Initiating coverage | Pharma

January 3, 2017

Alkem Laboratories

BUY

CMP

`1,620

Relieving pain

Target Price

`1,989

Alkem Laboratories is a Mumbai based pharma company engaged in

Investment Period

12 Months

manufacturing and marketing of generic drugs, APIs and neutraceutical products.

Company sells its drugs in India and ~50 countries including the US. It has 16

Stock Info

manufacturing facilities of which 14 are in India and two in the USA.

Sector

Pharma

Strong domestic business- Alkem is the 5th largest pharma company in India in

Market Cap (` cr)

19,397

terms of domestic revenues. Its acute segment contributes 88% of domestic

Net Debt (` cr)

80

revenue while chronic business contributes 12%. In the acute business, company

Beta

0.2

is ranked #1 in anti-infective segment and #3 each in pain and Gastro intestinal

52 Week High / Low

1,853/1,175

segments. Alkem is currently a small player in the chronic segment but it is

Avg. Daily Volume

36,397

expanding this business rapidly.

Face Value (`)

2

Domestic business to continue its outperformance vs. industry: Alkem is expected

BSE Sensex

26,595

to continue its outperformance vs. industry due to strong growth in its acute and

Nifty

8,180

chronic segments. Both segments are expected to grow at CAGR of 16% and 30%

Reuters Code

ALKE.BO

respectively in next 3 years due to higher sales of major brands and market share

gains. We expect domestic sales to grow at 15.8% CAGR to `5,620cr in FY19E,

Bloomberg Code

ALKEM IN

vs. domestic industry growth of ~14% in next 3 years.

US revenue to double with increased ANDA monetization: Alkem’s ANDA pipeline

Shareholding Pattern (%)

increased 2.5x from 31 ANDAs in FY12 to 76 ANDAs in H1FY17. ANDA

Promoters

66.9

approvals also grew by 2.8x during the same period. In next three years company

expects increased ANDA launches on the back of approval to 2/3rd of its pipeline.

MF / Banks / Indian Fls

3.3

This will to double its US revenue from `991cr in FY16 to `1,919cr in FY19E.

FII / NRIs / OCBs

3.7

Improving operating performance: Alkem’s operating performance is expected to

Indian Public / Others

26.1

improve with better sales mix (increasing exports) and market share gains in

chronic segment. The company has already seen margin improvement and with

rising profitability of US business, we estimate 70-100bps margin expansion.

Abs. (%)

3m 6m 1yr

Sensex

(4.6)

(2.1)

1.7

Outlook and Valuation: The stock at the CMP of `1,620 is available at P/E of

15.5x of FY19E EPS of `105, which is at ~15% discount to average P/E (18.4x) of

Alkem

(2.5)

18.7

8.2

the peer group. In our view this discount is unwarranted considering 1) Strong

earnings momentum (CAGR of 22.3% in PAT from FY16-FY19E vs. CAGR of

Price Chart

18.3% from FY11-FY16), 2) Improving RoE (average 21.5% RoE from FY17E-

2,000

1,800

FY19E) and 3) Increasing ANDA pipeline and near term launches in the US. We

1,600

rate Alkem ‘Buy’ with a price target of `1,989 (19.0x of FY19E earnings).

1,400

1,200

1,000

Key Financials (Consolidated)

800

Y/E March (` cr)

FY15

FY16

FY17E

FY18E

FY19E

600

Net Sales

3,743

4,992

6,043

6,893

8,114

400

% chg

19.7

33.3

21.1

14.1

17.7

200

0

Net Profit

392

684

973

1,062

1,251

% chg

(10.0)

71.9

44.5

9.2

17.8

OPM (%)

11.3

17.0

18.7

19.3

19.4

EPS (`)

32.8

56.3

81.4

88.8

104.7

Source: Company, Angel Research

P/E (x)

49.5

28.8

19.9

18.2

15.5

P/BV (x)

6.5

5.5

4.5

3.8

3.3

RoE (%)

13.1

19.2

22.7

20.9

21.0

RoCE (%)

8.0

17.6

20.3

20.5

21.1

Shrikant Akolkar

EV/Sales (x)

5.2

3.8

3.1

2.7

2.3

022 - 3935 7800 Ext: 6846

EV/EBITDA (x)

46.2

22.3

16.8

14.2

11.8

Source: Company, Angel Research; Note: CMP as of January 2, 2017

Please refer to important disclosures at the end of this report

1

Initiating coverage | Alkem Laboratories

Company background

Alkem is a leading Indian pharmaceutical company with major operations in India

and the USA. It is the fifth largest pharmaceutical company in India in terms of

domestic sales and a market leader in anti-infective therapeutic segment. Alkem

was founded in 1973 and produces branded generics, generic drugs, active

pharmaceutical ingredients, which are then sold in its end markets. For FY2016,

Alkem generated 73% revenue from domestic operations and rest 27% from

international operations. It has a portfolio of more than 800 brands in India and a

pipeline of 76 abbreviated new drugs applications (ANDA) of which 34 are

approved as of September Q2FY2016.

