3QFY2016 Result Update | Pharmaceutical

February 2, 2016

Alembic Pharma

NEUTRAL

CMP

`618

Performance Highlights

Target Price

-

Y/E March (` cr)

3QFY2016 2QFY2016

% chg (qoq) 3QFY2015

% chg (yoy)

Investment Period

-

Net Sales

921

1008

(8.6)

507

81.8

Other Income

4

1

262.9

1

266.7

Stock Info

Operating Profit

384

375

2.3

102

276.3

Interest

1

1

42.5

1

42.5

Sector

Pharmaceutical

Net Profit

269

289

(6.7)

71

281.4

Market Cap (` cr)

11,645

Source: Company, Angel Research

Net Debt (` cr)

814

Alembic Pharmaceuticals (Alembic Pharma) posted better-than-expected results

Beta

0.8

for 3QFY2016. It posted an 81.8% yoy growth in sales for the quarter to `921cr

52 Week High / Low

792/382

V/s `507cr in 3QFY2015 (and V/s an expected `700cr). Sales growth was mainly

Avg. Daily Volume

33,825

driven by the international business, which posted a 248% yoy growth, while the

Face Value (`)

2

Indian branded formulation business posted a 15% yoy growth. Consequently, on

BSE Sensex

24,871

the operating front, the EBITDA margin came in at 41.7% V/s 20.1% in

3QFY2015 (and V/s an expected 27.5%). The same was aided by gross margin

Nifty

7,564

expansion, which came in at

77.6% V/s

65.6% in 3QFY2015. The R&D

Reuters Code

ALEM.BO

expenditure during the quarter was 7.6% of sales V/s 6.0% of sales in 3QFY2015.

Bloomberg Code

ALPM@IN

Thus, the PAT came in at `269cr V/s `71cr in 3QFY2015 (and V/s an expected

`160cr), a yoy growth of 281.4%. We maintain our Neutral rating on the stock

considering fuller valuations.

Shareholding Pattern (%)

Promoters

74.1

Results better than expectations: Alembic Pharma posted better-than-expected

MF / Banks / Indian Fls

8.1

results for 3QFY2016. It posted an 81.8% yoy growth in sales for the quarter to

`921cr V/s `507cr in 3QFY2015 (and V/s an expected `700cr). Sales growth was

FII / NRIs / OCBs

4.5

mainly driven by the international business, which posted a 248% yoy growth,

Indian Public / Others

13.3

while the Indian branded formulation business posted a 15% yoy growth.

Consequently, on the operating front, the EBITDA margin came in at 41.7% V/s

20.1% in 3QFY2015 (and V/s an expected 27.5%). The same was aided by gross

Abs. (%)

3m 1yr

3yr

margin expansion, which came in at 77.6% V/s 65.6% in 3QFY2015. The R&D

Sensex

(7.3)

(16.2)

24.4

expenditure during the quarter was 7.6% of sales V/s 6.0% of sales in 3QFY2015.

Alembic Pharma

(9.1)

28.9

708.0

Thus, the PAT came in at `269cr V/s `71cr in 3QFY2015 (and V/s an expected

`160cr), a yoy growth of 281.4%.

