Initiating coverage | Auto Ancillary

October 16, 2017

Endurance Technologies Ltd

BUY

CMP

`1,111

A Healthy Upward Ride

Target Price

`1,277

Endurance Technologies is an Aurangabad based Auto Ancillary Company. It has

Investment Period

12 Months

18 manufacturing plants in India and 8 in Europe. The company’s domestic

business is diversified, new clients have been added and diversification into newer

Stock Info

products continues. Hence, the dependence on the legacy casting business has

Sector

Auto Ancillary

come down to 44% from more than 50% a few years ago. In Europe, Endurance

Market Cap (` cr)

15,621

is a 4W aluminum casting supplier and is moving in complex products. Company

Net Debt (` cr)

474

derives 2/3rd revenue from India and the rest from Europe.

Beta

0.8

Diversified business with improving business mix: While Bajaj Auto was a big

52 Week High / Low

1024 / 518

revenue driver for Endurance (>50% by FY2010), in the last few years company

Avg. Daily Volume

38,418

has added new clients and has expanded in Europe. This has reduced its client

Face Value (`)

10

concentration and with HMCL and HMSI increasing their revenue pie with

Endurance, the business mix is likely to see a rapid change in the next few years.

BSE Sensex

32,433

Nifty

10,167

Growing proprietary business to enhance margins: Endurance is increasing its

Reuters Code

ENDU.NS

content with the OEMs, especially in scooters such as CVT and front forks. This is

Bloomberg Code

ENDU.IN

a fairly large opportunity, as scooters have continued to grow rapidly compared

to motorcycles. We believe that overall increase in the proprietary sales will

increase its EBITDA margins by ~150bps by FY2020E.

Shareholding Pattern (%)

Cash rich business leading to debt free balance sheet by FY2020E: With the lower

Promoters

82.5

capex requirement, Endurance is likely to generate `1,074cr FCF over the next

MF / Banks / Indian Fls

4.7

three years v/s. >`1,268cr between FY2012-17. This is expected to make

FII / NRIs / OCBs

9.1

Endurance an almost debt free company by FY2020E.

Indian Public / Others

3.7

Outlook and valuation: Shares of Endurance have seen a strong appreciation

since its lasting last year. At the CMP of `1,095, the stock is trading at the PE of

26x of its FY2020E EPS. We forecast top-line and bottom-line CAGR of 14.3%

Abs. (%)

3m 6M e Listing

and

21.3% respectively over the next three years. We also forecast

Sensex

1.2

10.1

15.9

~150bps/200bps jump in its EBITDA margins and ROE respectively. With the

Endurance Tech.

23.6

33.7

71.5

strong FCF generation, we believe that Endurance will become almost debt free in

the next three years. We value Endurance Technologies at 29.0x of its FY2020E

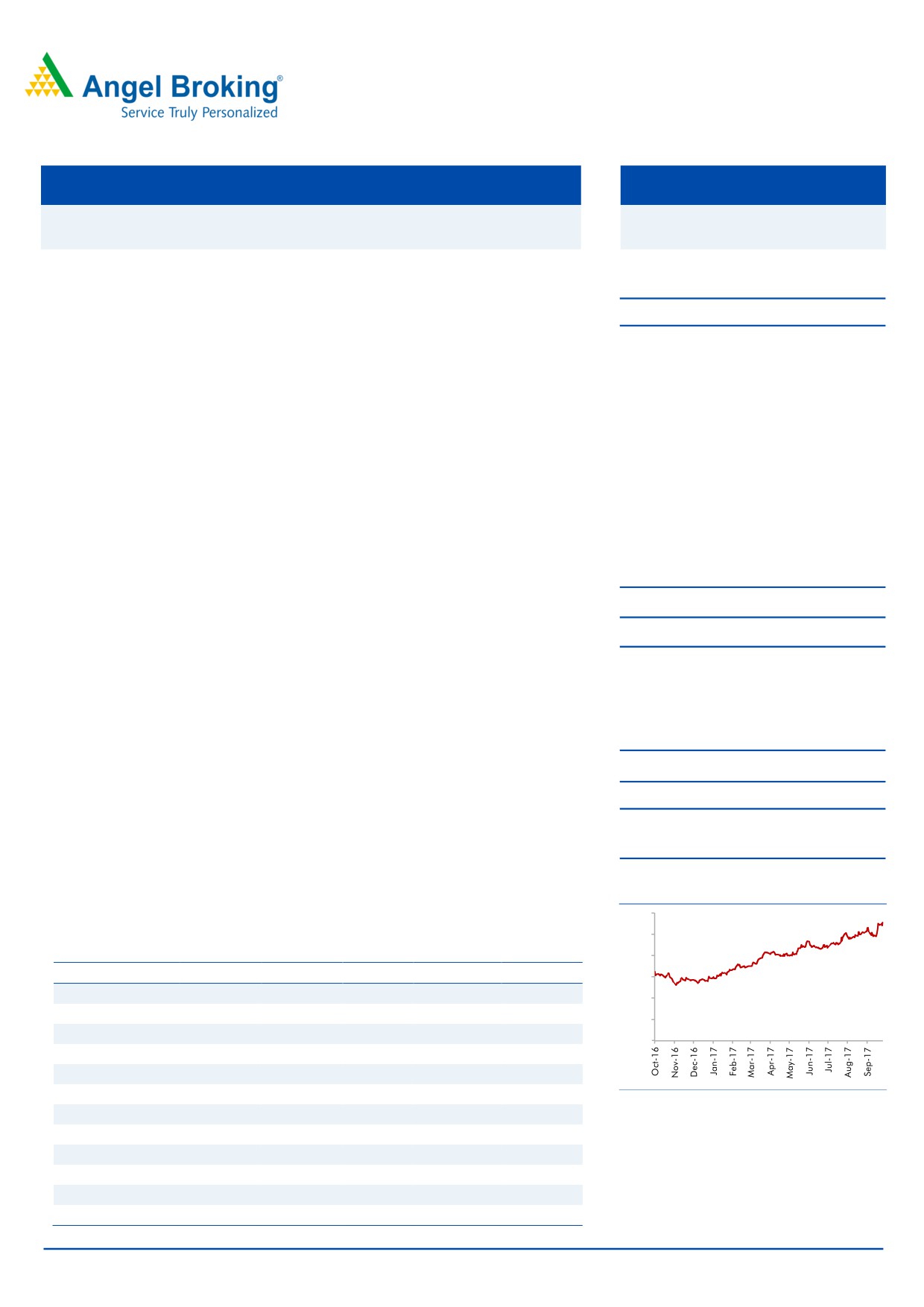

Price Chart

EPS of `42.8 to derive the core business price target of `1,242 and add `35, NPV

1,200

of ABS opportunity to derive the target price of `1,277, implying 15% upside.

1,000

Key Financials (Consolidated)

800

Y/E March (` cr)

FY16

FY17

FY18E

FY19E

FY20E

600

Net Sales

5,230

5,588

6,665

7,479

8,351

400

% chg

6.4

6.8

19.3

12.2

11.7

200

Net Profit

299

328

456

529

603

0

% chg

18.6

9.5

39.1

15.9

13.9

OPM (%)

13.0

13.5

14.1

14.6

15.0

EPS (`)

21.3

23.3

32.4

37.6

42.8

Source: Company, Angel Research

P/E (x)

52.2

47.6

34.2

29.5

25.9

P/BV (x)

10.8

9.0

7.4

6.3

5.5

RoE (%)

23.1

20.6

23.8

23.1

22.8

RoCE (%)

19.1

19.2

22.7

23.2

23.6

Shrikant Akolkar

EV/Sales (x)

3.1

2.9

2.4

2.1

1.9

022 - 3935 7800 Ext: 6846

EV/EBITDA (x)

