1QFY2018 Result Update | Automobile

24 July 2017

Bajaj Auto

ACCUMULATE

CMP

`2,815

Performance Highlights

Target Price

`3,151

Y/E March (` cr)

Q1FY18

Q1FY17

% chg (yoy) Q4FY17

% chg (qoq)

Investment Period

12 Months

Net Sales

5,442

5,748

-5.3

4,897

11.1

EBITDA

938

1,176

-20.2

906

3.6

Stock Info

EBITDA Margin (%)

17.2

20.5

-322 bp

18.5

-126 bp

Sector

Automobile

Adj. PAT

956

978

-2.3

802

19.2

Market Cap (` cr)

81,457

Source: Company, Angel Research

Net Debt (` cr)

(88.4)

Beta

0.9

Results below estimates on weak sales: Bajaj Auto reported weak Q1 result due to

52 Week High / Low

3,122/2,510

lower volumes sold in the quarter and higher RM cost. Revenue and EBITDA were

Avg. Daily Volume

31,565

1.5% and 13% below the consensus estimates respectively. Though PAT beat the

Face Value (`)

10

street estimates by 2%, this was due to 71% jump in the other income (dividend by

BSE Sensex

32,029

KTM). Net sales and PAT declined by 5% (yoy) and 6% (yoy) respectively to

Nifty

9,915

`5,442cr and `524cr. EBITDA declined by 20% (yoy) to `938cr due to sharp

increase in RM costs. EBITDA margin was at 17.2% vs. 18.5% in 4QFY17 and

Reuters Code

BAJA NS

20.5% in 1QFY17. PAT declined by 5.5% (yoy), slower than decline in operating

Bloomberg Code

BJAUT IN

profit due to steep increase in other income. Adjusted for `32cr exceptional

expenses (GST led dealer compensation), Q1 PAT is at

`956cr. Blended

Shareholding Pattern (%)

realization was at `59,976 showing a yoy growth of 5.7% and qoq decline of

Promoters

49.3

1.7%. RM cost per vehicle accelerated by 10% yoy (faster than realization)

MF / Banks / Indian Fls

8.3

reflecting higher RM prices. In the nutshell, the GST led destocking by the dealers

FII / NRIs / OCBs

17.5

in June and higher RM costs led to the weak results during this quarter.

Indian Public / Others

24.9

The company has guided of pick up in volumes in the remainder of the year. It

has indicated of a monthly run rate of ~21,000 in domestic 3Ws in 2Q/3Q of

Abs. (%)

3m 1yr 3yr

FY18 while in exports, it expects to clock ~1.8mn export sales volumes despite

volatility in the markets. Company is likely to announce a deal with a premium

Sensex

9.1

14.7

24.5

segment motorcycle manufacturer in next two weeks which needs to be watched

Bajaj Auto

0.2

1.7

35.9

carefully. There will be no new launches in FY18E and company expects ~19.5%-

20% EBITDA margin in FY18E vs. >20% margins FY16 and FY17 each.

Outlook and valuation: We expect Bajaj Auto to report 13.3%/12.5% CAGR in

sales/PAT over the next two years and maintain ROE over ~22%. We value Bajaj

Auto at 18.0x of FY19E EPS to `2,845/share and add KTM stake value of

`139/share. We derive a target price of `3,151 with an accumulate rating.

Key financials (Standalone)

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

Net Sales

21,612

22,688

21,767

23,936

27,955

% chg

7.3

5.0

(4.1)

10.0

16.8

Net Profit

3,154

3,652

3,828

4,163

4,842

% chg

(2.8)

15.8

4.8

8.8

16.3

OPM (%)

19.0

21.1

20.3

19.5

20.1

EPS (Rs)

97.2

126.2

132.3

142.7

167.3

P/E (x)

29.0

22.3

21.3

19.7

16.8

P/BV (x)

7.6

6.1

4.8

4.3

3.8

RoE (%)

26.3

27.5

22.5

21.7

22.8

RoCE (%)

