3QFY2017 Result Update | Banking

February 15, 2017

Bank Of Baroda

NEUTRAL

CMP

`168

Performance Highlights

Target Price

-

Particulars (` cr)

Q3FY17

Q2FY17

% chg (qoq)

Q3FY16

% chg (yoy)

Investment Period

NII

3,134

3,426

(8.5)

2,705

15.9

Pre-prov. profit

2,595

2,690

(3.5)

1,704

52.3

Stock Info

PAT

253

552

(54)

(3342)

(107.6)

Source: Company, Angel Research

Sector

Banks

Market Cap (` cr)

37,546

BoB’s 3QFY17 results remained disappointing. The bank continues to face

headwinds on asset quality on one hand, while on the other hand the balance

Beta

1.5

sheet continued to de-grow as the management intentionally downsized some low

52 Week High / Low

192/126

margin business. Coming few quarters might be challenging for the bank.

Avg. Daily Volume

1,148,032

Loan book continued to decline as overseas portfolio downsized: Overall loan

Face Value (`)

2

growth declined by 8.9% YoY, as the overseas loan portfolio decline by 20.1%

BSE Sensex

28,156

YoY. The management has taken a cautious call of downsizing the low margin

Nifty

8,725

portfolio like buyers credit and hence there was de growth in loan book. While the

Reuters Code

BOB.BO

bank intends to focus on profitable segment and lend selectively, this might take a

Bloomberg Code

BOB@IN

toll on the overall growth in the near term. While CASA growth remained strong

up 25% YoY, the bank’s overseas deposit portfolio declined by 14.1%YoY and

hence overall deposit base remained flat YoY, but saw a 3.9% growth QoQ.

Shareholding Pattern (%)

NIM was under pressure, likely to remain subdued in the near term: NIM was

Promoters

59.2

under pressure and declined to 2.06% vs 2.29% QoQ due to interest reversals to

MF / Banks / Indian Fls

22.6

the tune of `260 cr. The bank as a strategy has been downsizing the overseas

FII / NRIs / OCBs

12.1

loan book, which attracts very low margin and higher contribution from the

Indian Public / Others

6.1

domestic business can lead to better margins in the long run, however in the near

term we expect NIM to remain under pressure.

No Respite from asset quality issues: While the bank has been maintaining that

Abs.(%)

3m 1yr 3yr

large part of the asset quality might get over, the slippages remained elevated.

Sensex

7.0

19.5

38.2

Gross slippages of `4135cr (slippages ratio of 4.16%) was much higher than

Bank of Baroda

(6.4)

16.9

52.2

`2,861cr (slippage ratio of 2.84%) in 2QFY17. Though slippages remained high,

aggressive write off resulted in sequential decline in GNPAs. GNPAs % for the

quarter stood at 11.4% vs 11.35% qoq, while NNPA% was at 5.43% vs 5.46%.The

3-year price chart

250

bank intends to improve its provisioning coverage ratio and hence in absolute

terms the provisions might remain high in the quarters to come.

200

Outlook and valuation: With continued pressure on asset quality and resultant

150

credit cost the earnings of the bank might remain under pressure in the near term

100

Further as the bank is looking to downsize the low margin business the overall

loan growth might disappoint and the stock might remain range bound. At the

50

current market price, the stock is trading at 1.7x FY2018E ABV.We have a

0

NEUTRAL rating on the stock.

Key financials (Standalone)

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

Source: Company, Angel Research

NII

13,187

12,740

13,532

15,445

% chg

10.2

(3.4)

6.2

14.1

Net profit

3,398

(5,393)

1,670

3,417

% chg

(25.7)

(258.7)

(131.0)

104.6

NIM (%)

2.0

1.9

2.1

2.2

EPS (`)

15.3

(23.3)

7.2

14.8

P/E (x)

11.1

(7.3)

23.5

11.5

P/ABV (x)

1.2

1.9

1.8

1.7

Siddharth Purohit

RoA (%)

0.5

(0.8)

0.2

0.5

022 - 3935 7800 Ext: 6872

RoE (%)

9.0

(13.5)

4.1

8.0

Source: Company, Angel Research; Note: CMP as of February 14, 2017

Please refer to important disclosures at the end of this report

1

Bank Of Baroda | 3QFY2017 Result Update

Exhibit 1: 3QFY17 Income Statement ( Standalone)

