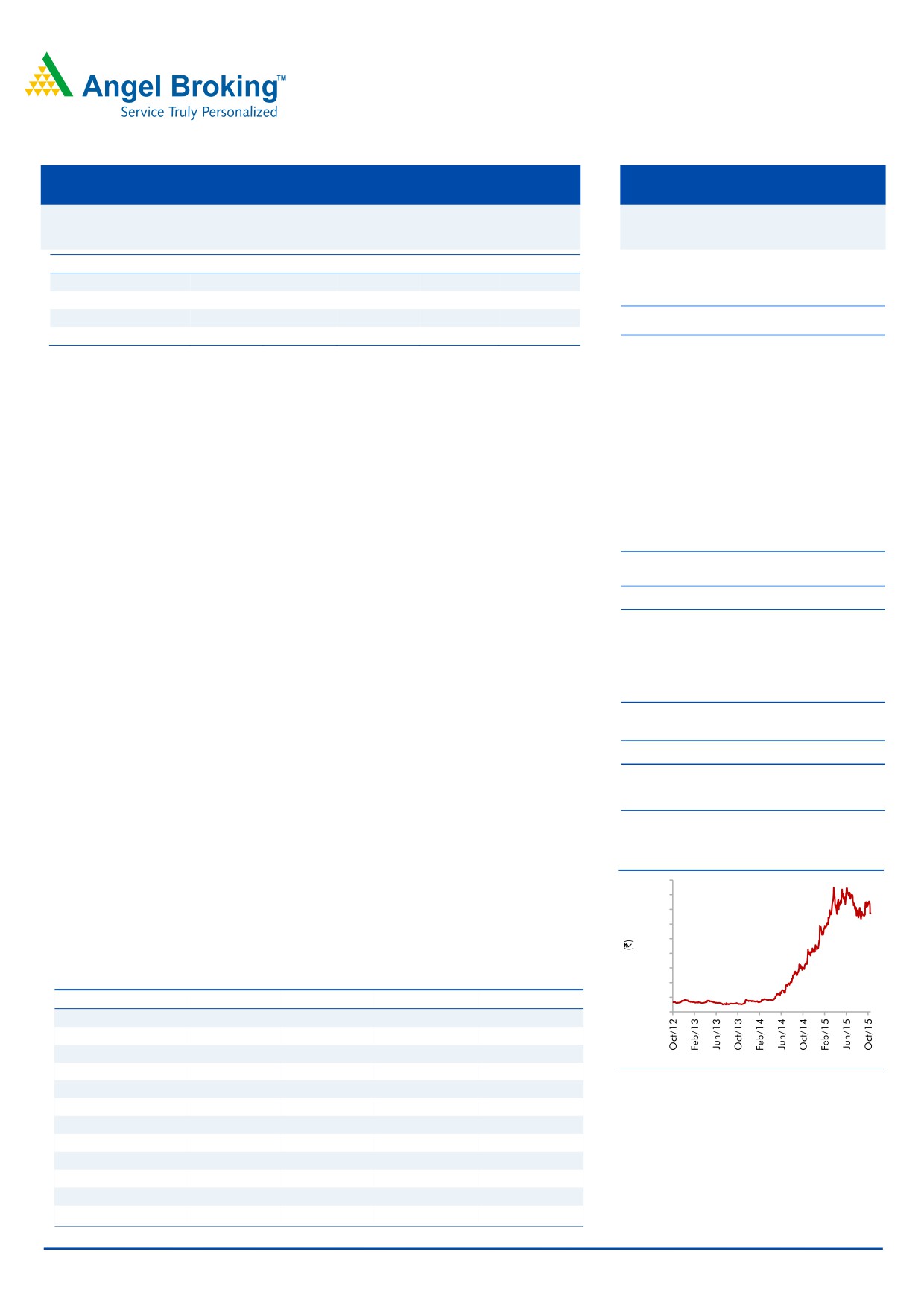

3 Year Price Chart

Outlook and valuation: We expect HHLS to post a 15.0% CAGR in revenue over

1,800

FY2015-17E to `2,081cr. The EBITDA margin is expected to be at 8.8% in

1,600

FY2017E. PAT is expected to post a CAGR of 8.1% over FY2015-17E to `91cr. At

1,400

1,200

the current levels, the stock is trading at a PE of 40.2x its FY2016E earnings which

1,000

we believe is expensive. We maintain our Neutral view on the stock.

