2QFY2016 Result Update | Auto Ancillary

November 2, 2015

Bharat Forge

BUY

CMP

`862

Performance Highlights

Target Price

`1,016

Y/E March - Standalone (` cr) 2QFY16 2QFY15

% chg (yoy) 1QFY16

% chg (qoq)

Investment Period

12 Months

Net Sales

1,117

1,138

(1.9)

1,129

(1.0)

EBITDA

321

325

(1.0)

346

(7.1)

Stock Info

EBITDA margin (%)

28.8

28.5

30 bp

30.7

(190 bp)

Sector

Auto Ancillary

Adjusted PAT

175

179

(2.0)

195

(10.4)

Source: Company, Angel Research

Market Cap (` cr)

20,068

For 2QFY2016, Bharat Forge Ltd (BFL)’s results have come in below estimates.

Net Debt (` cr)

1,187

Beta

1.2

The top-line declined marginally, led by a steep decline in industrial exports which

is

owing to weakness in the oil and gas segment. A subdued

52 Week High / Low

1,363/805

top-line and adverse mix (industrial exports have high machining component)

Avg. Daily Volume

243,839

negated most of the benefits of lower steel prices. Given the subdued top-line, the

Face Value (`)

2.0

net profit too declined marginally on a yoy basis.

BSE Sensex

26,559

Nifty

8,051

Top-line declines marginally: After seven consecutive quarters of double-digit

Reuters Code

BFRG.BO

growth, BFL’s revenues declined by 2% yoy to `1,117cr during the quarter. The decline

was led by the export segment which dipped by 9%. Industrial segment exports declined

Bloomberg Code

BHFC@IN

sharply by 32% yoy due to weakness in the oil and gas sector. The domestic market, in

contrast, grew a healthy 9% yoy led by the non-auto segment, which reported a growth

Shareholding Pattern (%)

of 20% yoy.

Promoters

46.7

Subdued topline and adverse mix impacts profitability: BFL’s revenues were under

MF / Banks / Indian Fls

21.6

pressure during the quarter, which led to operating deleverage. Further, the

FII / NRIs / OCBs

18.5

product mix worsened given the decline in the industrial export segment which

Indian Public / Others

13.2

levied pressure on profitability. The net profit, at `175cr, declined by 2% yoy.

Outlook and valuation: The outlook in the near term remains subdued given the

pressures in the industrial export segment (particularly in the oil and gas space).

Abs. (%)

3m 1yr 3yr

However, BFL expects the topline to return to double digit growth rate from

Sensex

(5.5)

(4.7)

41.6

FY2017 on back of expected recovery in the commercial vehicle export markets.

Bharat Forge

(24.8)