Particulars (` cr)

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

% YoY

% QoQ

Interest earned

11,276

11,156

10,614

11,014

10,434

10,485

10,406

(2.0)

(0.8)

- on Advances / Bills

8,033

7,712

7,169

6,882

7,162

6,840

6,736

(6.0)

(1.5)

- on investments

2,651

2,739

2,686

2,689

2,495

2,533

2,719

1.2

7.3

- on balance with RBI & others

296

291

353

365

325

392

521

47.3

32.9

- on others

297

414

406

1,077

452

721

430

6.1

(40.3)

Interest Expended

7,817

7,912

7,909

7,684

7,062

7,059

7,272

(8.1)

3.0

Net Interest Income

3,460

3,244

2,705

3,330

3,371

3,426

3,134

15.9

(8.5)

Other income

967

1,144

1,113

1,775

1,444

1,561

1,775

59.5

13.7

- Fee income

519

841

799

1162

848

948

887

11.0

(6.4)

- Treasury income

435

224

289

509

557

546

839

190.3

53.7

- Others

13

79

24

104

39

68

49

104.2

(27.9)

Operating income

4,427

4,389

3,818

5,105

4,815

4,988

4,909

28.6

(1.6)

Operating expenses

2,223

2,051

2,114

2,533

2,146

2,297

2,314

9.5

0.7

- Employee expenses

1,343

1,044

1,155

1,434

1,108

1,169

1,139

(1.4)

(2.5)

- Other Opex

880

1,008

959

1,098

1,038

1,129

1,175

22.5

4.1

Pre-provision Profit

2,204

2,337

1,704

2,572

2,669

2,690

2,595

52.3

(3.5)

Provisions & Contingencies

600

1,892

6,165

6,858

2,004

1,796

2,080

(66.3)

15.8

PBT

1,604

445

(4,460)

(4,285)

665

894

516

(111.6)

(42.3)

Provision for Tax

550

321

(1,118)

(1,055)

242

342

263

(123.5)

(23.1)

PAT

1,054

124

(3,342)

(3,230)

424

552

253

(107.6)

(54.2)

Effective Tax Rate (%)