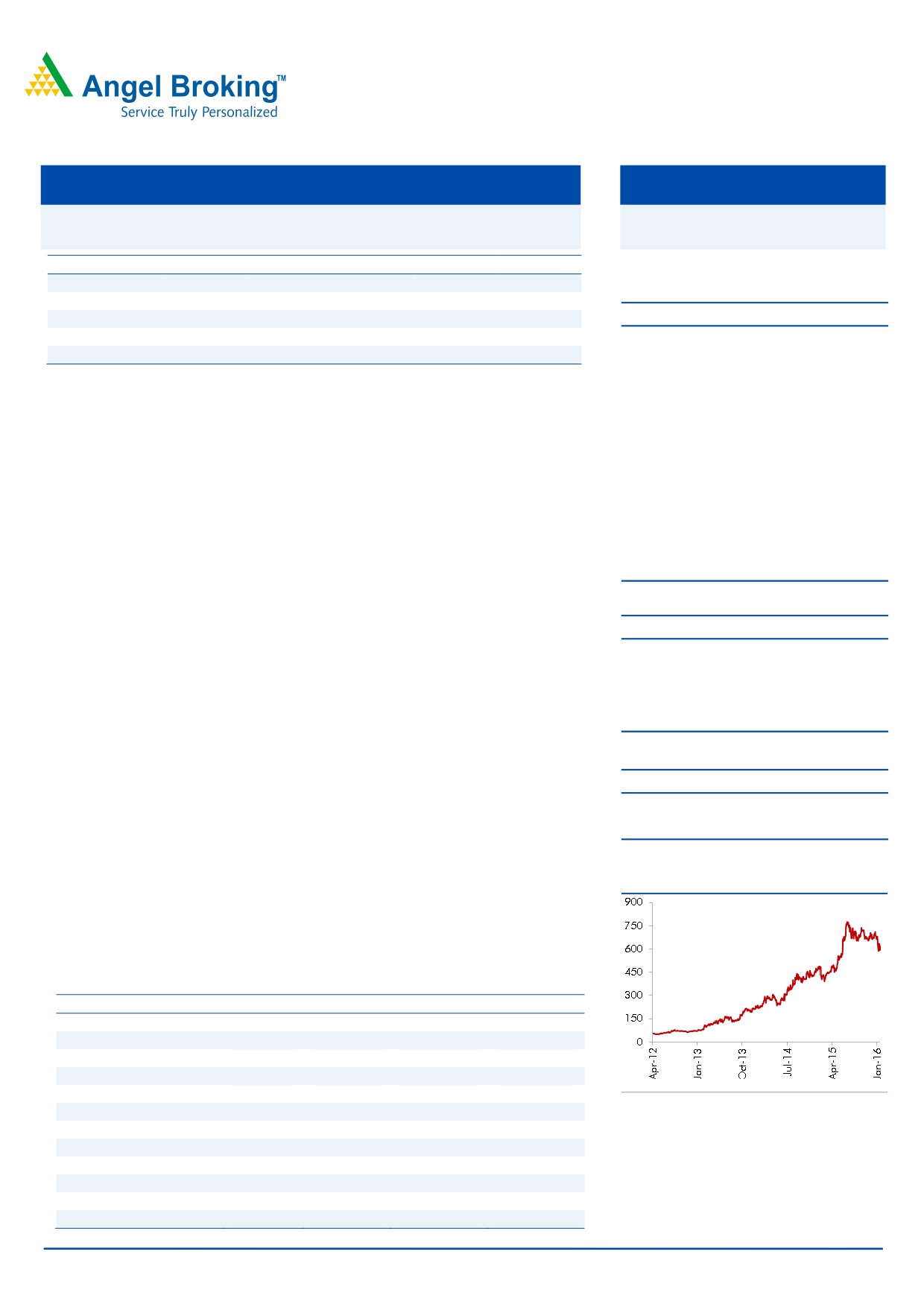

3-year price chart

Outlook and valuation: Alembic Pharma’s growth and profitability profile has

improved post the restructuring carried out by the Management. Over

FY2015-17E, we expect the company to post a CAGR of 36.1% and 38.2% in

sales and net profit, respectively. We recommend a Neutral rating on the stock.

Key Financials (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

Net Sales

1,863

2,053

3,274

3,802

% chg

22.9

10.2

59.5

16.1

Net Profit

236

283

660

541

% chg

43.0

20.0

133.0

(18.0)

EPS (`)

12.5

15.0

35.0

28.7

Source: Company, Angel Research

EBITDA Margin (%)

19.2

19.5

26.9

19.4

P/E (x)

49.4

41.1

17.7

21.5

RoE (%)

40.0

36.3

55.6

31.2

RoCE (%)

39.9

30.2

49.3

31.3

P/BV (x)

