2QFY2016 Result Update | HFC

October 27, 2015

HDFC

NEUTRAL

CMP

`1,275

Performance Highlights

Target Price

-

Particulars (` cr)

2QFY16 1QFY16

% chg (qoq) 2QFY15

% chg (yoy)

Investment Period

-

NII

2,076

2,116

(1.9)

1,955

6.2

Pre-prov. profit

2,376

2,002

18.7

2,017

17.8

Stock Info

PAT

1,605

1,361

17.9

1,358

18.2

Source: Company, Angel Research

Sector

HFC

For 2QFY2016, HDFC posted an 18.2% yoy increase in PAT, which is broadly in-

Market Cap (` cr)

2,01,178

line with our expectation. The NII for the quarter grew 6.2% yoy, which is slightly

Beta

1.4

below our expectation due to moderate growth in advances.

52 Week High / Low

1,399/1,030

Loan book growth moderate; Asset quality fairly stable

Avg. Daily Volume

29,42,025

For 2QFY2016, HDFC’s loan book grew by 12.1% yoy, with loans to the

Face Value (`)

2

individual segment growing by 23% yoy (after adding back loans sold in the

BSE Sensex

27,253

preceding 12 months) whereas the corresponding growth in the reported loan

Nifty

8,233

book was of 14.0% yoy, which is below our expectation. This is due to greater

Reuters Code

HDFC.BO

amount of loans having been sold to HDFC Bank in recent quarters. During the

quarter, incremental growth in the loan book came through growth in individual

Bloomberg Code

HDFC@IN

loans, which now constitute almost 69.7% of the total loans portfolio as compared

to 68.6% in 2QFY2015.

Shareholding Pattern (%)

The spread stood largely stable at 2.32% as compared to 2.29% in September

Promoters

0.0

2014, while the NIM contracted to 3.95% from a slightly higher 4% in September

MF / Banks / Indian Fls

78.2

2014, despite spreads widening. In declining rate environment, as HDFC has

FII / NRIs / OCBs

9.9

large Net Worth, even with constant spreads, NIM’s would have a slightly

Indian Public / Others

12.0

downward bias. Overall, we expect the loan book to grow at a CAGR of 15.0%

over FY2015-17E, while the NII growth at a CAGR of 11.6% over the same period.

Abs. (%)

3m 1yr

3yr

The company continued to keep its asset quality under check, with gross non-

Sensex

(1.1)

1.9

46.2

performing assets as a % of total loans rising marginally by 2bp to 0.71% (vs

0.69% in 1QFY2016). The company continues to maintain a 100% Provision

HDFC

(4.5)

23.1

68.6

Coverage Ratio.

3-year price chart

Outlook and valuation: HDFC continues to post moderate set of numbers despite

1,600

sluggish economic environment. Overall, we expect HDFC to post a healthy PAT

1,400

CAGR of 15.3% over FY2015-17E. The stock has surged significantly from the

1,200

lows witnessed in the month of August 2015. Currently, HDFC’s core business

1,000

800

(after adjusting `482/share towards the value of its subsidiaries) trades at 4.5x

600

FY2017E ABV, which in our view, offers limited scope for upside from here on.

400

Hence, we maintain our Neutral rating on the stock.

Key financials (standalone)

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

Source: Company, Angel Research

NII*

6,666

7,631

8,341

9,502

% chg

12.5

14.5

9.3

13.9

Net profit

5,440

5,990

6,466

7,407

% chg

12.2

10.1

8.0

14.5

Vaibhav Agrawal

NIM (%)

3.4

3.4

3.3

3.3

022 - 3935 7800 Ext: 6808

EPS (`)

34.9

38.0

41.1

47.0

P/E (x)

37.7

34.5

32.0

27.9

P/ABV (x)

7.3

6.7

6.1

5.5

Chintan Shah

RoA (%)

2.5

2.4

2.3

2.3

022 - 4000 3600 Ext: 6828

RoE (%)

20.5

20.3

19.9

20.8

Source: Company, Angel Research; Note: * Core NII; CMP as of October 27, 2015.

