Initiating Coverage | Auto Ancillary

December 22, 2015

Gabriel India

BUY

CMP

`87

Shocks absorbed; smooth ride ahead

Target Price

`101

Gabriel India Ltd (Gabriel) is one of the leading manufacturers of ride control

Investment Period

12 Months

products viz shock absorbers, front forks and struts across automotive segments. It

commands a market share of 25% in both two-wheelers and passenger vehicles and

Stock Info

is the market leader in commercial vehicles segment with a 75% market share.

Sector

Auto Ancillary

Recovery in two-wheelers bodes well for Gabriel

Market Cap (` cr)

1,256

The two-wheeler industry, which contributes ~52% of Gabriel’s revenues, is

poised to recover (we expect 7% CAGR growth over next two years on account of

Net Debt (` cr)

2

acceleration in urban markets (60% of 2W demand) due to better economic

Beta

1.1

growth and further easing of interest rates. Also, the implementation of the

52 Week High / Low

107/72

Seventh Commission would result in ~23% pay hike for about 5mn central

Avg. Daily Volume

36,354

government employees & the expected subsequent hikes for

12 mn state

Face Value (`)

1

government employees would aid demand recovery. (Implementation of Sixth pay

commission in FY09 had contributed to 25% growth both in FY10 and FY11).

BSE Sensex

25,736

Gabriel to outpace 2W industry on market share gains by key clients

Nifty

7,834

Gabriel is likely to outpace the two-wheeler industry growth on back of market

Reuters Code

GABR.BO

share gains of its key clients viz Honda India, TVS Motors and Royal Enfield (which

Bloomberg Code

GABR@IN

form 75% of 2W revenues) due to expansion of their distribution reach, new

products and increased proportion of fast growing scooters. GIL is likely to

register 9-10% growth in 2W as against industry growth of 7%

Shareholding Pattern (%)

Healthy growth in PV and CV segment to boost revenues

Promoters

54.6

We expect PV segment (27% of revenues) to grow a healthy 8% due to better OEM

MF / Banks / Indian Fls

8.4

industry growth and entry into new platforms. CV OEM segment (9% of revenues)

FII / NRIs / OCBs

10.7

is expected to grow 15% over next two years due to higher freight availability.

Indian Public / Others

26.3

Aftermarket and export segments to be key growth drivers

Increased shift towards branded product and new product introduction coupled

with GIL strategy to initiate supplies to OEM’s overseas arms and taping

Abs. (%)

3m 1yr 3yr

aftermarket exports would result in 15% CAGR for both aftermarket and exports

over next two years.

Sensex

(1.7)

(6.0)

33.7

Outlook and valuation: Two-wheeler recovery coupled with market share gains,

Gabriel

1.5

(0.8)

220.9

healthy growth in passenger vehicle segment, increased focus on aftermarket and

exports are likely to lead to a 10% CAGR in revenue for Gabriel over FY2016-2018

3-Year Daily price chart

period. Gabriel’s margins are also expected to improve by 60bp in the next two years

120

on back of operating leverage and cost control measures, resulting into 17% earnings

100

CAGR over the next two years. GIL is a quality ancillary company with bright earnings

growth, healthy return ratios and attractive valuations. We initiate coverage on Gabriel

80

with Buy rating and target price of `101 (based on 16x FY2018E earnings).

60

Key financials

40

Y/E March (` cr)

FY2015

FY2016E

FY2017E

FY2018E

20

Net sales

1,444

1,415

1,544

1,715

0

% chg

12.2

(2.0)

9.1

11.1

Net profit (Adj.)

61

66

78

90

% chg

29.5

9.1

17.4

16.6

EBITDA margin (%)

8.1

8.7

9.0

9.3

Source: Company, Angel Research

EPS (`)

4.2

4.6

5.4

6.3

P/E (x)

20.6

18.9

16.1

13.8

P/BV (x)

3.8

3.4

3.0

2.7

RoE (%)

18.6

18.1

18.9

19.5

RoCE (%)

25.5

24.0

24.7

25.5

Bharat Gianani

EV/Sales (x)

0.9

0.9

0.8

0.7

022-39357800 Ext: 6817

EV/EBITDA (x)