6.1

219.0

Further, the ramp up in the passenger vehicle exports due to new order wins and

addition of new customers and markets in the export industrial segments would

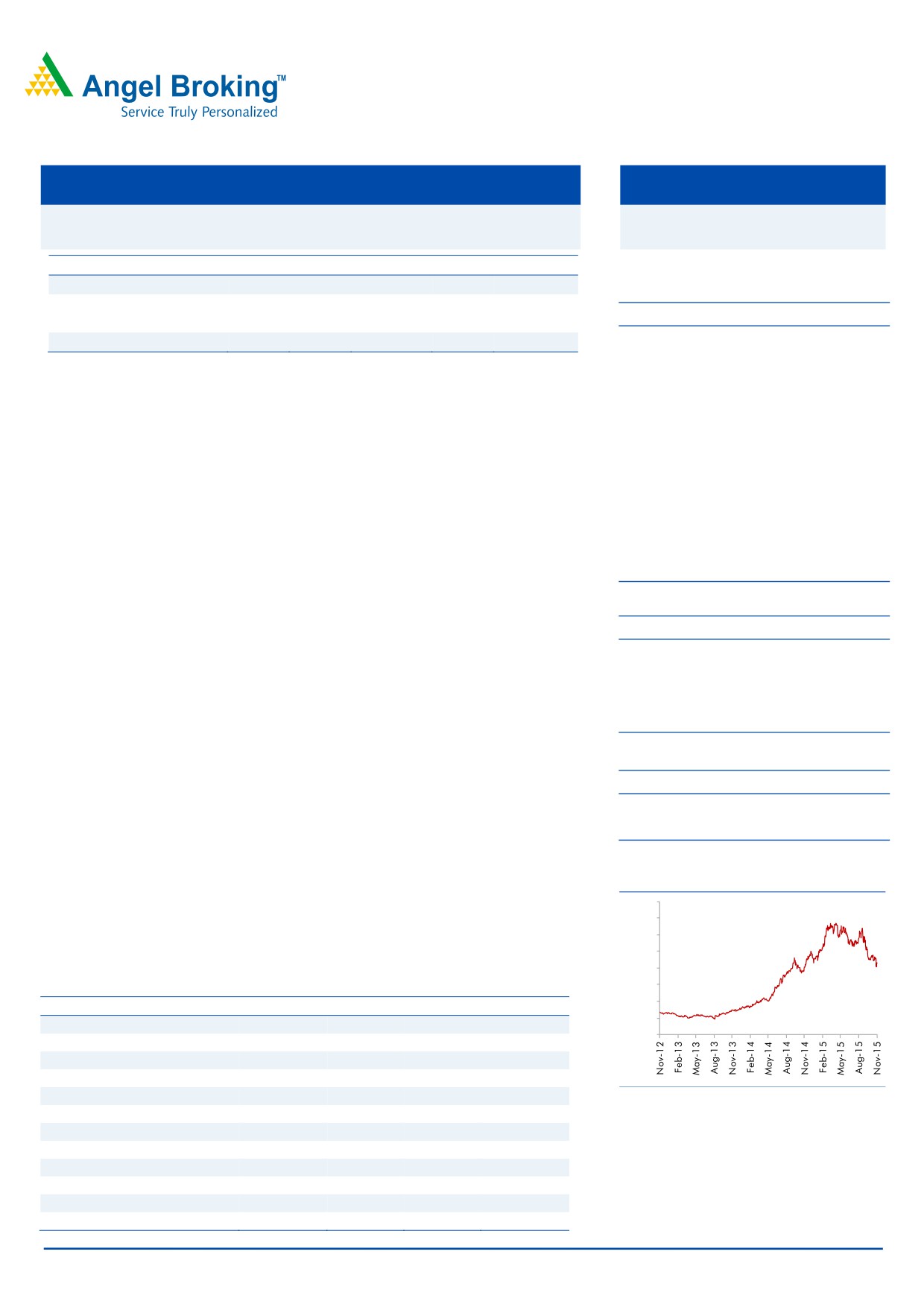

3-year price chart

enable BFL to outpace industry growth. Given the focus on technological

1,600

innovation and the ability to tap new segments and customer base, we have

1,400

1,200

positive view on the stock. We assign Buy rating to the stock with a price target of

1,000

`1,016 (based on 24x FY2017 earnings).

800

600

Key financials (Consolidated)

400

Y/E March (` cr)

FY2014

FY2015 FY2016E

FY2017E

200

Net sales

6,716

7,625

8,013

9,250

0

% chg

17.8

13.5

5.1

15.4

Net profit

267

646

819

986

% chg

17.3

142.0

26.8

20.3

EBITDA (%)

15.3

18.9

20.0

20.3

Source: Company, Angel Research

EPS (`)

11.5

27.8

35.2

42.3

P/E (x)

40.3

26.3

24.5

20.4

P/BV (x)

7.5

5.8

4.8

4.0

RoE (%)

10.8

21.1

21.6

21.4

RoCE (%)

13.4

19.3

19.1

21.1

Bharat Gianani

EV/Sales (x)

3.0

2.7

2.6

2.2

022-3935 7800 Ext: 6817

EV/EBITDA (x)

20.2

14.8

13.1

10.9

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Bharat Forge | 2QFY2016 Result Update

Exhibit 1: Financial performance (Standalone)

Y/E March (` cr)

2QFY16

2QFY15

% chg (yoy)

1QFY16

% chg (qoq)

1HFY16

1HFY15

% chg (yoy)

