4QFY2016 Result Update | Cons. Durables

June 3, 2016

Blue Star

BUY

CMP

`415

Performance Highlights

Target Price

`495

Y/E March (` cr)

4QFY2016 4QFY2015

% chg (yoy) 3QFY2016

% chg (qoq)

Investment Period

12 Months

Net Sales

1,103

1,005

9.8

686

60.9

EBITDA

57

69

(17.4)

28

104.9

Stock Info

EBITDA margin (%)

5.2

6.9

(170)bp

4.1

111bp

Adj. PAT

24

68

(64.8)

7

253.9

Sector

Cons. Durable

Source: Company, Angel Research (Standalone)

Market Cap (` cr)

3,733

Blue Star’s standalone numbers for 4QFY2016 were subdued on the margin and

Net Debt

87

bottom-line front mainly on account of the company having to provide for the last

Beta

0.6

leg of the legacy orders. Sans the provision for legacy orders, the operating

profile was in-line with our estimates. The top-line grew by 9.8% yoy while the

52 Week High / Low

444 / 306

margin contracted by 170bp yoy to 5.2%. The company over the past two years

Avg. Daily Volume

11,723

has carried out multiple restructuring initiatives which include transferring its PEIS

Face Value (`)

2

business to its wholly owned subsidiary and amalgamating its associate Blue Star

Infotech (BSIL) with itself. There was net exceptional income of `48cr arising from

BSE Sensex

26,843

profit on sale of IT business of BSIL, as well as cost update on major contracts.

Nifty

8,221

Also owing to BSIL’s merger, the depreciation expense was significantly higher.

Reuters Code

BLUS.BO

Adjusting for the exceptional item, the net profit for the quarter came in at `24cr.

Bloomberg Code

BLSTR IN

Improvement in macro scenario to support growth: The Cooling/Unitary Products

Division (CPD/UPD) has been the key performer for the company, largely due to

its room air conditioning (RAC) business. The RAC business has been outgrowing the

industry by ~10% points over the last few quarters, resulting in the company

Shareholding Pattern (%)

consistently gaining market share from ~7% in FY2014 to 10.5% at present. Various

Promoters

39.5

industry players as well as the company Management have upgraded the FY2017

MF / Banks / Indian Fls

22.5

growth guidance for the industry from 12-15% earlier to 20% now which augurs well

FII / NRIs / OCBs

10.6

for the division. The company has also forayed into other products such as air coolers,

water purifiers and air purifiers which should drive growth for the division. As for

Indian Public / Others

27.4

Electro Mechanical Projects and Packaged Air-conditioning Systems (EMPPAC)

division, the order book is now clean and order inflow has started to pick up but

execution is a near term monitorable. We expect the gradual improvement in the

Abs.(%)

3m 1yr 3yr

macro scenario to drive the performance of the division.

Sensex

10.7

(1.3)

36.9

Outlook and valuation: We have upgraded our numbers to factor in higher

BLUESTAR

25.9

22.1

149.3

revenue guidance for the RAC business as well as improvement in performance of

the EMPPAC division. As reported in our earlier report(s), the merger with BSIL has

improved the balance sheet strength of the company by way of cash infusion which the

