3QFY2016 Result Update | Infra

February 2, 2016

Gujarat Pipavav Port

NEUTRAL

CMP

`156

Performance Highlights

Target Price

-

Particulars (` cr)

3QFY16 2QFY16

% chg (qoq) 3QFY15

% chg (yoy)

Investment Period

-

Net Sales

152

140

8.3

170

(10.3)

EBITDA

87

68

28.2

86

1.4

Stock Info

Sector

Infrastructure

Adj. PAT

53

61

(12.6)

89

(40.3)

Source: Company, Angel Research

Market Cap (` cr)

7,539

Net debt (` cr)

(245)

For 3QFY2016, Gujarat Pipavav Port (GPPL) reported 10.3% yoy decline in

Beta

0.8

revenues to `152cr. On sequential basis revenue was up 8.3%. Reported top-line

52 Week High / Low

262/136

number is below our expectation of `170cr. Top-line de-growth on a yoy basis is

on account of (1) 9.2% decrease in Container business volumes (to 178,000TEUs),

Avg. Daily Volume

733,016

and (2) 63.3% decrease in Dry Bulk business (to 443,000MT).

Face Value (`)

10

BSE Sensex

24,539

GPPL reported an EBITDA of `87cr, which is ahead of our expectation of `81cr.

Nifty

7,456

The reported EBITDA margin of the company came in at 57.1%, up from 48.2% in

Reuters Code

GPPL.BO

the sequential previous quarter and from 50.5% in the corresponding quarter a

year ago. EBITDA during the quarter benefitted from shift in business mix and `1cr

Bloomberg Code

GPPV@IN

of reversal with regards the dredging cost.

GPPL reported an Adj. PAT of `53cr, down 40.3% yoy, and 12.6% qoq. Adj. PAT

Shareholding Pattern (%)

margin for the quarter came in at 35.0% vs 52.7% in the corresponding quarter a

Promoters

43.0

year ago. Adj. PAT number, on yoy basis, was impacted by (1) `28cr of tax

MF / Banks / Indian Fls

9.9

expense (vs tax exemption in 3QFY2015), (2) 53.4% increase in depreciation

FII / NRIs / OCBs

39.5

expenses to `25cr, and (3) 1.6% decrease in other income to `20cr. The sharp

Indian Public / Others

7.6

increase in depreciation expense is owing to the change in the estimated useful life

of assets.

Outlook and Valuation: At the current market price of `156, GPPL is trading at

Abs. (%)

3m 1yr 3yr

FY2016E and FY2017E P/E multiple of 31.4x and 31.4x, respectively. We have

Sensex

(7.7)

(15.4)

24.2

valued the Ports business using free cash flow to equity holders (FCFE) to arrive at

GPPL

(3.9)

(24.6)

271.3

FY2017E based business value of `160. We have assigned 10x P/E multiple to our

FY2017E earnings estimate of Pipavav Rail Corporation Ltd (PRCL) to arrive at

3-year price chart

business value of `7 (adj. for 38.8% stake). On using the sum-of-the-parts (SOTP)

300

based valuation methodology, we arrive at a FY2017E based price target of `167.

250

Given the limited upside potential in the stock from the current levels, we maintain our

200

Neutral rating on the stock.

150

Key Financials

100

Y/E March (` cr)

FY13

FY15*

FY16E

FY17E

50

Net Sales

474

792

632

705

0

% chg

67.2

(20.2)

11.5

Net Profit

192

389

240

240

% chg

102.6

(38.4)

0.2

Source: Company, Angel Research

EBITDA (%)

44.9

53.8

51.6

52.2

EPS (`)

4

8

5

5

P/E (x)

39.2

19.4

31.4

31.4

P/BV (x)

4.0

3.8

3.2

3.1

RoE (%)

14.7

24.3

12.5

11.2

RoCE (%)

13.3

26.4

15.9

16.7

Yellapu Santosh

EV/Sales (x)

16.1

9.2

11.6

10.3

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

35.8

17.1

22.6

19.7

Source: Company, Angel Research; Note: CMP as of February 2, 2016; *GPPL switched from Dec to Mar year ending