35.4

33.2

23.9

22.7

24.6

EV/Sales (x)

3.8

3.6

3.7

3.4

2.9

Shrikant Akolkar

EV/EBITDA (x)

19.7

16.9

18.4

17.4

14.4

022-3935 7800 Ext: 6846

Source: Company, Angel Research; Note: CMP as of July 21, 2017

Please refer to important disclosures at the end of this report

1

Bajaj Auto | 1QFY2018 Result Update

Exhibit 1: Quarterly financial performance (Standalone)

Y/E March (` cr)

Q1FY18

Q1FY17

% chg (yoy)

Q4FY17

% chg (qoq)

Total operating income

5,442

5,748

-5.3

4,897

11.1

Raw material consumption

3,809

3,863

-1.4

3,320

14.7

% of total operating inhume

70.0

67.2

67.8

Employee expense

273

268

1.6

227

19.9

% of total operating income

5.0

4.7

4.6

Other expenditure

422

441

-4.2

444

-4.9

% of total operating income

7.8

7.7

9.1

Total expenditure

4,504

4,572

-1.5

3,991

12.8

% of total operating income

83

80

82

EBIDTA

938

1,176

-20.2

906

3.6

EBITDA margin (%)

17.2

20.5

18.5

Depreciation and Ammortisation

75

77

-2.9

76

-0.6

EBIT

863

1,099

-21.4

830

4.0

Other Income

457

267

71.2

294

55.7

Net Interest exp

0

0

9.1

0

0.0

Profit before tax (PBT)

1,320

1,365

-3.3

1,124

17.5

Taxes

364

387

-6.0

322

13.2

% of PBT

27.6

28.4

28.6

Extraordinary income/(expense)

32

0

0

Reported PAT

924

978

-5.5

802

15.2

Adjusted PAT

956

978

-2.3

802

19.2

Equity capital

289

289

289

Reported EPS (`)

33.0

33.8

-2.3

27.7

19.2

Adjusted EPS (`)