Please refer to important disclosures at the end of this report

1

HDFC | 2QFY2016 Result Update

Exhibit 1: Quarterly performance (standalone)

Particulars (` cr)

2QFY16

1QFY16

% chg (qoq)

2QFY15

% chg (yoy)

FY2015

FY2014

% chg

Income from operations

6,994

6,980

0.2

6,428

8.8

26,272

23,338

12.6

Interest expensed

4,918

4,863

1.1

4,474

9.9

17,975

16,029

12.1

NII

2,076

2,116

(1.9)

1,955

6.2

8,297

7,309

13.5

Non-interest income

487

89

448.8

242

100.9

1,199

859

39.6

Operating income

2,563

2,205

16.2

2,197

16.7

9,496

8,168

16.3

Operating expenses

187

203

(7.7)

180

3.8

707

628

12.5

Pre-prov. profit

2,376

2,002

18.7

2,017

17.8

8,789

7,540

16.6

Provisions & cont.

52

50

4.0

35

48.6

165

100

65.0

PBT

2,324

1,952

19.0

1,982

17.3

8,624

7,440

15.9

Prov. for taxes

719

591

21.7

624

15.2

2,634

2,000

31.7

PAT

1,605

1,361

17.9

1,358

18.2

5,990

5,440

10.1

EPS (`)

10.2

8.6

17.7

8.7

17.5

38.0

34.9

9.1

Cost-to-income ratio (%)

7.3

9.2

(190)bp

8.2

(90)bp

7.4

7.7

-

Effective tax rate (%)