24.0

21.3

17.0

14.4

12.4

Source: Company, Angel Research; Note: as CMP of Oct 13, 2017

Please refer to important disclosures at the end of this report

1

Initiating coverage | Endurance Technologies

Endurance at a glance

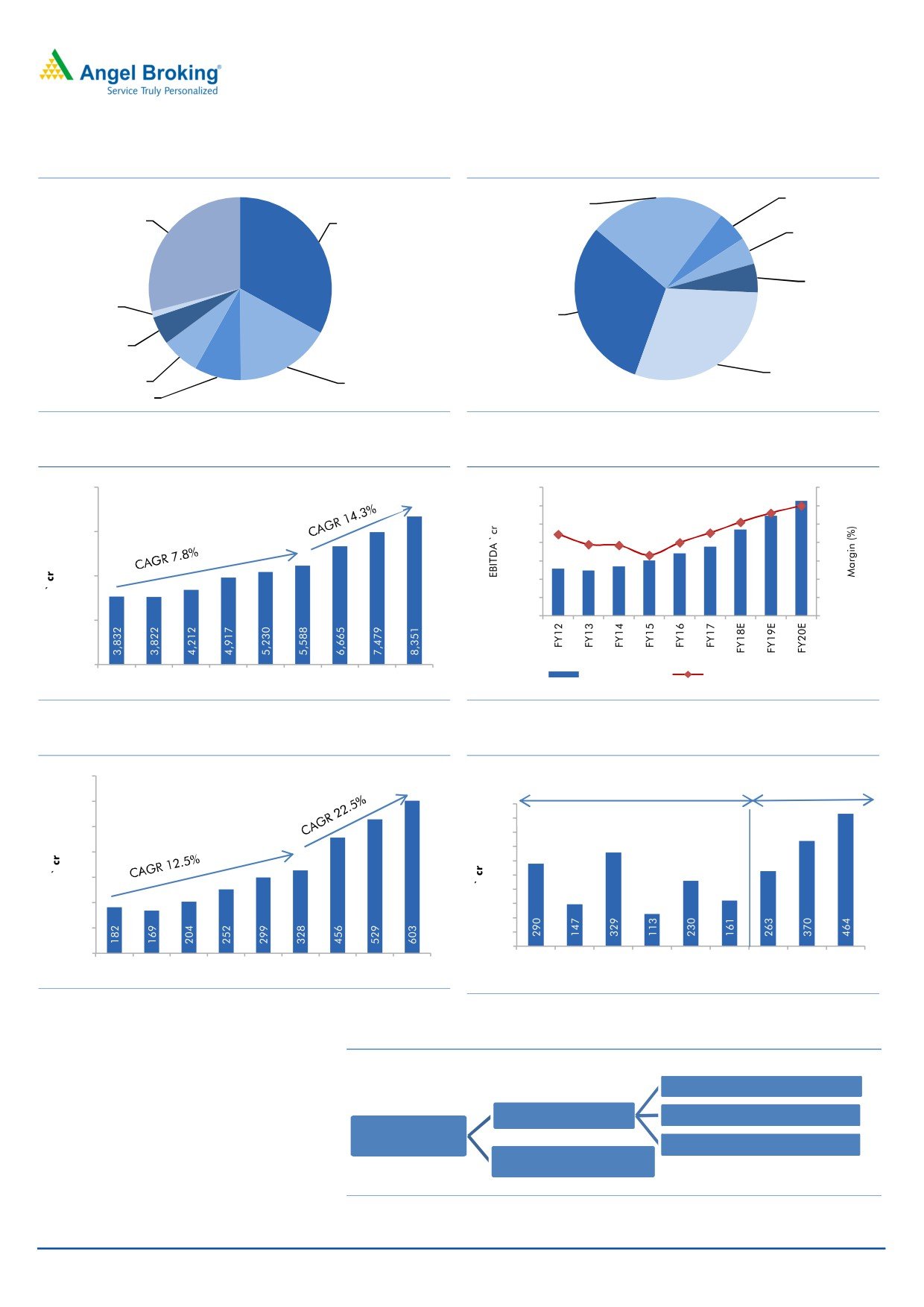

Exhibit 1: Client mix

Exhibit 2: Diversified Business mix

Transmission,

Suspension,

6%

24%

Others, 29%

Bajaj Auto,

Brake Systems,

33%

5%

Aftermarket

and others, 5%

Domestic

HMCL, 1%

casting, 31%

Daimler, 5%

Eurpoean

business, 30%

Royal Enfield,

Fiat Chrysler,

7%

17%

HMSI, 8%

Source: Company, Angel Research, *Consolidated

Source: Company, Angel Research, *Consolidated

Exhibit 3: 14% revenue CAGR over next three years

Exhibit 4: EBITDA margins continue to improve

10,000

1,400

15.0

16

14.6

1,200

14.1

15

13.4

13.5

1,000

13.0

14

7,500

12.9

12.8

800

12.3

13

600

12

5,000

400

11

200

10

0

9

2,500

0

EBITDA (` cr)

EBITDA margins (%)

FY12

FY13

FY14

FY15

FY16

FY17

FY18E FY19E FY20E

Source: Company, Angel Research, *Consolidated

Source: Company, Angel Research, *Consolidated

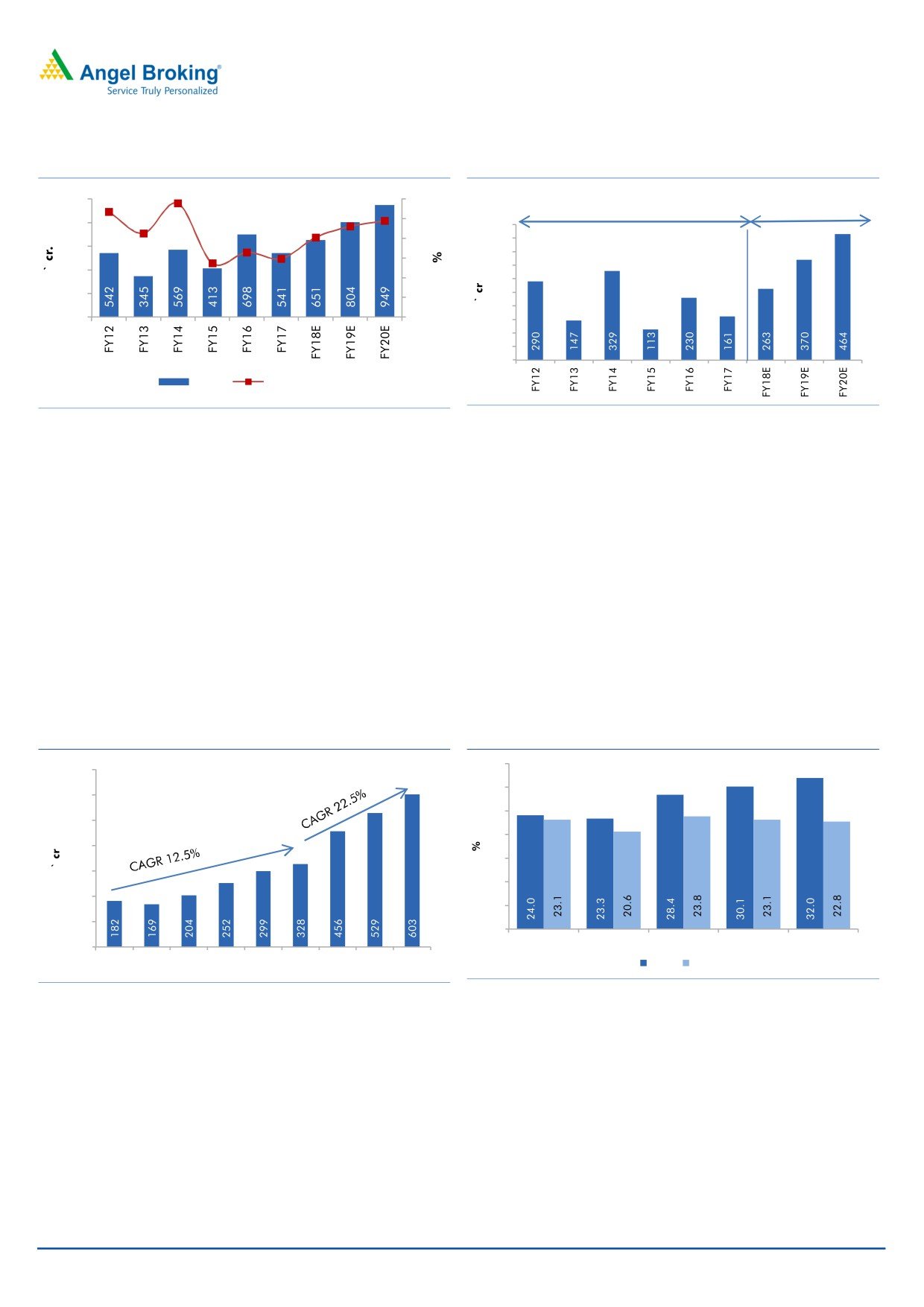

Exhibit 5: 22.5% PAT CAGR over next three years

Exhibit 6: Strong free cash flow generation

700

FY18E-FY20E

FY12-FY17

600

500

`1,268cr

``1,098cr

450

500

400

350

400

300

300

250

200

200

150

100

100

50

0

0

FY12

FY13

FY14

FY15

FY16

FY17

FY18E FY19E FY20E

FY12

FY13

FY14

FY15

FY16

FY17

FY18E FY19E FY20E

Source: Company, Angel Research, *Consolidated

Source: Company, Angel Research, *Consolidated

Exhibit 7: Endurance group structure

Endurance Fondalmec SpA

Endurance Overseas Srl

Endurance FOA SpA

Endurance

Technologies

Endurance Engineering Srl

Endurance Amann GmbH

Source: Company, Angel Research

October 16, 2017

2

Initiating coverage | Endurance Technologies

About company

Endurance Technologies is an Aurangabad based multi-product Auto Ancillary

Company having total 26 strategically located manufacturing plants of which 18

are in India and 8 plants are in Europe. Company derives 70% revenue from India

and the rest 30% from Europe. Company is also developing an automotive

proving ground (test track) on 26 acre land in Aurangabad. This is expected to be

operational in the current fiscal and will help Endurance to develop and launch

new products.

Its domestic business is comprised of Aluminum castings, suspension, transmission,

braking and aftermarket. Aluminum casting is the largest segment which

contributes 44% of domestic revenues while rest is contributed by suspension

(34%), transmission (8%), Braking (7%) and aftermarket and others (7). The

domestic business is mostly a 2W business. In the domestic market, over past

several years, company has diversified in different products (other than castings),

which has seen dependence on the legacy casting business coming down to 44%

from more than 50% a few years ago.

Exhibit 8: Endurance Technologies - business segments products and customers

Business segment

Sub segment

Products

Customers

High pressure aluminum

Bajaj, Honda, Hero, Tata Motors and

Crank cases cylinder blocks and covers

castings

Royal Enfield

Aluminum Casting

Crown handles (Yamaha)

and Machining

Low pressure AL castings

Several

Cylinder heads (Bajaj Auto and Royal

Enfield)

Aluminum alloy wheels

Yamaha and Bajaj Auto

High-pressure die-casting

FCA Italy SpA, Daimler and other

Components for engines, transmission, vehicle body

products (Euro VI standards)

European 4W OEMs

Aluminum Casting

Transmission system

Pistons, gearbox housing, transmissions housing and

and Machining

Fiat, Lancia and Jeep

components

torque convertor housing

(Europe)

Steel, cast iron and

Suspension parts such as steel wheel hubs, head axles Several

engineering plastic parts

Twin/ Mono tube Hydraulic, Oil and gas-filled shock

Bajaj, Honda, Royal Enfield, Hero,

Shock absorbers

absorbers, Mono shock absorbers, Spring-in-spring

Yamaha, Harley-Davidson.

