3QFY2017 Result Update | Pharmaceutical

February 23, 2017

Aurobindo Pharma

BUY

CMP

`686

Performance Highlights

Target Price

`877

Y/E march (` cr)

3QFY17 2QFY17

% chg (QoQ) 3QFY16

% chg (yoy)

Investment Period

12 months

Net sales

3,844

3,714

3.5

3,432

12.0

Other income

70

70

(0.7)

70

(0.9)

Stock Info

Operating profit

833

867

(3.9)

760

9.7

Sector

Pharmaceutical

Interest

(2)

(3)

(41.9)

23

(106.8)

Adj. Net profit

579

606

(4.6)

544

6.3

Market Cap (` cr)

40,137

Net debt (` cr)

3,265

Source: Company, Angel Research

Beta

1.1

For 3QFY2017, Aurobindo Pharma (APL) posted numbers which were almost in-

52 Week High / Low

895/582

line with expectations on sales and net profit front, with sales marginally higher

Avg. Daily Volume

177,746

than expected and net profit marginally lower than expected. On sales front, the

Face Value (`)

1

company posted sales of `3844cr (v/s. `3,715cr expected) v/s. `3,432cr in

BSE Sensex

28,762

3QFY2016, posting a yoy growth of 12.0%. On the operating front, the EBITDA

Nifty

8,927

margin came in at 21.7% (vs. 23.1% expected) v/s. 22.1% in 3QFY2016.

Reuters Code

ARBN.BO

Consequently, the Adj. PAT came in at `579cr (v/s. `603cr expected) v/s. `544cr

Bloomberg Code

ARBP@IN

in 3QFY2016, a yoy growth of 6.3%. We maintain our Buy rating on the stock.

Results mostly in-line with expectation: Aurobindo Pharma’s (APL) posted

Shareholding Pattern (%)

numbers which were almost in-line with expectations on sales and net profit

fronts, with sales marginally higher than expected and net profit marginally lower

Promoters

51.9

than expected. On sales front, the company posted sales of `3844cr (v/s.

MF / Banks / Indian Fls

13.8

`3,715cr expected) v/s. `3,432cr in 3QFY2016, posting a yoy growth of 12.0%.

FII / NRIs / OCBs

24.5

The formulation sales (`3,130cr) posted a yoy growth of 11.4%, while API

Indian Public / Others

9.8

(`775.9cr) posted a yoy growth of 11.6%. On the operating front, the EBITDA

margin came in at 21.7% (v/s. 23.1% expected) v/s. 22.1% in 3QFY2016.

Abs. (%)

3m 1yr

3yr

Consequently, the Adj. PAT came in at `579cr (v/s. `603cr expected) v/s. `544cr

Sensex

11.6

21.3

38.9

in 3QFY2016, a yoy growth of 6.3%.

Aurobindo

(3.6)

