3QFY2016 Result Update | Tyres

November 6, 2015

Goodyear India

ACCUMULATE

CMP

`573

Performance Highlights

Target Price

`622

Y/E December (` cr) 3QFY2016 3QCY2014* % chg (yoy) 2QFY2016

% chg (qoq)

Investment Period

12 Months

Net sales

382

402

(5.0)

432

(11.8)

EBITDA

46

40

14.4

59

(22.6)

Stock Info

EBITDA margin (%)

11.9

9.9

202bp

13.6

(168)bp

Sector

Tyres

Adjusted PAT

29

25

15.2

36

(19.9)

Source: Company, Angel Research; Note: *reporting changed from CY to FY starting Jan 2015

Market Cap (` cr)

1,321

Net Debt

(365)

Note- Goodyear India (GIL) is shifting from calendar year reporting followed until

Beta

0.8

now, to financial year reporting. Hence FY2016 will consist of five quarters.

52 Week High / Low

713 / 502

GIL reported a disappointing set of numbers for 3QFY2016. Its top-line witnessed

Avg. Daily Volume

20,231

a 5.0% yoy decline to `382cr. The raw material cost declined by 495bp yoy to

Face Value (`)

10

63.4% of sales, while employee and other expense increased by 193bp yoy and

BSE Sensex

26,304

100bp yoy to 7.7% and 16.9% of sales respectively. The EBITDA margin

Nifty

7,955

expanded by 202bp yoy to 11.9%. On the back of lower raw material cost, the

Reuters Code

GDYR.BO

net profit for the quarter increased by 15.2% yoy to `29cr.

Bloomberg Code

GDYR IN

Expansion drive to lead to recovery in top-line: GIL has laid out plans to

significantly grow its presence in the passenger car segment in India, over the

Shareholding Pattern (%)

next five years. The company aspires to be one of the top players in the mid to

Promoters

74.0

premium, and SUV segments, for passenger cars. It is also evaluating entry into

MF / Banks / Indian Fls

8.0

newer segments; in order to reach its goal, the company is weighing organic as

FII / NRIs / OCBs

0.8

well as in-organic growth options, to expand in India.

Indian Public / Others

17.2

Strong balance sheet with high RoIC: GIL is a debt free-cash rich company with

RoIC estimated at 75.8% for FY2017. The company’s cash and equivalents are

expected to be at `524cr by FY2017-end, which would amount to ~40% of the

Abs. (%)

3m 1yr 3yr

current market cap. More importantly, GIL is one of the cheapest MNCs available

Sensex

(6.8)

(5.8)

40.2

to invest in, in the similar market cap range.

GOODYEAR

(10.6)

(13.0)

73.4

Outlook and valuation: We expect the company’s top-line to be at `1,888cr and

`1,680cr in FY2016E and FY2017E respectively. Raw material cost is expected to

remain stable over FY2016E-17E resulting in EBITDA margin of 12.1% in

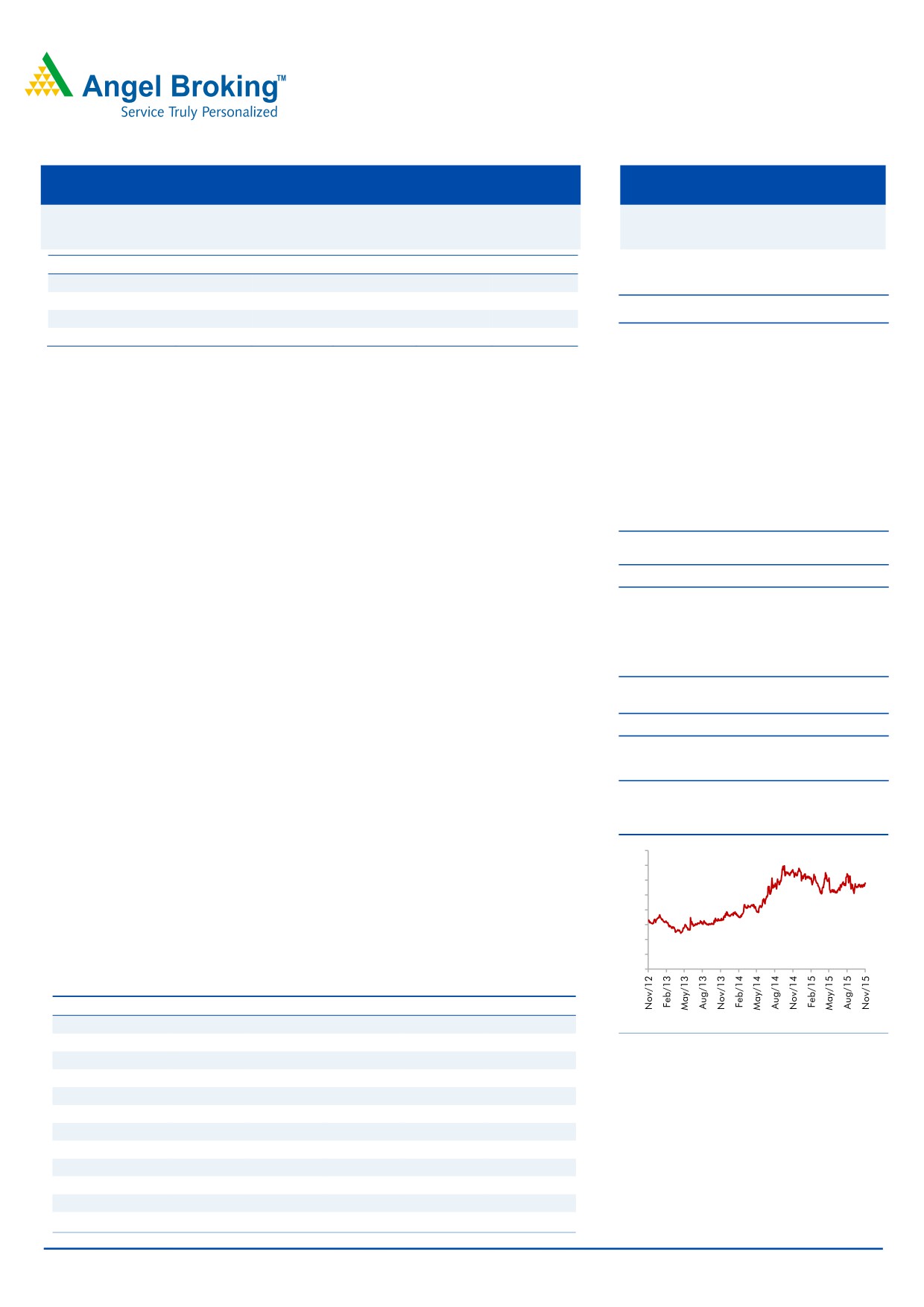

3-year Daily Price Chart

FY2016E and 11.9% in FY2017E. Consequently, we estimate the net profit to be

800

at `130cr in FY2017E. At the current market price, the stock is trading at a PE of