Suspension

and spring-on-spring hydraulic shock absorbers

Bajaj CT100, Bajaj Pulsar, Avenger

Front forks

Cartridge variety and Inverted forks

and Royal Enfield

Bajaj and Piaggio Ape (3W) and

Clutch assemblies

Bajaj Quadricycles.

CVTs

Hero MotoCorp, Mahindra

Transmission

2W - Bajaj Auto, Royal Enfield

Friction plates

3W, Bajaj Auto, Piaggio

Bajaj Quadricycles

Hydraulic disc brake assemblies

Bajaj Auto, Royal Enfield

Rotary brake discs assemblies

Bajaj Auto, Royal Enfield Yamaha

Brake Systems

Hydraulic drum brake assemblies

Bajaj Auto (3W)

Tandem master cylinder assemblies

Bajaj Auto (3W)

Source: Company, Angel Research

Company primarily was a supplier to Bajaj Auto, however it has successfully added

new customers like Hero MotoCorp, Honda Motorcycles and Scooters, Royal

Enfield, Yamaha, etc. This has led to the reduction in the dependence on Bajaj

Auto from 58% in FY2010 to 33% in FY2017.

October 16, 2017

3

Initiating coverage | Endurance Technologies

In Europe, Endurance is a 4W aluminum casting supplier. The European 4W

casting business contributes ~30% to the consolidated revenues of the company.

It has customers like FCA Italy SpA, Daimler, Jeep, etc.

Exhibit 9: European subsidiaries

Subsidiary

Nature of operations

Facility

Manufacturing of high pressure die casting and

Endurance Amann GmbH

Massenbachhausen, Germany

machined components

SPV incorporated for making strategic overseas

Endurance Overseas SrL

Turin, Italy

investments

Production of machining components such as

engine, gearbox, transmission groups, machining

Endurance Fondalmec SpA

Turin, Italy

and assembling of components of aluminum alloys,

cast iron and steel

Manufacturing of high pressure die casting and

Endurance Foa SpA

Turin, Italy

machined components

Production of engineering plastic

Endurance Engineering SrL

Turin, Italy

components for automotive applications

Source: Company, Angel Research.

Key Management Personnel

Mr. Anurang Jain - Founder and Managing Director

Mr. Jain promoted Endurance in 1985. He is responsible for the overall operations

of the company. He holds an MBA from the University of Pittsburgh.

Mr. Naresh Chandra - Chairman and Non-Executive Director

Mr Chandra has been with Endurance since inception and became the Chairman

in 1999. He has over 33 years of experience in the automobile industry.

Mr. Ramesh Gehaney - Executive Director and COO

Mr. Gehaney has been with the company since 2004 and he is responsible for the

company’s manufacturing operations. He holds Diploma in Mechanical

Engineering from University of Delhi. Before becoming COO, he had worked

across multiple departments in Endurance Technologies.

Mr. Satrajit Ray - Chief Financial Officer

Mr. Ray has been with Endurance since 2010. He is an associate member of ICAI

and has an experience of over 32 years. He has previously worked with the Indian

Aluminum Company Ltd (Indal), Hindalco Industries Ltd and MIRC Electronics Ltd.

Massimo Venuti - CEO- Endurance Overseas

Mr. Venuti has been the CEO of Endurance Overseas SRL since June 2008 and he

looks after Endurance’s European operations. He has over 22 years of experience

in the automotive industry and holds a Degree in Philosophy and Letters from the

University of Urbino.

October 16, 2017

4

Initiating coverage | Endurance Technologies

Investment Rationale

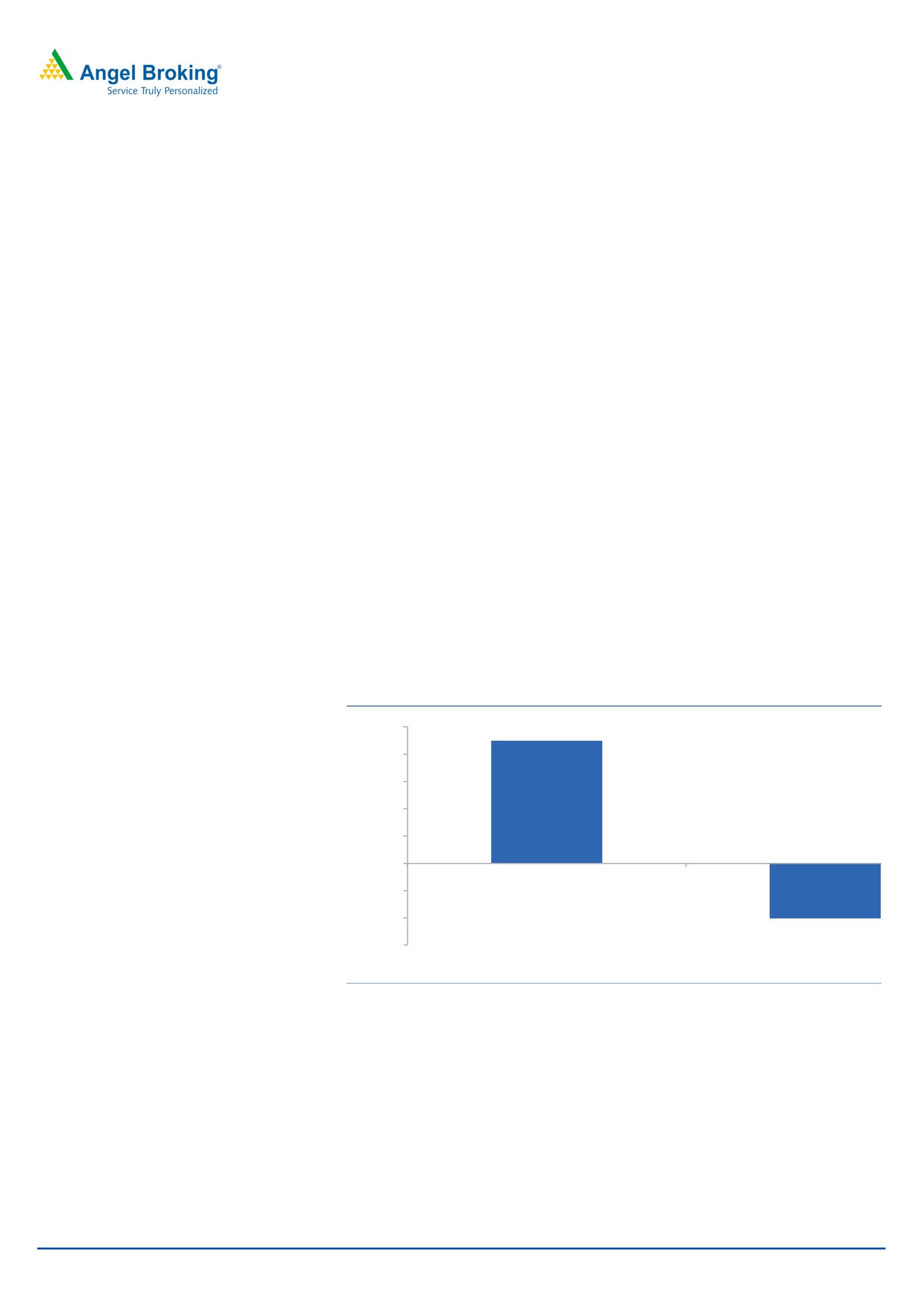

Growth to rebound in casting business due to client diversification:

Endurance started its business as a die casting supplier to Bajaj Auto. Over the

past several years, casting segment has become its largest segment contributing

44% of domestic revenues in FY2017. In FY2010, Bajaj Auto and Yamaha were its

two major clients in the casting business and Bajaj Auto contributed ~70% of its

domestic sales (casting + other segments). With Bajaj Auto as its main client,

growth of the casting business was largely pegged with the growth of the Bajaj

Auto.

With the rapid growth of scooters, the motorcycle sales in India have been

adversely impacted in the past several years. As a result of which Bajaj Auto has

suffered since it has no exposure to scooters. In FY2016, Bajaj Auto reported ~2%

yoy growth in the 2W volumes as exports started to decline. In FY2017, while

domestic motorcycle volumes grew by 5.4% yoy, exports declined by 16.5% yoy to

pull down the total volumes.

In the last seven years, company has added other clients such as Royal Enfield,

Hero MotoCorp (HMCL), Honda Motorcycle & Scooter India (HMSI), etc. This has

reduced the company’s dependence of casting business on Bajaj Auto. The

diversification of clients in the casting business has been positive for Endurance

despite the sluggish growth in Bajaj Auto’s 2W volumes. Moreover, Endurance

grew its casting business by 4.5% between FY2014-17.

Exhibit 10: Casting business grew 4.5% despite Bajaj Auto’s sluggish

volume growth (FY2014-17)

5.00%

4.50%

4.00%

3.00%

2.00%

1.00%

0.00%

-1.00%

-2.00%

-2.01%

-3.00%

Endurance Tech (Casting business)

Bajaj Auto volumes

Source: Company, Angel Research

Bajaj Auto numbers expected to improve: With the rapid growth in scooters

segment (Scooterization), the motorcycle sales in India were impacted in the past

several years. This impacted Bajaj Auto, which has no exposure in scooters

segment. However, we believe that Bajaj Auto is now in the recovery mode. In

FY2016, Bajaj Auto reported ~2% yoy growth in the 2W volumes, as exports

started to decline. In FY2017, while domestic motorcycle volumes grew by 5.4%

yoy, exports declined by 16.5% yoy to pull down the total volumes.

