4QFY2016 Result Update | Banking

May 4, 2016

Axis Bank

ACCUMULATE

CMP

`470

Performance Highlights

Target Price

`494

Particulars (` cr)

4QFY16 3QFY16

% chg (qoq) 4QFY15

% chg (yoy)

Investment Period

12 Months

NII

4,553

4,162

9.4

3,799

19.8

Pre-prov. profit

4,399

3,985

10.4

4,013

9.6

Stock Info

PAT

2,154

2,175

(1.0)

2,181

(1.2)

Sector

Banking

Source: Company, Angel Research

Market Cap (` cr)

111,986

Axis Bank has come out with a mixed set of numbers for 4QFY2016. The NII

Beta

1.4

grew 19.8% yoy to `4,553cr, in line with our expectations. However, higher than

52 Week High / Low

613/366

expected provision led to a 1.2% decline in PAT to `2,154cr.

Avg. Daily Volume

12,803,997

Face Value (`)

2

Advances growth remains healthy; During 4QFY2016, the bank reported an

advance growth of 21.0% yoy, while deposits grew by 11% yoy. The retail book

BSE Sensex

25,230

grew by 24% yoy and accounted for 41% of the advances as on March 31,

Nifty

7,747

Reuters Code

AXBK.BO

2016.For FY2017, the bank expects credit growth to be of around 18-20%.

Bloomberg Code

AXSB@IN

CASA ratio came in at 47.3%, increasing by 409bp qoq and 255bp on a yoy

basis. NIM jumped by 18bp qoq and stood at 3.97% while the cost of funds fell

by 2bp qoq to 5.84%. The bank expects its NIM to remain above 3.6% for

Shareholding Pattern (%)

FY2017. The bank created contingency provision to the extent of `300cr during

Promoters

29.7

the quarter, thereby taking the outstanding contingency provision to `480cr.

MF / Banks / Indian Fls

15.7

Corporate lending watch list a concern, asset quality likely to be under pressure;

44.6

FII / NRIs / OCBs

Asset quality for the quarter remained stable with GNPA & NNPA ratios to 1.67%

Indian Public / Others

10.0

and 0.7% vs 1.68% & 0.75% qoq. Slippages came in at `1,474cr, whereas the

bank transferred 1 account worth `170cr under 5/25 scheme and conducted

strategic debt restructuring in 4 accounts worth `205cr. The bank had already

Abs. (%)

3m

1yr

3yr

recognized AQR accounts in 3QFY16.In a significant development the bank has

Sensex

4.2

(6.6)

28.9

come out with a disclosure where in it has mentioned `22,600 cr worth of loans

Axis Bank

23.4

(17.3)

59.3

from the corporate loan book are under stress and ~60% of the same can fall

into NPAs over the next eight quarters. This will keep the provisions on a higher

