2QFY2016 Result Update | Automobile

October 23, 2015

Hero MotoCorp

NEUTRAL

CMP

`2,619

Performance Highlights

Target Price

-

Y/E March (` cr)

2QFY16 2QFY15

% chg (yoy) 1QFY16

% chg (qoq)

Investment Period

-

Net Sales

6,837

6,915

(1.1)

6,955

(1.7)

EBITDA

1,083

935

15.9

1,048

3.4

Stock Info

EBITDA margin (%)

15.8

13.5

230 bp

15.1

70 bp

Sector

Automobile

Adj. PAT

772

763

1.1

750

2.9

Market Cap (` cr)

52,299

Source: Company, Angel Research

Net Debt (` cr)

(3,313)

Beta

0.7

Hero MotoCorp (HMCL)’s 2QFY2016 results have come in ahead of our

52 Week High / Low

3,272/2,252

estimates with the company positively surprising on the operating margin front.

Avg. Daily Volume

17,212

Revenues declined by 1% yoy to `6,837cr, although they are marginally ahead of

Face Value (`)

2

our estimate of

`6,657cr. While volumes declined by

7% yoy, the

BSE Sensex

27,288

realization/vehicle grew 6% yoy on account of price hikes, better product mix and

Nifty

8,252

higher spare sales. Despite the subdued top-line, the company’s margins

Reuters Code

HROM.BO

improved by 230bp yoy to 15.8% (better than our estimate of 14.7%). Soft

Bloomberg Code

HMCL@IN

commodity prices and cost control initiatives undertaken by the company under

the “Leap” program led to an improvement in margins. Given the strong

Shareholding Pattern (%)

operating performance, the net profit for the quarter came in at `772cr, beating

our expectation of `726cr.

Promoters

34.6

MF / Banks / Indian Fls

15.3

Outlook and valuation: HMCL’s volumes are likely to be subdued in the near

FII / NRIs / OCBs

38.4

term, given the poor sentiments in rural areas, which account for about half of the

Indian Public / Others

11.6

company’s sales. Deficient rainfall for a second consecutive year, and only a

moderate increase in the MSPs, have impacted rural income levels, and in turn

rural demand. Given the demand weakness, the company has also delayed its

Abs. (%)

3m 1yr 3yr

capacity expansion plans by two quarters. We believe, in the domestic two-

Sensex

(3.2)

2.7

46.1

wheeler universe, HMCL is likely to be most impacted by the rural slowdown,

Hero MotoCorp

(2.5)

(12.6)

41.6

given that rural demand accounts for a higher proportion of HMCL’s overall

sales, vis-a- vis competition. Also, the margins are likely to decline in 2HFY2016,