4.6

180.4

Outlook and valuation: We estimate the company’s net sales to log a CAGR of

15.1% over FY2016-18E to `18,078cr on the back of US formulations, which

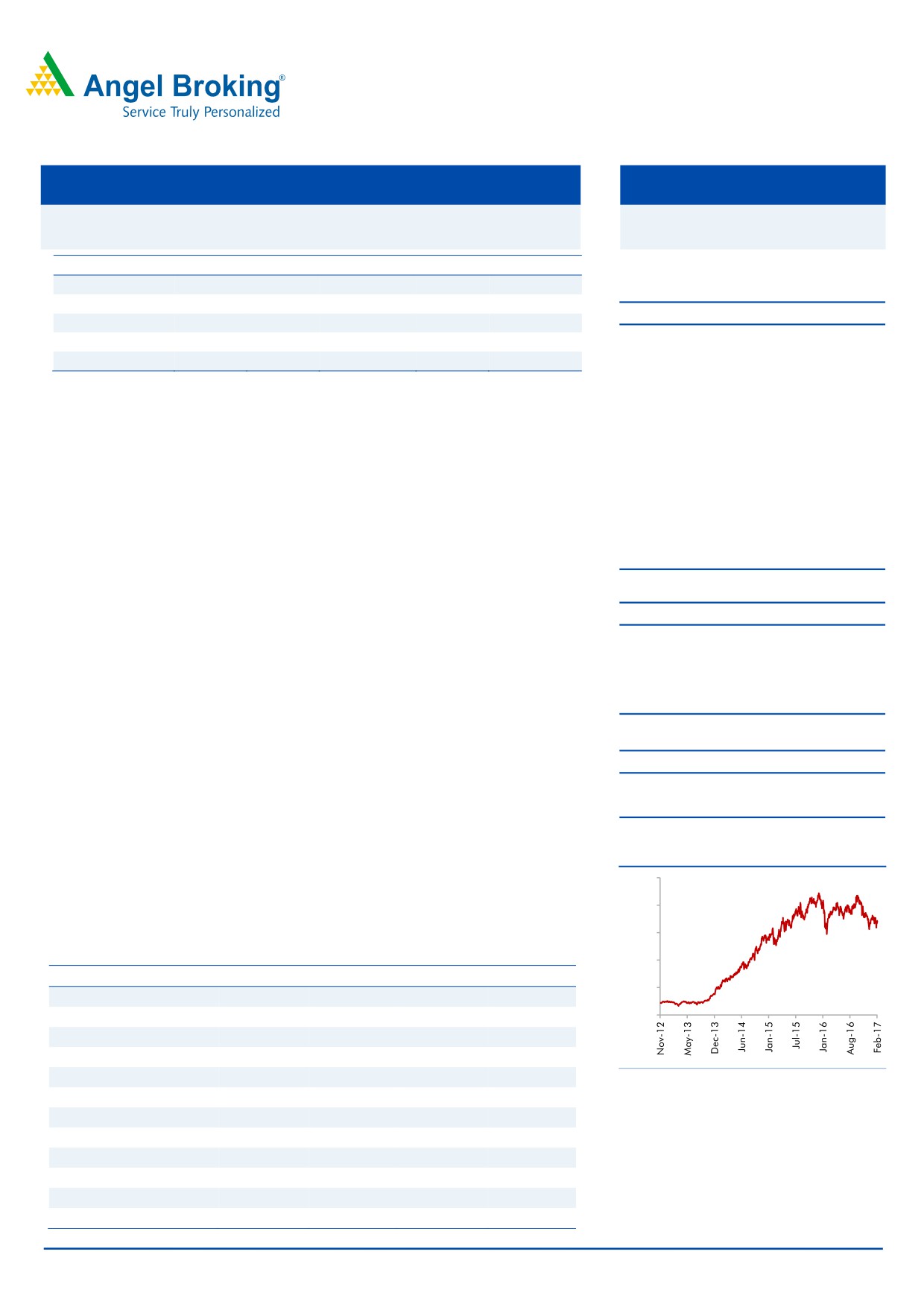

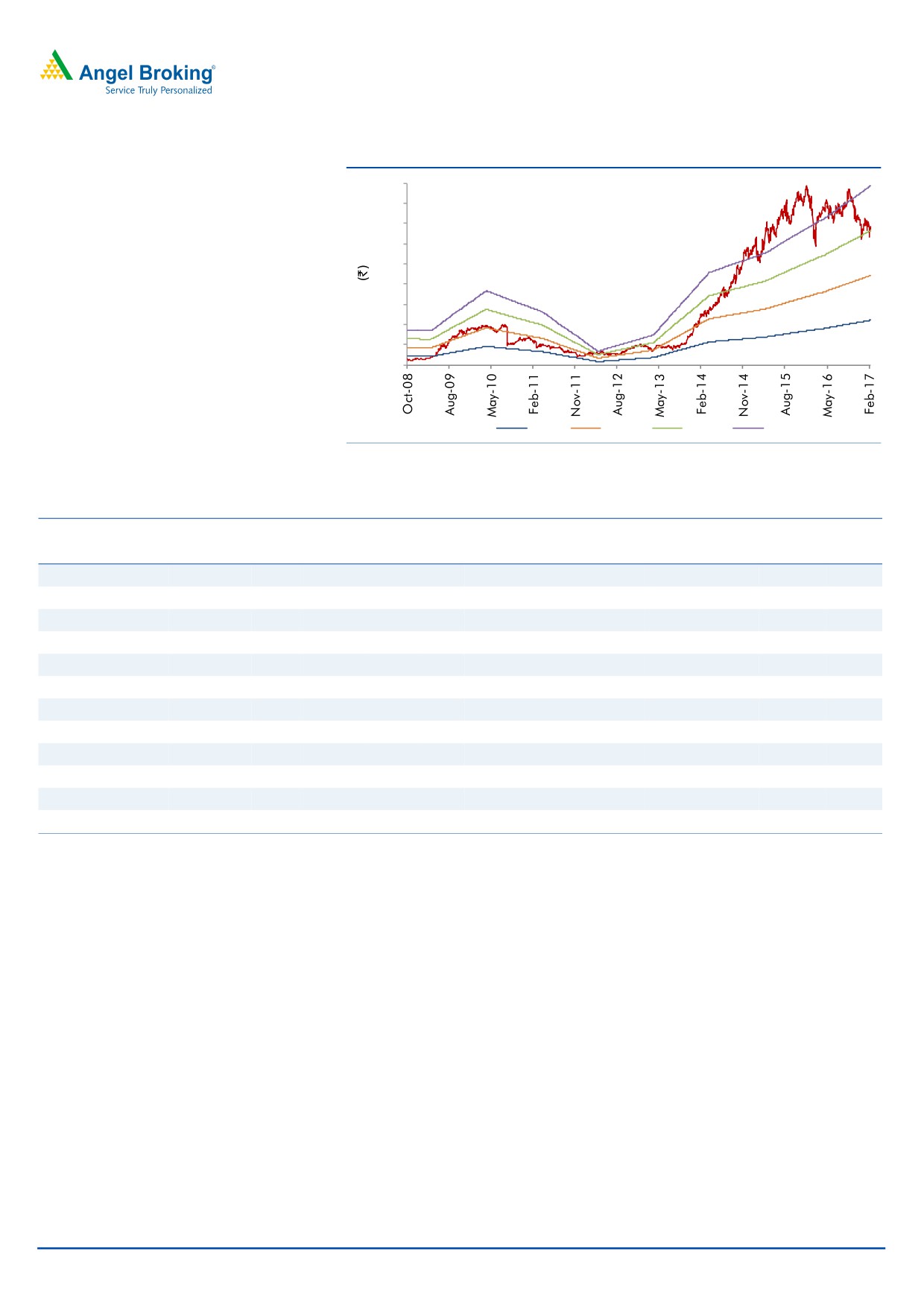

3-year daily price chart

will be supplemented through the recent acquisitions of the Western European

1,000

formulation businesses of Actavis and US’ Natrol. The acquisitions have also led

APL to become a >US$2bn sales company, with ~80% of sales being accounted

800

by formulations. We recommend a Buy rating with a target price of `877.

600

Key financials (Consolidated)

400

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

200

Net sales

12,043

13,651

15,720

18,078

0

% chg

49.8

13.3

15.2

15.0

Adj. Net profit

1,619

1,982

2,418

2,763

% chg

21.5

22.4

22.0

14.2

EPS (`)

27.7

33.9

41.4

47.3

Source: Company, Angel Research

EBITDA margin (%)

20.6

21.7

23.7

23.7

P/E (x)

24.7

20.2

16.6

14.5

RoE (%)

36.4

32.5

29.6

26.1

RoCE (%)

25.3

24.8

24.0

22.5

P/BV (x)

3.9

5.7

4.3

3.4

Sarabjit Kour Nangra

EV/Sales (x)

1.9

3.2

2.8

2.4

+91 22 3935 7800 Ext: 6806

EV/EBITDA (x)

9.4

14.6

11.7

10.1

Source: Company, Angel Research; Note: CMP as of February 21, 2017

Please refer to important disclosures at the end of this report

1

Aurobindo Pharma | 3QFY2017 Result Update

Exhibit 1: 3QFY2017 performance (Consolidated)

Y/E March (` cr)

3QFY2017

2QFY2017

% chg (QoQ) 3QFY2016

% chg (YoY) 9MFY2017 9MFY2016

% chg (YoY)

Net sales

3,844

3,714

3.5

3,432

12.0

11,263

10,036

12.2

Other income

70

70

(0.7)

70

(0.9)

218

223

(2.2)

Total income

3,914

3,784

3.4

3,502

11.8

11,480

10,258

11.9

Gross profit

2,135

2,085

2.4

1,879

13.6

6,245

5,500

13.6

