4QFY2016 Result Update | Automobile

February 6, 2016

Eicher Motors

ACCUMULATE

CMP

`18,128

Performance Highlights

Target Price

`20,044

Y/E December (` cr)

4QFY16* 3QCY14

% chg (yoy) 3QFY16*

% chg (qoq)

Investment Period

12 Months

Net Sales

3,317

2,294

44.6

3,123

6.2

EBITDA

517

303

70.6

493

4.9

Stock Info

EBITDA Margin (%)

15.6

13.2

240 bp

15.8

(20 bp)

Sector

Automobile

Adj. PAT

271

154

76.1

255

6.0

Market Cap (` cr)

49,226

Source: Company, Angel Research; * FY16 is a 15month period

Net Debt (` cr)

(422)

Beta

1.2

Results in line with estimates: Eicher Motors’ 4QFY2016 consolidated results have

52 Week High / Low

21,618/13,930

come in in line with our estimates. Consolidated revenues grew 45% yoy to

Avg. Daily Volume

10,398

`3,316cr, coming broadly in line with our expectation. The 2W business (Royal

Face Value (`)

10

Enfield)’s top-line grew strongly by 55% yoy to `1,284cr, driven largely by volume

BSE Sensex

24,617

growth. The VECV segment’s revenues grew 39% yoy, driven majorly by strong

demand in the commercial vehicle (CV) segment and market share gains.

Nifty

7,489

Consolidated operating margins at 15.6% were in line with our estimates of

Reuters Code

EICH.BO

15.3%. Royal Enfield posted its highest ever margins of 28.6% (a 90bp sequential

Bloomberg Code

EIM IN

improvement despite slightly lower volumes due to disruption by Chennai rains).

Royal Enfield’s margins were better than our estimate of 26.5%. The VECV

Shareholding Pattern (%)

segment’s margins at

7.4% were lower than our estimate of

8.1%. The

Promoters

54.9

consolidated net profit at `271cr was in line with our estimate.

MF / Banks / Indian Fls

7.2

Outlook and Valuation: Demand for Royal Enfield continues to remain strong on

FII / NRIs / OCBs

26.6

increasing acceptance of leisure biking in India. The company continues to have

Indian Public / Others

11.3

an order backlog with higher number of orders being taken per month than the

actual production despite huge capacity addition. Also, the company has recently

introduced the 400cc adventure tourer bike “Himalayan” which is likely to boost

Abs. (%)

3m 1yr

3yr

demand going ahead. Also, commercial vehicle (VECV) business is witnessing

Sensex

(6.4)

(14.7)