given the increase in advertising and branding expenses. We have broadly

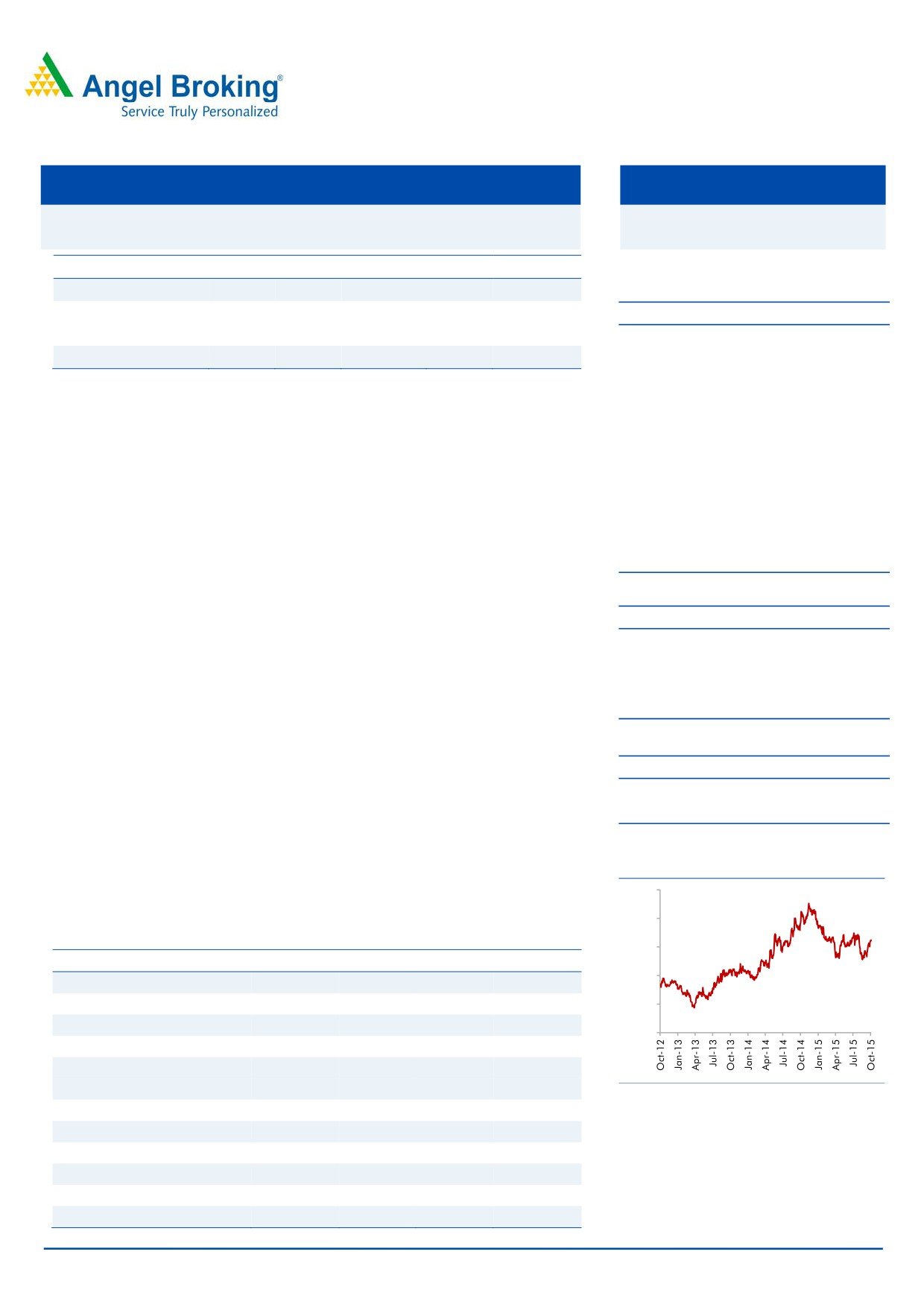

3-year price chart

retained our earnings estimates for both FY2016 and FY2017. We continue to

3,500

maintain a Neutral view on the stock.

3,000

Key financials (Standalone)

2,500

Y/E March (` cr)

FY2014

FY2015 FY2016E

FY2017E

2,000

Net Sales

25,275

27,585

28,561

31,559

% chg

6.3

9.1

3.5

10.5

1,500

Net Profit

2,109

2,386

3,018

3,259

1,000

% chg

(0.4)

13.1

26.5

8.0

EBITDA margin (%)

14.0

12.8

14.7

14.7

EPS (`)

105.6

127.2

151.1

163.2

Source: Company, Angel Research

P/E (x)

24.8

20.6

17.3

16.1

P/BV (x)

9.3

8.0

6.7

5.7

RoE (%)

37.7

38.8

38.7

35.6

RoCE (%)

51.7

53.2

53.6

48.8

Bharat Gianani

EV/Sales (x)

1.9

1.8

1.7

1.5

022-3935 7800 Ext: 6817

EV/EBITDA (x)

13.6

13.8

11.2

10.0

Source: Company, Angel Research; Note: CMP as of October 21, 2015

Please refer to important disclosures at the end of this report

1

Hero MotoCorp | 2QFY2016 Result Update

Exhibit 1: Quarterly financial performance (Standalone)

Y/E March (` cr)

2QFY16

2QFY15

% chg (yoy)

1QFY16

% chg (qoq)

1HFY16 1HFY15

% chg (yoy)

Net Sales

6,837

6,915

(1.1)

6,955

(1.7)

13,792

13,952

(1.1)

Consumption of RM

4,666

4,971

(6.1)

4,811

(3.0)

9,477

10,082

(6.0)

(% of Sales)

68.2

71.9

69.2

68.7

72.3

Staff Costs

310

285

8.7

314

(1.5)

624

553

12.9

(% of Sales)

4.5

4.1

4.5

4.5

4.0

Other Expenses

778

725

7.3

782

(0.6)

1,560

1,435

8.7

(% of Sales)

11.4

10.5

11.3

11.3

10.3

9.9

Total Expenditure

5,754

5,981

(3.8)

5,907

(2.6)

11,661

12,070

(3.4)

Operating Profit

1,083

935

15.9

1,048

3.4

2,131

1,882

8.7

OPM (%)

15.8

13.5

15.1

15.5

13.5

Interest

1

5

(89.1)