Net Sales

1,117

1,138

(1.9)

1,129

(1.0)

2,245

2,126

5.6

Consumption of RM

407

456

(10.8)

398

2.4

805

816

(1.3)

(% of Sales)

36.5

40.1

35.3

35.9

38.4

Staff Costs

92

81

14.0

92

(0.4)

185

160

15.1

(% of Sales)

8.2

7.1

8.2

8.2

7.5

Manufacturing expenses

182

193

(5.5)

183

(0.2)

365

378

(3.5)

(% of Sales)

16.3

16.9

16.2

16.2

17.8

Other Expenses

114

84

36.2

110

3.9

224

165

35.6

(% of Sales)

10.2

7.3

9.7

10.0

7.8

Total Expenditure

795

814

(2.2)

782

1.7

1,578

1,518

3.9

Operating Profit

321

325

(1.0)

346

(7.1)

668

608

9.8

OPM (%)

28.8

28.5

30.7

29.7

28.6

Interest

22

31

(29.1)

21

4.4

44

63

(30.9)

Depreciation

65

66

(1.6)

64

1.6

130

132

(1.9)

Other Income

25

30

(15.1)

29

(11.7)

54

54

0.2

PBT

259

257

0.9

289

(10.4)

549

467

17.5

(% of Sales)

23.2

22.6

25.6

24.4

22.0

Provision for Taxation

84

78

7.6

94

(10.3)

178

144

24.3

(% of PBT)

32.5

30.5

32.5

32.5

30.7

Extraordinary items

0

(4)

NA

0

NA

0

(4)

NA

Reported PAT

175

174

0.3

195

(10.4)

370

319

15.9

Adjusted PAT

175

179

(2.0)

195

(10.4)

370

324

14.5

Adj. PATM

15.7

15.7

17.3

16.5

15.2

Equity capital (cr)

47

47

47

47

47

Reported EPS (`)

7.5

7.5

0.3

8.4

(10.4)

15.9

13.7

15.9

Adjusted EPS (`)

7.5

7.7

(2.0)

8.4

(10.4)