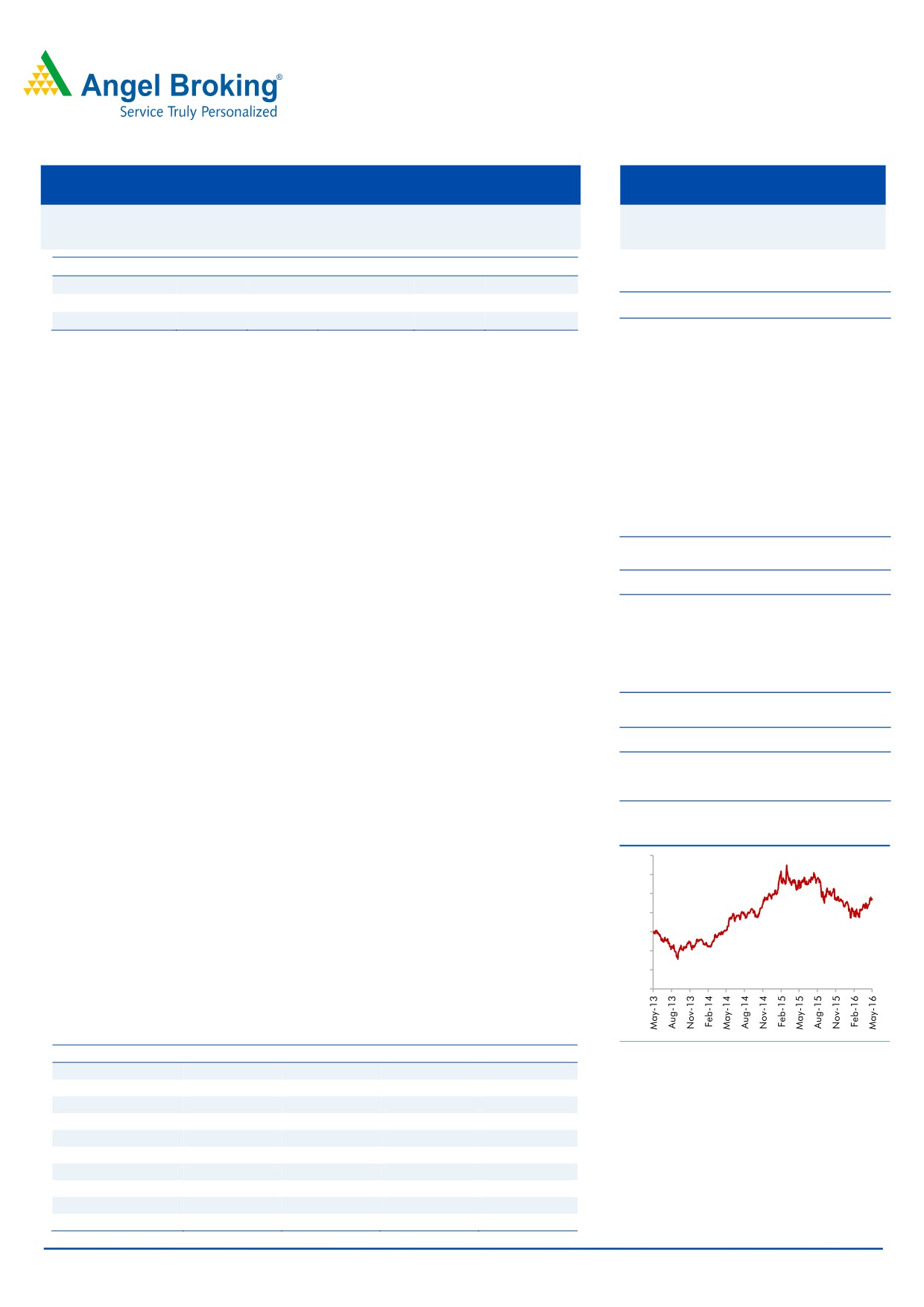

3-year price chart

side over the next 2 years.

700

600

Outlook and valuation: Though the incremental slippages can remain high over

500

the next two years, the disclosure by the bank gives better clarity on earnings

400

going ahead. On a positive side, the core business of the bank continues to grow

300

strong. With higher credit cost we don’t expect FY17 to be a good year with

200

sluggish earnings growth, but remain upbeat on FY18. The stock currently trades

100

at 1.7x P/ABV FY2017E. We maintain our Accumulate rating on the stock with a

0

price target of `494.

Key financials (Standalone)

Source: Company, Angel Research

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

NII

14,224

16,833

18,872

21,601

% chg

19.0

18.3

12.1

14.5

Net profit

7,358

8,224

8,441

10,380

% chg

18.3

11.8

2.6

23.0

Siddharth Purohit

NIM (%)

3.5

3.6

3.5

3.3

022 - 3935 7800 Ext: 6872

EPS (`)

31.0

34.5

35.4

43.4

P/E (x)

13.2

13.6

13.3

10.8

P/ABV (x)

2.2

2.1

1.7

1.6

Chintan Shah

RoA (%)

1.7

1.7

1.5

1.5

022 - 4000 3600 Ext: 6828

RoE (%)

17.9

16.8

14.9

16.0

Source: Company, Angel Research; Note: CMP as of May 3, 2016

Please refer to important disclosures at the end of this report

1

Axis Bank | 4QFY2016 Result Update

Exhibit 1: 4QFY2016 performance summary (Standalone)

Particulars (` cr)

4QFY16

3QFY16

% chg (qoq)

4QFY15

% chg (yoy)

FY2016

FY2015

% chg

Interest earned

10,899

10,193

6.9

9,697

12.4

40,988

35,479

15.5

- on Advances / Bills

8,093

7,529

7.5

7,025

15.2

30,041

25,868

16.1

- on investments

2,421

2,293

5.6

2,530

(4.3)

9,378

9,117

2.9

- on balance with RBI & others

64

69

(7.2)

67

(4.8)