700

10.1x its FY2017E earnings. On a TTM basis, GIL is one of the cheapest MNCs

600

available as it trades at a PE of 14.0x while other MNCs (having market cap of

500

400

`1,000cr-`5,000cr) trade above the 20.0x mark (median of 33.1x). We maintain

300

our Accumulate rating on the stock and assign a target price of `622 based on a

200

target PE of 11x for FY2017E.

100

0

Key Financials

Y/E Dec (` cr)

CY2012

CY2013

CY2014

FY2016E*

FY2017E

Net Sales

1,481

1,569

1,579

1,888

1,680

% chg

(2.1)

5.9

0.7

19.6

(11.0)

Source: Company, Angel Research

Net Profit

57

94

101

144

130

% chg

(13.4)

66.3

7.6

41.8

(9.1)

EBITDA (%)

6.1

8.9

9.7

12.1

11.9

EPS (`)

24.5

40.8

43.9

62.2

56.6

P/E (x)

23.4

14.0

13.0

9.2

10.1

P/BV (x)

3.7

3.1

2.7

2.2

1.8

RoE (%)

16.9

24.2

22.0

25.9

19.7

RoIC (%)

65.1

95.4

94.6

102.1

75.8

Milan Desai

EV/Sales (x)

0.7

0.6

0.6

0.5

0.5

+91- 22- 4000 3600 Ext: 6846

EV/EBITDA (x)

11.9

7.2

6.2

3.9

4.0

Source: Company, Angel Research; Note: *reporting changed from CY to FY starting January 2015; CMP as Nov. 5, 2015

Please refer to important disclosures at the end of this report

1

Goodyear | 3QFY2016 Result Update

Exhibit 1: 2QFY2016 performance

Y/E December (` cr)

3QFY16 3QCY14*

yoy chg (%)

2QFY16

qoq chg (%) 9MFY2016 9MCY2014

% chg

Net Sales

382

402

(5.0)

432

(11.8)

1089

1222

(10.9)

Net raw material

242

275

(11.9)

278

(13.0)

692

855

(19.1)

(% of Sales)

63.4

68.4

(495)bp

64.3

(92)bp

63.5

70.0

(644)bp

Staff Costs

30

23

26.7

28

6.4

82

68

20.3

(% of Sales)

7.7

5.8

193bp

6.4

132bp

7.5

5.6

195bp

Other Expenses

64

64

1.0

68

(4.5)

184

175

5.5

(% of Sales)

16.9

15.9

100bp

15.6

128bp

16.9

14.3

263bp

Total Expenditure

336

362

(7.1)

374

(10.0)

958

1098

(12.7)

EBITDA

46

40

14.4

59

(22.6)

131

124

5.5

EBITDA margin (%)

11.9

9.9

202bp

13.6

(168)bp

12.0

10.2

186bp

Interest

1

1

(12.7)

1

4.5

2

3

(28.6)

Depreciation

8

7

5.0

8

(4.1)

25

21

18.1

Other Income

7

7

10.3

6

26.7

20

24

(18.6)

PBT

44

38

16.0

56

(20.5)

124

125

12.6

(% of Sales)

11.6

9.5

12.9

11.4

10.2

Tax

15

13

17.6

20

(21.7)

43

43

1.6

(% of PBT)

34.6

34.1

35.1

34.8

34.1

Reported PAT

29

25

15.2

36

(19.9)

81

82

(1.6)

PATM

7.6

6.3

8.4

7.4

6.7

Equity capital (cr)

23

23

23

23

23

EPS (`)

12.6

10.9

15.2

15.7

(19.9)

35.1

35.6

(1.6)

Source: Company, Angel Research; *reporting changed from CY to FY starting January 2015

Exhibit 2: Actual vs. Angel estimates (2QFY2016)

Actual (` cr)

Estimate (` cr)

Var (%)

Total Income

382

412

(7.3)

EBIDTA

46

56

(18.4)

EBIDTA margin (%)

11.9

13.6

(163)bp

Adjusted PAT

29

37

(21.5)

Source: Company, Angel Research

Revenue and margin below expectations

For 3QFY2016, GIL reported numbers that were mostly below our estimates. The

top-line witnessed a decline of 5.0% yoy to `382cr which is below our estimate of

`412cr. The subdued top-line is owing to poor tractor sales coupled with declining

realizations on account of pass through of lower raw material prices. Tractor

volumes for M&M and Escorts, have declined in 1HFY2016 by 20.7% and 19.9%

yoy respectively. As per our estimates, the overall tractor industry witnessed a

volume decline of ~20.3% for the same period. The raw material cost declined by

495bp yoy to 63.4% of sales while employee and other expense increased by

193bp yoy and 100bp yoy to 7.7% and 16.9% of sales respectively. The EBITDA

margin expanded by 202bp yoy to 11.9%. On the back of lower raw material cost,

the net profit for the quarter increased by 15.2% yoy to `29cr.

November 6, 2015

2

Goodyear | 3QFY2016 Result Update

Investment rationale

Focus to be among the leading players in passenger car segment

GIL is targeting towards becoming one of the top players in the passenger car tyre

segment in the next five years. The company is focusing on increasing its presence

in both the OEM and the aftermarket segments. It will be launching new products

and widening its product portfolio in the mid to premium and SUV segments of

passenger vehicles. To reach its goal, the company is weighing both organic as

well as in-organic growth options to expand in the segment. The Management has

indicated that apart from farm and passenger car tyres, it is looking at entering

into newer segments and ramping up newer launches to grow in India.