17.2

13.2

7.8

5.9

Sarabjit Kour Nangra

EV/Sales (x)

6.3

5.7

3.5

3.0

+91- 22- 36357600 - 6806

EV/EBITDA (x)

32.7

29.4

13.0

15.3

Source: Company, Angel Research; Note: CMP as of January 29, 2016

Please refer to important disclosures at the end of this report

1

Alembic Pharma | 3QFY2016 Result Update

Exhibit 1: 3QFY2016 performance (Consolidated)

Y/E March (` cr)

3QFY2016

2QFY2016

% chg(qoq) 3QFY2015

% chg (yoy) 9MFY2016 9MFY2015

% chg (yoy)

Net sales

921

1,008

(8.6)

507

81.8

2,511

1,551

61.9

Other income

4

1

262.9

1

266.7

5

3

82.0

Total income

925

1,009

508

82.1

2,517

1,554

Gross profit

715

782

(8.5)

332

115.1

1866

1010

84.7

Gross margin

77.6

77.5

65.6

74.3

65.1

Operating profit

384

375

2.3

102

276.3

860

303

183.9

Operating margin (%)

41.7

37.2

20.1

34.3

19.5

Interest

1

1

42.5

1

42.5

2

1

138.0

Depreciation

22

13

63.1

12

81.9

48

33

44.9

PBT

365

362

0.7

90

303.7

815

271

200.9

Provision for taxation

95

74

29.3

19

392.1

187

58

223.1

PAT before Extra-ordinary item

269

289

(6.7)

71

281.4

628

213

195.5

Extra-Ordinary Expenses

0

0

0

0

0

PAT after Extra-ordinary item & MI

269

289

(6.7)

71

281.4

628

213

195.5

EPS (`)

14.3

15.3

3.7

33.3

11.3

Source: Company, Angel Research

Exhibit 2: 3QFY2016 - Actual vs Angel estimates

` cr

Actual

Estimates

Variation (%)

Net Sales

921

700

31.6

Other Income

4

1

266.7

Operating Profit

384

191

100.7

Interest

1

1

42.5

Tax

95

19

392.1

Net Profit

269

160

67.8

Source: Company, Angel Research

Sales much above our expectations: The company posted better-than-expected

results for 3QFY2016. It posted an 81.8% yoy growth in sales to `921cr V/s

`507cr in 3QFY2015 and V/s an expected `700cr.

Sales growth was mainly driven by the international business, which posted a

248% yoy growth, while the Indian branded formulation business posted a

15% yoy growth. However the Indian generic business posted a 40% yoy dip in

sales. Overall, formulations accounted for 86% of sales V/s 78% in 3QFY2015.

APIs on the other hand posted a yoy growth of 24%.

In the Indian market, for 9MFY2016, the acute segment constituted ~40% of

domestic sales while the chronic segment accounted for the remaining. The

international generic segment posted growth, mainly on back of gAbilify.

The current ANDA filings are at 74 including 29 pending approvals, of which,

~50% are Para IV and shared exclusivity filings.

