1

Please refer to important disclosures at the end of this report

1

1

The Promoter of Equitas Small Finance Bank (ESFB) i.e. Equitas Holdings Limited

(EHL) was granted the RBI Final Approval on June 30, 2016, to establish a Small

Finance Bank (SFB). Subsequently, the Bank was converted to a SFB and it

commenced operations on September 05, 2016. Unlike other microfinance

companies, it has a diversified loan portfolio and less dependence on

microfinance business. The main focus of ESFB is on financially unserved and

underserved customers.

Positives : (1) The bank is well capitalized (CAR – 23.6% & CET 1 – 22.4% as on

Q1FY21, (2) Bank has diversified portfolio ( SME- 42%, Vehicle - 24%, MFI- 24%,

Housing – 4% and remaining others, (3) It has highest number of outlets

compared to all SFBs. (4) ESFB has the best CASA ratio among SFB (ESFB –

20.5%, Ujjivan SFB – 12% & AUSFB -14.5%.

Concerns: (1) ESFB for FY20 reported RoA/RoE of 1.4%/9.8%, which we believe is

lower; whereas listed players Ujjivan SFB reported RoA/RoE of 2.2%/14%, AU SFB

reported RoA/RoE of 1.6%/15.6%, (2) Asset quality ratio is weak compared to

listed peers. For FY20, GNPA of ESFB was 2.7%, for Ujjivan and AUSFB it was 1%

and 1.7%, respectively, (3) ESFBs provision coverage ratio is at 48% vs. That of

listed peers at >65%, (4) 36.2% of the loan book is under moratorium as on

August 31, 2020, which would increase possibility of jump in GNPA and will

impact return ratios adversly.

Market outlook and valuation: At the upper end of the price band, Equitas SFB

demands Adj. PB of 1.26x post considering fresh issue. Though the bank has

diversified loan book and best CASA ratio among SFBs, the return ratios are

subdued with GNPA above 2.5% for last 3 years. Our concern for Equitas SFB is

fresh formation of bad loans from moratorium book that would keep provisions

high and return ratios compressed. We believe invesors should wait for price

discovery before making any investment decision. Considering above factors, we

recommend NEUTRAL rating for the IPO.

Key Financials

Y/E March (` cr)

FY17

FY18

FY19

FY20

NII

521

858

1,147

1,489

% chg

65

34

30

Net profit

104

32

211

244

% chg

(69)

561

16

NIM (%)

6.2

8.2

8.4

9.0

EPS (`)

1.0

0.3

2.1

2.3

P/E (x)

32

104

16

14

P/ABV (x)

1.7

1.7

1.5

1.3

RoA (%)

1.1

0.3

1.4

1.4

RoE (%)

5.2

1.6

9.8

9.7

Source: Valaution done on upper price band.

NEUTRAL

Issue Open: Oct 20, 2020

Issue Close: Oct 22, 2020

Offer for sale: `238cr

QIBs 50% of issue

Non-Institutional 15% of issue

Retail 35% of issue

Promoters 82.0%

Others 18.0%

Fresh issue: `280cr

Issue D etails

Face Value: `10

Present Eq. Paid up Capital: ` 1053cr

Post Issu e Shareh o ldin g Pa ttern

Post Eq. Paid up Capital: `1,138cr

Issue size (amount): **`518cr

Price Band: `32-33

Lot Size: 450 shares and in multiple

thereafter

Post-issue implied mkt. cap: *`3,651cr

- **`3,756cr

Promoters holding Pre-Issue: 95%

Promoters holding Post-Issue: 82%

*Calculated on lower price band

** Calculated on upper price band

Book B uilding

EQUITAS SMALL FINANCE BANK LIMITED

IPO Note | BFSI

Oct 19, 2020

2

Oct

19,

Equitas Small Finance Bank Limited | IPO Note

Oct 19, 2020

2

Compnay Details

ESFB was originally incorporated as ‘V.A.P. Finance Private Limited’ on June 21,

1993. The Bank’s Promoter, Equitas Holdings Limited (EHL) was granted the RBI

Final Approval on June 30, 2016, to establish an SFB. Subsequently, the Bank was

converted to SFB and it commenced operations on September 05, 2016 as a SFB.