10.7

9.8

8.4

7.2

Source: Company, Angel Research; CMP as of December 21, 2015

Please refer to important disclosures at the end of this report

1

Gabriel India | Initiating Coverage

Investment Arguments

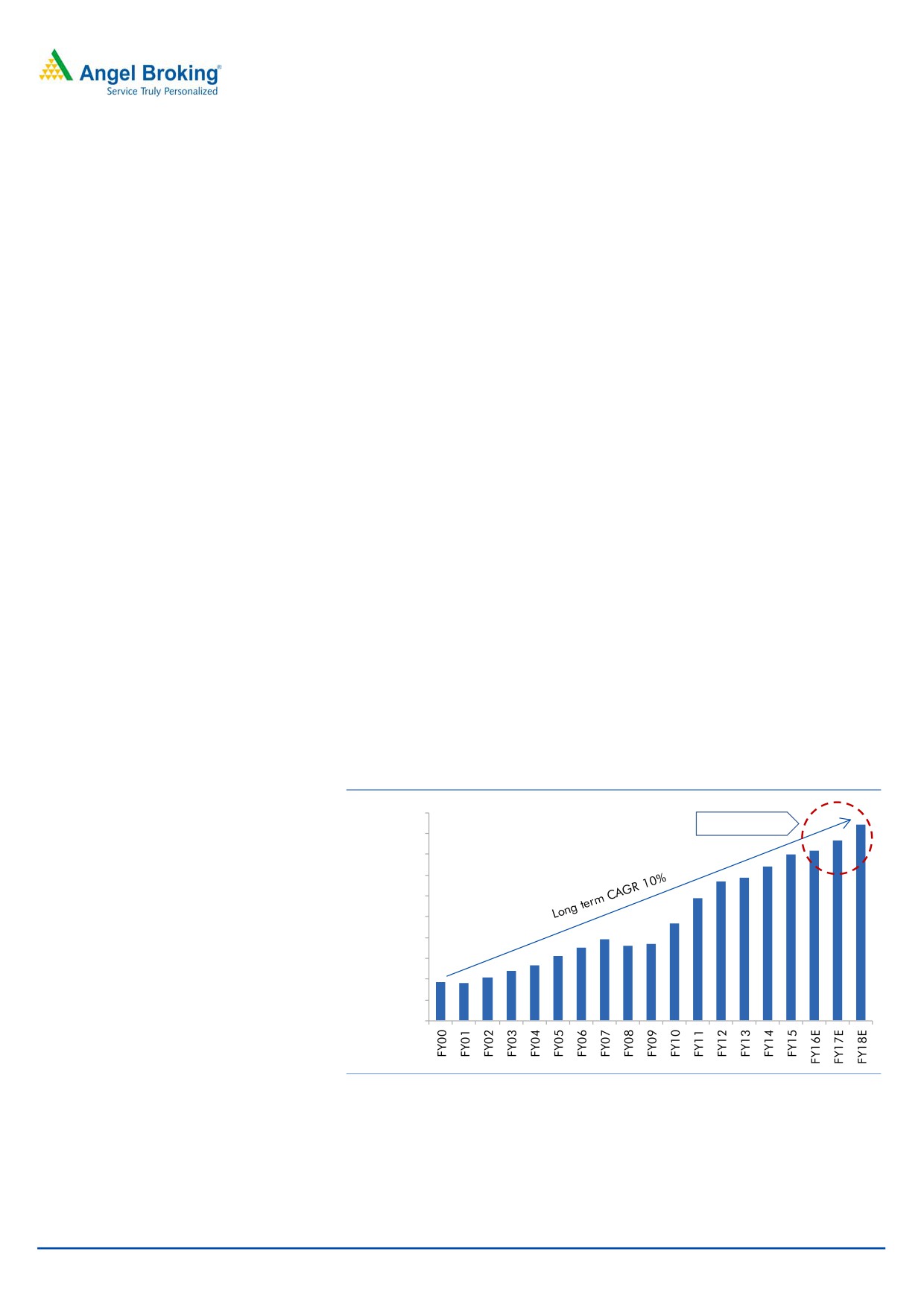

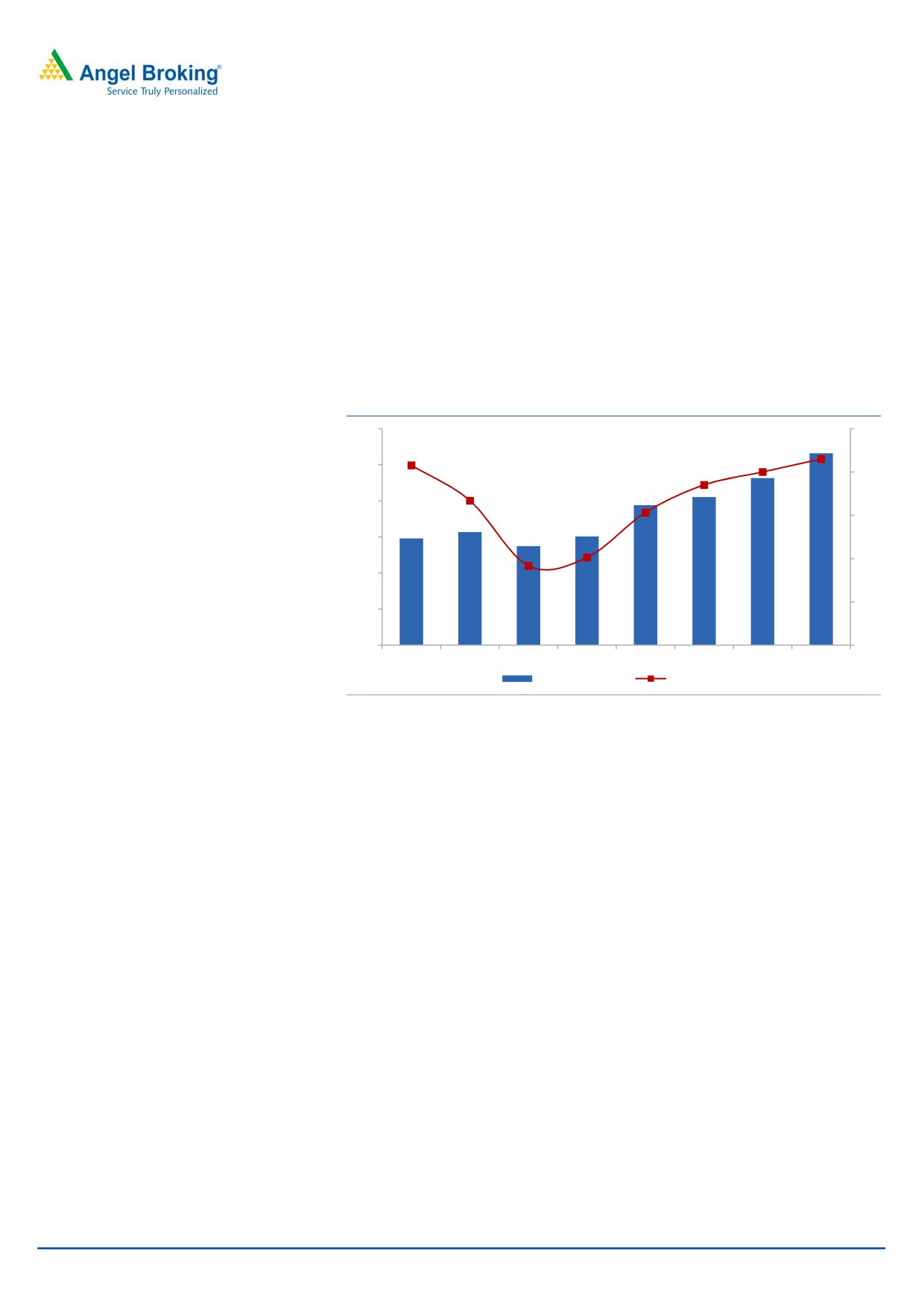

Two-wheeler volumes to recover in FY2017

The two-wheeler industry slowed down considerably in the last 4 quarters with the

segment reporting flattish volumes. (January 2015-November 2015) volumes grew

marginally by 1%. A decline in rural volumes on account of two consecutive years

of deficient rainfall led to sluggishness in two-wheeler sales. Rural sales account for

~40% of total two-wheeler volumes and are estimated to have dipped by 3% to

4% during January 2015-November 2015; while urban volumes are expected to

have grown by 4% to 5% during the same period.

We expect the two-wheeler industry to return to the growth trajectory in FY2017

and realign with its long term CAGR of ~10%. Acceleration in urban volumes on

account of better economic growth, resulting in higher incomes in the hands of

consumers, coupled with a further reduction in interest rates, are likely to boost

volumes. Further, the implementation of the Seventh Pay Commission

(recommending a 23% average salary hike) would result in higher incomes for

5mn government employees and this would act as an important catalyst for growth

in two-wheeler demand. Earlier in FY2009, when the Sixth Pay Commission had

declared a 35% salary hike, two-wheeler volumes resultantly witnessed buoyancy

in FY2010 and FY2011 (volumes grew by 25% in each year). Post the pay hike for

central government employees, various state governments (state govt employs

about 12 million) also raise salaries, which could further stoke demand. Also, a

gradual recovery in rural demand on expectations of a normal monsoon in

FY2017 and increase in Minimum Support Prices (MSPs) for agricultural output