800

600

Key financials

400

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

200

-

Net sales

1,100

1,573

1,779

2,081

% chg

18.3

43.0

13.1

17.0

Net profit

8

78

59

91

% chg

(47.8)

866.1

(23.8)

53.3

EBITDA margin (%)

5.6

9.0

7.8

8.8

EPS (`)

3.0

28.6

21.8

33.4

P/E (x)

454.5

47.0

61.7

40.2

P/BV (x)

15.2

11.7

10.0

8.1

RoE (%)

3.4

28.1

17.4

22.1

RoCE (%)

7.7

24.0

19.0

24.0

Milan Desai

EV/Sales (x)

3.4

2.4

2.1

1.8

+91- 22- 4000 3600 Ext: 6846

EV/EBITDA (x)

61.6

26.8

27.2

20.3

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

HHLS | 2QFY2016 Result update

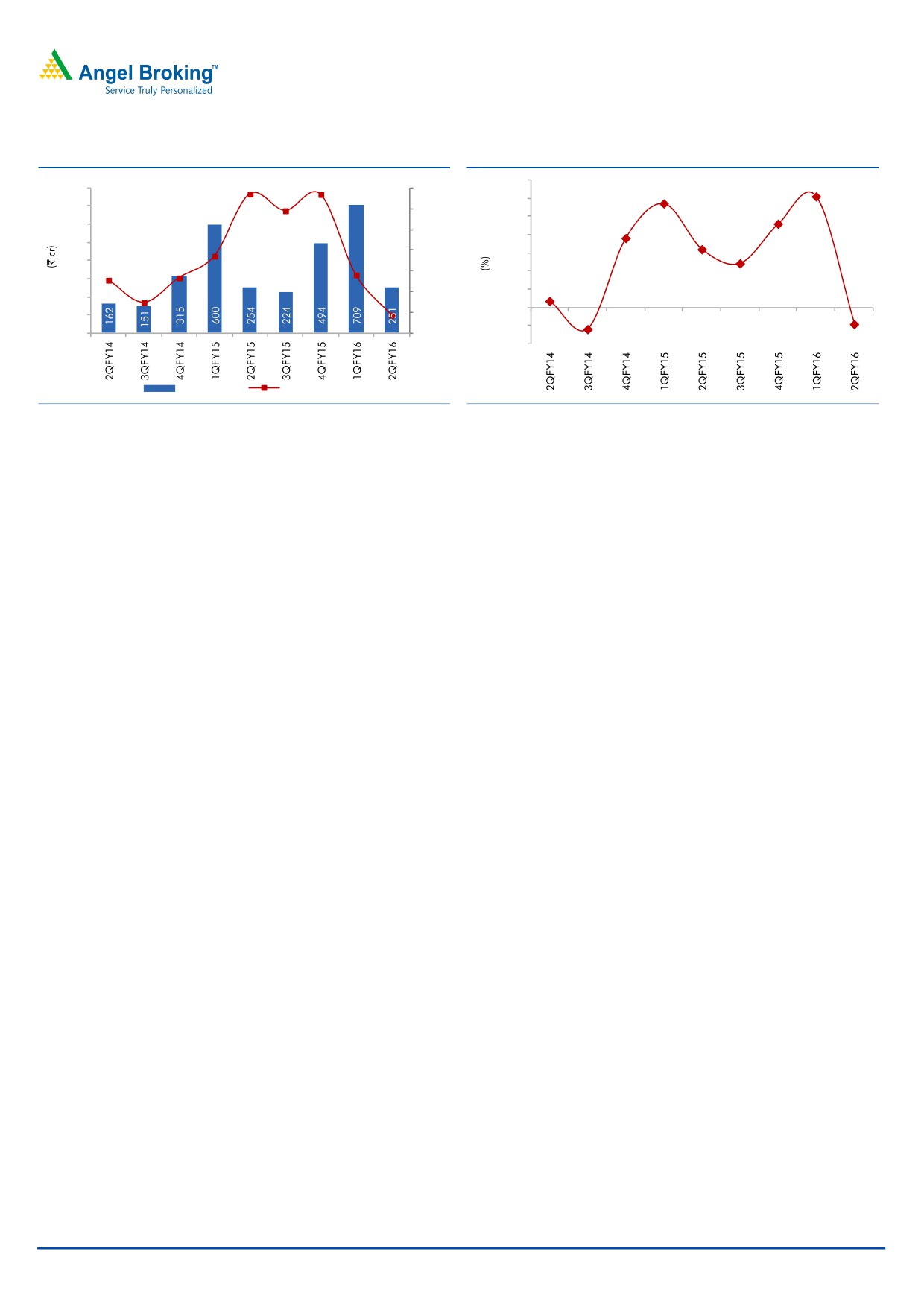

Exhibit 1: 2QFY2016 performance

Y/E March (` cr)

2QFY16

2QFY15

yoy chg (%)

1QFY15

qoq chg (%)

1HFY16

1HFY15

% chg

Net Sales

251

254

(1.2)

709

(64.6)

959

854

12.3

Net raw material

159

151

5.2

445

(64.2)

604

529

14.2

(% of Sales)

63.5

59.7

387bp

62.8

63.0

61.9

Staff Costs

26

25

2.5

28

(9.9)

54

53

1.8

(% of Sales)

10.2

9.8

37bp

4.0

5.6

6.2

Other Expenses

70

61

15.1

149

(52.7)

219

187

17.2

(% of Sales)

28.1

24.1

398bp

21.0

22.9

21.9

Total Expenditure

255

237

7.4

622

(59.0)

877

769

14.1

EBITDA

(5)

16

(128.0)

87

(105.3)

82

85

(3.4)

EBITDA margin (%)

(1.8)

6.4

(822)bp

12.2

(1402)bp

8.5

9.9

(139)bp

Interest (incl. forex losses)

3

3

2.2

6

(54.8)

9

5

86.8

Depreciation

10

8

28.4

11

(7.0)

22

16

36.0

Other Income

0

3

(85.2)

0

11.0

1

4

(82.8)

PBT

(17)

8

(316.3)

70

(124.9)

52

68

(23.6)

(% of Sales)

(6.9)

3.2

9.8

5.4

8.0

Tax

(7)

(1)

525.0

23

(128.7)

16

16

0.8

(% of PBT)

38.2

(13.2)

33.2

31.5

23.9

Reported PAT

(11)

9

(218.1)

47

(123.1)

36

52

(31.3)

PATM

(4.3)

3.6

6.6

3.7

6.1