312

231

35.0

- on others

321

302

6.1

75

326.9

1,258

262

379.2

Interest Expended

6,346

6,031

5.2

5,898

7.6

24,155

21,254

13.6

Net Interest Income

4,553

4,162

9.4

3,799

19.8

16,833

14,224

18.3

Other income

2,694

2,338

15.2

2,687

0.2

10,866

12,732

(14.7)

Other income excl. treasury

2,694

2,000

34.7

2,412

11.7

9,619

11,597

(17.1)

- Fee Income

2,254

1,885

19.6

2,124

6.1

7,502

6,779

10.7

- Trading gains

95

338

(71.9)

275

(65.5)

1,247

1,135

9.9

- Others

440

115

282.7

288

52.6

623

451

38.0

Operating income

7,247

6,500

11.5

6,487

11.7

26,204

22,589

16.0

Operating expenses

2,848

2,515

13.3

2,474

15.1

10,101

9,204

9.7

- Employee expenses

908

830

9.4

799

13.7

3,376

3,115

8.4

- Other Opex

1,940

1,685

15.1

1,675

15.8

6,725

6,089

10.4

Pre-provision Profit

4,399

3,985

10.4

4,013

9.6

16,104

13,385

20.3

Provisions & Contingencies

1,168

713

64.0

710

64.6

3,710

2,329

59.3

PBT

3,230

3,272

(1.3)

3,303

(2.2)

12,394

11,057

12.1

Provision for Tax

1,076

1,097

(1.9)

1,122

(4.1)

4,170

3,699

12.7

PAT

2,154

2,175

(1.0)

2,181

(1.2)

8,224

7,358

11.8

Source: Company, Angel Research

May 4, 2016

2

Axis Bank | 4QFY2016 Result Update

Exhibit 2: 4QFY2016 performance analysis (Standalone)

Particulars

4QFY16

3QFY16

% chg (qoq) 4QFY15

% chg (yoy)

Balance sheet

Advances (` cr)

3,38,774 3,15,367

7.4

2,81,083

20.5

Deposits (` cr)

3,57,968 3,38,343

5.8

3,22,442

11.0

Credit-to-Deposit Ratio (%)

94.6

93.2

143bp

87.2

746bp

Current deposits (` cr)

63,652

53,564

18.8

56,108

13.4

Saving deposits (` cr)

1,05,793

92,758

14.1

88,292

19.8

CASA deposits (` cr)

1,69,445 1,46,322

15.8

1,44,400

17.3

CASA ratio (%)

47.3

43.2

409bp

44.8

255bp

CAR (%)*

15.3

15.5

(18)bp

15.1

20bp

Tier 1 CAR (%)*

12.5

12.4

16bp

12.1

44bp

Profitability Ratios (%)

Cost of funds

5.8

5.9

(2)bp

6.3

(42)bp

Reported NIM

4.0

3.8

18bp

3.8

16bp

Cost-to-income ratio

39.3

38.7

61bp

38.1

117bp

Asset quality

Gross NPAs (` cr)

6,088

5,724

6.3

4,110

48.1

Gross NPAs (%)

1.7

1.7

(1)bp

1.3

33bp

Net NPAs (` cr)

2,522

2,514

0.3

1,317

91.5

Net NPAs (%)

0.7

0.8

(5)bp

0.4

26bp

Provision Coverage Ratio (%)

72.0

72.0

0bp

78.0

(600)bp

Slippage ratio (%)

2.1

3.0

(87)bp

1.1

103bp

Loan loss prov. to avg. assets (%)