Gross margins

55.5

56.2

54.7

55.5

54.8

Operating profit

833

867

(3.9)

760

9.7

2,527

2,148

17.6

OPM (%)

21.7

23.4

(7.2)

22.1

22.4

21.4

Interest

(2)

(3)

(41.9)

23

(106.8)

9

108

(91.3)

Dep & amortisation

111

110

0.9

99

11.7

328

281

16.6

PBT

793

830

(4.4)

708

12.0

2,408

1,982

21.5

Provision for taxation

218

224

(2.8)

186

17.0

643

514

24.9

Net profit

575

606

(5.0)

522

10.3

1,766

1,467

20.3

Less : Exceptional items (gains)/loss

-

-

-

0

-

-

MI & share in associates

3

0

13

3

3

-

PAT after Exceptional items

579

606

(4.6)

544

6.3

1,769

1,470

20.3

Adjusted PAT

579

606

(4.6)

544

6.3

1,769

1,470

20.3

EPS (`)

9.9

10.4

9.3

30.3

25.2

Source: Company, Angel Research

Exhibit 2: Actual v/s Estimate

(` cr)

Actual

Estimate

Variation %

Net sales

3,844

3,715

3.5

Other operating income

70

60

16.8

Operating profit

833

857

(2.8)

Tax

218

193

13.0

Adj. Net profit

579

603

(4.0)

Source: Company, Angel Research

Revenue up 12.0% yoy; marginally higher than our expectation: On sales front,

the company posted sales of `3844cr (v/s. `3,715cr expected) v/s. `3,432cr in

3QFY2016, a yoy growth of 12.0%. The formulation sales (`3,130cr) posted a yoy

growth of 11.4%, while API (`775.9cr) posted a yoy growth of 11.6%. The US

business, which contributed 46% to the gross sales, witnessed a yoy growth of

17.8% in 3QFY2017.

In the formulation segment, the US (`1,735cr) posted a yoy growth of 17.8%,

while Europe & ROW (`990cr) posted a yoy growth of 7.6%. ARV (`279cr) posted

a yoy de-growth of 0.6%. Overall, formulations now contribute around 80.1% of

sales, while the balance is accounted by APIs. The company has 303 approved

ANDAs including 41 tentative approvals.