1

1.9

1

8

(86.5)

Depreciation

109

75

45.5

103

5.9

212

366

(42.1)

Other Income

103

194

(47.0)

102

0.7

205

306

(33.2)

PBT (excl. Extr. Items)

1,076

1,048

2.7

1,046

2.9

2,123

1,814

17.0

Extr. Income/(Expense)

-

-

-

-

-

PBT (incl. Extr. Items)

1,076

1,048

2.7

1,046

2.9

2,123

1,814

17.0

(% of Sales)

15.7

15.2

15.0

15.4

13.0

Provision for Taxation

304

285

6.8

296

2.8

600

488

23.1

(% of PBT)

28.3

27.2

28.3

28.3

26.9

Reported PAT

772

763

1.1

750

2.9

1,522

1,326

14.8

Adj PAT

772

763

1.1

750

2.9

1,522

1,326

14.8

Adj. PATM

11.3

11.0

10.8

11.0

9.5

Equity capital (cr)

39.9

39.9

39.9

39.9

39.9

Adjusted EPS (`)

38.7

38.2

1.1

37.6

2.9

76.2

66.4

14.8

Source: Company, Angel Research

Exhibit 2: 2QFY2016 - Actual vs Angel estimates

Y/E March (` cr)

Actual

Estimates

Variation (%)

Net Sales

6,837

6,657

2.7

EBITDA

1,083

980

10.5

EBITDA margin (%)

15.8

14.7

130 bp

Adj. PAT

772

726

6.4

Source: Company, Angel Research

Exhibit 3: Quarterly volume performance

(units)

2QFY16

2QFY15

% chg (yoy)

1QFY16

% chg (qoq)

1HFY16

1HFY15

% chg (yoy)

Total two-wheelers

1,574,861

1,692,523

(7.0)

1,645,853

(4.3)

3,220,714

3,407,654

(5.5)

Domestic

1,515,302

1,633,046

(7.2)

1,600,552

(5.3)

3,115,854

3,311,522

(5.9)

Exports

59,559

59,477

0.1

45,301

31.5

104,860

96,132

9.1

Motorcycles

1,402,270

1,497,690

(6.4)

1,477,047

(5.1)

2,879,317

3,020,419

(4.7)

Domestic

1,359,777

1,466,494

(7.3)

1,451,644

(6.3)

2,811,421

2,959,192

(5.0)

Exports

42,493

31,196

36.2

25,403

67.3

67,896

61,227

10.9

Scooters

172,591

194,833

(11.4)

168,806

2.2

341,397

387,235

(11.8)

Domestic

155,525

166,552

(6.6)

148,908

4.4

304,433

352,330

(13.6)

Exports

17,066

28,281

(39.7)

19,898

(14.2)