Before converting into SFB, Equitas used to give small loans in joint lending group,

similar to Spandana and Credit Access.

EHL to hold 82% stake in ESFB post listing.

Average ticket size of entire loan book is Rs0.4mn; 96% of market in this ticket size

is unorganized and indicates huge untapped potential.

As on June 30, 2020, it had 856 branches and 322 ATMs across 17 states and

UTs. It does not have a presence in East India and at present plans to leverage on

existing presence in South, West and North India.

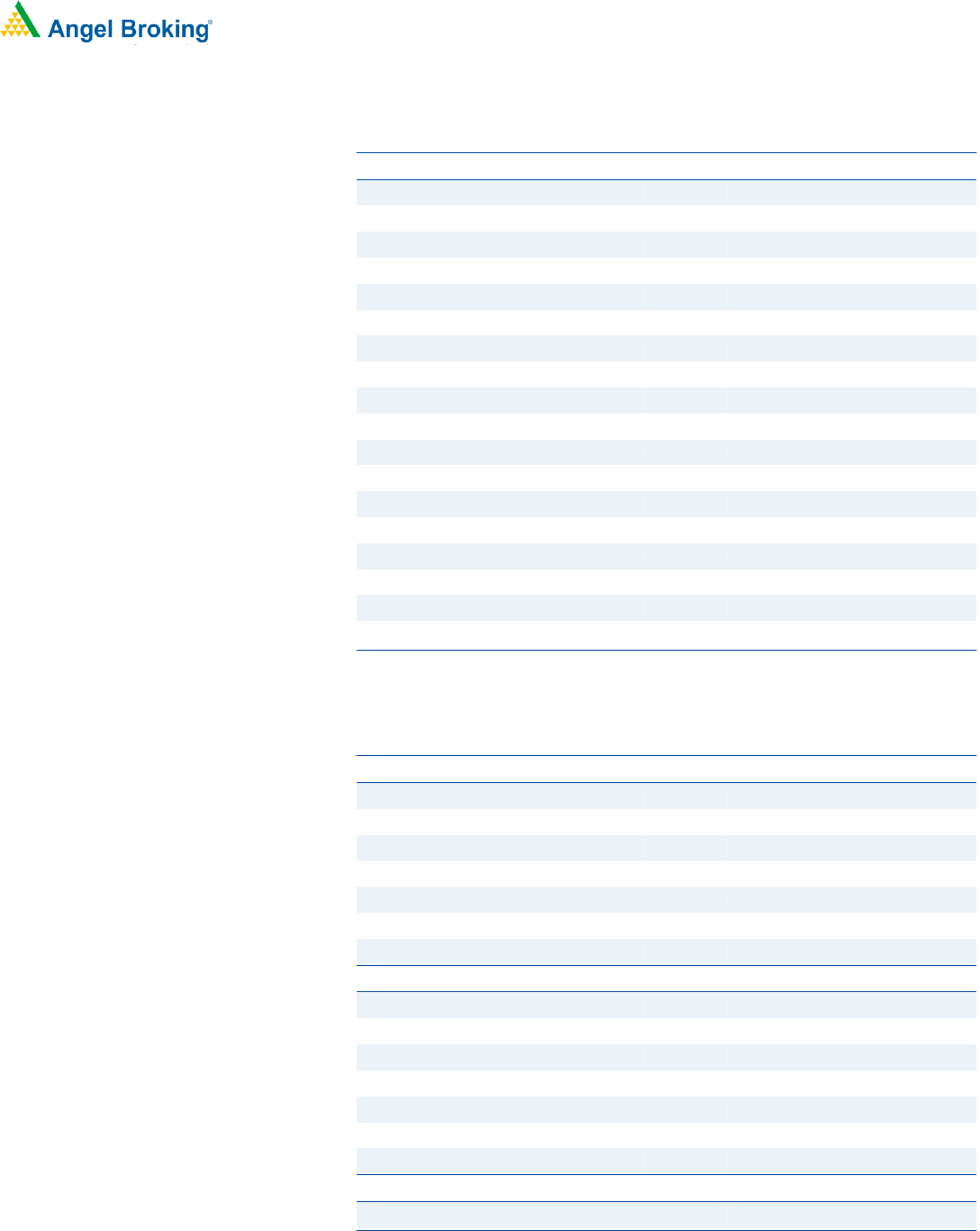

Exhibit 1: Listed peers portfolio diversification (%) FY20

SFB / Peers

MFI

HFC

Vehicle

SME

Retail

Other

Outlet

Equitas SFB

23

4

24

42

7

604

Ujjivan SFB

76

11

7

6

575

AU SFB

2.3

42

38

2.7

15

467

Spandana Sphoorthy

100

Credit Access Gramin

100

Bandhan Bank

51

21

7

21

1018

Source: Company

Key Management Personnel:

