2QFY2017 Result Update | Pharmaceutical

November 7, 2016

Alembic Pharmaceuticals

NEUTRAL

CMP

`676

Performance Highlights

Target Price

-

Y/E March (` cr)

2QFY2017 1QFY2017

% chg (qoq) 2QFY2016

% chg (yoy)

Investment Period

-

Net Sales

872

727

19.9

1008

(13.5)

Stock Info

Other Income

0

1

(97.2)

1

(95.9)

Sector

Pharmaceutical

Operating Profit

177

156

13.6bp

375

(52.8)bp

12,363

Market Cap (` cr)

Interest

1

1

(10.3)

1

Net Debt (` cr)

814

Adj. Net Profit

120

104

15.5

289

(58.5)

Beta

0.5

Source: Company, Angel Research

52 Week High / Low

727/514

Alembic Pharmaceuticals posted sales of `872cr (vs. `1,008cr in 2QFY2016), a

Avg. Daily Volume

19,547

2

dip of 13.5% yoy, mainly on back of base effect. International business declined

Face Value (`)

27,274

owing to lower contribution from Abilify. On the operating front, the gross margin

BSE Sensex

Nifty

8,434

is expected to come in at 72.5% (vs. 77.5% in 2QFY2016) and EBIDTA margin at

Reuters Code

ALEM.BO

20.3% (vs. 37.2% in 2QFY2016). Consequently, the PAT is expected to come in at

Bloomberg Code

ALPM@IN

`120cr (vs. `289cr in 2QFY2016), a yoy dip of 58.5%. We maintain our Neutral

rating on the stock.

Shareholding Pattern (%)

Results below expectations: Alembic Pharmaceuticals posted sales of `872cr

Promoters

74.4

(vs. `1,008cr in 2QFY2016), a dip of 13.5% yoy, mainly on back of base effect.

MF / Banks / Indian Fls

3.7

International business declined owing to lower contribution from Abilify. On the

FII / NRIs / OCBs

11.3

operating front, the gross margin is expected to come in at 72.5% (vs. 77.5% in

Indian Public / Others

10.6

2QFY2016) and EBIDTA margin at

20.3% (vs.

37.2% in 2QFY2016).

Consequently, the PAT is expected to come in at

`120cr (vs.

`289cr in

2QFY2016), a yoy dip of 58.5%.

Abs. (%)

3m

1yr

3yr

Sensex

(1.0)

3.2

29.1

Outlook and valuation: Over FY2016-18E, we expect the company to post a

Alembic Pharma

15.7

0.2

241.0

CAGR of 13.9% in sales, while profitability will be under pressure on back of

higher R&D spend, which is likely to reach 13-14% of sales in FY2017-FY2018E.

We recommend a Neutral rating on the stock.

3-year price chart

900

Key Financials (Consolidated)

800

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

700

600

Net Sales

2,053

3,145

3,483

4,083

500

% chg

10.2

53.2

10.8

17.2

400

300

Net Profit

283

720

459

572

200

% chg

20.0

154.1

(36.2)

24.7

100

0

EPS (`)

15.0

38.2

24.3

30.4

EBITDA Margin (%)

19.5

31.9

20.2

21.4

Source: Company, Angel Research

P/E (x)

45.0

17.7

27.8

21.6

RoE (%)

36.3

57.9

25.5

25.3

RoCE (%)

30.2

51.0

27.2

27.5

P/BV (x)

14.4

8.0

6.4

5.0

EV/Sales (x)

6.2

3.9

3.6

3.0

Sarabjit Kour Nangra

EV/EBITDA (x)

32.1

12.3

17.6

13.8

+91- 22- 36357600 - 6806

Source: Company, Angel Research; Note: CMP as of November 4, 2016

Please refer to important disclosures at the end of this report

1

Alembic Pharma | 2QFY2017 Result Update

Exhibit 1: 2QFY2017 performance (Consolidated)

Y/E March (` cr)