Please refer to important disclosures at the end of this report

1

GPPL | 3QFY2016 Result Update

Exhibit 1: 3QFY2016 Performance

Particulars (` cr)

3QFY16

2QFY16

% chg (qoq)

3QFY15

% chg (yoy)

9mFY16

9mFY15

% chg

Net Sales

152

140

8.3

170

(10.3)

465

483

(3.6)

Total Expenditure

65

73

(10.2)

84

(22.2)

224

228

(1.6)

Operating Expenses

29

33

(9.7)

47

(37.0)

103

118

(13.2)

Employee benefits Expense

13

14

(7.1)

12

8.4

40

36

9.0

Other Expenses

23

26

(12.4)

25

(9.5)

82

73

12.0

EBITDA

87

68

28.2

86

1.4

241

255

(5.3)

EBIDTA %

57.1

48.2

50.5

51.9

52.8

Depreciation

25

23

9.8

16

53.4

72

50

44.2

EBIT

62

45

37.5

69

(10.8)

170

205

(17.3)

Interest and Financial Charges

0

0

6.3

0

(19.6)

0

18

(99.4)

Other Income

20

16

24.3

20

(1.6)

53

72

(25.8)

PBT before Exceptional Items

82

61

34.1

89

(8.7)

223

259

(14.1)

Exceptional Items

0

(60)

0

(60)

0

PBT after Exceptional Items

82

121

(32.7)

89

(8.7)

283

259

9.2

Tax

28

68

(58.5)

0

96

0

% of PBT

35

56

nmf*

34

nmf*

PAT

53

53

0.4

89

(40.3)

187

259

(28.0)

Adj. PAT

53

61

(12.6)

89

(40.3)

247

259

(4.8)

PAT %

35.0

37.8

52.7

40.1

53.7

Adj. PAT %

35.0

43.4

52.7

53.0

53.7

Dil. EPS (after excep. Items)

1.10

1.10

0.0

1.85

(40.5)

3.86

5.37

(28.1)

Adj. Dil. EPS (after excep. Items)

1.10

1.26

(12.7)

1.85

(40.5)

5.07

5.37

(5.6)

Source: Company, Angel Research; Note: nmf*- Not meaningful; ** GPPL switched from Dec to Mar year ending