FY2018, however, seems to end differently for Bajaj Auto. While 1HFY2018

exports have witnessed 6% yoy growth, domestic numbers have been soft owing to

October 16, 2017

5

Initiating coverage | Endurance Technologies

(1) BSIV (Bharat Stage Emission Standards) implementation (where Bajaj was first

to move to BSIV, but discounts by competitors hurt Bajaj Auto’s volumes), and (2)

GST implementation, which has hurt all vehicle manufacturers. In September

2017, company reported 7% yoy growth in the domestic volumes while exports

grew by 20.5% yoy. With the satisfactory monsoon and recovery in the rural

economy, we believe that Bajaj Auto is likely to post better domestic volumes

whereas the exports are expected to grow, as it has entered in the new countries,

which have reduced the dependence on high volume countries like Sri Lanka,

Nigeria, etc.

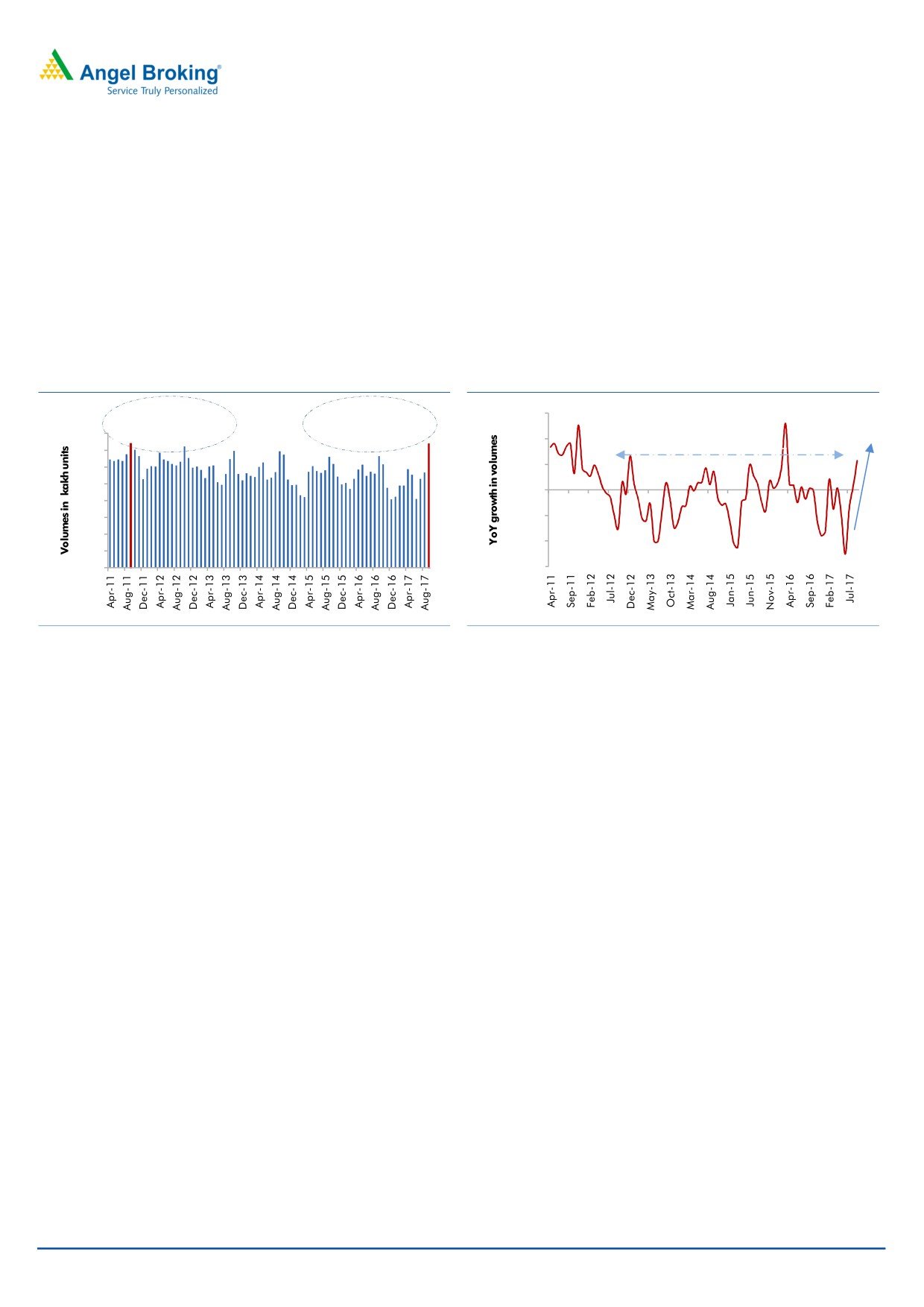

Exhibit 11: Bajaj Auto - 2nd highest monthly volumes in

Exhibit 12: Bajaj Auto’s growth was impacted in the

Sept-17

previous years but it is now in recovery mode

Period of sluggish growth owing to

30.0%

Sept-11 - 3.71

Sept-17 - 3.70

higher scooter sales, poor rural

4.00

lakh units

lakh units

20.0%

economy, BSIV and GST

3.50

3.00

10.0%

2.50

0.0%

2.00

1.50

-10.0%

1.00

-20.0%

0.50

0.00

-30.0%

Source: Bajaj Auto, Angel Research

Source: Bajaj Auto, Angel Research

This rebound in Bajaj Auto’s volumes is expected to benefit the casting business of

Endurance, which should grow by 6-7% going ahead.

Proprietary products, diversifying in new products and customers: Endurance’s

proprietary products i.e. suspension, transmission and braking products, contribute

about 1/3rd of the total revenue. Endurance introduced suspension products in

1996, transmission products in 1998 and brake systems in 2004. This is the

business in which the company has greater scope to increase value added

products, expand the business, add more clients to diversify further. Unlike casting

business, company has already achieved a decent diversification in the suspension

and transmission business and there is still a scope to add more clients in the

braking business.

Suspension: The suspension market, estimated to be `4,200cr in FY2017,

which is expected to grow at a CAGR of 12.7% to reach `5,300cr in FY2019E.

The 2W and 3W suspension includes front fork and shock absorber units.

While the suspension volumes are expected to grow at 8.6% CAGR by

FY2019, market is expected grow at 12.7% CAGR indicating that the

suspension products are expected to witness better realizations compared to

the earlier years. The replacement of shock absorbers by front forks in the

scooters is the main driver for the growth of the 2W transmission. Company

expects that by 2019-20, all scooters in India will have suspension front forks

instead of lower price shock absorbers.

October 16, 2017

6

Initiating coverage | Endurance Technologies

Exhibit 13: 8.6% CAGR in suspension volumes

Exhibit 14: ...and 12.7% CAGR in market size

60

6,000

50

5,000

40

4,000

30

3,000

20

2,000

10

1,000

0

0

FY12

FY13

FY14

FY15

FY16

FY17P

FY18P

FY12

FY13

FY14

FY15

FY16

FY17P FY18P FY19P

Source: DRHP, Angel Research

Source: DRHP, Angel Research

Exhibit 15: Endurance’s suspension family

Source: Company, Angel Research

Transmission: The transmission market has two categories i.e. Clutch assemblies

and Continues Variable Transmission (CVT). Clutch assemblies are used in vehicles

with gears i.e. motorcycles while CVTs are used in non-gear vehicles, i.e. scooters.

The rapid scooterization in the country has been driving the CVT volumes in India

and the same is expected to benefit Endurance.