36,964

34,905

5.9

Source: Company, Angel Research

October 23, 2015

2

Hero MotoCorp | 2QFY2016 Result Update

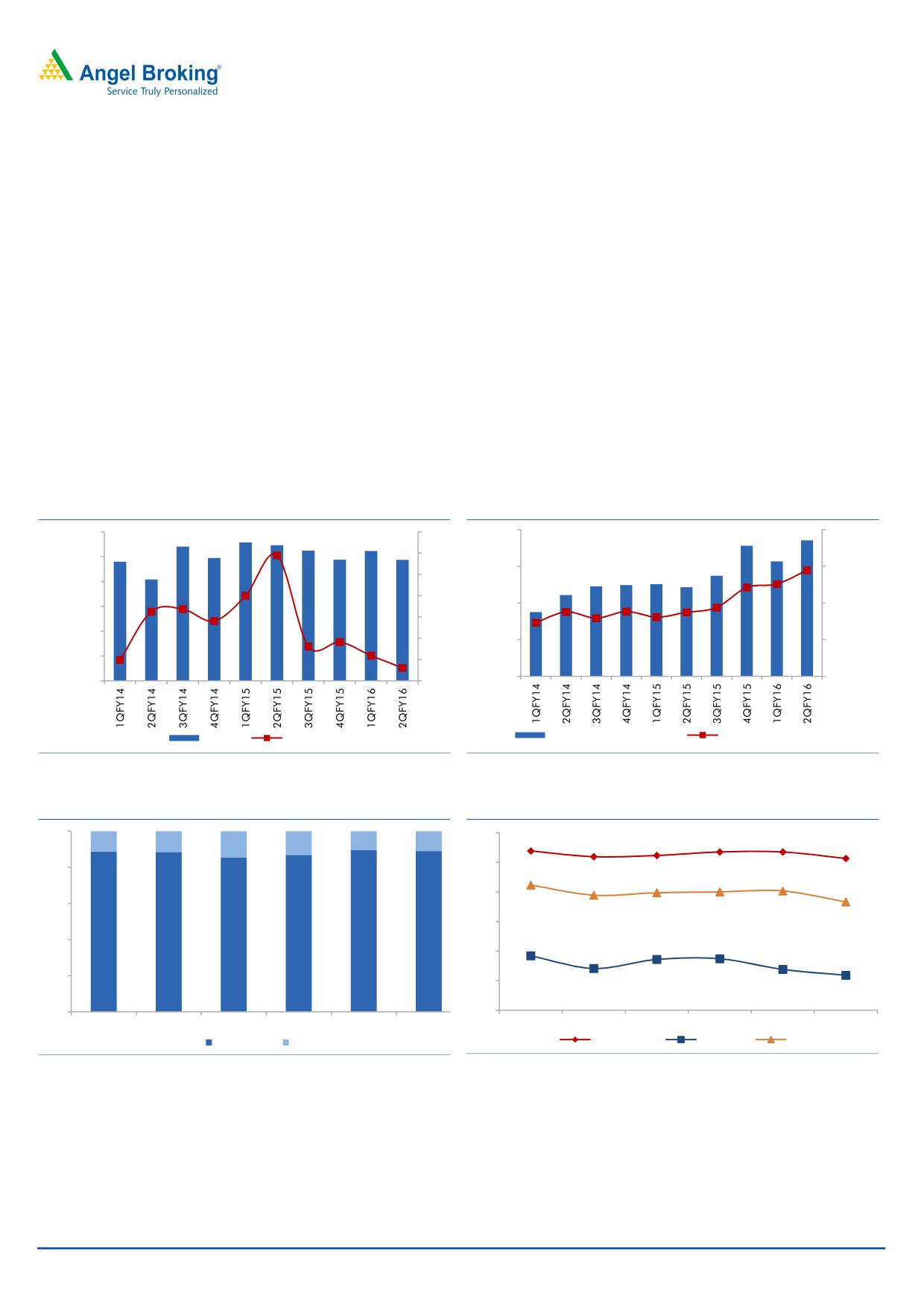

Volumes remained under pressure, declining for the fourth consecutive

quarter. Slowdown in the rural segment due to deficient rainfall and owing to

only a moderate increase in Minimum Support Prices (MSPs) for crops, hurt the

company’s volumes. HMCL lost market share by 230bp yoy, primarily due to

production adjustments, before new model launches, in the scooter segment.

Realisation/vehicle grew 6% yoy to `43,414 and was better than our estimate

of `42,267 on account of better product mix, price hikes and increased

proportion of spares. Contribution/vehicle, at `13,785, grew 5.8% qoq and

was slightly ahead of our estimate. Subdued commodity prices and raw

material cost savings under the margin improvement program boosted gross

margins.

The share of scooters in the overall mix declined marginally to 11% as the

company made production adjustments prior to the launch of two new

scooters (Maestro Edge and Duet).

Exhibit 4: Volumes flat yoy

Exhibit 5: Realisation & contribution/vehicle improve

1,800,000

25

44,000

16,000

1,600,000

20

42,000

14,000

15

1,400,000

10

1,200,000

40,000

12,000

5

1,000,000

0

38,000

10,000

800,000

(5)

36,000

8,000

600,000

(10)

Volumes

yoy growth (%)

Realisation/vehicle (`)

Contribution/vehicle (`)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 6: Volume mix