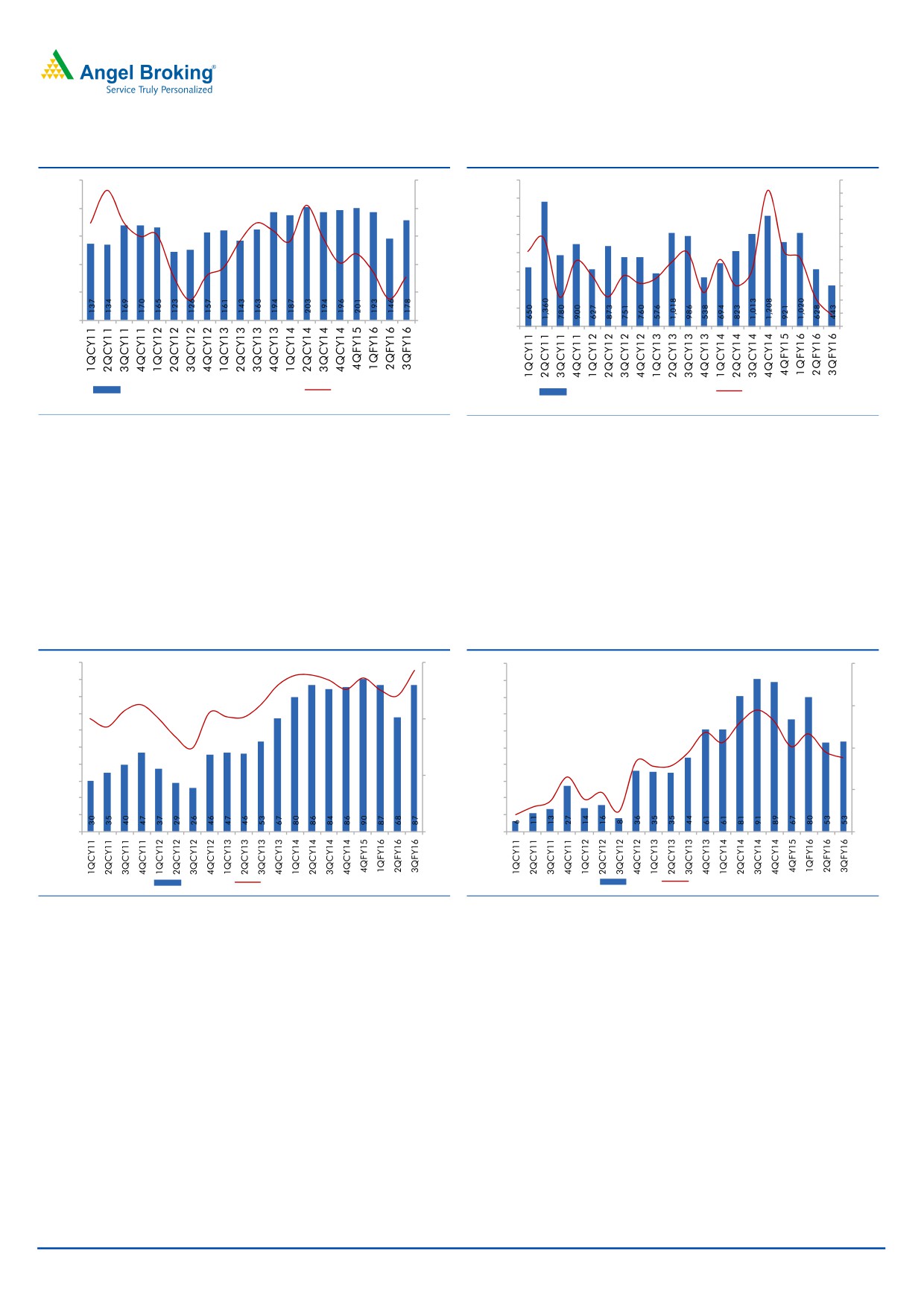

Top-line disappoints

GPPL reported 10.3% yoy decline in revenues to `152cr for 3QFY2016. On

sequential basis revenue was up 8.3%. Reported top-line number is below our

expectation of `170cr. Top-line de-growth on yoy basis is on account of (1) 9.2%

decrease in Container business volumes (to 178,000 TEUs), and

(2)

63.3%

decrease in Dry Bulk business (to 443,000MT). Decline in Container and Dry Bulk

revenues is attributable to (1) re-alignment of services by FE3, and (2) impact of

global slowdown.

Bulk volumes were impacted due to lower fertilizer and mineral volumes (declined

on qoq basis). A sharp decline in the coal volumes (owing to lower imports and

rail freight differential) contributed to the decline in yoy Bulk volumes. Coal volume

used to account for 60% of the Bulk volumes, but the mix declined to 40% during

3QFY2016.

The only positive on the top-line front is the 29% yoy increase in the Liquid Cargo

business to 189,000MT and further ramp-up in Ro-Ro business (7 calls/~4,500

cars were handled during the quarter).

February 2, 2016

2

GPPL | 3QFY2016 Result Update

Exhibit 2: Container volumes decline 9.2% yoy

Exhibit 3: Bulk volumes decline 63.3% yoy

250

60

1,600

140

120

1,400

200

40

100

1,200

80

150

20

1,000

60

40

800

20

100

0

600

0

400

(20)

50

(20)

(40)

200

(60)

0

(40)

0

(80)

Container Volume (TEUs in '000s)

yoy change (%)

Bulk Volumes (MT in '000s)

yoy change (%)

Source: Company, Angel Research

Source: Company, Angel Research

EBITDA Margin dips below 50% levels

GPPL reported an EBITDA of `87cr, which is ahead of our expectation of `81cr.