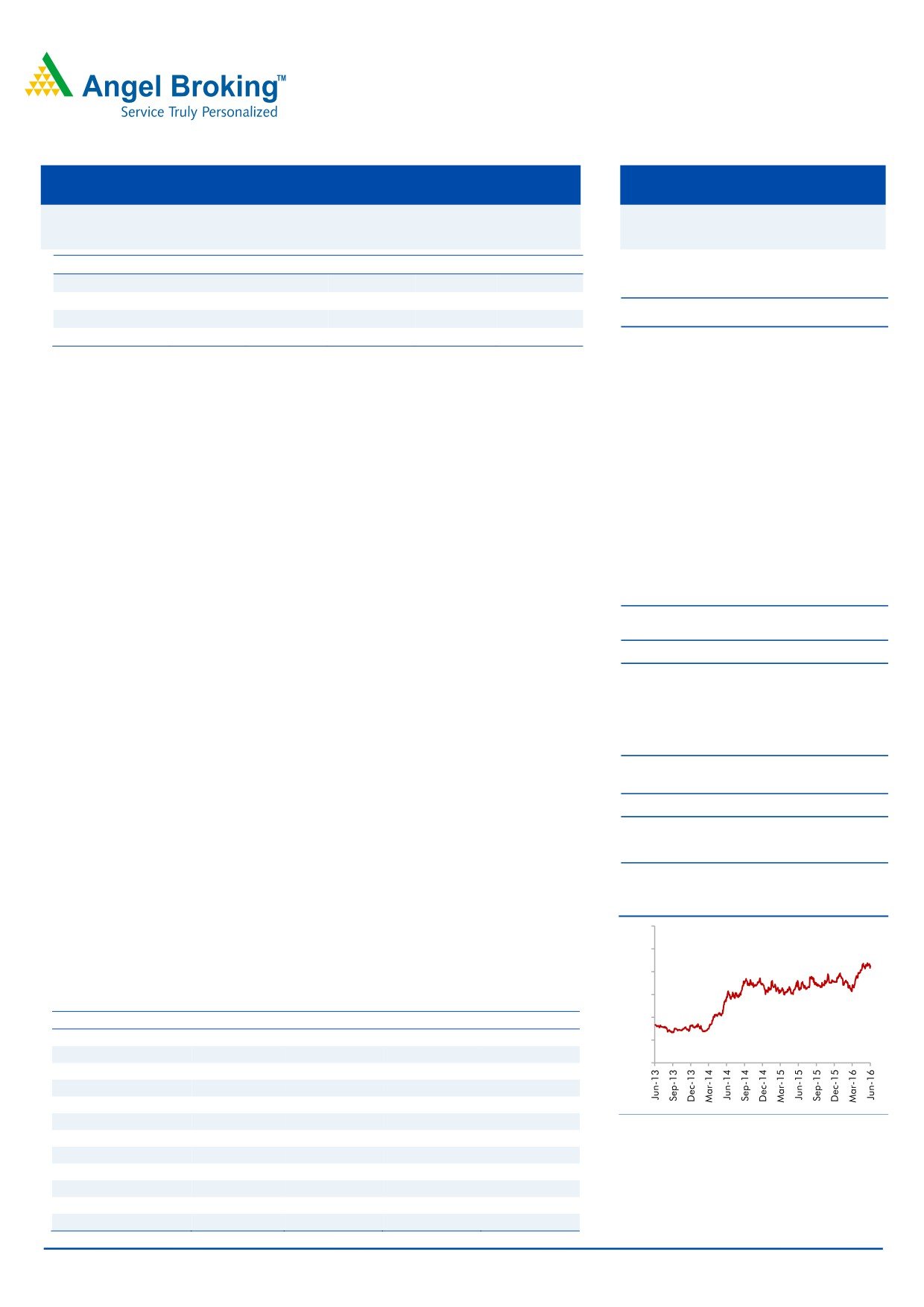

3 Year Price Chart

company will utilize to grow the UPD division as well as the exports of the company. At

600

the current market price, the stock trades at 20.1x its FY2018E earnings and at 0.8x

500

FY2018E EV/sales (while its close peer Voltas trades at 1.4x its FY2018E EV/sales). We

400

maintain our BUY recommendation on the stock with a target price of `495.

300

Key financials (Consolidated)

200

Y/E March (` cr)

FY2015

FY2016E

FY2017E

FY2018E

Net Sales

3,182

3,770

4,351

5,024

100

% chg

8.4

18.5

15.4

15.5

-

Net Profit

96

103

164

197

% chg

23.1

7.5

59.3

20.2

EBITDA (%)

5.3

5.7

6.4

7.1

EPS (`)

10.6

11.4

17.2

20.6

P/E (x)

39.0

36.3

24.2

20.1

P/BV (x)

8.2

5.6

5.2

4.5

RoE (%)

20.5

18.4

23.1

24.1

RoIC (%)

16.6

22.2

28.4

32.2

Milan Desai

EV/Sales (x)

1.3

1.1

0.9

0.8

+91 22 3935 7800 Ext: 6846

EV/EBITDA (x)

24.4

18.7

14.4

11.3

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Blue Star | 4QFY2016 Result Update

Exhibit 1: 4QFY2016 performance highlights (Standalone)

Y/E March (` cr)

4QFY2016

4QFY2015

yoy chg (%)

3QFY2016

qoq chg (%)