25.2

strong demand given the recovery in the CV segment. We have marginally

Eicher Motors

2.5

14.6

530.7

increased our earnings estimates given the margin beat at Royal Enfield. We

maintain our Accumulate recommendation on the stock with a revised SOTP

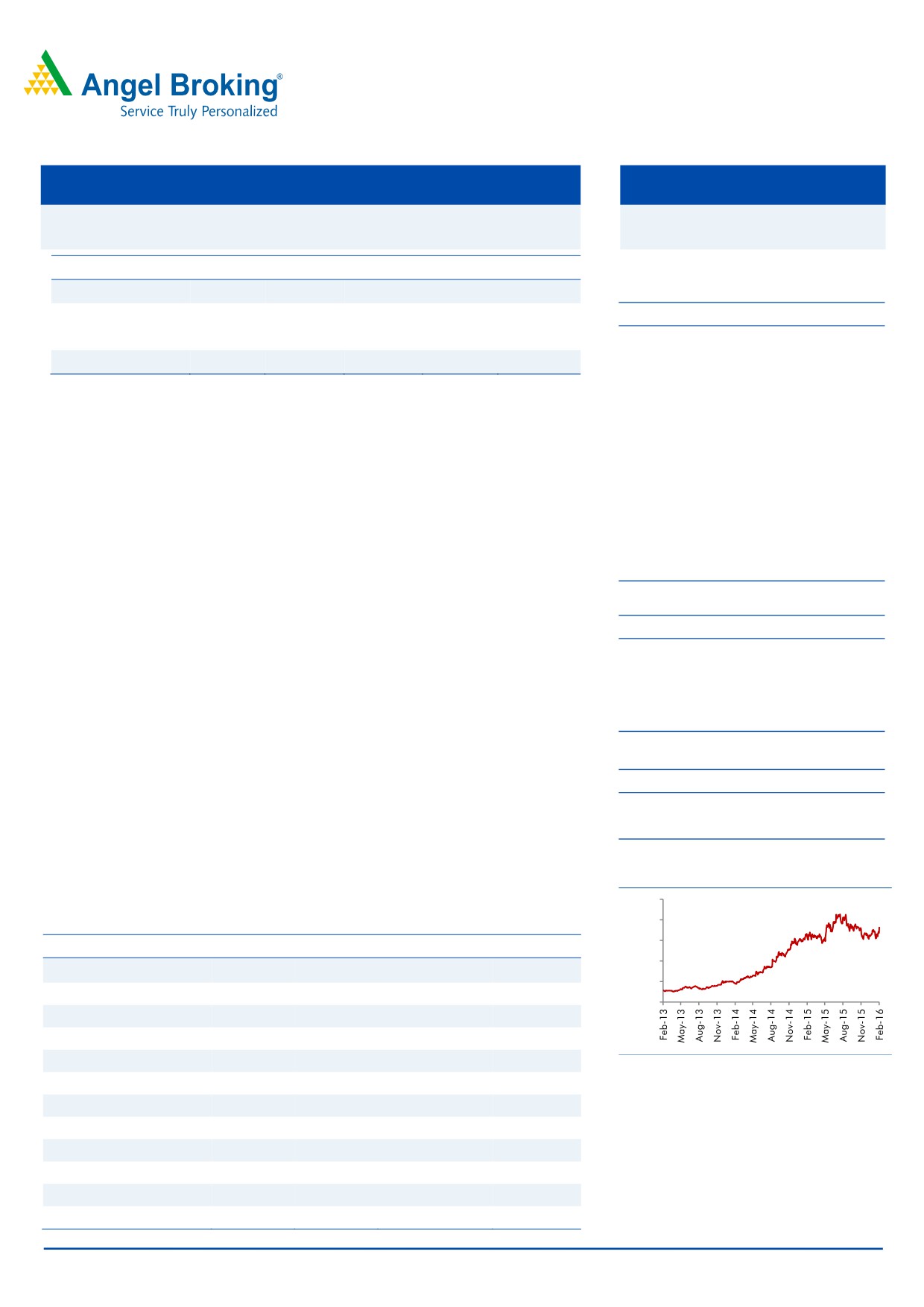

3-year price chart

based target price of `20,044.

25,000

20,000

Key financials (Consolidated)

15,000

Y/E December (` cr)

CY2013

CY2014

15MFY2016E

FY2017E

10,000

Net Sales

6,810

8,738

15,556

16,747

5,000

% chg

6.6

28.3

49.3

28.9

0

Net Profit

394

615

1,262

1,622

% chg

21.2

55.9

77.0

52.1

EBITDA (%)

10.5

12.8

15.5

17.3

Source: Company, Angel Research

EPS (`)

145.6

227.1

464.8

597.5

P/E (x)

124.5

79.8

39.0

30.3

P/BV (x)

24.2

19.7

14.2

10.5

RoE (%)

19.2

24.5

36.2

34.3

RoCE (%)

19.8

25.1

39.8

39.9

Bharat Gianani

EV/Sales (x)

7.0

5.4

3.1

2.8

022-3935 7800 Ext: 6817

EV/EBITDA (x)

66.8

42.6

19.8

16.2

Source: Company, Angel Research; Note: CMP as of February 5, 2016

Please refer to important disclosures at the end of this report

1

Eicher Motors | 4QFY2016 Result Update

Exhibit 1: Quarterly financial performance (Consolidated)

Y/E December (` cr)

4QFY16*

4QCY14

% chg (yoy)

3QFY16*

% chg (qoq)

12MFY16* CY14

% chg (yoy)

Net Sales

3,317

2,294

44.6

3,123

6.2

11,924

8,738

36.5

Consumption of RM

2,132

1,493

42.8

2,017

5.7

7,708

5,766

33.7

(% of Sales)