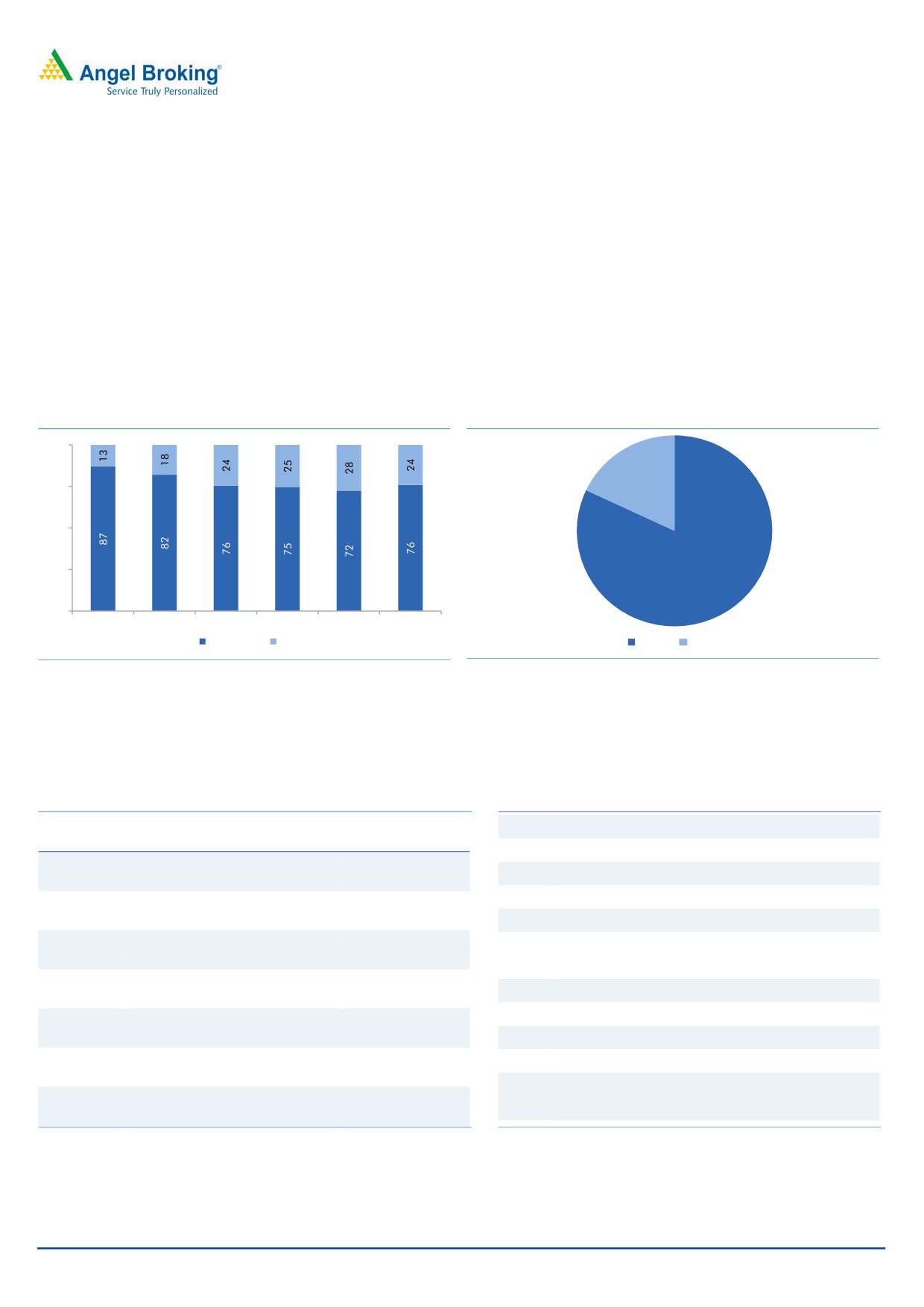

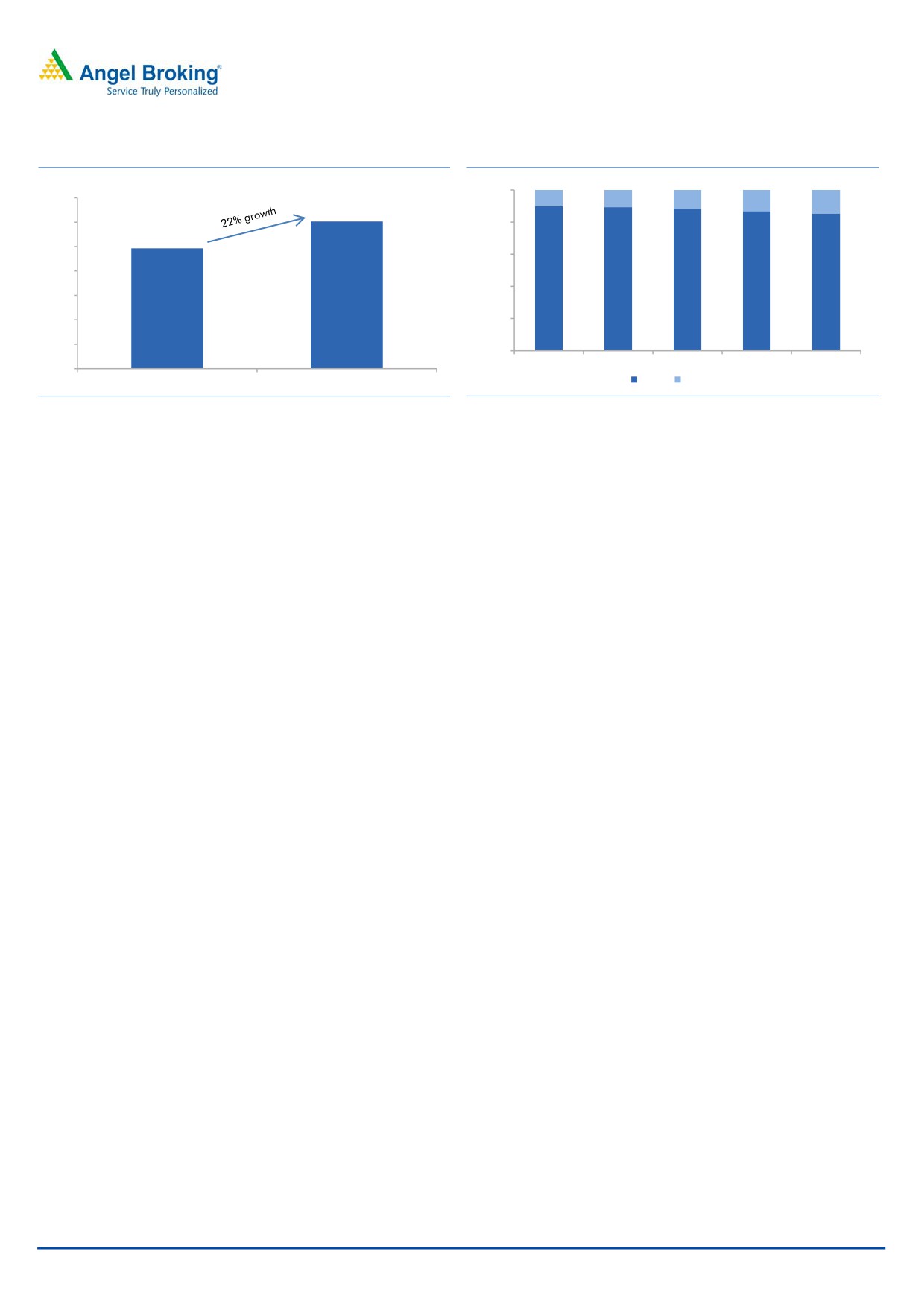

Exhibit 1: Evolution of business mix (%)

Exhibit 2: Domestic business mix

100

18

75

50

25

82

0

FY2012

FY2013

FY2014

FY2015

FY2016

Q2FY2017

Domestic

Exports

Acute

Chronic

Source: Company, Angel Research

Source: Company, Angel Research

Alkem has total 16 manufacturing facilities, 14 in India and 2 in USA - all

approved by regulatory authorities such as USFDA, UK MHRA, TGAAustralia,

WHO, etc.

Exhibit 3: Manufacturing facilities

Exhibit 4: Key milestones in corporate history

Geographical

1973 Incorporation of the company

Facility

Regulatory approval

Focus

1978 Established Taloja manufacturing facility

Baddi

USFDA, UK-MHRA, WHO-GMP

India + US + Global

1992 Established Mandva manufacturing facility

2003 Set up of Taloja R&D facility for ANDA development

Sikkim

WHO-GMP

India

2007 Filed its first ANDA in the US

Received its first ANDA approval

#Daman USFDA, UK-MHRA, Indian GMP

India + US + Global

2009

Acquisition of Pharmacor Pty Ltd

#Mandva Indian GMP, USFDA

India + US

2010 Acquisition of Ascend Laboratories

2011 Acquisition of Enzene

*Ankaleshwar Indian GMP, USFDA, TGA-Australia US

2012 Acquisition of an API Manufacturing facility in the USA.

2014 Acquisition of “Clindac-A” brand from Galderma S.A.

California

USFDA

US

Acquisition of formulation 1) manufacturing facility in

2015

the US 2) 51% stake in Indchemie Health Specialities

St. Louis

USFDA

US

and Cachet Pharma IPO and listing

Source: Company, Angel Research; Note: * Ankaleshwar facility was inspected by

Source: Company, Angel Research

USFDA authorities and received 3 observations on the facility. # Daman and Mandva

Facilities have received the Establishment Investigation Report from the USFDA.