30.9

30.3

31.5

30.5

26.9

Source: Company, Angel Research

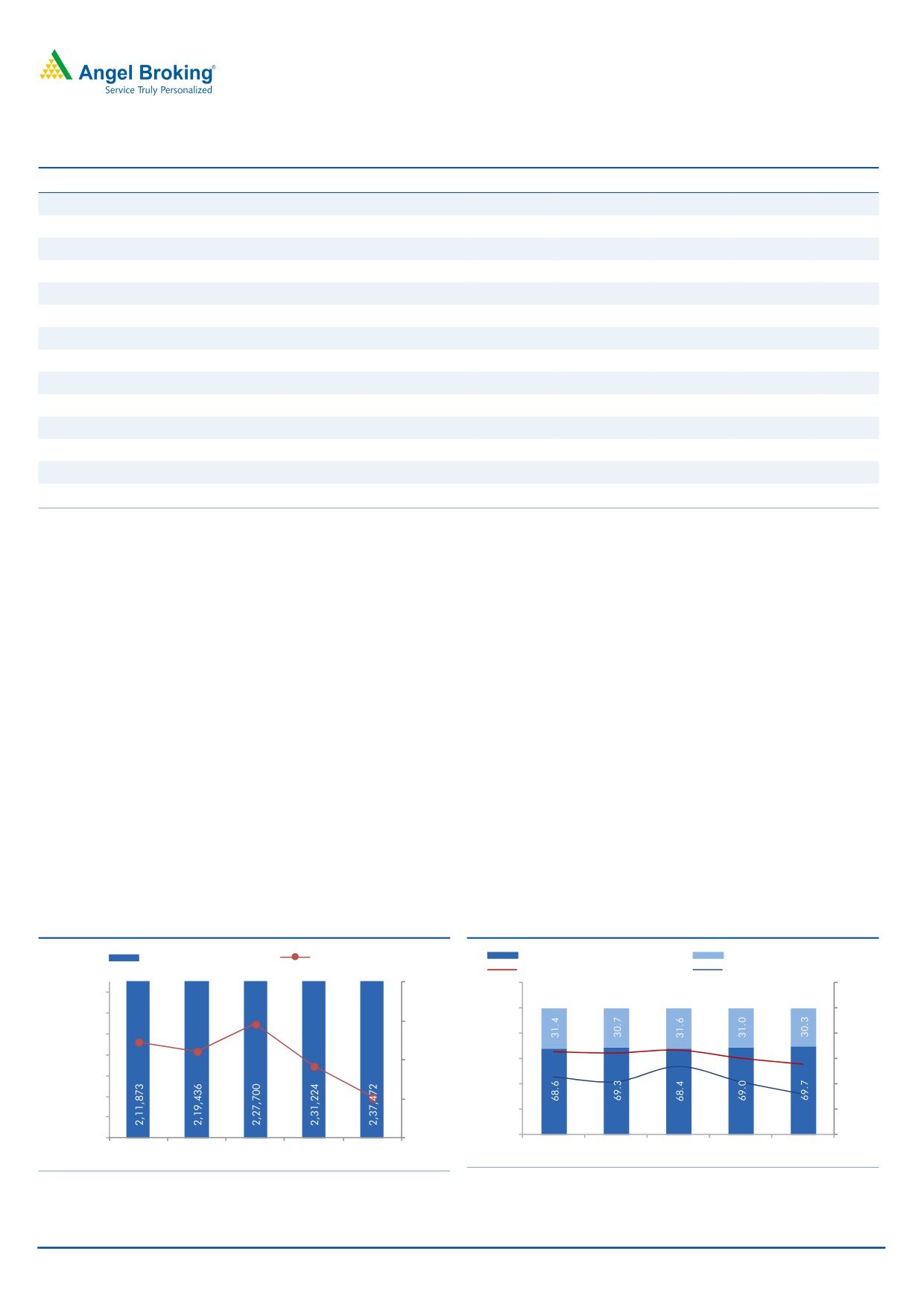

Moderate growth in retail loan book; corporate growth subdued

For 2QFY2016, HDFC’s loan book grew by 12.1% yoy, with loans to the individual

segment growing by 23% yoy (after adding back loans sold in the preceding

12 months) whereas the corresponding growth in the reported loan book was of

14.0% yoy, which is below our expectation. This is due to greater amount of loans

having been sold to HDFC Bank in recent quarters. Until the previous quarters,

55% of loans sourced by HDFC Bank for HDFC were bought back by HDFC Bank.

However, from this quarter onwards, they have started buying back 70% of its

loans thereby having a significant impact on the individual loan growth of HDFC.

The individual loan book has been consistently outpacing the corporate book over

the past few quarters. During the quarter, incremental growth in the loan book

came through growth in individual loans which now constitute almost 69.7% of the

total loans portfolio as compared to 68.6% in 2QFY2015. We expect individual

loan growth to be subdued for FY2016 as well as single-digit corporate book

growth.

Exhibit 2: Loan book grows at a moderate pace

Exhibit 3: Individual loans grew at 14.0% yoy

Advances (`cr)

Growth (yoy, %)

Ind. loans as % to Total

Non Ind. loans as % to Total

Ind. Loan growth (%) -RHS

Non Ind. loan growth (%) -RHS

18.0

120.0

30.0

1,90,000

15.8

100.0

25.0

1,70,000

14.9

16.0

1,50,000

14.4

80.0

20.0

13.7

1,30,000

14.0

60.0

15.0

1,10,000

12.1

40.0

10.0

90,000

12.0

20.0

5.0

70,000

50,000

10.0

-

-

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Source: Company, Angel Research