64.3

65.1

64.6

64.6

66.0

Staff Costs

228

167

36.3

214

6.2

830

660

25.9

(% of Sales)

6.9

7.3

6.9

7.0

7.5

Other Expenses

440

330

33.2

398

10.5

1,578

1,198

31.7

(% of Sales)

13.3

14.4

12.8

13.2

13.7

Total Expenditure

2,800

1,991

40.6

2,630

6.5

10,116

7,624

32.7

Operating Profit

517

303

70.6

493

4.9

1,807

1,115

62.1

OPM (%)

15.6

13.2

15.8

15.2

12.8

Interest

2

2

13.8

3

(23.2)

8

10

25.9

Depreciation

99

60

65.0

88

12.8

343

220

56.1

Other Income

31

15

103.9

13

143.3

84

107

(21.9)

PBT (excl. Extr. Items)

447

256

74.3

415

7.7

1,540

993

55.1

Extr. Income/(Expense)

PBT (incl. Extr. Items)

447

256

74.3

415

7.7

1,540

993

55.1

(% of Sales)

13.5

11.2

13.3

12.9

11.4

Provision for Taxation

136

75

80.6

129

5.4

471

291

61.8

(% of PBT)

30.4

29.4

31.1

30.6

29.3

PAT before MI

311

181

71.7

286

8.7

1,069

702

52.4

Minority Interest

40

27

46.6

30

31.6

126

86

46.0

Net Profit after MI

271

154

76.1

255

6.0

943

615

53.3

PATM

8.2

6.7

8.2

7.9

7.0

Equity capital (cr)

27

27

27

27

27

Reported EPS (`)

99.7

56.7

75.8

94.1

6.0

348

227

53.0

Source: Company, Angel Research; * FY16 is a 15month period

Exhibit 2: 4QFY2016 - Actual vs Angel estimates

Y/E December (` cr)

Actual

Estimates

Variation (%)

Net Sales

3,317

3,278

1.2

EBITDA

517

503

2.9

EBITDA margin (%)

