2QFY2017 Result Update | Auto Ancillary

November 8, 2016

Amara Raja Batteries

BUY

CMP

`1,010

Performance Highlights

Target Price

`1,167

Y/E March (` cr)

3QFY16 3QFY15

% chg (yoy) 2QFY16

% chg (qoq)

Investment Period

12 Months

Net Sales

1,346

1,158

16.2

1,321

1.9

EBITDA

230

199

15.6

227

1.1

Stock Info

EBITDA Margin (%)

17.1

17.2

(8 bp)

17.2

(13 bp)

Sector

Auto Ancillary

Adj. PAT

136

123

11.2

131

4.3

Market Cap (` cr)

17,259

Source: Company, Angel Research

Net Debt (` cr)

(76)

Results ahead of estimates: Amara Raja Batteries (ARBL) reported 16.2% yoy

Beta

0.8

growth in its 2QFY2017 sales to `1,346cr. The company reported PAT of `136cr,

52 Week High / Low

1,077/773

yoy 11.2% growth. EBTIDA margins were at 17.1% vs. 17.2% in Q2FY2016.

Avg. Daily Volume

28,165

Margins contracted by 8bp yoy as raw material costs increased by 16.6% yoy. In

Face Value (`)

1

percent of sale terms, RM costs were at 64.3% vs. 64.0% in Q2FY2016. During

BSE Sensex

27,591

this period, lead prices have gone up by 9% yoy. In Q2FY2017, ARBL gained

Nifty

8,544

market share in the automotive battery segment, due to double digit growth in

Reuters Code

AMAR.BO

aftermarket brands, Amaron and PowerZone. During the quarter company also

Bloomberg Code

AMRJ@IN

saw higher sales of batteries to automobile OEMs. Capacity utilization improved

as exports have picked up. Company also reported a double digit growth in its

industrial battery business despite a challenging environment.

Shareholding Pattern (%)

Outlook and Valuation: We believe that ARBL is likely to continue gaining market

Promoters

52.1

share in the automotive battery segment. The strategy followed by automotive

MF / Banks / Indian Fls

7.8

OEMs of sourcing from multiple vendors as against having a single vendor is

FII / NRIs / OCBs

21.5

likely to benefit ARBL. Further, with the company’s strengthening distribution

Indian Public / Others

18.6

network in the Western and Eastern markets, we expect replacement sales to grow

in strong double digits, going forward. We also expect healthy growth in exports

as company is targeting ~10% of sales form exports from current ~6%. Overall,

Abs. (%)

3m 1yr

3yr

we expect ARBL to post a healthy top-line CAGR of 19% over FY2016 to FY2018E

Sensex

6.3

(2.3)

