1QFY2017 Result Update | Capital Goods

August 11, 2016

Bharat Electronics (BEL)

BUY

CMP

`1,232

Performance Highlights

Target Price

`1,414

Quarterly highlights - Standalone

Investment Period

12 Months

Y/E March (` cr)

1QFY17

1QFY16

% chg (yoy)

Stock Info

Net sales

847

1,071

(20.9)

Sector

Capital Goods

EBITDA

(71)

(21)

nmf

Market Cap (` cr)

29,572

PAT

36

77

(52.9)

Net debt (` cr)

(7,524)

Source: Company, Angel Research; Note- nmf- Not Meaningful

Beta

1.1

Bharat Electronics Ltd (BEL) reported bad set of numbers for 1QFY2017. Its

52 Week High / Low

1,417/983

top-line declined by 20.9% yoy to `847cr, which is below our estimate. For the

Avg. Daily Volume

330,665

Face Value (`)

10

quarter, BEL reported below than expected negative EBITDA of `71cr. Negative

operating leverage in our view led to EBITDA de-growth. In-line with EBITDA de-

BSE Sensex

27,775

growth, PAT de-grew 52.9% yoy to `36cr. PAT margins were down 290bps yoy to

Nifty

8,575

4.3%, which is below our expectation.

Reuters Code

BAJE.BO

Bloomberg Code

BHE@IN

For 1QFY2017, BEL reported order inflows of

`1,003cr, which includes

Homeland Security, Navigational Complex System, and Next generation Main

Automatic Exchange order wins. Post these wins, order book as of 1QFY2017-

Shareholding Pattern (%)

end stood at `32,139cr. Order book/ last twelve month (LTM) sales ratio as of

Promoters

75.0

1QFY2017-end stood at 4.5x.

MF / Banks / Indian Fls

14.7

FII / NRIs / OCBs

3.9

Valuation: Despite disappointing quarterly results, we maintain our positive view

Indian Public / Others

6.4

towards the stock. Considering the delays in clearance from customer side, there

exists possibility of better 2Q revenue booking. On the back of continuous order

wins and strong order book, there exists some scope for the company delivering

Abs. (%)

3m 1yr 3yr

favorable performance going forward.

Sensex

8.5

(1.2)

46.6

On the back of strong market positioning, large order book, debt free status, we

BEL

6.5

(5.6)

211.6

expect BEL to report increased traction in sales and earnings growth, going

forward. We recommend BUY on the stock with price target of `1,414.