Continuous innovation to aid growth

GIL is a 74% subsidiary (indirect) of Goodyear Tire & Rubber Company (USA). GIL

benefits from the advanced technology and support from its American parent

which helps it in launching technologically superior products for the Indian

markets. In the past year, it launched Run-on-Flat tyres, which have a capability of

covering a distance of up to 80km after a puncture. Recently, the company has

launched Assurance TripleMax tyre with HYDROGRIP technology, which has the

ability to reduce braking distance by more than 2 meters on wet roads compared

to other tyres. The company had been drawing mixed reviews for its products in

the past. However, the reviews have now turned more favorable with various

measures adopted by the company to further improve the quality of its product

portfolio. Introduction of innovative products and technologies has enabled GIL to

shore up consumer confidence and initiatives like “Worry Free Service Program”

are likely to work in favor of the company going forward.

Strong balance sheet with high RoIC; valuations remain

attractive!

GIL is a debt free-cash rich company with RoIC estimated at 75.8% for FY2017.

The company’s cash and equivalents are expected to be at

`524cr by

FY2017-end, which would amount to ~40% of the current market cap.

As far as valuations are concerned, GIL is among the cheapest MNCs available

with market cap in the range of `1,000cr-`5,000cr. On TTM basis, GIL trades at a

P/E of 14.0x vis-à-vis median TTM PE of ~33.1x for other MNCs. Thus, GIL is

available at an attractive valuation considering the fact that all other MNCs are

trading above the 20.0x mark.

November 6, 2015

3

Goodyear | 3QFY2016 Result Update

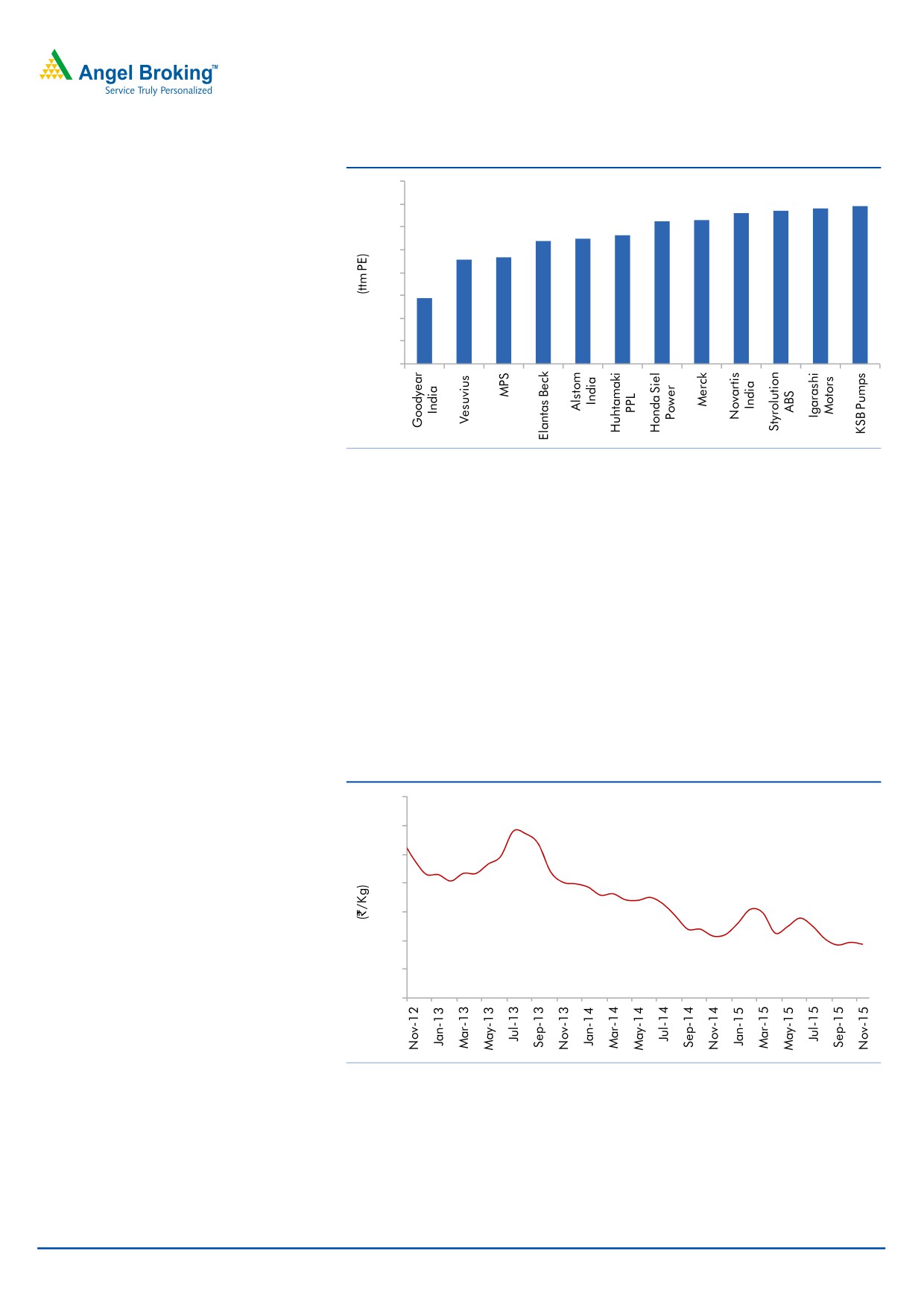

Exhibit 3: On TTM PE basis, GIL is cheapest amongst MNCs

40

34

35

33

34

35

31

32

28

28

30

27

23

23

25

20

14

15

10

5

0

Source: Company, Angel Research

Stable rubber prices to keep margins at current levels

Natural Rubber (NR) has been trading at lower levels in the recent past leading to

tyre companies reporting all-time-high margins. NR prices are unlikely to increase

significantly, tracing high global inventory levels and slowdown in demand from

China. Moreover, price of SBR (synthetic rubber) is expected to remain under

pressure tracing weakness in butadiene prices.

Despite Thai government’s efforts to shore up NR prices by curtailing supplies, NR

continues to show no signs of gaining strength and is likely to remain range

bound, at around current levels. NR currently trades at `112/kg in the domestic

market; we expect it to likely trade at the levels of ~`130/kg in the near future.