33.0

33.8

-2.3

27.7

19.2

Source: Company, Angel Research

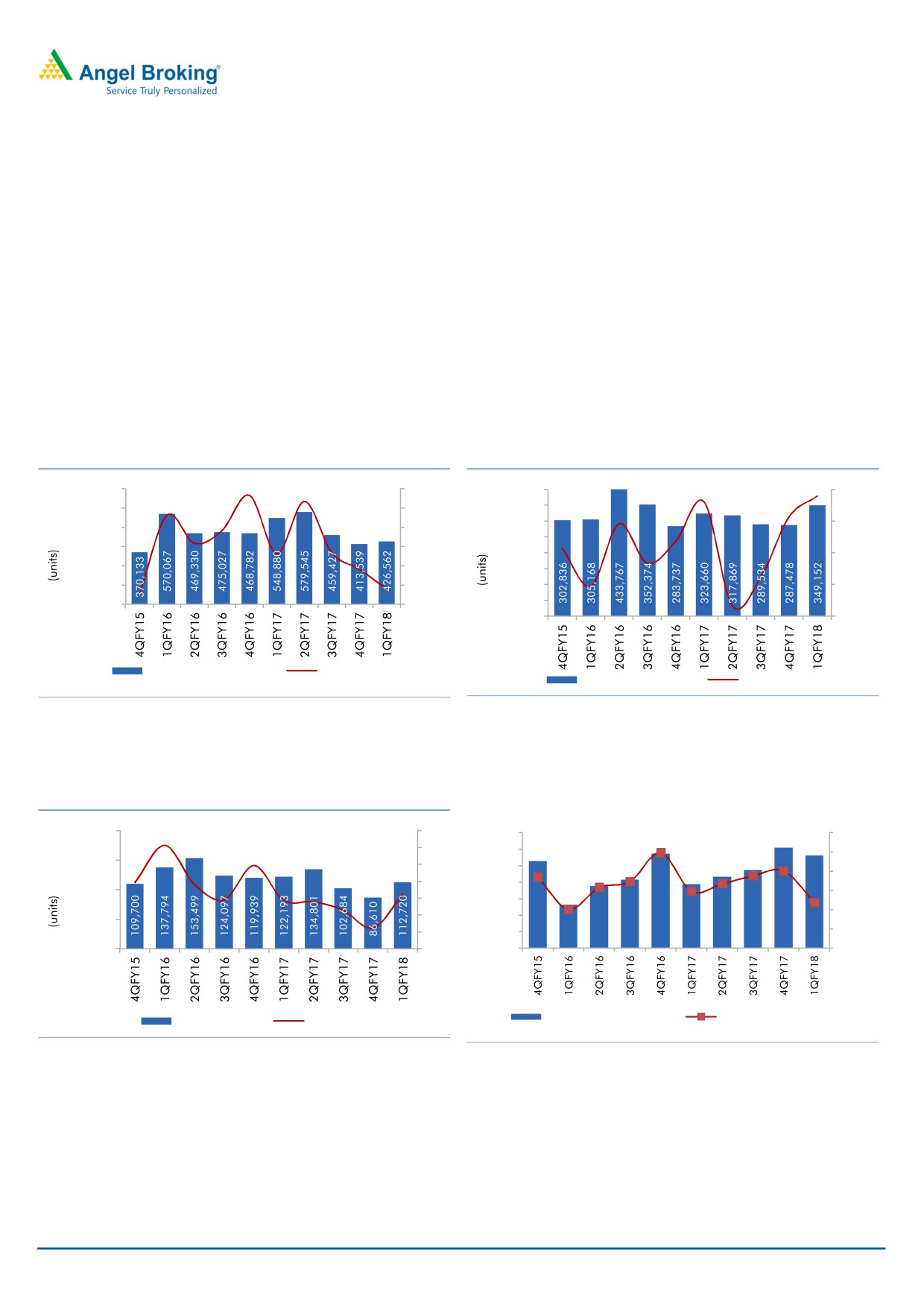

Exhibit 2: Quarterly volume performance

Y/E March

1QFY18

1QFY17

% chg (yoy)

4QFY17

% chg (qoq)

Motorcycles (Domestic)

426,562

548,880

-22.3

413,539

3.1

Motorcycles (Exports)

349,152

323,660

7.9

287,478

21.5

Total Motorcycles

775,714

872,540

-18.5

701,017

-20.4

Three wheeler (Domestic)

52,347

75,204

-30.4

50,037

4.6

Three wheeler (Exports)

60,373

46,989

28.5

36,573

65.1

Total Three wheeler

112,720

122,193

-0.7

86,610

-21.3

Overall Domestic

478,909

624,084

-23.3

463,576

3.3

Overall Exports

409,525

370,649

10.5

324,051

26.4

Total volumes

888,434

994,733

-16.4

787,627

-20.5

Source: Company, Angel Research

Bajaj Auto has continued to report decline in the domestic volumes for the

third quarters in row. Domestic volumes at 478,909, declined by 23%.

Exports volumes were at 409,525 grew by 10% yoy, in line with management

expectation of revival in the export volumes. Company has indicated that

July 24, 2017

2

Bajaj Auto | 1QFY2018 Result Update

entering in the new countries has been a successful strategy and has helped to

reduce the dependence on high volume countries like Sri Lanka, Nigeria, etc.

Domestic vehicle realisation/unit grew 8% yoy to `68,099, led by the price

hikes. Export realization was at `60,534 per unit, showing a yoy growth of 9%.

Company realized `66.8/USD in 1QFY2018 as against `67.1/USD accrued

in 1QFY2017.

Contribution/vehicle declined by 3% yoy and 8% qoq due to higher material

costs and weak sales.

Blended realization was at `59,976/vehicle showing a yoy growth of 5.7%

and qoq decline of 1.7%.