During 3QFY2017, the company filed 9 ANDAs with the USFDA, i.e. 5 in the oral

category and 4 in the injectable category. The company received 23 ANDA

approvals from the USFDA including 14 final approvals and 3 tentative approvals

during the quarter.

February 23, 2017

2

Aurobindo Pharma | 3QFY2017 Result Update

Exhibit 3: Sales break-up (Consolidated)

(` cr)

3QFY2017

2QFY2017

% chg (qoq)

3QFY2016

% chg (yoy)

9MFY2017 9MFY2016

% chg

Formulations

3,130

3,004

4.2

2,809

11.4

9,166

8,098

13.2

US

1,745

1,735

0.6

1,558

12.0

5,184

4,445

16.6

Europe & ROW

1,043

990

5.4

946

10.3

3,058

2,773

10.3

ARV

342

279

22.8

305

12.0

924

881

4.8

API

776

769

0.9

695

11.6

2279

2109

8.1

SSP

525

511

2.7

449

16.8

1531

1355

13.0

Cephs

251

258

(2.6)

246

2.1

748

755

(0.9)

NPNC

3,906

3,773

3.5

3,504

11.5

11,445

10,207

12.1

Source: Company, Angel Research

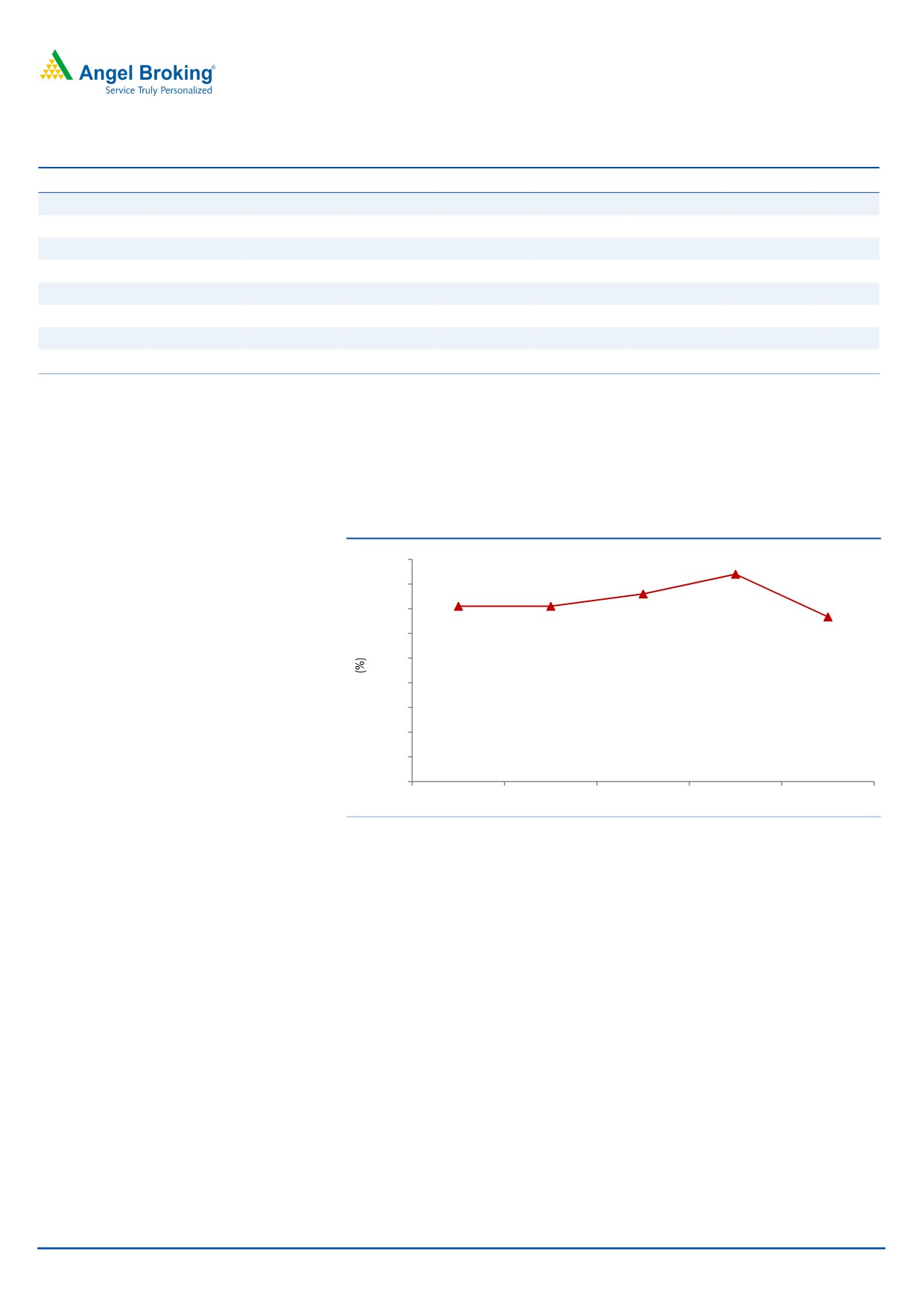

OPM comes in at 21.7%: On the operating front, the EBITDA margin came in at

21.7% (v/s. 23.1% expected) v/s. 22.1% in 3QFY2016. The gross margin came in

at 55.5% in 3QFY2017 v/s. 54.7% in 3QFY2016. Other expenses posted a yoy

growth of 16.4%.