Source: Company, Angel Research

October 27, 2015

2

HDFC | 2QFY2016 Result Update

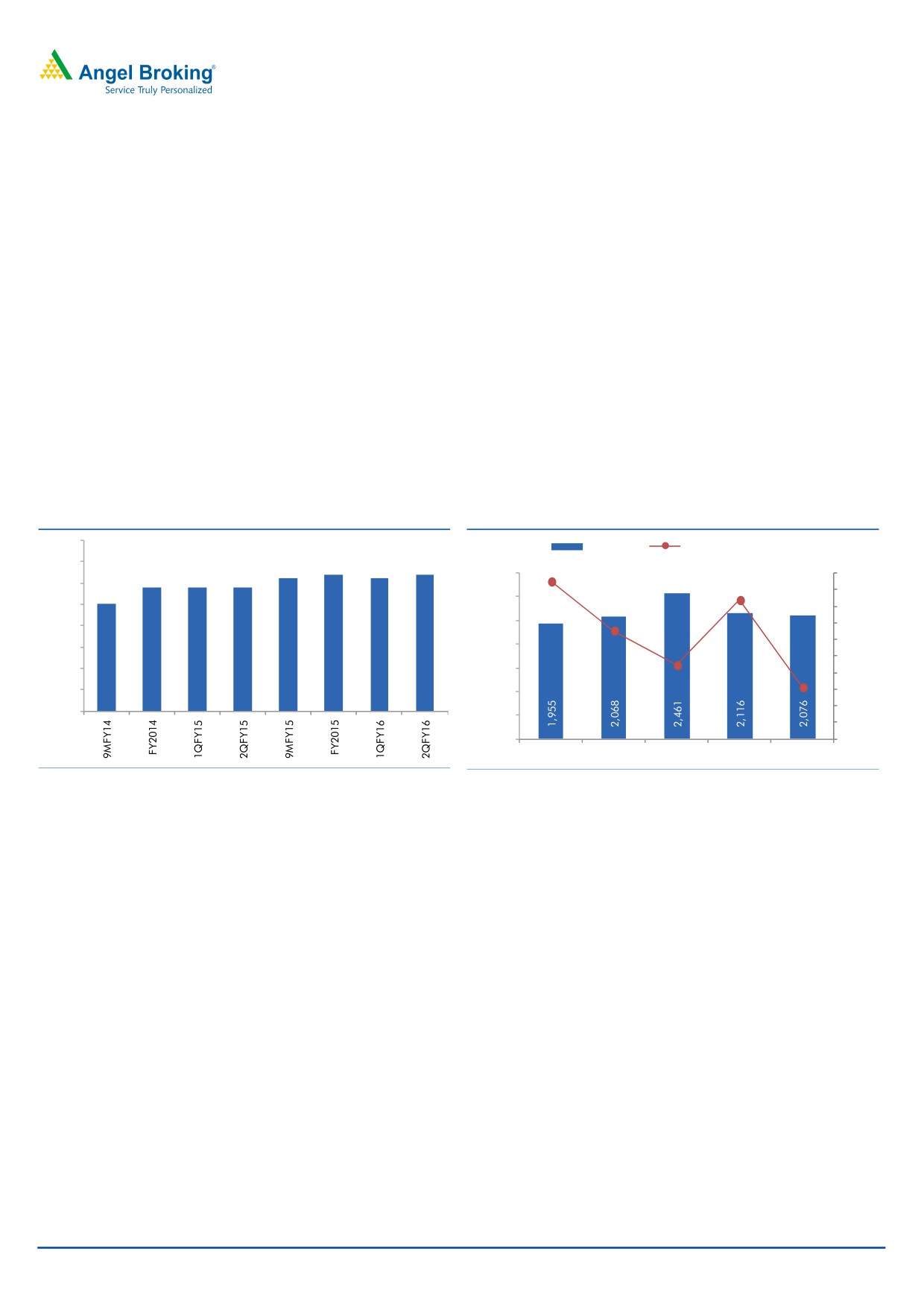

NII growth weakens

The spread stood largely stable at 2.32% as compared to 2.29% in September

2014, while the NIM contracted to 3.95% from a slightly higher 4% in September

2014, despite spreads widening. In declining rate environment, as HDFC has

large Net Worth, even with constant spreads, NIM’s would have a slightly

downward bias. Overall, we expect the loan book to grow at a CAGR of 15.0%

over FY2015-17E, while the NII growth at a moderate CAGR of 11.6% over the

same period.

Dividend received from HDFC Bank boosted other income

Non-interest income for the company came in at INR 486.6cr as compared to INR

242.2cr in 2QFY2015. The increase is attributed to the dividend income from

HDFC Bank, which in FY 2015 was received in first quarter, whereas in FY 2016, it

has been received in this quarter. PBT level earnings, adjusted for dividends and

sale of investments grew by 4.3% yoy which was below expectations.