Exhibit 16: 8.7% CAGR in transmission volumes

Exhibit 17: ...and 15.7% CAGR in market size

30

3,500

3,000

25

2,500

20

2,000

15

1,500

10

1,000

5

500

0

0

FY12

FY13

FY14

FY15

FY16

FY17P

FY18P

FY12

FY13

FY14

FY15

FY16

FY17P FY18P FY19P

Source: Company, Angel Research

Source: Company, Angel Research

October 16, 2017

7

Initiating coverage | Endurance Technologies

Exhibit 18: Endurance’s transmission family

Source: Company, Angel Research

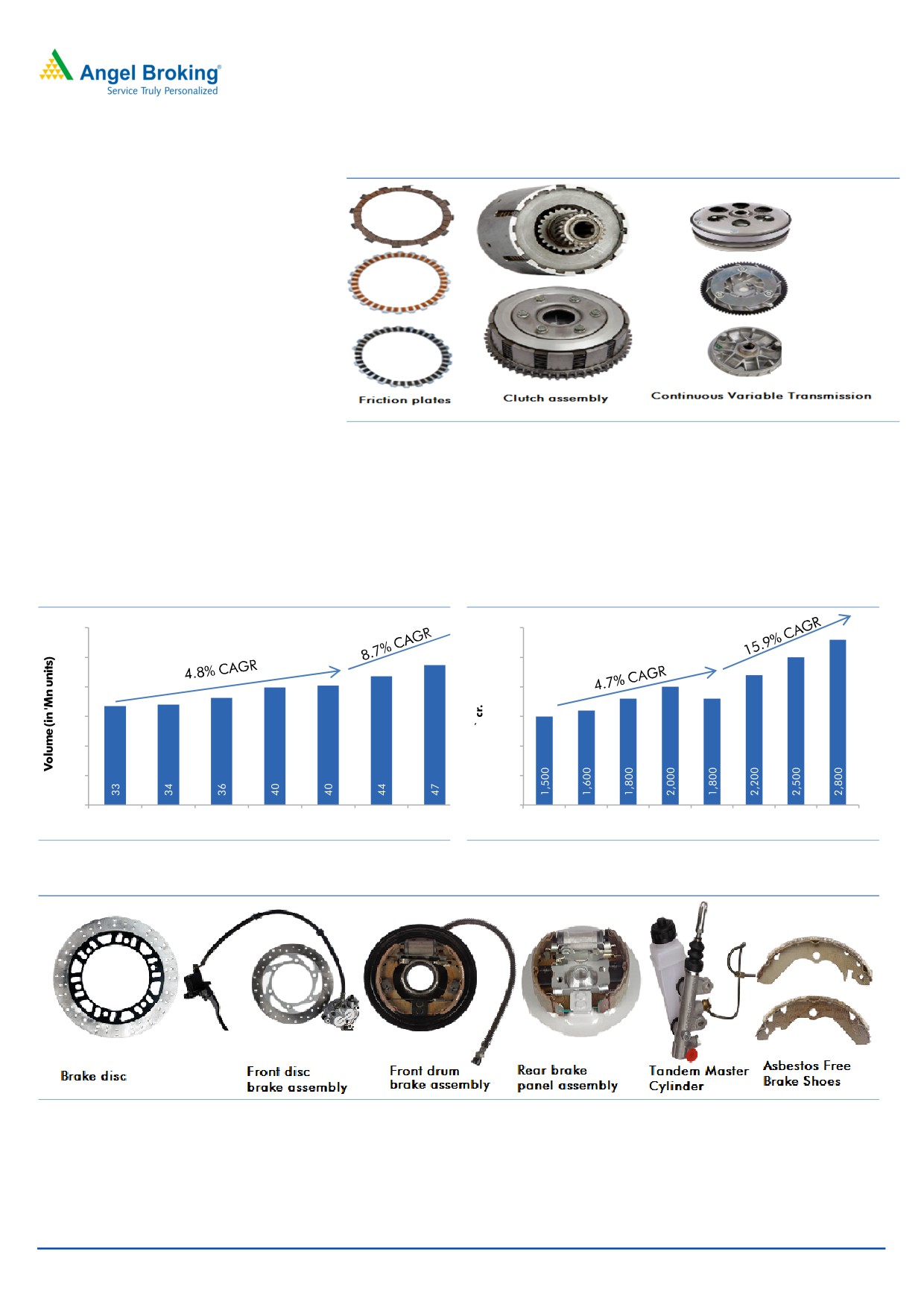

Braking: The braking market is also an equally attractive market. The market

for 2W and 3W brakes is expected to grow from `2,200cr in FY2017 to

`2,800cr in FY2019E. In volume terms, braking volumes are expected to grow

at a CAGR of 8.7% (FY2016-19E) whereas during the same period in value

terms market is expected to grow at ~16%.

Exhibit 19: 8.7% CAGR in braking volumes

Exhibit 20: ...and 15.9% CAGR in market size

60

3,000

50

2,500

40

2,000

30

1,500

20

1,000

10

500

0

0

FY12

FY13

FY14

FY15

FY16

FY17P

FY18P

FY12

FY13

FY14

FY15

FY16

FY17P FY18P FY19P

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 21: Endurance’s braking family

Source: Company, Angel Research

October 16, 2017

8

Initiating coverage | Endurance Technologies

Exhibit 22: Proprietary business, diversified products and OEM clients

Segment

Products

OEM clients

Twin/ Mono tube Hydraulic, Oil and gas-filled shock absorbers, Mono shock

Bajaj, Honda, Royal Enfield, Hero, Yamaha,

Suspension

absorbers, Spring-in-spring and spring-on-spring hydraulic shock absorbers,

Harley-Davidson.

Cartridge variety and Inverted forks

Bajaj and Piaggio Ape (3W) and Bajaj

Clutch assemblies

Quadricycles.

Transmission

Hero MotoCorp, Bajaj Auto, Royal Enfield, Bajaj

CVTs, Friction plates

Auto, Mahindra, Piaggio, Bajaj Quadricycles

Hydraulic disc brake assemblies

Bajaj Auto, Royal Enfield

Rotary brake discs assemblies

Bajaj Auto, Royal Enfield Yamaha

Brake Systems

Hydraulic drum brake assemblies

Bajaj Auto (3W)

Tandem master cylinder assemblies

Bajaj Auto (3W)

Source: Company, Angel Research

Strategy for proprietary products: For the proprietary products, Endurance’s

journey can be divided in two parts (1) add more OEMs and (2) increase the

content per vehicle. We believe that the first part of this journey has been executed

before the IPO. During this phase, company added Hero, Honda, Mahindra and

Royal Enfield in the last ten years. TVS Motor Company is the only missing large

two wheeler company from its client list. From our discussions, we understand that

company intends to add TVS as its client in future. Endurance already has Bajaj

and Piaggio in the three wheeler category, these two companies together hold

almost 80% market share. Company is also supplying inverted front forks to KTM

and has plans to increase the export of inverted front forks to KTM in big ways.

This is also expected to help the proprietary business pie in the total business.

We believe that the company is in the second phase of the journey that will see

increasing revenue share of its clients. Also with proprietary products being of the

high value adds than the low margin casting business, Endurance has more to

gain in its domestic business from this strategy.

Incremental opportunities for Endurance in proprietary business:

Opportunity with Hero MotoCorp (HMCL) - Endurance has been a die casting

and suspension part supplier to HMCL’s Manesar and Rajasthan plants. It has

also become a suspension part supplier to HMCL’s new Halol plant in

Gujarat. Currently, these supplies are made from Aurangabad plant and

Endurance is in process to set up a plant at Halol. Hero’s Karnataka plant has

annual capacity of 2.4mn while Halol plant (commissioned in March 2017)

has a peak capacity of 1.8mn vehicles. Hero is targeting to produce 2,700

vehicles per day in FY2018 and take it to 6,200 per day in FY2019.

Endurance is also starting with clutches and CVT parts from HMCL at Halol

plant in the second half of this fiscal. HMCL is currently contributing <2% to

the company’s revenue and going ahead, this is expected to see a sharp

increase.

Opportunity with Honda

- While Endurance is already a casting and

suspension part supplier to Honda, an incremental opportunity is in the

Honda’s scooter only plant in Vithalapur, Gujarat. This plant has a capacity of

1.2mn vehicles. Company will be supplying front forks and shock absorbers to

this scooter plant. While company is supplying casting and suspension

products to Honda’s dream series bikes, braking is expected to follow going

October 16, 2017

9

Initiating coverage | Endurance Technologies

ahead. Company expects braking for Honda to start in FY2019. Honda

contributes ~13% to company’s revenue and the same has a scope to

increase further as Endurance meets 100% requirement for suspension at

Honda’s Karnataka plant and sizable portion (~65%) of shock absorbers for

scooters. In Gujarat, company has 80% share in suspension and 60-65% in

casting. Barring Activa (125 CC) and Aviator (110 CC), Honda’s other

scooters are yet to move to the telescopic suspension, which makes Honda a

big opportunity for Endurance. Endurance’s component sales to Honda have

already been seeing more than 30% yoy growth and once Gujarat plant

reaches its full capacity i.e. in FY2019, the growth will be even higher.

Exhibit 23: Dio and Activa (100cc category) is yet to move to telescopic

suspension

Model/Engine

Front suspension type

Activa - 110 CC

Spring loaded hydraulic type

Activa I - 110 CC

Spring loaded hydraulic type

Dio - 110 CC

Tube type

Aviator - 110 CC

Telescopic

Activa - 125 CC

Telescopic

Source: Company, Angel Research

Opportunity with Royal Enfield - Endurance supplies castings, suspension and

transmission to Royal Enfield and it has been growing at 30% rate and

contributes ~10% in revenue. Company in the last fiscal started to supply disc

brake assemblies to RE’s 350CC bikes and expects to increase the share of

this business to Royal Enfield. For Royal Enfield, Endurance is moving its

production from Pune to Chennai, as the orders from Royal Enfield are

growing fast. This is expected to help in saving logistics and packaging costs,

which will help it in the margins as well as maintaining a relationship through

which it can get more orders.

Opportunity in ABS/CBS - Braking segment will also see an opportunity in

terms of mandatory Antilock Braking System for two wheelers above 125CC

vehicles from 2018 onwards and ABS or Combined Braking System (CBS) in

two wheelers below 125CC capacity. Currently, Bosch and Continental are the

only two players in ABS/CBS and Endurance is in advanced stage to

manufacture its version of ABS/CBS and has a technology tie up with a US

company BWI North America Inc. Company has already received approval for

CBS from Bajaj Auto for two vehicles in the June quarter. Company is also

expecting to add more clients in ABS/CBS and we too remain positive, as there

are only two established players. India’s vehicle mix includes ~40% of

125CC, hence we believe that total opportunity at `3,000/vehicle is expected

to be `2200-2500cr in FY2019E. With only 3-4 manufacturers of ABS, we

believe Endurance can gain a market share 8-10% in the first year in its

existing clients leading to a top line addition of ~`200-250cr with a good

margin.