Exhibit 4: OPM Trend

23.4

24.0

23.0

22.1

21.7

22.0

22.6

21.0

22.1

20.0

19.0

18.0

17.0

16.0

15.0

3QFY2016

4QFY2016

1QFY2017

2QFY2017

3QFY2017

Source: Company, Angel Research

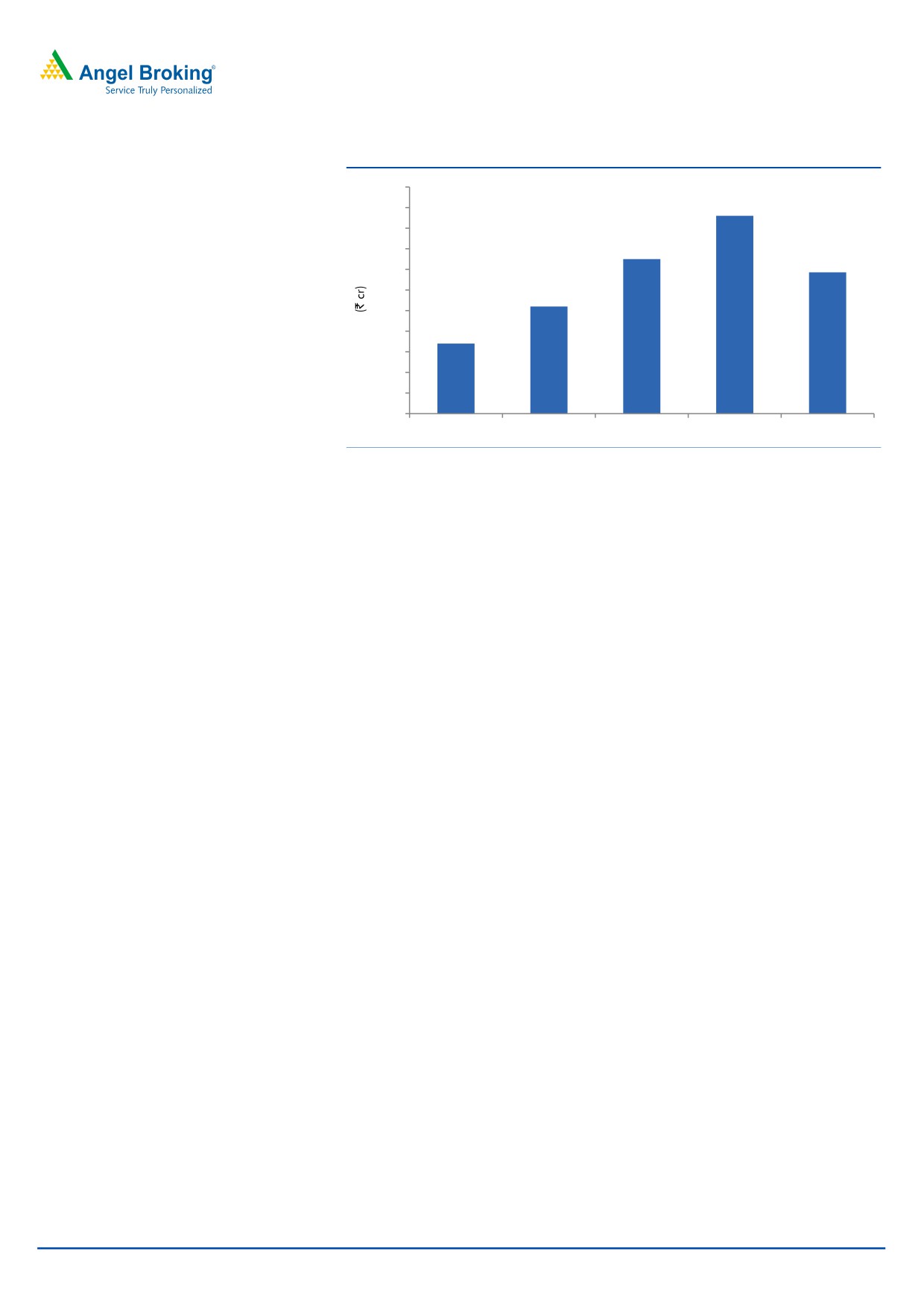

Net profit marginally lower than estimate: Consequently, the Adj. PAT came in at

`579cr (v/s. `603cr expected) v/s. `544cr in 3QFY2016, a yoy growth of 6.3%.

The lower than estimated net profit growth was aided by lower than expected

OPM.