Exhibit 4: Spreads strong at 2.32% for 2QFY2016

Exhibit 5: NII growth weakens

2.40

(%)

NII (`cr)

Growth yoy (%, RHS)

2.35

2.32

2.32

19.0

2.31

2.31

2.29

2.29

2.29

2,800

20.0

2.30

2.25

16.7

18.0

2,400

2.25

16.0

2,000

13.1

14.0

2.20

12.0

2.15

1,600

8.9

10.0

2.10

1,200

6.2

8.0

2.05

800

6.0

4.0

2.00

400

2.0

-

-

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Source: Company, Angel Research

Source: Company, Angel Research

October 27, 2015

3

HDFC | 2QFY2016 Result Update

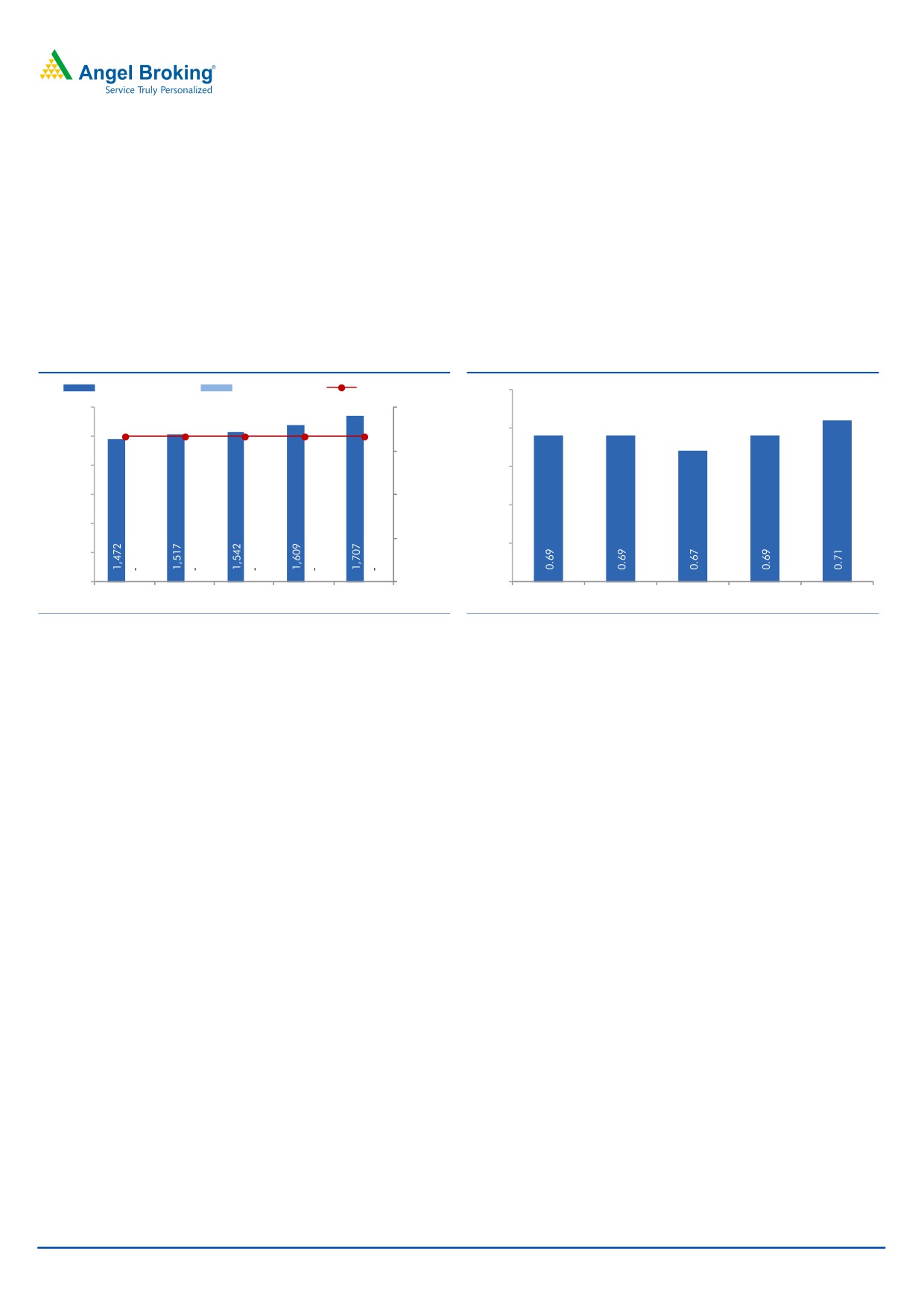

Asset quality remains fairly stable

Asset quality continues to remain fairly stable for the company, as its gross non-

performing assets as a % of total loans increased 2bp to 0.71% (vs 0.69% in

1QFY2016). The Gross NPA ratio for individual loans went up to 0.53% as against

0.51% in 1QFY2016, while the Gross NPA ratio for the non-individual loans

portfolio went up by 3bp qoq to 1.04%. The company continues to maintain a

100% Provision Coverage Ratio. In fact, the company carries `330cr of excess

provision over and above the regulatory requirement of `1,797cr.

Exhibit 6: NPA coverage remains at 100%

Exhibit 7: Gross NPA ratio remains stable

Gross NPA (`cr)

Net NPA (`cr)

PCR (%, RHS)

0.75

Gross NPA % (3 months)

1,800

120.0

100.0

100.0

100.0

100.0

100.0

0.70

1,500

90.0

1,200

0.65

900

60.0

0.60

600

30.0

0.55

300

-

-

0.50

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Source: Company, Angel Research

Source: Company, Angel Research

October 27, 2015

4

HDFC | 2QFY2016 Result Update

Outlook and valuation

HDFC continues to post good set of numbers despite sluggish economic

environment. Overall, we expect HDFC to post a healthy PAT CAGR of 15.3% over

