IPO note | Infrastructure

July 29, 2016

Dilip Buildcon

SUBSCRIBE

sue Open: August 01, 2016

Is

A differentiated and potentially remunerative business…

Issue Close: August 03, 2016

IPO note

Company background: Dilip Buildcon Ltd (DBL) is a Bhopal based infra player

Issue Details

focused on (1) Roads & Highways construction (85% of Order Book [OB]), (2)

Face Value: `10

Irrigation (6% of OB), (3) Bridge (5% of OB) and (4) Urban Development (3% of

OB). In November 2007 it forayed into BOT-Toll & Annuity projects. Currently, it’s

Present Eq. Paid up Capital: `117.1cr

executing 64+ EPC projects and 18 BOT projects; 12 (including 11 Annuity/

Fresh Issue: 2.01 cr Shares

Annuity+Toll projects) of the 18 BOT projects are already operational.

Offer for Sale: 1.02cr Shares

Pros: (1) OB to FY2016 sales (for the standalone entity) stands at 2.6x, which

gives good revenue visibility, (2) strong NHAI and MoRTH Roads & Highways bid-

Post Eq. Paid up Capital: `136.8cr

pipeline suggests scope for OB growth, (3) superior margin profile and better

Issue size (amount): `649*-654cr**

return ratios, (4) strong earnings growth potential, (5) scope for improvement in

Price Band: `214-219

the Free Cash Flows (FCF).

Lot Size: 65 shares

Risks & Concerns: (1) Delays in execution of projects out of its home state Madhya

Post-issue implied mkt. cap:

Pradesh (MP) (accounts for 60% of its OB), (2) higher dependency on debt to fund

`2,926cr- 2,995cr

upcoming BOT projects, (3) any negative outcome of legal proceedings against

Promoters holding Pre-Issue: 90.2%

the company’s promoters.

Promoters holding Post-Issue: 75.6%

Valuation: DBL is poised to deliver healthy growth on the top-line as well as the

*At Lower end of the price band; ** At Upper end of

the price band

bottom-line front on the back of its strong order book (FY2016 OB/LTM ratio

stands at 2.6x). On the valuation front, at the higher-end of the issue price band,

Book Building

the company is available at a slight discount to its other listed road focused EPC

QIBs

50% of issue

peers on an Adj. P/E basis (on FY2016E EPS). The company reported a RoE of

22.4% in FY2016, which is among the best in the industry. Given the growth

Non-Institutional

15% of issue

prospects and the likelihood of strong FCF generation (supported by WC cycle

Retail

35% of issue

compression), this issue has the potential to deliver good returns for investors in

the near-to-medium term. Accordingly, we advise investors to SUBSCRIBE to the

issue.

Post Issue Shareholding Pattern

Key Financials (Standalone)

Promoters Group

75.6

Y/E March (` cr)

FY11

FY12

FY13

FY14

FY15

FY16

Net Sales

437

1,190

1,919

2,384

2,762

4,315

DIIs/FIIs/Public & Others

24.4

% chg

172.3

61.3

24.2

15.9

56.2

Net Profit

39

108

241

186

88

197

% chg

275.0

222.2

76.0

46.2

223.3

EBITDA (%)

21.2

22.2

24.7

22.0

24.9

23.1

EPS (`)

11

18

41

31

7

17

P/E (x)

19.7

12.0

5.4

7.0

29.3

13.0

P/BV (x)

22.7

8.7

4.8

3.6

0.0

0.0

RoE (%)

41.7

53.0

58.2

29.6

11.5

21.8

RoCE (%)

35.7

40.8

33.6

22.0

15.7

18.7

Yellapu Santosh

EV/Sales (x)

6.1

2.5

1.8

1.8

1.9

1.4

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

28.7

11.4

7.5

8.1

7.6

6.1

Source: Company, Angel Research; Note: Valuation multiples at higher- end of the price band

Please refer to important disclosures at the end of this report

1

Dilip Buildcon | IPO note

Issue Details

DBL is offering 2.99cr equity shares of `10 each via the book building route in a

price band of `214-219, consisting of fresh equity issue of 1.96cr shares and offer

for sale by Promoters and PE firm (Banyan Tree Growth Capital LLC) of 1.02cr

equity shares.