FY2016

FY2015

% chg

Net Sales

1,103

1005

9.8

686

60.9

3,414

3,081

10.8

Net raw material

813

720

12.9

472

72.2

2,427

2,134

13.8

(% of Sales)

73.7

71.6

205bp

68.9

482bp

71.1

69.3

184bp

Staff Costs

71

69

3.4

67

6.5

262

257

2.1

(% of Sales)

6.4

6.8

(40)bp

9.7

(328)bp

7.7

8.3

(66)bp

Other Expenses

162

148

10.1

119

36.4

547

517

5.8

(% of Sales)

14.7

14.7

4bp

17.4

(265)bp

16.0

16.8

(75)bp

Total Expenditure

1,046

936

11.8

658

59.0

3,237

2,907

11.3

Operating Profit

57

69

(17.4)

28

104.9

178

174

2.4

OPM

5.2

6.9

(170)bp

4.1

111bp

5.2

5.6

(43)bp

Interest

9

11

(21.8)

9

(1.9)

36

43

(18.3)

Depreciation

19

10

82.2

11

67.0

51

39

29.8

Other Income

5.5

3.6

51.9

1.4

302.2

9

10

(8.9)

Exceptional Item

48

38

(2)

30

42

PBT

83

89

(7.5)

7

1,106.1

130

143

12.6

(% of Sales)

7.5

8.9

1.0

3.8

4.6

Tax

11

(17)

2

21

(10)

(% of PBT)

13

(19)

30

16

(7)

Reported PAT

72

106

(32.4)

5

1394.2

110

153

(28.0)

Extraordinary Item

(48)

(38)

2

(30)

(42)

Adjusted PAT

24

68

(64.8)

7

253.9

80

111

(28.0)

PATM

2.2

6.8

1.0

2.3

3.6

Source: Company, Angel Research

Margin and bottom-line below expectations mainly on account of

provision

For 4QFY2016, the standalone top-line grew by 9.8% yoy to `1,103cr which is in-

line with our estimates. On the operating front, the EBITDA margin contracted by

170bp yoy to 5.2% largely owing to a 205bp yoy increase in raw material cost to

73.7% of sales. The depreciation expense was significantly higher on account of

BSIL’s merger, which added by ~`6cr to this expense head. There was a net

exceptional income of `48cr arising from profit on sale of IT business of BSIL, as

well as cost update on major contracts. Adjusting for the exceptional item, the net

profit came in at `24cr.

June 3, 2016

2

Blue Star | 4QFY2016 Result Update

Segment-wise performance

Exhibit 2: Segment-wise performance (Standalone)

Y/E March (` cr)

4QFY2016 4QFY2015 % chg (yoy) 3QFY2016 % chg (qoq)

Total Revenue

A) EMPPAC

439

361

21.5

459

(4.3)

B) Cooling Products

238

197

21.0

246

(3.2)

C) PEIS

9

38

(76.2)

12

(27.9)

Total

686

596

15.1

717

(4.3)

Less: Inter-Segmental Rev.

-

-

-

Net Sales

686

596

15.1

717

(4.3)

Segmental Profit

A) EMPPAC

26

3

785.5

26

(2.2)

B) Cooling Products

17

10

67.5

14

20.6

C) PEIS

2

7

(76.0)

2

(21.5)

Segmental Margin (%)

A) EMPPAC

5.8

0.8

505bp

5.7

12bp

B) Cooling Products

7.1

5.1

198bp

5.7

140bp

C) PEIS

18.7

18.5

17bp

17.2

153bp

Source: Company, Angel Research

Concall Takeaways

Order inflow for the year was up by ~19.0% yoy to `3,652cr while carry

forward order book grew by ~17.0% yoy to `1,628cr.

Metro accounts for ~22% of the order book and is likely to perform well. The

balance is made up of

18% industrial,

14% offices,

11% mixed use

development, 11% of power generation and distribution, 8% Malls,

8%

hospitals and 8% others.

While the order inflow has improved for the EMPPAC segment, the

Management is however cautious on the execution part in the near term on

factoring in the near term liquidity scenario. It has guided for margins to be in

the range of ~6%.

The RAC industry growth estimate has been revised to ~20% for FY2017 and

the company has guided for growth in excess of 30% for the same period.

The Jammu plant will likely be the first to commence production among

upcoming facilities, which is in FY2018E, and will add to the overall capacity

by 1.5 lakh units.