would also aid recovery, going ahead. Gabriel, which draws 50% of its sales from

the 2WOEM segment, is likely to benefit from an expected recovery in the two-

wheeler segment.

Exhibit 1: Two-wheeler industry growth trend

20,000,000

Implied CAGR 7%

18,000,000

16,000,000

14,000,000

12,000,000

10,000,000

8,000,000

6,000,000

4,000,000

2,000,000

0

Source:SIAM, Angel Research

December 22, 2015

2

Gabriel India | Initiating Coverage

Increased sourcing and market share gains of key customers to

enable Gabriel outpace two-wheeler industry growth

Gabriel’s key customers TVS Motors, Honda Motorcycles and Scooters India (HMSI)

and Royal Enfield, which form about 75% of its two-wheeler segment sales and

38% of the overall revenues, are poised to outgrow the two wheeler industry and

gain market share. TVS Motors and HMSI are expected to gain market share on

the back of new product launches, widening of their distribution reach and higher

proportion of the fast growing scooters (scooter constitutes 60% and 35% of HMSI

and TVS two wheeler volumes respectively). Further, Royal Enfield is also expected

to outpace the industry with a rising trend of leisure biking, a segment where it is

the market leader. We expect Gabriel’s key customers to gain 100-150bp market

share over the next two years, thereby enabling it to outpace the two-wheeler

industry growth.

Further, Gabriel is likely to increase sourcing to HMSI. Post the split with the Hero

group, HMSI is looking to increasingly source supplies from non-Hero vendors

which puts Gabriel in a favorable position. Gabriel is expected to receive increased

orders from HMSI’s upcoming plant in Gujarat which is likely to commence

operations in 4QFY2016. Gabriel’s share of business from HMSI currently stands

at 35% and is expected to reach 40% levels over the next two years. The above

factors are likely to enable Gabriel to report 9-10% growth in the two-wheeler

segment in the next two years as against industry growth of about 7%.