34

72

25

25

36

38

51

Source: Company, Angel Research

February 15, 2017

2

Bank Of Baroda | 3QFY2017 Result Update

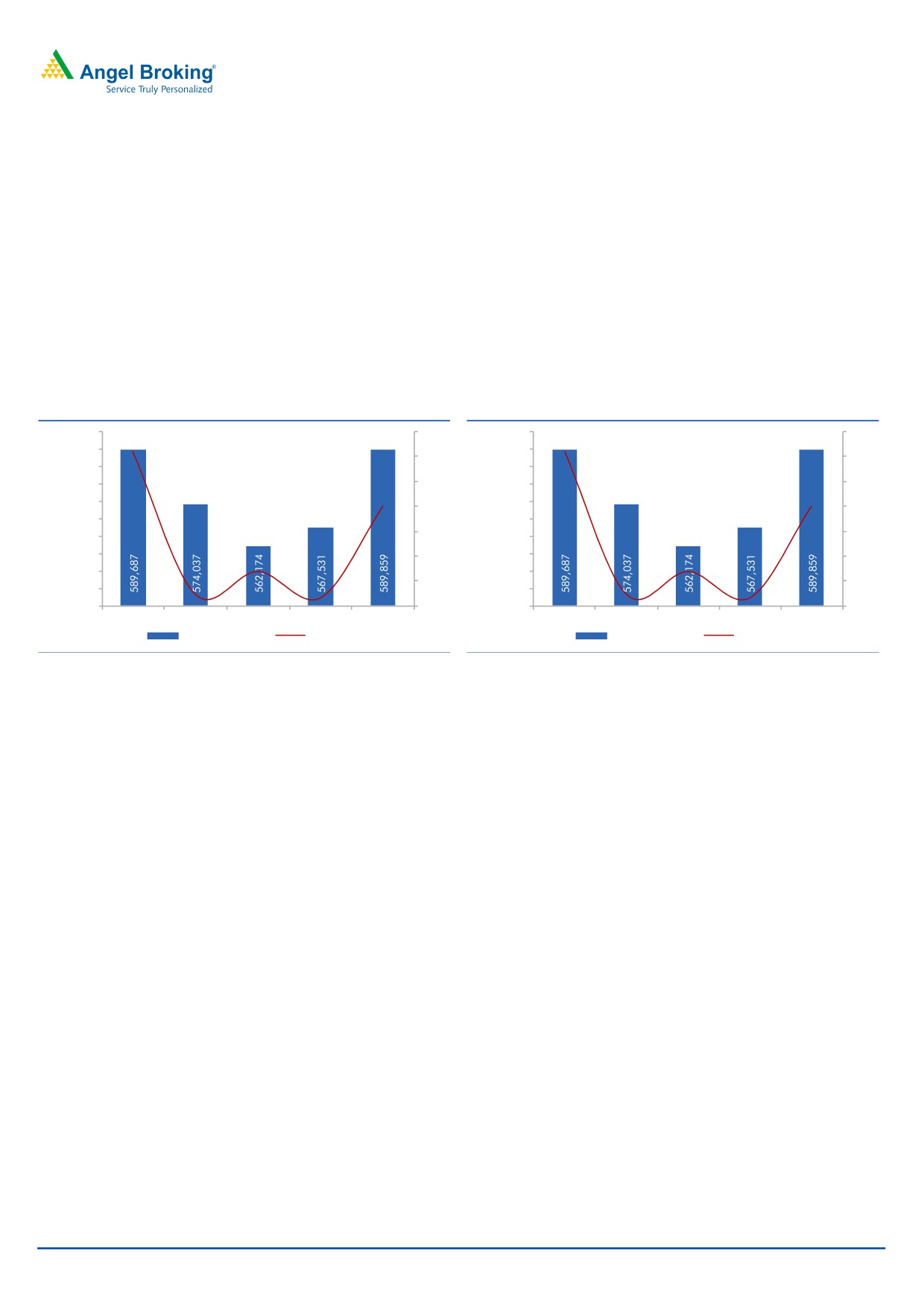

Loan book continued to decline as overseas portfolio downsized: Overall loan

growth declined by

8.9% YoY, as the overseas loan portfolio decline by

20.1% YoY. The management has taken a cautious call of downsizing the low

margin portfolio like buyers credit and hence there was de growth in loan book.

While the bank intends to focus on profitable segment and lend selectively, this

might take a toll on the overall growth in the near term

Despite high growth in CASA, decline in overseas deposits resulted in overall

decline in deposit base: While CASA growth remained strong up 25% YoY, the

bank’s overseas deposit portfolio declined by 14.1%YoY and hence overall deposit

base remained flat YoY, but saw a 3.9% growth QoQ.

Exhibit 2: Loan book continued to decline

Exhibit 3: Deposit base remained flat

595,000

6.0

595,000

6.0

590,000

4.4

590,000

4.4

4.0

4.0

585,000

585,000

580,000

2.0

580,000

2.0

575,000

575,000

0.0

0.0

0.0

0.0

570,000

570,000

(2.0)

(2.0)

565,000

565,000

560,000

(4.0)

560,000

(4.0)

555,000

(5.2)

555,000

(5.2)

(7.0)

(6.0)

(7.0)

(6.0)

550,000

550,000

(7.3)

(7.3)

545,000

(8.0)

545,000

(8.0)

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Deposits (` Cr)

% Growth YoY

Deposits (` Cr)