February 2, 2016

2

Alembic Pharma | 3QFY2016 Result Update

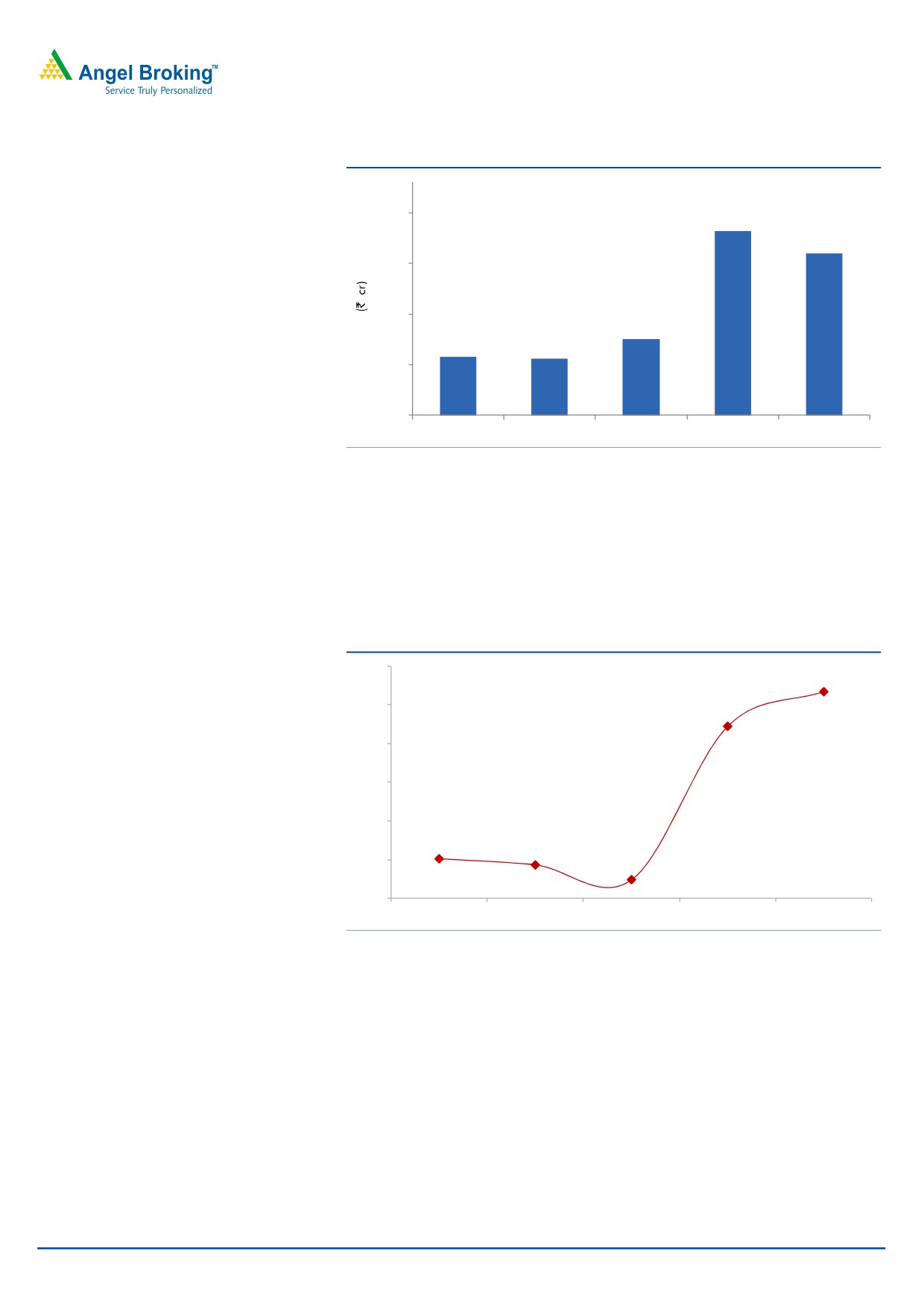

Exhibit 3: Sales trend

1,080

1,008

921

880

680

582

511

502

480

280

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

Source: Company, Angel Research

OPM better than expectation: Consequently, on the operating front, the EBITDA

margin came in at 41.7% V/s 20.1% in 3QFY2015 (V/s 27.5% expected), aided by

gross margins of 77.6% V/s 65.6% in 3QFY2015. The R&D expenditure during the

quarter was 7.6% of sales V/s 6.0% of sales in 3QFY2015. Going ahead, the

Management expects R&D expenses to stabilize at 8% of sales due to increased

complexity of filings.