Exhibit 2: Two wheeler market share of key customers

50%

45%

40%

35%

30%

FY13

FY14

FY15

FY16E

FY17E

FY18E

Source: SIAM, Angel Research

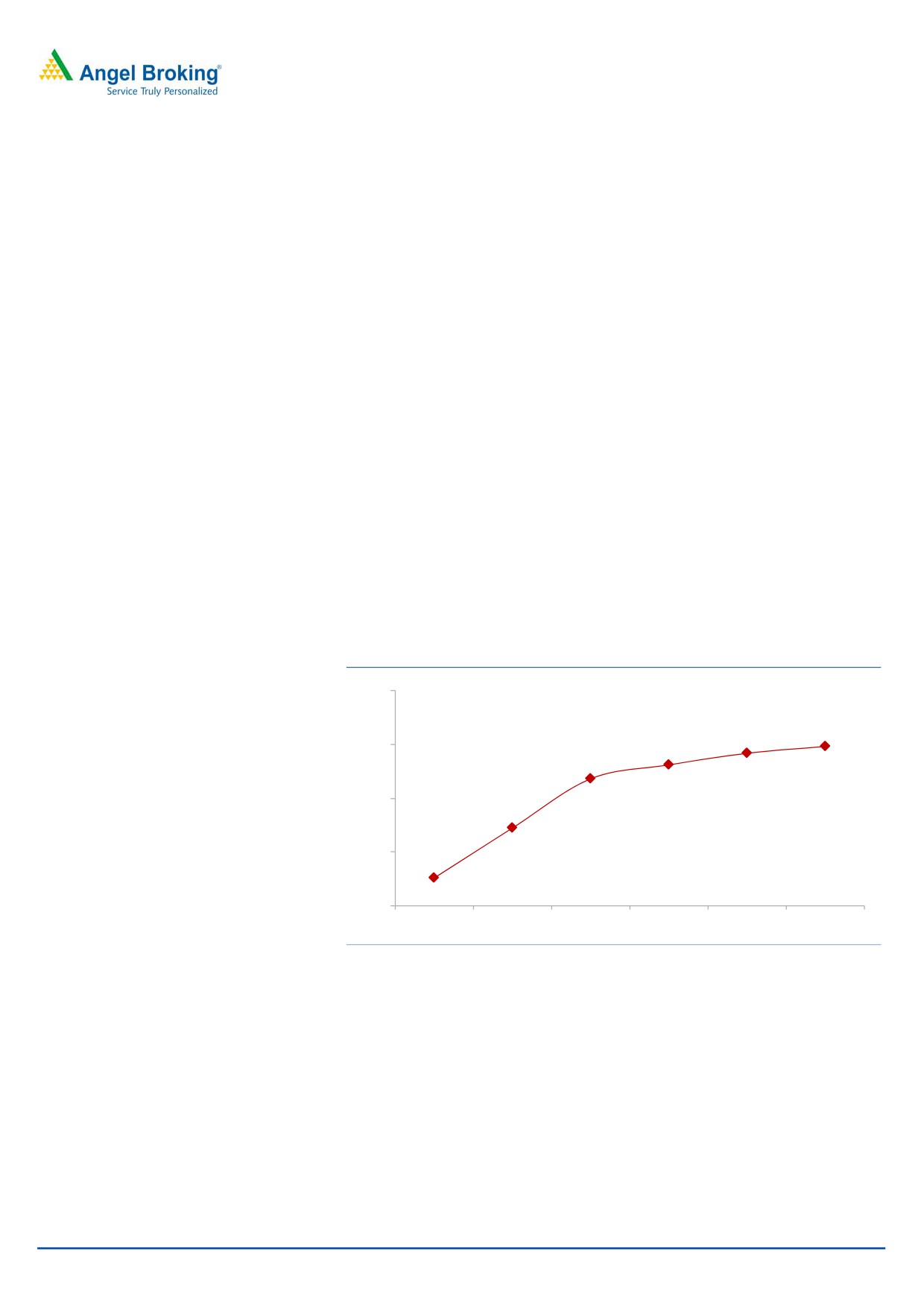

Aftermarket and export segment to be the key growth drivers

Gabriel is increasing focus on growing revenues in the aftermarket space. It has

been successful in leveraging its brand image and strong relationships with OEMs

to increase presence in the aftermarket segment. The company’s aftermarket

revenues have grown at a CAGR of 18% over the last five years and currently

account for 13% of the top-line. The company has recently launched suspension

allied products such as front row coils and bush kits which will augment its

revenues. Further, the company is also introducing new products, viz wheel rims

and coolants, which would further drive its sales in the aftermarket space. Also,

increasing preference for branded products is likely to lead to shift from the

December 22, 2015

3

Gabriel India | Initiating Coverage

unorganized segment (unorganized players accounts for about 30%-35% of the

overall market) thus benefitting players like Gabriel who already have a large

OEM base and strong recall. The company is expecting a healthy double-digit

growth in the aftermarket space and is aiming to increase aftermarket revenues

from 13% currently to 15% over the next two years.

Similarly, Gabriel is focusing on increasing its export revenues by tapping overseas

arms of the OEMs to whom it is currently supplying in India. The company has

received approval from SML Isuzu and the supplies would commence from

4QFY2016. The company is also tapping the aftermarket segment in the export

markets to drive growth. It is aiming to increase export revenues from the current

3% to about 10% over the next two to three years.

Exhibit 3: Aftermarket growth trend

Exhibit 4: Export growth trend

250

80

140

120

70

200

100

60

80

50

60

150

40

40

20

100

30

0

20

(20)

50

10

(40)

0

(60)

0

FY11

FY12

FY13

FY14

FY15

FY16E FY17E FY18E

FY10

FY11

FY12

FY13

FY14

FY15

FY16E FY17E FY18E

Exports (` cr)

Growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

Passenger vehicle business poised for recovery

Gabriel’s passenger vehicle segment (contributing 27% of the revenues) has been

under pressure with the segment’s revenues having declined by about 10% in

1HFY2016. This is on account of car platforms of Maruti Suzuki (mini segment)

and Tata Motors (older platforms) in which Gabriel is the supplier not performing

well. Underperformance of its key customer - Mahindra & Mahindra (M&M) (M&M

volumes dipped 8% in 1HFY2016 as against passenger vehicle industry growth of

6%), has also led to decline in the company’s passenger vehicle segment revenues.

However, Gabriel has been nominated in new platforms of Maruti (S Cross and an

upcoming LCV) and M&M (K1OO compact SUV), which would enable recovery in

the passenger vehicle business from FY2017, in our view. Also, Gabriel is in

negotiations with Ford, Renault, and General Motors to increase supplies. We

believe Gabriel’s passenger vehicle segment would grow at a CAGR of 8% over

FY2017-18, which would be broadly in line with the passenger vehicle industry

growth.