Exhibit 1: Shareholding Pattern

Pre-Issue

Post-Issue

Particulars

No. of Shares

(%)

No. of Shares

(%)

Promoter Group

10,57,14,087

90.2

10,34,41,359

75.6

Retail & HNI Investors

34,66,424

3.0

139,18,116

10.2

Institutional Investors

79,54,545

6.8

1,94,10,285

14.2

Source: Company, Angel Research

Objects of the Offer

`202cr to be utilized to pre-pay or schedule repayment of a portion of the

term loans availed.

`200cr to be utilized for funding WC requirements, and

General corporate purposes.

July 29, 201

2

Dilip Buildcon | IPO note

Company details

DBL is M.P. based Road EPC contractor focused in building Roads & Highways,

Bridges, Dams, Canals, & Water Supply Projects. Currently DBL is working on 64+

sites across 12 states with aggregate length of 8,421 lane kms. At FY2016-end,

Order book stands at `10,779cr.

In addition to EPC works, DBL also has portfolio of 18 BOT projects. Of these 12

are operational (totaling 1,683 lane kms, from Gujarat and Madhya Pradesh) and

6 are under construction stages. Notably, 16 of the 18 BOT projects are Annuity/

Annuity+Toll based projects, whereas remaining 2 are pure Toll based projects.

Exhibit 2: List of some of the large ticket projects being executed

Total Length in

Total Length of

Project

TPC

O/s OB

Appointment

Completion

Project Name

Single Lane (km)

the Road (km)

Type

(` in cr)

(` in cr)

Date

Date

(where applicable)

(where applicable)

Gwalior- Shivpuri

Road

962.9

395.8

Feb-2012

Jun-2016

125.3

501.2

Vijayawada-

Road

740.7

740.7

Jan-2016

Jan-2018

64.6

258.4

Machilipatnam

Mahulia- Baharagora

Road

674.1

674.1

Feb-2016

Feb-2018

71.6

286.4

Amritsar- Taran-taran-

Road

558.0

479.7

Sep-2015

Sep-2017

45.9

183.7

Harike section

Goa-Zuari Cable-Stayed

Bridge

545.4

545.4

Feb-2016

Feb-2019

Not applicable

Not applicable

Bridge

Kerala Border to Kollegal Road

419.4

129.3

May-2014

Jun-2016

129.3

258.6

Mohanpura Major

Irrigation

415.8

195.7

Mar-2014

Mar-2018

-

-

Multipurpose

Source: Company, Angel Research

July 29, 201

3

Dilip Buildcon | IPO note

Investment rationale

Order book/LTM sales at 2.6x… gives strong revenue visibility…

DBL has grown its order book from `2,601cr in FY12 to `10,779cr in FY2016,

mainly led by order wins from the Road segment. Till FY2012, DBL was pre-

dominantly MP-based road EPC player. In last 4 years, DBL diversified and is now

present across 12 states. In last 3 years, NHAI and MoRTH order wins helped DBL

grow its order book.

Dilip Buildcon at FY2016-end is sitting on order book of `10,779cr, which is 2.6x

its FY2016 revenues (LTM). Given that road projects awarded by NHAI and MoRTH

have 2-2.5 year’s execution, OB of DBL gives strong near-to-medium term revenue

growth visibility.

Exhibit 3: OB grows 4.1x during FY2012-16

Exhibit 4: Segment-wise Order book split

12,000

3.5x

Bridge

10,779

2.9x

5%

Mining

3.0x

1%

10,000

2.6x

BOT

2.2x

7,475

2.5x

8,000

15%

1.7x

2.0x

Urban Dev.

1.6x

6,000

5,161

3%

1.5x

Irrrigation

4,000

3,320

2,601

1.0x

6%

EPC - Road

2,000

0.5x

70%

0

0.0x

FY2012

FY2013

FY2014

FY2015

FY2016

Order Book (` in cr)

OB/LTM sales (x)

Source: Company, Angel Research

Source: Company, Angel Research

Notably, 63% of the current Order book is from the Road EPC works awarded by

NHAI and MoRTH.

EPC business enjoys strong Margin profile & better Return ratios

DBL follows differentiated approach towards its EPC business, which resulted in the

company reporting superior margins vs. its peers.

Exhibit 5: Reported strong EBITDA% during FY2012-16

Exhibit 6: Industry vs. DBL % reconciliation...