The company is focusing on growing its products business in the export

markets and is looking at three new countries in Africa.

June 3, 2016

3

Blue Star | 4QFY2016 Result Update

Investment Rationale

Improvement in macro scenario to support growth

The EMPPAC division of Blue Star contributed ~54% of total revenues in FY2015.

The division mainly caters to industrial/institution clients in sectors like IT/ITeS,

retail (including malls and multiplexes), healthcare, hospitality, infrastructure, etc.

The order execution and finalization has been witnessed to be sluggish in the

recent past, thereby affecting the segment. With slow recovery in various client

industries and improvement in the economic environment post interest rate cuts,

we expect the segment to recover and be a key contributor to the company’s

overall top-line.

Quality order execution to support EBITDA margin expansion

The company continues to be selective in terms of order booking; such practice

has hurt its margins in the past. So far, the delay in execution of high-margin

projects, coupled with delayed closure of low margin jobs, has resulted in snail-

paced expansion of the EBITDA margin. The carry forward order book has been

witnessing upward movement over the past few quarters and with legacy jobs

coming off the books, we expect the segment’s profitability to improve from here

on.

Cooling Products division to be the backbone

The superior performance of the division is mainly on the back of high growth seen

in the RAC segment which is consistently growing at 10% points faster than the

overall RAC market. The company has been able to leverage on its cultivated

perception of being a “Cooling Expert” and successfully grown its market share

from ~7% levels in FY2015 to the present 10.5%. As a result of this growth, the

Cooling Products segment’s share as a percentage of total revenue has increased

from 23.4% in FY2009 to ~43.2% in FY2016 (ex of BSIL numbers) and the

segment in recent times has been delivering better profitability than the other

major segment - EMMPAC. We expect the division to be a key contributor as there

is significant potential to capitalize on the underpenetrated RAC market in India.

Blue Star can add to its current market share as it has good channel coverage and

it has been selectively expanding the channel network in tier 3, 4 and 5 cities.

Foray into newer products and focus on growing international

business

Blue Star has forayed into new areas like air purifiers and air coolers in FY2016.

As per Management estimates, the domestic air purifiers market is of ~`200cr,

which it expects to grow by 5x over the next five years. Further the Management

sounded confident that it can rely on its brand equity to successfully scale up the

air coolers business using its vast channel network.

Additionally, the company post its merger with Blue Star Infotech Ltd (BSIL) will be

using the cash influx to grow its international business. Apart from this, the

company has entered into a 51% joint venture with W. J. Towell & Co. LLC, Oman,

in the MEP contracting business. The company intends to scale up the business to

`500cr over the next few years.