Exhibit 4: Domestic Monthly Average Prices

215

195

175

155

135

115

113

95

75

Source: Rubber Board, Angel Research

November 6, 2015

4

Goodyear | 3QFY2016 Result Update

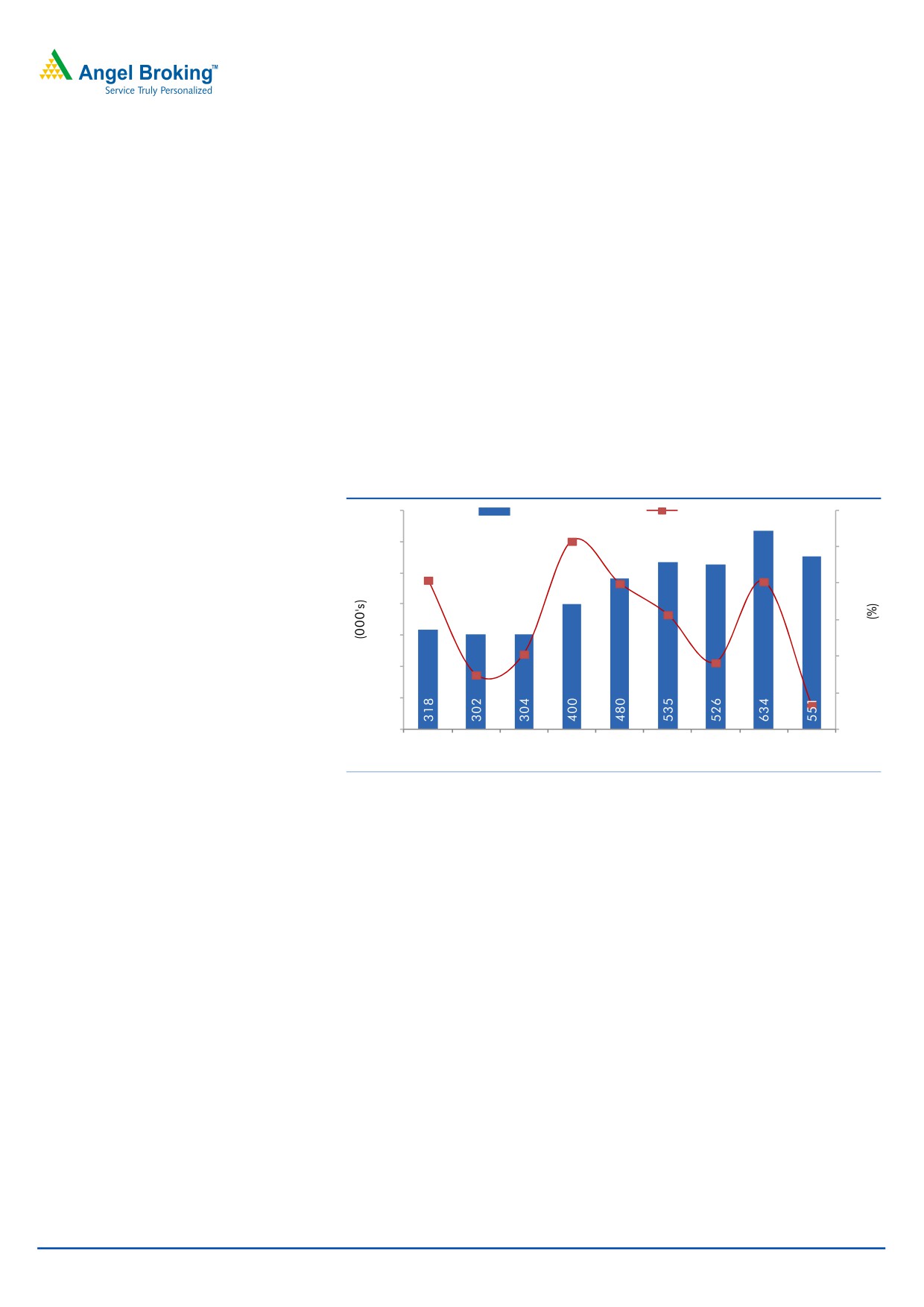

Tractor demand outlook muted in the near term, long term

prospects remain intact

GIL is a market leader in the tractor tyre industry, with a market share of ~22% in

the front tyre segment and ~34% in the rear tyre segment. After a strong

performance in the first two quarters of calendar year 2014, tractor sales declined

on a month on month basis in the latter half of the year. The trend seems to be

continuing with tractor sales being dismal in 2015, mainly due to unseasonal

rains; further, only a moderate increase in minimum support prices (MSPs) this

year has hurt the rural economy, and in turn, tractor sales numbers.

Industry reports suggest that the tractor industry is expected to post a CAGR of 6-

7% over the next five years due to an anticipated increase in MSPs, easy availability

of financing, government initiatives to improve irrigation (aimed at reducing

dependence on erratic monsoon) and need for higher level of tractor penetration.

Exhibit 5: Domestic Tractor sales trend

700

Tractor volume (LHS)

yoy growth (RHS)

40

600

31.6

30

500

20.0

20.9

20.5

20

400

11.5

10

300

0.7

0

(5.0)

(1.7)

200

(10)

100

(13

.1)

0

(20)