9,000

26.0

24.7

25%

8,000

20.0%

24.0

7,000

20%

21.3

15.0%

6,000

22.0

20.3

15%

5,000

19.6

19.0

20.0

4,000

10%

3,000

18.0

5%

2,000

1.6%

1.8%

1.7%

16.0

1,000

+

+

+

=

0%

0

14.0

Ind. Peer %

Sub-Cont.

Early Bonus

Opr. Levers

DBL %

2012

2013

2014

2015

2016

(RM, Equip.

EBITDA (` in cr)

EBITDA %

Fleet)

Source: Company, Angel Research

Source: Company, Angel Research

July 29, 201

4

Dilip Buildcon | IPO note

DBL historically has reported above industry average EBITDA margins of

19.0-24.7% during FY2012-16. Proper due-diligence, well defined systems in

place, has helped DBL historically complete many of its projects ahead of

schedule. As a result, DBL received 1.8% of total sales during FY2012-16 as early

completion bonus. DBL does not follow the strategy of sub-contracting as a result it

leads to cost savings thereby adding ~1.5-1.6% to margins. In absence of sub-

contracting strategy, DBL follows the strategy of using its in-house efficient

Equipments fleet, rather than depending on ‘leasing of equipments’ strategy. Also,

DBL resorts to bulk purchase of raw materials, taking nearby quarries on lease

from medium term perspective. All these initiatives help DBL save 4.8-5.0% on

EBITDA margins. This explains for the superior EBITDA margins of the company vs.

its peers.