FY2015-17E. The stock has surged significantly from the lows witnessed in the

month of August

2015. Currently, HDFC’s core business (after adjusting

`482/share towards the value of its subsidiaries) trades at 4.5x FY2017E ABV,

which in our view, offers limited scope for upside from here on. Hence, we

maintain our Neutral rating on the stock.

Company Background

HDFC is India's leading housing finance company, with a balance sheet size of

around `2.6 lakh cr. The company's primary business is to provide loans for the

purchase or construction of residential houses. HDFC's distribution network spans

392 outlets, covering more than 2,400 towns and cities across India. HDFC also

has representative offices in London, Dubai and Singapore and service associates

in Kuwait, Oman, Qatar, Abu Dhabi and Saudi Arabia to cater to NRIs. From its

origins as a specialized mortgage company, HDFC has grown into a financial

conglomerate with market leading group companies in banking, asset

management and insurance verticals.

October 27, 2015

5

HDFC | 2QFY2016 Result Update

Income statement (standalone)

Y/E March (` cr)

FY12

FY13

FY14

FY15

FY16E

FY17E

NII*

4,998

5,927

6,666

7,631

8,341

9,502

- YoY Growth (%)

17.7

18.6

12.5

14.5

9.3

13.9

Other Income

1,199

1,329

1,503

1,865

2,017

2,350

- YoY Growth (%)

12.0

10.8

13.0

24.1

8.1

16.5

Operating Income

6,198

7,257

8,168

9,496

10,358

11,852

- YoY Growth (%)

16.5

17.1

12.6

16.3

9.1

14.4

Operating Expenses

452

539

628

707

795

898

- YoY Growth (%)

18.6

19.3

16.5

12.5

12.5

13.0

Pre - Provision Profit

5,746

6,718

7,540

8,789

9,563

10,954

- YoY Growth (%)

16.4

16.9

12.2

16.6

8.8

14.5

Prov. & Cont.