0.5

0.5

(4)bp

0.4

14bp

Source: Company, Angel Research *Basel III excluding profits

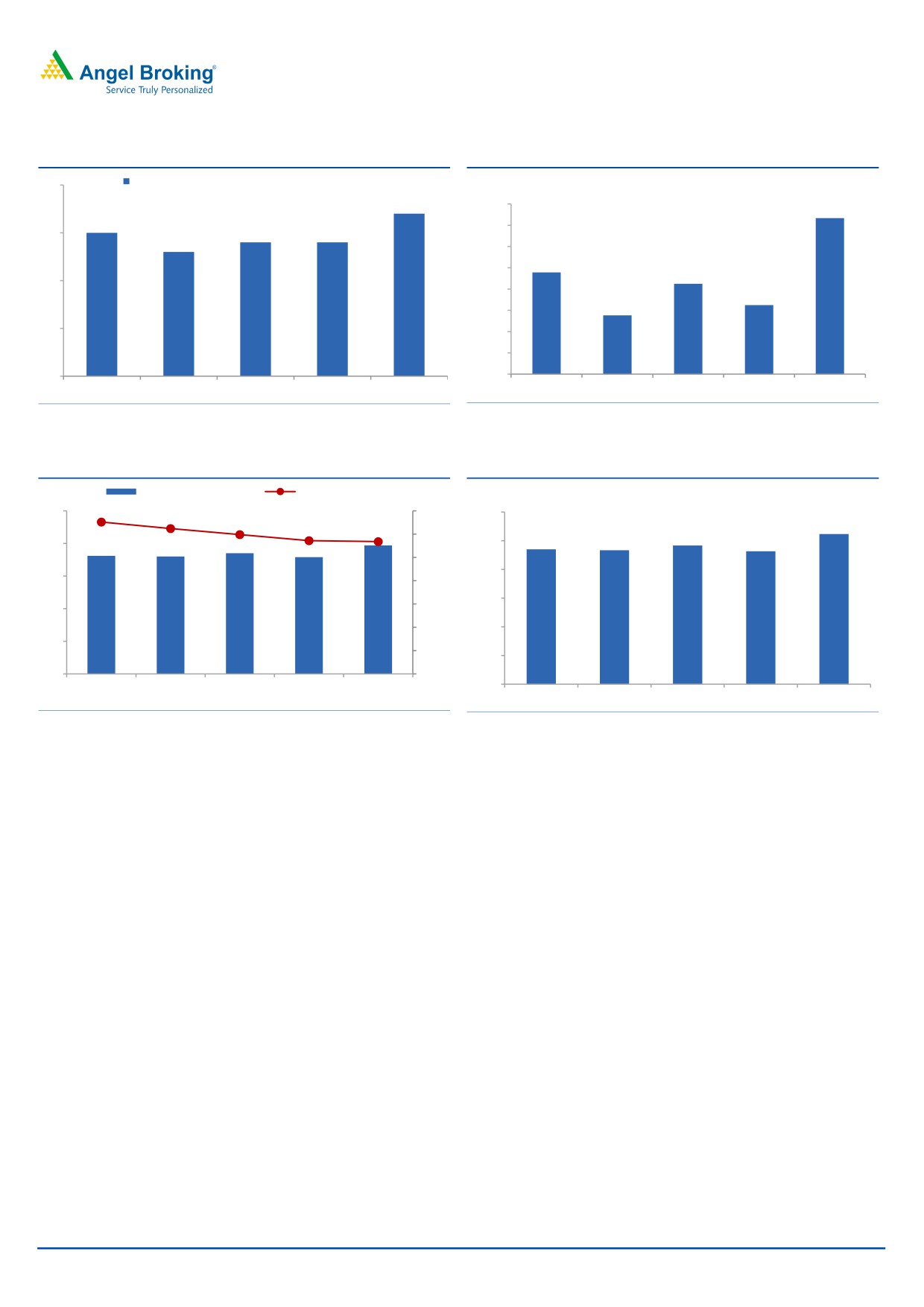

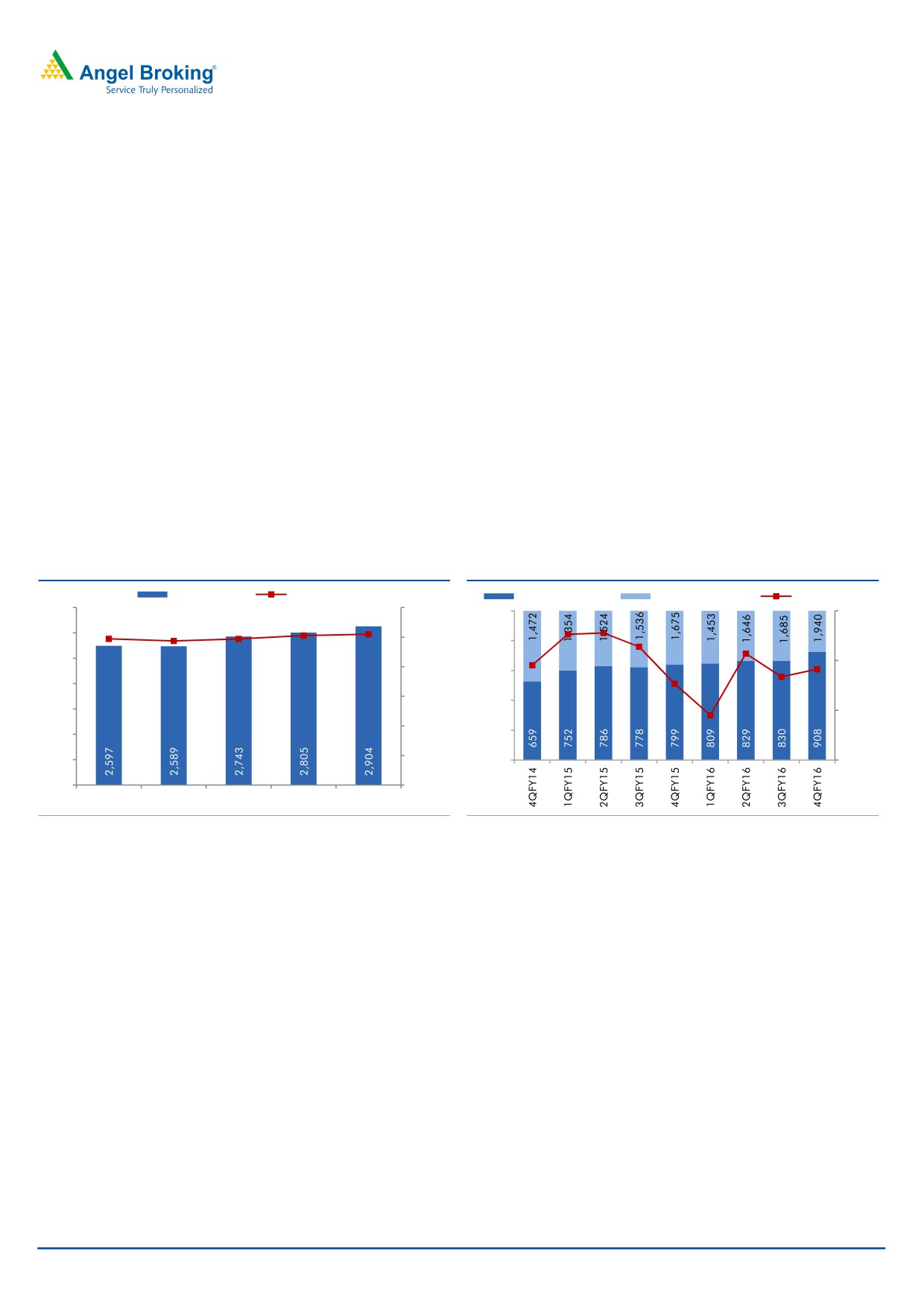

Advances growth remains healthy; NIM declines qoq

During 4QFY2016, the bank reported an advance growth of 21.0% yoy, while

deposits grew by 11% yoy. The retail book grew by 24% yoy and accounted for

41% of the advances as on March 31, 2016. Overall, for the current financial year

(FY2017), the bank expects credit growth to be of around 18-20%.

The CASA ratio came in at 47.3%, increasing by 409bp qoq and 255bp on a yoy

basis. The NIM jumped by 18bp qoq and stood at 3.97% while the cost of funds

fell by 2bp qoq to 5.84%. The bank created contingency provision to the extent of

`300cr during the quarter, thereby taking the outstanding contingency provision to

`480cr.

May 4, 2016

3

Axis Bank | 4QFY2016 Result Update