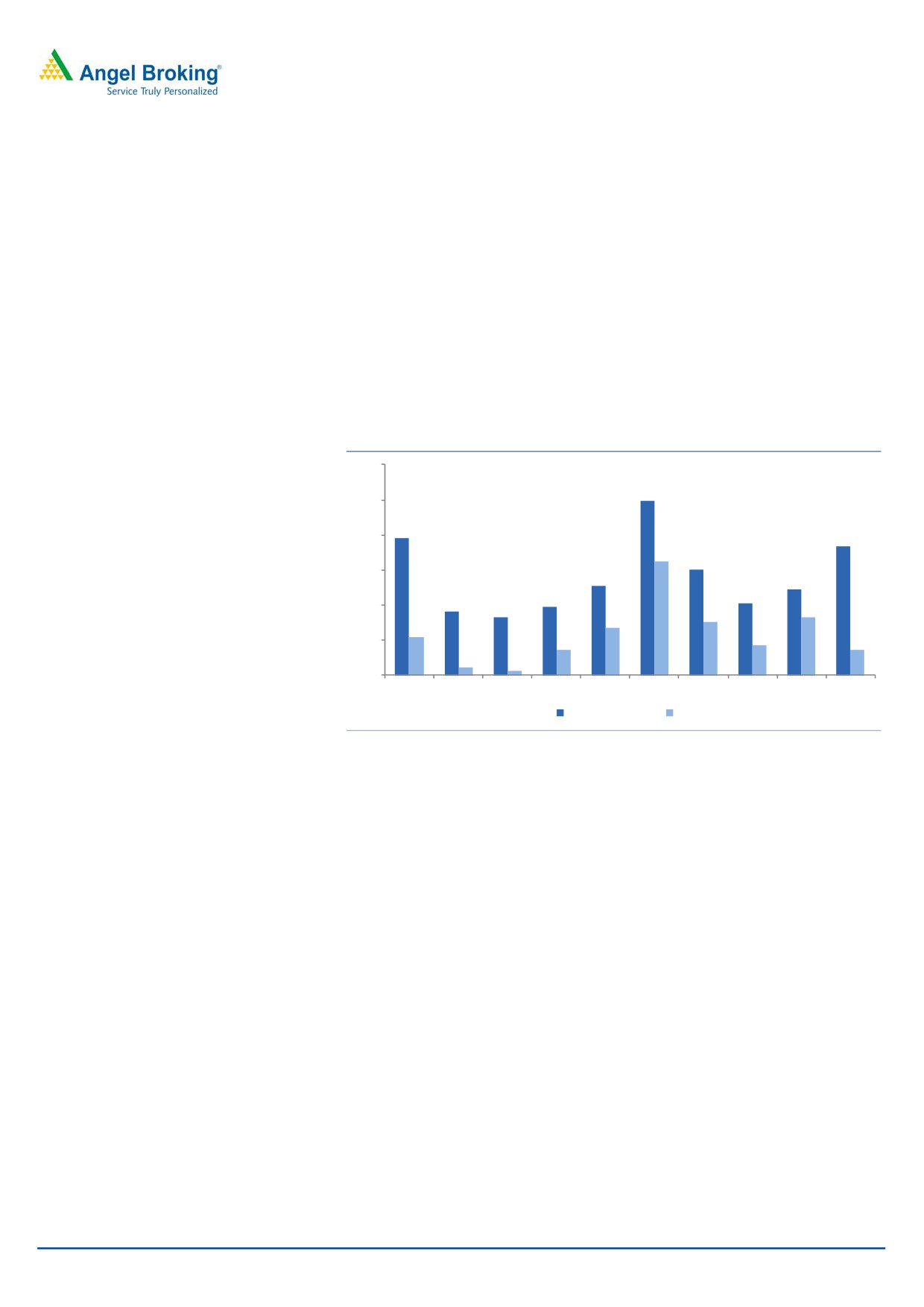

Exhibit 7: Enjoys superior margin profile to most of its peers...

30

24.8

25

19.6

20

18.4

16.2

15.1

15

12.7

12.3

9.7

10.2

9.1

10

8.2

8.3

7.6

6.8

5.4

4.2

3.7

3.6

5

1.1

0.7

0

DBL

Simplex

NCC MBL Infra. Ahluwalia KNR Con. J Kumar Sadbhav ABL (std.) ITNL (std.)

Infra.

FY2016 EBITDA %

FY2016 PAT %

Source: Company, Angel Research

Large fleet size of 7,345 vehicles held by DBL resulted in higher depreciation. As a

result, PAT margins of the company are lower than peers, despite the strong

EBITDA margin profile. DBL reported PAT margin of 5.4% in FY2016.

Scope for earnings growth potential during FY2016-18E…

We see multiple levers for DBL (standalone), which could help it report strong

earnings growth during FY2016-18E. DBL is currently having an Order Book of

`10,779cr (OB to LTM sales ratio stands at 2.6x). Considering 2-3 years for

execution of these road projects, we expect DBL to report ~20% top-line CAGR

during FY2016-18E.

On lowering EBITDA margin assumptions (to factor non-receipt of early completion

bonus), we expect DBL to report 15.7% EBITDA CAGR during FY2016-18E.

DBL at FY2016-end invested `1,465cr towards Plant & Machinery. With sales

growth outpacing incremental capex growth (`100cr for FY2017-18 each), there

exists scope for improvement in the asset leverage.

DBL at FY2016-end reported WC as % of sales ratio at 37.6%. DBL is expected to

use `200cr raised from IPO proceeds towards working capital funding. Stretch in

WC cycle for most of the BOT players is owing to SPV funding through short-term

loans and advances, whereas, DBL’s working capital stretch is owing to funding of

July 29, 201

5

Dilip Buildcon | IPO note

Inventory and Accounts Receivable. With improvement in collections cycle, we

expect 200-300 bps improvement in WC as % of sales ratio, going forward. DBL is

expected to use `202cr of IPO proceeds towards re-payment of term loans. We

expect future growth to be partly funded by debt, which on the back of improved

credit rating would be at cheaper rates. On a whole, we expect DBL to re-finance

its high cost debt with low cost debt. Accordingly, we see yearly `2cr of savings for

every 1% reduction in interest rate.

Scope for improvement in the Free Cash Flows…

Even though DBL (standalone) has generated healthy margins in the past, Free

Cash Flows (FCF) have been negative during FY2012-FY16, reflecting continuous

increase in the working capital requirements, higher interest costs (due to increase

in debt) and additions to gross block. Interestingly, DBL has been able to reduce

the Receivable days from 167 days in FY2015 to 111 days in FY2016, on the back

of (1) improvement in collection cycle for government orders and (2) resumption of

works at 2 of the delayed projects. Also, improvement in (1) government order

collection’s cycle and (2) inventory days should help in release of over `1,000cr in

FY2017E. Improved Cash flow from Operations (CFO) when coupled with lower

estimated capex of `100cr for FY2017-18, each should lead to improvement in

FCF during FY2017-18E. Strong FCF potential should help DBL in funding equity

requirement of its upcoming BOT projects (`650cr equity is required for next 3

years).