2QFY2017

1QFY2017

% chg (qoq) 2QFY2016

% chg (yoy) 1HFY2017 1HFY2016

% chg (yoy)

Net sales

872

727

19.9

1,008

(13.5)

1,595

1,585

0.6

Other income

0

1

(97.2)

1

(95.9)

1

2

(27.5)

Total income

872

728

1,009

(13.6)

1,596

1,587

Gross profit

632

536

17.8

782

(19.2)

1168

1151

1.5

Gross margin

72.5

73.7

77.5

73.2

72.6

Operating profit

177

156

13.6

375

(52.8)

333

476

(30.0)

Operating margin (%)

20.3

21.4

37.2

20.9

30.0

Interest

1

1

(10.3)

1

2

1

103.0

Depreciation

21

19

6.4

13

55.4

40

26

53.8

PBT

156

137

13.6

362

(57.0)

294

451

(34.9)

Provision for taxation

33

33

(0.4)

74

(54.9)

66

92

(27.8)

PAT before Extra-ordinary item

122

104

18.1

289

(57.6)

227

360

(36.9)

(Profit)/Loss of Associate Company

4

(2)

(0)

-4

0

PAT after Extra-ordinary item & MI

120

104

15.5

289

(58.5)

224

360

(37.9)

EPS (`)

6.4

5.5

15.3

11.9

19.1

Source: Company, Angel Research

Exhibit 2: 2QFY2017 - Actual vs Angel estimates

(` cr)

Actual

Estimates

Variation (%)

Net Sales

872

750

16.2

Other Income

0

1

(95.9)

Operating Profit

177

164

7.7

Interest

1

1

(12.7)

Tax

33

33

(0.5)

Net Profit

120

112

6.0

Source: Company, Angel Research

Sales above expectation: The sales came in at `872cr (vs. `750cr expected vs.

`1,008cr in 2QFY2016), a dip of 13.5% yoy, mainly on back of base effect.

International formulation business (`352cr in 2QFY2017) posted a yoy dip of

38.4%, while the Indian formulation (`338cr in 2QFY2017) posted a yoy growth of

19.0%. API posted sales of `164cr in 2QFY2017, a yoy growth of 19.7%.

The growth in the Indian formulations segment was driven by the specialty segment

which grew by 16% yoy, while the acute segment grew by 22% yoy during the

period. During FY2016, the specialty segment had a 60% share in domestic

formulations while the rest was accounted by the acute segment (40%).

The API business (`292.5cr) posted a growth of 14.0% yoy. Indian generics posted

sales of `25cr in 2QFY2017. Till date, the company has filed 82 products (4 in

2QFY2017) in USA.