June 3, 2016

4

Blue Star | 4QFY2016 Result Update

Financials

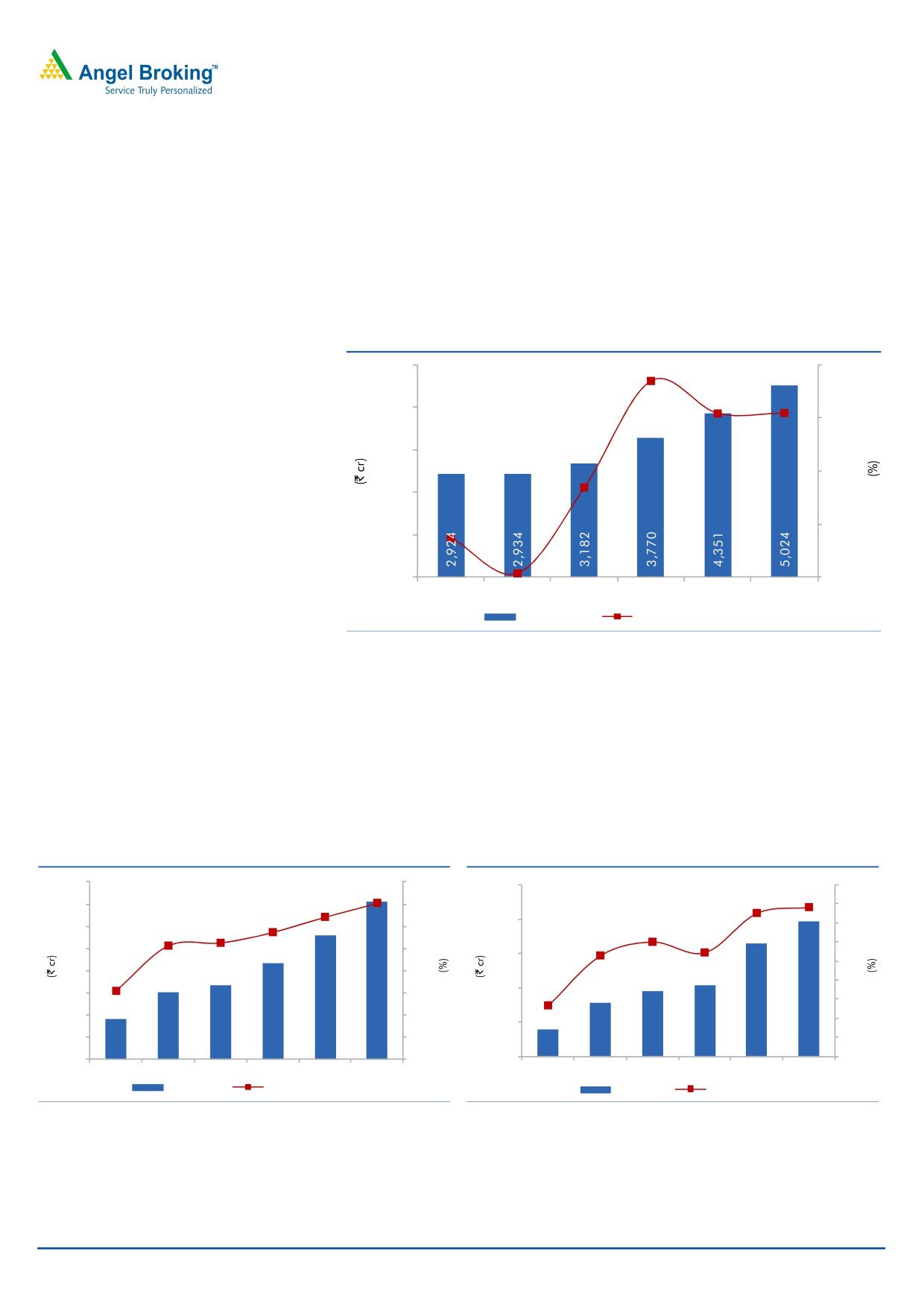

Improvement in revenue growth

We are building in revenue CAGR of 15.4% over FY2016-18E to `5,024 on

account of 1) strong growth prospects of the Cooling/Unitary Products division led

by increased demand and penetration of room air conditioners and

2)

improvement in prospects of the EMPPAC division.

Exhibit 3: Revenue growth estimates

5,500

18.5

20.0

15.4

15.5

4,500

15.0

3,500

10.0

2,500

8.4

5.0

1,500

3.7

0.4

500

-

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Revenue (LHS)

Revenue growth (RHS)

Source: Company, Angel Research

EBITDA margin to improve

We expect the EMPPAC segment’s performance to improve considering that the

order book clean up has now been done and that the new margin should be at

~6.0% as guided by the Management. We expect the EBITDA margin to improve

from 5.7% in FY2016 to 7.1% in FY2018E. Consequently, the net profit is expected

to be at `197cr in FY2018E.

Exhibit 4: EBITDA margin to improve

Exhibit 5: PAT expected to improve

400

8.0

250

4.5

3.9

3.8

350

7.1

7.0

4.0

200

300

6.4

6.0

3.0

3.5

5.7

2.7

5.3

3.0

250

5.0

5.1

150

2.6

2.5

200

4.0

2.0

100

150

3.1

3.0

1.5

1.3

100

2.0

1.0

50

50

1.0

0.5

90

150

167

216

280

354

39

78

96

103

164

197

-

-

-

-

FY2013

FY2014 FY2015 FY2016 FY2017E FY2018E

FY2013

FY2014 FY2015 FY2016 FY2017E FY2018E

EBITDA (LHS)

EBITDA margin (RHS)

PAT (LHS)

PAT margin (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

June 3, 2016

5

Blue Star | 4QFY2016 Result Update

Outlook and valuation

We have upgraded our numbers to factor in higher revenue guidance for the RAC

business as well as improvement in performance of the EMPPAC division. As

reported in our earlier report(s), the merger with BSIL has improved the balance

sheet strength of the company by way of cash infusion which the company will

utilize to grow the UPD division as well as the exports of the company. At the current

market price, the stock trades at 20.1x its FY2018E earnings and at 0.8x FY2018E

EV/sales (while its close peer Voltas trades at 1.5x its FY2018E EV/sales). We maintain

our BUY recommendation on the stock with a target price of `495.