15.6

15.3

30 bp

Adj. PAT

271

271

0.0

Source: Company, Angel Research

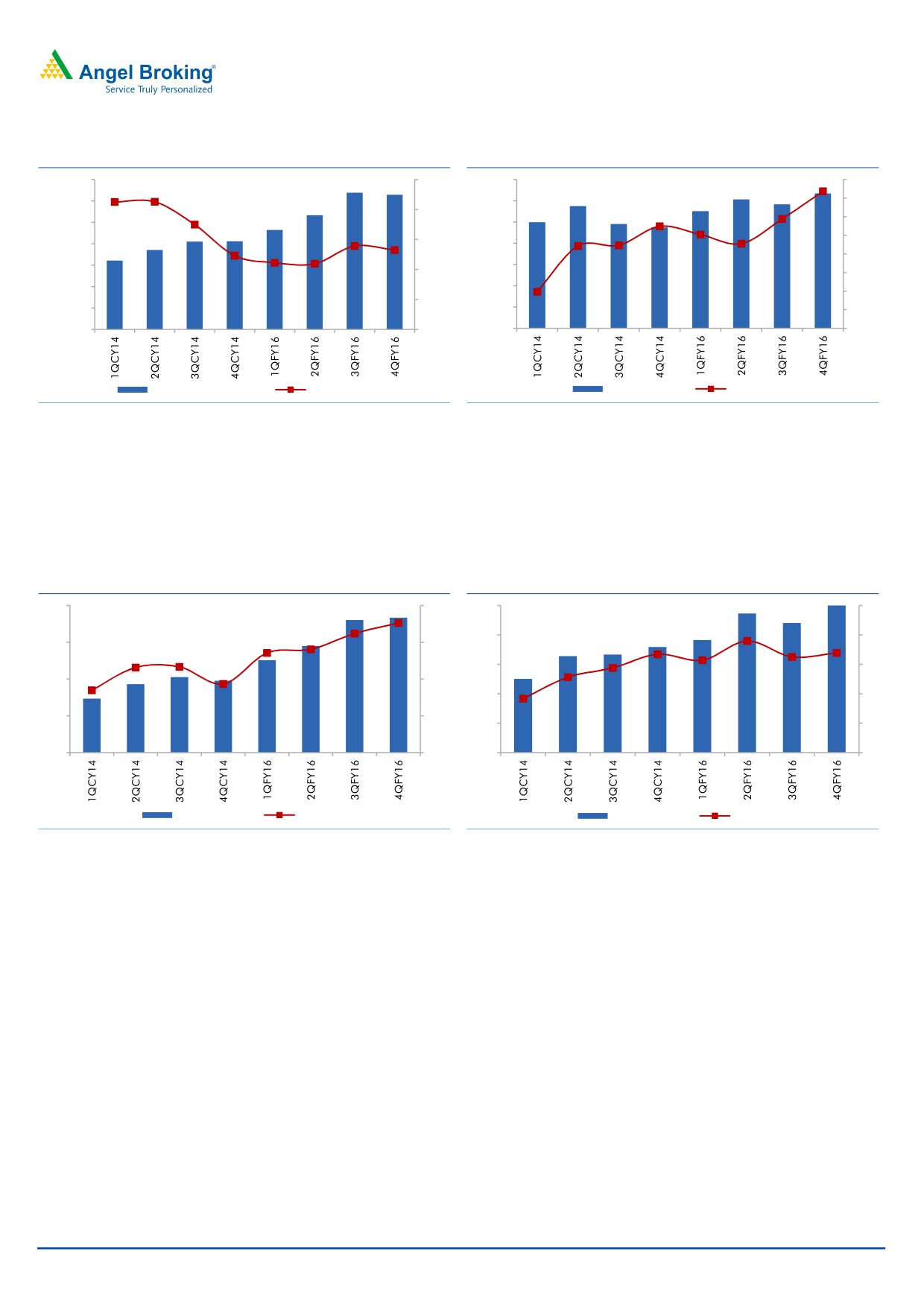

Royal Enfield continued with its robust double-digit volume growth, led by

capacity expansion as demand continues to outstrip supply. In 4QFY2016,

volumes grew 53% yoy but declined marginally by 1% on a sequential basis.

Volumes were impacted by about 11,200 units due to production disruptions

owing to floods in Chennai. The current order backlog for Royal Enfield stands

at 3-4 months.

VECV volumes continued to report healthy double-digit growth, led by

improvement in LMD and HD volumes. VECV reported the second consecutive

month of double-digit growth (volumes grew by 34% yoy).

February 6, 2016

2

Eicher Motors | 4QFY2016 Result Update

Exhibit 3: Royal Enfield growth trend

Exhibit 4: VECV growth trend

140,000

100

14,000

40

120,000

12,000

30

80

20

100,000

10,000

10

80,000

60

8,000

0

60,000

6,000

40

(10)

40,000

4,000

(20)

20

20,000

2,000

(30)

0

0

0

(40)

Royal Enfield Volumes

Growth yoy (%)

VECV volumes

Growth yoy (%)

Source: Company, Angel Research

Source: Company, Angel Research

Royal Enfield’s margins are in a constant uptrend, buoyed by a sharp jump in

volumes, tremendous pricing power and benign commodity prices. In

4QFY2016, Royal Enfield posted lifetime high margins of 28.6%.

VECV margins at 7.4% improved marginally on a yoy basis.

Exhibit 5: Royal Enfield margins at record high

Exhibit 6: VECV margins improve marginally

400

30

150

9

120

8

300

27

90

7

200

24

60

6

100

21

30

5

0

18

0

4

EBIDTA (` cr)

Margin (%)

EBIDTA (` cr)

Marign (%)

Source: Company, Angel Research

Source: Company, Angel Research

Conference call - Key highlights

The demand for Royal Enfield bikes continues to remain strong with the

company taking more orders every month as compared to sales volumes.

However, given the huge capacity increase, the waiting period for bikes has

reduced from 4-6 months earlier to 3-4 months currently.