37.5

on the back of strong recovery in OEM market, brand strength and gain in

Amara Raja

11.6

14.2

221.6

market share. We also assume company to benefit from its ongoing capacity

expansion program. We expect ARBL to clock 20% earnings CAGR over the next

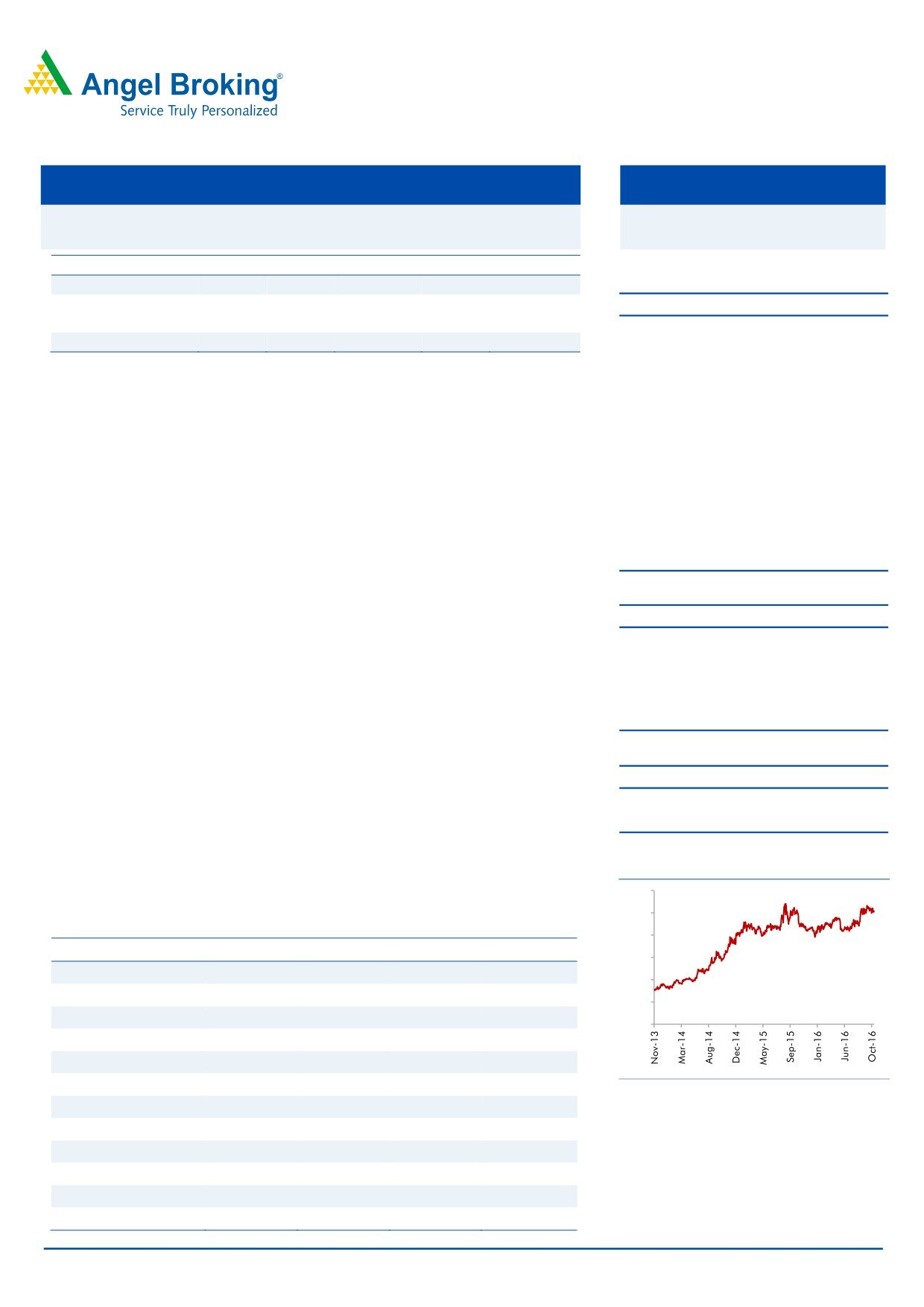

3-year price chart

two years. We maintain our positive view on the stock and reiterate our Buy rating

1200

on the stock with a target price of `1,167 (based on 28.5x FY2018E earnings).

1000

Key financials (Standalone)

800

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

600

Net Sales

4,211

4,691

5,504

6,605

400

% chg

22.0

11.4

15.7

15.7

200

Net Profit

411

489

571

699

0

% chg

11.8

19.1

16.7

22.4

OPM (%)

16.7

17.4

17.6

17.5

EPS (`)

24.1

28.7

33.4

40.9

Source: Company, Angel Research

P/E (x)

42.0

35.3

30.2

24.7

P/BV (x)

10.2

8.2

6.7

5.4

RoE (%)

24.2

23.3

22.1

22.0

RoCE (%)

32.0

31.1

29.8

29.4

Amarjeet S Maurya

EV/Sales (x)

4.1

3.7

3.1

2.6

022-3935 7800 Ext: 6846

EV/EBITDA (x)

24.4

21.0

17.8

14.7

Source: Company, Angel Research; Note: CMP as of November 8, 2016

Please refer to important disclosures at the end of this report

1

Amara Raja Batteries | 2QFY2017 Result Update

Exhibit 1: Quarterly financial performance (Standalone)

Y/E March (` cr)

2QFY17

2QFY16

% chg (yoy) 1QFY17

% chg (qoq) 6MFY17 6MFY16

% chg (yoy)

Net Sales

1,346

1,158

16.2

1,321

1.9

2,666

2,289

16.5

Raw-material cost

865

742

16.6

875

(1.1)

1,739

1,476

17.9

(% of Sales)

64.3

64.0

66.2

519.2

491.5

Staff cost

69

58

19.6

66

5.7

135

114

18.5

(% of Sales)

5.2

5.0

5.0

40.3

37.9

Other Expenses

182

160

13.8

153

18.7

335

300

11.6

(% of Sales)

13.5

13.8

11.6

100.0

100.0

Total Expenditure

1,116

960

16.3

1,094

2.0

2,209

1,890

16.9

Operating Profit

230

199

15.6

227

1.1

457

399

14.6

OPM (%)

17.1

17.2

17.2

136.4

132.8

Interest

1

0

n.a.