15.9

13.9

14.5

Source: Company, Angel Research

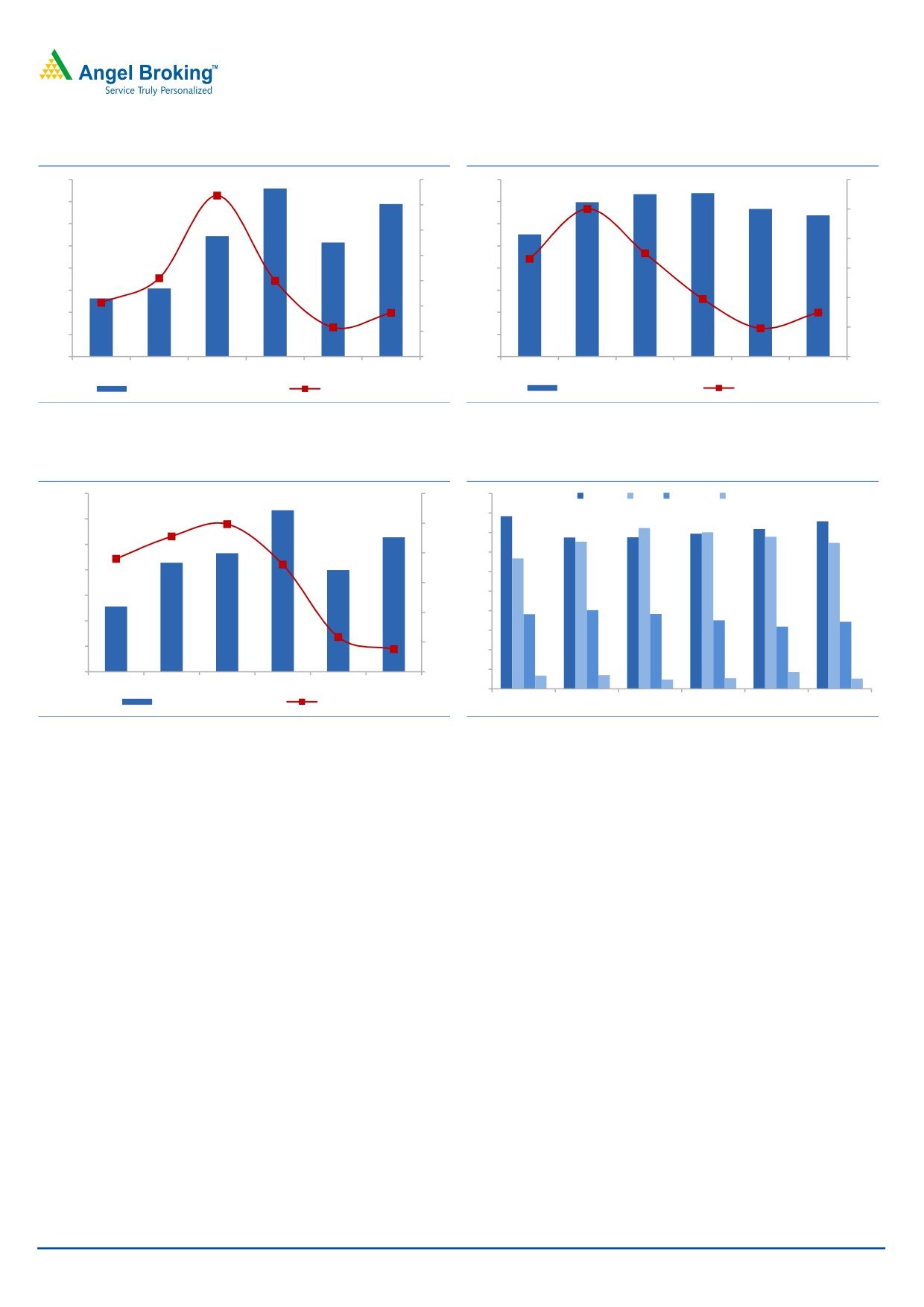

Standalone revenues under pressure due to steep decline in industrial exports: For

2QFY2016, standalone revenues were under pressure, declining by 2% yoy to

`1,117cr, owing to a steep 9% yoy decline in export revenues. While the export

automotive segment grew by a healthy 15% yoy due to ramp up in the passenger

vehicle business, the export non-automotive segment declined sharply by 32% yoy

due to slowdown in the oil and gas sector. In contrast, domestic revenues grew

8.6% yoy led by a strong 20% growth in the non-automotive segment. The

domestic automotive segment revenues grew by 3% yoy. BFL’s overall volumes

grew

4% yoy, driven by the domestic segment; however, the net average

realization declined 5.5% yoy on account of an adverse product-mix (decline in the

high machining export industrial segment). The USD/INR realization on the exports

front stood at `66.6/USD, up 1% qoq.

November 2, 2015

2

Bharat Forge | 2QFY2016 Result Update

Exhibit 2: Domestic revenues continue to recover

Exhibit 3: Exports remain sluggish

490

35

800

40

480

30

700

30

470

600

25

20

460

500

20

450

400

10

15

440

300

0

10

430

200

(10)

420

5

100

410

0

0

(20)

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Domestic revenues (` cr)

Growth yoy (%)

Export revenues (` cr)

Growth yoy (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 4: Volume growth dragged by exports

Exhibit 5: Geographical break-up of revenue

58,000

30

50

India

US Europe

Others

44

43

45

41

41

56,000

4040

25

39

39

39

38

37

40

54,000

33

20

35

52,000

30

15

25

50,000

20

19

19

18

17

10

20

16

48,000

15

5

46,000

10

44,000

0

5

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

0

Shipment tonnage (MT)

Growth yoy (%)

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Source: Company, Angel Research