Equity capital (cr)

23

23

23

23

23

EPS (`)

(4.7)

4.0

(218.1)

20.3

(123.1)

15.6

22.7

(31.3)

Source: Company, Angel Research

Exhibit 2: 2QFY2016 - Actual vs. Angel estimates

(` cr)

Actual

Estimate

Variation (%)

Net Sales

251

320

(21.6)

EBITDA

(4.5)

20.8

(121.9)

EBIDTA margin (%)

(1.8)

6.5

(831)bp

Adjusted PAT

(11)

6

(267.5)

Source: Company, Angel Research

Top-line disappoints; loss at EBITDA level

The top-line for 2QFY2016 declined by 1.2% yoy to `251cr, which is far below our

expectation of `320cr. Industry reports suggest the room AC segment grew by

~5% in value terms during the quarter. HHLS’s operating expenses during the

quarter increased by 7.4% on a yoy basis to `255cr, resulting in an EBITDA loss of

`5cr. The loss was due to a 387bp yoy increase in raw material costs as a

percentage of sales to 63.5%, and 398bp yoy increase in other expenses as a

percentage of sales to 28%. Employee expense grew by a marginal 37bp yoy to

10.2% of sales. On account of higher depreciation and lower other income, the

company reported a net loss of `11cr while we had estimated a net profit of `6cr

for the quarter.

October 30, 2015

2

HHLS | 2QFY2016 Result update

Exhibit 3: Revenue trend

Exhibit 4: EBITDA Margins

57.0

56.8

14.0

12.2

800

60.0

11.4

49.0

12.0

700

50.0

9.2

10.0

600

7.6

40.0

8.0

6.4

500

27.1

30.0

6.0

400

16.6

4.9

15.5

18.1

20.0

4.0

300

4.8

2.0

0.7

10.0

200

0.0

100

0.0

(1.2)

(2.0)

0

(10.0)

(2.4)

(1.8)

(4.0)

Revenue (LHS)

yoy growth (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

Updates on Open offer, Change in parent company

On January 14, 2015, HHLS’s parent - Hitachi Appliances, had divested its stake

in HHLS to a new proposed JV entity between Johnson Controls and Hitachi.