CY06

CY07

CY08

CY09

CY10

CY11

CY12

CY13

CY14E

Source: TMA, Industry Reports, Angel Research

November 6, 2015

5

Goodyear | 3QFY2016 Result Update

Financials

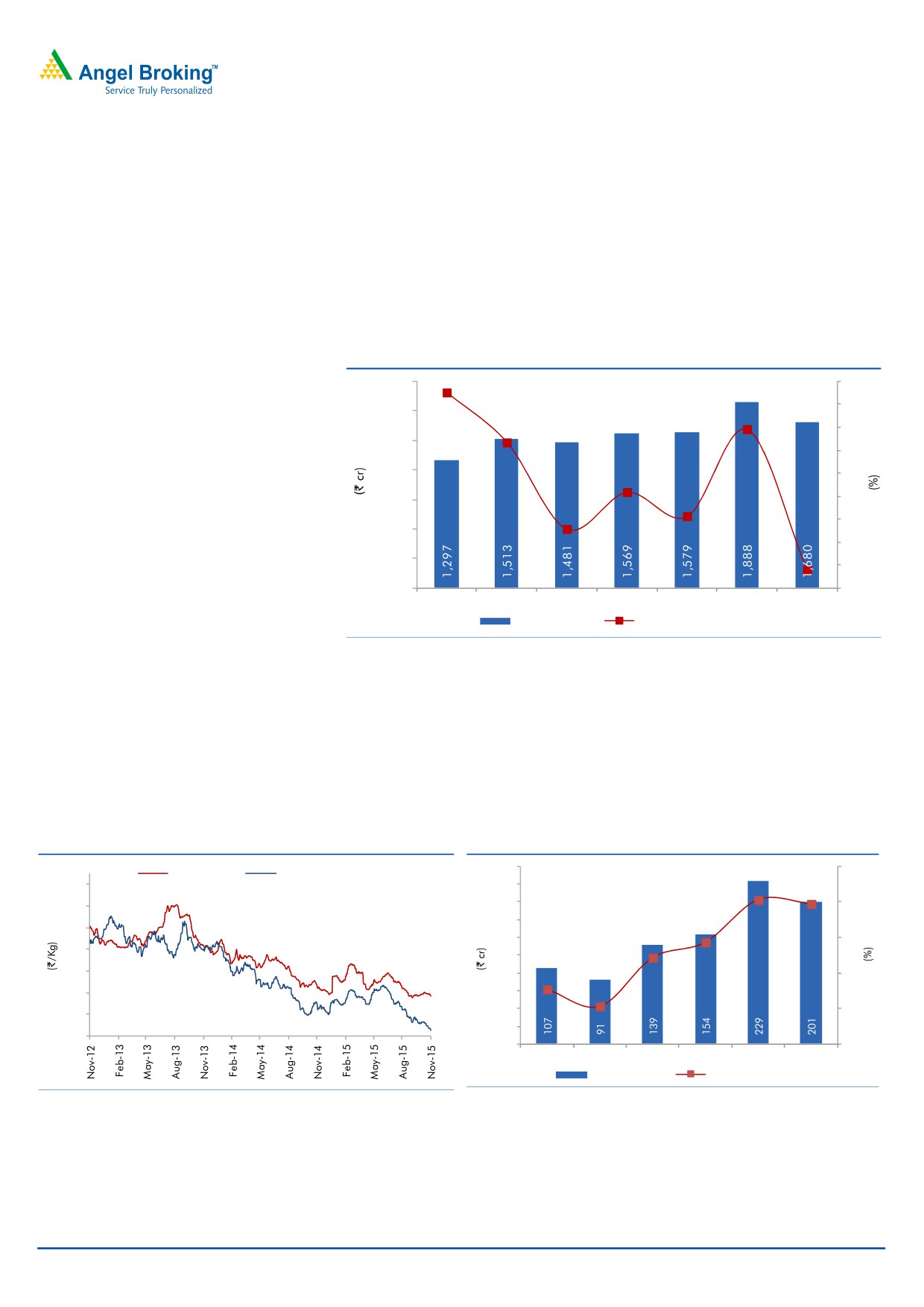

Revenue growth to recover in CY2016

Although the near term outlook remains subdued owing to poor tractor sales, we

expect stable improvement in the company’s performance over FY2016E-17E

citing recovery in tractor sales, Management’s drive to expands its presence in the

passenger vehicle segment and entry into newer segments. We expect GIL’s

revenue to be at `1,888cr and `1,680cr in FY2016E and FY2017E, respectively.

Exhibit 6: Top-line to recover

2,100

30

27.6

25

1,800

19.6

20

16.7

1,500

15

1,200

10

5.9

5

0.7

900

0

(2.1)

600

(5)

300

(11

.0)

(10)

0

(15)

CY2010

CY2011

CY2012

CY2013

CY2014 FY2016E* FY2017E

Revenue (LHS)

Revenue yoy growth (RHS)

Source: Company, Angel Research; *reporting changed from CY to FY starting January 2015