December 22, 2015

4

Gabriel India | Initiating Coverage

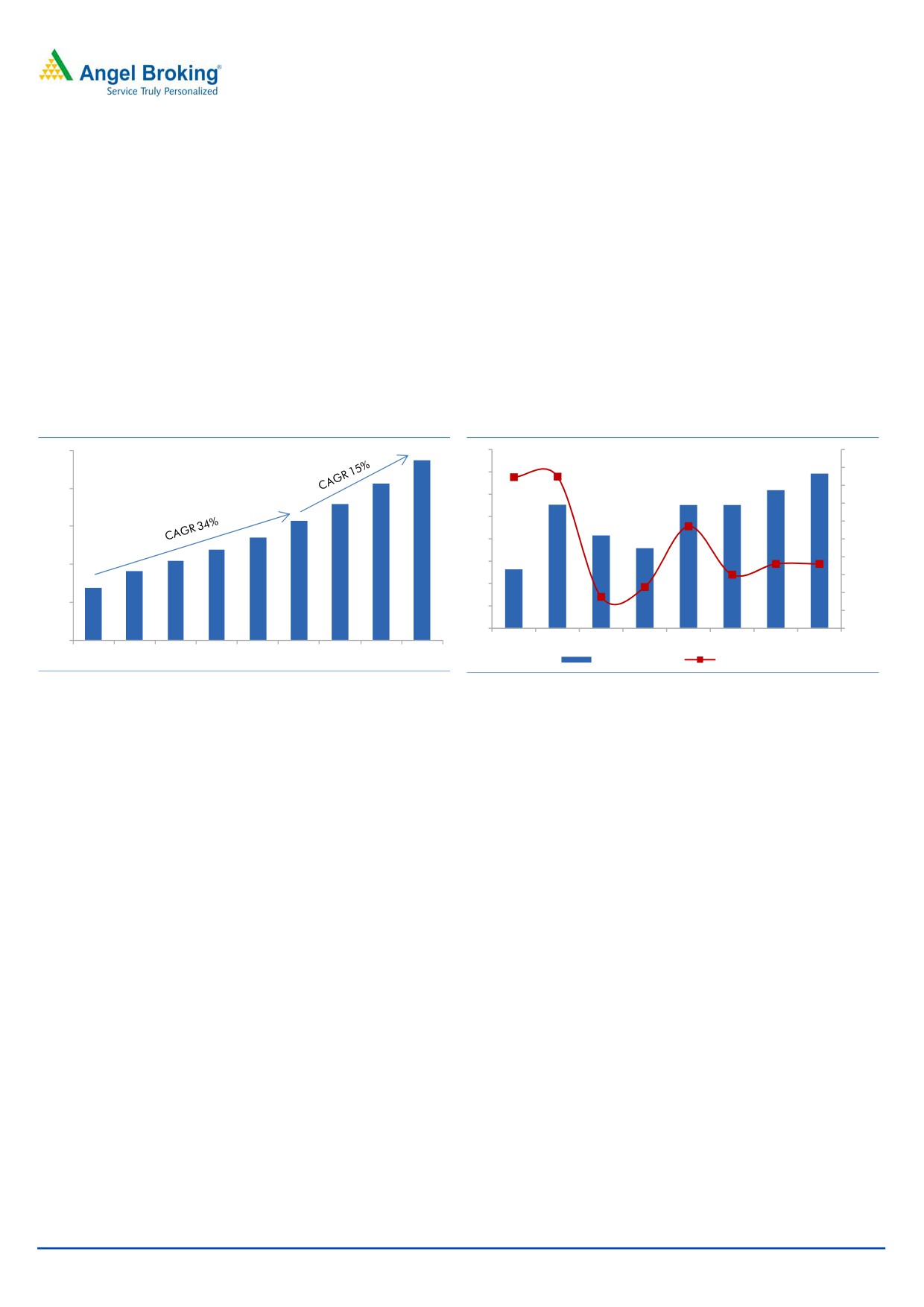

Operating leverage coupled with raw material savings to

improve margins

Gabriel’s top-line is estimated to post a CAGR of ~10% over FY2017-18. The

company is poised to gain benefits of operating leverage on back of healthy

top-line growth. Further, Gabriel has embarked upon a programme on reducing

raw material expenses where it is focusing on value engineering to bring down the

raw material costs. Also, Gabriel is contemplating to procure from new vendors to

draw better raw material prices. Softness in raw material prices is expected to

continue benefitting the company. We estimate Gabriel’s margins to improve by

60bp over the next two years.

Exhibit 5: EBIDTA margin trend

180

10

150

9

120

8

90

7

60

6

30

0

5

FY11

FY12

FY13

FY14

FY15

FY16E

FY17E

FY18E

EBIDTA (` cr)

Margin (%)