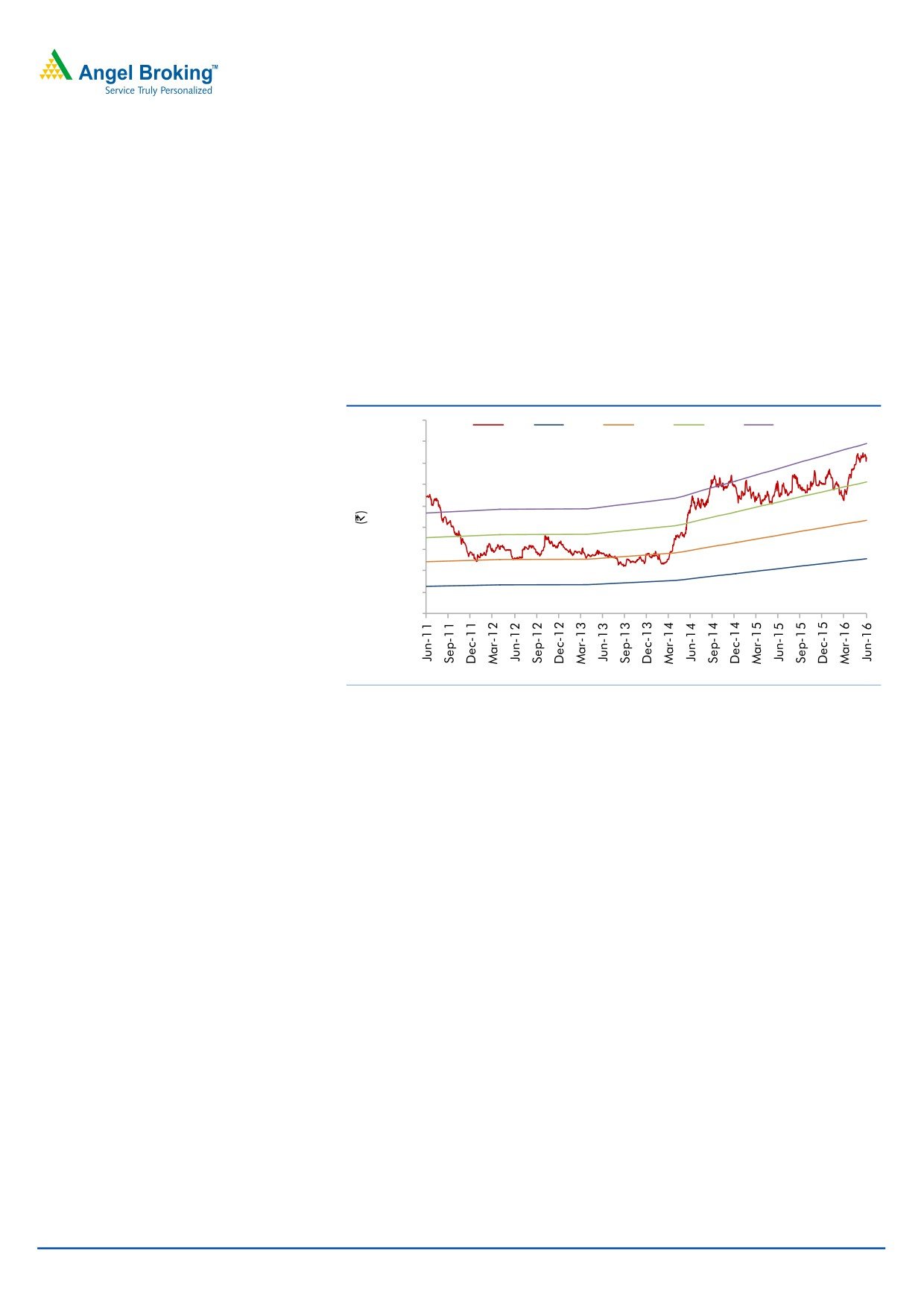

Exhibit 6: One year forward EV/sales band

5,000

EV

0.4x

0.6x

0.8x

1.0x

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

Source: Company, Angel Research

Key concerns

Slowdown in investment cycle may impact order inflow, thus impacting

revenue. It may also force the Management to compromise on its strategy of

avoiding low margin projects.