80

145

100

165

175

213

- YoY Growth (%)

14.3

81.3

(31.0)

65.0

6.1

21.6

Profit Before Tax

5,666

6,573

7,440

8,624

9,388

10,741

- YoY Growth (%)

16.4

16.0

13.2

15.9

8.9

14.4

Prov. for Taxation

1,543

1,725

2,000

2,634

2,922

3,334

- as a % of PBT

27.2

26.2

26.9

30.5

31.1

31.0

PAT

4,123

4,848

5,440

5,990

6,466

7,407

- YoY Growth (%)

16.6

17.6

12.2

10.1

8.0

14.5

Note: *Core NII

Balance sheet (standalone)

Y/E March (` cr)

FY12

FY13

FY14

FY15

FY16E

FY17E

Share Capital

295

309

312

315

315

315

Reserve & Surplus

18,722

24,691

27,643

30,655

33,661

37,092

Loan Funds

1,39,128

1,58,828

1,84,298

2,08,694

2,33,413

2,76,726

- Growth (%)

20.9

14.2

16.0

13.2

11.8

18.6

Other Liabilities & Prov.

9,375

11,703

13,504

14,383

16,153

18,962

Total Liabilities

1,67,520

1,95,531

2,25,757

2,54,047

2,83,542

3,33,095

Investments

12,207

13,613

13,804

14,294

15,020

16,238

Advances

1,40,422

1,69,571

1,96,554

2,27,700

2,55,024

3,00,928

- Growth (%)

20.2

20.8

15.9

15.8

12.0

18.0

Fixed Assets

234

238

276

677

758

894

Other Assets

14,657

12,109

15,123

11,376

12,741

15,034

Total Assets

1,67,520

1,95,531

2,25,757

2,54,047

2,83,542

3,33,095

October 27, 2015

6

HDFC | 2QFY2016 Result Update

Ratio analysis (standalone)

Y/E March

FY12

FY13

FY14

FY15

FY16E

FY17E

Profitability ratios (%)

NIMs

3.6

3.6

3.4

3.4

3.3

3.6

Cost to Income Ratio

7.3

7.4

7.7

7.4

7.7

7.3

RoA

2.7

2.6

2.5

2.4

2.3

2.7

RoE

22.7

22.0

20.5

20.3

19.9

22.7

Asset Quality (%)

Gross NPAs

0.76

0.71

0.69

0.68

0.70

0.76

Net NPAs

-

-

-

-

-

-

Provision Coverage

100.0

100.0

100.0

100.0

100.0

100.0

Per Share Data (`)

EPS

27.9

31.4

34.9

38.0

41.1

27.9

ABVPS (75% cover.)

128.8

161.7

179.1

196.7

215.8

128.8

DPS

11.0

12.5

14.0

15.1

16.1

11.0

Valuation Ratios

PER (x)

45.7

40.7

36.6

33.5

31.1

45.7

P/ABVPS (x)

9.9

7.9

7.1

6.5

5.9

9.9

DuPont Analysis#

NII

3.4

3.4

3.3

3.3

3.2

3.4

(-) Prov. Exp.

0.1

0.1

0.0

0.1

0.1

0.1

Adj. NII

3.4

3.3

3.2

3.2

3.1

3.4

Treasury

0.2

0.2

0.1

0.2

0.1

0.2

Int. Sens. Inc.

3.6

3.5

3.4

3.4

3.3

3.6

Other Inc.

0.5

0.4

0.5

0.4

0.5

0.5

Op. Inc.

4.1

3.9

3.8

3.9

3.7

4.1

Opex

0.3

0.3

0.3

0.3

0.3

0.3

PBT

3.8

3.6

3.5

3.6

3.4

3.8

Taxes

1.1

1.0

1.0

1.1

1.1

1.1

RoA

2.7

2.6

2.5

2.4

2.3

2.7

Leverage

14.4

12.6

11.1

10.9

10.8

14.4

RoE

39.3

33.2

28.1

26.3

24.7

39.3

Note: # Core RoEs excluding income and investments in subsidiaries

October 27, 2015

7

HDFC | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

HDFC

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

October 27, 2015

8