Exhibit 8: Working Capital Cycle to improve...

Exhibit 9: Cash Flow from Operations (` cr)

180

167

7,000

6,510

162

160

140

6,000

136

140

120

119

113

111

5,000

120

105

100

90

4,000

80

70

3,000

53

60

2,000

40

1,000

427

20

220

0

0

FY13

FY14

FY15

FY16

FY13

FY14

FY15

FY16

Inventory days

Receivables days

Payables days

(1,000)

(53)

Source: Company, Angel Research

Source: Company, Angel Research

Consol. D/E Ratio to decline post the IPO…

DBL (consol.) at FY2016 had debt of `3,221cr, reflecting D/E ratio of 3.2x. DBL is

expected to use `200cr of the IPO proceeds towards Working capital funding and

remaining `202cr towards Term loan repayments. Accordingly, consol. D/E ratio

would decline to ~2.0x.

Currently 12 of 18 BOT projects are operational (11 being Annuity/Annuity+Toll;

all 12 of them are 100% owned). Debt o/s at FY2016-end, towards these project

stands at `1,150cr. These projects reported FY2016 Annuity income of `207cr and

~`20cr of Toll Income. With ~90% EBITDA margins across these projects, there

exists strong case for the SPVs to repay ~`200cr yearly towards debt and interest

re-payments.

July 29, 201

6

Dilip Buildcon | IPO note

With equity raised from IPO being used to lower debt, when coupled with SPV level

debt repayments should lead to consol. Level D/E ratio declining, in the near-term.

However, with funding of BOT projects in the pipeline, should lead to gradual

increase in the consol. D/E ratio.

Mature Annuity Portfolio…augurs well for DBL

DBL entered the BOT space in Nov-2007, and currently has 18 BOT projects in its

portfolio. Of this 12 are already operational (with total investments of `1,571cr)

and 6 are under construction. 11 of 12 BOT projects have Annuity/ Annuity+Toll

model. Again 11 of these operational projects are awarded by Madhya Pradesh

Road Development Corporation (MPRDC). DBL recently won `1,012.9cr Guna-

Biora BOT project, first large ticket project from NHAI.

The Annuity portfolio gives assured cash flows and insulates the business from any

traffic related risks. Further, we are of view that the operational BOT projects have

reasonable IRRs. To-date, DBL has invested `370cr equity towards these 12 BOT

projects (accounts for 37% of consol. networth). These assets in FY2016 earned

Annual Income of `370cr and Toll income of `20cr. Notably, weighted average

Residual life of operational BOT projects is 12.1 years. This indicates that DBL’s

(current) operational Annuity projects have potential to collect yearly Annuity

Income of `2,500cr and Toll Income of `250+cr for remaining life of the asset.

July 29, 201

7

Dilip Buildcon | IPO note

Exhibit 10: BOT Projects Operational

Annual

Capital

Concession

TPC Length COD/ Residual

Project Company

Project

Type

Counterparty

Annuity

Inv.

period

(` in cr)

(km) PCOD Life (Yrs)

(` in cr)

(` in cr)

(Yrs)

DBL Nadiad Modasa

R & BD

Nadiad- Modasa

Annuity

35

29

14

208

108 Dec-13

10.3

Tollways Ltd.

GOG

DBL Bankhlafata

Bankhlafatta-

Dogawa Tollways

Annuity

MPRDC

20

16

15

116

65 Mar-14

12.4

Dogawa

Ltd.

DBL Jaora-Sailana

Jaora-Piploda

Annuity

MPRDC

24

20

15

134

88 May-14

12.3

Tollways Ltd

Suryavanshi

Infrastructure Private

Mandsaur- Sitamau Toll

MPRDC

-

6

25

35

44 Feb-09

16.6

Ltd.

DBL Sardarpur

Sardarpur-

Annuity

Badnawar Tollways

MPRDC

9

10

15

98

43 Jun-12

10.7

Badnawar

+ Toll

Ltd.

DBL Silwani

Annuity

Sultanganj Tollways

Silwani- Sultanganj

MPRDC

19

21

15

129

76 Mar-13

10.9

+ Toll

Ltd

DBL Sitamau-

Annuity

Suwasara Tollways

Sitamau- Suwasara

MPRDC

7

8

15

60

35 Mar-13

11.1

+ Toll

Ltd

DBL Mundi-

Annuity

Sanawad Tollways

Mundi- Sanawad

MPRDC

17

21

15

141

68 May-13

11.0

+ Toll

Ltd.