Increasing the contents in scooters is the thrust - For long, Endurance’s major

domestic business was associated with motorcycles, however with its association

with Hero and Honda, the same is expected to change. Especially with Honda’s

strong market share and high growth in the scooters segment, Endurance is

October 16, 2017

10

Initiating coverage | Endurance Technologies

expected to benefit strongly. Honda already contributes ~8% of Endurance’s

consolidated revenue and with increasing pace of scooterization in India,

Endurance looks to emerge a strong beneficiary due to (1) association with

Honda’s all scooter Gujarat plant, and (2) replacement of shock absorbers by front

forks. Endurance’s new products such as front forks, CVT are especially targeting

the scooters and with its strong repute and track record we believe that Endurance

is well placed to seize this opportunity.

Aftermarkets - small business with high margin: Endurance’s aftermarket

business was established in 2001 in order to build the ‘Endurance’ brand.

Company only distributes its proprietary products through this business.

Aftermarket business is currently at 5% of domestic sales but the company intends

to increase this to 10% of domestic business in the next 3 years. Company has

expanded its aftermarket business to Argentina, Dominican Republic, and El

Salvador in FY2017 and also saw increased sales in countries like Honduras and

Peru. It also intends to increase the number of countries going ahead, which is

expected to increase the revenue contribution from aftermarket business. This, we

believe is a positive move, as aftermarket is a B2C business, which has significant

high margins than other businesses.

The aftermarket business has grown at

~15% growth, lower than the

management’s expectation. Domestic aftermarket segment is fragmented and

there is scope for the organized players like Endurance to grow. We believe that

this business can grow faster with expansion in new countries and emergence of

ecommerce sales channel in the aftermarket segment.

European business- concentrated but focused: Endurance’s European business

is fully acquired business. It has three manufacturing plants in Massenbachhausen,

Germany and five in Torino, Italy. The company has recently (in FY2017)

commissioned a new machining plant in Massenbachhausen, Germany. In Europe

Endurance caters to four-wheeler OEMs, focusing on engine and transmission

components. Its products include raw and machined aluminum castings (high-

pressure and gravity die-casting products) and steel, cast iron and engineering

plastic parts. Its main customers in Europe are Fiat Chrysler Group (FCA), Daimler,

General Motors, Volkswagen, BMW, etc. Customer concentration in European

business is high with ~85% of European sales coming from the top 5 customers.

Company has indicated that its major customers in Europe (FCA and VW) are

growing faster than the market ~15% yoy. It has also indicated that it will continue

to focus on the existing customers rather than adding any new customers.

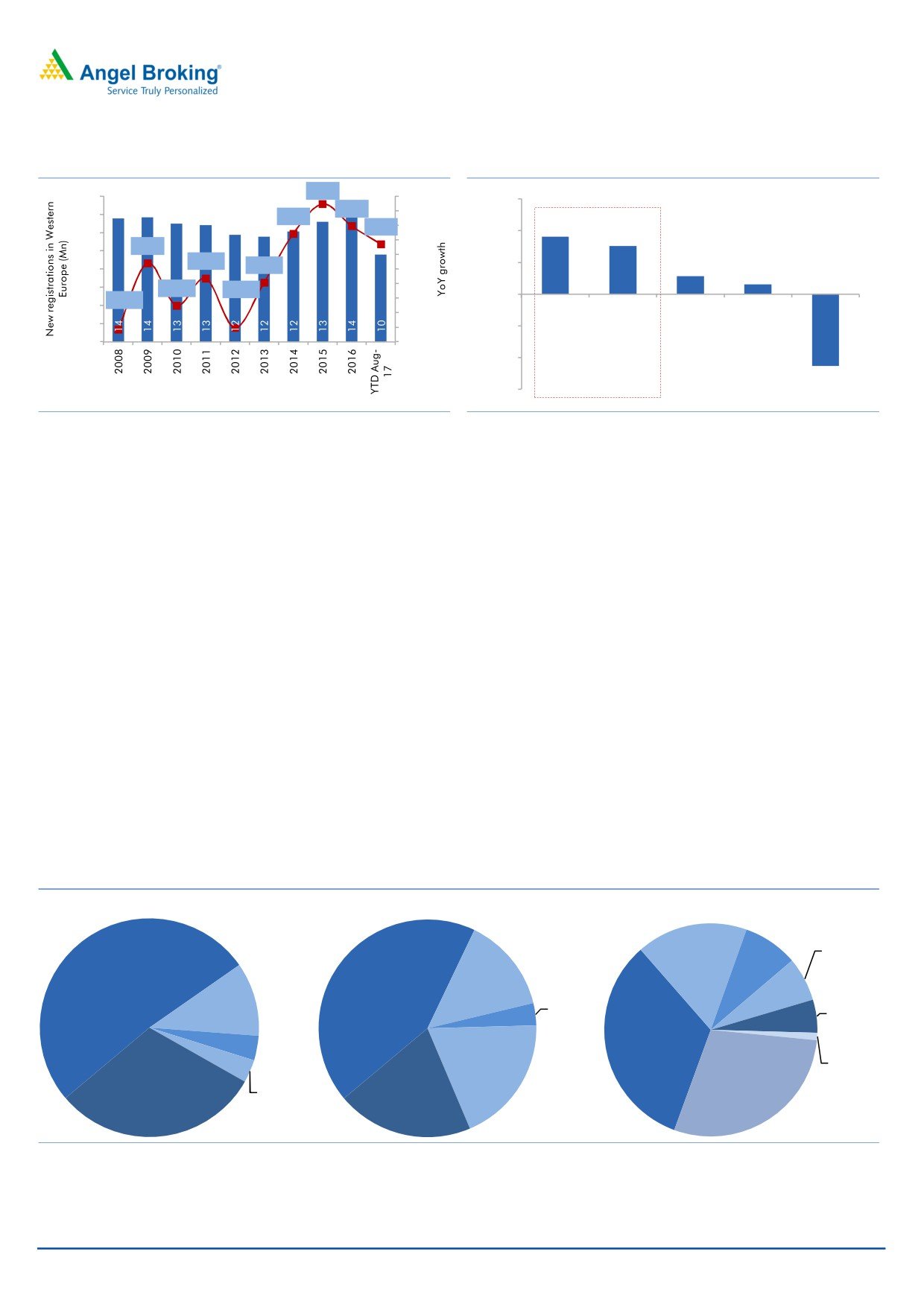

European auto industry in strong recovery mode: The European auto market

is one of the largest in the world and was impacted for long after the financial

crisis of 2007-08 and following the debt crisis in Europe. The market is now in

recovery mode with strong demand and positive sentiment. After the consistent

slump in the new car registrations post the financial crisis, European car

registrations have been growing for the last three years and the trend has

continued in the year 2017 as well.

Endurance’s major clients i.e. FCA and Daimler have also shown a yoy growth of

9.1% and 7.6% respectively in the first 8 months of CY2017. Both of these

companies contribute about 3/4th of Endurance’s European business. Endurance

has indicated that it has order book visibility till 2025E for engines components

and up to 2028E for transmission components. This gives us comfort in the revenue

visibility of the company for long period going ahead.

October 16, 2017

11

Initiating coverage | Endurance Technologies

Exhibit 24: Recovery in the European auto sector

Exhibit 25: Volume growth in Endurance’s clients

8.9%

16.0

10.0%

15.0%

YoY growth in 8MCY2017

5.9%

8.0%

14.0

4.8%

3.4%

6.0%

9.1%

12.0

10.0%

7.6%

4.0%

0.8%

10.0

2.0%

-1.3%

5.0%

2.9%

8.0

-1.9%

0.0%

1.5%

-2.0%

6.0

-5.0%

-8.1%

0.0%

-8.3%

-4.0%

4.0

FCA

DAIMLER

VW

BMW

GM

-6.0%

2.0

-8.0%

-5.0%

0.0

-10.0%

70% contrubition in

-10.0%

Eundurance's

European business

-11.3%

-15.0%

Source: Automobile manufacturers Association, Angel Research

Source: European Automobile manufacturers Association, Angel Research

European business likely to see higher margins: Endurance intends to reduce the

simple parts and increase the value-added complex products (such as structural

parts and large and complex engine and transmission castings) with its European

clients. The European business is already a high EBITDA margin business (13-14%)

and increasing value added content will be margin accretive in our opinion.

Company is also intending to continue with its inorganic route of growth in Europe

and has indicated that it may acquire a small and profitable business. It has set a

ticket size of €20-40mn and is looking for a small company (with 10% EBITDA

margin) with space availability for Greenfield expansion. While 10% EBITDA

margins are less than what Endurance enjoys in Europe currently, we believe that

management has shown their capability to run overseas operations successfully.

Changing client mix, a big positive: Bajaj Auto has been the major revenue driver

of Endurance since inception, however, that has been changing over the last few

years. Bajaj Auto contributed 51.5% in FY2010, which has come down to 33% in

FY2017 and we believe that this will further reduce with the higher contribution

from other clients, HMCL is contributing less than 2% in Endurance’s revenue and,

as the business with HMCL would increase, the pie will grow further. Company

expects HMCL’s contribution through Halol plant to be annually `275cr in

FY2019E (3.5-4% as per our estimates). Similarly, with the ramp up at Honda’s

new scooters plant and overall increasing content especially in the scooters,

Honda’s share in Endurance is expected to grow.

Exhibit 26: Bajaj Auto’s revenue continues to shrink significantly reducing the client concentration risk

FY10

FY14

FY17

Royal

Enfield,

Fiat

7%

Bajaj

Chrysler,

Fiat

HMSI,

Auto,

Bajaj

Fiat

17%

Group,

8%

51.4%

Auto,

Group,

10.9%

43.20%

14.20%

Royal

Daimler,

Enfield,

5%

Daimler

3.30%

AG,

Bajaj

3.60%

Auto,

Next 5 ,

33%

HMCL,

19.00%

1%

HMSI,

Others,

3.40%

Others,

29%

Others,

30.7%

20.30%

Source: Company, Angel Research

Company in the last two years has added a new small client (Getrag) which is the

largest independent maker of transmission systems for cars and vans. Company sells

October 16, 2017

12

Initiating coverage | Endurance Technologies

aluminum castings to Getrag, which fetched `78cr for Endurance in FY2017. Company

expects Getrag revenues to double to ~175cr by FY2019E.