EML has received a board approval for commencing its third manufacturing

plant for Royal Enfield, given the strong demand. Royal Enfield is targeting to

have a total capacity of 9 lakh units by CY2018, given the ramp up at the

second plant and commencement of the third unit. EML has given production

guidance of 620,000 units for CY2016 and 780,000 units for CY2017.

EML recently introduced an all new

411cc adventure bike “Himalyan”.

Himalyan has an all new engine developed by EML and would be positioned

as an mid adventure tourer bike. As per EML, this is an altogether new

segment as the current rugged off-roader bikes are in the higher cc segment.

February 6, 2016

3

Eicher Motors | 4QFY2016 Result Update

The bookings for Himalyan would commence in mid March 2016. To broaden

the product portfolio, EML would introduce another new bike in CY2017.

Royal Enfield has been expanding its dealer network in tier 2 and tier 3 cities.

It increased the dealership strength from 400 dealers in CY2014 to 500

dealers in CY2015. Royal Enfield plans to have more than 550 dealers by

CY2016.

EML is targeting export markets as a new growth driver for Royal Enfield. It is

eyeing potential in South East Asia and Latin American markets which have a

huge commuter bike base to boost exports. EML has established presence in

Thailand and Jakarta and is likely to commence exports shortly.

VECV volumes continued to improve given the uptick in the MHCV industry on

account of better freight availability and improved fleet operator sentiments

due to subdued diesel prices. VECV posted second consecutive month of

double-digit growth in 4QFY2016.

VECV lost some market share in the MHCV space due to high discounting in

the industry. VECV market share slipped marginally from 11.7% in CY2014 to

10.6% in CY2015.

Engine supplies to Volvo have been ramping up. In 4QFY2016, VECV shipped

about 4,728 units as against 2,600 units in the corresponding quarter last

year.

Royal Enfield undertook a price increase of about 1% in January 2016 while

VECV increased prices by 1.2% in November 2015.

Eicher-Polaris JV for all terrain vehicles has been progressing as per plans.

Eicher is expanding the distribution of its recently introduced “Multix” vehicle.

So far Multix has sold 650 units in the last six months.

Investment arguments

Royal Enfield demand to remain strong; ramping capacity to meet demand:

EML’s two-wheeler business (Royal Enfield) is in a demand sweet spot and is

expected to report a healthy 30% CAGR in volume over the next two years.

Royal Enfield is the direct beneficiary of pick up in the leisure biking trend.

Customers are increasingly opting for leisure bikes as an upgrade. Currently,

the segment just accounts for about 3% of the motorcycle industry and has

tremendous demand potential. EML enjoys virtual monopoly in the space

commanding a market share of 95% on back of strong brand image and

appropriate pricing which is very difficult to replicate. EML has an order backlog

of about 5 months and continues to ramp capacity to meet demand. Recently,

EML has acquired land for another plant in Chennai to boost production.

CV volumes to recover on back of improving demand cycle and new product

launches: After three consecutive years of downturn, the commercial vehicle

segment is poised to recover over the next two to three years. Better economic

growth and improvement in fleet utilization is expected to boost volumes.

Further, VECV aims to gain market share in the HCV space on back of new

product launches in technological tie up with Volvo. Also, the discounting levels

which are currently at record highs are likely to recede given the recovery in

volumes.

February 6, 2016

4

Eicher Motors | 4QFY2016 Result Update

Outlook and valuation

Demand for Royal Enfield continues to remain strong on increasing acceptance of

leisure biking in India. The company continues to have an order backlog with

higher number of orders being taken per month than the actual production despite

huge capacity addition. Also, the company has recently introduced the 400cc

adventure tourer bike “Himalayan” which is likely to boost demand going ahead.

Also, commercial vehicle (VECV) business is witnessing strong demand given the

recovery in the CV segment. We have marginally increased our earnings estimates

given the margin beat at Royal Enfield. We maintain our Accumulate

recommendation on the stock with a revised SOTP based target price of `20,044.