Exhibit 7: Domestic market share trend

100

60

53.8

53.5

53.5

11.2

11.5

10.3

11.0

51.9

52.3

51.3

14.4

13.1

50

80

42.3

39.7

40.0

40.3

38.9

36.6

40

60

30

88.8

88.5

85.6

86.9

89.7

89.0

40

18.4

17.2

17.4

20

14.1

13.8

11.8

20

10

0

0

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Motorcycles

Scooters

Motorcycles

Scooters

Overall

Source: Company, Angel Research

Source: SIAM, Angel Research

October 23, 2015

3

Hero MotoCorp | 2QFY2016 Result Update

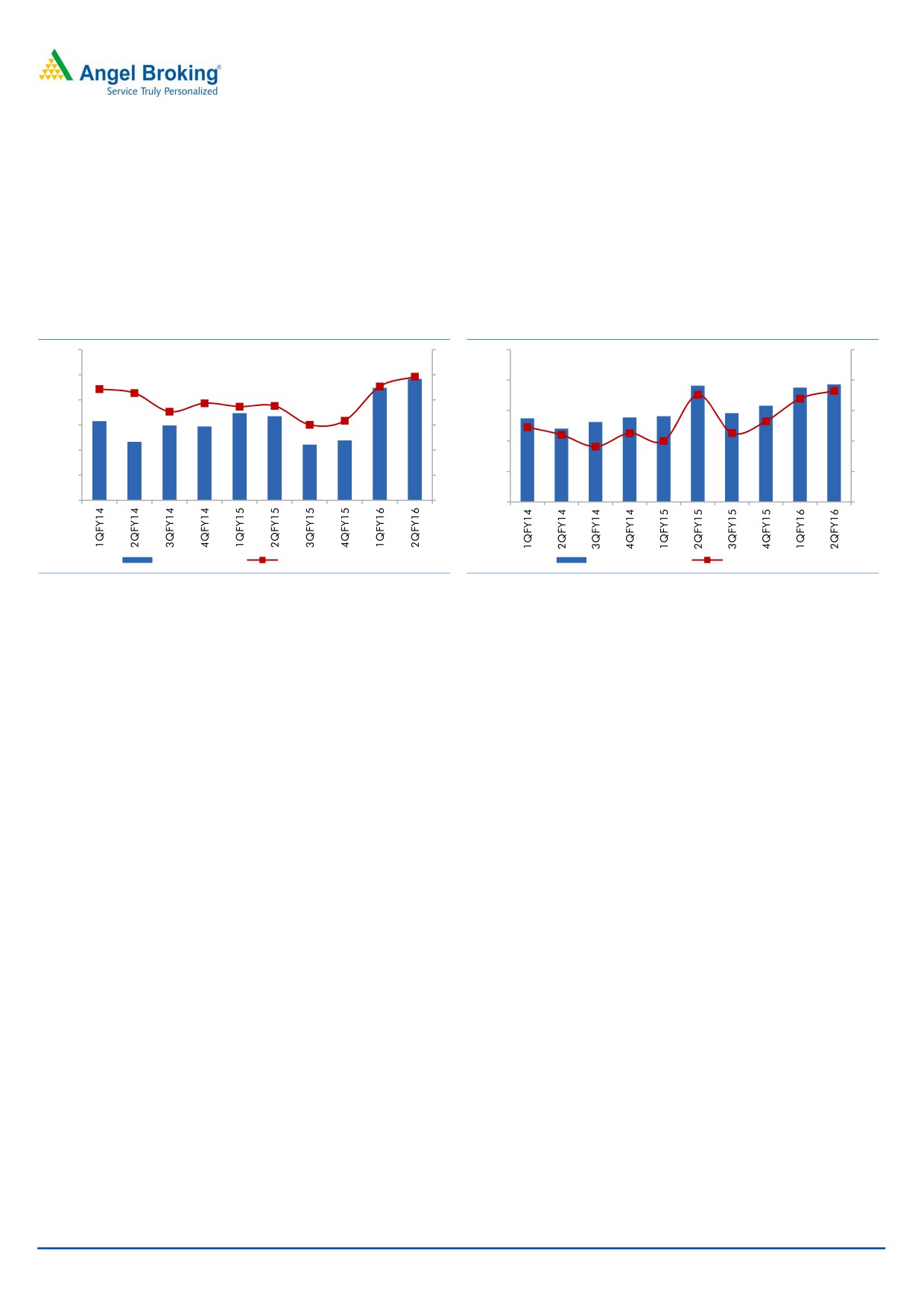

EBIDTA margin, at 15.8%, improved strongly by 230bp yoy, led by subdued

commodity prices and cost control initiatives undertaken by the company

under the margin improvement program - “Leap”.

A robust operating performance boosted the bottom-line. The Adjusted Net

Profit at `772cr (beat our estimate of `726cr) grew marginally on a yoy basis,

despite a decline in volumes.

Exhibit 8: EBITDA margin beats estimate

Exhibit 9: Bottom-line grows despite subdued volumes

1,200

1

1,000

14

1,100

1

800

12

1,000

1

600

10

900

1

400

8

800

1

200

6

700

8

600

6

0

4

EBIDTA (` cr)

EBIDTA Margin (%)

Net Profit (` cr)

Net Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

Conference call - Key highlights

The two-wheeler industry continues to remain sluggish owing to weak rural

sentiments. Rural areas contribute by about 40-45% to the industry’s overall

sales. Deficient rainfall and only a moderate increase in MSPs has hurt the

rural economy, and in turn, demand for two-wheelers. HMCL expects the two-

wheeler industry to recover from 2HFY2016 given the onset of the festive

season and a gradual pick up in the rural demand.