Source: Company, Angel Research

December 22, 2015

5

Gabriel India | Initiating Coverage

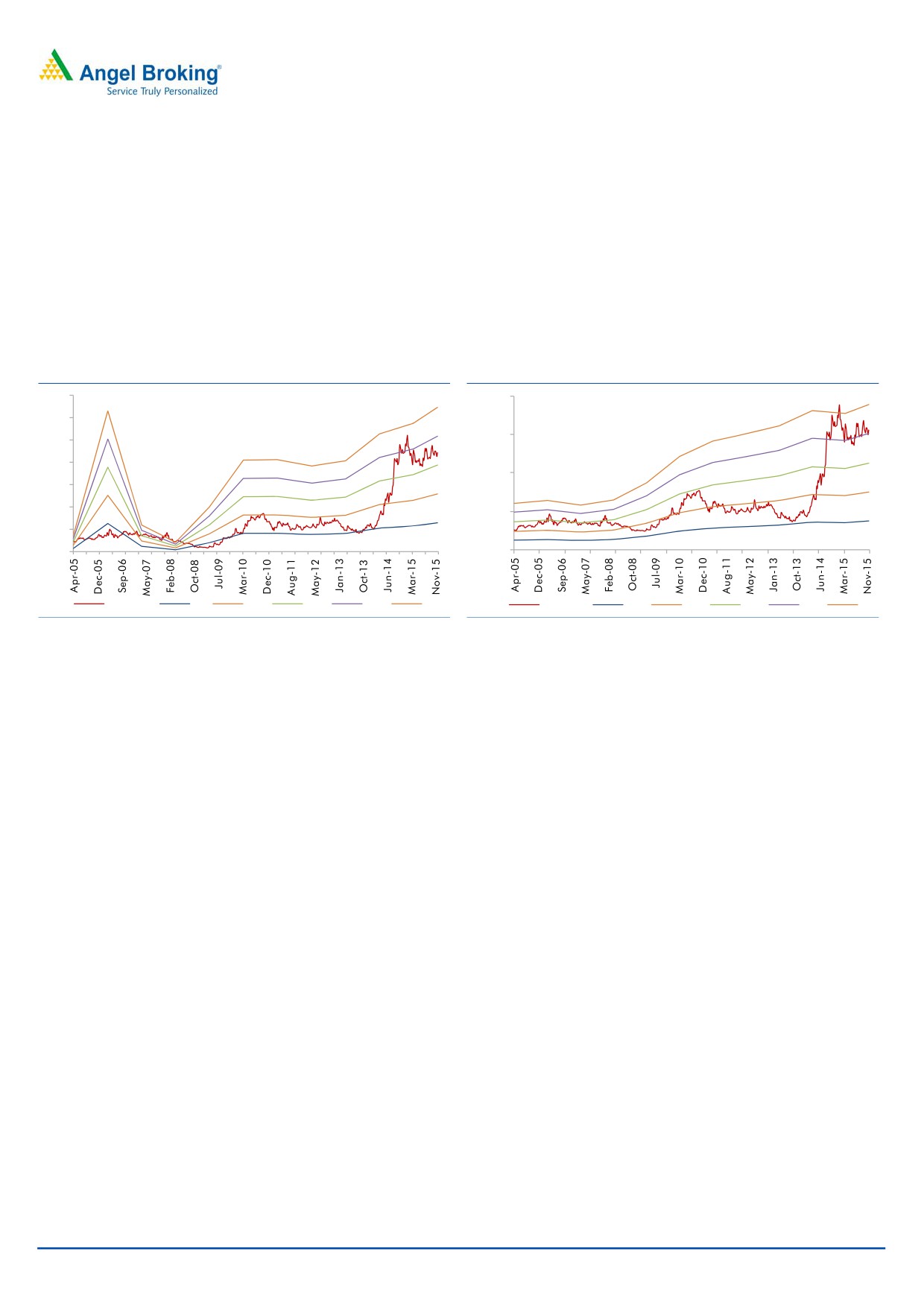

Outlook and Valuation

Two-wheeler recovery coupled with market share gains, healthy growth in

passenger vehicle segment, increased focus on aftermarket and exports are likely

to lead to a 10% CAGR in revenue for Gabriel over FY2016-2018 period. Gabriel’s

margins are also expected to improve by 60bp in the next two years on back of

operating leverage and cost control measures, resulting into 17% earnings CAGR over

the next two years. GIL is a quality ancillary company with bright earnings growth,

healthy return ratios and attractive valuations. We initiate coverage on Gabriel with Buy

rating and target price of `101 (based on 16x FY2018E earnings).

Exhibit 6: One year forward P/E Band

Exhibit 7: One year forward EV/Sales Band

140

1,600

120

1,200

100

80

800

60

40

400

20

0

0

Price (`)

5x

10x

15x

20x

25x

EV (` cr)