January 3, 2017

2

Initiating coverage | Alkem Laboratories

Investment Rationale

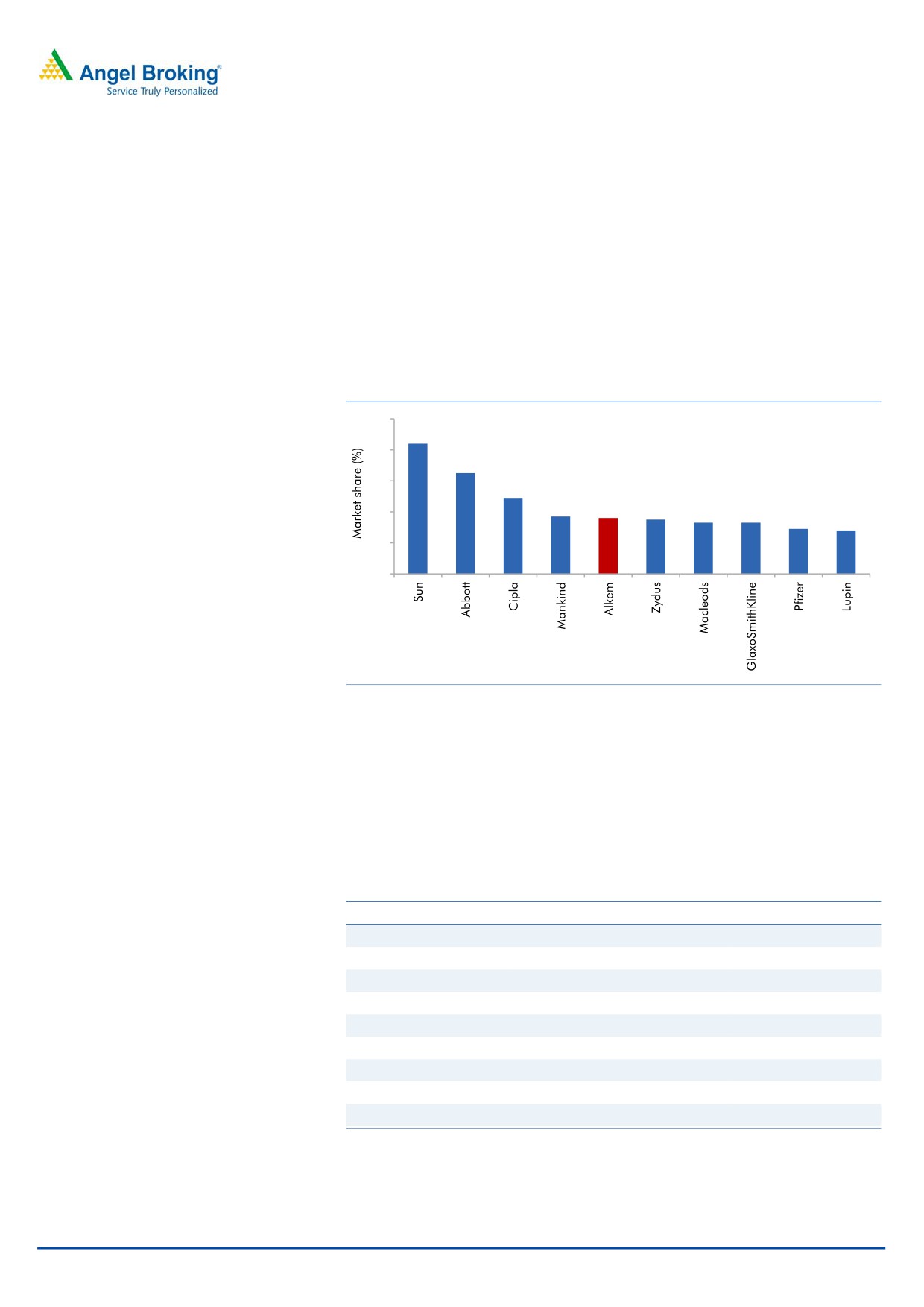

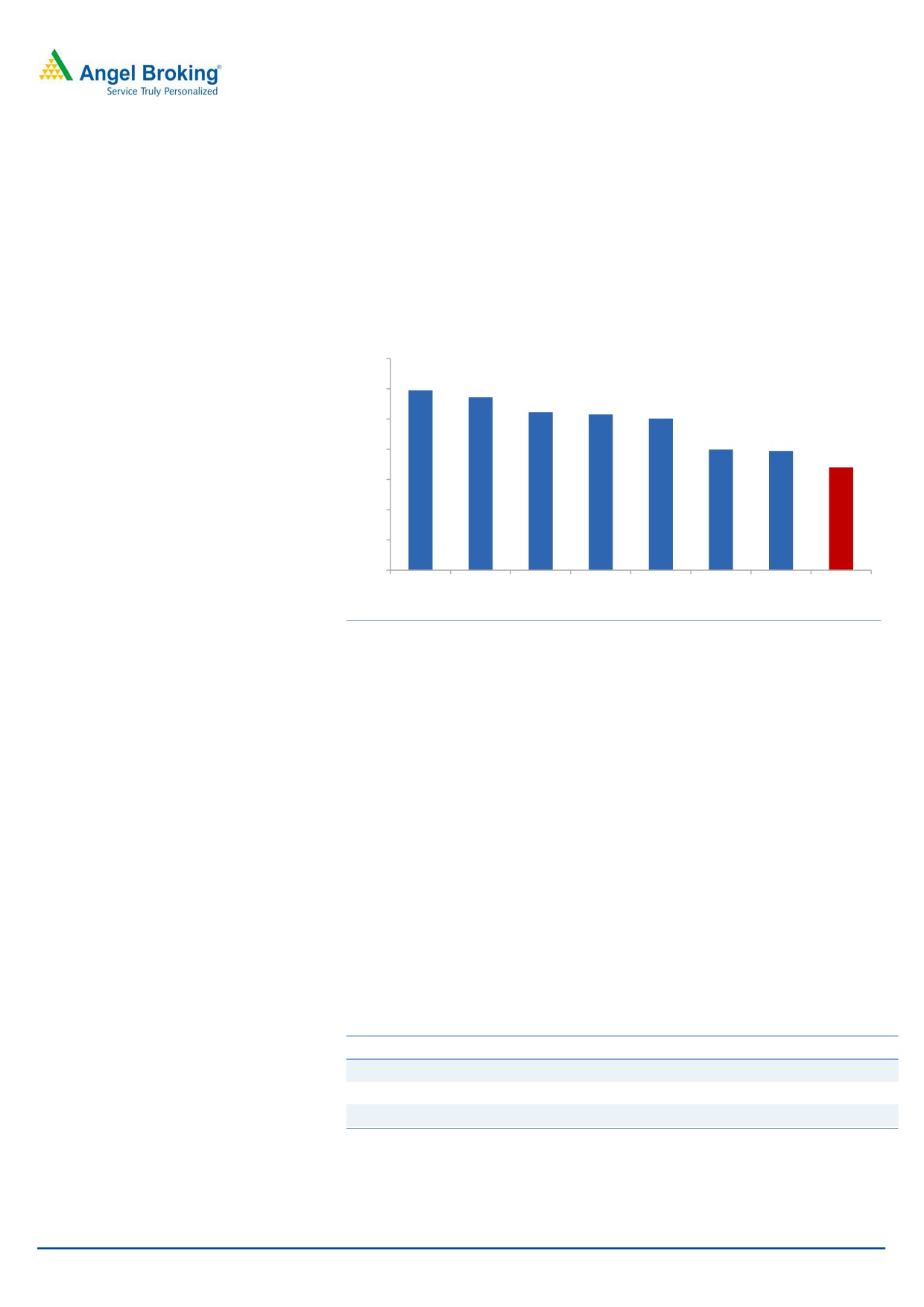

Strong player in domestic market: Alkem Laboratories is a 5th largest

pharmaceutical company in India in terms of domestic sales. The company in

FY16 recorded domestic revenue of `3,618cr and held market share of ~3.6%.

Alkem has a comprehensive portfolio of more than 800 brands, which covers all

major domestic therapeutic segments and in some of the segments, it is ranked in

top three market positions. It holds #1 position in Anti-infective segment and is

ranked #3 in Gastro-Intestinal and Pain/Analgesics segments. It also holds 7.9%

share of overall prescriptions in India.

Exhibit 5: Alkem is one of the top 5 domestic pharma players

10

8.4

8

6.5

6

4.9

3.7

3.6

3.5

4

3.3

3.3

2.9

2.8

2

0

Source: Company, Angel Research

The company has some mega brands such as Clavam, Taxim, Pan, Gemcal,

Ondem, Xone, Enzoflam, Taximax, etc., which are from various therapeutic

segments. 5 of its brands feature in top 50 brands in the Indian pharmaceutical

industry; while a total 14 brands feature in list of top 300 brands. The three brand

franchisees, namely Clavam, Pan and Taxim add ~`800cr in its domestic revenue

(~22% of annual domestic revenue), which shows strength of its mega brands.

Exhibit 6: Major brands and their sales in FY15

Brand name

Market share (%)

Sales in ` cr

Clavam

15.5

215

Taxim-O

19.7

151

Taxim

76.6

151

Pan

28.9

145

Pan-D

26.0

129

A to Z NS

4.4

73

Gemcal

12.7

69

Sumo

38.4

66

Xone

10.4

62

Source: Company, Angel Research

January 3, 2017

3

Initiating coverage | Alkem Laboratories

Significantly outperforming the domestic pharma market: Alkem, in last seven

years, has outperformed the domestic pharma industry due to 1) strong brand

strength 2) leadership position in key therapeutics segments 3) good relationships

with doctors and 4) effective execution of its sales strategy.

The company currently employs ~6000 Medical Representatives (MR) in India. Its

average net revenue per MR was `49lakh in FY15 but significantly improved to

`60lakh in FY16, which is now at par with the industry (~`55Lakh-`60Lakh per

MR). Over the last few years, the company has increased its field force aggressively

to improve its chronic business revenue where its sees strong business

opportunities.

Alkem has a strong sales network, which is supporting its strong performance in

the domestic markets. Besides 6,000 MRs, it also has 40 sales depots, 49 clearing

and forwarding agents, 19 consignees and eight central warehouses covering over

7,000 stockists. The company also tracks its stock in real time throughout

Pan-India, which also helps to ensure consistent supply of the drugs in the country.

Aided by this infrastructure, company has been outperforming the industry growth

by ~400-500bps over FY12-FY16. During this period, company reported a CAGR

of 20% in domestic revenue compared to industry growth of ~13%.