Overall, the diversifying client base removes the client concentration risk, which

would further improve the company’s business fundamentals.

Financials

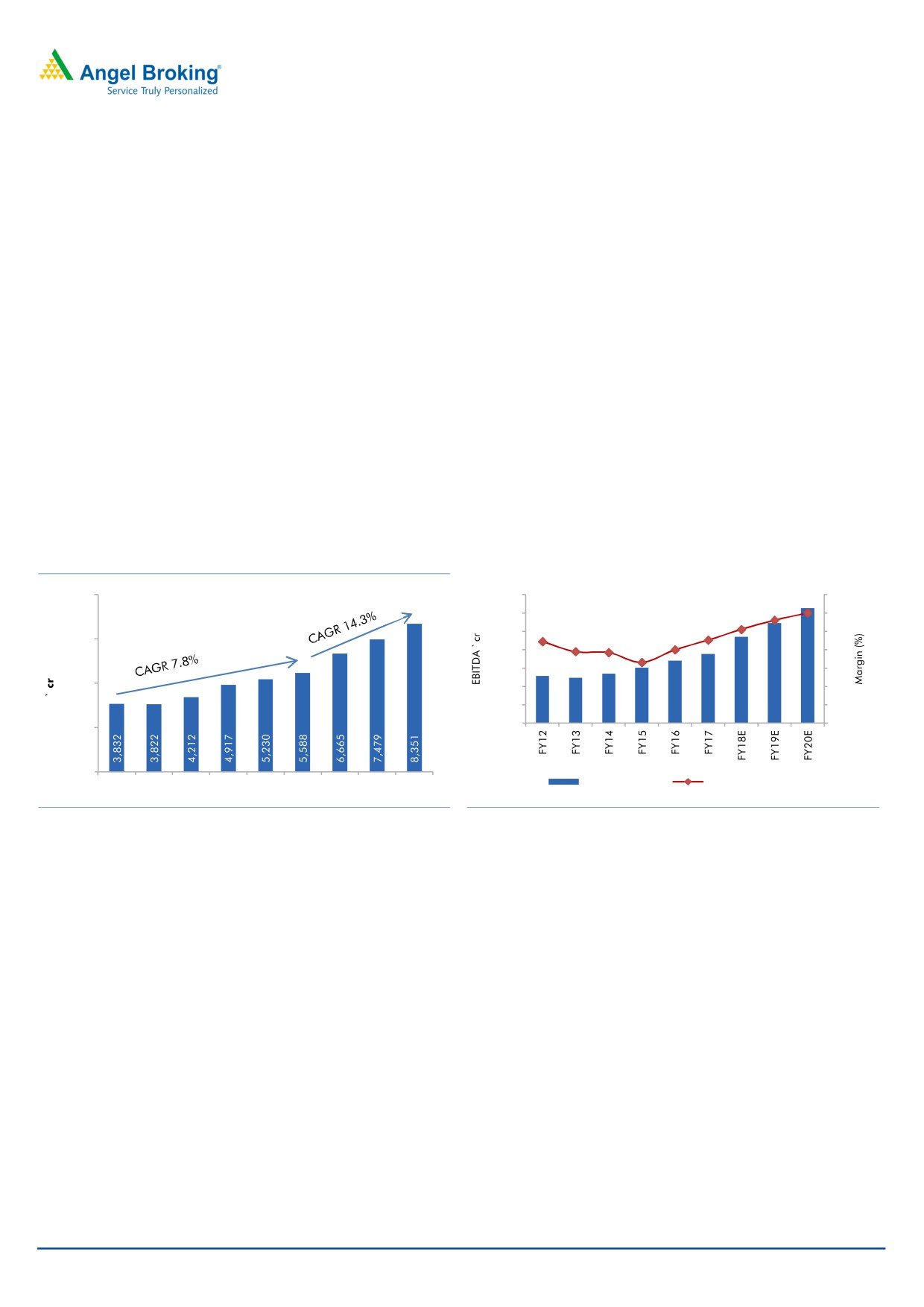

14% revenue CAGR, ~150bps margin expansion: With Bajaj Auto expected to

improve its performance, we believe, its legacy casting business would see a faster

growth. Casting business, which grew by ~4.5% over past few years due to decline

in Bajaj Auto’s market share, can now see growth of ~6%. We also expect the

Suspension, Transmission and Braking business to clock in double digit revenue

growth mainly due to the increasing content, especially in the scooters and higher

revenue contribution from HMCL, HMSI and Royal Enfield. We also believe that

Aftermarket + Exports (including Getrag) have a potential to grow by more than

20% going ahead. Overall, we anticipate Endurance to register a top-line CAGR of

14.3% over FY2017-20E.

Exhibit 27: 14% Revenue CAGR over FY2017-20E

Exhibit 28: 150bps margin improvement (FY2017-20E)

10,000

1,400

15.0

16

14.6

1,200

14.1

15

13.4

13.5

1,000

14

7,500

12.9

12.8

13.0

800

12.3

13

600

12

5,000

400

11

200

10

2,500

0

9

0

EBITDA (` cr)

EBITDA margins (%)

FY12

FY13

FY14

FY15

FY16

FY17

FY18E FY19E FY20E

Source: Company, Angel Research

Source: Company, Angel Research

With the increasing contribution of the proprietary products, Endurance has seen

improving EBITDA margins between FY2015-17, and we believe that this pace of

improvement would accelerate with (1) higher contribution of the proprietary

products, (2) growth in Bajaj Auto’s business, which will increase utilization of the

casting business assets, (3) sustained growth momentum in the European business

and strong order book over next 5-7 years, and (4) growing share of the

aftermarket business including Getrag transmission revenues.

Solid FCF generation over the next three years: Owing to the lower capex

requirement and efficient working capital management, Endurance would witness

a period of strong free cash flow generation over FY2018E-20E. The company has

efficiently managed the working capital (FY2017 - inventory days 29 days, debtor

days 50 days and creditor days 56 days, total working capital cycle of 23 days).

We believe that company is set to see free cash flow of `1,098cr over the next

three years (FY2018E-20E), compared to `1,268 in the earlier six years (FY2012-

17). This will be aided by improving margins, lower capex requirement and

sweetening of the domestic assets.

October 16, 2017

13

Initiating coverage | Endurance Technologies

Exhibit 29: Lower capex to improve FCF/CFO

Exhibit 30: Period of strong cash generation ahead

53

58

49

1000

60

FY18E-FY20E

FY12-FY17

46

43

33

40

50

800

500

40

450

``1,098cr

600

27

30

400

30

350

400

20

300

200

250

10

200

0

0

150

100

50

0

CFO

FCF to CFO

Source: Company, Angel Research

Source: Company, Angel Research

Endurance has been strengthening its balance sheet over the last five years. In

FY2012 company had debt of `980cr, which has reduced to `694cr in FY2017.

The debt to equity ratio was at 1.6x in FY2012, which has come down to 0.4x in

FY2017. Over the years, company has improved the balance sheet by reducing

the debt and achieving operational efficiency. With the strong free cash flow

generation over the next three years, we believe that the company is likely to

become debt free in FY2020E.

Profitability and Return ratios: With the improving balance sheet and higher

profitability, company has consistently maintained ROE of 18-20% over the period

of FY2012-17. Also, with the improving cash profile, the ROIC ratio has been

mostly above 22%, and we believe that Endurance would continue this trend. We

forecast average ROE of 23% and average ROIC of ~30% over FY2018E-20E.

Exhibit 31: PAT CAGR of 22.5% over FY2017-20E

Exhibit 32: Average 23% ROE over FY2018E-20E

35.0

700

30.0

600

25.0

500

20.0

400

15.0

300

10.0

200

5.0

100

-

FY16

FY17

FY18E

FY19E

FY20E

0

FY12

FY13

FY14

FY15

FY16

FY17

FY18E FY19E FY20E

ROIC ROE

Source: Company, Angel Research

Source: Company, Angel Research

Endurance v/s. peers: There is no clear comparable peer for Endurance

Technologies due to its multiproduct profile therefore we look at bigger auto

ancillary universe. While Endurance is the largest 2W auto ancillary in India, we

believe that it is best placed in terms of operating performance, returns, product

segments, etc.

Majority of domestic auto ancillaries are single product ancillaries. While

Endurance Technologies was not so different in business a few years ago,

company has been deliberately growing its business in other segments as well as

has expanded in Europe as well. During this period, Endurance has become a

October 16, 2017

14

Initiating coverage | Endurance Technologies

diversified ancillary with operations across 2W, 3W and 4Ws (Europe) and we

believe the revenue mix will be far different in the next three years.

Endurance’s EBITDA margins are already better than most domestic ancillaries but

compared to the MNC ancillaries, there is a further scope for improvement. While

Endurance’s main breadwinner is casting business, the increasing pie of its

proprietary products is likely to see rapid improvement in its margin profile. Over

the next three years, we believe that Endurance is positioned to see more than

100bps improvement in its EBITDA margins.

On the returns front, Endurance is amongst the top ranked ancillaries with its 20%

ROE. Gabriel India, Wabco India, and Bosch have better ROE profile than

Endurance. We forecast Endurance to see 200-250bps jump in the ROE profile

over the next three years.