DBL Uchera- Nagod

Annuity

Uchera- Nagod

MPRDC

17

32

15

114

56 May-14

11.7

Tollways Ltd.

+ Toll

DBL Ashoknagar-

Annuity

Ashoknagar- Vidisha

MPRDC

10

20

15

85

36

Jul-14

12.6

Vidisha Tollways Ltd.

+ Toll

DBL Tikamgarh-

Tikamgarh (Dhajrai)

Annuity

Nowgaon Tollways

Jatara-Palera

MPRDC

18

26

15

130

76 May-15

13.4

+ Toll

Ltd.

Nowgaon

DBL Betul- Sarni

Betul Sarni

Annuity

MPRDC

31

81

15

322

124 May-15

13.0

Tollways Ltd.

Junnardeo- Parasia

+ Toll

Source: Company, Angel Research

Another `650cr of equity investments is

required for 6 BOT projects under

construction phase in the next 3 years.

Exhibit 11: BOT Projects Under Construction

Annual

Concession

TPC

Length

Counter-

Scheduled Residual

Project Company

Project

Type

Annuity

period

(` in

(km)

party

COD#

Life

(` in cr)

(Yrs)

cr)

(approx)

DBL Hata-Dargawan

Annuity +

Hata Fatehpur

MPRDC

14

15

87

64

Apr-18

15

Tollways Ltd.

Toll

Jalpa Devi

Guna-Biora

Toll

NHAI

Nil

26

715

94

Awaited

Awaited

Tollways Ltd.

DBL Patan Rehli

Annuity +

Patan-Tendukeda- Rehli

MPRDC

35

15

225

87

Apr-18

15

Tollways Ltd.

Toll

DBL Mundargi

Mundargi - Hadagali -

Harapanahalli

Annuity

KRDCL

35

10

157

51

Awaited

Awaited

Harapanahalli

Tollways Ltd.

DBL Hassan

Hassan - Ramanathapura -

Periyapatna

Annuity

KRDCL

53

10

220

74

Awaited

Awaited

Periyapatna

Tollways Ltd.

DBL Hirekerur

Ranibennur

Hirekerur - Ranibennur

Annuity

KRDCL

39

10

174

56

Awaited

Awaited

Tollways Ltd.

Source: Company, Angel Research

July 29, 201

8

Dilip Buildcon | IPO note

Risks & Concerns

1. DBL has entered 12 states and is executing 64+ projects in different states.

Madhya Pradesh currently accounts for 40% of its Order Book. With major

chunk of orders being executed outside the state, there exists scope for decline

in the margins on account of project execution delays.

2. DBL has guided for equity commitment of `650cr over the next 3 years for

construction of 6 BOT projects. We expect this requirement to be met by

internal accruals. Any inability to improve its free cash flow generation

potential could lead to increased dependency on the debt funding, which

in-turn could lead to Balance Sheet pressure.

3. There are few legal proceedings outstanding against DBL’s promoters, some

of the directors. Any negative outcome of these legal proceedings could affect

the growth prospects of the company.

July 29, 201

9

Dilip Buildcon | IPO note

Outlook and Valuation

During FY2012-16, DBL (standalone entity) reported 36.2% top-line and 22.1%

bottom-line CAGR, respectively. PAT CAGR during the same period was restricted

on account of higher depreciation and interest expenses. In order to grow its

financials during the same period, DBL built EPC order book by taking up NHAI,

MoRTH EPC projects and other state govt. BOT projects in its portfolio. With huge

pipeline of NHAI & MoRTH projects likely to be awarded in FY2017-18E, there

exists scope for new order inflows.

We expect the OB of DBL to report healthy 15.5% CAGR during FY2016-18E, from

the current level of `10,779cr. The Management has indicated that all projects are

running as per schedule while some of these are even ahead of schedule. On a

conservative basis, we are not factoring in any early project completion bonus for

the company going forward and hence expect FY2017-18E EBITDA margins to be

at ~18% levels. Further with improving fixed asset leverage, we expect the

standalone entity to report a 23.4% CAGR in profitability during FY2016-18E.