February 23, 2017

3

Aurobindo Pharma | 3QFY2017 Result Update

Exhibit 5: Adj. net profit

620

606

610

600

590

585

579

580

570

562

560

550

544

540

530

520

510

3QFY2016

4QFY2016

1QFY2017

2QFY2017

3QFY2017

Source: Company, Angel Research

Management takeaways

At the end of 3QFY2017, the company had filed 421 ANDAs, with 303 final

approvals, and 41 tentative approvals.

R&D as % of sales to be ~5-6% in FY2018/FY2019.

Planning to increase Auro Life capacity in the US by 3x.

Transferred manufacturing of 42 products (to be sold in EU) to India till now;

plans to transfer >60 by the end of 4QFY2017.

Recommendation rationale

US and ARV formulation segments - the key drivers for base business: APL’s

business will primarily be driven by the US and ARV segments on the

formulation front. The company has been an aggressive filer in the US market

with 421 ANDAs filed until 3QFY2017. Amongst peers, APL has emerged as

one of the top ANDA filers. The company has aggressively filed ANDAs in the

last few years and is now geared to reap benefits, even though most of the

filings are for highly competitive products. Going ahead, with US$70bn going

off-patent in the US over the next three years, we believe APL is well placed to

tap this opportunity and is one of the largest generic suppliers. The company

enjoys high market share, as it is fully integrated in all its products apart from

having a larger product basket. Also, the company plans to launch

18

injectables in the next 2 years, which would drive its growth and profitability.

The US revenue has grown at a CAGR of 31% over FY2009-2015 to

`4,832cr. Going forward, the US business of the company is expected to post

a CAGR of 15% over FY2016-18E.

Acquisitions to augment growth and improve sales mix: APL announced the

signing of a binding offer to acquire commercial operations in seven Western

European countries from Actavis. The net sales from the acquired businesses

were around EUR320mn in 2013 with a growth rate of over 10% yoy. With

this, the European sales of the company would now be ~EUR400mn.

Although these businesses are currently loss-making (by around EUR20mn),

February 23, 2017

4

Aurobindo Pharma | 3QFY2017 Result Update

APL expects them to return to profitability in combination with its vertically

integrated platform and existing commercial infrastructure.

The acquisition will make APL one of the leading Indian pharmaceutical

companies in Europe with a position in the top 10 in several key markets,

which it plans to leverage to supply or widen its product portfolio through

introduction of its own products, especially high margin products like

injectiables.

Also, in December 2014, Aurobindo USA, spent US$132.5mn to acquire the

assets of Natrol with an agreement to take on certain liabilities. With this

acquisition, the company gets an entry into the nutraceutical markets.

Aurobindo USA believes that Natrol is an excellent strategic fit and provides

the right platform for creating a fully-integrated OTC platform in the USA and

in other international markets. Natrol, which manufactures and sells nutritional

supplements in USA and other international markets, provides Aurobindo

with-strong brand reputation and presence in a variety of attractive

supplement markets. Natrol has a proven performance in the mass market,

health food and specialty channels, and has existing long term relationships

with key distribution and retail partners. It addresses a broad range of

consumers and has an effective growth strategy to expand market penetration.

Outlook and valuation

We estimate the company’s net sales to log a CAGR of 15.1% over FY2016-18E to

`18,078cr on the back of US, which accounts for the largest portion of its product

pipeline. This, along with the recent acquisitions of the Western European

formulation businesses of Actavis and US’ Natrol, will lead APL to become a

>US$2bn sales company, with ~ 80% of sales being accounted by formulations.

We maintain our Buy rating on the stock.

Exhibit 6: Key assumptions

FY2017E

FY2018E

Sales Growth (%)

15.2

15.0

Operating Margins (%)

23.7

23.7

Capex (`cr)

800

800

Source: Company, Angel Research

February 23, 2017

5

Aurobindo Pharma | 3QFY2017 Result Update

Exhibit 7: One-year forward PE

900

800

700

600

500

400

300

200

100

0

5x

10x

15x

20x

Source: Company, Angel Research

Exhibit 8: Recommendation summary

Company

Reco

CMP Tgt. price Upside

FY2018E

FY16-18E

FY2018E

(`)

(`)

% PE (x) EV/Sales (x) EV/EBITDA (x) CAGR in EPS (%) RoCE (%) RoE (%)

Alembic Pharma

Neutral

593

-

-

19.5

2.6

12.2

(10.8)

27.5

25.3

Aurobindo Pharma Buy

686

877

27.9

14.5

2.4

10.1

18.1

22.5

26.1

Cadila Healthcare Neutral

440

-

-

22.9

3.6

16.6

13.5

23.6

27.1

Cipla

Sell

593

465

(21.5)

24.2

2.7

16.3

14.2

12.2

13.9

Dr Reddy's

Neutral

2,899

-

-

22.1

2.6

11.4

(2.7)

15.3

15.2

Dishman Pharma Neutral

229

-

-

20.3

2.3

10.0

13.3

10.3

10.9

GSK Pharma*

Neutral

2,683

-

-

44.5

6.8

32.8

16.9

37.5

34.5

Indoco Remedies

Reduce

272

240

(11.8)