Source: Company, Angel Research

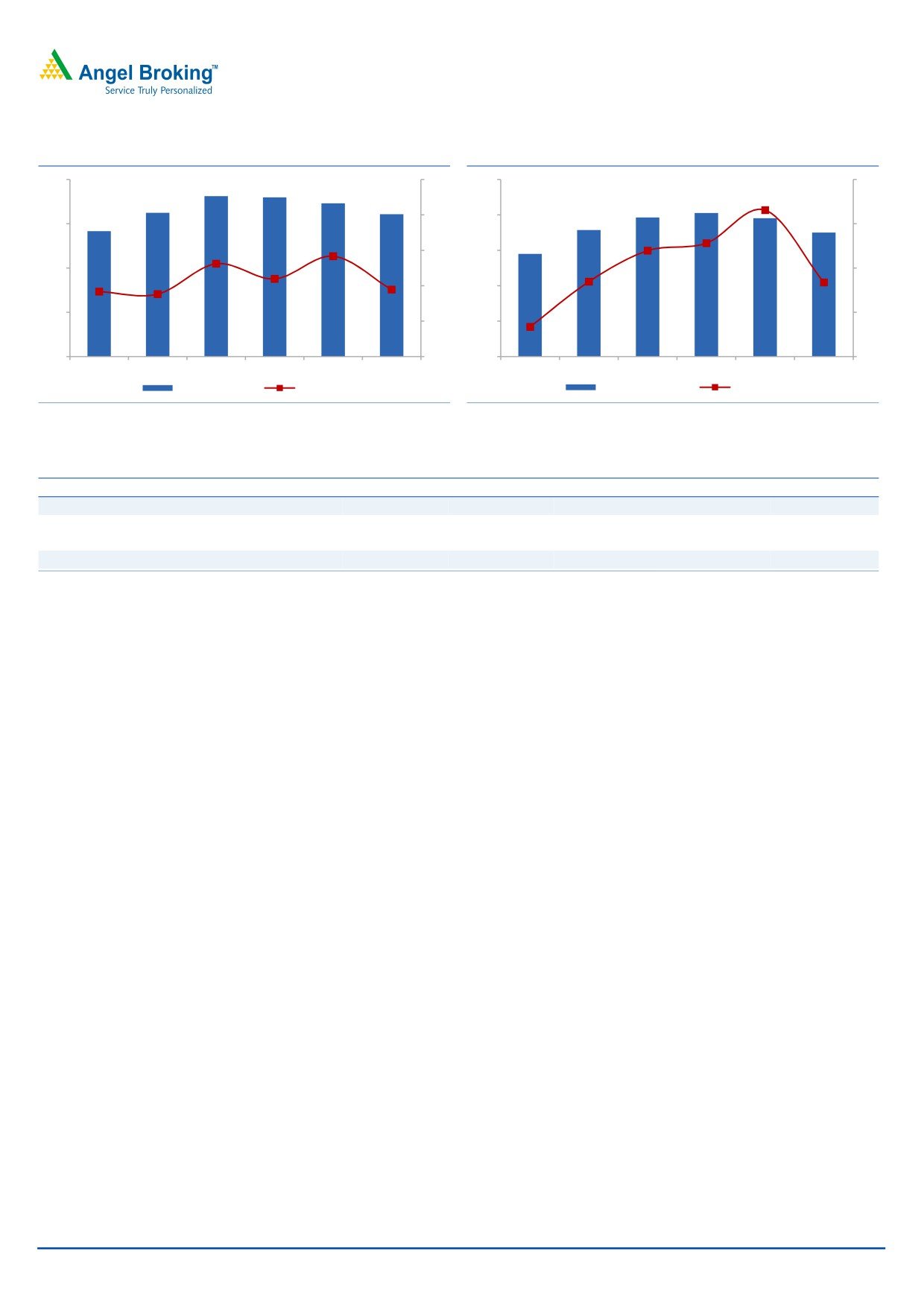

EBITDA margins up marginally yoy: On the operating front, EBITDA margins

improved marginally by 30bp yoy to 28.8%, driven primarily by softness in steel

prices. Raw material cost/sales declined 360bp yoy to 36.5%. However, the

subdued top-line resulted in operating deleverage, thus leading to a 220bp yoy

increase in other expenditure. As a result the benefits of lower commodity prices

got negated. On a sequential basis, however, margins declined 190bp, mainly

due to an adverse product mix. Led by a subdued top-line, the net profit declined

marginally by 2% yoy to `175cr.