Exhibit 7: Market share in key segments FY16

Exhibit 8: CAGR of 20% from FY11-FY16

Segment

Industry size (` cr)

Market share (%)

Rank

4,000

Domestic business

27.8

30

Anti-infective

11,338

11.60

1

3,500

25

GI

9,679

5.70

3

3,000

20.0

18.6

16.8

20

Pain /analgesics

6,971

5.10

3

2,500

15.3

Vitamin/minerals

2,000

15

6,921

3.70

5

/nutrients

1,500

Gynecology

4,759

2.60

9

10

1,000

Respiratory

7,156

1.50

19

5

500

Neuro/CNS

5,366

1.90

13

0

0

Derma

5,952

1.50

15

FY11

FY12

FY13

FY14

FY15

FY16

Cardiac

10,304

0.60

31

Domestic sales (` cr)

Growth rate (%)

Source: Company, Angel Research

Source: Company, Angel Research

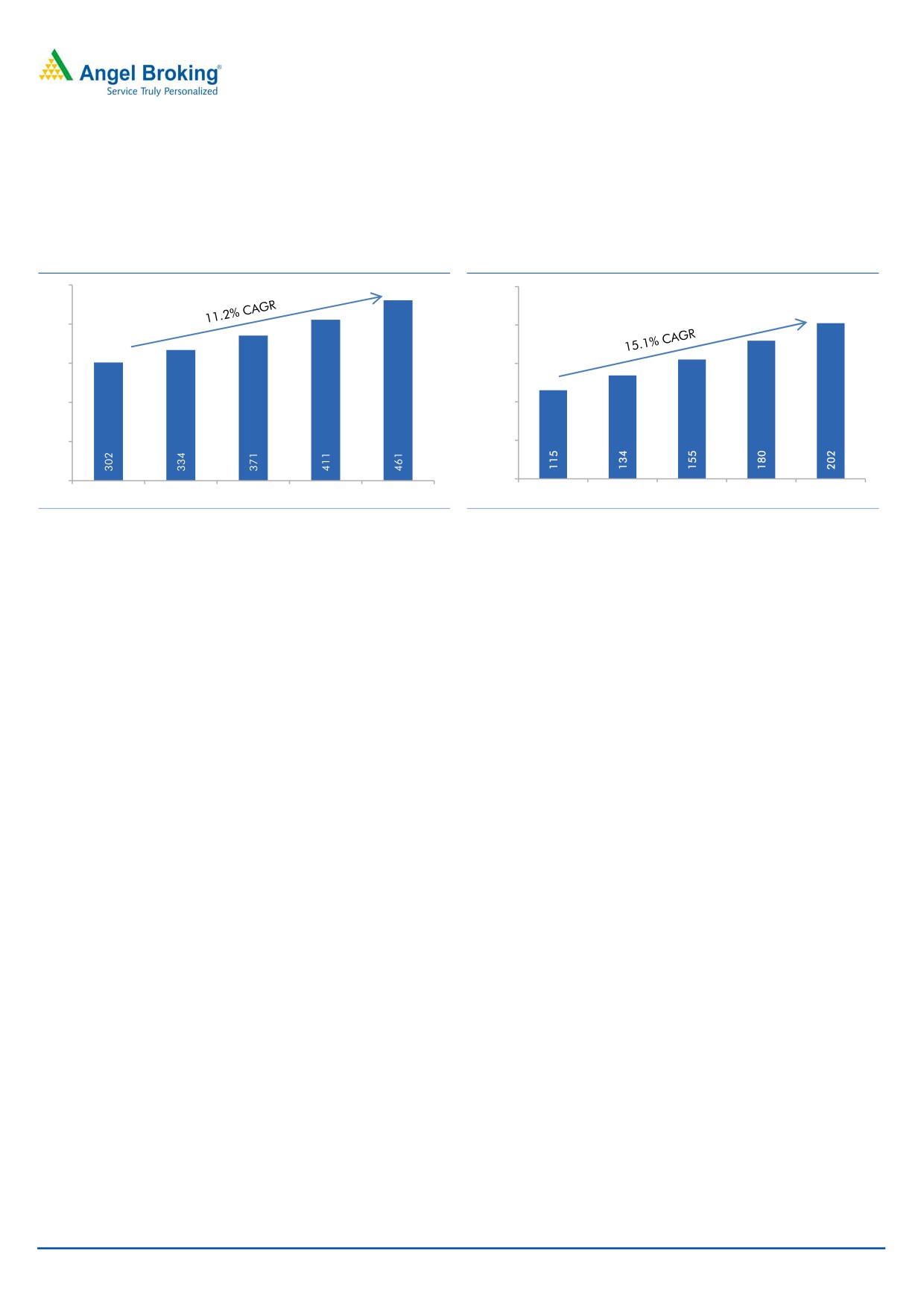

Chronic therapies to lead the industry growth: Currently the domestic formulations

industry is valued at ~`868billion, which has been growing at a compounded

annual growth rate of ~13% since 2012. The industry is expected to continue

growing at the same rate to reach ~`1,400billion in 2020, largely due to the

rising healthcare spending, increasing medical facilities, increasing penetration of

medical insurance, change in lifestyle, etc. This is going to drive the overall market

size of the pharmaceutical industry in India. The domestic formulation can be

further divided in two sub-segments i.e. Acute and Chronic.

1) Acute - The diseases which last for short duration with quicker onset such as

bacterial infections, injuries, flu, burns, etc.

2) Chronic - The diseases which last for long duration such as heart disease,

diabetes, stroke, cancer, HIV/AIDs, etc.

The acute segment has the highest share in the domestic formulations market

(~70%) and is growing at a rate of ~11%. The chronic segment (30% of the total

January 3, 2017

4

Initiating coverage | Alkem Laboratories

industry) is growing rapidly at 15% as the overall disease profile of the country is

moving towards the long duration diseases due to rapid change in the lifestyle of

people. Going forward, chronic segment is expected to exhibit high growth rate, whereas

acute segment is expected to hold the high market share and continue to grow.

Exhibit 9: Acute segment size (` bn) and growth (%)

Exhibit 10: Chronic segment size (`bn) and growth (%)

500

250.00

400

200.00

300

150.00

200

100.00

100

50.00

0

0.00

FY11

FY12

FY13

FY14

FY15

FY11

FY12

FY13

FY14

FY15

Source: Company, Angel Research

Source: Company, Angel Research

Growth drivers of domestic formulations are:

1) Acute - Greater awareness in patients, higher penetration of branded drugs,

increasing preference of patients to self medicate by using OTC brands,

volume growth as acute conditions are treated by mostly general practitioners,

etc.

2) Chronic - Overall increase in chronic conditions, growing investments in

specialty hospitals in tier II/tier III cities, coverage of chronic conditions by

insurers, increasing affordability of medicines and surgeries, launch of niche

and patented products, etc.

Alkem to benefit from investments in the chronic segment: Alkem is a market

leader in the acute segment from which it derives 88% of its domestic revenue. We

believe that the company by leveraging on its mega brands and relationships with

doctors is likely to continue growing its acute business revenues. We forecast

revenue CAGR of 15.7% from FY16-FY19E in the acute business segment.

While maintaining its leadership position in acute business, the company has

made sizable investments to grow its share in chronic business and has allocated

~25% of its field force (1,500 MRs) to cater to this segment. In our opinion

company has a long way to go in the chronic segment which contributes 12% of

domestic sales. The company realizing this is now focusing on growth of this

segment. Most of the current field force (MRs) has been hired from the leading

pharmaceutical players over the last three years. The productivity of these MRs is

expected to increase going ahead, which will increase the market share of the

company in the chronic segment.

January 3, 2017

5

Initiating coverage | Alkem Laboratories

Exhibit 11: Improving MR productivity

Exhibit 12: Domestic sales mix to change in near term

(` lakh)

100%

70.0

10%

11%

12%

13%

15%

60

60.0

80%

49

50.0

60%

40.0

90%

89%

88%

87%

40%

85%

30.0

20.0

20%

10.0

0%

0.0

FY2015

FY2016

FY2017E

FY2018E

FY2019E

FY2015

FY2016

Acute Chronic

Source: Company, Angel Research

Source: Company, Angel Research

Though there is competition in chronic segment from the MNC giants, we see that

Alkem, despite being a late entrant, has been able to garner some market share.

Its growth rate of ~20% in chronic segment is likely to help it gain more market

share in future.

NLEM impact offset by higher volumes: National List of Essential Medicines (NLEM)

includes list of essential drugs whose prices are to be controlled as per Drug

Pricing Control Order (DPCO). As per DPCO, the prices of each of the

formulations are determined based on the average of all drugs having an Indian

market share of more than 1% by value. In 1994, prices of 74 drugs were

controlled, which rose to 348 in 2013 and further to 376 in 2015. We believe that

NLEM uses WHO Essential Medicines List as a model and scope of including the

drugs is taken accordingly. In 2015, there were 414 drugs in the WHO EML list

and 376 drugs in NLEM list. We believe that NLEM in the next revision may include

more number of drugs.

Some of the Alkem’s drugs (Taxim O, Ondem, Cetriz, etc.) appear in the list of

NLEM. Overall, 30% of its portfolio is exposed to NLEM; however, the higher

volumes have largely offset the impact of NLEM on its business. In Q2FY17, the

impact was ~3%; while that in Q1FY2017 along with FDC ban, was ~4-5%.