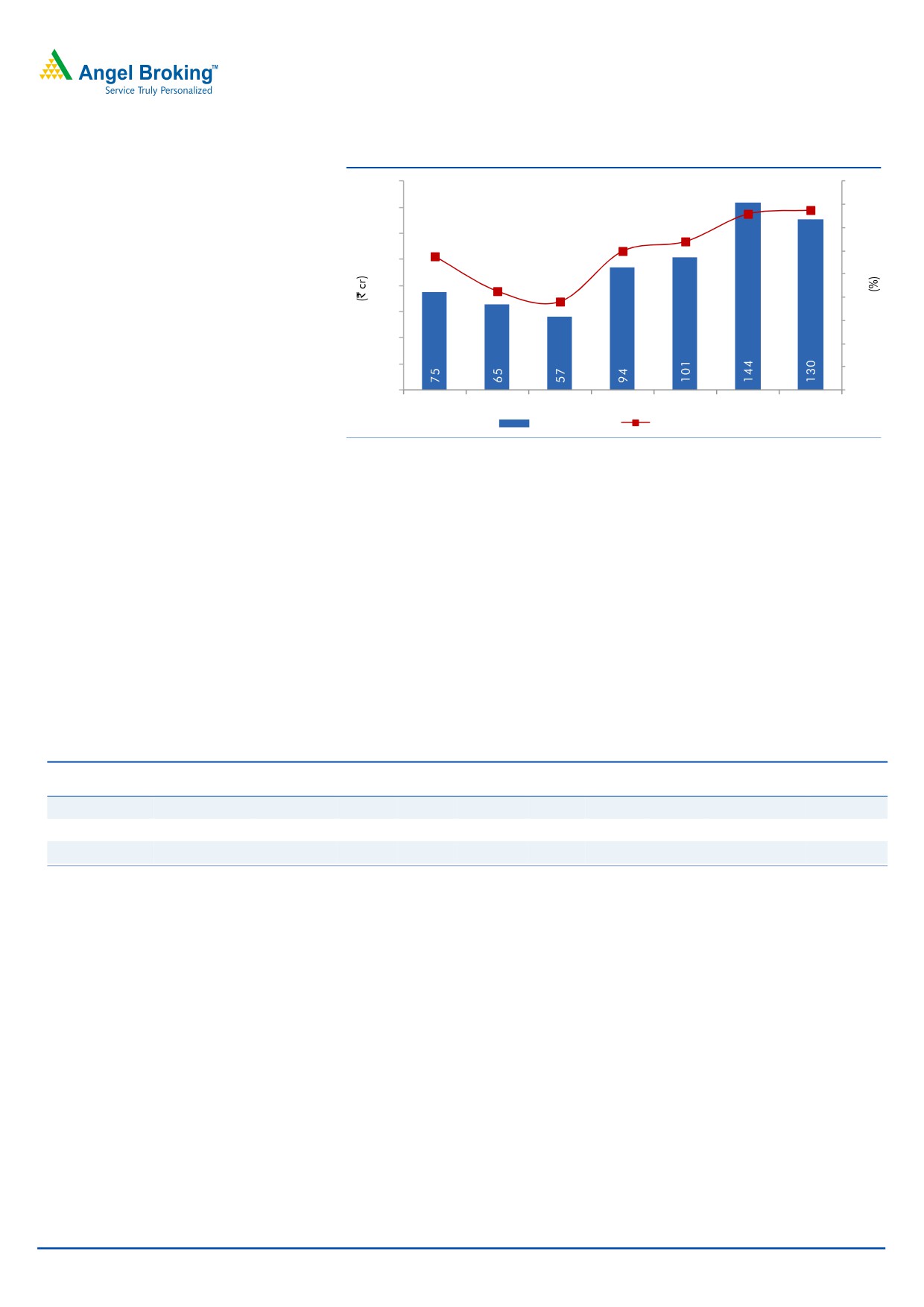

Improvement in margins

Domestic rubber prices have seen a declining trend since November 2011 from

the high of ~`200/kg to current levels of ~`112/kg while international prices are

trading close at ~`81/kg. We expect rubber prices to remain at an average level

of ~`130/kg in FY2016-17E, thus leading the EBITDA margin to be at 11.9%

Exhibit 7: Rubber price trend

Exhibit 8: Improvement in EBITDA margin...

250

14

Domestic Price

International Price

215

225

12.1

11.9

200

12

195

175

175

150

10

9.7

155

125

8.9

135

100

8

115

112

75

7.1

50

6.1

6

95

25

81

75

0

4

CY2011

CY2012

CY2013

CY2014

FY2016E* FY2017E

EBITDA (LHS)

EBITDA margin (RHS)

Source: Rubber Board, Angel Research

Source: Company, Angel Research; *reporting changed from CY to FY

starting January 2015

Led by recovery in volumes, coupled with raw material prices remaining at lower

levels, the net profit is expected to be at `144cr and at `130cr in FY2016E and

FY2017E, respectively.

November 6, 2015

6

Goodyear | 3QFY2016 Result Update

Exhibit 9: Net profit trend

160

9

7.8

7.6

140

8

6.4

7

120

6.0

5.8

6

100

4.3

5

80

3.8

4

60

3

40

2

20

1

0

0

CY2010

CY2011

CY2012

CY2013

CY2014

FY2016E* FY2017E

PAT (LHS)

PAT margin (RHS)

Source: Company, Angel Research; *reporting changed from CY to FY starting January 2015