Any slowdown in consumer segments like IT/ITES, healthcare, hospitality and

infrastructure could impact the company’s growth.

Foreign exchange fluctuations have a direct impact on the profit of the

Cooling Products division since commercial refrigerators are imported. Any

further depreciation in the local currency may impact the company’s profits.

The RAC industry has been witnessing high traction and the company has

been able to outperform the industry over the past few years. Any unexpected

drop in performance of the RAC industry would pose a threat to our estimates.

June 3, 2016

6

Blue Star | 4QFY2016 Result Update

Company Background

Blue Star is India's largest central air-conditioning company with a network of

32 offices, seven manufacturing facilities, over

2,000 dealers and around

2,500 employees. The company’s operations could be classified under three main

segments:

EMPPACS: This segment comprises central and packaged air-conditioning

(involving design, engineering, manufacturing, installation, commissioning and

support of large central air conditioning plants, packaged air conditioners and

ducted split air conditioners) as well as electrical projects and plumbing and fire

fighting projects. In addition, the company promotes after-sales service as a

business, by offering several value added services in the areas of upgrades and

enhancements, air management, water management, energy management and

LEED consultancy for Green Buildings.

Cooling Products: Blue Star offers a wide range of contemporary window and split

air conditioners. The company also manufactures and markets a comprehensive

range of commercial refrigeration products and services that cater to the industrial,

commercial and hospitality sectors.

PEIS: This division has been the exclusive distributor in India for many

internationally renowned manufacturers of hi-tech professional electronic

equipment and services, as well as industrial products and systems.

June 3, 2016

7

Blue Star | 4QFY2016 Result Update

Profit and loss statement (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

FY2018E

Total operating income

2,934

3,182

3,770

4,351

5,024

% chg

0.4

8.4

18.5

15.4

15.5

Net Raw Materials

2,087

2,214

2,607

3,010

3,487

Personnel

248

267

346

387

432

Other

450

533

600

674

751

Total Expenditure

2,784

3,015

3,554

4,072

4,670

EBITDA

150

167

216

280

354

% chg

(1.8)

8.3

17.9

14.6

14.7

(% of Net Sales)

5.1

5.3

5.7

6.4

7.1

Depreciation& Amortisation

38

43

60

56

63

EBIT

113

124

156

223

291

% chg

97.4

10.2

25.4

43.4

30.5

(% of Net Sales)

3.8

3.9

4.1

5.1

5.8

Interest (incl. forex loss)

54

49

43

37

33

Other Income

18

8

17

21

22

(% of Net Sales)

0.6

0.3

0.4

0.5

0.4

Exceptional Items

(0.1)

(41.4)

5.6

-

-

PBT

76

43

135

207

281

% chg

87.1

(44.0)

217.5

53.0

35.7

Tax

2

(8)

27

44

84

(% of PBT)

2.9

(18.5)

19.9

21.0

30.0

PAT (reported)

74

51

108

164

197

Extraordinary (Expense)/Inc.

0

41

(6)

-

-

Share of Profit of Associate

4

4

-

-

-

Minority Interest

0

ADJ. PAT

78

96

103

164

197

% chg

98.6

23.1

7.5

59.3

20.2

(% of Net Sales)

2.6

3.0

2.7

3.8

3.9

Basic EPS (`)

8.6

10.6

11.4

17.2

20.6

Fully Diluted EPS (`)

8.6

10.6

11.4

17.2

20.6

% chg

198.6

123.1

107.5

150.3

120.2

June 3, 2016

8

Blue Star | 4QFY2016 Result Update

Balance sheet (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

FY2018E

SOURCES OF FUNDS

Equity Share Capital

18

18

18

19

19

Pref. Share Capital/Suspense

18

-

173

-

-

Reserves& Surplus

443

438

472

735

857

Shareholders’ Funds

479

456

663

754

876

Minority Interest

-

-

1

1

1

Total Loans

494

398

364

333

305

Deferred Tax Liability

(1)

(17)

(22)

(22)

(22)