Exhibit 3: Domestic 2W volumes decline by 22% yoy

Exhibit 4: Exports showing a recovery

700,000

30.0

400,000

10.0

600,000

20.0

350,000

300,000

0.0

500,000

10.0

250,000

400,000

0.0

200,000

(10.0)

300,000

(10.0)

150,000

200,000

(20.0)

100,000

(20.0)

100,000

(30.0)

50,000

0

(30.0)

Domestic 2W volumes

yoy growth

Export two-wheelers

yoy growth

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 5: 3W volumes remain subdued

Exhibit 6: Blended realizations and contribution decline

200,000

30.0

64,000

22,000

20.0

62,000

21,000

150,000

10.0

60,000

20,000

0.0

58,000

100,000

19,000

(10.

56,000

18,000

(20.

54,000

50,000

(30.

52,000

17,000

0

(40.

50,000

16,000

Realisation/vehicle (`)

Contribution/vehicle (`)

Three wheelers

yoy growth

Source: Company, Angel Research

Source: Company, Angel Research

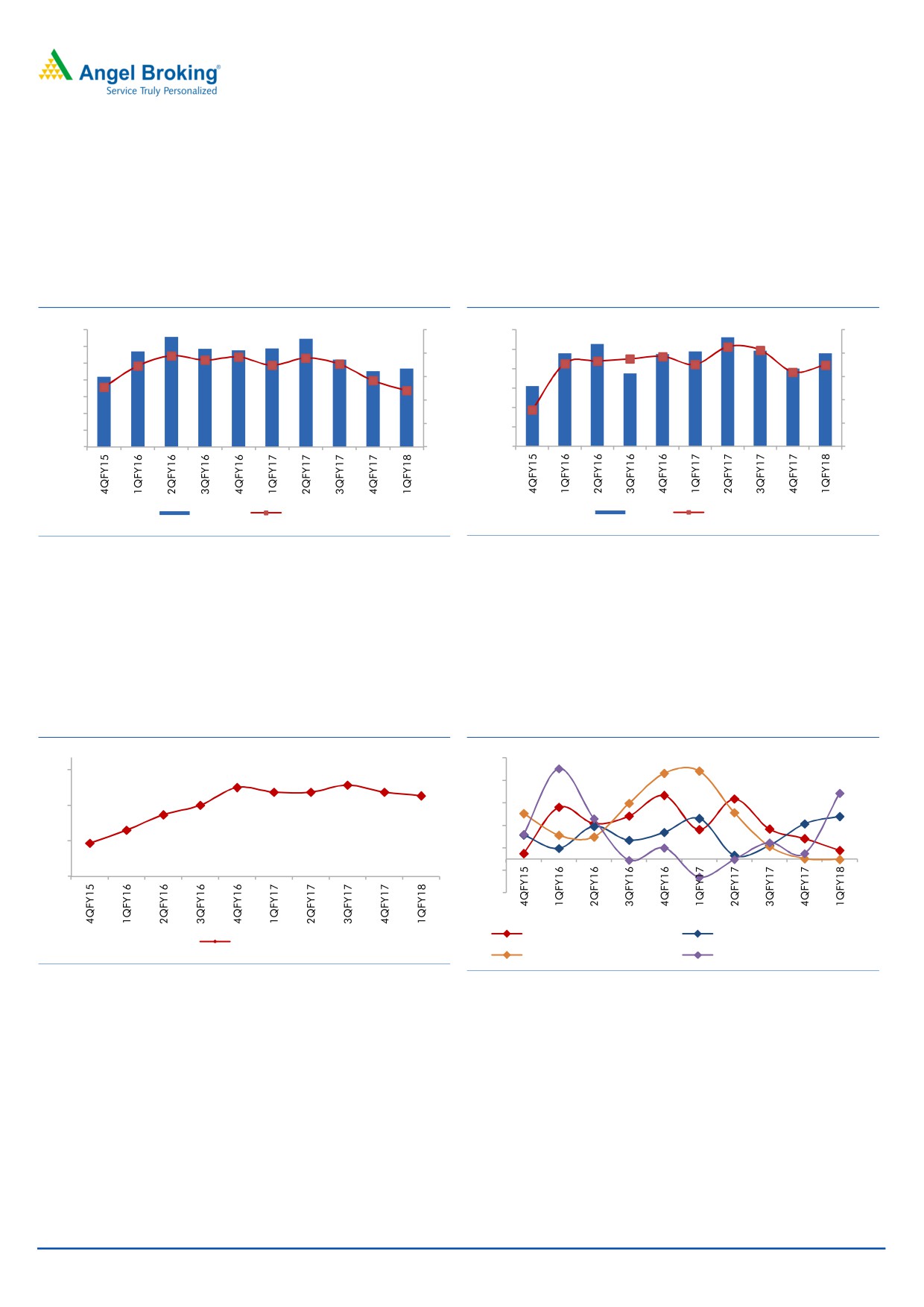

Due to the higher material costs and overheads, the company has seen

weakest EBITDA margins in the last 11 quarters. Company has now seen

consistent decline in the margins since 2QFY17 (21.4%) to 17.2% in the

1QFY18.

July 24, 2017

3

Bajaj Auto | 1QFY2018 Result Update

During the quarter company paid `32cr to the dealers as compensation to

clear the stocks on account of GST. The 1QFY18 PAT is at `924cr vs. `978cr

in 1QFY17. This was due to higher other income to the tune of `457cr, up

71% yoy.

Exhibit 7: Operating margin lowest in 11 quarters

Exhibit 8: Other income boosts adj. PAT

1,400

25

1,200

20

1,200

1,000

22

18

1,000

800

19

16

800

600

600

16

14

400

400

13

12

200

200

0

10

0

10

EBIDTA (` cr)

EBIDTA Margin %

PAT (` cr)

PAT Margin %

Source: Company, Angel Research

Source: Company, Angel Research

Company has indicated that here will be no new product launches in FY18E.

Company expects to see momentum in the 3W business on the back of the

new permits in Maharashtra and Delhi, the diesel vehicle ban in Bangalore