Exhibit 4: OPM Trend (%)

45.0

41.7

40.0

37.2

35.0

30.0

25.0

20.1

19.3

20.0

17.4

15.0

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

Source: Company, Angel Research

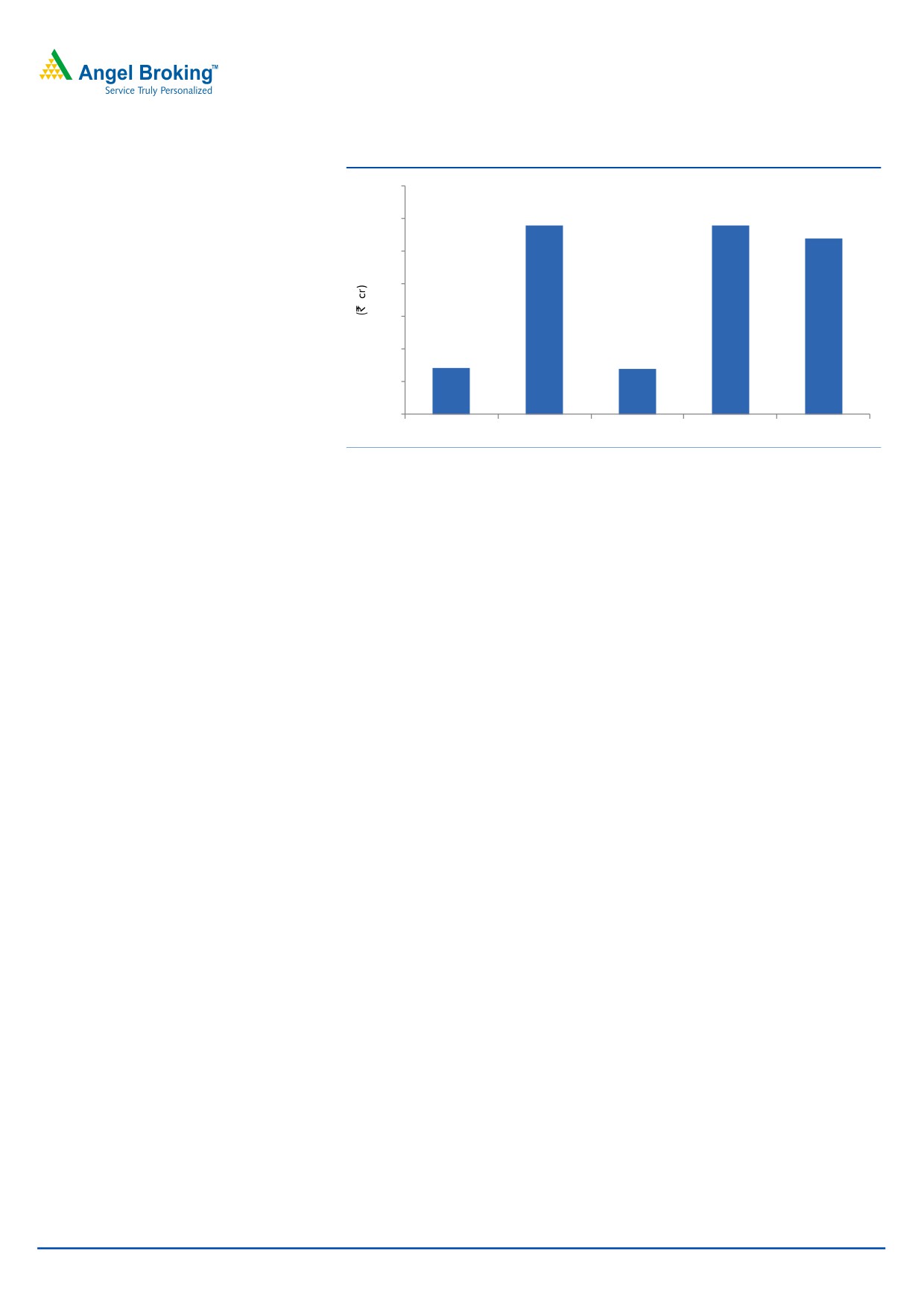

Net profit above expectation: Thus, the PAT came in at `270cr V/s `71cr in

3QFY2015 (and V/s an expected `160cr), a yoy growth of 281%.