Exhibit 3: CASA balances grew at 17% yoy

Exhibit 4: Period-end CASA ratio at 47.3%

Reported yoy growth in average CASA balances (%)

20

(%)

17

48.0

47.3

15

14

14

47.0

15

13

46.0

44.8

45.0

44.2

10

44.0

43.2

42.8

43.0

5

42.0

41.0

0

40.0

4QFY15

1QFY16

2QFY16

3QFY16

4QFY16

4QFY15

1QFY16

2QFY16

3QFY16

4QFY16

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 5: Cost of funds declines qoq

Exhibit 6: NIM at 3.97%

Reported NIMs (%)

Cost of funds (%)

(%)

6.26

4.5

6.12

6.50

4.2

5.99

3.97

5.86

5.84

6.00

3.85

3.9

3.81

3.80

3.79

4.0

5.50

3.6

3.5

5.00

3.3

4.50

3.0

4.00

3.0

2.5

3.50

2.7

3.81

3.80

3.85

3.79

3.97

2.0

3.00

2.4

4QFY15

1QFY16

2QFY16

3QFY16

4QFY16

4QFY15

1QFY16

2QFY16

3QFY16

4QFY16

Source: Company, Angel Research

Source: Company, Angel Research

Slow growth in other income

Fees growth was muted at 6% yoy which constituted 31% of operating revenue.