Considering DBL’s higher dependency on the Roads & Highways vertical, and

given its business mix and balance sheet size, we are considering 6 EPC players for

the purpose of peer group comparison.

To value the EPC business (capturing standalone business) on FY2016E numbers,

we adjusted the value of BOT projects from their current market price.

Exhibit 12: Peer group comparison

Particulars

FY16

Revenues

EBITDA Adj. PAT EBITDA (%) PAT (%) OB/LTM RoE (%)

Adj. P/E

CMP

M-Cap

(` in cr)

D/E (x)

FY16

FY16

FY16

FY16

FY16

(x)

FY16

FY16 (x)

DBL

219

1,327

2.0

4,085

799

220

19.6

5.4

2.6

22.4

7.8

Simplex Infra.

306

1,515

2.1

5,773

528

66

9.1

1.1

2.4

10.9

22.9

MBL Infra.

135

560

1.2

2,314

225

85

9.7

3.7

1.8

12.9

3.4

Ahluwalia Cont.

290

1,943

0.3

1,247

158

84

12.7

6.8

3.3

11.9

23.1

KNR Const.

592

1,666

0.2

993

246

161

24.8

16.2

3.5

22.2

8.1

J Kumar Infra.

218

1,647

0.3

1,366

206

103

15.1

7.6

2.3

8.0

15.9

PNC Infra.

563

2,885

0.0

2,014

266

243

13.2

12.1

2.9

17.8

9.9

Average

0.7

14.1

7.9

2.7

14.0

13.9

Source: Company, Angel Research; Note: Valued PowerMech is valued using post IPO shares o/s

At FY2016E EPS, DBL would trade at 7.8x its Adj. P/E multiple assuming that it lists

at the higher end of the issue price band. In our view, at such a valuation DBL

would trade at a discount to some of its peers and also lower than the peer

group’s average of 13.9x.

Considering the standalone entity’s attractive valuation and adding-up value of 12

operational BOT projects (valued at BV of 1.0x, adds up to `27/share), the issue

leaves space for an upside in the stock price, once listed. On looking at possible

catalysts, like (1) standalone entity’s growth potential (higher awarding from the

NHAI and MoRTH), and (2) the company’s strong margin and return profile, the

issue has the potential to generate good returns in the near-to-medium term.

Accordingly, we recommend SUBSCRIBE to the IPO.

July 29, 201

10

Dilip Buildcon | IPO note

Profit & Loss Statement (Consolidated)

Y/E March (` cr)

FY11

FY12

FY13

FY14

FY15

FY16

Net Sales

437

1,190

1,919

2,384

2,762

4,315

% Chg

172.3

61.3

24.2

15.9

56.2

Total Expenditure

344

926

1,446

1,859

2,075

3,320

Cost of Raw Materials Consumed

252

593

840

1,097

1,271

2,060

Change in Inventories of WIP

78

313

523

659

675

984

Employee benefits Expense

8

11

22

25

38

73

Other Expenses

6

9

61

77

91

203

EBITDA

93

264

473

525

687

996

% Chg

283.8

178.3

109.9

129.8

144.0

EBIDTA %

21.2

22.2

24.7

22.0

24.9

23.1

Depreciation

19

44

76

100

206

284

EBIT

76

223

405

442

487

745

% Chg

292.0

180.5

108.2

109.1

151.9

Interest and Financial Charges

17

59

115

201

354

514

Other Income

2

3

7

18

7

34

PBT

59

164

290

242

133

231

Tax

20

56

48

56

46

34

% of PBT

33.5

34.2

16.7

23.2

34.2

14.8

PAT before Exceptional item

39

108

241

186

88

197

Exceptional item

0

0

0

0

0

0

PAT

39

108

241

186

88

197

Minority Interest

(0)

(0)

0

0

0

0

PAT after Minority Interest

39

108

241

186

88

197

% Chg

275.0

222.2

76.0

46.2

223.3

PAT %

9.0

9.1

12.6

7.8

3.2

4.6

EPS (on pre-IPO shares o/s)

11.11

18.25

40.73

31.35

7.48

16.79

% Chg

163.3

222.2

76.0

22.9

223.3

July 29, 201

11

Dilip Buildcon | IPO note

Balance Sheet (Consolidated)

Y/E March (` cr)

FY11

FY12

FY13

FY14

FY15

FY16

Sources of Funds

Equity Capital

35

59

59

59

117

117

Reserves Total & Minority Int.