% Growth YoY

Source: Company, Angel Research

Source: Company, Angel Research

February 15, 2017

3

Bank Of Baroda | 3QFY2017 Result Update

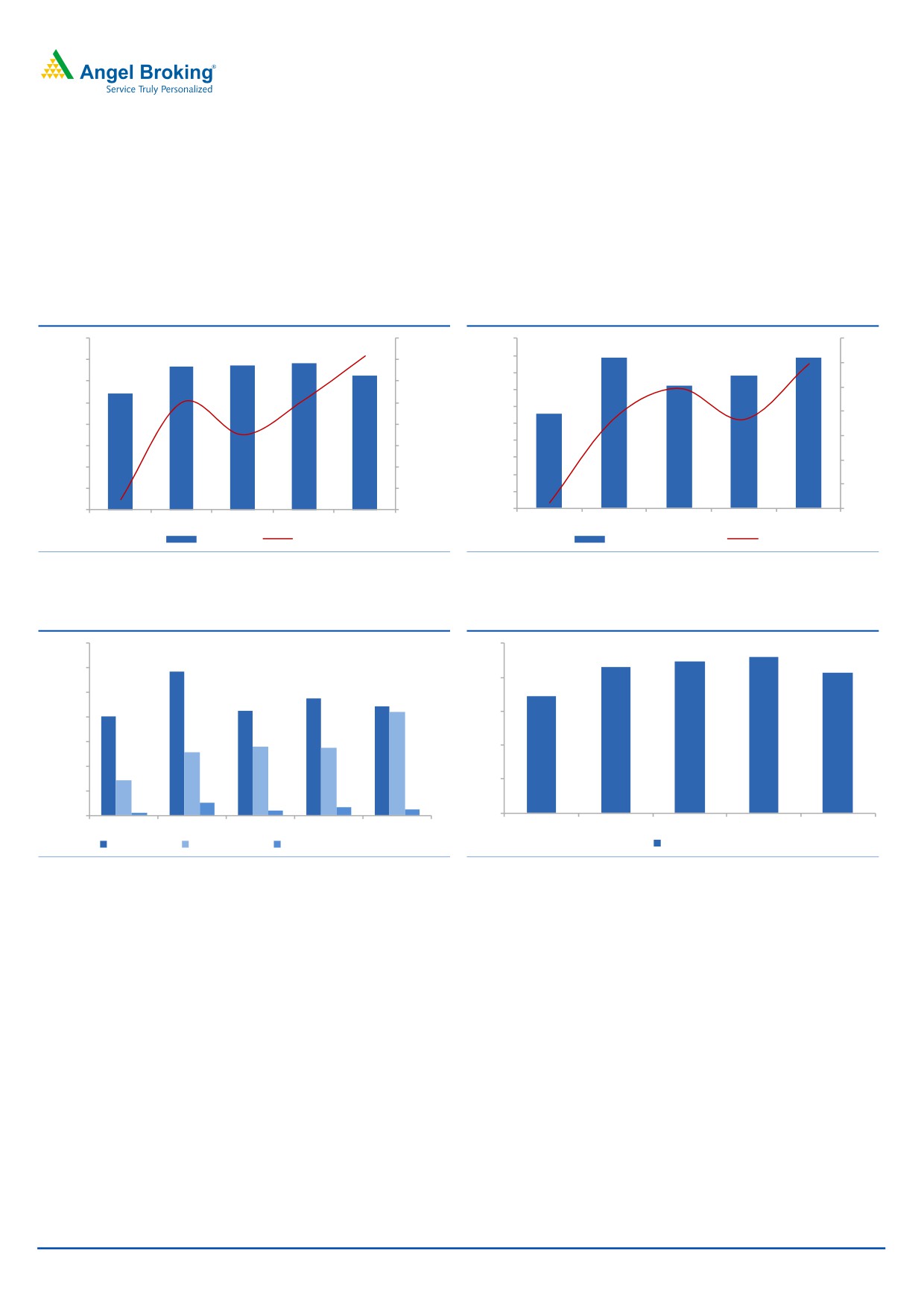

NIM was under pressure, likely to remain subdued in the near term: NIM was

under pressure and declined to 2.06% vs 2.29% QoQ due to interest reversals to

the tune of `260 cr. The bank as a strategy has been downsizing the overseas loan

book, which attracts very low margin and higher contribution from the domestic

business can lead to better margins in the long run, however in the near term we

expect NIM to remain under pressure.

Exhibit 4: NII Growth was on a low base

Exhibit 5: Other income got boost from treasury gain

4,000

20.0

2,000

70.0

15.9

1,775

1,775

3,371

3,426

3,330

1,800

3,500

15.0

1,561

60.0

3,134

59.5

1,600

1,444

3,000

2,705

10.0

1,400

49.3

50.0

5.0

5.6

2,500

5.0

1,113

1,200

40.0

37.0

36.5

2,000

0.0

1,000

(2.6)

800

30.0

1,500

(5.0)

600

20.0

1,000

(10.0)

400

10.0

500

(15.0)

200

(17.7)

2.1

-

(20.0)

-

0.0

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

NII (` Cr)

% YoY

Other Income (` Cr)

% YoY

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 6: Break Up Of Other Income

Exhibit 7: NIM Trend

1,400

2.5

2.3

2.2

2.2

1,162

2.1

1,200

2.0

948

1.7

1,000

887

848

839

799

1.5

800

557

546

600

509

1.0

400

289

0.5

200

104

68

49

24

39

-

-

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Fees Income

Trading Gains

Recovery From Writeen off ac

NIM % ( Global)

Source: Company, Angel Research

Source: Company, Angel Research

February 15, 2017

4

Bank Of Baroda | 3QFY2017 Result Update

No Respite from asset quality issues: While the bank has been maintaining that

large part of the asset quality might get over, the slippages remained elevated.