HMCL’s margin improvement program - “Leap” has been running successfully

and the same has enabled towards considerable cost savings. HMCL realized

benefits of `169cr and `329cr in FY2014 and FY2015 respectively. Further,

HMCL realized `60cr benefits in 1HFY2016 and aims to garner benefits to the

tune of `200cr in FY2016.

To tap the festive demand, HMCL has introduced three new products, which

include Splendor Pro in the bike space and Maestro Edge and Duet in the

scooter space.

HMCL expects commodity prices to remain soft in the near term.

HMCL has commenced operations at its Colombian plant under the CKD

format. Currently, the plant assembles about 3,000 units/month and aims to

increase the volumes to about 4,000 units/month by the end of FY2016.

On the export front, HMCL aims to sell 250,000 units in FY2016, implying a

growth of 25% yoy; and aims to enter major export markets of Nigeria,

Argentina and Mexico, going forward.

As per the Management, margins are expected to come down in 2HFY2016,

given the incurrence of higher advertising and marketing spends. HMCL has

October 23, 2015

4

Hero MotoCorp | 2QFY2016 Result Update

given an overall margin guidance of 15% for FY2016 as against 15.5%

margin achieved in 1HFY2016.

Given the slowdown in the two-wheeler industry, HMCL has delayed its

capacity expansion plans. The new Gujarat plant will commence production

from 2QFY2017 and will have an initial capacity of 750,000 units as against

1200,000 planned earlier. The plant would reach production level of 1.2mn

units only by the end of FY2017.

October 23, 2015

5

Hero MotoCorp | 2QFY2016 Result Update

Investment arguments

Expect demand to recover from 2HFY2016: We expect demand to recover

from 2HFY2016 on account of the festive season, gradual recovery in the rural

economy, reduction in interest rates and new product launches scheduled by

the company. Further, HMCL is entering new export geographies which would

enhance volumes, going ahead. We expect the company to register a positive

volume growth from 2HFY2016 onwards, as compared to demand decline in

the last four quarters.

Capacity expansion to meet future increase in demand: HMCL has a current

installed capacity of

7.65mn units across its four plants in Haridwar,

Dharuhera, Gurgaon and Neemrana. The company is setting up a new plant

in Gujarat (1.8mn units) and would further increase capacity at Neemrana

plant (by ~0.5mn units) which would come on stream in FY2017, thus taking

the overall capacity to 9.9mn units. As a result of capacity expansion, HMCL

remains well-poised to meet increase in demand, going ahead.

Outlook and valuation

HMCL’s volumes are likely to be subdued in the near term, given the poor

sentiments in rural areas, which account for about half of the company’s sales.

Deficient rainfall for a second consecutive year, and only a moderate increase in

the MSPs, have impacted rural income levels, and in turn rural demand. Given the

demand weakness, the company has also delayed its capacity expansion plans by

two quarters. We believe, in the domestic two-wheeler universe, HMCL is likely to

be most impacted by the rural slowdown, given that rural demand accounts for a

higher proportion of HMCL’s overall sales, vis-a- vis competition. Also, the

margins are likely to decline in 2HFY2016, given the increase in advertising and

branding expenses. We have broadly retained our earnings estimates for both

FY2016 and FY2017. We continue to maintain a Neutral view on the stock.

Exhibit 10: Key assumptions - Volumes

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Total motorcycles

5,779,621

5,499,322

5,538,356

5,799,695

5,700,404

6,016,800

Domestic

5,628,513

5,362,807

5,425,118

5,679,634

5,547,950

5,808,733

Exports

151,108

136,515

113,238

120,061

152,454

208,067

Total scooters

455,584

574,336

707,604

832,008

880,000

1,003,200

Domestic

414,389

549,808

690,079

752,052

782,454

881,267

Exports

41,195

24,528

17,525

79,956

97,546

121,933

Total two-wheelers

6,235,205

6,073,658

6,245,960

6,631,703

6,580,404

7,020,000

Source: Company, Angel Research

October 23, 2015

6

Hero MotoCorp | 2QFY2016 Result Update

Company background

Hero MotoCorp (HMCL) is a leading 2W manufacturer globally and the market

leader in the domestic motorcycle segment with an ~52% market share. HMCL

has four manufacturing facilities in India, located at Gurgaon, Dharuhera,

Haridwar and Neemrana with a total capacity of ~7.7mn units/year as of

FY2014. Over 2008-14, HMCL recorded a strong volume CAGR of ~11%,

backed by its strong brands (Passion and Splendor) and a well-entrenched

dealership network, which has a good presence across rural areas. Rural areas

account for ~49% of total volumes of the company.