0.2x

0.4x

0.6x

0.8x

1x

Source: Angel Research

Source: Angel Research

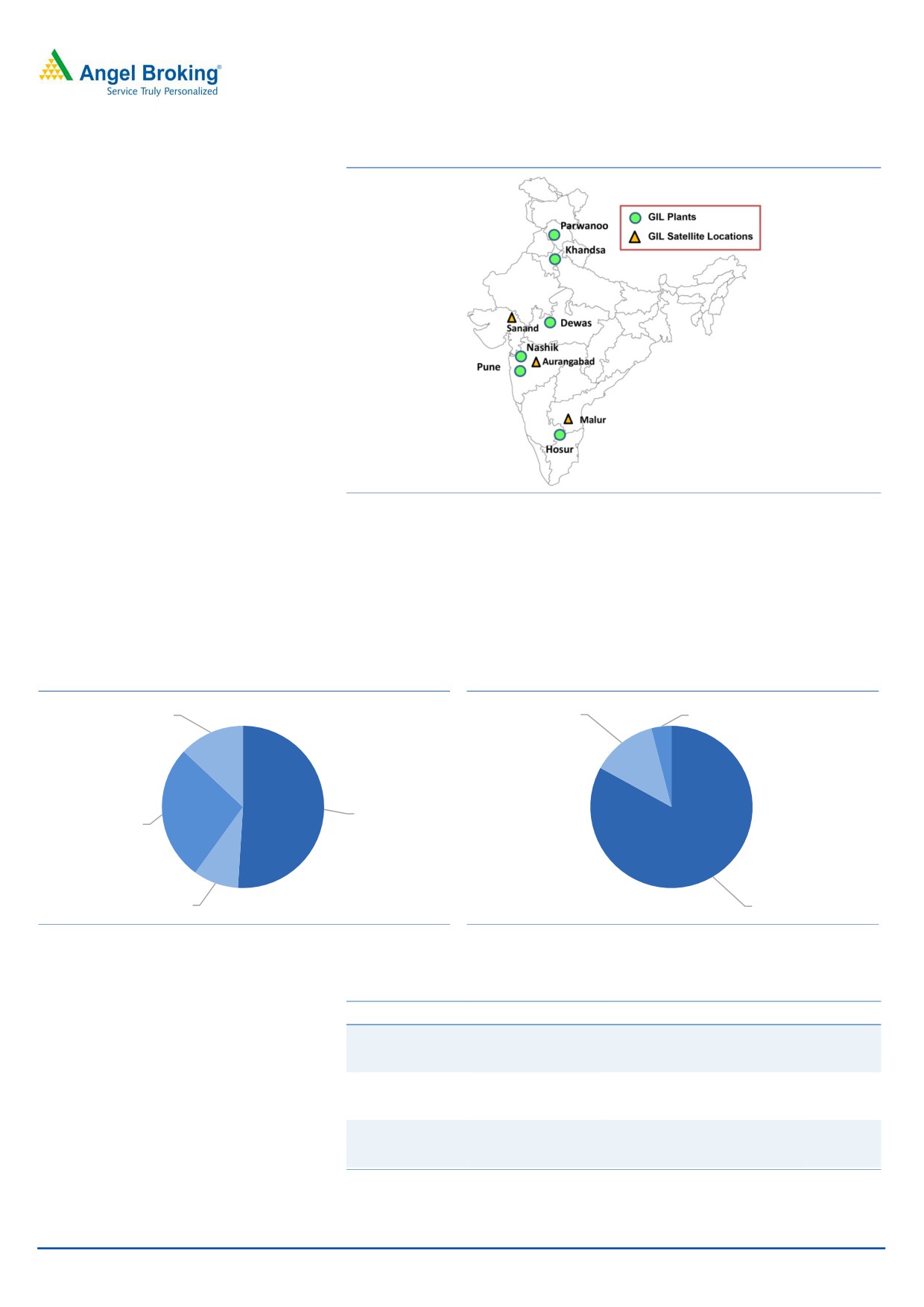

Company Background

Gabriel India Limited (GIL) is the flagship company of ANAND group and a

leading name in the Indian Auto Component Industry. Established in 1961, GIL

has been the pioneer of ride control products in India. GIL provides the widest

range of ride control products including shock absorbers, struts and front forks,

across every automotive segment with over 300 product models on offer. GIL has

wide manufacturing presence with facilities spread across the country located at

Pune, Nashik, Hosur, Dewas, Gurgaon, Parwanoo. It has technological

collaboration with KYB Corporation of Japan. KYB is the world leader in supplier

of shocks and struts for OEMs and the aftermarket. The company has 32 facilities

in 21 countries including 15 manufacturing plants in Asia, the United States, and

Europe.

December 22, 2015

6

Gabriel India | Initiating Coverage

Exhibit 8: Manufacturing footprint

Source: Company, Angel Research

Two-wheelers form the biggest chunk of the company’s revenues, contributing half

of the top-line. Passenger vehicles is the second largest segment constituting 27%

of the revenues. Commercial Vehicles and the three-wheeler segment form 13%

and 9% of revenues, respectively. OEMs form the largest customer base forming

83% of the top-line. Aftermarket and exports constitute 13% and 4%, respectively.

Exhibit 9: Segmentwise breakup

Exhibit 10: Customerwise breakup

CV, 13%

Aftermarket,

Exports, 4%

13%

2W, 51%

Cars, 27%

3W, 9%

OEM, 83%

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 11: Product and client base

Segment

Products

Customers

Market share

Front forks, gas and

TVS Motors, Honda India,

Two wheelers

hydraulic shock

Yamaha India, Bajaj Auto,

25%

absorber

Royal Enfield

Maruti Suzuki, M&M, Toyota

Mc Pherson struts,

Passenger vehicles

India, Hyundai, Volkswagen

25%

gas shock absorber

India, Ford India

Shock absorber,

Tata Motors, Ashok Leyland,

Commercial vehicles

cabin and seat

VECV, Bharat Benz,

75%

dampers

Force Motors

Source: Company, Angel Research

December 22, 2015

7

Gabriel India | Initiating Coverage

Profit & Loss Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

FY2018E

Total operating income

1,205

1,287

1,444

1,415

1,544

1,715

% chg

6.8

6.7

12.2

(2.0)

9.1

11.1

Total Expenditure

1,123

1,196

1,328

1,292

1,405

1,556

Net Raw Materials

875

928

1,043

1,016

1,106

1,226

Personnel

91

94

108

105

114

127

Other

157

175

177

171

185

202

EBITDA

82

90

116

123

139

160

% chg

(12.5)

9.8

28.8

5.7

12.9

14.8

(% of Net Sales)

6.8

7.0

8.1

8.7

9.0

9.3

Depreciation & Amortisation

27

27

31

33

36

39

EBIT

59

69

90

94

108

126

% chg

(19.6)

16.3

30.0

4.7

14.9

16.6

(% of Net Sales)

4.9

5.4

6.2

6.6

7.0

7.3

Interest & other Charges

12

9

5

2

0

0

Other Income

4

6

4

4

5

5

PBT (recurring)

47

60

84

92

108

126

% chg

(16.9)

27.2

40.3

9.1

17.4

16.6

Extraordinary Expense/(Inc.)