February 2, 2016

3

Alembic Pharma | 3QFY2016 Result Update

Exhibit 5: Net profit trend

350

289

289

300

269

250

200

150

71

100

70

50

0

3QFY2015

4QFY2015

1QFY2016

2QFY2016

3QFY2016

Source: Company, Angel Research

Concall highlights

US sales for gAbilify during the quarter pertain to July-September sales as the

amount was received from the partner in 3QFY2016. As per the

Management, the partner has regained lost market share of gAbilify to some

extent during the quarter amid increased competition. Ex-gAbilify also, US

sales registered yoy growth.

USFDA audits were conducted in September and May

2015 for the

formulation and API plants, respectively. The other two API facilities are

expecting USFDA inspections in the near future.

The company has guided for ~8% R&D spend for FY2016. of the total R&D

expenses

80-85% are expected to be spent for generic formulations

(injectables & dermatology).

The company has given a capex guidance of `280-300cr for FY2016, of

which `200cr of capex has already been expended till 3QFY2016.

The company has maintained its guidance of 30-35% base business growth in

international sales.

Investment arguments

Focus on chronic segment to drive domestic formulation growth: Alembic Pharma

has been restructuring its business portfolio, which would aid in improving its

growth and operating performance. The company’s domestic formulation business

contributed 52% to its total sales in FY2015. The company has a strong field force

of ~3,600 medical representatives. Going forward, the company expects its

domestic formulation business to at least grow in line with the industry growth rate,

before it sees an improvement in the share of the high growth chronic segment.

For FY2015-17E, we expect the domestic formulation business to grow at a CAGR

of 13.0%.

Exports- US the key growth driver: On the exports front, the formulation business

contributed 31% to the total turnover, with majority of the contribution coming

from Europe and the US. In the US, the company has filed for ~70 ANDAs till date

February 2, 2016

4

Alembic Pharma | 3QFY2016 Result Update

and received 44 approvals. The company, going forward, expects to keep its

momentum high in terms of number of filings, by filing around 10-12 ANDAs per

annum. For FY2015-17E, we expect exports to register a CAGR of 95.5%.

Outlook and valuation: Alembic Pharma’s growth and profitability profile has

improved post the restructuring carried out by the Management. Over FY2015-17,

we expect the company to post a CAGR of 36.1% and 38.2% in sales and

net profit, respectively. We recommend a Neutral on the stock, owing to fuller

valuations.

Exhibit 6: Key assumptions

FY2016E

FY2017E

Domestic formulation sales growth (%)

10.0

16.0

Exports sales growth (%)

227.0

17.0

R&D as % of sales

8.0

8.0

Operating margins (%)

26.9

19.4

Capex (` cr)

200

200

Net Debt/Equity (x)

(0.0)

(0.2)

Source: Company, Angel Research

Exhibit 7: Recommendation summary

Reco.

CMP Tgt Price Upside

FY2017E

FY15-17E

FY2017E

(`)

(`)

(%) PE (x) EV/Sales (x) EV/EBITDA (x)

CAGR in EPS (%) RoCE (%) RoE (%)

Alembic Pharma

Neutral

618

-

-

21.5

3.0

15.3

38.2

31.3

31.2

Aurobindo Pharma Neutral

833

-

-

19.5

3.1

13.5

15.6

23.5

30.2

Cadila Healthcare

Buy

305

352

15.5

17.3

2.6

11.8

24.6

25.2

29.0

Cipla

Accumulate

586

636

8.6

20.3

2.8

14.5

21.4

17.1

16.8

Dr Reddy's

Buy

3,104

3,933

26.7

17.4

2.6

11.2

17.2

19.1

20.4

Dishman Pharma

Neutral

331

-

-

16.6

1.8

8.2

15.9

9.5

11.2

GSK Pharma*

Neutral

3,224

-

-

47.2

8.2

37.3

6.6

33.7

34.3

Indoco Remedies

Neutral

323

-

-

23.8

2.6

14.1

23.0

19.7

19.7

Ipca labs

Buy

669

900

34.6

23.9

2.4

12.9

17.9

11.8

14.0

Lupin

Neutral

1,710

-

-

25.0

4.3

15.9

13.1

29.6

24.7

Sanofi India*

Neutral

4,242

-

-

28.0

3.6

17.4

33.1

27.9

25.5

Sun Pharma

Accumulate

873

950

8.8

32.5

5.8

18.8

8.4

15.8

16.6

Source: Company, Angel Research; Note: *December year end

Company Background

Alembic Pharma is a leading pharmaceutical company in India. The company is

vertically integrated to develop pharmaceutical substances and intermediates. The