and mandatory transition from 2-stroke to 4-stroke vehicles in Karnataka.

Exhibit 9: Export Realisation trend

Exhibit 10: Exports recover, domestic volumes decline

60

69

67.5

67.7

67.1

67.1

67.1

66.8

40

66.0

65.2

66

20

63.9

62.8

0

63

(20)

(40)

60

(60)

2W Domestic growth (%)

2W Exports growth (%)

Export Realisation (INR/USD)

3W Domestic growth (%)

3W Exports growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

July 24, 2017

4

Bajaj Auto | 1QFY2018 Result Update

Conference call - Key highlights

During the quarter, company has seen expiry of the fiscal incentives at its

Pantnagar plant. This plant represents ~33% of its motorcycle capacity.

Company expects a run rate of ~25,000 units in V model and ~12,000-

15,000 units in the Avenger models.

As per company, industry is expected to see 7% growth in volumes this fiscal.

During the remainder of FY18E, Bajaj Auto expects growth of 10%, on

conservative basis. Company is expecting EBITDA margins of 19.5-20% for full

year FY18E.

Company has given a guidance of average 20,000-21,000 3W unit sales

each month from July to December. This is expected on account of

1)

Maharashtra opening auto rickshaw permits, execution of 10,000 permits in

Delhi, mandatory conversion of 2-stroke to 4-stroke vehicles in Karnataka and

ban on diesel vehicles in Bangalore.

In the exports, company expects 1.6mn vehicles and by H1FY18E it expects to

exports ~0.8mn vehicles, however company has acknowledged of the volatile

market conditions in its exports segment.

The sales were impacted during the quarter due the destocking by the dealers

and company expects sales to normalize going ahead. The dealer level

inventory was at ~1,50,000 units by the end of 1QFY18 and company keeps

inventory or ~4-4.5 weeks with the dealers. Company paid `32cr to its

dealers on the stock that dealers held until end of June to compensate the

losses arising due to the GST implementation.