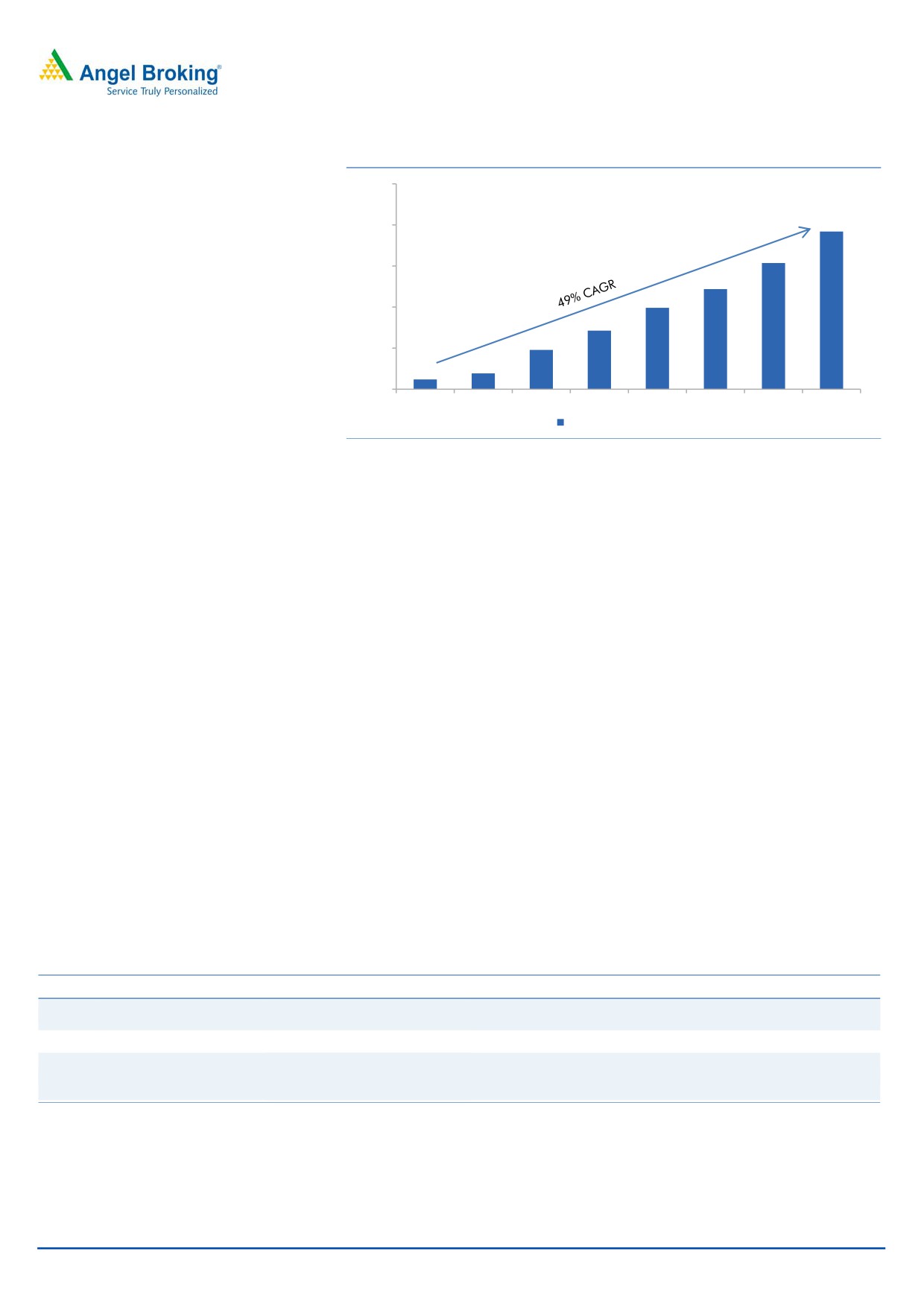

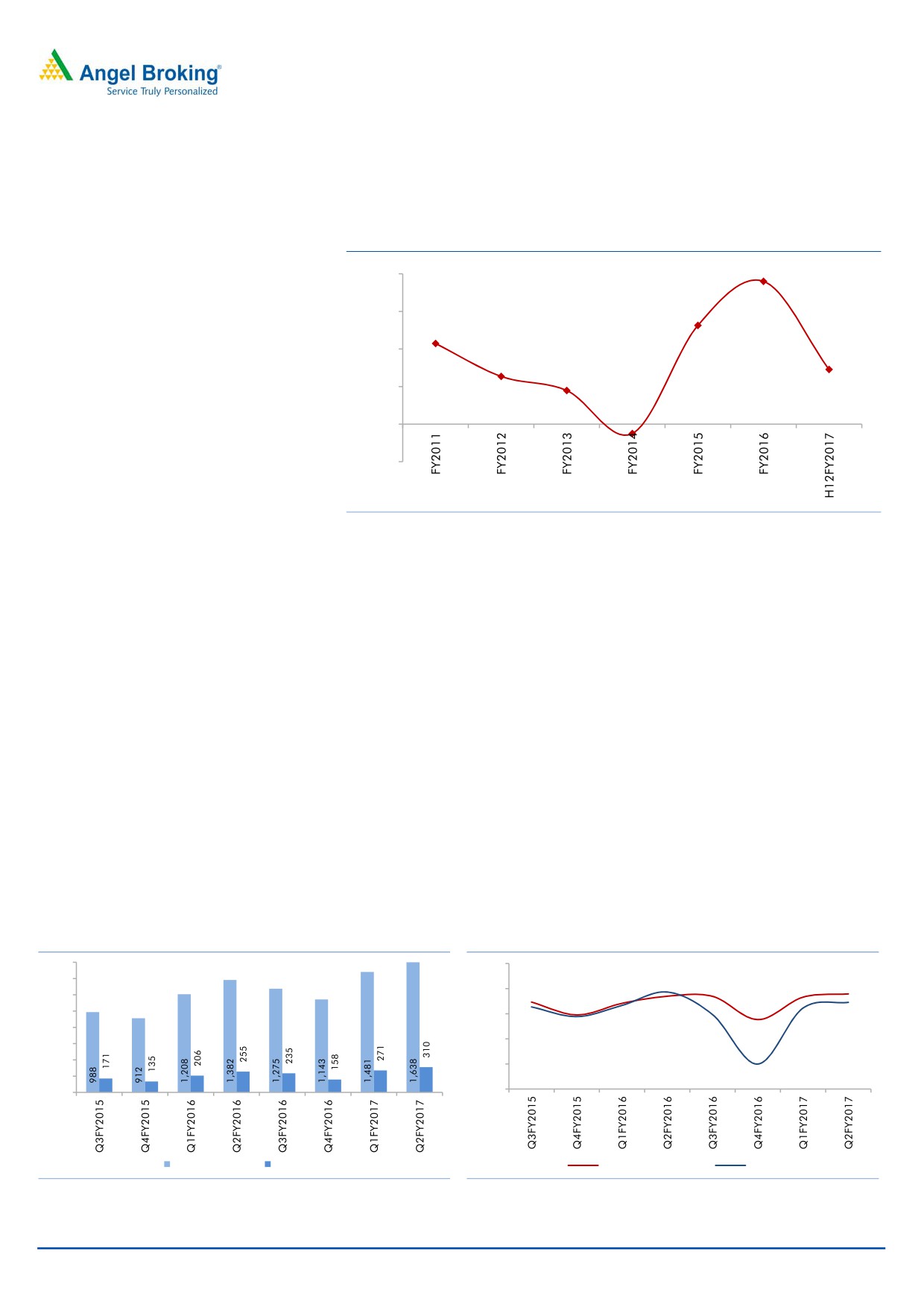

US- The key focus area despite late entry: Alkem is a late entrant in the US

market compared to top Indian pharma companies. Almost all big Indian pharma

companies entered the US market in early 2000s, and have shown a sustainable

growth rate in the mid term there. Alkem is also trying to achieve similar track

record in the US markets, despite lagging behind the bigger peers. It entered the

US market in FY10 and since then, it has grown its US business to `991cr in

FY2016. This works out to be 70% CAGR on the base of FY2012 revenue of

`118cr. The company markets its products through its marketing subsidiary,

Ascend Laboratories LLC.

January 3, 2017

6

Initiating coverage | Alkem Laboratories

Exhibit 13: Strong growth in US revenues

2,500

2,000

1,500

1,000

500

0

FY12

FY13

FY14

FY15

FY16

FY17E FY18E FY19E

US revenue (` cr)

Source: Company, Angel Research

This has been possible as the company utilized the opportunity presented by

acquisition of Ascend, which already had a portfolio of generic products and

established sales channels. It has further acquired two more businesses, which

improved its manufacturing and research abilities.

The Pharmanetwork LLC: This is a holding company of Ascend Laboratories

and was acquired in July 2010. This acquisition has given Alkem a launch pad

to commercialize its products in the United States. Ascend was established in

2003 and had its own generic portfolio and also had relationship with various

sales channels like wholesalers, distributors, food and grocery stores,

pharmaceutical retailers, etc. in the United States.