November 2, 2015

3

Bharat Forge | 2QFY2016 Result Update

Exhibit 6: EBITDA margin grows marginally

Exhibit 7: Subdued top-line impacts profitability

400

35

250

18

33

200

300

17

31

150

200

16

29

100

100

15

27

50

0

25

0

14

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

EBIDTA (` cr)

Margin (%)

Net Profit (` cr)

Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 8: Subsidiaries’ performance

Y/E December - Overseas subsidiary (` cr)

July-Sep 15

July-Sep 14

% chg (yoy)

Apr-June 15

% chg (qoq)

Net Sales

549

543

1.0

601

(8.6)

EBITDA

36

31

14.7

38

(4.8)

EBITDA margin (%)

6.5

5.7

80 bp

6.3

20 bp

Profit before tax

(3)

1

0

Source: Company, Angel Research

Overseas subsidiaries’ performance remains subdued: The company’s overseas

subsidiaries’ performance remained under pressure, given the weak global

demand. The top-line at `549cr remained flat on a yoy basis. The margin

improved 80bp yoy, given the cost control initiatives. However due to higher

depreciation and interest expenses, the subsidiaries reported a loss at the PBT

level.

November 2, 2015

4

Bharat Forge | 2QFY2016 Result Update

Investment arguments

Automotive business to grow driven by domestic CV upcycle and ramp up in

PV segment: BFL is the leader in the domestic MHCV segment, commanding a

market share of ~60%. BFL would be the beneficiary of an upcycle in the

MHCV space (MHCV is likely to grow at 15% CAGR over FY2015-2018) due

to economic recovery and huge pent up demand getting converted into sales.

Also, BFL has received orders from two new passenger vehicle OEMs for

supply to various platforms which would boost its revenues going ahead.

Further, the US and the European CV segments are also expected to recover

gradually, thus boosting demand.

Industrial segment to provide huge growth opportunity: BFL aims to increase

the share of the industrial segment from 45% of standalone revenues in

FY2015 to 60%, going ahead. The government’s “Make in India” initiative

would result in localization in a host of sectors such as defence, aerospace,

power, and metal & mining, which throws a huge opportunity for BFL. Also

given the economic recovery, the domestic investment cycle is likely to improve

which would provide impetus to the industrial segment. BFL is also tapping the

industrial segment in export markets by introducing new products, which

would boost growth for the company.

Well diversified business model: BFL has a fairly diversified presence. Over the

years it has enhanced revenue stream by entering new global markets and

new segment particularly in the non-auto space. The share of the auto

business declined from about 80% in FY2007 to about 55% currently. Also the

contribution of India business has reduced from 60% in FY2010 to about 40%

currently. Given the broad-based presence, BFL has de-risked itself from

possible sharp economic downturns in any particular region/segment.

Outlook and valuation

The outlook in the near term remains subdued given the pressures in the industrial

export segment (particularly in the oil and gas space). However, BFL expects the

topline to return to double digit growth rate from FY2017 on back of expected

recovery in the commercial vehicle export markets. Further, the ramp up in the

passenger vehicle exports due to new order wins and addition of new customers

and markets in the export industrial segments would enable BFL to outpace

industry growth. Given the focus on technological innovation and the ability to tap

new segments and customer base, we have positive view on the stock. We assign

Buy rating to the stock with a price target of `1,016 (based on 24x FY2017

earnings).

November 2, 2015

5

Bharat Forge | 2QFY2016 Result Update

Company background

Bharat Forge, a global forging conglomerate, is the largest exporter of automotive

components from India and a leading chassis component manufacturer in the

world. The company manufactures a wide range of safety and critical components

for passenger cars, SUVs, LCVs, MHCVs and tractors through its facilities spread

across locations globally - India (4), Germany (3) and Sweden (1). BHFC also

produces forged and machined components for non-automotive industries, such

as power generation, marine, oil & gas, railways and construction. The automotive

industry currently contributes ~55% to the company's consolidated revenue;

although through diversification BHFC expects the share of the automotive

industry's revenue to fall to ~40%.