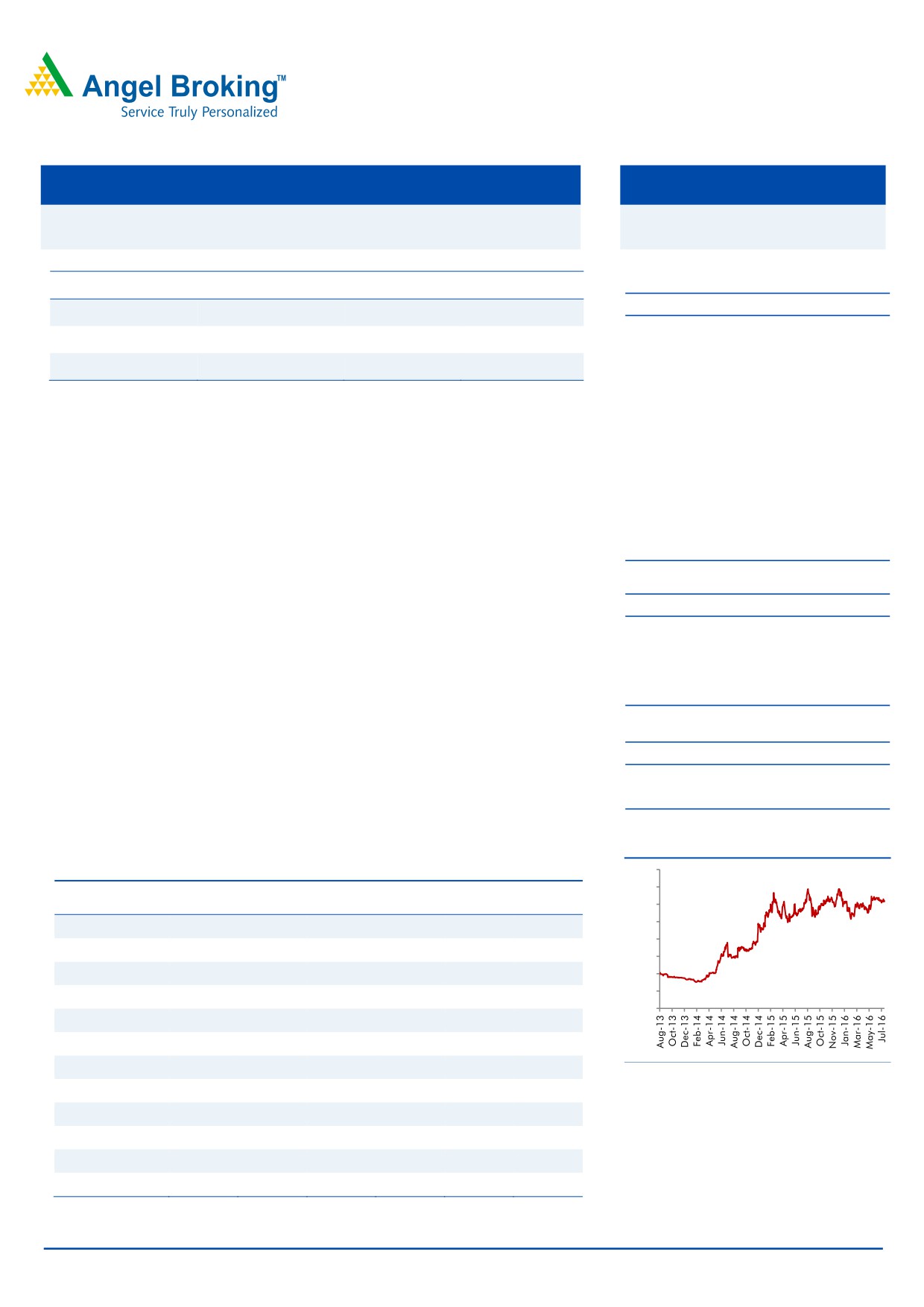

3-Year Daily Price Chart

Key Financials (Consolidated)

1600

1400

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

1200

1000

Net Sales

6,273

6,518

7,093

7,549

8,137

9,169

800

% chg

6.1

3.9

8.8

6.4

7.8

12.7

600

Net Profit

906

951

1,197

1,394

1,410

1,499

400

200

% chg

7.0

5.0

25.8

16.5

1.1

6.3

0

EBITDA (%)

10.6

14.1

16.6

20.4

16.8

17.2

EPS (`)

38

40

50

58

59

62

P/E (x)

32.5

31.1

24.7

21.3

21.0

19.7

Source: Company, Angel Research

P/BV (x)

4.6

4.1

3.6

3.3

3.0

2.8

Adj. RoE (%)

30.3

20.1

36.8

66.4

44.6

46.3

RoCE (%)

26.6

23.9

30.7

34.1

28.2

27.7

Yellapu Santosh

EV/Sales (x)

3.9

3.9

3.4

3.0

2.7

2.4

022 - 3935 7800 Ext: 6811

EV/EBITDA (x)

36.6

27.1

20.1

14.3

15.7

13.8

Source: Company, Angel Research; CMP as of August 10, 2016; Reported as per Ind AS, FY2016 numbers

& other remaining quarters continue to be reported as per Indian GAAP; It needs to be noted that yoy

growth for FY2017E is not comparable as FY2016 continues to be reported under Indian GAAP

Please refer to important disclosures at the end of this report

1

BEL | 1QFY2017 Result Update

Exhibit 1: Quarterly Performance (Standalone)

Particulars (` cr)

1QFY17*

1QFY16*

% chg (yoy)

Net Sales

847

1,071

(20.9)

Total Expenditure

918

1,092

(15.9)

Cost of materials consumed

673

683

(1.5)

Purchases of stock-in-trade

(203)