company is a market leader in the Macrolides segment of anti-infective drugs in

India. Its manufacturing facilities are located in Vadodara and in Baddi (Himachal

Pradesh; for the domestic and non-regulated export market). The Panelav facility

houses API and formulation manufacturing plants (both USFDA approved).

February 2, 2016

5

Alembic Pharma | 3QFY2016 Result Update

Profit & Loss Statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014E

FY2015E

FY2016E

FY2017E

Gross sales

1,526

1,871

2,064

3,294

3,825

Less: Excise duty

10

8

11

20

23

Net sales

1,516

1,863

2,053

3,274

3,802

Other operating income

3.1

3.2

5.7

2.0

2.0

Total operating income

1,519

1,866

2,058

3,276

3,804

% chg

4.0

22.8

10.3

59.2

16.1

Total expenditure

1,267

1,506

1,653

2,393

3,066

Net raw materials

681

713

715

1,149

1,483

Other mfg costs

67

82

90

144

167

Personnel

194

247

307

380

472

Other

326

463

542

720

945

EBITDA

249

358

400

881

736

% chg

22.5

43.7

11.7

120.5

(16.5)

(% of Net Sales)

16.4

19.2

19.5

26.9

19.4

Depreciation& amortisation

35

40

44

47

53

Interest & other charges

15

10

2

16

12

Other income

4

0

0

-

-

(% of PBT)

2

0

0

-

-

Share in profit of Associates

-

-

-

-

-

Recurring PBT

206

308

360

819

671

% chg

28.0

49.4

16.8

127.7

(18.0)

Extraordinary expense/(Inc.)

-

-

-

-

-

PBT (reported)

206

308

360

819

671

Tax

41

75

76

159

130

(% of PBT)

19.9

24.4

21.2

19.4

19.4

PAT (reported)

165

236

283

660

541

Add: Share of earnings of asso.

-

-

-

-

-

Less: Minority interest (MI)

-

-

-

-

-

Prior period items

-

-

-

-

-

PAT after MI (reported)

165

236

283

660

541

ADJ. PAT

165

236

283

660

541

% chg

26.7

43.0

20.0

133.0

(18.0)

(% of Net Sales)

10.9

12.7

13.8

20.2

14.2

Basic EPS (`)

8.8

12.5

15.0

35.0

28.7

Fully Diluted EPS (`)

8.8

12.5

15.0

35.0

28.7

% chg

26.7

43.0

20.0

133.0

(18.0)

February 2, 2016

6

Alembic Pharma | 3QFY2016 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

SOURCES OF FUNDS

Equity share capital

37.7

37.7

37.7

37.7

37.7

Preference Capital

-

-

-

-

-

Reserves & surplus

465

638

847

1,452

1,939

Shareholders funds

503

676

885

1,490

1,976

Minority Interest

Other Long Term Liabilities

12.8

12.7

15.8

14.3

14.3

Long Term Provisions

6.1

6.7

6.4

7.4

7.4

Total loans

187

78

239

150

150

Deferred tax liability

14

23

31

31

31

Total liabilities

722

795

1,177

1,693

2,179

APPLICATION OF FUNDS

Gross block

572

665

907

1,107

1,307

Less: acc. depreciation

228

268

313

359

412

Net block

344

397

595

748

895

Capital work-in-progress

32

21

35

35

35

Goodwill

Long Term Loans and Adv.