1

6.4

2.89

1

118.9

Depreciation

46

34

33.2

44

3.7

90

67

33.7

Other Income

12

12

2.9

9

33.9

20.93

25

-16.9

PBT (excl. Extr. Items)

195

176

10.5

191

2.0

385

356

8.4

Extr. Income/(Expense)

0

PBT (incl. Extr. Items)

195

176

10.5

191

2.0

385

356

8.4

(% of Sales)

14.5

15.2

14.4

115.0

118.4

Provision for Taxation

58

53

8.9

60

(3.2)

118

111

6.9

(% of PBT)

29.9

30.4

31.5

44.3

45.2

Reported PAT

136

123

11.2

131

4.3

267

245

9.0

Adj PAT

136

123

11.2

131

4.3

267

245

9.0

Adj. PATM

10.1

10.6

9.9

79.7

81.6

Equity capital (cr)

17

17

17

17

17

Reported EPS (`)

7.98

7.18

11.2

7.65

4.3

15.6

14.3

9.0

Source: Company, Angel Research

ARBL continues to gain market share: ARBL in the first quarter of FY2017 reported

a healthy 16.8% growth in its revenues and in Q2FY2017 the momentum has

continued. Its competitor Exide Industries in FY2017 so far has reported a yoy

growth of 11% which indicates that ARBL continues to gain market share. From the

results, it is also clear ARBL continues to maintain higher profitability compared to

its competitor. While ARBL reported EBITDA margin of 17.1% in Q2FY2017, Exide

Industries reported EBITDA margin of 15.2% in the same quarter. This superior

performance has on the back of competitive pricing, just in-time deliveries, custom

designed products and solutions and strong brand positioning.