10

nmf

Employee benefits Expense

316

295

7.4

Other Expenses

132

104

27.1

EBITDA

(71)

(21)

nmf

EBIDTA %

(8.4)

(2.0)

Depreciation

43

41

6.7

EBIT

(115)

(62)

85.8

Interest and Financial Charges

0

0

nmf

Other Income

163

163

0.5

PBT before Exceptional Items

49

101

(51.8)

Exceptional Items

0

0

PBT after Exceptional Items

49

101

(51.8)

Tax

13

24

(48.0)

% of PBT

25.7

23.9

7.7

PAT from ordinary items

36

77

(52.9)

Other Comprehensive Items

13

13

Total Comprehensive Income

23

63

(63.5)

PAT %

4.3

7.2

Dil. EPS (after extra-ord. Items)

1.50

3.20

(53.1)

Source: Company, Angel Research; Note: nmf- Not meaningful;*Reported as per Ind AS, FY2016 numbers &

other remaining quarters continue to be reported as per Indian GAAP; It needs to be noted that yoy growth

for FY2017E is not comparable as FY2016 continues to be reported under Indian GAAP

Revenue reports 20.9% yoy sales de-growth

BEL reported 20.9% yoy sales de-growth in 1QFY2017 to `847cr, which is below

our expectation. Management attributed delays in customer clearances, to be the

key reason for miss on expected revenues front. Majority of the revenues for the

quarter has been from 3D Tactical Control Radar, Akash Weapons System for the

Indian Army.

Exhibit 2: Projects contributing to 1QFY2017 revenues

3D Tactical Control Radar

Akash Weapon System (Army)

New Generation Hull Mounted Sonar

L70 Gun Upgrade

Fire Control Systems

Source: Company, Angel Research

Management expects better revenue booking from 2QFY17 onwards, and has

maintained its 10% yoy top-line growth target for FY2017E.

Exports for 1QFY2017 grew ~47% yoy to $17mn (`116cr) in 1QFY2017.

August 11, 2016

2

BEL | 1QFY2017 Result Update

Reports negative operating margins

For the quarter, BEL reported below than expected, negative EBITDA of `71cr.

Negative operating leverage led to yoy EBITDA de-growth. EBITDA was impacted

on account of 27.1% yoy increase in other expenses to `132cr.

Operating performance restricts PAT growth

In-line with EBITDA de-growth, PAT de-grew 52.9% yoy to `36cr. PAT margins on

yoy basis were down 290bps to 4.3%, which is below our expectation. PAT margin

was also impacted on account of (1) just 0.5% yoy increase in other income to

`163cr, (2) 6.7% increase in depreciation expenses to `43cr, (3) higher effective

tax rate of 25.7%.

1QFY2017 Order Inflows at `1,003cr

BEL in 1QFY2017 reported `1,003cr of order inflows, which include Homeland

Security, Navigational Complex System, and Next generation Main Automatic

Exchange order wins.

We maintain our view that BEL would report order inflows of `18,000cr/`20,000cr

for FY2017/18E, respectively, considering the strong emerging bid pipeline.

Amongst the projects in the pipeline, we expect the company to report order wins

from Akash Missile Systems (7 sqdn), Tactical Communication System, Early

Warning Suite for Fighter Aircraft, Mobile Cellular Communication System, Ship

Data Network, Commander TI sights and Advanced Composite Communication

Systems.

The order book as of 1QFY2017-end stood at `32,139cr which gives revenue

visibility for the next two years. The order book/LTM sales ratio at 1QFY2017-end

stood at 4.5x.

Valuation

Despite weak quarterly numbers, we expect BEL to report strong financial

performance in the coming quarters (revenue booking post project clearance to be

seen in 2QFY2017). We expect BEL to report strong order inflows and revenues,

on the back of strong market positioning, large Order Book (which gives visibility

for next few quarters).

On the back of increase in order inflows, we are optimistic that the company

should see increased traction in sales and earnings growth, going forward. Since

our initiation report, the stock has attained our then recommended target price of

`1,414 but has thereafter corrected. Post the correction seen in the stock price, the

valuations has turned attractive. We maintain BUY on the stock with price target of

`1,414.