We like Endurance’s diversifying business, multiproduct focus and improving

returns/margins which stand out v/s. its most peers.

Exhibit 1: Endurance has better operating performance and has a scale to grow

Name of the company

Business Description Mcap (`cr) Revenue (`cr) EBITDA margins Adj PAT(`cr)

ROE ROIC ROCE

Bosch

Multiproduct, diversified

65,653

10,435

21.6%

1,293

14.7%

63.6%

20.5%

Endurance

Multiproduct, diversified

15,346

5,588

13.5%

328

19.0%

23.3%

19.2%

WABCO India

Multiproduct, diversified

11,902

2,067

15.8%

200

15.8%

41.4%

20.9%

Minda Industries

54% 4W, 46% 2W

7,133

3,505

10.9%

167

16.3%

25.0%

15.9%

Gabriel India

Suspension

2,873

1,529

9.3%

82

18.3%

28.5%

23.3%

Lumax Industries Ltd

Lightings across vehicle types

1,415

1,300

7.7%

55

17.4%

21.5%

14.5%

Rico Auto Industries

Castings

1,316

1,079

10.5%

49

9.5%

9.5%

8.7%

Munjal Showa

2W, 3W, 4W

1,100

1,460

6.5%

53

10.3%

19.6%

12.9%

Source: Capitaline, Angel Research, Mcap is current, P&L numbers and returns based on FY17 numbers

Outlook and valuation

Shares of Endurance have seen a strong appreciation since its lasting last year. At

the CMP of `1,095, the stock is trading at the PE of 26x of its FY2020E EPS. We

forecast top-line and bottom-line CAGR of 14.3% and 21.3% respectively over the

next three years. We also forecast ~150bps/200bps jump in its EBITDA margins

and ROE respectively. With the strong FCF generation, we believe that Endurance

will become almost debt free in the next three years. We also look at the MNC

Auto ancillaries which are richly valued and believe that Endurance should

command premium over its homegrown domestic peers.

We value Endurance Technologies at 29.0x of its FY2020E EPS of `42.8 to derive

the core business price target of `1,242 and add `35, NPV of ABS opportunity to

derive the target price of `1,277, implying 15% upside.

October 16, 2017

15

Initiating coverage | Endurance Technologies

Income statement

Y/E March (` cr)

FY16

FY17

FY18E

FY19E

FY20E

Total operating income

5,230

5,588

6,665

7,479

8,351

% chg

6.4

6.8

19.3

12.2

11.7

Total Expenditure

4,551

4,833

5,725

6,387

7,098

Raw Material Consumed

3,114

3,226

3,852

4,308

4,794

Personnel Expenses

482

546

640

696

768

Others Expenses

954

1,061

1,233

1,384

1,537

EBITDA

680

755

940

1,092

1,253

% chg

12.3

11.2

24.4

16.2

14.7

(% of Net Sales)

13.0

13.5

14.1

14.6

15.0

Depreciation& Amortisation

243

291

311

367

430

EBIT

436

465

629

725

822

% chg

15.4

6.6

35.2

15.2

13.5

(% of Net Sales)

8.3

8.3

9.4

9.7

9.8

Net Interest charges

16

0

(9)

(15)

(20)

Recurring PBT

420

465

638

740

843

% chg

16.9

10.5

37.3

15.9

13.9

Extraordinary Expense/(Inc.)

-

-

-

-

-

PBT (reported)

420

465

638

740

843

Tax

120

134

182

211

240

(% of PBT)

28.5

28.9

28.5

28.5

28.5

PAT before MI

300

330

456

529

603

Minority Interest (after tax)

1

2

-

-

-

Profit/Loss of Associate Company

-

-

-

-

-

PAT after MI(reported)

299

328

456

529

603

Exceptional items

-

-

-

-

-

Reported PAT

299

328

456

529

603

% chg

18.6

9.5

39.1

15.9

13.9

(% of Net Sales)

5.7

5.9

6.8

7.1

7.2

Basic EPS (`)

21.3

23.3

32.4

37.6

42.8

Fully Diluted EPS (`)

21.3

23.3

32.4

37.6

42.8

% chg

18.6

9.5

39.1

15.9

13.9

October 16, 2017

16

Initiating coverage | Endurance Technologies

Balance sheet

Y/E March (` cr)

FY16

FY17

FY18E

FY19E

FY20E

SOURCES OF FUNDS

Equity Share Capital

18

141

141

141

141

Reserves& Surplus

1,432

1,589

1,963

2,327

2,683

Shareholder’s Funds

1,450

1,729

2,103

2,468

2,823

Minority Interest

-

-

-

-

-

Total Loans

831

694

666

661

656

Other liabilities

39

37

39

40

42

Deferred Tax Liability

-

-

-

-

-

Total Liabilities

2,320

2,460

2,808

3,169

3,521

APPLICATION OF FUNDS

Gross Block

1,689

2,005

2,393

2,826

3,311

Less: Acc. Depreciation

249

507

818

1,185

1,616

Net Block

1,440

1,498

1,575

1,641

1,695

Capital Work in Progress

103

44

44

44

44

Goodwill

147

135

135

135

135

Investments

48

33

33

33

33

Other long term assets

247

229

290

319

351

Current Assets

1,295

1,570

1,930

2,294

2,685

Inventories

410

444

511

574

641

Sundry Debtors

593

761

877

984

1,098

Cash

167

220

342

512

695

Loans & Advances

125

145

200

224

251

Current liabilities

961

1,049

1,199

1,299

1,422

Net Current Assets

334

521

731

996

1,263

Total Assets

2,320

2,460

2,808

3,168

3,521

October 16, 2017

17

Initiating coverage | Endurance Technologies

Cash flow statement

Y/E March (` cr)

FY16

FY17

FY18E

FY19E

FY20E

Profit before tax

420

465

638

740

843

Depreciation

243

291

311

367

430

Change in Working Capital

39

(89)

(147)

(122)

(114)

Interest / Dividend (Net)

47

32

31

30

30

Direct taxes paid

(105)

(134)

(182)

(211)

(240)

Others Expenses

54

(23)

-

-

-

Cash Flow from Operations

698

541

651

804

949

(Inc.)/ Dec. in Fixed Assets

(469)

(380)

(388)

(434)

(484)

(Inc.)/ Dec. in Investments

(46)

17

(0)

-

-

Others Expenses

6

2

-

-

-

Cash Flow from Investing

(509)

(361)

(388)

(434)

(484)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

(1.5)

(86.1)

(28.0)

(5.0)

(5.0)

Dividend Paid (Incl. Tax)

(29.6)

(6.3)

(70.3)

(140.7)

(211.0)

Others

(83.0)

(33.8)

(42.5)

(53.7)

(65.4)

Cash Flow from Financing

(114)

(126)

(141)

(199)

(281)

Inc./(Dec.) in Cash

76

54

122

170

183

Opening Cash balances

90

166

220

342

512

Closing Cash balances

166

220

342

512

695

October 16, 2017

18

Initiating coverage | Endurance Technologies

Key Ratios

Y/E March

FY16

FY17

FY18E

FY19E

FY20E

Valuation Ratio (x)

P/E (on FDEPS)

52.2

47.6

34.2

29.5

25.9

P/CEPS

28.8

25.3

20.4

17.4

15.1

P/BV

10.8

9.0

7.4

6.3

5.5

Dividend yield (%)

0.0

0.0

0.0

0.0

0.0

EV/Sales

3.1

2.9

2.4

2.1

1.9

EV/EBITDA

24.0

21.3

17.0

14.4

12.4

EV / Total Assets

5.0

4.6

4.0

3.5

3.2

Per Share Data (`)

EPS (Basic)

21.3

23.3

32.4

37.6

42.8

EPS (fully diluted)

21.3

23.3

32.4

37.6

42.8

Cash EPS

38.6

44.0

54.5

63.7

73.4

DPS

2.1

2.5

5.0

10.0

15.0

Book Value

103.1

122.9

149.5

175.4

200.7

Dupont Analysis

EBIT margin

8.3

8.3

9.4

9.7

9.8

Tax retention ratio

0.7

0.7

0.7

0.7

0.7

Asset turnover (x)

2.5

2.6

2.8

2.9

3.0

ROIC (Post-tax)

15.1

15.2

18.8

20.1

21.4

Cost of Debt (Post Tax)

0.0

0.0

(0.0)

(0.0)

(0.0)

Leverage (x)

0.5

0.3

0.2

0.1

(0.0)

Operating ROE

22.0

19.4

21.7

21.3

21.1

Returns (%)

ROCE

19.1

19.2

22.7

23.2

23.6

Angel ROIC (Pre-tax)

24.0

23.3

28.4

30.1

32.0

ROE

23.1

20.6

23.8

23.1

22.8

Turnover ratios (x)

Asset Turnover (Gross Block)

3.1

2.8

2.8

2.6

2.5

Inventory / Sales (days)

29

29

28

28

28

Receivables (days)

41

50

48

48

48

Payables (days)

52

56

54

52

51

Working capital cycle (ex-

cash) (days)

18

22

22

24

25

Solvency ratios (x)

Net debt to equity

0.4

0.3

0.1

0.0

(0.0)

Net debt to EBITDA

0.9

0.6

0.3

0.1

(0.1)

Interest Coverage (EBIT /

27.3

1,409.0

(66.9)

(48.2)

(40.2)

Interest)

October 16, 2017

19

Initiating coverage | Endurance Technologies

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager and Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking

Private Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide

registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory

authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Endurance Technologies

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

October 16, 2017

20