Bajaj Auto, on 24th May, has taken the price hike (Rs 500-1,000 in 2W

segment and Rs 1,500-2,000 in CV segment) which covers about 90% of price

increase in the raw materials. The ambit of the price hike was only limited to

the GST and input prices hence the hike is not expected to boost the

profitability of the company. There were no discounts owing to the GST. In the

exports segment, company has taken a price hike effective form 1st July for

both 2W and 3W.

Company during the quarter maintained profitability 64% of business i.e.

exports, three wheelers, and KTM segments, however in the motorcycle

segment (36% of the business) profitability took a significant hit due to the

overheads. Company has indicated that overall profitability was maintained in

April 2017 and May 2017 however due to GST, June saw the most severe

impact.

Management has indicated that a deal with a motorcycle company is awaited

however decline to comment further on this. It also expects to launch a electric

3W within the next year and said that it will require minimum cost.

July 24, 2017

5

Bajaj Auto | 1QFY2018 Result Update

Investment arguments

Significant market share and diversified product offerings - Bajaj Auto is a

diversified automobile manufacturer with presence in 2W/3W categories. In

the 2W segment, company has presence in the entry level (price segment -

Platina and CT-100), premium (Pulsar and Avenger), Value (V series) and

Super sports (KTM, Ninja, RS200, Dominor-400) while in 3W it has presence

across both PV and CV categories. In the 2W category, company has a

market share of 18%, in the vehicles like Platina and CT100 (100cc category),

company has market share of ~32% by end of FY17. In the 3W - CV

category, company has a market share of 49.5% in FY17 and in the petrol /

alternate fuel category, it has market share of 88% and in the diesel category,

market share stands at 34%. Company exports both 2W and CV and which

constitute ~40% of its total volumes and 35% of its sales.

Healthy operating performance despite weak volumes- Bajaj Auto has

maintained a healthy operating performance despite weak volume growth. In

FY16 and FY17, when volume growth was weak the company recorded

EBITDA margins of more than 20% and ROE level more than 20%. The ROIC

levels also remain healthy.

Industry expected to grow in FY18E- The domestic 2W industry grew by 6.9%

in FY17 vs. 3% in FY16. The 3W industry growth declined to 4.9% in FY17 vs.

just 1% growth in FY16. This year, 2W industry is expected to continue to the

growth momentum on the back of the normal monsoon, lower interest rates

and strong consumption trend. The 3W industry is expected to see revival due

to the new licenses issuance in Maharashtra, and Delhi as well as mandatory

conversion of 2-stroke vehicles to 4-stroke vehicles in Karnataka and ban on

diesel vehicles in Bangalore. We believe that Automobile industry is currently

in good shape and is expected to see growth in FY18E.

July 24, 2017

6

Bajaj Auto | 1QFY2018 Result Update

Outlook and valuation

We expect Bajaj Auto to report 13.3%/12.5% CAGR in sales/PAT over the next two

years and maintain ROE levels over ~22%. We value Bajaj Auto at 17x of FY19E

EPS to `2,845/share and add KTM stake value of `139/share. We derive a target

price of `3,151 with an accumulate rating.

Exhibit 11: Key assumptions - Volumes

Y/E March (` cr)

FY15

FY16

FY17

FY18E

FY19E

Motorcycles (Domestic)

1,761,474

1,983,206

2,001,391

2,022,585

2,265,301

Motorcycles (Exports)

1,530,610

1,375,046

1,218,541

1,363,820

1,554,761

Total Motorcycles

3,292,084

3,358,252

3,219,932

3,386,405

3,820,062

Three wheeler (Domestic)

234,345

254,995

253,496

238,420

262,267

Three wheeler (Exports)

284,772

280,334

192,792

235,341

277,709

Total three-wheelers + Quadricycle

519,117

535,329

446,288

473,761

539,976

Total volumes

3,811,201

3,893,581

3,666,220

3,860,166

4,360,038

% chg

-1.5

2.2

-5.8

5.3

12.9

Source: Company, Angel Research

Company background

Bajaj Auto is the one of the largest 2W manufacturer in the country (~18% market

share) and a market leader in the 3W segment (~49.5% market share). Company

has three manufacturing facilities in India, located at Waluj, Chakan and

Pantnagar, with a total installed capacity (2W - 5.4mn and 3W - 0.6mn) of 6.0mn

units. The company is also one of India's largest auto exporters, with exports

forming 40% of volumes in FY2017. Company also has 48% stake in KTM AG,

maker of sports bikes.