Vasudevan Pathangi Narasimhan is the MD and CEO of the Bank. He has

extensive experience in the financial services sector and had served as the

executive vice president and head of consumer banking group in Development

Credit Bank Ltd, for more than one and half years. He has also worked for about

2 decades in Cholamandalam Investment and Finance Co. Ltd., part of the

Murugappa Group.

Sridharan Nanuiyer is the CFO of the Bank. He joined erstwhile Equitas Holding,

now the Bank on August 16, 2010.

Sampathkumar K. Raghunathan is the Company Secretary and Compliance

Officer of the Bank. Prior to joining the Bank, he worked at Hinduja Leyland

Finance Ltd.

3

Oct

19,

Equitas Small Finance Bank Limited | IPO Note

Oct 19, 2020

3

Issue details

This IPO is a mix of OFS and issue of fresh shares. The issue would constitute fresh

issue worth `280cr and OFS worth of `238cr. OFS is primarily to meet regulatory

(RBI) requirements. Small Finance Banks, with a net worth of more than `500cr,

were mandated by the RBI to list within three years of launching operations.

In this IPO, there is a reservation kept for employees and share holders of Equitas

Holdings worth `1cr and `51cr respectively. (Eligible EHL Shareholders: Individuals

and HUFs who are the public equity shareholders of Equitas Holdings & the

Promoter, as on the date of the Red Herring Prospectus i.e. October 11, 2020.

Exhibit 2: Pre and Post shareholding pattern

Particualr

No of shares (Pre-issue)

%

No of shares (Post-issue)

%

Promoter

1,00,59,43,363

95

93,39,43,363

82

Public

4,74,58,239

5

20,43,06,724

18

Total

1,05,34,01,602

100

1,13,82,50,087

100

Source: RHP Note, Calculated on upper price band

Objects of the offer

Ensuring adequate capital to support growth and expansion, including

enhancing the Bank’s solvency and capital adequacy rati.

Meet regulatory requirement of listing.

Risk

Improvement in asset quality and deposits in mid-term would be key risk to

our NEUTRAL call.