NORAC Inc: Acquired in December 2012, Norac is engaged in manufacturing

of specialty APIs and providing contract research and manufacturing services

(CRAMs).

Long Pharmaceuticals LLC: Acquired in June-2015 and is engaged in

formulations of semi-solids, liquids and nasals. This acquisition helps Alkem in

diversifying its manufacturing capabilities and also provides it with capacity to

produce formulations in semi-solids, liquid and nasals. The company is

scaling up the manufacturing capacity and R&D capabilities of this facility in

view to file niche ANDAs from there.

Exhibit 14: Alkem growing through acquisitions

Year

Company

Business description

Benefit to Alkem Laboratories

Acquisition helped to set-up a front end to commercialize its

Jul-10

The Pharmanetwork LLC

Portfolio of generic products

products in USA

Dec-12 NORAC Inc

APIs manufacturing and CRAMs Enhancing manufacturing and R&D capabilities

Semi-solids, liquid and nasal

Jun-15 Long Pharmaceuticals LLC

formulation manufacturing

Enhancing manufacturing capabilities

capabilities.

Source: Company, Angel Research

January 3, 2017

7

Initiating coverage | Alkem Laboratories

Well executed inorganic growth: The inorganic growth strategy has been adopted

by many Indian generic companies and Alkem is also travelling on the same path

to grow its US business. With three acquisitions in the US, Alkem now has

capabilities such as CRAMs, API manufacturing, formulations located in USA,

which will give the company scale and capability to launch new products. The

Ascend has given Alkem sales and marketing infrastructure for launching new

products through its sales channels. We believe that the company has well

executed the inorganic strategy so far.

From our interaction with the company, we understand that going ahead it may

look for inorganic growth opportunities, mostly in selected therapeutic segments

such as Oncology. In the pharma space, we have seen generic pharma companies

showing keen interest in oncology assets either by acquiring USFDA approved

oncology manufacturing facilities or increasing R&D efforts to increase pipeline of

oncology ANDAs. In our opinion, Alkem’s plan of possible foray in oncology is

positive in long term and it may further put them on a strong profitability path. An

acquisition at the right valuation in oncology space would be positive for the

company.

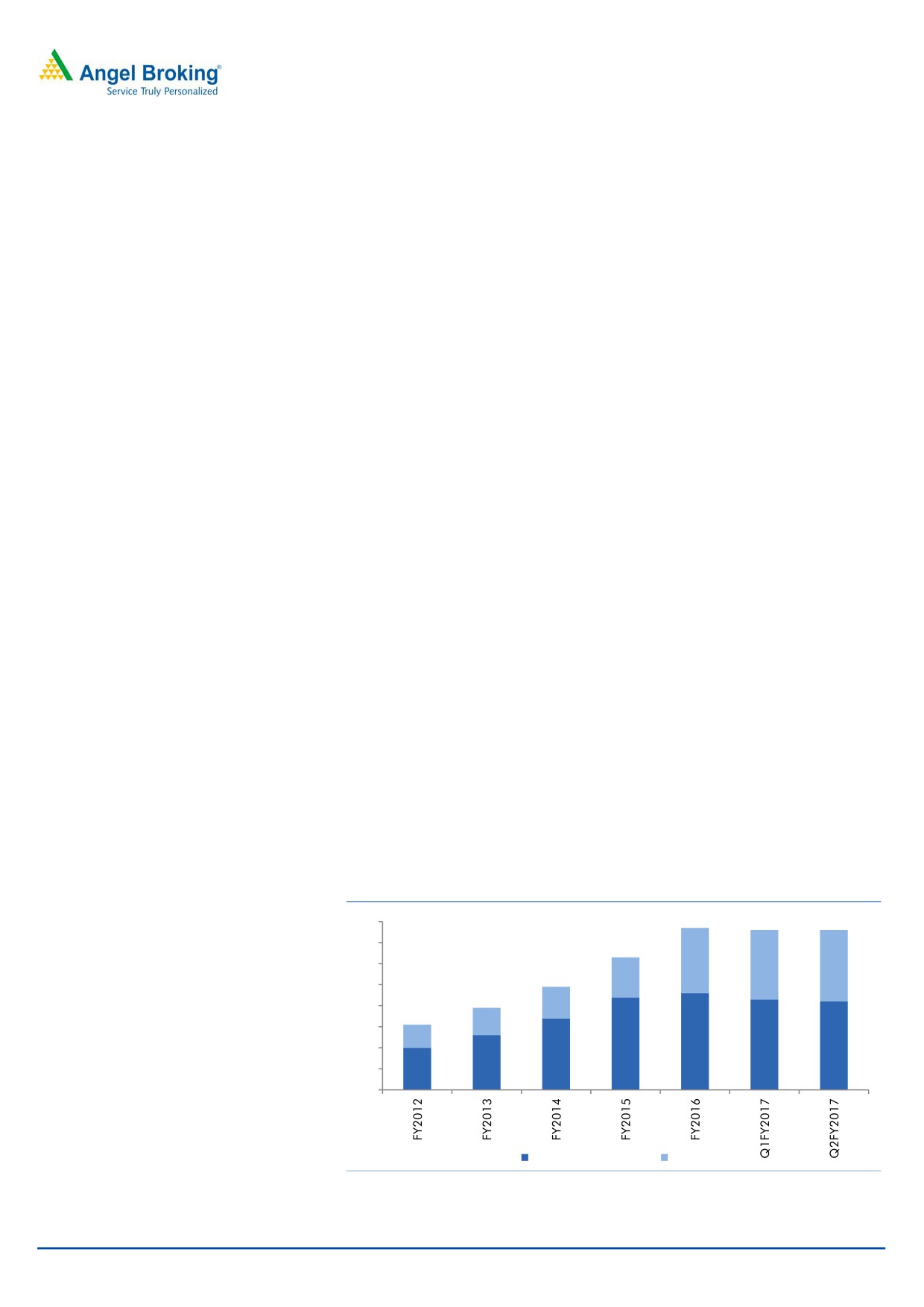

ANDA pipeline to gain momentum: In the USA, Alkem has filed total 76 ANDAs,

of which 34 have received final approval. As of March-2016, 30 of these 76

ANDAs are Para IV filings with limited competition, indicating a possible strong

revenue generating opportunity in mid-term. The company generates ~$6million

to $7million revenue from each ANDA.

Alkem expects increase in approval momentum with 2/3rd of its pipeline to get

approved in the next three years. Going ahead, the company expects to monetize

this ANDA pipeline by launching high single digit products (~8-9) in the US.

Assuming a launch of ~7 ANDAs each year going ahead and average revenue of

~$6million per ANDA, we believe that its existing pipeline is expected to generate

more than `850cr of incremental revenue taking its US revenue to ~`1,900cr in

FY2019E from `991cr in FY2016. The company has guided that US revenue

would double in the next three years ($300million by FY2019E), which would lead

to increase in US revenue pie from 6% in FY2012 to ~25% in FY2019E.

Exhibit 15: Alkem's ANDA pipeline

77

76

76

80

70

63

60

31

33

34

49

19

50

39

40

15

31

13

30

11

44

46

43

20

42

34

26

10

20

0

Pending approval

Approved

Source: Company, Angel Research

January 3, 2017

8

Initiating coverage | Alkem Laboratories

Resolve of USFDA issues at Daman, positive for the stock: Alkem’s Daman facility

received 13 observations in Sept-16 USFDA inspection. Daman facility contributes

<30% of the US sales, which works out to be ~5-6% of the total revenue. It also

has 50% of the pending ANDAs filed from this facility hence it is a critical for its

future US business plans.

Daman facility received Establishment Investigation Report (EIR) in December 2016

indicating that the USFDA has cleared the Daman facility. We see this as a positive

development for the company as a major hangover on its US business plans has

gone.

USFDA issues at Ankaleshwar facility not material for US business: Alkem’s

Ankaleshwar facility was audited by USFDA in December-2016 and has issued 3

observations. This is an API facility and there are no ANDAs filed from here. The

contribution of the drug which uses API from this facility is <1% hence there is

almost no impact of this facility on its US revenues, as per company.

Exhibit 16: Alkem - USFDA inspections

Facility

Scope

Inspection year Comment

Baddi

Formulation

2015

Successful completion

California - API Facility

API

2015

Successful completion

St. Louis

Formulation

2015

Successful completion

Mandva

API

2016

Establishment Investigation Reportreceived in March 2016

Daman

Formulation

2016

Establishment Investigation Reportreceived in December 2016

Ankaleshwar

API

2016

Form 483 - 3 observations

Source: Company, Angel Research

Other international business, currently not the focus area: Alkem derives

~7% revenue from four countries i.e. Australia, Chile, Kazakhstan and Philippines.