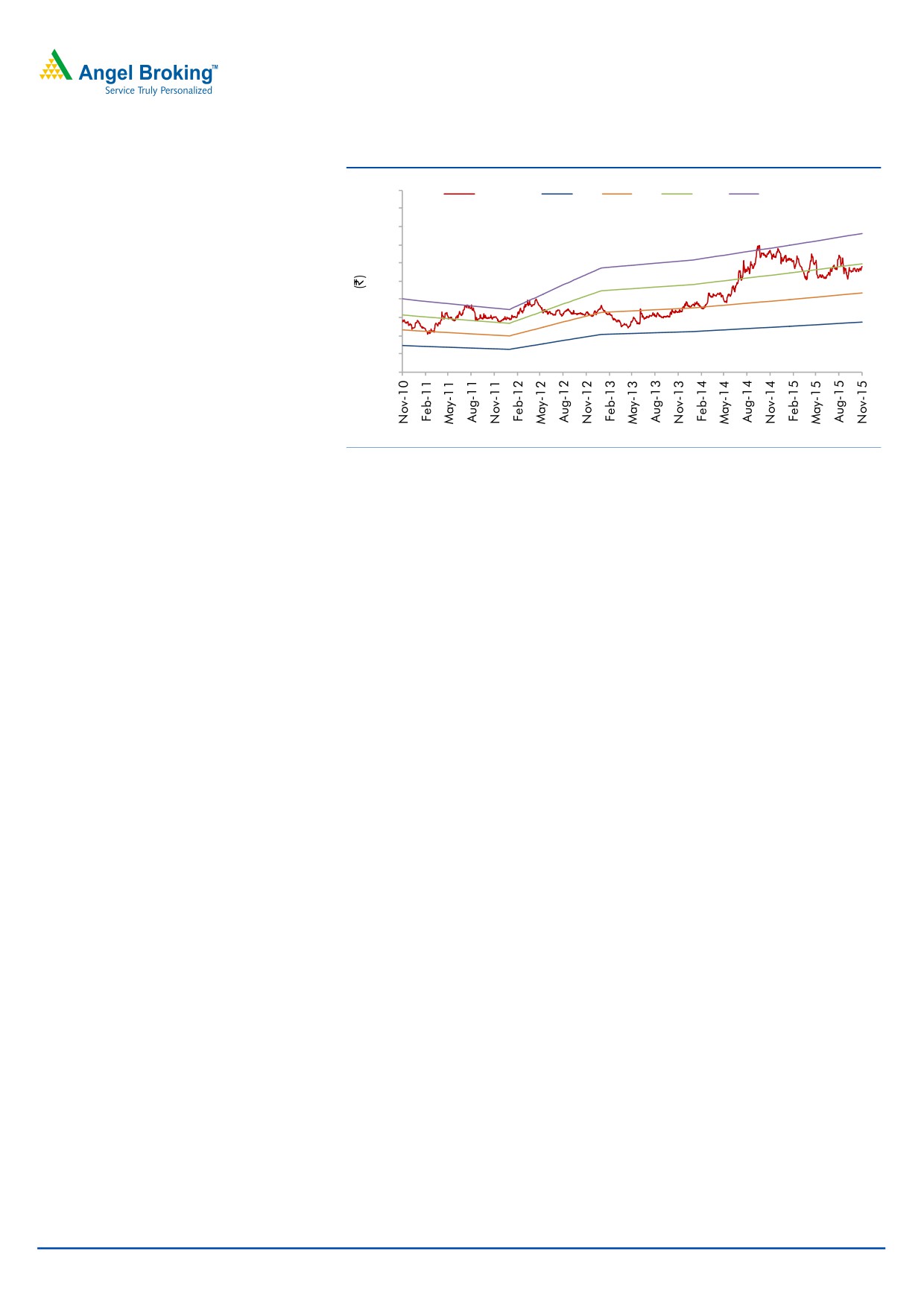

Outlook and valuation

We have estimated the top-line to be at `1,888cr and `1,680cr in FY2016E (15

months) and FY2017E, respectively, while the net profit is expected to be at `144cr

and `130cr for the same period. At the current market price, GIL trades at a PE of

10.1x its FY2017E earnings (14.0x on TTM basis). GIL is among the cheapest

stocks available in the MNC space (with market cap in the range of `1,000cr-

`1,500cr). All other MNCs, falling in a similar market cap range, are trading

above the 20.0x mark on TTM basis with median PE being 33.1x. We maintain our

Accumulate recommendation on the stock and assign a target price of `622 based

on a target PE of 11x for FY2017E.

Exhibit 10: Relative valuation

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/EBITDA

EV/Sales

Year end

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

Apollo

FY2017E

12,689

16.0

968

19.0

14.1

8.4

1.1

5.0

0.8

MRF

FY2017E

14,488

21.1

1,611

3,797.9

21.2

10.1

1.9

4.8

1.0

Goodyear

FY2017E

1,680

11.9

130

56.6

19.7

10.1

1.8

4.0

0.5

Source: Angel Research

GIL is fairly priced vis-à-vis its peers in the tyre industry in terms of PE and PBV

multiples considering its high ROE; but it is trading at a relatively lower valuation

of 0.5x EV/Sales multiple based on FY2017E earnings.

November 6, 2015

7

Goodyear | 3QFY2016 Result Update

Exhibit 11: One-year forward P/E band

1000

Price (`)

5x

8x

11x

14

900

800

700

600

500

400

300

200

100

0

Source: Company, Angel Research

November 6, 2015

8

Goodyear | 3QFY2016 Result Update

Risks

Volatile rubber prices: Rubber constitutes ~65% of the total raw-material cost in

the manufacture of tyres. Domestic rubber prices have declined from the level of

`200/kg in June 2012 to average levels of `135/kg in CY2014 and to `112/kg

currently. However, any increase in rubber prices would have a negative impact on

the company’s EBITDA margin and consequently on its profit.

Concentrated product portfolio: GIL’s product portfolio is primarily

concentrated to tractor and passenger car tyres. Both these segments constitute

~98% of the total tonnage off-take of the company. Due to high dependency on

these segments, GIL is exposed to the risk of any slowdown in these segments.

Termination of off-take agreement: GIL is in an off-take agreement (on a

non-exclusive basis and can be terminated by either party with a four-month

notice) with Goodyear South Asia Tyres Pvt Ltd, from which it procures passenger

vehicle tyres. Considering that a significant percentage of GIL’s sales are backed

by this agreement, termination of the same may affect GIL’s sales considerably.

Hike in import duty of rubber: In the wake of falling domestic rubber prices, the

Central Government has increased the import duty on natural rubber to lower of

25% or `30/kg, from lower of 20% or `30/kg. Further upward revision in the

import duty will have an adverse impact on GIL’s profitability.

Company Background

GIL is a subsidiary of Goodyear Orient Company (Private) Ltd (a wholly owned

subsidiary of Goodyear Tire and Rubber Company, USA), which holds a 74% stake

in the company. The company majorly caters to the tractor tyre segment, where it

has a market share of ~22.0% in tractor front tyres and ~34.3% in tractor rear

tyres as of CY2012.

November 6, 2015

9

Goodyear | 3QFY2016 Result Update

Profit & Loss Statement

Y/E December (` cr)

CY2012

CY2013

CY2014

FY2016E*

FY2017E

Gross sales

1,613

1,706

1,709

2,048

1,822

Less: Excise duty

132

137

130

160

142

Net Sales

1,481

1,569

1,579

1,888

1,680

Other operating income

-

-

-

-

-

Total operating income

1,481

1,569

1,579

1,888

1,680

% chg

(2.1)

5.9

0.7

19.6

(11.0)

Net Raw Materials

1,102

1,116

1,094

1,210

1,086

Personnel

81

88

99

140

124

Other

207

226

232

310

269

Total Expenditure

1,391

1,430

1,426

1,660

1,480

EBITDA

91

139

154

229

201

% chg

(15.3)

53.2

10.5

49.0

(12.3)

(% of Net Sales)

6.1

8.9

9.7

12.1

11.9

Depreciation

24

25

29

39

35

EBIT

67

114

125

190

166

% chg

(23.7)

70.8

9.9

51.8

(12.8)

(% of Net Sales)

4.5

7.3

7.9

10.1

9.9

Interest & other charges

4

2

3

4

3

Other Income

22

30

32

31

35

(% of sales)

1.5

1.9

2.0

1.6

2.1

PBT

85

142

154

217

198

% chg

(12.1)

67.7

8.2

41.7

(9.1)

Tax

28

48

52

74

67

(% of PBT)

33.5

33.7

34.0

34.0

34.0

PAT (reported)

56

94

101

144

130

Extraordinary (Exp)/Inc.