4

Oct

19,

Equitas Small Finance Bank Limited | IPO Note

Oct 19, 2020

4

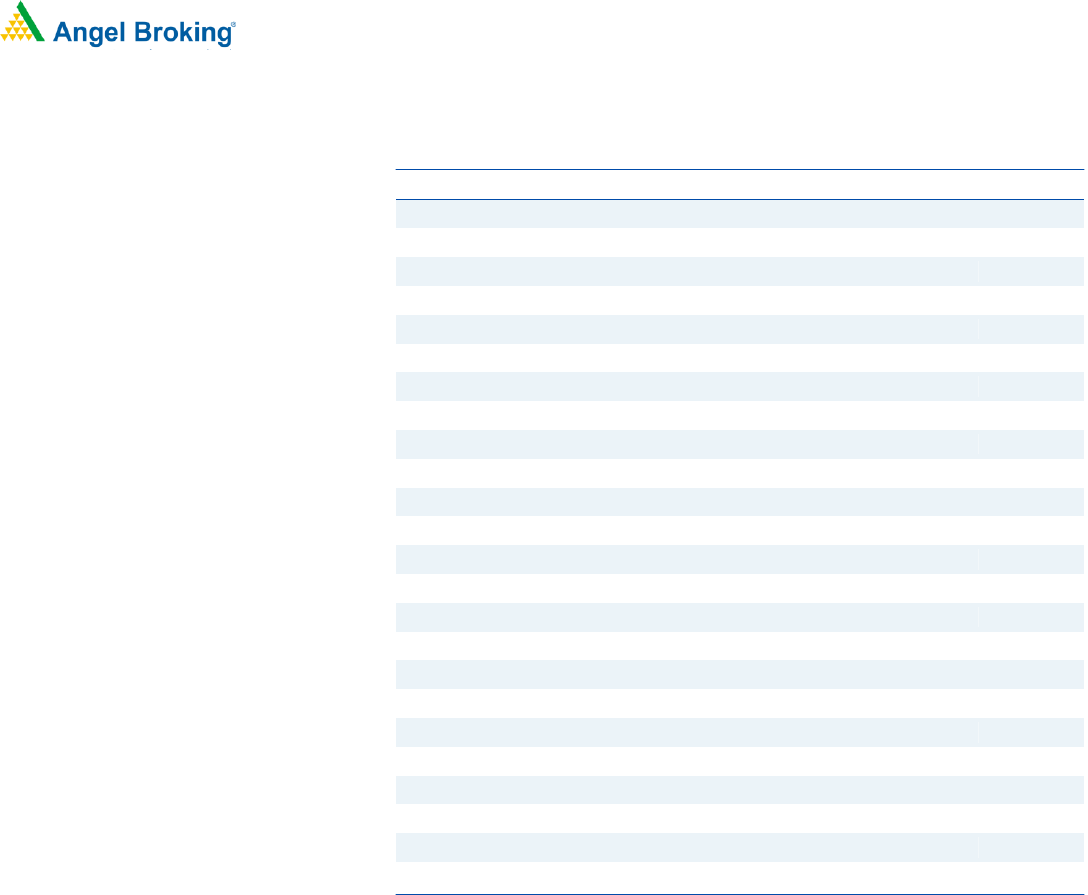

Exhibit 3: Relative valuation and operating metrics

Particular (`cr)

AUM

CASA

(%)

NIM

(%)

GNPAs

(%)

NNPAs

(%)

Cost/

Asset

PCR

(%)

CARR

(%)

Market

Cap

P/BV

(X)

P/E

(X)

ROA

(%)

ROE

(%)

Equitas SFB

15,600

21.0

8.6

2.7

1.4

5.7

48

21.6

3,756

1.26

15.4

1.4

9.7

Ujjivan SFB

14,366

12.0

12.2

1.0

0.2

5.8

80

29.0

5,331

1.75

15.2

2.2

14.0

AU SFB

30,036

14.5

5.0

1.7

0.6

2.7

65

21.7

22,377

4.91

37.2

1.6

15.6

Spandana S

6,800

15.5

0.6

0.1

3.6

81

53.0

3,505

1.30

10.4

6.7

15.0

CreditAccess

9,680

12.6

1.6

- .0

3.4

100

23.7

10,368

3.54

31.6

2.4

13.1

Bandhan Bank

74,300

37.1

8.2

1.4

0.5

2.6

66

23.7

50,379

3.21

16.7

4.1

22.9

Source: Equitas SFB valuation done on upper band of IPO, and other Co. valuation taken as on CMP of 17/10/2; P/BV done on Q1FY21 Networth; For