Other Long Term Liabilities

4

7

11

11

11

Total Liabilities

976

843

1,016

1,077

1,171

APPLICATION OF FUNDS

Gross Block

514

549

625

700

784

Less: Acc. Depreciation

269

304

364

420

483

Net Block

245

245

260

279

300

Capital Work-in-Progress

15

22

15

60

60

Goodwill

11

11

9

8

6

Investments

33

36

223

111

111

Long term Loans & adv

120

139

190

205

221

Current Assets

1,911

1,704

1,870

2,088

2,391

Cash

68

44

54

44

37

Loans & Advances

130

116

112

128

148

Inventory

466

479

540

627

718

Debtors

833

795

888

971

1,122

Other current assets

414

270

275

317

366

Current liabilities

1,359

1,315

1,551

1,673

1,919

Net Current Assets

552

389

319

414

472

Misc. Exp. not written off

-

-

-

-

-

Total Assets

976

843

1,016

1,077

1,171

June 3, 2016

9

Blue Star | 4QFY2016 Result Update

Cash flow statement (Consolidated)

Y/E March (` cr)

FY2014 FY2015 FY2016E FY2017E FY2018E

Profit before tax

76

43

135

207

281

Depreciation

38

43

60

56

63

Change in Working Capital

(47)

139

79

(105)

(65)

Other income

(18)

(8)

(17)

(21)

(22)

Direct taxes paid

(2)

(7)

(33)

(44)

(84)

Others

37

28

-

-

-

Cash Flow from Operations

83

237

226

93

173

(Inc.)/Dec. in Fixed Assets

(71)

(43)

(66)

(118)

(83)

(Inc.)/Dec. in Investments

(6)

(3)

(187)

111

-

(Inc.)/Dec. In L.T loans and adv

(8)

(20)

(51)

(14)

(17)

Other income

18

8

17

21

22

Others

62

(14)

-

-

-

Cash Flow from Investing

(6)

(71)

(286)

0

(77)

Issue of Equity

18

(18)

173

2

-

Inc./(Dec.) in loans

73

(97)

(33)

(31)

(28)

(Dec.)/Inc. in long term prov.

(1)

2

5

-

-

Forex diff. on cash equivalent

-

-

-

-

-

Dividend Paid (Incl. Tax)

(42)

(54)

(70)

(75)

(75)

Others

(74)

(23)

(4)

-

-

Cash Flow from Financing

(26)

(190)

70

(103)

(103)

Inc./(Dec.) in Cash

52

(24)

10

(10)

(7)

Opening Cash balances

17

68

44

54

44

Closing Cash balances

68

44

54

44

37

June 3, 2016

10

Blue Star | 4QFY2016 Result Update

Key ratios

Y/E March

FY2014

FY2015

FY2016E

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

48.1

39.0

36.3

24.2

20.1

P/CEPS

32.3

26.9

22.9

18.0

15.2

P/BV

7.8

8.2

5.6

5.2

4.5

Dividend yield (%)

1.0

1.2

1.6

1.6

1.6

EV/Sales

1.4

1.3

1.1

0.9

0.8

EV/EBITDA

27.6

24.4

18.7

14.4

11.3

EV / Total Assets

4.3

4.8

4.0

3.7

3.4

Per Share Data (`)

EPS (Basic)

8.6

10.6

11.4

17.2

20.6

EPS (fully diluted)

8.6

10.6

11.4

17.2

20.6

Cash EPS

12.8

15.4

18.1

23.1

27.2

DPS

4.0

5.0

6.5

6.5

6.5

Book Value

53.2

50.7

73.7

79.1

91.9

Returns (%)

ROCE (Pre-tax)

12.5

13.6

16.7

21.3

25.9

Angel ROIC (Pre-tax)

14.6

16.6

22.2

28.4

32.2

ROE

17.7

20.5

18.4

23.1

24.1

Turnover ratios (x)

Asset Turnover (Gross Block)

6.1

6.0

6.4

6.6

6.8

Inventory / Sales (days)

61

54

49

49

49

Receivables (days)

104

93

81

81

81

Payables (days)

176

162

147

150

150

WC cycle (ex-cash) (days)

57

47

29

27

29

Solvency ratios (x)

Net debt to equity

0.9

0.8

0.4

0.2

0.2

Net debt to EBITDA

2.6

1.9

0.4

0.6

0.4

Interest Coverage (EBIT / Int.)

2.1

2.6

3.6

6.0

8.9

June 3, 2016

11

Blue Star | 4QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Blue Star

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

June 3, 2016

12