November 7, 2016

2

Alembic Pharma | 2QFY2017 Result Update

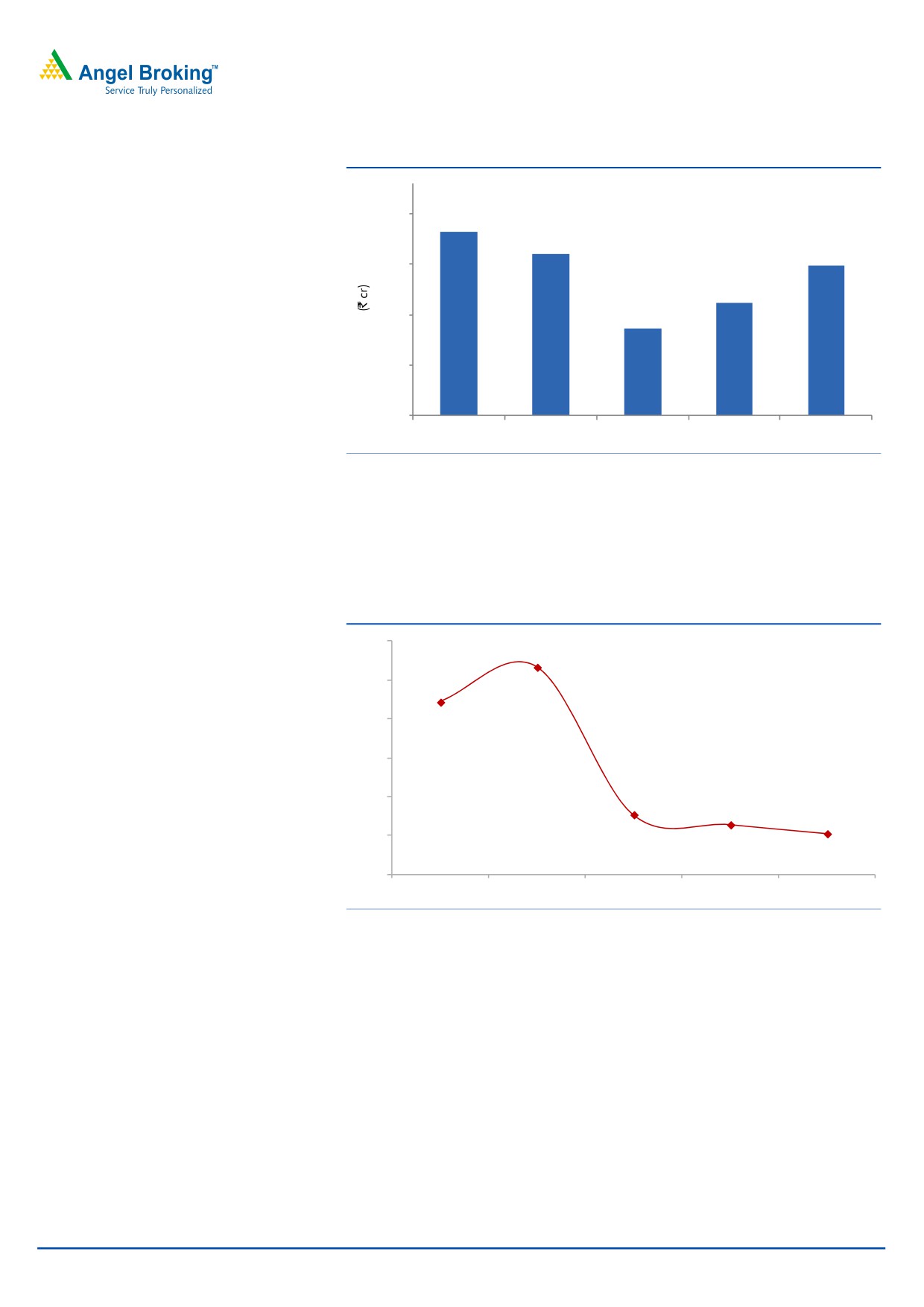

Exhibit 3: Sales trend

1080

1,008

921

872

880

727

680

626

480

280

2QFY2016

3QFY2016

4QFY2016

1QFY2017

2QFY2017

Source: Company, Angel Research

OPM lower than expectation: On the operating front, the gross margin came in at

72.5% (vs. 73.4% expected vs. 77.5% in 2QFY2016) and EBIDTA margin at 20.3%

(vs. 21.9% expected vs. 37.2% in 2QFY2016). The R&D expenses, during the

quarter, came in at 12.5% of sales (vs. 7.7% of sales in 2QFY2016).

Exhibit 4: OPM Trend (%)