The company has said that it wants to have greater focus on the US market, which

is more attractive right now. It also does not intend to enter in more countries just

to be present in multiple geographies.

Exhibit 17: Low focus on other international business

500

12.0

10.2

9.2

10.0

400

7.1

7.7

8.0

6.4

300

6.0

200

4.0

100

2.0

144

255

287

244

383

0

0.0

FY2012

FY2013

FY2014

FY2015

FY2016

Intl business ex-US (` cr)

Contribution in total revenues (%)

Source: Company, Angel Research

January 3, 2017

9

Initiating coverage | Alkem Laboratories

Strong headroom for margin expansion: Alkem has been able to improve its

margin over the last few years, due to operating leverage and improving sales of

its brands. Most Indian pharma companies, who are in branded formulations in

India and exports market, have better EBITDA margin than Alkem. These

companies have benefitted due to their early entry in the US markets as well as

monetization of their ANDA pipeline. We believe that Alkem is also on the similar

path.

Exhibit 18: Headroom for margin expansion (Peer group FY16 margins)

35.0

29.8

28.6

30.0

26.1

25.8

25.1

25.0

20.0

19.7

20.0

17.0

15.0

10.0

5.0

0.0

Sun

Lupin

Cadila

Natco Dr Reddys Cipla Glenmark Alkem

Pharma

Health

Pharma

Lab

Source: Company, Angel Research

As Alkem launches more products in the US market, its profitability is likely to go

up. Currently, the company has significantly lower profitability of US business due

to higher R&D expenditure (~20% of US sales). Once it starts monetizing its ANDA

pipeline, profitability is likely go up as operating leverage will come in play. The

R&D expenses are not likely go up in the same proportion which will help to

improve its margins.

In the domestic market, company has already made significant investments to

create infrastructure for growth of its chronic segment. This investment is in terms

of expansion of its sales force which is likely to show strong productivity going

ahead. As chronic segment starts to show strong results, the same will be reflected

in its margin.

Tax rate to go up gradually: Alkem has been able to claim special tax benefits

at some of its manufacturing facilities. Overall, it has seen lower tax rate ranging

from 10% to 19% since FY2011.

Exhibit 19: Tax benefits to

Facility / Unit

Expiry of 100% Tax benefit

Baddi Betalactum

FY17 (30% tax deduction on profit till FY22)

Sikkim Kumrek

FY18

Sikkim Samardung Cephalsporin

FY23

Source: Company, Angel Research

The tax rate however is likely to go up gradually as 100% tax benefits on profit are

gradually ending at two of its facilities in next two years. In order to support

January 3, 2017

10

Initiating coverage | Alkem Laboratories

growing domestic business, Alkem has commenced construction of two new units

at Sikkim, which are also expected to derive tax benefits and so the company’s tax

rate is unlikely to go up drastically.

Exhibit 20: Low tax rate

20.0%

19.0%

15.0%

13.1%

10.7%

10.0%

7.3%

6.4%

5.0%

4.5%

0.0%

-1.2%

-5.0%

Source: Company, Angel Research

Alkem has guided of lower tax rate of 10-11% in FY2017E and the same may rise

going ahead, as it sees partial expiry of its tax benefits in its plants. Considering

this, we have taken tax rate of 17% in FY18E and FY19E.

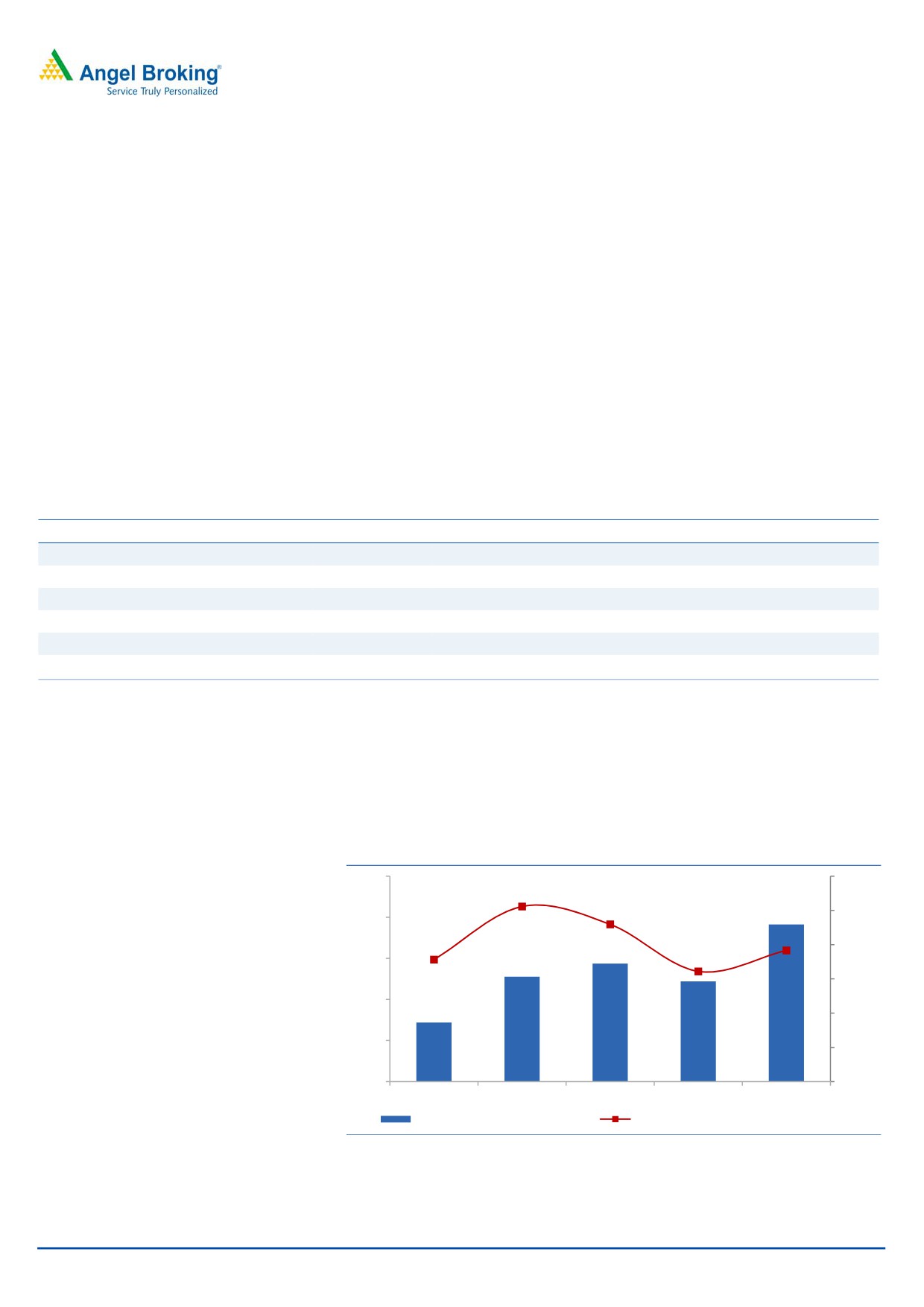

Recent financial performance: In Q2FY2017, the company reported total

revenue of `1638.4cr, showing a growth of 18.6% yoy. India sales grew by 18.4%

yoy due to strong performance in acute segment. The strong performance was

mainly due to the higher prevalence of Chikungunya and Dengue in India, which

helped overall industry, and Alkem specifically due to its leadership in the anti-

infective segment. In the chronic segment too, it did well by reporting higher rates

than industry in some therapeutic segments. Owing to its strong performance,

mainly in acute segment, the company reported market share of 3.82% in the

domestic market vs. 3.6% in FY2015. Exports grew by 19.7% yoy, mainly due to

strong growth in the US market, which grew by healthy 23.9% yoy.

EBITDA margin was at

18.95% vs.

18.31% in Q1FY2017 and

18.5% in

Q2FY2016, showed decent expansion. Net profit for the quarter was at `282.8cr,

showing yoy growth of 17.3%.

Exhibit 21: Quarterly revenue and EBITDA

Exhibit 22: Strong margin profile

1600

25.00

1400

20.00

1200

1000

15.00

800

10.00

600

400

5.00

200

0

0.00

Net sales (`cr)

EBITDA (`cr)

EBITDA margins (%)

Pat margins (%)

Source: Company, Angel Research

Source: Company, Angel Research

January 3, 2017

11

Initiating coverage | Alkem Laboratories

Outlook and Valuation

The stock at the CMP of `1,620 is available at P/E of 15.5x of FY19E EPS of `105,

which is at ~15% discount to average P/E (18.4x) of the peer group. In our view

this discount is unwarranted considering 1) Strong earnings momentum (CAGR of

22.3% in PAT from FY16-FY19E vs. CAGR of 18.3% from FY11-FY16),

2)

Improving RoE (average 21.5% RoE from FY17E-FY19E) and 3) Increasing ANDA

pipeline and near term launches in the US. We rate Alkem ‘Buy’ with a price target

of `1,989 (19.0x of FY19E earnings).