November 8, 2016

2

Amara Raja Batteries | 2QFY2017 Result Update

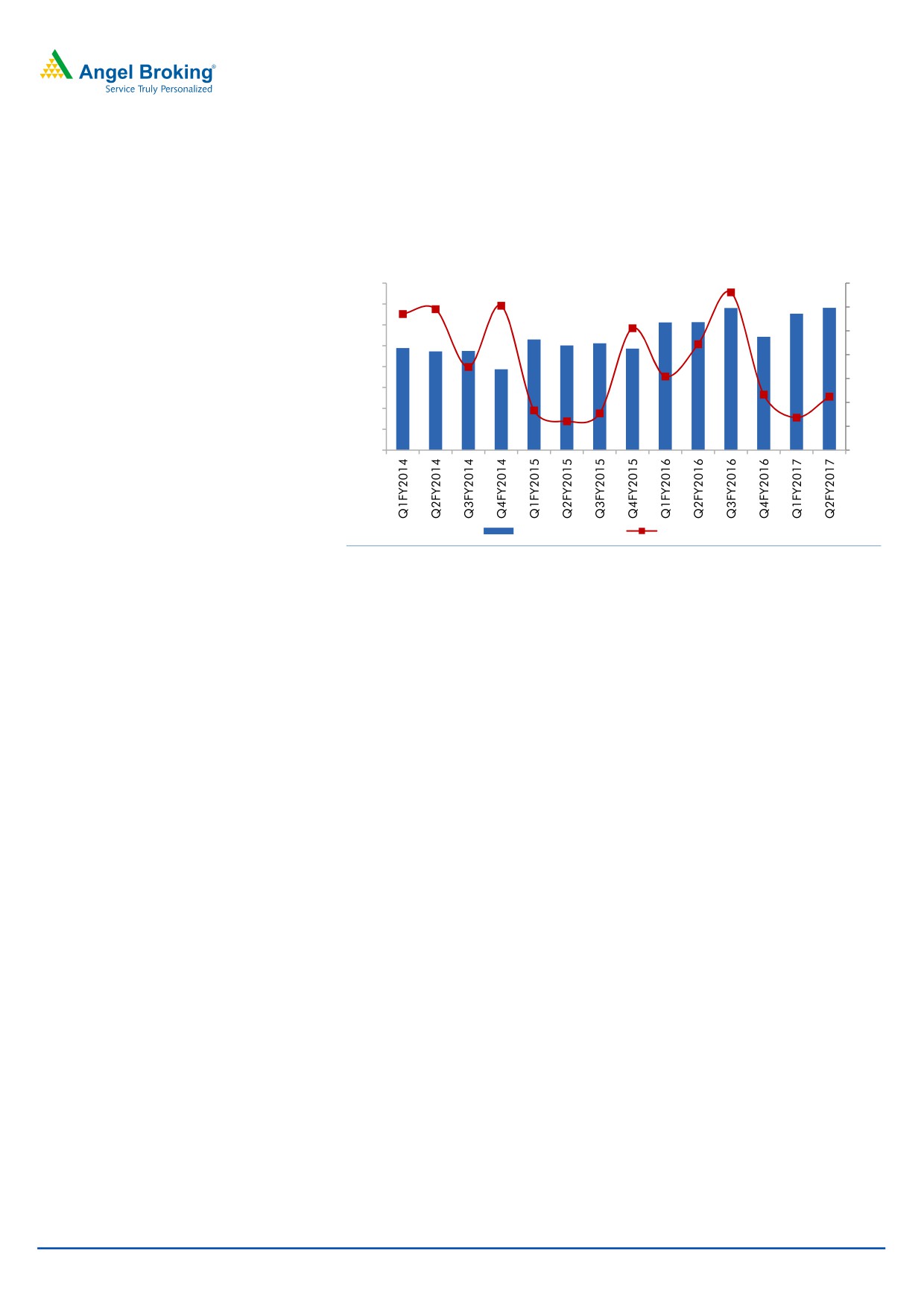

Exhibit 2: Top-line is witnessing strong growth in FY2017

1,600

35

1,400

30

1,200

25

1,000

20

800

15

600

10

400

200

5

0

0

Net sales (` cr)

YoY growth (%)

Source: Company, Angel Research

Lead prices slowly firming up: In 2QFY2017, lead prices have moved up by 9%

yoy which led to increase in ARBL’s raw material costs. Its raw material costs

increased by 16.6% yoy vs. sales growth of 16.2% yoy which led to 22bp yoy

decline in gross margins to 35.7%.Currently the lead prices are at USD 2,070 per

MT, showing yoy rise of 23% indicating that the company may see rise in the raw

material prices in the next quarter.

Exhibit 3: Recent uptrend in lead prices

Exhibit 4: Flat EBITDA margin due to rising lead prices

2,500.0

250

20

2,300.0

200

15

150

2,100.0

10

100

5

1,900.0

50

0

0

1,700.0

1,500.0

EBITDA (` cr)

EBITDA margins (%)

Source: Company, Angel Research

Source: Company, Angel Research

November 8, 2016

3

Amara Raja Batteries | 2QFY2017 Result Update

Net profit grows by yoy 11%: ARBL’s adjusted net profit for the quarter was at

`136cr, showing a yoy growth of 11.2%. Net margins however declined by

~100bp mainly due to the higher depreciation expenses on account its ongoing

capacity expansion plan, which rose by 33.2% yoy to `45.7cr.

Exhibit 5: Bottom-line growth impacted due to the high base in Q2FY16

160

35

140

30

120

25

100

20

80

15

60

10

40

20

5

0

0

Net profit (` cr)

YoY growth (%)

Source: Company, Angel Research

November 8, 2016

4

Amara Raja Batteries | 2QFY2017 Result Update

Investment arguments

Demand scenario for automotive and industrial batteries to remain positive in

the long run: We expect growth traction in the automotive battery segment to

continue over the next two years. The automotive OEM segment is likely to

witness strong growth over the next two years on the back of recovery in the

OEM sales, subdued fuel prices and further easing of interest rates. The high

margin automotive replacement demand is likely to maintain growth

momentum. Further, given the economic recovery, the industrial segment

(railways, UPS and telecom) is also poised to register double-digit growth over

the next two years.

Likely to outpace industry growth on increased sourcing by automotive OEM

segment: ARBL has outpaced the battery industry over the last four to five

years. Penetration into the new automotive OEM segment has led to market

share gains for ARBL. OEM customers both in the 4W and 2W segments have

strategically opted to source from ARBL in order to follow multiple sourcing

and reduce dependence on a single supplier. Also, by strengthening its

distribution reach in the Eastern and Western markets, ARBL is likely to gain

market share in the automotive replacement segment as well. We believe

ARBL would continue to gain market share in the near term and expect it to

post a top-line CAGR of 19% over FY2016-2018E.