Johnson Controls would own 60% and Hitachi would hold the balance 40% in the

JV. On January 26, 2015, both the parties jointly made an offer to acquire

25.75% shares in HHLS at `821.38/share (against the then prevalent market price

of HHLS of `1,133). Upon completion of global acquisition on October 1, 2015,

Hitachi’s share holding in HHLS was transferred to JCHAC India Holdco Ltd which

is now being controlled by Johnson Controls-Hitachi Air Conditioning Holding (UK)

Ltd (the global joint venture between the Hitachi group and Johnson Controls). The

follow-up open offer was made on October 9, 2015 at `880.12/share.

October 30, 2015

3

HHLS | 2QFY2016 Result update

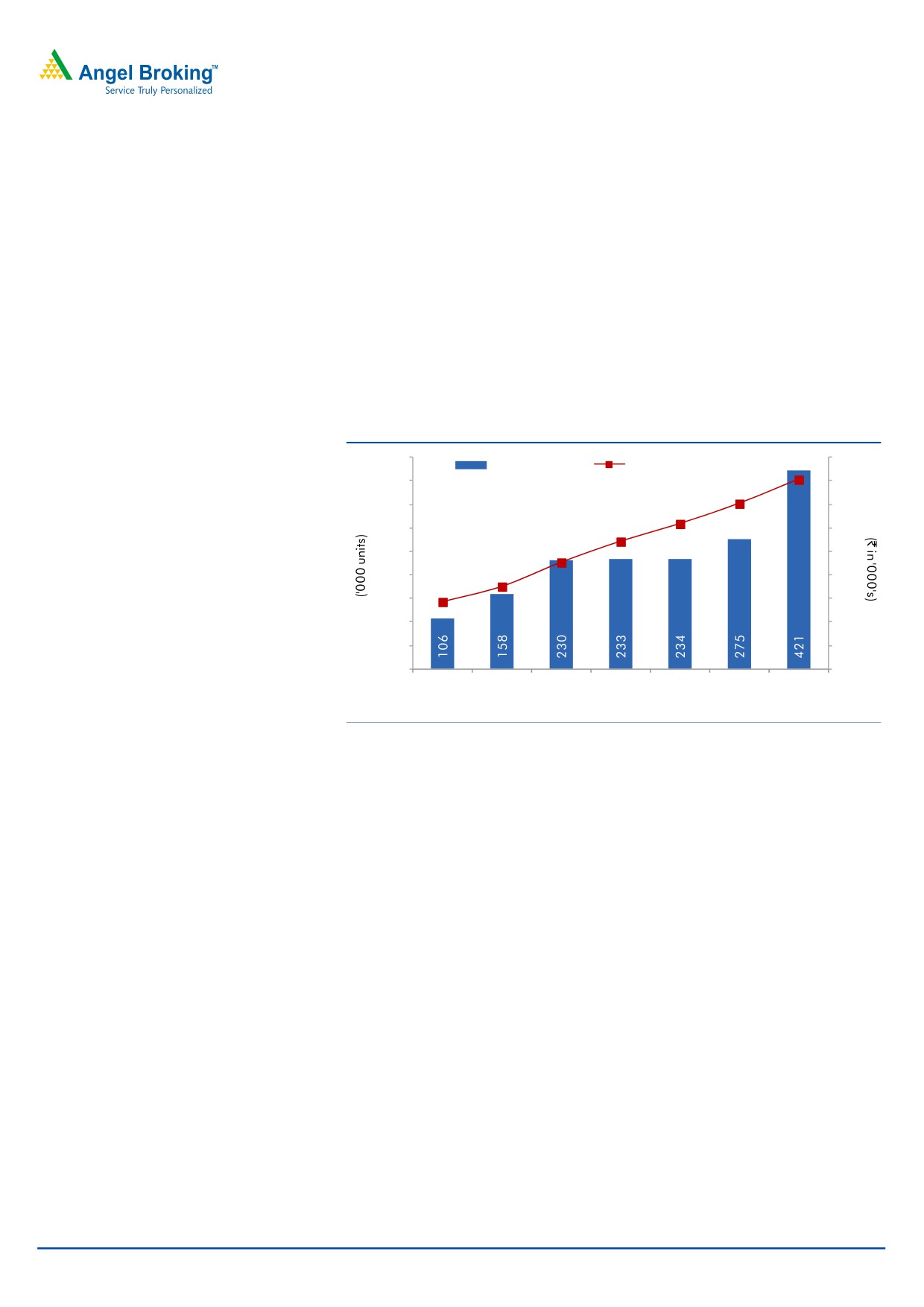

Investment rationale

Favorable outlook for the RAC industry

With an imminent improvement in economic conditions, the disposable income

levels of consumers in India are expected to improve, going forward. As per IMF

estimates, the per capita income in India grew at a 11.7% CAGR over FY2009-15

to `1,00,463 in FY2015 while HHLS’ room AC sales volume posted a 25.8%

CAGR over the same period. We believe that the expected improvement in

disposable incomes augurs well for HHLS’ room AC sales, going forward.

Moreover, industry reports suggest that the penetration levels of room ACs in India

are lower compared to most developed and developing markets.

Exhibit 5: RAC sales volume for HHLS vs per capita income

450

110

AC volume (LHS)

Per capita income (RHS)

100

400

100

90

350

82

90

300

74

80

65

250

70

55

200

60

48

150

50

100

40

50

30

0

20

FY09

FY10

FY11

FY12

FY13

FY14

FY15

Source: IMF, Angel Research

Apart from its premium range of products, the company has also diversified into

the low-priced AC segment. In order to widen its reach in tier II & tier III cities, the

company has expanded its distribution network to more than 4,000 outlets. Since

tier-II and tier-III cities are expected to be the major contributors to the growth in

the consumer durables segment going forward, revenue contribution from these

segments would add to the company’s top-line growth.

Strong technological support from parent

HHLS has been sourcing superior technology from its Japanese parent which has

enabled it to create a strong presence in the room AC segment. HHLS continues to

leverage on its strong parental roots in terms of R&D to launch superior products

for the Indian market. This association and the brand pull have helped the

company in steadily growing its market share in India. As per HHLS, its market

share in the RAC segment has improved from mere 5.3% in FY2009 to 13.3% in

FY2015.