Equitas Fresh issue added in Networth calculation, PE on FY20 EPS

Exhibit 4: Listed peers Dupont compared with Equitas SFB

SFB

Ujjivan

AU

Bandhan

Equitas

Particular

FY19

FY20

FY19

FY20

FY19

FY20

FY19

FY20

Interest earned

15.8

16.8

11.5

11.5

13.2

14.7

14.5

15.1

Interest expended

6.2

6.7

6.2

6.4

4.3

6.2

6.6

6.6

Net Interest Income

9.5

10.2

5.2

5.1

8.9

8.5

7.9

8.5

Other income

1.8

2.0

1.8

1.7

2.1

2.1

1.9

1.6

Total income

11.3

12.2

7.0

6.8

11.0

10.6

9.8

10.1

Operating expenses

8.6

8.2

4.2

3.8

3.6

3.3

6.9

6.7

Empolyee Exp

4.5

4.5

2.3

2.0

2.0

1.8

3.8

4.0

Other Exp

4.2

3.7

1.9

1.8

1.6

1.4

3.1

2.6

PPOP

2.7

4.0

2.8

3.0

7.4

7.4

2.9

3.4

provisions

0.4

1.1

0.6

0.8

1.5

1.9

0.7

1.4

PBT

2.3

2.9

2.3

2.2

6.0

5.5

2.2

2.0

Exceptional items

- .0

- .0

- .0

0.2

- .0

- .0

- .0

- .0

Tax items

0.6

0.7

0.8

0.6

2.1

1.4

0.8

0.6

RoA

1.7

2.2

1.5

1.6

3.9

4.1

1.4

1.4

Leverage

6.7

6.4

9.5

9.9

4.9

5.6

6.8

7.0

RoE

11.5

14.0

14.0

15.6

19.0

22.9

9.8

9.7

5

Oct

19,

Equitas Small Finance Bank Limited | IPO Note

Oct 19, 2020

5

Income Statement

Y/E March (` cr)

FY17

FY18

FY19

FY20

Q1FY21

Net Interest Income

521

858

1,147

1,489

404

- YoY Growth (%)

65

34

30

Other Income

233

241

283

282

30

- YoY Growth (%)

3

17

(0)

Operating Income

754

1,100

1,430

1,772

434

- YoY Growth (%)

46

30

24

Operating Expenses

497

879

1,004

1,174

292

- YoY Growth (%)

77

14

17

Pre - Provision Profit

258

221

426

598

142

- YoY Growth (%)

(14)

93

40

Prov. & Cont.

96

172

102

247

68

- YoY Growth (%)

78

(41)

141

Profit Before Tax

161

49

324

351

74

- YoY Growth (%)

(70)

567

8

Prov. for Taxation

57

17

113

107

16

- as a % of PBT

36

34

35

31

22

PAT

104

32

211

244

58

- YoY Growth (%)

(69)

561

16

Balance Sheet

Y/E March (` cr)

FY17

FY18

FY19

FY20

Q1FY21

Equity

1,006

1,006

1,006

1,053

1,053

Reserve & Surplus

1,006

1,038

1,248

1,691

1,748

Networth

2,012

2,044

2,254

2,744

2,802

Deposits

1,921

5,604

9,007

10,788

11,787

- Growth (%)

192

61

20

Borrowings

4,779

5,177

3,973

5,135

5,526

Other Liab. & Prov.

533

488

531

650

778

Total Liabilities

9,245

13,313

15,765

19,317

20,892

Cash Balances

248

386

403

381

429

Bank Balances

866

825

858

2,156

1,497

Investments

1,891

3,857

2,344

2,343

3,479

Advances

5,702

7,707

11,595

13,747

14,389

- Growth (%)

35

50

19

Fixed Assets

288

281

237

213

198

Other Assets

251

258

327

478

902

Total Assets

9,245

13,313

15,765

19,317

20,892

- Growth (%)

44

18

23

6

Oct

19,

Equitas Small Finance Bank Limited | IPO Note

Oct 19, 2020

6

Key Ratio

Y/E March

FY17

FY18

FY19

FY20

Profitability ratios (%)

NIMs

6.2

8.2

8.4

9.0

Cost to Income Ratio

66

80

70

66

RoA

1.1

0.3

1.4

1.4

RoE

5.2

1.6

9.8

9.7

B/S ratios (%)

CASA Ratio

29.2

25.3

20.5

Credit/Deposit Ratio

3.0

1.4

1.3

1.3

CAR

35.5

29.6

22.4

23.6

Tier I

32.3

27.1

20.9

22.4

Asset Quality (%)

Gross NPAs

3.3

2.7

2.5

2.7

Net NPAs

1.5

1.7

1.6

1.8

Slippages

-

4.5

2.7

3.0

Loan Loss Prov. /Avg. Assets

1.0

1.5

0.7

1.4

Provision Coverage

54

37

36

33

Per Share Data (`)

EPS

1.0

0.3

2.1

2.3

BVPS

20.0

20.3

22.4

26.1

ABVPS (70% cover.)

19.6

19.6

21.4

24.9

DPS

Valuation Ratios

PER (x)

32

104

16

14

P/ABVPS (x)

1.7

1.7

1.5

1.3

Valaution done at upper price band of the IPO

7

Oct

19,

Equitas Small Finance Bank Limited | IPO Note

Oct 19, 2020

7

Research Team Tel: 022 - 39357800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National

Commodity & Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and

Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered

entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164.

Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities

Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of securities of

the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information..