July 24, 2017

7

Bajaj Auto | 1QFY2018 Result Update

Profit and loss statement (Standalone)

Y/E March (`cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

Total operating income

21,612

22,688

21,767

23,936

27,955

% chg

7.3

5.0

(4.1)

10.0

16.8

Total Expenditure

17,495

17,908

17,344

19,275

22,342

Cost of Materials

14,850

15,057

14,624

16,307

18,971

Personnel

897

918

997

1,131

1,261

Others Expenses

1,748

1,933

1,723

1,836

2,110

EBITDA

4,117

4,780

4,422

4,662

5,613

% chg

0.3

16.1

(7.5)

5.4

20.4

(% of Net Sales)

19.0

21.1

20.3

19.5

20.1

Depreciation& Amortisation

267

307

307

305

339

EBIT

3,849

4,472

4,115

4,357

5,274

% chg

(2.0)

16.2

(8.0)

5.9

(% of Net Sales)

17.8

19.7

18.9

18.2

18.9

Interest & other Charges

6

0

1

1

1

Other Income

582

913

1,222

1,545

1,644

(% of PBT)

13.2

17.0

22.9

26.2

23.8

Recurring PBT

4,425

5,385

5,336

5,901

6,918

% chg

(4.5)

21.7

(0.9)

10.6

17.2

Prior Period & Extra. Exp./(Inc.)

340

-

-

32

-

PBT (reported)

4,085

5,385

5,336

5,869

6,918

Tax

1,271

1,733

1,508

1,738

2,075

(% of PBT)

31.1

32.2

28.3

29.6

30.0

PAT (reported)

2,814

3,652

3,828

4,131

4,842

Add: Share of earnings of asso.

-

-

-

-

-

Less: Minority interest (MI)

-

-

-

-

-

PAT after MI (reported)

2,814

3,652

3,828

4,131

4,842

ADJ. PAT

3,154

3,652

3,828

4,163

4,842

% chg

(2.8)

15.8

4.8

8.8

16.3

(% of Net Sales)

14.6

16.1

17.6

17.4

17.3

Basic EPS (`)

97.2

126.2

132.3

142.7

167.3

Fully Diluted EPS (`)

97.2

126.2

132.3

142.7

167.3

% chg

(13.3)

29.8

4.8

7.9

16.3

July 24, 2017

8

Bajaj Auto | 1QFY2018 Result Update

Balance sheet statement (Standalone)

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

SOURCES OF FUNDS

Equity Share Capital

289

289

289

289

289

Reserves& Surplus

10,403

12,977

16,745

18,705

20,943

Shareholders’ Funds

10,692

13,267

17,034

18,994

21,232

Minority Interest

-

-

-

-

-

Total Loans

194

206

205

179

188

Deferred Tax Liability

142

203

314

314

314

Other Liabilities

58

30

49

70

82

Total Liabilities

11,086

13,706

17,602

19,557

21,817

APPLICATION OF FUNDS

Gross Block

4,101

4,301

4,570

4,922

5,471

Less: Acc. Depreciation

2,184

2,365

2,672

2,977

3,316

Net Block

1,917

1,936

1,899

1,945

2,154

Capital Work-in-Progress

102

27

11

11

11

Intangibles

153

115

76

76

76

Other non-current assets

511

743

757

786

908

Noncurrent Investments

3,353

8,941

8,681

9,384

10,963

Current Investments

5,801

1,320

6,050

6,050

6,050

Investments

Current Assets

3,726

3,405

3,341

4,376

4,866

Inventories

814

719

728

836

1,051

Sundry Debtors

717

718

953

964

1,126

Cash

586

860

294

699

770

Loans & Advances

1,262

60

270

938

1,096

Other Assets

347

1,049

1,096

938

822

Current liabilities

4,477

2,781

3,213

3,071

3,212

Net Current Assets

(751)