Exhibit 7: SOTP valuation

Particulars

Value/share

Remarks

Royal Enfield

18,188

At 35x FY17 earnings

VECV

1,856

At 12x FY17 EV/EBIDTA

Target Price

20,044

Source: Company, Angel Research

Company background

Eicher Motors Ltd (EML) manufactures commercial vehicles in collaboration with

global giant Volvo (through the subsidiary VECV) and manufactures two-wheelers

(Royal Enfield). VECV is one of the leading commercial vehicle manufacturers,

commanding a market share of about 7%. Apart from commercial vehicles, VECV

also manufactures engines for captive usage and supplies to Volvo for their global

range of trucks. VECV’s manufacturing plant is located in Pithampur, Madhya

Pradesh. Royal Enfield is the market leader in the leisure biking space, having a

market share in excess of 95%. Two-wheelers are currently manufactured at the

Chennai plant.

February 6, 2016

5

Eicher Motors | 4QFY2016 Result Update

Profit and loss statement (Consolidated)

Y/E December (` cr)

CY2011

CY2012

CY2013

CY2014 15MFY2016E

FY2017E

Total operating income

5,700

6,390

6,810

8,738

15,556

16,747

% chg

28.9

12.1

6.6

28.3

49.3

28.9

Total expenditure

5,110

5,841

6,097

7,624

13,146

13,844

Net raw material costs

4,135

4,585

4,639

5,766

10,011

10,673

Employee expenses

346

457

533

660

1,070

1,026

Other

629

798

925

1,198

2,066

2,145

EBITDA

590

549

713

1,115

2,410

2,903

% chg

54.7

(6.9)

29.9

56.3

88.1

42.0

(% of total op. income)

10.3

8.6

10.5

12.8

15.5

17.3

Depreciation & amort.

64

82

130

220

449

455

EBIT

666

603

678

1,002

2,035

2,615

% chg

55.9

(9.3)

12.4

47.8

78.5

44.5

(% of total op. income)

11.7

9.4

10.0

11.5

13.1

15.6

Interest and other charges

8

4

8

10

11

13

Other income

140

137

95

107

74

168

Recurring PBT

658

600

671

993

2,024

2,603

% chg

57.6

(8.9)

11.8

48.0

79.0

52.9

Extraordinary items

-

-

-

-

PBT (reported)

658

600

671

993

2,024

2,603

Tax

163

125

145

291

613

757

(% of PBT)

24.7

20.8

21.7

29.3

30.3

29.1

PAT before MI

496

475

525

702

1,411

1,845

% chg

61.9

1.6

10.6

33.6

71.4

54.5

(% of total op. income)

8.7

7.4

7.7

8.0

9.1

11.0

Minority Interest

189

151

131

86

149

223

Profit after MI

307

324

394

615

1,262

1,622

Basic EPS (`)

103.3

120.1

145.6

227.1

464.8

597.5

Adj. EPS (`)

103.3

120.1

145.6

227.1

464.8

597.5

% chg

46.6

16.3

21.2

55.9

77.0

52.1

February 6, 2016

6

Eicher Motors | 4QFY2016 Result Update

Balance sheet statement

Y/E December (` cr)

CY2011 CY2012 CY2013 CY2014 15MFY2016E FY2017E

SOURCES OF FUNDS

Equity share capital

27

27

27

27

27

27

Reserves & surplus

1,466

1,728

2,028

2,489

3,455

4,698

Shareholders’ Funds

1,493

1,755

2,055

2,516

3,482

4,725

Total loans

44

23

84

58

58

58

Minority Interest

838

948

1,040

1,085

1,234

1,424

Deferred tax liability

64

123

180

239

239

239

Other long term liabilities

28

18

14

17

17

17

Long term provisions

43

56

60

73

80

90

Total Liabilities

2,510

2,923

3,433

3,988

5,111

6,553

APPLICATION OF FUNDS

Gross block

989

1,526

2,299

3,137

4,337

5,337

Less: Acc. depreciation

484

534

643

828

1,277

1,732

Net Block

504

992

1,656

2,309

3,060

3,605

Capital work-in-progress

352

504

464

419

419

419

Investments

513

639

825

1,078

1,078

1,278

Long term loans and adv.