Gross slippages of `4135 cr (slippages ratio of 4.16%) was much higher than

` 2861 cr (slippage ratio of 2.84%). While recovery and up gradation combined at

`2667 cr remained flat qoq, there was sharp spike in write off - `1775 cr vs ` 216

cr in 2QFY17. Though slippages remained high, aggressive write off resulted in

sequential decline in GNPAs. GNPAs % for the quarter stood at 11.4% vs 11.35%

qoq, while NNPA% was at 5.43% vs 5.46%. Total stressed assets stood at 18.6% of

the book (GNPAs 11.4%+Restructured 7.2%).

Outstanding restructured book was at `29,019 cr vs `28,464 cr, of which

standard restructured was `14,059 cr vs `13,860 cr qoq. Outstanding S4A

accounts were at `1,948 cr, accounts under DSR were at `6,944 cr, while accounts

where 5:25 has been implemented were to the tune of `7,408cr. Asset quality

issues continue to impact the performance of BoB and the trend doesn’t seem to

be reversing any time soon.

Exhibit 8: GNNPAs & NNPAs remained stable

Exhibit 9: Restructured loan book saw marginal rise

12.00

5.80

30,500

5.73

5.67

11.40

29,801

11.35

30,000

11.50

5.60

29,500

11.15

29,004

29,019

11.00

5.40

29,000

5.43

28,464

5.46

10.50

28,500

5.20

28,000

10.00

9.99

5.06

27,500

5.00

9.50

9.68

26,938

27,000

9.00

4.80

26,500

26,000

8.50

4.60

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

25,500

GNPAs (%)

NNPAs (%)

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 10: Slippages ratio remained elevated

Exhibit 11: Credit cost went up further

16.0

8.0

14.6

14.0

7.0

7.1

6.4

12.0

6.0

10.0

5.0

8.0

4.0

6.0

5.8

5.8

3.0

2.4

4.0

4.2

2.0

2.2

2.0

2.0

2.8

1.0

-

-

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Slippages Ratio %

Credit Cost Annualized

Source: Company, Angel Research

Source: Company, Angel Research

February 15, 2017

5

Bank Of Baroda | 3QFY2017 Result Update

Outlook and Valuation

With continued pressure on asset quality and resultant credit cost the earnings of

the bank might remain under pressure in the near term. Further as the bank is

looking to downsize the low margin business the overall loan growth might

disappoint. At the current market price, the stock is trading at 1.7x FY2018E

ABV.We have a NEUTRAL rating on the stock.

Company Background

Bank Of Baroda is one of the leading PSU banks and has large overseas presence.

Looking at the lower margin in the overseas business the management is trimming

down it international business .International business contributed ~27% of the total

business for the bank at the end of the quarter. In the domestic market the bank

has got 5,382 branches and 10,404 ATMs.

February 15, 2017

6

Bank Of Baroda | 3QFY2017 Result Update

Income statement (Standalone)

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

Net Interest Income

11,965

13,187

12,740

13,532

15,445

- YoY Growth (%)

5.7

10.2

(3.4)

6.2

14.1

Other Income

4,463

4,402

4,999

5,969

5,328

- YoY Growth (%)

22.9

(1.4)

13.6

19.4

(10.7)

Operating Income

16,428

17,589

17,739

19,501

20,772

- YoY Growth (%)

9.9

7.1

0.9

9.9

6.5

Operating Expenses

7,106

7,674

8,921

9,104

9,600

- YoY Growth (%)

19.5

8.0

16.2

2.1

5.4

Pre - Provision Profit

9,322

9,915

8,818

10,396

11,172

- YoY Growth (%)

3.6

6.4

(11.1)

17.9

7.5

Prov. & Cont.