October 30, 2015

4

HHLS | 2QFY2016 Result update

Financials

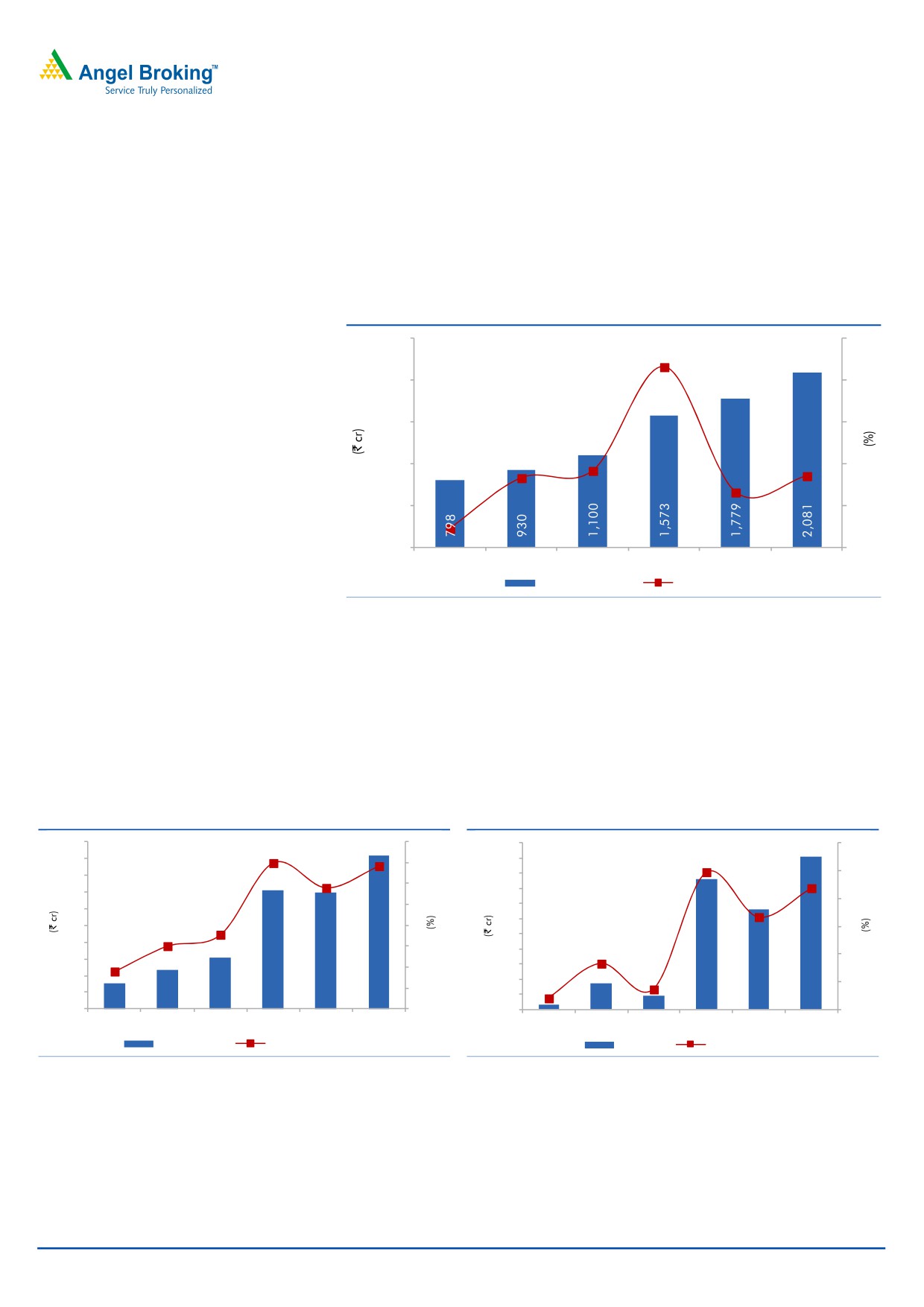

Revenue to grow at a CAGR of 15.0% over FY2015-17E

The company’s room AC segment has grown at more than twice the industry

growth rate over the last five years. We expect HHLS’ revenue to grow at a CAGR

of 15.0% over FY2015-17E to `2,081cr in FY2017E.

Exhibit 6: Revenue growth to be at 15.0% CAGR

2,500

50

43.0

2,000

40

1,500

30

1,000

16.5

18.3

20

17.0

13.1

500

10

4.5

0

0

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

Revenue (LHS)

Revenue growth (RHS)

Source: Company, Angel Research

EBITDA margins to consolidate at 8.8%

HHLS has relocated the manufacturing facilities in Jammu to its main plant at

Kadi, Gujarat in order to centralise the production activity. With an exception of the

current quarter, the benefits of this move are evident in the company’s operating

performance in the past few quarters. With improvement in volumes, we expect the

EBITDA margin to be at 8.8% and net profit to be at `91cr in FY2017E.

Exhibit 7: EBITDA margin trend

Exhibit 8: Net profit margin trend

200

10

99

6

9.0

8.8

180

90

4.9

9

7.8

81

5

160

8

4.4

72

140

3.3

4

7

63

120

5.6

54

100

6

3

5.0

45

80

5

36

1.7

3.8

2

60

4

27

40

0.7

18

0.4

1

20

3

30

47

61

141

139

184

9

15

78

59

91

3

8

0

2

0

0

FY2012

FY2013

FY2014 FY2015 FY2016E FY2017E

FY2012

FY2013

FY2014 FY2015 FY2016E FY2017E

EBITDA (LHS)

EBITDA margin (RHS)

PAT (LHS)

PAT margin (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

October 30, 2015

5

HHLS | 2QFY2016 Result update

Outlook and valuation

We expect HHLS to post a 15.0% CAGR in revenue over FY2015-17E. The EBITDA

margin is expected to be at 8.8% in FY2017E. PAT is expected to post a CAGR of

8.1% over FY2015-17E to `91cr. At the current levels, the stock is trading at a PE

of 40.2x its FY2016E earnings, which we believe is expensive. We maintain our

Neutral view on the stock.