45.0

41.7

40.0

37.2

35.0

30.0

22.7

25.0

21.4

20.3

20.0

15.0

2QFY2016

3QFY2016

4QFY2016

1QFY2017

2QFY2017

Source: Company, Angel Research

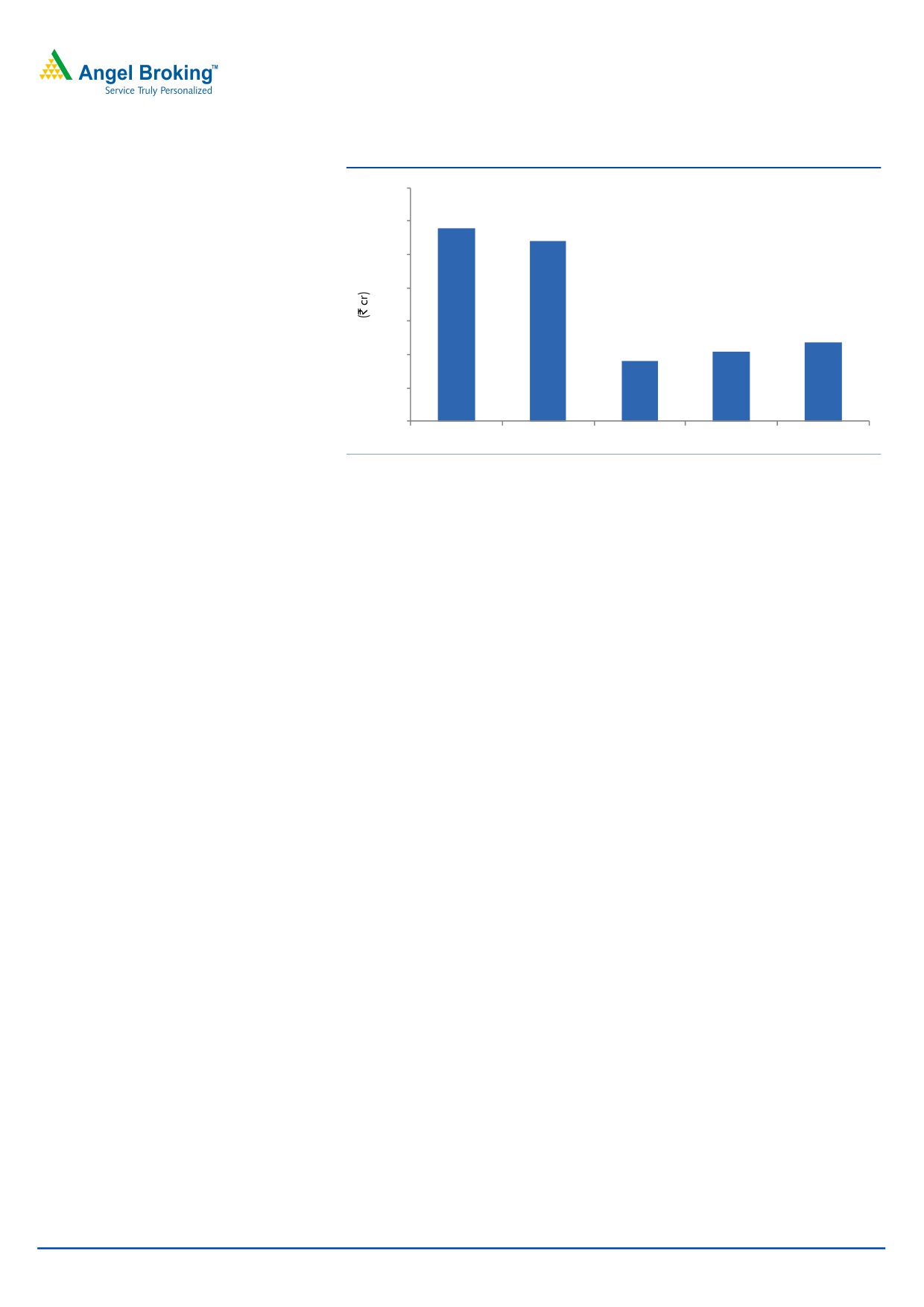

Net profit above expectation: The Adj. net profit stood at `120cr (vs. `289cr in

2QFY2017), a yoy de-growth of 58.5%. This was against the expectation of

`112cr.

November 7, 2016

3

Alembic Pharma | 2QFY2017 Result Update

Exhibit 5: Net profit trend

350

289

269

300

250

200

150

119

104

91

100

50

0

2QFY2016

3QFY2016

4QFY2016

1QFY2017

2QFY2017

Source: Company, Angel Research

Concall highlights

Oncology oral solids and injectable facilities to be operational by FY2017

end.