17.0

2.0

10.9

33.2

19.1

20.1

Ipca labs

Accum

554

613

10.7

28.8

2.0

12.9

34.8

8.6

9.5

Lupin

Buy

1,469

1,809

23.1

21.2

4.0

13.1

17.2

24.4

20.9

Sanofi India

Neutral

4,186

-

-

24.3

3.2

17.4

22.2

25.6

28.8

Sun Pharma

Buy

673

847

25.8

19.1

4.0

12.2

26.5

18.9

20.1

Source: Company, Angel Research; Note: *December year ending

February 23, 2017

6

Aurobindo Pharma | 3QFY2017 Result Update

Company background

Aurobindo Pharma manufactures generic pharmaceuticals and APIs. The

company’s manufacturing facilities are approved by several leading regulatory

agencies like the USFDA, UK MHRA, WHO, Health Canada, MCC South Africa

and ANVISA Brazil among others. The company’s robust product portfolio is

spread over six major therapeutic/product areas encompassing antibiotics,

antiretrovirals, CVS, CNS, gastroenterological, and anti-allergics. The company

has acquired the generic business of Actavis, which has made it a US$2bn

company and a leading company in Europe. With this acquisition, formulations

now contribute around 80% to the company’s sales (as in FY2016).

February 23, 2017

7

Aurobindo Pharma | 3QFY2017 Result Update

Profit & loss statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Gross sales

5,863

8,198

12,221

13,878

15,959

18,353

Less: Excise duty

80

159

178

227

239

275

Net Sales

5,783

8,038

12,043

13,651

15,720

18,078

Other operating income

72

61

77

245

245

245

Total operating income

5,855

8,100

12,121

13,896

15,965

18,323

% chg

26.5

38.3

49.6

14.6

14.9

14.8

Total Expenditure

4,966

5,968

9,557

10,691

12,001

13,802

Net Raw Materials

2,792

3,606

5,506

6,158

6,288

7,231

Other Mfg costs

578

804

1,204

1,365

1,572

1,808

Personnel

663

832

1,302

1,551

1,783

2,051

Other

932

726

1,545

1,617

2,358

2,712

EBITDA

817

2,071

2,486

2,960

3,718

4,276

% chg

53.2

153.5

20.1

19.1

25.6

15.0

(% of Net Sales)

14.1

25.8

20.6

21.7

23.7

23.7

Depreciation& Amort.

249

313

333

393

532

588

EBIT

568

1,758

2,154

2,567

3,187

3,689

% chg

38.8

209.5

22.5

19.2

24.1

15.7

(% of Net Sales)

9.8

21.9

17.9

18.8

20.3

20.4

Interest & other Charges

131

108

84

159

192

220

Other Income

29

23

81

68

68

68

(% of PBT)

5.3

1.3

3.6

2.5

2.1

1.8

Share in profit of Asso.

-

-

-

-

-

-

Recurring PBT

538

1,735

2,227

2,722

3,309

3,782

% chg

62.3

222.7

28.4

22.2

21.5

14.3

Extraordinary Exp./(Inc.)

163.4

203.1

59.6

-

-

-

PBT (reported)

374

1,532

2,168

2,722

3,309

3,782

Tax

82.7

363.5

596.6

744.4

893.4

1,021.2

(% of PBT)

22.1

23.7

27.5

27.3

27.0

27.0

PAT (reported)

291

1,168

1,571

1,978

2,416

2,761

Less: Minority int. (MI)

(2)

(4)

(5)

(4)

(3)

(2)

PAT after MI (reported)

294

1,172

1,576

1,982

2,418

2,763

ADJ. PAT

432

1,333

1,619

1,982

2,418

2,763

% chg

118.5

208.6

21.5

22.4

22.0

14.2

(% of Net Sales)

5.1

14.6

13.1

14.5

15.4

15.3

Basic EPS (`)

7.4

22.8

27.7

33.9

41.4

47.3

% chg

8.9

208.6

21.5

22.4

22.0

14.2

February 23, 2017

8

Aurobindo Pharma | 3QFY2017 Result Update

Balance sheet (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

SOURCES OF FUNDS

Equity Share Capital

29

29

29

58

58

58

Share Application Money

-

-

-

-

-

-

Reserves & Surplus

2,577

3,721

5,127

6,998

9,246

11,838

Shareholders Funds

2,606

3,750

5,156

7,057

9,304

11,896

Minority Interest

11

26

26

60

57

55

Long-term provisions

9

9

24

24

24

24

Total Loans

3,384

3,769

3,864

4,076

5,500

5,500

Deferred Tax Liability

68

205

211

236

236

236

Total Liabilities

6,069

7,760

9,280

11,452

15,098

17,688

APPLICATION OF FUNDS

Gross Block

3,316

4,107

6,095

7,195

7,995

8,795

Less: Acc. Depreciation

1,140

1,461

1,794

2,187

2,718

3,306

Net Block

2,175

2,645

3,752

4,865

5,277

5,490

Capital Work-in-Progress

645

310

310

310

310

310

Goodwill

55

76

64

89

89

89

Investments

22

20

20

0

0

0

Long-term loans and adv.