(6)

(4)

(1)

0

0

0

PBT (reported)

41

56

84

92

108

126

Tax

3

13

24

26

30

35

(% of PBT)

7.4

23.6

28.2

28.0

28.0

28.0

PAT (reported)

38

43

60

66

78

90

ADJ. PAT

44

47

61

66

78

90

% chg

(6.9)

6.2

29.5

9.1

17.4

16.6

(% of Net Sales)

3.7

3.6

4.2

4.7

5.0

5.3

Basic EPS (`)

2.7

3.0

4.2

4.6

5.4

6.3

Fully Diluted EPS (`)

3.1

3.3

4.2

4.6

5.4

6.3

% chg

(6.9)

6.2

29.5

9.1

17.4

16.6

December 22, 2015

8

Gabriel India | Initiating Coverage

Balance sheet statement

Y/E March (` cr)

FY2013 FY2014 FY2015 FY2016E FY2017E FY2018E

SOURCES OF FUNDS

Equity Share Capital

14

14

14

14

14

14

Reserves& Surplus

242

271

311

350

396

449

Shareholders Funds

257

285

325

364

410

464

Total Loans

66

56

6

4

0

0

Deferred Tax Liability

11

10

10

10

10

10

Other long term liab.

4

0

0

0

0

0

Long term provisions

6

4

9

12

15

18

Total Liabilities

343

355

351

391

436

492

APPLICATION OF FUNDS

Gross Block

459

492

524

555

594

647

Less: Acc. Dep.

204

225

257

290

325

364

Net Block

255

267

268

265

268

283

Capital WIP

6

12

3

0

0

0

Investments

0

0

0

0

0

0

Long Loans and adv.

31

23

23

23

25

27

Current Assets

Cash

7

5

4

44

76

105

Other

252

278

317

314

343

381

Current liabilities

209

231

265

259

282

312

Net Current Assets

44

47

51

55

61

69

Total Assets

343

355

351

391

436

492

December 22, 2015

9

Gabriel India | Initiating Coverage

Cash flow statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E FY2018E

Profit before tax

41

56

84

92

108

126

Depreciation

25

21

32

33

36

39

Change in Working Capital

35

(4)

(4)

(4)

(6)

(8)

Others

4

(7)

4

1

1

1

Direct taxes paid

(3)

(13)

(24)

(26)

(30)

(35)

Cash Flow from Operations

102

53

92

97

108

123

(Inc.)/ Dec. in Fixed Assets

(69)

(39)

(23)

(28)

(39)

(53)

(Inc.)/ Dec. in Investments

0

0

0

0

0

0

(Inc.)/ Dec. in Loans & Adv

7

7

1

(0)

(2)

(3)

Cash Flow from Investing

(63)

(31)

(22)

(28)

(41)

(56)

Issue of Equity

7

0

0

0

0

0

Inc./(Dec.) in loans

(25)

(9)

(51)

(2)

(4)

0

Dividend Paid (Incl. Tax)

(11)

(12)

(18)

(27)

(32)

(37)

Others

(9)

(2)

(2)

0

0

0

Cash Flow from Financing

(38)

(24)

(70)

(29)

(36)

(37)

Inc./(Dec.) in Cash

1

(2)

(1)

40

32

29

Opening Cash balances

6

7

5

4

44

76

Closing Cash balances

7

5

4

44

76

105

December 22, 2015

10

Gabriel India | Initiating Coverage

Key ratios

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

28.4

26.7

20.6

18.9

16.1

13.8

P/CEPS

28.4

26.7

20.6

18.9

16.1

13.8

P/BV

4.9

4.4

3.8

3.4

3.0

2.7

Dividend yield (%)

0.9

1.0

1.4

2.2

2.5

3.0

EV/Sales

1.1

1.0

0.9

0.9

0.8

0.7

EV/EBITDA

15.9

14.4

10.7

9.8

8.4

7.2

EV / Total Assets

3.8

3.7

3.6

3.1

2.7

2.3

Per Share Data (`)

EPS (Basic)

3.1

3.3

4.2

4.6

5.4

6.3

EPS (fully diluted)

3.1

3.3

4.2

4.6

5.4

6.3

Cash EPS

5.0

5.1

6.4

6.9

7.9

9.0

DPS

0.7

0.9

1.2

1.9

2.2

2.6

Book Value

17.9

19.9

22.7

25.4

28.6

32.3

Returns (%)

ROCE (Pre-tax)

17.3

19.4

25.5

24.0

24.7

25.5

Angel ROIC (Pre-tax)

17.7

19.7

25.8

27.0

29.9

32.5

ROE

17.2

16.4

18.6

18.1

18.9

19.5

Turnover ratios (x)

Asset Turnover (Gross Block)

2.6

2.6

2.8

2.6

2.6

2.7

Inventory / Sales (days)

33.7

33.1

28.3

29.0

29.0

29.0

Receivables (days)

35.4

38.6

43.6

44.0

44.0

44.0

Payables (days)

63.3

65.5

67.1

66.8

66.6

66.4

WC cycle (ex-cash) (days)

13.2

13.4

13.0

14.2

14.4

14.6

Solvency ratios (x)

Net debt to equity

0.2

0.2

0.0

(0.1)

(0.2)

(0.2)

Net debt to EBITDA

0.7

0.6

0.0

(0.3)

(0.5)

(0.7)

Interest Coverage (EBIT / Int.)

4.9

7.7

16.4

46.9

NA

NA

December 22, 2015

11

Gabriel India | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Gabriel India

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

December 22, 2015

12