12-16 US ANDA approvals expected till FY2018 end.

R&D expenses to be `400-450cr in FY2017.

33 pending ANDAs, of which ~40% are Para IV/ FTFs.

Capex for FY2017 to be `600cr.

Investment arguments

Focus on chronic segment to drive domestic formulation growth: Alembic

Pharmaceuticals has been restructuring its business portfolio, which would aid in

improving its growth and operating performance. The company’s domestic

formulation business contributed 44% to its total sales in FY2016. The company

has a strong field force of ~3,600 medical representatives. Going forward, the

company expects its domestic formulation business to at least grow in line with the

industry growth rate, before it sees an improvement in the share of the high growth

chronic segment. For FY2016-18E, we expect the domestic formulation business to

grow at a CAGR of 15.0%.

Exports- US the key growth driver: On the exports front, the formulation business

contributed by 30% to the total turnover, with majority of the contribution coming

from Europe and the US. In the US, the company has filed for ~82 ANDAs till date

and received 49 approvals. The company, going forward, expects to keep its

momentum high in terms of number of filings, by filing around 10-12 ANDAs per

annum. For FY2016-18E, we expect exports to register a CAGR of 13.6%, mainly on

back of base effect impact of FY2016 (sales grew by 46%, due to launch of Abilify).

Outlook and valuation: Over FY2016-18E, we expect the company to post a

CAGR of 13.9% in sales, while profitability will be under pressure on back of

higher R&D spend, which is likely to reach 13-14% of sales in FY2017-FY2018E.

We recommend our Neutral rating on the stock.

November 7, 2016

4

Alembic Pharma | 2QFY2017 Result Update

Exhibit 6: Key assumptions

FY2017E

FY2018E

Domestic formulation sales growth (%)

16.0

14.0

Exports sales growth (%)

8.0

20.0

R&D as % of sales

14.0

13.0

Operating margins (%)

20.2

21.4

Capex (` cr)

400

200

Net Debt/Equity (x)

(0.1)

(0.2)

Source: Company, Angel Research

Exhibit 7: Recommendation summary

Reco.

CMP Tgt Price Upside

FY2018E

FY16-18E

FY2018E

(`)

(`)

(%) PE (x) EV/Sales (x) EV/EBITDA (x)

CAGR in EPS (%) RoCE (%) RoE (%)

Alembic Pharma

Neutral

656

-

-

21.6

2.9

13.4

(10.8)

27.5

25.3

Aurobindo Pharma Accumulate

727

877

20.7

15.4

2.5

10.7

18.1

22.5

26.1

Cadila Healthcare

Neutral

390

-

-

18.4

3.1

14.3

13.4

22.7

25.7

Cipla

Neutral

545

-

-

20.0

2.5

13.8

20.4

13.5

15.2

Dr Reddy's

Neutral

3,077

-

-

21.5

2.8

12.4

1.7

16.2

15.9

Dishman Pharma

Neutral

227

-

-

20.1

2.3

9.9

3.1

10.3

10.9

GSK Pharma

Neutral

2,775

-

-

46.7

6.0

42.1

15.9

33.7

30.6

Indoco Remedies

Neutral

276

-

-

17.7

2.1

11.3

31.5

19.1

19.2

Ipca labs

Accumulate

583

613

5.1

29.6

2.0

13.4

36.5

8.8

9.4

Lupin

Buy

1,421

1,809

27.3

20.5

3.9

12.6

17.2

24.4

20.9

Sanofi India*

Neutral

4,276

-

-

25.3

3.4

18.2

21.2

24.9

28.4

Sun Pharma

Buy

653

944

44.6

19.9

3.9

12.6

22.0

33.1

18.9

Source: Company, Angel Research; Note: *December year end

Company Background

Alembic Pharmaceuticals is a leading pharmaceutical company in India. The

company is vertically integrated to develop pharmaceutical substances and

intermediates. The company is a market leader in the Macrolides segment of

anti-infective drugs in India. Its manufacturing facilities are located in Vadodara

and in Baddi (Himachal Pradesh; for the domestic and non-regulated export

market). The Panelav facility houses the API and formulation manufacturing (both

USFDA approved) plants.