This was due to decline in corporate fees and flattish transaction banking fees,

which restricted the overall fee growth. However, retail fees grew 15% yoy and

treasury fees grew 12% yoy.

During the quarter, miscellaneous income was up 20% yoy, mainly due to receipt

of dividend from subsidiaries and on account of the bank booking `169cr of

exchange gains from repatriation of profits from its foreign branches compared to

`156cr in 4QFY2015. The sharp sequential jump in miscellaneous income was

also due to higher cash recoveries of `83cr.

Corporate watch list a cause of concern

The asset quality improved marginally with a dip in Gross and Net NPA ratios to

1.67% and 0.7% from 1.68% and 0.75% in the sequential previous quarter.

Slippages came in at `1,474cr, whereas the bank transferred 1 account worth

`170cr under 5/25 scheme and conducted strategic debt restructuring in

4

accounts worth `205cr. The bank has stated that it has taken into account the full

impact of asset quality review conducted by the RBI, which accounted for ~50% of

the total slippages during 3QFY2016.

May 4, 2016

4

Axis Bank | 4QFY2016 Result Update

The bank has come out with strong disclosure this time in which, the management

has outlined that ~`22,600 worth of loans are under stress of which ~60% can

fall into NPA over the next eight quarters. Further large part of the incremental

NPA from this accounts are likely to come up in FY17 itself and hence we believe

slippages to remain high in the 1Q and 2Q of FY17.

24% of the said loans are from metal sector while ~23% are from power and in

the absence of major revival in the above two sector we believe it is fair to assume

that large part of this combined 47% of the loans to turn NPAs over the next few

quarters.

Assuming 60% of the said accounts turns NPAs, it can fairly be said ~`13,500cr of

incremental slippages over the next eight quarters and since the management has

indicated it intends to keep its provisioning coverage ratio at 70%, we can look

towards ~`9,500cr of provisions from this itself over the same period.

Though the slippages numbers indicated by the managements looks like, what we

like is the disclosure and the management’s confidence that no much of other

slippages to come other than from the said accounts.

Exhibit 7: Steady network expansion continues

Exhibit 8: Cost-to-income ratio at 39.3%

Branches

ATMs (RHS)

Staff costs (` cr)

Other opex (` cr)

CIR (%, RHS)

3200

15000

1,250

44.0

12,631

12,743

12,355

12,179

12,352

2800

12500

1,000

42.1

42.2

2400

41.1

40.0

10000

750

40.6

39.6

2000

39.3

7500

38.1

38.7

500

35.6

1600

36.0

5000

250

1200

2500

800

-

32.0

400

0

4QFY15

1QFY16

2QFY16

3QFY16

4QFY16

Source: Company, Angel Research;

Source: Company, Angel Research

May 4, 2016

5

Axis Bank | 4QFY2016 Result Update

Outlook and valuation: Though the incremental slippages expected remains high

over the next two years, the disclosure by the bank gives better clarity on earnings

going ahead. On a positive side the core business of the bank continues to grow

strong. With higher credit cost we don’t expect FY17 to be a good year with

sluggish earnings growth, but remain upbeat on FY18. The stock currently trades

at 1.7x P/ABV FY2017E. We maintain our Accumulate rating on the stock with a price

target of `494.

Exhibit 9: Recommendation summary

CMP

Tgt. Price

Upside

FY2017E

FY2017E

FY2017E

FY15-17E

FY2017E

FY2017E

Company

Reco.