The reported EBITDA margin of the company came in at 57.1%, up from 48.2% in

the sequential previous quarter and from 50.5% in the corresponding quarter a

year ago. EBITDA during the quarter benefitted from a shift in the business mix

and `1cr of reversal with regards to the dredging cost.

Exhibit 4: EBITDA% expands to 57.1%

Exhibit 5: PAT% declines to 35.1%

100

60

100

80

90

90

80

80

60

70

70

40

60

60

50

50

40

40

40

20

30

30

20

20

20

10

10

0

0

0

0

EBITDA

EBITDA Margins (%)

PAT

PAT Margins (%)

Source: Company, Angel Research

Source: Company, Angel Research

GPPL reported an Adj. PAT of `53cr, down 40.3% yoy, and 12.6% qoq. In

2QFY2016, GPPL reversed asset impairment provision (`60.4cr) and deferred tax

charge of `60.0cr (for 1HFY2016) to arrive at an Adj. PAT of `61cr. Adj. PAT

margin during the quarter was at 35.0% vs 52.7% in the corresponding quarter a

year ago. Adj. PAT number on yoy basis was impacted due to (1) `28cr of tax

expense (vs tax exemption in 3QFY2015), (2) 53.4% increase in depreciation

expenses to `25cr, and (3) 1.6% decrease in other income to `20cr. A sharp

increase in depreciation expense is owing to change in estimated useful life of

assets.

February 2, 2016

3

GPPL | 3QFY2016 Result Update

Revision of our estimates

On incorporating adjustments for (1) decline in Container & Dry Bulk business

volumes, which could lead to change in the EBITDA mix, and (2) tax treatment, we

are reducing our PAT estimates for FY2016E and FY2017E to `240cr and `240cr,

respectively.

Exhibit 6: Revised estimates

FY2016E

FY2017E

Particulars (` cr)

Old New

% chg.

Old New

% chg.

Net Sales

629

632

0.5

684

705

3.1

EBITDA

321

326

1.6

357

368

3.1

EBITDA Margins (%)

51.0

51.6

52.2

52.2

Rep. PAT

309

240

(22.3)

284

240

(15.5)

Rep. PAT Margins (%)

49.1

38.0

41.5

34.0

Source: Company, Angel Research

February 2, 2016

4

GPPL | 3QFY2016 Result Update

Investment Arguments

Stable Container volumes and ramp-up in Bulk business to lead

to strong revenues for FY2016-17E

Ramp-up of operations from Hanjin, Maersk, and NMG helped GPPL report an

18.7% CAGR in Container volumes during CY2010-14 to 780,000 TEUs. Also, in

the last few quarters, GPPL has maintained an average quarterly Container volume

run-rate of ~180,000+ TEUs with the exception of 2QFY2016 (where it reported

~146,000 TEUs). Again, with the exception of 2QFY2016 and 3QFY2016, the

Container business in the prior 5 quarters has been running at over 90% utilization

levels (at the yard level). Sensing that the port would soon hit peak utilization, GPPL

embarked upon an expansion plan. This expansion plan (yard level capacity would

increase from 850,000 TEUs to 1,350,000 TEUs) is likely to get completed by

4QFY2016.

Notably, at the backdrop of a global slump in the pricing environment, many

shipping lines are exploring alternatives. This when coupled with loss of business

from FM3 and NMG in 2QFY2016, indicates that GPPL may find it challenging to

further scale up operations from here-on. Accordingly, we now expect GPPL to

report ~712,000 and ~758,000 TEUs for FY2016E and FY2017E, respectively.

Similarly, despite the recent traction in Bulk volumes business, we are now building

lower volumes for FY2016-17E.

Given the loss of business and slump in the global pricing environment, we expect

delays in ramp-up in operations from here-on. Accordingly, we have revised down

our estimates for FY2016-17E.