243

789

486

434

434

436

Current Assets

4,128

5,631

8,279

10,001

12,249

15,113

Cash

208

179

469

834

2,089

2,275

Loans & Advances

332

789

692

784

409

1,625

Other

3,587

4,664

7,118

8,383

9,751

11,213

Current liabilities

1,200

1,730

3,634

4,247

3,261

3,750

Net Current Assets

2,928

3,901

4,645

5,755

8,988

11,363

Mis. Exp. not written off

-

18

5

-

-

-

Total Assets

6,069

7,760

9,280

11,452

15,098

17,688

February 23, 2017

9

Aurobindo Pharma | 3QFY2017 Result Update

Cash flow statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Profit before tax

374

1,532

2,168

2,722

3,309

3,782

Depreciation

249

313

333

393

532

588

(Inc)/Dec in Working Capital

(191)

(457)

(757)

(796)

(1,979)

(2,188)

Less: Other income

29

23

81

68

68

68

Direct taxes paid

(83)

(363)

(597)

(744)

(893)

(1,021)

Cash Flow from Operations

321

1,001

1,066

1,507

900

1,093

(Inc.)/Dec.in Fixed Assets

(283)

(455)

(1,989)

(1,100)

(800)

(800)

(Inc.)/Dec. in Investments

(16)

(2)

-

(20)

-

-

Other income

29

23

81

68

68

68

Cash Flow from Investing

(271)

(435)

(1,908)

(1,051)

(732)

(732)

Issue of Equity

-

-

-

-

-

-

Inc./(Dec.) in loans

288

385

94

213

1,424

-

Dividend Paid (Incl. Tax)

(17)

(102)

(171)

(171)

(171)

(171)

Others

(183)

(879)

1,209

(132)

(167)

(4)

Cash Flow from Financing

88

(596)

1,133

(90)

1,086

(175)

Inc./(Dec.) in Cash

138

(30)

291

365

1,255

186

Opening Cash balances

71

208

179

469

834

2,089

Closing Cash balances

208

179

469

834

2,089

2,275

February 23, 2017

10

Aurobindo Pharma | 3QFY2017 Result Update

Key ratios

Y/E March

FY2013

FY2014

FY2015

FY2016

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

92.7

30.0

24.7

20.2

16.6

14.5

P/CEPS

36.8

13.5

10.5

16.9

13.6

12.0

P/BV

7.7

5.3

3.9

5.7

4.3

3.4

Dividend yield (%)

0.1

0.1

0.1

0.1

0.1

0.1

EV/Sales

4.0

2.9

1.9

3.2

2.8

2.4

EV/EBITDA

28.3

11.4

9.4

14.6

11.7

10.1

EV / Total Assets

3.8

3.0

2.5

3.8

2.9

2.4

Per Share Data (`)

EPS (Basic)

7.4

22.8

27.7

33.9

41.4

47.3

EPS (fully diluted)

7.4

22.8

27.7

33.9

41.4

47.3

Cash EPS

18.6

51.0

65.4

40.7

50.5

57.4

DPS

0.5

0.5

0.5

0.5

0.5

0.5

Book Value

89.5

128.8

176.6

120.8

159.3

203.7

Dupont Analysis

EBIT margin

9.8

21.9

17.9

18.8

20.3

20.4

Tax retention ratio

77.9

76.3

72.5

72.7

73.0

73.0

Asset turnover (x)

1.0

1.2

1.5

1.4

1.4

1.3

ROIC (Post-tax)

8.0

20.1

19.2

19.5

20.0

19.2

Cost of Debt (Post Tax)

3.2

2.3

1.6

2.9

2.9

2.9

Leverage (x)

1.3

1.1

0.8

0.6

0.4

0.3

Operating ROE

14.0

39.5

33.4

28.9

27.1

24.4

Returns (%)

ROCE (Pre-tax)

9.9

25.4

25.3

24.8

24.0

22.5

Angel ROIC (Pre-tax)

11.5

28.5

27.6

27.5

27.9

26.7

ROE

17.5

41.9

36.4

32.5

29.6

26.1

Turnover ratios (x)

Asset Turnover (Gross Block)

1.8

2.2

2.4

2.1

2.1

2.2

Inventory / Sales (days)

98

49

90

95

101

108

Receivables (days)

129

95

93

95

63

63

Payables (days)

78

73

114

119

81

81

WC cycle (ex-cash) (days)

159

145

119

119

135

159

Solvency ratios (x)

Net debt to equity

1.2

1.0

0.7

0.5

0.4

0.3

Net debt to EBITDA

3.9

1.7

1.4

1.1

0.9

0.8

Interest Coverage (EBIT / Int.)

4.3

16.3

25.5

16.2

16.6

16.8

February 23, 2017

11

Aurobindo Pharma | 3QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Aurobindo Pharma

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 23, 2017

12