(`)

(`)

(%)

P/ABV (x)

Tgt. P/ABV (x)

P/E (x)

EPS CAGR (%)

RoA (%)

RoE (%)

HDFCBk

Accumulate

1,117

1,262

12.9

3.4

3.8

18.2

22.7

2.0

20.0

ICICIBk*

Accumulate

221

254

14.7

1.5

1.4

9.1

13.5

1.6

14.7

YesBk

Neutral

932

-

-

2.4

2.0

13.4

20.5

1.6

19.6

AxisBk

Accumulate

470

494

5.1

1.9

2.0

10.8

18.4

1.7

18.9

SBI*

Neutral

184

-

-

1.0

0.7

8.9

8.3

0.6

11.2

FedBk

Neutral

47

-

-

0.9

0.9

8.5

(2.9)

0.9

10.8

SIB

Neutral

18

-

-

0.6

0.6

5.4

21.6

0.7

11.6

BOB

Neutral

153

-

-

1.0

1.0

11.8

(7.9)

0.4

7.3

PNB

Neutral

83

-

-

0.5

0.5

3.8

14.4

0.6

10.0

BOI

Neutral

88

-

-

0.2

0.9

2.6

14.0

0.3

7.6

IndBk

Neutral

96

-

-

0.3

0.2

3.2

19.4

0.6

8.6

Vijaya Bank

Neutral

31

-

-

0.4

0.4

4.7

14.1

0.4

8.8

OBC

Neutral

87

-

-

0.2

0.3

1.9

65.5

0.5

9.4

Allahabad Bank Neutral

56

-

-

0.3

0.2

2.1

56.2

0.6

11.9

UnionBk

Neutral

124

-

-

0.4

0.3

3.2

18.1

0.6

11.4

CanBk

Neutral

196

-

-

0.3

0.3

2.8

12.0

0.6

11.2

IDBI#

Neutral

68

-

-

0.4

0.5

4.8

61.6

0.6

9.3

DenaBk

Neutral

29

-

-

0.2

0.3

2.9

45.6

0.4

7.9

Source: Company, Angel Research; Note:*Target multiples=SOTP Target Price/ABV (including subsidiaries), #Without adjusting for SASF

Company Background

Axis Bank is India's third-largest private sector bank after ICICI Bank and HDFC

Bank. The bank is promoted by government institutions, led by UTI (SUUTI

currently holds 12% stake in the bank). The bank has an extensive network of

2,743 branches and 12,352 ATMs spread across 1,796 centers (~51% in metro

and urban regions). The bank's strong growth has been backed by robust retail

branch expansion, strong corporate relationships and a wide range of fee income

products.

May 4, 2016

6

Axis Bank | 4QFY2016 Result Update

Income statement (Standalone)

Y/E March (` cr)

FY12

FY13

FY14

FY15

FY16

FY17E

FY18E

Net Interest Income

8,018

9,666

11,952

14,224

16,833

18,872

21,601

- YoY Growth (%)

22.2

20.6

23.6

19.0

18.3

12.1

14.5

Other Income

5,420

6,551

7,405

8,365

9,371

10,866

12,732

- YoY Growth (%)

17.0

20.9

13.0

13.0

12.0

15.9

17.2

Operating Income

13,438

16,217

19,357

22,589

26,204

29,738

34,332

- YoY Growth (%)

20.0

20.7

19.4

16.7

16.0

13.5

15.5

Operating Expenses

6,007

6,914

7,901

9,204

10,101

11,834

13,869

- YoY Growth (%)

25.7

15.1

14.3

16.5

9.7

17.2

17.2

Pre - Provision Profit

7,431

9,303

11,456

13,385

16,104

17,904

20,464

- YoY Growth (%)

15.8

25.2

23.1

16.8

20.3

11.2

14.3

Prov. & Cont.

1,143

1,750

2,107

2,329

3,710

5,306

4,971

- YoY Growth (%)

(10.7)

53.1

20.4

10.5

59.3

43.0

(6.3)

Profit Before Tax

6,288

7,553

9,349

11,057

12,394

12,598

15,493

- YoY Growth (%)

22.4

20.1

23.8

18.3

12.1

1.6

23.0

Prov. for Taxation

2,046

2,373

3,131

3,699

4,170

4,157

5,113

- as a % of PBT

32.5

31.4

33.5

33.5

33.6%

33.0%

33.0%

PAT

4,242

5,179

6,218

7,358

8,224

8,441

10,380

- YoY Growth (%)

25.2

22.1

20.0

18.3

11.8

2.6

23.0

Balance sheet (Standalone)

Y/E March (` cr)

FY12

FY13

FY14

FY15

FY16

FY17E

FY18E

Share Capital

413

468

470

474

477

477

478

Reserve & Surplus

22,395

32,640

37,751

43,463

52,688

59,863

68,686

Deposits

2,20,104

2,52,614

2,80,945

3,22,442

3,57,968

4,29,561

5,15,473

- Growth (%)

16.3

14.8

11.2

14.8

11.0

20.0

20.0

Borrowings

34,072

43,951

50,291

79,758

99,226

1,18,129

1,41,755

Other Liab. & Prov.