August 11, 2016

3

BEL | 1QFY2017 Result Update

Company background

BEL is a Bangalore based public sector undertaking (PSU) established in 1954

under the control of Ministry of Defence (MoD) to cater to specialised electronic

needs of the Indian Defense. BEL, a Nava-Ratna company, has over the years

grown to be a multi-segment, multi-technology company servicing a diverse range

of clients across India and in the international markets.

Business segments

BEL operates across 8 business segments, with ~20-30% of its current order book

contributed by its largest business segment- Radars, Sonars & Weapons Systems.

Exhibit 3: Business Segments

Radars, Sonars & Weapon Systems

Communication

Electronic Warfare

Network Centric Systems

Anti Submarine Warfare

Electro-Optics

Tank Electronics

Civilian Products (such as EVM machines

Source: Company, Angel Research

Details of Manufacturing Plants

To-date BEL has set-up 9 manufacturing plants across Bangalore (headquarters),

Chennai, Machilipatnam (post take-over of Andhra Scientific Company in 1983),

Hyderabad, Pune, Navi Mumbai, Panchkula, Kotdwara, and Ghaziabad, which

are into manufacture of entire range of defense products offered by the company.

Exhibit 4: Details of Manufacturing facilities

Production Facilities

Production details

(since)

Military Communication Equipment, Network Centric Systems,

Military Radars, Naval Systems, Electronic Warfare (Air-force),

Avionics, Weapon Management System, Telecom and

Bangalore (1966)

Broadcast System, Components, Coastal Surveillance System,

Electronic Voting Machines, Solar Products, Traffic Signals,

Security Systems, Microwave Super Components

Tank Electronics, Gun Upgrades, Multi-purpose Advanced

Chennai

Stabilized systems

Machilipatnam (1983) Electro-Optics (Night Vision Devices)

Hyderabad

Electronic Warfare Systems

Pune (1981)

X-ray Tubes, Batteries, Laser Products

Navi Mumbai

Shelters, Masks

Panchkula

Military Communication Equipment, Encryption Products

Kotdwara

Telecommunication Systems, Military Communication Systems

Network Centric Systems, Radars, Satcom (Defense),

Ghaziabad

Microwave components

Source: Company AR’s, Angel Research

August 11, 2016

4

BEL | 1QFY2017 Result Update

Investment Arguments

BEL is a PSU and a leader in the domestic defense electronics space, with a major

proportion of its revenue coming in from the Indian Navy and Army.

Defense spending at an inflexion point: After years of lull, the government

announced a 6.9% yoy increase in Defense Capital Budget to `69,705cr. In our

view, the company is at an inflexion point where Indian Defense capex cycle, led

by government spending is entering new era of growth. Our view strengthens on

account of the following developments, (1) Defense sector getting high priority in

government’s ‘Make in India’ campaign, with increased emphasis on the

indigenization aspect, (2) increase in FDI limits in defense from 26% to 49%, and

(3)

$50bn worth of projects cleared by Defense Acquisition Council (DAC) since the

new government has come to power, indicating faster clearances in place. Also the

recently released Defense Procurement Procedures (DPP) is good for the industry.

The current bid pipeline, which could lead to strong award activity for the next few

years, along with above-mentioned factors indicate that good times are ahead for

the Defense sector.

BEL to emerge as key beneficiary: At the backdrop of higher allocation made

towards defense capex with ~$50bn worth of projects cleared by DAC, we expect

good times ahead for defense players, including for BEL. BEL in FY2016 had a

market share of

~35% in domestic defense electronics.

(1) A bid-pipeline

dominated by Indian Airforce and Navy’s platform projects, which have high

Defense Electronics components requirement, (2) BEL’s in-house R&D capabilities,

(3) tie-up with Thales, France for product development, and (4) zero net debt status

with potential for further improvement in working capital cycle, all point out that

BEL would be able to maintain its strong market positioning in the Defense

Electronics space. On the whole, we expect BEL to emerge as a key beneficiary of

the revival in the defense capex cycle.