Capacity expansion to address growing demand: To cater the growing

demand in automotive segment, ARBL has taken capacity expansion program

in 2W battery segment. This will be completed in the next four years taking its

capacity from current ~11mn units to ~25mn units per annum. ARBL has

already commissioned its Chittoor 2W battery capacity. On 4W battery front,

ARBL is expanding its capacity from 8.25mn units to 11mn units per year. The

tabular capacity has already been completed has started to contribute in

production. Overall company is in capacity expansion mode and

commissioning of new capacities will give a much required thrust for future

growth of the company.

Outlook and valuation

We believe that ARBL is likely to continue gaining market share in the automotive

battery segment. The strategy followed by automotive OEMs of sourcing from

multiple vendors as against having a single vendor is likely to benefit ARBL.

Further, with the company’s strengthening distribution network in the Western and

Eastern markets, we expect replacement sales to grow in strong double digits,

going forward. We also expect the Industrial segment growth to be in healthy

double digits over FY2017E-2018E, given that the telecom players are resorting to

aggressive network expansion, and also with ARBL entering tubular battery

manufacturing. We expect ARBL to record a healthy top-line CAGR of 19% over

FY2016 to FY2018E on the back of strong recovery in OEM market, brand

strength and gain in market share. We assume some impact of the increasing lead

prices on its raw material however we expect net profit growth to remain strong.

We expect ARBL to clock 20% earnings CAGR over the next two years. We

maintain our positive view on the stock and reiterate our Buy rating on the stock

with a target price of `1,167 (based on 28.5x FY2018E earnings).

November 8, 2016

5

Amara Raja Batteries | 2QFY2017 Result Update

Company background

Amara Raja Batteries Ltd (ARBL) is a leading automobile and industrial battery

manufacturer in India. It is the second largest lead acid battery manufacturer

having a market share of about ~35% in the organized battery industry. ARBL has

a technological tie-up with US based Johnson Controls, which also holds 26%

stake in it. The Automotive and Industrial battery segments each accounted for

~50% of the company's total revenue in FY2015.

November 8, 2016

6

Amara Raja Batteries | 2QFY2017 Result Update

Profit and loss statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

Total operating income

2,979

3,452

4,211

4,691

5,504

6,605

% chg

25.5

15.9

22.0

11.4

17.3

20.0

Total Expenditure

2,517

2,880

3,510

3,874

4,537

5,447

Cost of Materials

1,991

2,283

2,776

2,964

3,513

4,241

Personnel

127

158

195

243

285

337

Others Expenses

399

439

538

666

739

869

EBITDA

461

572

702

817

967

1,159

% chg

29.0

23.9

22.8

16.4

18.4

19.8

(% of Net Sales)

15.5

16.6

16.7

17.4

17.6

17.5

Depreciation& Amortisation

66

65

134

140

175

200

EBIT

395

507

568

677

792

959

% chg

27.0

28.3

12.0

19.2

17.0

21.0

(% of Net Sales)

13.3

14.7

13.5

14.4

14.4

14.5

Interest & other Charges

0

1

0

0

5

4

Other Income

27

30

42

46

45

56

(% of PBT)

6.4

5.7

6.9

6.3

5.4

5.6

Share in profit of Ass.

-

-

-

-

-

-

Recurring PBT

422

537

610

722

833

1,011

% chg

32.4

27.2

13.6

18.4

15.3

21.4

Prior Period & Extra. Exp.

-

-

-

-

-

-

PBT (reported)

422

537

610

722

833

1,011

Tax

135

169

199

233

261

311

(% of PBT)

32.0

31.5

32.6

32.2

31.4

30.8

PAT (reported)

287

367

411

489

571

699

Add: Share of earnings of ass.

-

-

-

-

-

-

Less: Minority interest (MI)

-

-

-

-

-

-

PAT after MI (reported)

287

367

411

489

571

699

ADJ. PAT

287

367

411

489

571

699

% chg

32.4

28.2

11.8

19.1

16.7

22.4

(% of Net Sales)

9.6

10.6

9.8

10.4

10.4

10.6

Basic EPS (`)

16.8

21.5

24.1

28.7

33.4

40.9

Fully Diluted EPS (`)