36

42

118

118

118

Investments

3.3

3.4

2.3

3.3

3.3

Current assets

632

755

891

1,673

2,153

Cash

16

24

55

209

454

Loans & advances

116

147

120

426

494

Other

500

584

716

1,038

1,205

Current liabilities

325

422

464

884

1,027

Net current assets

307

333

426

789

1,127

Mis. Exp. not written off

-

-

-

-

-

Total assets

722

795

1,177

1,693

2,179

February 2, 2016

7

Alembic Pharma | 3QFY2016 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015 FY2016E FY2017E

Profit before tax

206

308

360

819

671

Depreciation

35

40

44

47

53

(Inc)/Dec in Working Capital

(78)

(84)

66

(266)

103

Less: Other income

-

-

-

-

-

Direct taxes paid

41

75

76

159

130

Cash Flow from Operations

121

190

393

441

696

(Inc.)/Dec.in Fixed Assets

(84)

(81)

(257)

(200)

(200)

(Inc.)/Dec. in Investments

-

-

-

-

-

Other income

-

-

-

-

-

Cash Flow from Investing

(84)

(81)

(257)

(200)

(200)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

(165)

(109)

164

(89)

0

Dividend Paid (Incl. Tax)

(55)

(55)

(55)

(55)

(55)

Others

(39)

(34)

184

160

51

Cash Flow from Financing

(259)

(197)

293

16

(4)

Inc./(Dec.) in Cash

(31)

8

31

154

245

Opening Cash balances

47

16

24

55

209

Closing Cash balances

16

24

55

209

454

February 2, 2016

8

Alembic Pharma | 3QFY2016 Result Update

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

70.6

49.4

41.1

17.7

21.5

P/CEPS

58.3

42.1

35.6

16.5

19.6

P/BV

23.2

17.2

13.2

7.8

5.9

Dividend yield (%)

0.4

0.4

0.4

0.4

0.4

EV/Sales

7.8

6.3

5.7

3.5

3.0

EV/EBITDA

47.4

32.7

29.4

13.0

15.3

EV / Total Assets

16.3

14.7

10.0

6.8

5.2

Per Share Data (`)

EPS (Basic)

8.8

12.5

15.0

35.0

28.7

EPS (fully diluted)

8.8

12.5

15.0

35.0

28.7

Cash EPS

10.6

14.7

17.4

37.5

31.5

DPS

2.5

2.5

2.5

2.5

2.5

Book Value

26.7

35.8

46.9

79.0

104.8

Dupont Analysis

EBIT margin

14.1

17.0

17.3

25.5

18.0

Tax retention ratio

80.1

75.6

78.8

80.6

80.6

Asset turnover (x)

2.1

2.5

2.2

2.5

2.4

ROIC (Post-tax)

23.9

32.5

29.6

51.6

34.3

Cost of Debt (Post Tax)

4.5

5.6

0.9

6.4

6.4

Leverage (x)

0.6

0.2

0.1

0.1

0.0

Operating ROE

34.8

38.2

33.8

55.4

34.3

Returns (%)

ROCE (Pre-tax)

29.6

39.9

30.2

49.3

31.3

Angel ROIC (Pre-tax)

31.9

44.5

38.7

65.8

43.5

ROE

36.8

40.0

36.3

55.6

31.2

Turnover ratios (x)

Asset Turnover (Gross Block)

2.9

3.0

2.6

3.3

3.2

Inventory / Sales (days)

63.1

56.5

61.5

55.6

71.5

Receivables (days)

51.9

49.5

56.3

51.3

62.6

Payables (days)

72.6

79.8

79.3

41.5

45.9

WC cycle (ex-cash) (days)

78.6

58.6

60.3

53.0

60.1

Solvency ratios (x)

Net debt to equity

0.3

0.1

0.2

(0.0)

(0.2)

Net debt to EBITDA

0.7

0.2

0.5

(0.1)

(0.4)

Interest Coverage (EBIT / Int.)

14.3

32.3

199.5

53.7

56.9

February 2, 2016

9

Alembic Pharma | 3QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Alembic Pharma

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 2, 2016

10