Risks & Concerns

To increase indigenization in the defense sector, the Government of India

(GoI) increased the FDI limit in the Defense sector to 49% in Jul-2014. Till

now, recent developments/ announcements have failed to attract any major

international defense players into India. With more positive announcements

expected and a fast growing bid pipeline, international defense giants could

be compelled to forge partnership with domestic players at the time of

bidding. This could possibly lead to loss of market share for BEL, which we

have not incorporated in to our estimates.

Last few years have seen sluggish ordering activity from the Defense sector.

Even though the Defense sector in the last few months has seen positive

announcements, any further delays in the awarding activity, could act as a risk

to our estimates.

Defense is a highly technology focused sector. BEL would have to continuously

spend on R&D to regularly upgrade its product profile. Any shift away from the

R&D could make their products unattractive (vs the peers), resulting in loss of

market share and further delays in execution.

August 11, 2016

5

BEL | 1QFY2017 Result Update

Any government announcement to de-list the products manufactured by BEL

could open up the competition and further impact their market positioning

within the domestic markets, which again acts as a risk to our market share

assumptions and threatens our earnings growth estimates.

Profit & Loss Statement (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

Net Sales

6,273

6,518

7,093

7,549

8,137

9,169

% Chg

6.1

3.9

8.8

6.4

7.8

12.7

Total Expenditure

5,610

5,596

5,918

6,008

6,773

7,589

Raw Materials Consumed

3,156

3,344

3,495

3,578

4,146

4,658

Purchase of stock-in-trade

760

444

440

339

423

452

Employee benefits Expense

1,125

1,046

1,281

1,323

1,406

1,564

Other Expenses

569

762

702

768

798

915

EBITDA

663

922

1,175

1,541

1,364

1,579

% Chg

4.3

39.1

27.4

31.2

(11.5)

15.8

EBIDTA %

10.6

14.1

16.6

20.4

16.8

17.2

Depreciation

136

150

166

200

218

243

EBIT

526

772

1,008

1,341

1,145

1,337

% Chg

3.2

46.6

30.6

33.0

(14.6)

16.7

Interest and Fin. Charges

1

4

3

6

7

7

Other Income

625

437

507

533

653

668

EBT before Excep & prior-

1,151

1,205

1,513

1,869

1,791

1,997

period items

Excep. & Prior period Items

(9)

1

1

0

0

0

EBT

1,142

1,206

1,513

1,869

1,791

1,997

Tax Expenses

236

254

316

475

381

498

% of PBT

20.7

21.1

20.9

25.4

21.3

24.9

PAT before Minority Interest

906

952

1,197

1,394

1,410

1,499

Minority Interest

0

0

(0)

(1)

0

1

PAT

906

951

1,197

1,394

1,410

1,499

% Chg

7.0

5.0

25.8

16.5

1.1

6.3

PAT %

14.4

14.6

16.9

18.5

17.3

16.3

Diluted EPS

38

40

50

57.8

58.7

62.5

% Chg

7.6

4.4

25.8

15.9

1.6

6.3

Reported as per Ind AS, FY2016 numbers & other remaining quarters continue to be reported as per

Indian GAAP; It needs to be noted that yoy growth for FY2017E is not comparable as FY2016

continues to be reported under Indian GAAP

August 11, 2016

6

BEL | 1QFY2017 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY13

FY14

FY15

FY16E FY17E FY18E

Sources of Funds

Equity Capital

80

80

80

240

240

240

Reserves & Surplus

6,407

7,140

8,037

8,746

9,579

10,444

Networth

6,487

7,220

8,117

8,986

9,819

10,684

Total Debt

0

0

25

29

30

35

Minority Interest & Govt. Grants

163

224

207

182

181

181

Other Long-term Liab. & Prov.

386

365

435

517

536

553

Total Liabilities

7,037

7,809

8,784

9,713

10,567

11,454

Application of Funds

Gross Block

2,106

2,366

2,894

3,254

3,659

4,082

Accumulated Depreciation

1,506

1,671

1,821

2,021

2,239

2,482

Net Block

600

695

1,073

1,233

1,420

1,600

Cap. WIP & Intan. Assets under

328

458

140

432

305

300

Develop.