Ramp-up in Liquid Farms business:

Sensing business opportunity, GPPL tied-up with Aegis Logistics, IMC, and Gulf

Petrochem to construct and set-up Liquid Tank Farms. We expect GPPL to continue

reporting strong growth in profitability, well aided by ramp-up in business in Liquid

Tank Farms, which also happens to be a high margins business. EBITDA margin in

Liquid Tank Farms is in the range of 65-70%.

Outlook and Valuation

We expect GPPL to report soft earnings during FY2016-2017E, on the back of (1)

weak container volume growth outlook, and (2) delays in further ramp-up in the

Bulk business.

At the current market price of `156, GPPL is trading at FY2016E and FY2017E P/E

multiple of 31.4x and 31.4x, respectively. At current valuations, the stock price is

capturing all the possible positives.

We have valued the Ports business (on revised numbers) using free cash flow to

equity holders (FCFE) to arrive at FY2017E based business value of `160. Given

that the company is debt free, has negative working capital, strong market

positioning, and better revenue visibility, we have assumed cost of equity of 11%

for discounting the FCFE. We have assigned 10x P/E multiple to our FY2017E

earnings of Pipavav Rail Corporation Ltd (PRCL) to arrive at a business value of `7

(adjusted for

38.8% stake). On using the sum-of-the-parts based valuation

methodology, we arrive at FY2017E based price target of `167. Given the limited

upside potential in the stock from the current levels, we maintain our Neutral

rating on the stock.

February 2, 2016

5

GPPL | 3QFY2016 Result Update

Exhibit 7: SoTP Valuation Summary

Valuation

Particulars

Valuation (` cr)

Stake (%)

Per Share (`) Valuation Basis

(adj. for stake; ` cr)

Pipavav Port

7,750

100

7,750

160

FCFE valuation, 11% Cost of Equity

Pipavav Rail Corp.

903

39

350

7

10x FY17E P/E

Total Value of GPPL

8,653

8,100

167

Source: Angel Research

Company Background

Gujarat Pipavav Port Ltd (GPPL) is India's first BOT Port project awarded to SKIL

Infrastructure led JV (Gujarat Maritime Board being the other partner in the JV) in

1992. In 2005, an APM Terminals (part of AP Moller Maersk) led consortium

bought the entire stake in GPPL from SKIL. APM Terminals, through APM Terminals

Mauritius Ltd, holds 43.01% stake in GPPL.

Details of the Concession Agreement

Gujarat Pipavav Port Ltd. (GPPL) signed a 30 years’ concession agreement with a

JV led by Gujarat Maritime Board (GMB; SKIL being the other partner) to build,

construct, operate and maintain Pipavav Port, at Amreli district in Gujarat in Aug-

1992. In 1998, GMB divested its entire stake in GPPL to SKIL. Later in 2005, SKIL

divested its entire stake to APM Terminals led investors.

GPPL is looked upon as one of the most efficient port operators by shipping liners.

Located near the entrance of the Gulf of Khambhat, this port enjoys a location

advantage as the 2 islands act as natural breakwater. This location advantage

helps it in being identified as part of the main maritime trade route, which is

helpful in import and export to USA, Middle East, China and other European

markets.

February 2, 2016

6

GPPL | 3QFY2016 Result Update

Income Statement

Y/E March (` cr)

CY13

FY15*

FY16E

FY17E

Net Sales

474

792

632

705

% Chg

67.2

(20.2)

11.5

Total Expenditure

261

366

306

337

Operating Expenses

132

185

145

162

Employee benefits Expense

42

62

52

59

Other Expenses

87

119

109

116

EBITDA

213

426

326

368

% Chg

100.6

(23.5)

12.8

EBIDTA %

44.9

53.8

51.6

52.2

Depreciation

61

83

97

112

EBIT

152

343

230

256

% Chg

126.0

(33.0)

11.5

Interest and Financial Charges

37

26

0

0

Other Income

61

116

74

102

PBT

175

433

304

358

Tax

0

0

125

118

% of PBT

0.0

0.0

41.0

33.0

PAT before Exceptional item

175

433

179

240

Exceptional item

(16)

45

(60)

0

PAT

192

389

240

240

% Chg

102.6

(38.4)