November 2, 2015

6

Bharat Forge | 2QFY2016 Result Update

Profit and loss statement (Consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Total operating income

6,279

5,702

6,716

7,625

8,013

9,250

% chg

23.4

(9.2)

17.8

13.5

5.1

15.4

Total expenditure

5,283

4,933

5,686

6,184

6,410

7,372

Net raw material costs

2,913

2,531

2,461

2,884

2,965

3,423

Employee expenses

780

801

789

905

962

1,110

Other

1,589

1,601

2,436

2,395

2,484

2,840

EBITDA

996

769

1,030

1,441

1,603

1,878

% chg

(41.0)

(22.8)

33.9

39.9

11.2

17.2

(% of total op. income)

15.9

13.5

15.3

18.9

20.0

20.3

Depreciation & amortization

302

336

357

362

391

420

EBIT

694

433

673

1,078

1,211

1,458

% chg

(51.6)

(37.6)

55.3

60.2

12.3

20.3

(% of total op. income)

11.1

7.6

10.0

14.1

15.1

15.8

Interest and other charges

186

191

169

136

132

119

Other income

92

113

125

137

153

153

Recurring PBT

600

355

629

1,080

1,232

1,491

% chg

(55.4)

(40.8)

77.0

71.8

14.2

21.0

Extraordinary items

0

0

77

39

0

0

PBT (reported)

600

355

551

1,041

1,232

1,491

Tax

180

173

210

359

413

506

(% of PBT)

29.9

48.6

38.1

34.5

33.5

33.9

Profit before MI

420

182

341

682

819

986

Share of associate

0

0

0

0

0

0

Minority interest (MI)

7

(45)

(3)

(3)

0

0

PAT (reported)

413

228

344

685

819

986

ADJ. PAT

413

228

267

646

819

986

% chg

(65.6)

(44.9)

17.3

142.0

26.8

20.3

(% of total op. income)

6.6

4.0

4.0

8.5

10.2

10.7

Basic EPS (`)

17.8

9.8

14.8

29.4

35.2

42.3

Adj. EPS (`)

17.8

9.8

11.5

27.8

35.2

42.3

% chg

(65.6)

(44.9)

17.3

142.0

26.8

20.3

November 2, 2015

7

Bharat Forge | 2QFY2016 Result Update

Balance sheet statement (Consolidated)

Y/E March (` cr)

FY2012 FY2013 FY2014

FY2015

FY2016E

FY2017E

SOURCES OF FUNDS

Equity share capital

47

47

47

47

47

47

Reserves & surplus

2,137

2,210

2,637

3,398

4,109

5,005

Shareholders’ funds

2,184

2,256

2,683

3,444

4,155

5,051

Minority interest

196

164

17

(2)

(2)

(2)

Total loans

2,419

2,333

2,007

2,365

2,065

1,865

Deferred tax liability

89

135

164

164

164

164

Other long term liabilities

22

38

18

60

60

60

Long term provisions

88

107

116

120

120

120

Total Liabilities

4,997

5,033

5,006

6,150

6,561

7,257

APPLICATION OF FUNDS

Goodwill

3

3

6

54

54

54

Gross block

5,019

5,644

5,389

5,645

6,095

6,545

Less: Acc. depreciation

2,370

2,737

2,860

3,070

3,461

3,881

Net Block

2,649

2,907

2,528

2,575

2,634

2,663

Capital work-in-progress

517

632

583

859

759

659

Investments

445

416

801

496

529

585

Long term loans and adv.