October 23, 2015

7

Hero MotoCorp | 2QFY2016 Result Update

Profit and loss statement (Standalone)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Total operating income

23,579

23,768

25,275

27,585

28,561

31,559

% chg

21.6

0.8

6.3

9.1

3.5

10.5

Total expenditure

19,960

20,484

21,735

24,043

24,356

26,929

Net raw material costs

17,282

17,398

18,230

19,754

19,544

21,592

Employee expenses

736

821

930

1,173

1,292

1,430

Other

1,943

2,265

2,575

3,116

3,520

3,907

EBITDA

3,619

3,284

3,540

3,542

4,205

4,630

% chg

38.5

(9.2)

20.3

0.1

18.7

10.1

EBITDA margin

15.3

13.8

14.0

12.8

14.7

14.7

Depreciation & amort.

1,097

1,142

1,107

540

471

662

EBIT

2,521

2,143

2,879

3,495

4,179

4,476

% chg

14.1

(15.0)

13.3

21.4

19.6

7.1

(% of total op. income)

10.7

9.0

11.4

12.7

14.6

14.2

Interest and other charges

21

12

12

11

7

12

Other income

365

398

446

493

445

508

Recurring PBT

2,865

2,529

2,867

3,484

4,172

4,464

% chg

15.3

(11.7)

13.4

21.5

19.7

7.0

Extraord. income/(exp.)

0

0

0

(155)

0

0

PBT

2,865

2,529

2,867

3,329

4,172

4,464

Tax

487

411

758

943

1,154

1,205

(% of PBT)

17.0

16.3

26.4

27.1

27.7

27.0

PAT (reported)

2,378

2,118

2,109

2,541

3,018

3,259

ADJ. PAT

2,378

2,118

2,109

2,386

3,018

3,259

% chg

18.4

(10.9)

(0.4)

20.5

18.8

8.0

(% of total op. income)

10.1

8.9

8.3

9.2

10.6

10.3

Basic EPS (`)

119.1

106.1

105.6

127.2

151.1

163.2

Adj. EPS (`)

119.1

106.1

105.6

127.2

151.1

163.2

% chg

18.4

(10.9)

(0.4)

20.5

18.8

8.0

October 23, 2015

8

Hero MotoCorp | 2QFY2016 Result Update

Balance sheet statement (Standalone)

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015E FY2016E

FY2017E

SOURCES OF FUNDS

Equity share capital

40

40

40

40

40

40

Reserves & surplus

4,250

4,966

5,560

6,501

7,754

9,106

Shareholders’ Funds

4,290

5,006

5,600

6,541

7,794

9,146

Total loans

-

-

-

-

Deferred tax liability

208

132

(106)

(74)

(106)

(106)

Other long term liabilities

1,011

302

24

31

31

31

Long term provisions

38

30

50

66

75

95

Total Liabilities

5,547

5,471

5,568

6,565

7,794

9,167

APPLICATION OF FUNDS

Gross block

6,308

6,685

6,909

8,158

9,458

10,758

Less: Acc. depreciation

2,523

3,614

4,666

5,191

5,662

6,324

Net Block

3,786

3,071

2,243

2,967

3,796

4,434

Capital work-in-progress

39

62

854

713

400

200

Investments

3,964

3,624

4,089

3,154

3,343

3,611

Long term loans and adv.

534

780

477

617

772

903

Other noncurrent assets

26

36

48

60

60

60

Current assets

1,541

2,068

2,280

2,938

3,996

5,006

Cash

77

181

118

159

1,346

2,128

Loans & advances

476

554

550

568

570

580

Other

988

1,334

1,612

2,211

2,080

2,298

Current liabilities

4,341

4,171

4,423

3,883

4,574

5,047

Net current assets

(2,801)

(2,102)

(2,143)

(946)

(577)

(41)

Misc. exp. not written off

-

-

-

-

Total Assets

5,547

5,471

5,568

6,565

7,794

9,167

Note: Cash includes cash with scheduled banks on dividend current accounts

October 23, 2015

9

Hero MotoCorp | 2QFY2016 Result Update

Cash flow statement (Standalone)