Exhibit 9: One-year forward PE band

1800.0

1600.0

1400.0

1200.0

1000.0

800.0

600.0

400.0

200.0

0.0

Oct-10

Oct-11

Oct-12

Oct-13

Oct-14

Oct-15

Price

25x

35x

45x

55x

Source: Company, Angel Research

Exhibit 10: Relative valuation

Year end

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/EBITDA EV/Sales

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

HHLS

FY2017E

2,081

8.8

91

33.4

22.1

40.2

8.1

20.3

1.8

Blue Star

FY2017E

4,196

6.1

140

15.5

26.0

25.4

6.1

14.9

0.9

Voltas

FY2017E

6,413

8.9

463

14.1

18.0

20.2

3.4

15.4

1.3

Source: Angel Research, Bloomberg

Company Background

HHLS is part of a global joint venture between Johnson Controls of USA and

Hitachi Ltd. HHLS was transferred into a global joint venture between Johnson

Controls and Hitachi Air Conditioning Holding (UK) Ltd with the latter controlling

HHLS indirectly. Johnson Controls indirectly holds 60% in HHLS while Hitachi Ltd

owns the balance.

HHLS manufactures and sells ACs and is engaged in the trading of refrigerators,

washing machines and chillers. The company’s manufacturing capacity at Gujarat

has an installed capacity of of 2,30,000 units per annum. The company’s air

conditioners segment includes home ACs, commercial/ductable ACs and telecom

ACs. The company operates in the mass premium segment.

October 30, 2015

6

HHLS | 2QFY2016 Result update

Profit & Loss Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

Gross sales

1,019

1,199

1,707

1,941

2,275

Less: Excise duty

89

100

134

162

194

Net Sales

930

1,100

1,573

1,779

2,081

Total operating income

930

1,100

1,573

1,779

2,081

% chg

16.5

18.3

43.0

13.1

17.0

Net Raw Materials

603

697

960

1,118

1,297

Personnel

65

82

114

123

141

Other

216

260

358

399

459

Total Expenditure

883

1,039

1,432

1,640

1,897

EBITDA

47

61

141

139

184

% chg

53.8

31.1

131.3

(1.9)

32.7

(% of Net Sales)

5.0

5.6

9.0

7.8

8.8

Depreciation

20

30

36

41

45

EBIT

26

31

105

97

139

% chg

120.6

17.6

239.4

(7.5)

42.3

(% of Net Sales)

2.8

2.8

6.7

5.5

6.7

Interest (incl. forex loss on ECB)

7

25

11

15

11

Other Income

2

6

7

4

6

(% of Net sales)

0.2

0.5

0.5

0.2

0.3

PBT

21

11

101

87

134

% change

640.4

(45.5)

791.9

(13.7)

53.3

Tax

5

3

23

28

43

(% of PBT)

25.7

28.9

23.0

32.0

32.0

PAT (reported)

15

8

78

59

91

Extraordinary (Exp.)/Inc.

0

-

-

-

-

ADJ. PAT

15

8

78

59

91

% chg

371.7

(47.8)

866.1

(23.8)

53.3

(% of Net Sales)

1.7

0.7

4.9

3.3

4.4

Basic EPS (`)

6.7

3.0

28.6

21.8

33.4

Adjusted EPS (`)

6.7

3.0

28.6

21.8

33.4

% chg

371.7

(47.8)

866.1

(23.8)

53.3

October 30, 2015

7

HHLS | 2QFY2016 Result update

Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

SOURCES OF FUNDS

Equity Share Capital

23

27

27

27

27

Reserves & Surplus

159

213

286

340

427

Shareholders’ Funds

236

240

313

367

454

Total Loans

166

125

140

133

119

Deferred Tax Liability

0

(1)

1

1

1

Other Long Term Liabilities

0

0

0

0

0

Long Term Provisions

14

28

33

37

43

Total Liabilities

416

392

486

538

618

APPLICATION OF FUNDS

Gross Block

260

305

381

419

461

Less: Acc. Depreciation

82

110

138

179

224

Net Block

178

195

243

240

237

Capital Work-in-Progress

11

2

3

3

3

Goodwill

-

-

-

-

-

Investments

-

-

-

-

-

Long term Loans & adv

18

31

25

28

33

Other non current assets

0

-

-

-

-

Current Assets

625

532

808

883

1,057

Cash

72

22

6

23

51

Loans & Advances

28

29

27

31

36

Inventory

306

290

490

520

609

Debtors

165

188

284

308

361

Other current assets

55

1

1

1

1

Current liabilities

415

368

592

615

712

Net Current Assets

210

164

216

268

346

Misc. Exp. not written off

-

-

-

-

-

Total Assets

416

392

486

538

618

October 30, 2015

8

HHLS | 2QFY2016 Result update

Cash Flow Statement

Y/E March (` cr)