249

330

298

478

700

754

Other noncurrent assets

6

6

7

8

8

8

Current assets

2,169

2,000

2,086

2,116

3,330

4,209

Cash

1,192

804

683

481

188

839

Loans & advances

163

220

318

380

767

826

Other

815

977

1,085

1,256

2,375

2,545

Current liabilities

1,284

1,548

1,904

2,419

3,484

3,719

Net current assets

886

452

182

(303)

(153)

490

Total Assets

2,510

2,923

3,433

3,988

5,111

6,553

February 6, 2016

7

Eicher Motors | 4QFY2016 Result Update

Cash flow statement

Y/E December (` cr)

CY2011 CY2012 CY2013 CY2014 15MFY2016E FY2017E

Profit before tax

660

600

671

993

2,024

2,603

Depreciation

57

50

109

185

449

455

Change in working capital

177

46

149

283

(442)

7

Others

(196)

(58)

40

(145)

(215)

(77)

Direct taxes paid

(163)

(125)

(145)

(291)

(613)

(757)

Cash Flow from Operations

536

513

824

1,025

1,203

2,230

(Inc.)/Dec. in fixed assets

(463)

(689)

(733)

(793)

(1,200)

(1,000)

(Inc.)/Dec. in investments

(54)

(126)

(187)

(252)

-

(200)

Cash Flow from Investing

(517)

(815)

(919)

(1,046)

(1,200)

(1,200)

Issue of equity

-

-

-

-

-

-

Inc./(Dec.) in loans

(52)

(21)

61

(26)

-

-

Dividend paid (Incl. Tax)

(43)

(54)

(81)

(159)

(295)

(380)

Others

22

(10)

(5)

3

-

-

Cash Flow from Financing

(73)

(86)

(25)

(181)

(295)

(380)

Inc./(Dec.) in cash

(54)

(388)

(121)

(202)

(293)

651

Opening Cash balances

1,246

1,192

803

683

480

188

Closing Cash balances

1,192

803

683

480

188

839

February 6, 2016

8

Eicher Motors | 4QFY2016 Result Update

Key ratios

Y/E December

CY11

CY12

CY13

CY14

15MFY16E FY17E

Valuation Ratio (x)

P/E (on FDEPS)

153.7

132.2

109.0

69.9

39.0

30.3

P/CEPS

114.9

105.4

82.0

51.5

28.8

23.7

P/BV

29.2

24.8

21.2

17.3

14.2

10.5

Dividend yield (%)

0.1

0.1

0.2

0.3

0.5

0.7

EV/Sales

7.3

6.5

6.1

4.7

3.1

2.8

EV/EBITDA

70.1

75.6

58.2

37.2

19.8

16.2

EV / Total Assets

16.5

14.2

12.1

10.4

9.4

7.2

Per Share Data (`)

EPS (Basic)

103.3

120.1

145.6

227.1

464.8

597.5

EPS (fully diluted)

103.3

120.1

145.6

227.1

464.8

597.5

Cash EPS

138.2

150.6

193.7

308.2

630.2

765.1

DPS

16.0

20.0

30.0

50.0

93.0

119.5

Book Value

543.4

640.2

749.9

918.4

1,272.7

1,730.4

Returns (%)

ROCE (Pre-tax)

26.5

20.6

19.8

25.1

39.8

39.9

Angel ROIC (Pre-tax)

50.5

28.5

24.7

28.6

41.3

45.8

ROE

20.6

18.5

19.2

24.5

36.2

34.3

Turnover ratios (x)

Asset Turnover (Gross Block)

5.8

4.2

3.0

2.8

3.6

3.1

Inventory / Sales (days)

27

28

28

27

28

28

Receivables (days)

22

25

27

23

26

26

Payables (days)

76

82

94

91

71

70

WC cycle (ex-cash) (days)

(26)

(29)

(38)

(40)

(16)

(16)

Solvency ratios (x)

Net debt to equity

(0.8)

(0.4)

(0.3)

(0.2)

(0.0)

(0.2)

Net debt to EBITDA

(1.9)

(1.4)

(0.8)

(0.4)

(0.1)

(0.3)

Interest Coverage (EBIT / Int.)

86.8

159.2

86.1

102.5

184.0

209.2

February 6, 2016

9

Eicher Motors | 4QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Eicher Motors

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 6, 2016

10