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E

Profit before tax

2,865

2,529

2,867

3,484

4,172

4,464

Depreciation

1,097

1,142

1,052

526

471

662

Change in working capital

(691)

(787)

(23)

(1,156)

819

245

Direct taxes paid

(583)

(613)

(758)

(943)

(1,154)

(1,205)

Others

(329)

(380)

(1,303)

(22)

(32)

-

Cash Flow from Operations

2,360

1,890

1,835

1,889

4,276

4,166

(Inc.)/Dec. in fixed assets

(503)

(600)

(1,016)

(1,108)

(987)

(1,100)

(Inc.)/Dec. in investments

1,443

628

(465)

935

(189)

(267)

Others

(847)

(760)

-

-

Cash Flow from Investing

93

(733)

(1,481)

(173)

(1,177)

(1,367)

Issue of equity

-

-

-

-

Inc./(Dec.) in loans

-

-

-

-

-

-

Dividend paid (Incl. Tax)

(2,097)

(899)

(740)

(1,396)

(1,766)

(1,906)

Others

(361)

(158)

-

-

Cash Flow from Financing

(2,458)

(1,056)

(740)

(1,396)

(1,766)

(1,906)

Inc./(Dec.) in cash

(6)

101

(386)

321

1,333

892

Opening Cash balances

39

34

181

118

159

1,346

Closing Cash balances

34

135

117

159

1,346

2,128

October 23, 2015

10

Hero MotoCorp | 2QFY2016 Result Update

Key ratios

Y/E March

FY2012

FY2013

FY2014

FY2015E

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

22.0

24.7

24.8

20.6

17.3

16.1

P/CEPS

15.1

16.0

16.3

17.0

15.0

13.3

P/BV

12.2

10.4

9.3

8.0

6.7

5.7

Dividend yield (%)

1.7

2.3

2.5

2.9

3.5

3.7

EV/Sales

2.0

2.0

1.9

1.8

1.7

1.5

EV/EBITDA

13.3

14.8

13.6

13.8

11.3

10.1

EV / Total Assets

8.8

8.9

8.6

7.5

6.1

5.1

Per Share Data (`)

EPS (Basic)

119.1

106.1

105.6

127.2

151.1

163.2

EPS (fully diluted)

119.1

106.1

105.6

127.2

151.1

163.2

Cash EPS

174.0

163.2

161.1

154.3

174.7

196.3

DPS

45.0

60.0

65.5

76.3

90.7

97.9

Book Value

214.8

250.7

280.4

327.6

390.3

458.0

Dupont Analysis

EBIT margin

10.7

10.7

11.4

12.7

14.6

14.2

Tax retention ratio

83.0

0.8

0.7

0.7

0.7

0.7

Asset turnover (x)

4.7

4.5

4.6

4.3

4.4

4.5

ROIC (Post-tax)

41.4

40.2

38.9

39.8

46.9

46.4

Cost of Debt (Post Tax)

-

-

-

-

Leverage (x)

(0.9)

(0.8)

(0.8)

(0.5)

(0.6)

(0.6)

Operating ROE

-

-

-

-

Returns (%)

ROCE (Pre-tax)

49.2

46.4

51.7

53.2

53.6

48.8

Angel ROIC (Pre-tax)

51.2

48.0

52.8

54.6

64.8

63.6

ROE

65.6

42.3

37.7

38.8

38.7

35.6

Turnover ratios (x)

Asset Turnover (Gross Block)

4.0

3.6

3.7

3.4

3.0

2.9

Inventory / Sales (days)

9

13

13

15

14

14

Receivables (days)

3

10

13

18

17

17

Payables (days)

40

42

42

42

38

38

WC cycle (ex-cash) (days)

(61)

(19)

(15)

(8)

(7)

(7)

Solvency ratios (x)

Net debt to equity

(0.9)

(0.8)

(0.8)

(0.5)

(0.6)

(0.6)

Net debt to EBITDA

(1.1)

(1.2)

(1.2)

(0.9)

(1.1)

(1.2)

Int. Coverage (EBIT / Int.)

118.4

213.4

243.6

315.1

591.0

373.0

October 23, 2015

11

Hero MotoCorp | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel has received in-principal

approval from SEBI for registering as a Research Entity in terms of SEBI (Research Analyst) Regulations, 2014. Angel or its associates

has not been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its

associates including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company

covered by Analyst. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of

securities of the company covered by Analyst during the past twelve months. Angel/analyst has not served as an officer, director or

employee of company covered by Analyst and has not been engaged in market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Hero MotoCorp

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

October 23, 2015

12