(0)

-

-

-

-

ADJ. PAT

57

94

101

144

130

% chg

(13.4)

66.3

7.6

41.8

(9.1)

(% of Net Sales)

3.8

6.0

6.4

7.6

7.8

Basic EPS (`)

24.5

40.8

43.9

62.2

56.6

Fully Diluted EPS (`)

24.5

40.8

43.9

62.2

56.6

% chg

(12.4)

66.3

7.6

41.8

(9.1)

*reporting changed from CY to FY starting January 2015

November 6, 2015

10

Goodyear | 3QFY2016 Result Update

Balance Sheet

Y/E December (` cr)

CY2012

CY2013

CY2014E

FY2016E*

FY2017E

SOURCES OF FUNDS

Equity Share Capital

23

23

23

23

23

Preference Capital

-

-

-

-

-

Reserves& Surplus

331

400

474

589

692

Shareholders’ Funds

354

424

497

613

715

Minority Interest

-

-

-

-

-

Total Loans

-

-

-

-

-

Deferred Tax Liability

11

13

14

12

12

Other Long Term Liabilities

-

3

5

4

4

Long Term Provisions

19

20

21

25

22

Total Liabilities

384

459

536

653

753

APPLICATION OF FUNDS

Gross Block

398

430

481

541

595

Less: Acc. Depreciation

201

220

241

280

316

Net Block

198

210

240

261

280

Capital Work-in-Progress

17

32

17

10

10

Goodwill

-

-

-

-

-

Investments

-

-

-

-

-

Long Term Loans and adv.

19

17

19

15

15

Other non-current assets

0

0

1

1

1

Current Assets

507

600

617

701

823

Cash

238

317

365

425

524

Loans & Advances

6

10

6

11

10

Inventory

104

99

123

124

133

Debtors

154

165

112

133

148

Other Current Assets

4

9

10

8

8

Current liabilities

357

400

358

335

376

Net Current Assets

150

200

259

366

447

Misc. Exp. not written off

-

-

-

-

-

Total Assets

384

459

536

653

753

*reporting changed from CY to FY starting January 2015

November 6, 2015

11

Goodyear | 3QFY2016 Result Update

Cash Flow Statement

Y/E December (` cr)

CY2012

CY2013

CY2014E FY2016E* FY2017E

Profit before tax

85

142

154

217

198

Depreciation

24

25

29

39

35

Change in Working Capital

(40)

29

(11)

(46)

18

Other income

(22)

(30)

(32)

(31)

(35)

Direct taxes paid

(28)

(48)

(52)

(75)

(67)

Others

7

14

12

-

-

Cash Flow from Operations

26

131

99

104

149

(Inc.)/Dec. in Fixed Assets

(23)

(46)

(36)

(53)

(54)

(Inc.)/Dec. in Investments

-

-

-

-

-

(Incr)/Decr In L.T. loan and adv.

(4)

2

(2)

3

-

Other income

22

30

32

31

35

Others

(10)

(18)

(17)

-

-

Cash Flow from Investing

(14)

(32)

(24)

(19)

(19)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

-

-

2

(1)

-

Inc./(Dec.) in L.T. Pro. & Liab.

1

1

1

4

(3)

Dividend Paid (Incl. Tax)

(19)

(24)

(28)

(28)

(28)

Others

(5)

3

(2)

-

-

Cash Flow from Financing

(23)

(21)

(27)

(25)

(30)

Inc./(Dec.) in Cash

(11)

78

48

60

99

Opening Cash balances

249

238

317

365

425

Closing Cash balances

238

317

365

425

524

*reporting changed from CY to FY starting January 2015

November 6, 2015

12

Goodyear | 3QFY2016 Result Update

Key Ratios

Y/E December

CY2012

CY2013

CY2014E

CY2015E

CY2016E

Valuation Ratio (x)

P/E (on FDEPS)

23.4

14.0

13.0

9.2

10.1

P/CEPS

16.4

11.1

10.2

7.2

8.0

P/BV

3.7

3.1

2.7

2.2

1.8

Dividend yield (%)

1.2

1.6

1.7

1.7

1.7

EV/Sales

0.7

0.6

0.6

0.5

0.5

EV/EBITDA

11.9

7.2

6.2

3.9

4.0

EV / Total Assets

2.8

2.2

1.8

1.4

1.1

Per Share Data (`)

EPS (Basic)

24.5

40.8

43.9

62.2

56.6

EPS (fully diluted)

24.5

40.8

43.9

62.2

56.6

Cash EPS

35.0

51.7

56.3

79.1

71.8

DPS

7.0

9.0

10.0

10.0

10.0

Book Value

153.5

183.6

215.4

265.6

310.1

Dupont Analysis

EBIT margin

4.5

7.3

7.9

10.1

9.9

Tax retention ratio

0.7

0.7

0.7

0.7

0.7

Asset turnover (x)

14.5

13.1

11.9

10.2

7.7

ROIC (Post-tax)

43.4

63.2

62.4

67.4

50.0

Cost of Debt (Post Tax)

-

-

-

-

-

Leverage (x)

(0.7)

(0.7)

(0.7)

(0.7)

(0.7)

Operating ROE

14.2

16.0

16.6

20.6

13.4

Returns (%)

ROCE (Pre-tax)

18.3

27.0

25.1

31.9

23.5

Angel ROIC (Pre-tax)

65.1

95.4

94.6

102.1

75.8

ROE

16.9

24.2

22.0

25.9

19.7

Turnover ratios (x)

Asset Turnover

3.8

3.8

3.5

3.7

3.0

Inventory / Sales (days)

23

24

26

30

28

Receivables (days)

35

37

32

32

32

Payables (days)

118

124

126

126

126

WC (ex-cash) (days)

(27)

(24)

(26)

(20)

(15)

Solvency ratios (x)

Net debt to equity

(0.7)

(0.7)

(0.7)

(0.7)

(0.7)

Net debt to EBITDA

(2.6)

(2.3)

(2.4)

(1.9)

(2.6)

Interest Coverage

17.5

52.7

36.7

53.9

63.7

*reporting changed from CY to FY starting January 2015

November 6, 2015

13

Goodyear | 3QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitian Stock Exchange of India Limited. It is also registered as a Depository Participant

with CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private

Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration

number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for

accessing /dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial

interest/beneficial ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any

compensation / managed or co-managed public offering of securities of the company covered by Analyst during the past twelve

months. Angel/analyst has not served as an officer, director or employee of company covered by Analyst and has not been engaged in

market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Goodyear India

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

November 6, 2015

14