3,794

4,495

15,514

7,690

5,782

- YoY Growth (%)

(9.0)

18.5

245.2

(50.4)

(24.8)

Profit Before Tax

5,529

5,421

(6,696)

2,706

5,390

- YoY Growth (%)

14.4

(2.0)

(223.5)

(140.4)

99.2

Prov. for Taxation

956

2,022

(1,303)

1,036

1,973

- as a % of PBT

172.8

111.5

(164.4)

(179.5)

90.4

PAT

4,572

3,398

(5,393)

1,670

3,417

- YoY Growth (%)

2.0

(25.7)

(258.7)

(131.0)

104.6

Balance sheet (Standalone)

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

Share Capital

431

444

462

462

462

Reserve & Surplus

35,555

39,392

39,737

41,240

43,672

Net Worth

35,986

39,835

40,199

41,702

44,134

Deposits

568,894

617,560

574,037

595,757

683,401

- Growth (%)

20.0

8.6

-7.0

3.8

14.7

Borrowings

36,813

35,264

33,472

35,745

41,004

- Growth (%)

38.5

-4.2

-5.1

6.8

14.7

Other Liab. & Prov.

17,811

22,329

23,668

23,830

27,336

Total Liabilities

659,505

714,989

671,376

697,035

795,874

Cash in Hand and with RBI

18,629

22,489

21,672

23,830

27,336

Bal.with banks & money at call

112,249

125,865

112,228

107,236

123,012

Investments

116,113

116,812

120,451

166,812

191,352

Advances

397,006

428,065

383,770

362,209

409,609

- Growth (%)

21.0

7.8

-10.3

-5.6

13.1

Fixed Assets

2,734

2,875

6,254

6,553

6,834

Other Assets

12,774

18,883

27,001

30,394

37,731

Total Assets

659,505

714,989

671,376

697,035

795,874

February 15, 2017

7

Bank Of Baroda | 3QFY2017 Result Update

Ratio analysis (Standalone)

Y/E March

FY14

FY15

FY16

FY17E

FY18E

Profitability Ratios (%)

NIMs

2.0

2.0

1.9

2.1

2.2

Cost to Income Ratio

43.3

43.6

50.3

46.7

46.2

RoA

0.8

0.5

-0.8

0.2

0.5

RoE

13.5

9.0

-13.5

4.1

8.0

B/S ratios (%)

CASA Ratio

25.7

26.4

24.1

0.0

0.0

Credit/Deposit Ratio

69.8

69.3

66.9

60.8

59.9

CAR

13.9

12.6

13.2

12.4

12.0

- Tier I

10.8

9.9

10.8

9.2

9.0

Asset Quality (%)

Gross NPAs

2.9

3.7

10.0

10.6

8.5

Net NPAs

1.5

1.9

5.1

5.3

5.1

Slippages

2.0

2.0

6.5

3.9

1.7

Loan Loss Prov./Avg. Assets

1.0

1.0

4.0

2.1

1.4

Provision Coverage

49.2

50.4

52.1

45.0

45.0

Per Share Data (`)

EPS

21.2

15.3

-23.3

7.2

14.8

ABVPS

137

143

90

97

101

DPS

4.4

4.7

4.9

2.5

4.0

Valuation Ratios

PER (x)

8.0

11.1

-7.3

23.5

11.5

P/ABVPS (x)

1.2

1.2

1.9

1.8

1.7

Dividend Yield

2.6

2.8

2.9

1.5

2.4

DuPont Analysis (%)

Interest Income

6.5

6.3

6.4

6.2

6.2

Interest Expenses

4.5

4.3

4.5

4.2

4.1

NII

2.0

1.9

1.8

2.0

2.1

Non Interest Income

0.7

0.6

0.7

0.9

0.7

Total Revenues

2.7

2.6

2.6

2.9

2.8

Operating Cost

1.2

1.1

1.3

1.3

1.3

PPP

1.5

1.4

1.3

1.5

1.5

Total Provisions

0.6

0.7

2.2

1.1

0.8

PreTax Profit

0.9

0.8

-1.0

0.4

0.7

Tax

0.2

0.3

-0.2

0.2

0.3

ROA

0.8

0.5

-0.8

0.2

0.5

Leverage

17.8

18.1

17.3

16.7

17.4

RoE (%)

13.5

9.0

-13.5

4.1

8.0

February 15, 2017

8

Bank Of Baroda | 3QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Bank Of Baroda

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 15, 2017

9