0.2

PAT %

40.5

49.1

37.9

34.1

Diluted EPS

4

8

5

5

% Chg

102.6

(38.4)

0.2

Note: * GPPL switched from Dec to Mar year ending

February 2, 2016

7

GPPL | 3QFY2016 Result Update

Balance Sheet

Y/E March (` cr)

CY13

FY15*

FY16E

FY17E

Sources of Funds

Equity Capital

483

483

483

483

Reserves Total

920

1,307

1,547

1,787

Networth

1,404

1,791

2,030

2,270

Total Debt

282

0

0

0

Other Long-term Liabilities

12

14

13

13

Other Long-term Provisions

24

24

24

24

Total Liabilities

1,721

1,829

2,067

2,307

Application of Funds

Gross Block

1,919

1,983

2,395

2,685

Accumulated Depreciation

561

645

740

852

Net Block

1,358

1,338

1,656

1,833

Capital WIP

106

65

40

14

Investments

83

83

83

83

Current Assets

Inventories

12

14

19

22

Sundry Debtors

34

36

35

37

Cash and Bank Balance

202

245

152

248

Loans, Advances & Deposits

66

202

202

202

Other Current Asset

4

7

4

4

Current Liabilities

145

163

126

139

Net Current Assets

173

340

286

373

Other Assets

1

3

3

3

Total Assets

1,721

1,829

2,067

2,307

Note: * GPPL switched from Dec to Mar year ending

February 2, 2016

8

GPPL | 3QFY2016 Result Update

Cash Flow Statement

Y/E March (` cr)

CY13

FY15P*

FY16E

FY17E

Profit before tax

192

433

304

358

Depreciation

61

83

97

112

Change in Working Capital

47

6

(43)

8

Interest Expenses & Other Adj.

(48)

13

0

(10)

Direct taxes paid

(22)

(41)

(125)

(118)

Cash Flow from Operations

230

494

233

350

(Inc)/ Dec in Fixed Assets

(91)

(23)

(370)

(265)

(Inc)/ Dec in Investments & Oth. Adj.

(85)

(40)

0

10

Cash Flow from Investing

(176)

(63)

(370)

(255)

Issue/ (Buy Back) of Equity

0

0

0

0

Inc./ (Dec.) in Loans

(17)

(282)

0

0

Dividend Paid (Incl. Tax)

0

0

0

0

Interest Expenses

(38)

(26)

0

0

Cash Flow from Financing

(54)

(308)

0

0

Inc./(Dec.) in Cash

(0)

124

(138)

95

Opening Cash balances

51

51

175

37

Closing Cash balances

51

175

37

133

Note: * GPPL switched from Dec to Mar year ending

Ratio Analysis

Y/E March

CY13

FY15P*

FY16E

FY17E

Valuation Ratio (x)

P/E (on FDEPS)

39.2

19.4

31.4

31.4

P/CEPS

29.8

16.0

22.4

21.4

Dividend yield (%)

0.0

0.0

0.0

0.0

EV/Sales

16.1

9.2

11.6

10.3

EV/EBITDA

35.8

17.1

22.6

19.7

EV / Total Assets

4.1

3.7

3.3

3.0

Per Share Data (`)

EPS (fully diluted)

4.0

8.1

5.0

5.0

Cash EPS

5.2

9.8

7.0

7.3

DPS

0.0

0.0

0.0

0.0

Book Value

38.7

41.3

48.0

50.7

Returns (%)

RoCE (Pre-tax)

13.3

26.4

15.9

16.7

Angel RoIC (Pre-tax)

12.6

25.7

15.0

15.8

RoE

14.7

24.3

12.5

11.2

Turnover ratios (x)

Asset Turnover (Gross Block) (X)

0.1

0.2

0.1

0.1

Inventory / Sales (days)

9

6

9

11

Receivables (days)

27

15

19

17

Payables (days)

55

58

72

57

Note: * GPPL switched from Dec to Mar year ending

February 2, 2016

9

GPPL | 3QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

GPPL

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 2, 2016

10