Investments

0

0

0

242

242

242

Current Assets

Inventories

3,255

3,340

3,424

4,213

4,077

4,356

Sundry Debtors

3,364

4,156

3,805

3,741

3,966

4,431

Cash and Bank Balance

5,331

4,605

6,038

7,553

8,125

7,867

Loans & Advances

1,378

1,190

684

487

500

680

Other Current Asset

81

69

54

59

57

59

Current Liabilities

7,814

7,166

6,941

8,811

8,704

8,693

Net Current Assets

5,594

6,192

7,064

7,242

8,021

8,700

Other Assets

515

464

506

565

580

612

Total Assets

7,037

7,809

8,784

9,713

10,567

11,454

August 11, 2016

7

BEL | 1QFY2017 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY13

FY14 FY15 FY16E FY17E FY18E

Profit before tax

1,147

1,206

1,513

1,869

1,791

1,997

Dep. & Other Non-cash Charges

(338)

(336)

(163)

(417)

(238)

(238)

Change in Working Capital

(2,104)

(1,237)

436

1,338

(207)

(938)

Interest & Financial Charges

1

4

3

6

7

7

Direct taxes paid

(245)

(206)

(356)

(475)

(381)

(498)

Cash Flow from Operations

(1,540)

(569)

1,434

2,320

972

331

(Inc)/ Dec in Fixed Assets

(353)

(369)

(225)

(650)

(278)

(418)

(Inc)/ Dec in Invest. & Oth. Adj.

2,106

1,128

(614)

(141)

438

142

Cash Flow from Investing

1,753

759

(839)

(791)

160

(277)

Issue/ (Buy Back) of Equity

0

0

0

160

0

0

Inc./ (Dec.) in Borrowings

0

(0)

25

4

2

5

Dividend Paid (Incl. Tax)

(157)

(209)

(220)

(504)

(555)

(610)

Interest Expenses & Oth. Adj.

(1)

(4)

(14)

(6)

(7)

(7)

Cash Flow from Financing

(157)

(213)

(209)

(347)

(560)

(613)

Inc./(Dec.) in Cash

56

(23)

386

1,182

572

(558)

Opening Cash balances

1,752

1,809

1,786

2,171

3,353

3,925

Closing Cash balances

1,809

1,786

2,171

3,353

3,925

3,367

August 11, 2016

8

BEL | 1QFY2017 Result Update

Key Ratios (x)

Y/E March

FY13

FY14

FY15

FY16E FY17E FY18E

Valuation Ratio (x)

Adj. P/E (on FDEPS)

32.5

31.1

24.7

21.3

21.0

19.7

Adj. P/E (on FDEPS)

28.2

26.9

21.7

18.6

18.2

17.0

Dividend yield (%)

1.7

1.6

1.3

0.7

0.6

0.6

EV/Sales

3.9

3.9

3.4

3.0

2.7

2.4

EV/EBITDA

36.6

27.1

20.1

14.3

15.7

13.8

EV / Total Assets

3.4

3.2

2.7

2.3

2.0

1.9

Per Share Data (`)

Adj. EPS (fully diluted)

38

40

50

58

59

62

Cash EPS

44

46

57

66

68

73

DPS

7.4

7.8

9.7

18.0

19.8

21.7

Book Value

270

301

338

374

409

445

Returns (%)

RoCE (Pre-tax)

26.6

23.9

30.7

34.1

28.2

27.7

Angel RoIC (Pre-tax)

35.8

35.0

36.4

62.4

60.4

50.1

Adj. RoE

30.3

20.1

36.8

66.4

44.6

46.3

Turnover ratios (x)

Asset Turnover (Gross Block) (x)

2.9

2.8

2.6

2.4

2.3

2.3

Inventory / Sales (days)

178

190

179

189

191

172

Receivables (days)

180

217

211

187

177

171

Payables (days)

541

489

435

479

472

418

WC (days)

(183)

(82)

(45)

(103)

(104)

(76)

Leverage Ratios (x)

D/E ratio (x)

0.0

0.0

0.0

0.0

0.0

0.0

August 11, 2016

9

BEL | 1QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Bharat Electronics

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

August 11, 2016

10