624

129

1,305

1,655

Deferred Tax Asset

-

-

-

-

-

Misc. Exp. not written off

-

-

-

-

-

Total Assets

11,086

13,706

17,602

19,557

21,817

July 24, 2017

9

Bajaj Auto | 1QFY2018 Result Update

Cash flow statement (Standalone)

Cash Flow Statement

Y/E March (`cr)

FY2015

FY2016

FY2017

FY2018E FY2019E

Profit before tax

4,085

5,547

5,336

5,869

6,918

Depreciation

267

307

307

305

339

Change in Working Capital

(583)

575

253

(800)

(401)

Interest / Dividend (Net)

6

90

1

0

0

Direct taxes paid

(1,285)

(1,782)

(1,503)

(1,738)

(2,075)

Others

(343)

(1,080)

(1,055)

0

1

Cash Flow from Operations

2,147

3,657

3,339

3,636

4,782

(Inc.)/ Dec. in Fixed Assets

(270)

(265)

(199)

(352)

(548)

(Inc.)/ Dec. in Investments

(145)

246

(3,489)

(703)

(1,579)

Cash Flow from Investing

(414)

(19)

(3,688)

(1,054)

(2,127)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

0

0

0

(6)

22

Dividend Paid (Incl. Tax)

(1,691)

(3,434)

(202)

(2,170)

(2,604)

Interest / Dividend (Net)

(6)

(0)

(1)

0

0

Others

64.26

69.86

-13.89

0

-1

Cash Flow from Financing

(1,633)

(3,364)

(217)

(2,176)

(2,584)

Inc./(Dec.) in Cash

100

274

(566)

405

71

Opening Cash balances

486

586

860

294

699

Closing Cash balances

586

860

294

699

770

July 24, 2017

10

Bajaj Auto | 1QFY2018 Result Update

Key ratios

Y/E March

FY2015

FY2016

FY2017

FY2018E FY2019E

Valuation Ratio (x)

P/E (on FDEPS)

29.0

22.3

21.3

19.7

16.8

P/CEPS

26.4

20.6

19.7

18.4

15.7

P/BV

7.6

6.1

4.8

4.3

3.8

Dividend yield (%)

1.8

2.0

2.0

2.7

3.2

EV/Sales

3.8

3.6

3.7

3.4

2.9

EV/EBITDA

19.7

16.9

18.4

17.4

14.4

EV / Total Assets

5.2

4.9

3.9

3.6

3.2

Per Share Data (`)

EPS (Basic)

97.2

126.2

132.3

142.7

167.3

EPS (fully diluted)

97.2

126.2

132.3

142.7

167.3

Cash EPS

106.5

136.8

142.9

153.3

179.1

DPS

50.0

55.0

55.0

75.0

90.0

Book Value

369.5

458.5

588.7

656.4

733.8

Returns (%)

ROCE

35.4

33.2

23.9

22.7

24.6

Angel ROIC (Pre-tax)

90.7

40.1

38.1

35.3

36.3

ROE

26.3

27.5

22.5

21.7

22.8

Turnover ratios (x)

Asset Turnover (Gross Block)

5.3

5.3

4.8

4.9

5.1

Inventory / Sales (days)

14

12

12

13

14

Receivables (days)

12

12

16

15

15

Payables (days)

30

33

38

35

30

Working capital cycle (ex-cash) (days)

(4)

(10)

(9)

(7)

(1)

July 24, 2017

11

Bajaj Auto | 1QFY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Bajaj Auto

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

July 24, 2017

12