FY2013

FY2014 FY2015 FY2016E FY2017E

Profit before tax

21

11

101

87

134

Depreciation

20

30

36

41

45

Change in Working Capital

(22)

(4)

(69)

(34)

(50)

Other income

56

23

12

(4)

(6)

Direct taxes paid

(8)

(3)

(25)

(28)

(43)

Cash Flow from Operations

68

58

55

62

80

(Inc.)/Dec. in Fixed Assets

(44)

(37)

(76)

(38)

(42)

(Inc.)/Dec. in Investments

-

-

-

-

-

(Inc.)/Dec. In L.T loans & adv

(1)

(13)

6

(3)

(5)

Balances in current/ credit/ FD

0

20

(20)

-

-

Interest received

2

6

7

4

6

Others

(69)

(28)

12

-

-

Cash Flow from Investing

(113)

(51)

(71)

(37)

(41)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

67

(41)

15

(7)

(13)

Inc. /(Dec.) in long term provision

3

14

5

4

6

Dividend Paid (Incl. Tax)

(5)

(5)

(5)

(5)

(4)

Others

49

(24)

(14)

-

-

Cash Flow from Financing

114

(56)

0

(8)

(11)

Inc./(Dec.) in Cash

69

(50)

(16)

17

29

Opening Cash balances

3

72

22

6

23

Closing Cash balances

72

22

6

23

51

October 30, 2015

9

HHLS | 2QFY2016 Result update

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

237.2

454.5

47.0

61.7

40.2

P/CEPS

102.8

96.1

32.2

36.5

26.9

P/BV

15.5

15.2

11.7

10.0

8.1

Dividend yield (%)

0.1

0.0

0.0

0.0

0.0

EV/Sales

4.0

3.4

2.4

2.1

1.8

EV/EBITDA

80.6

61.6

26.8

27.2

20.3

EV / Total Assets

10.4

9.6

7.8

7.0

6.0

Per Share Data (`)

EPS (Basic)

6.7

3.0

28.6

21.8

33.4

EPS (fully diluted)

6.7

3.0

28.6

21.8

33.4

Cash EPS

15.5

14.0

41.8

36.9

50.1

DPS

1.8

1.5

1.5

1.5

1.5

Book Value

103.0

88.3

115.1

135.1

167.0

Dupont Analysis

EBIT margin

2.8

2.8

6.7

5.5

6.7

Tax retention ratio

0.7

0.7

0.8

0.7

0.7

Asset turnover (x)

3.3

3.0

3.3

3.5

3.7

ROIC (Post-tax)

7.0

6.0

17.0

12.9

16.7

Cost of Debt (Post Tax)

3.2

14.5

6.3

7.5

6.3

Leverage (x)

0.4

0.4

0.4

0.3

0.1

Operating ROE

8.6

2.4

21.5

14.5

18.3

Returns (%)

ROCE (Pre-tax)

8.3

7.7

24.0

19.0

24.0

Angel ROIC (Pre-tax)

9.8

9.8

24.9

19.7

25.8

ROE

7.6

3.4

28.1

17.4

22.1

Turnover ratios (x)

Asset Turnover

3.6

3.6

4.1

4.2

4.5

Inventory / Sales (days)

113

99

91

104

99

Receivables (days)

61

63

66

63

63

Payables (days)

151

138

122

137

137

WC (ex-cash) (days)

39

43

41

47

47

Solvency ratios (x)

Net debt to equity

0.4

0.4

0.4

0.3

0.1

Net debt to EBITDA

2.0

1.7

0.9

0.8

0.4

Interest Coverage

3.7

1.2

9.2

6.7

12.5

October 30, 2015

10

HHLS | 2QFY2016 Result update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

HHLS

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

October 30, 2015

11