Risks to Our Estimates:

Alkem has received one USFDA observation at its Ankaleshwar API facility and

escalation of this in warning letter would be negative for the company.

Lower productivity of recently expanded sales force, mainly in chronic segment

can impact its plans to gain market share in chronic segment and would be

negative for the company.

Further decline/revision in the drugs included in NLEM may lead to have some

impact on Alkem’s domestic revenue.

Company has indicated of its inorganic growth plans in USA; however an

acquisition at high premium or that of a low margin business will impact its

future return ratios.

January 3, 2017

12

Initiating coverage | Alkem Laboratories

Income statement

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

FY19E

Total operating income

3,126

3,743

4,992

6,043

6,893

8,114

% chg

25.3

19.7

33.3

21.1

14.1

17.7

Total Expenditure

2,716

3,322

4,143

4,913

5,566

6,544

Cost of Materials

1,386

1,691

1,961

2,363

2,688

3,156

Personnel

532

646

917

1,039

1,155

1,359

Others Expenses

799

985

1,265

1,511

1,723

2,028

EBITDA

410

422

848

1,130

1,327

1,570

% chg

13.1

2.9

101.1

33.2

17.4

18.3

(% of Net Sales)

13.1

11.3

17.0

18.7

19.3

19.4

Depreciation& Amort.

52

71

101

110

130

155

EBIT

358

351

748

1,020

1,197

1,415

% chg

10.9

(1.9)

113.1

36.4

17.3

18.2

(% of Net Sales)

11.4

9.4

15.0

16.9

17.4

17.4

Interest & other Charges

93

81

67

47

47

47

Other Income

165

181

165

120

130

140

(% of PBT)

38.4

40.2

19.5

11.0

10.2

9.3

Share in profit of Ass.

-

-

-

-

-

-

Recurring PBT

430

451

845

1,093

1,280

1,508

% chg

7.1

4.8

87.5

29.4

17.1

17.8

Prior Period & Extra. Exp.

-

-

-

-

-

-

PBT (reported)

430

451

845

1,093

1,280

1,508

Tax

(5)

59

161

120

218

256

(% of PBT)

(1.2)

13.1

19.0

11.0

17.0

17.0

PAT (reported)

435

392

684

973

1,062

1,251

Add: Share of earnings of ass.

-

-

-

-

-

-

Less: Minority interest (MI)

-

-

11

-

-

-

PAT after MI (reported)

435

392

673

973

1,062

1,251

ADJ. PAT

435

392

673

973

1,062

1,251

% chg

13.5

(10.0)

74.8

42.1

9.2

17.8

(% of Net Sales)

13.9

10.5

13.5

16.1

15.4

15.4

Basic EPS (`)

364.0

32.8

56.3

81.4

88.8

104.7

Fully Diluted EPS (`)

364.0

32.8

56.3

81.4

88.8

104.7

% chg

13.5

(10.0)

74.8

42.1

9.2

17.8

January 3, 2017

13

Initiating coverage | Alkem Laboratories

Balance sheet

Y/E March (` cr)

FY14

FY15

FY16

FY17E FY18E FY19E

SOURCES OF FUNDS

Equity Share Capital

12

24

24

24

24

24

Reserves& Surplus

2,567

2,975

3,479

4,257

5,054

5,930

Shareholders’ Funds

2,579

2,999

3,503

4,281

5,078

5,954

Minority Interest

-

86

97

97

97

97

Total Loans

1,184

1,381

739

750

750

750

Deferred Tax Liability

78

126

153

153

153

153

Total Liabilities

3,841

4,591

4,490

5,280

6,077

6,953

APPLICATION OF FUNDS

Gross Block

1,170

1,745

1,889

2,389

2,739

3,089

Less: Acc. Depreciation

-

371

447

557

687

842

Net Block

1,170

1,374

1,442

1,832

2,052

2,247

Capital Work-in-Progress

-

111

172

250

300

300

Investments

588

481

422

422

422

422

Current Assets

2,553

3,325

3,394

3,941

4,640

5,562

Inventories

620

784

909

1,109

1,265

1,489

Sundry Debtors

367

527

565

662

755

889

Cash

206

791

796

670

910

1,172

Loans & Advances

159

175

240

290

331

389

Other Assets

1,201

1,048

884

1,209

1,379

1,623

Current liabilities

509

733

998

1,222

1,395

1,636

Net Current Assets

2,044

2,592

2,396

2,718

3,245

3,926

Deferred Tax Asset

39

34

58

58

58

58

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

3,841

4,591

4,490

5,280

6,077

6,953

January 3, 2017

14

Initiating coverage | Alkem Laboratories

Cash flow statement

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

FY19E

Profit before tax

430

451

845

1,093

1,280

1,508

Depreciation

52

71

101

110

130

155

Change in Working Capital

(36)

(12)

14

(448)

(287)

(419)

Interest / Dividend (Net)

(56)

(53)

(59)

47

47

47

Direct taxes paid

(111)

(106)

(198)

(120)

(218)

(256)

Others

11

(26)

24

-

-

-

Cash Flow from Operations

290

325

726

681

952

1,035

(Inc.)/ Dec. in Fixed Assets

353

(235)

189

(578)

(400)

(350)

(Inc.)/ Dec. in Investments

-

-

-

-

-

-

Cash Flow from Investing

353

(235)

189

(578)

(400)

(350)

Issue of Equity

-

-

-

-

-

-

Inc./(Dec.) in loans

(473)

87

(671)

11

-

-

Dividend Paid (Incl. Tax)

(32)

(57)

(185)

(195)

(266)

(375)

Interest / Dividend (Net)

11

569

598

(47)

(47)

(47)

Cash Flow from Financing

(494)

599

(258)

(230)

(313)

(423)

Inc./(Dec.) in Cash

149

690

657

(126)

239

262

Opening Cash balances

57

101

140

796

670

910

Closing Cash balances

206

791

796

670

910

1,172

January 3, 2017

15

Initiating coverage | Alkem Laboratories

Key Ratios

Y/E March

FY14

FY15

FY16

FY17E

FY18E

FY19E

Valuation Ratio (x)

P/E (on FDEPS)

4.5

49.5

28.8

19.9

18.2

15.5

P/CEPS

4.6

4.0

41.9

24.7

17.9

16.2

P/BV

0.8

6.5

5.5

4.5

3.8

3.3

Dividend yield (%)

2.7

1.6

0.3

1.0

1.0

1.4

EV/Sales

6.3

5.2

3.8

3.1

2.7

2.3

EV/EBITDA

48.2

46.2

22.3

16.8

14.2

11.8

EV / Total Assets

4.5

3.7

3.4

2.9

2.5

2.2

Per Share Data (`)

EPS (Basic)

364.0

32.8

56.3

81.4

88.8

104.7

EPS (fully diluted)

364.0

32.8

56.3

81.4

88.8

104.7

Cash EPS

354.0

407.7

38.7

65.7

90.6

99.7

DPS

43.2

26.6

4.7

15.4

16.3

22.2

Book Value

2,156.6

250.9

293.0

358.1

424.7

498.0

Dupont Analysis

EBIT margin

11.4

9.4

15.0

16.9

17.4

17.4

Tax retention ratio

1.0

0.9

0.8

0.9

0.8

0.8

Asset turnover (x)

1.1

1.2

1.7

1.5

1.5

1.6

ROIC (Post-tax)

12.2

9.8

20.0

23.0

22.1

23.0

Cost of Debt (Post Tax)

0.1

0.1

0.1

0.1

0.1

0.1

Leverage (x)

0.2

0.0

(0.1)

(0.1)

(0.1)

(0.1)

Operating ROE

14.0

10.2

17.3

21.2

19.6

19.7

Returns (%)

ROCE

9.5

8.0

17.6

20.3

20.5

21.1

Angel ROIC (Pre-tax)

12.1

11.3

24.7

25.9

26.6

27.7

ROE

16.9

13.1

19.2

22.7

20.9

21.0

Turnover ratios (x)

Asset Turnover (Gross Block)

2.7

2.1

2.6

2.5

2.5

2.6

Inventory / Sales (days)

72

76

67

67

67

67

Receivables (days)

43

51

41

40

40

40

Payables (days)

36

45

42

42

42

42

WC cycle (ex-cash) (days)

80

82

65

65

65

65

January 3, 2017

16

Initiating coverage | Alkem Laboratories

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Alkem Laboratories

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

January 3, 2017

17