392

253

236

240

240

240

Other noncurrent assets

51

37

26

23

23

23

Current assets

3,277

3,190

3,354

3,988

4,469

5,458

Cash

634

555

423

682

591

822

Loans & advances

733

892

1,027

1,418

1,731

2,158

Other

1,909

1,743

1,905

1,887

2,146

2,478

Current liabilities

2,337

2,406

2,529

2,084

2,146

2,425

Net current assets

939

784

826

1,903

2,323

3,033

Total Assets

4,997

5,033

5,006

6,150

6,561

7,257

November 2, 2015

8

Bharat Forge | 2QFY2016 Result Update

Cash flow statement (Consolidated)

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015 FY2016E FY2017E

Profit before tax

600

375

706

1,118

1,232

1,510

Depreciation

331

368

123

209

391

420

Change in working capital

218

77

(174)

(818)

(511)

(479)

Others

(31)

94

27

(0)

-

-

Direct taxes paid

(180)

(173)

(210)

(359)

(413)

(506)

Cash Flow from Operations

938

741

472

150

700

945

(Inc.)/Dec. in fixed assets

(834)

(740)

305

(532)

(350)

(350)

(Inc.)/Dec. in investments

(184)

29

(385)

306

(33)

(56)

Other income

(67)

139

17

(4)

-

-

Cash Flow from Investing

(1,085)

(572)

(63)

(230)

(383)

(406)

Issue of equity

-

-

-

-

-

-

Inc./(Dec.) in loans

532

(86)

(325)

357

(300)

(200)

Dividend paid (Incl. Tax)

(108)

(92)

(109)

(108)

(108)

(108)

Others

(40)

(69)

(107)

91

0

-

Cash Flow from Financing

385

(247)

(541)

339

(408)

(308)

Inc./(Dec.) in cash

237

(78)

(133)

259

(91)

231

Opening Cash balances

396

634

555

423

682

591

Closing Cash balances

634

555

423

682

591

822

November 2, 2015

9

Bharat Forge | 2QFY2016 Result Update

Key ratios

Y/E March

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

48.6

81.1

40.3

26.3

24.5

20.4

P/CEPS

28.1

34.4

23.5

17.8

16.6

14.3

P/BV

9.2

8.9

7.5

5.8

4.8

4.0

Dividend yield (%)

0.5

0.4

0.5

0.5

0.5

0.5

EV/Sales

3.3

3.7

3.0

2.7

2.6

2.2

EV/EBITDA

21.5

27.9

20.2

14.8

13.1

10.9

EV / Total Assets

4.3

4.3

4.2

3.5

3.2

2.8

Per Share Data (`)

EPS (Basic)

17.7

10.6

21.4

32.7

35.2

42.3

EPS (fully diluted)

17.8

9.8

11.5

27.8

35.2

42.3

Cash EPS

30.7

25.1

36.7

48.3

52.0

60.4

DPS

4.0

3.4

4.0

4.0

4.0

4.0

Book Value

93.8

96.9

115.2

147.9

178.5

216.9

Dupont Analysis

EBIT margin

11.1

7.6

10.0

14.1

15.1

15.8

Tax retention ratio

0.7

0.5

0.6

0.7

0.7

0.7

Asset turnover (x)

1.5

1.3

1.5

1.5

1.4

1.5

ROIC (Post-tax)

11.9

5.0

9.2

14.1

14.2

15.7

Cost of Debt (Post Tax)

6.1

4.1

4.8

4.1

4.0

4.0

Leverage (x)

0.6

0.6

0.4

0.3

0.3

0.2

Operating ROE

15.5

5.6

11.1

17.4

17.1

17.4

Returns (%)

ROCE (Pre-tax)

15.1

8.6

13.4

19.3

19.1

21.1

Angel ROIC (Pre-tax)

15.9

9.7

14.7

19.9

20.5

22.8

ROE

20.0

10.3

10.8

21.1

21.6

21.4

Turnover ratios (x)

Asset Turnover (Gross Block)

1.3

1.1

1.2

1.4

1.4

1.5

Inventory / Sales (days)

55

71

59

50

52

52

Receivables (days)

46

46

40

41

46

46

Payables (days)

126

147

128

91

89

87

WC cycle (ex-cash) (days)

18

15

22

58

79

87

Solvency ratios (x)

Net debt to equity

0.6

0.6

0.3

0.3

0.2

0.1

Net debt to EBITDA

1.3

1.8

0.8

0.8

0.6

0.2

Interest Coverage (EBIT / Int.)

3.7

2.3

4.0

8.0

9.2

12.2

November 2, 2015

10

Bharat Forge | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Bharat Forge

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 2, 2015

11