78

236

476

660

688

884

Networth

113

295

535

719

805

1,001

Total Debt

139

547

1,035

1,741

2,950

3,221

Other Long-term Liabilities

65

52

134

198

224

238

Deferred Tax Liability

6

14

15

36

75

101

Total Liabilities

323

908

1,718

2,694

4,054

4,562

Application of Funds

Net Block & Capital WIP

261

691

1,204

1,772

2,608

2,773

Goodwill

0

0

0

0

0

0

Current Assets

Inventories

64

197

363

522

948

1,580

Sundry Debtors

118

261

573

1,002

1,263

1,262

Cash and Bank Balance

48

96

55

73

267

116

Loans & Advances

55

66

130

103

197

366

Other Current Asset

0

0

0

0

0

0

Current Liabilities

224

497

677

874

1,538

1,825

Net Current Assets

62

123

444

826

1,136

1,499

Other Assets & Loans & Adv.

0

93

70

96

310

289

Total Assets

323

908

1,718

2,694

4,054

4,562

July 29, 201

12

Dilip Buildcon | IPO note

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY11

FY12

FY13

FY14

FY15

FY16

Profit before tax

59

164

290

242

133

231

Dep. & Other Non-cash Charges

19

43

75

98

212

287

Change in Working Capital

61

(138)

(262)

(281)

(255)

(430)

Interest & Financial Charges (net)

15

56

113

198

351

493

Direct taxes paid

(20)

(29)

(44)

(80)

(65)

(59)

Cash Flow from Operations

134

96

172

177

376

522

(Inc)/ Dec in Fixed Assets

(126)

(474)

(588)

(668)

(1,042)

(450)

(Inc)/ Dec in Investments

2

3

3

4

3

21

Cash Flow from Investing

(125)

(472)

(586)

(664)

(1,038)

(429)

Issue/ (Buy Back) of Equity

0

75

0

0

0

0

Inc./ (Dec.) in Loans

38

408

488

706

1,209

271

Dividend Paid (Incl. Tax)

(18)

(60)

(115)

(201)

(353)

(515)

Net Interest Expenses

0

0

0

0

0

0

Cash Flow from Financing

20

423

373

505

856

(244)

Inc./(Dec.) in Cash

30

48

(41)

18

194

(151)

Opening Cash balances

19

48

96

55

73

267

Closing Cash balances

48

96

55

73

267

116

July 29, 201

13

Dilip Buildcon | IPO note

Ratio Analysis (Consolidated)

Valuation Ratio (x) (on higher-band)

FY11

FY12

FY13

FY14

FY15

FY16

P/E (on FDEPS)

19.7

12.0

5.4

7.0

29.3

13.0

P/CEPS

44.2

16.9

8.1

9.0

8.7

5.3

Dividend yield (%)

0.0

0.0

0.0

0.0

0.0

0.0

EV/Sales

6.1

2.5

1.8

1.8

1.9

1.4

EV/EBITDA

28.7

11.4

7.5

8.1

7.6

6.1

EV/Total Assets

4.9

2.1

1.5

1.2

0.9

1.0

Per Share Data (`)

EPS (Adj.)

0.0

0.0

0.0

0.0

0.0

14.4

Cash EPS

5.0

13.0

27.1

24.4

25.1

41.0

DPS

0.0

0.1

0.1

0.1

0.1

0.0

Book Value

10

25

46

61

69

85

Returns (%)

RoCE (Pre-tax)

35.7

40.8

33.6

22.0

15.7

18.7

Angel RoIC (Pre-tax)

42.3

47.0

35.8

22.7

16.6

19.6

RoE

41.7

53.0

58.2

29.6

11.5

21.8

Turnover ratios (x)

Asset Turnover (Gross Block) (x)

1.1

1.2

1.0

0.8

0.6

0.7

Inventory (days)

27

40

53

68

97

107

Receivables (days)

74

58

79

121

150

107

Payables (days)

106

111

112

119

159

142

Leverage Ratios (x)

D/E ratio (x)

1.2

1.9

1.9

2.4

3.7

3.2

Interest Coverage Ratio (x)

4.4

3.8

3.5

2.2

1.4

1.4

July 29, 201

14

Dilip Buildcon | IPO note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

July 29, 201

15