8,643

10,888

13,789

15,795

15,109

18,042

23,196

Total Liabilities

2,85,628

3,40,561

3,83,245

4,61,932

5,25,468

6,26,071

7,49,589

Cash Balances

10,703

14,792

17,041

19,819

22,361

21,478

25,774

Bank Balances

3,231

5,643

11,197

16,280

10,964

17,182

20,619

Investments

93,192

1,13,738

1,13,548

1,32,343

1,22,006

1,46,051

1,75,261

Advances

1,69,760

1,96,966

2,30,067

2,81,083

3,38,774

4,06,528

4,87,834

- Growth (%)

19.2

16.0

16.8

22.2

20.5

20.0

20.0

Fixed Assets

2,259

2,356

2,410

2,514

3,523

4,323

5,123

Other Assets

6,483

7,067

8,981

9,893

27,839

30,509

34,978

Total Assets

2,85,628

3,40,561

3,83,245

4,61,932

5,25,468

6,26,071

7,49,589

- Growth (%)

17.7

19.2

12.5

20.5

13.8

19.1

19.7

May 4, 2016

7

Axis Bank | 4QFY2016 Result Update

Ratio analysis (Standalone)

Y/E March

FY12

FY13

FY14

FY15

FY16

FY17E

FY18E

Profitability ratios (%)

NIMs

3.1

3.2

3.4

3.5

3.6

3.5

3.3

Cost to Income Ratio

44.7

42.6

40.8

40.7

38.5

39.8

40.4

RoA

1.6

1.7

1.7

1.7

1.7

1.5

1.5

RoE

20.3

18.5

17.4

17.9

16.8

14.9

16.0

B/S ratios (%)

CASA Ratio

41.5

44.4

45.0

44.8

47.3

48.0

48.0

Credit/Deposit Ratio

77.1

78.0

81.9

87.2

94.6

94.6

94.6

CAR

13.7

17.0

16.3

16.0

15.4

14.9

14.0

- Tier I

9.4

12.2

12.8

12.2

12.6

12.4

11.8

Asset Quality (%)

Gross NPAs

1.1

1.2

1.4

1.4

1.7

2.8

2.9

Net NPAs

0.3

0.4

0.4

0.5

0.7

1.1

1.0

Slippages

1.3

1.2

1.3

1.2

2.5

1.6

0.8

Loan Loss Prov. /Avg. Assets

0.3

0.4

0.4

0.5

1.1

1.3

1.0

Provision Coverage

73.8

70.6

77.2

68.0

58.6

62.0

65.0

Per Share Data (`)

EPS

20.5

22.1

26.5

31.0

34.5

35.4

43.4

ABVPS (75% cover.)

110.3

141.0

161.7

184.1

218.9

246.9

283.4

DPS

3.2

3.6

4.0

5.9

5.0

6.0

6.5

Valuation Ratios

PER (x)

19.9

18.5

15.4

13.2

13.6

13.3

10.8

P/ABVPS (x)

3.7

2.9

2.5

2.2

2.1

1.7

1.6

Dividend Yield

0.8

0.9

1.0

1.4

1.1

1.3

1.4

DuPont Analysis

NII

3.0

3.1

3.3

3.4

3.4

3.3

3.1

(-) Prov. Exp.

0.4

0.6

0.6

0.6

0.8

0.9

0.7

Adj. NII

2.6

2.5

2.7

2.8

2.7

2.4

2.4

Other Inc.

2.0

1.9

2.0

1.7

1.9

1.9

1.9

Op. Inc.

4.7

4.6

4.8

4.8

4.6

4.2

4.3

Opex

2.3

2.2

2.2

2.2

2.0

2.1

2.0

PBT

2.4

2.4

2.6

2.6

2.5

2.2

2.3

Taxes

0.8

0.8

0.9

0.9

0.8

0.7

0.7

RoA

1.6

1.7

1.7

1.7

1.7

1.5

1.5

Leverage

12.6

11.2

10.1

10.3

10.1

10.1

10.6

RoE

20.3

18.5

17.4

17.9

16.8

14.9

16.0

May 4, 2016

8

Axis Bank | 4QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Axis Bank

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

May 4, 2016

9