16.8

21.5

24.1

28.7

33.4

40.9

% chg

32.4

28.2

11.8

19.1

16.7

22.4

November 8, 2016

7

Amara Raja Batteries | 2QFY2017 Result Update

Balance sheet statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

SOURCES OF FUNDS

Equity Share Capital

17

17

17

17

17

17

Reserves& Surplus

1,043

1,346

1,683

2,085

2,570

3,164

Shareholders’ Funds

1,060

1,363

1,700

2,102

2,587

3,181

Minority Interest

-

-

-

-

-

-

Total Loans

88

86

76

74

75

75

Deferred Tax Liability

24

34

42

65

65

65

Total Liabilities

1,172

1,482

1,817

2,241

2,727

3,321

APPLICATION OF FUNDS

Gross Block

680

996

1,441

1,915

2,415

2,865

Less: Acc. Depreciation

314

365

497

598

773

973

Net Block

366

631

944

1,316

1,641

1,891

Capital Work-in-Progress

103

145

86

120

120

120

Investments

16

16

16

16

16

16

Current Assets

1,285

1,192

1,340

1,456

1,641

2,085

Inventories

293

335

418

602

709

851

Sundry Debtors

381

453

554

592

679

814

Cash

411

295

222

150

127

268

Loans & Advances

173

60

75

64

72

86

Other Assets

28

49

70

48

55

66

Current liabilities

603

505

574

674

697

797

Net Current Assets

682

687

766

782

944

1,288

Deferred Tax Asset

5

4

5

6

6

6

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

1,172

1,482

1,817

2,241

2,727

3,321

November 8, 2016

8

Amara Raja Batteries | 2QFY2017 Result Update

Cash flow statement (Standalone)

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E FY18E

Profit before tax

422

537

610

722

833

1,011

Depreciation

59

65

134

140

175

200

Change in Working Capital

(9)

(132)

(145)

(68)

(185)

(203)

Interest / Dividend (Net)

(26)

(28)

(17)

(9)

5

4

Direct taxes paid

(137)

(160)

(192)

(218)

(261)

(311)

Others

27

(3)

5

(12)

-

-

Cash Flow from Operations

335

279

395

555

566

700

(Inc.)/ Dec. in Fixed Assets

(119)

(342)

(294)

(387)

(500)

(450)

(Inc.)/ Dec. in Investments

-

-

-

-

-

-

Cash Flow from Investing

(119)

(342)

(294)

(387)

(500)

(450)

Issue of Equity

-

-

-

-

-

-

Inc./(Dec.) in loans

-

(1)

-

-

1

-

Dividend Paid (Incl. Tax)

(32)

(43)

(65)

(161)

(86)

(105)

Interest / Dividend (Net)

(1)

(7)

138

70

(5)

(4)

Cash Flow from Financing

(34)

(51)

73

(92)

(90)

(109)

Inc./(Dec.) in Cash

182

(115)

174

76

(24)

141

Opening Cash balances

228

409

48

75

150

127

Closing Cash balances

411

295

222

150

127

268

November 8, 2016

9

Amara Raja Batteries | 2QFY2017 Result Update

Key ratios

Y/E March

FY13

FY14

FY15

FY16

FY17E FY18E

Valuation Ratio (x)

P/E (on FDEPS)

60.2

47.0

42.0

35.3

30.2

24.7

P/CEPS

65.6

48.9

39.9

31.7

27.4

23.1

P/BV

16.3

12.7

10.2

8.2

6.7

5.4

Dividend yield (%)

0.2

0.2

0.3

0.4

0.4

0.5

EV/Sales

5.7

4.9

4.1

3.7

3.1

2.6

EV/EBITDA

36.7

29.8

24.4

21.0

17.8

14.7

EV / Total Assets

9.5

8.6

7.2

5.9

5.0

4.1

Per Share Data (`)

EPS (Basic)

16.8

21.5

24.1

28.7

33.4

40.9

EPS (fully diluted)

16.8

21.5

24.1

28.7

33.4

40.9

Cash EPS

15.4

20.7

25.3

31.9

36.8

43.7

DPS

1.9

2.5

3.2

3.6

4.3

5.0

Book Value

62.1

79.8

99.5

123.0

151.5

186.3

Returns (%)

ROCE

34.4

35.0

32.0

31.1

29.8

29.4

Angel ROIC (Pre-tax)

54.8

44.6

36.9

33.7

31.5

32.2

ROE

27.1

27.0

24.2

23.3

22.1

22.0

Turnover ratios (x)

Asset Turnover (Gross Block)

4.4

3.5

2.9

2.4

2.3

2.3

Inventory / Sales (days)

36

35

36

47

47

47

Receivables (days)

47

48

48

46

45

45

Payables (days)

19

15

24

29

28

27

WC cycle (ex-cash) (days)

63

68

60

64

64

65

November 8, 2016

10

Amara Raja Batteries | 2QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Amara Raja Batteries

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 8, 2016

11