November 7, 2016

5

Alembic Pharma | 2QFY2017 Result Update

Profit & Loss Statement (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017E

FY2018E

Gross sales

1,871

2,064

3,181

3,522

4,128

Less: Excise duty

8

11

36

39

45

Net sales

1,863

2,053

3,145

3,483

4,083

Other operating income

3.2

5.7

3.6

3.6

3.6

Total operating income

1,866

2,058

3,149

3,487

4,087

% chg

22.8

10.3

53.0

10.7

17.2

Total expenditure

1,506

1,653

2,143

2,779

3,210

Net raw materials

713

715

769

1,045

1,225

Other mfg costs

82

90

138

153

180

Personnel

247

307

421

506

607

Other

463

542

814

1,075

1,198

EBITDA

358

400

1,002

704

873

% chg

43.7

11.7

150.9

(29.7)

24.0

(% of Net Sales)

19.2

19.5

31.9

20.2

21.4

Depreciation& amortisation

40

44

72

99

120

Interest & other charges

10

2

4

10

11

Other income

0

0

6

-

-

(% of PBT)

0

0

-

-

-

Share in profit of Associates

-

-

-

-

-

Recurring PBT

308

360

936

596

743

% chg

49.4

16.8

160.2

(36.3)

24.7

Extraordinary expense/(Inc.)

-

-

-

-

-

PBT (reported)

308

360

936

596

743

Tax

75

76

216

137

171

(% of PBT)

24.4

21.2

23.1

23.0

23.0

PAT (reported)

236

283

720

459

572

Add: Share of earnings of asso.

-

-

(0)

-

-

Less: Minority interest (MI)

-

-

-

-

-

Prior period items

-

-

-

-

-

PAT after MI (reported)

236

283

720

459

572

ADJ. PAT

236

283

720

459

572

% chg

43.0

20.0

154.1

(36.2)

24.7

(% of Net Sales)

12.7

13.8

22.9

13.2

14.0

Basic EPS (`)

12.5

15.0

38.2

24.3

30.4

Fully Diluted EPS (`)

12.5

15.0

38.2

24.3

30.4

% chg

43.0

20.0

154.1

(36.2)

24.7

November 7, 2016

6

Alembic Pharma | 2QFY2017 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017E

FY2018E

SOURCES OF FUNDS

Equity share capital

37.7

37.7

37.7

37.7

37.7

Preference Capital

-

-

-

-

-

Reserves & surplus

638

847

1,563

1,967

2,485

Shareholders funds

676

885

1,601

2,005

2,523

Minority Interest

Other Long Term Liabilities

12.7

15.8

33.9

14.3

14.3

Long Term Provisions

6.7

6.4

7.4

7.4

7.4

Total loans

78

239

133

150

150

Deferred tax liability

23

31

50

50

50

Total liabilities

795

1,177

1,824

2,227

2,744

APPLICATION OF FUNDS

Gross block

665

907

1,208

1,608

1,808

Less: acc. depreciation

268

313

385

483

603

Net block

397

595

824

1,125

1,206

Capital work-in-progress

21

-

-

-

-

Goodwill

35

44

Long Term Loans and Adv.

42

118

83

83

83

Investments

3.4

2.3

2.1

3.3

3.3

Current assets

755

891

1,507

1,955

2,554

Cash

24

55

451

398

729

Loans & advances

147

120

409

453

531

Other

584

716

647

1,104

1,294

Current liabilities

422

464

635

940

1,102

Net current assets

333

426

872

1,015

1,452

Mis. Exp. not written off

-

-

-

-

-

Total assets

795

1,177

1,824

2,227

2,744

November 7, 2016

7

Alembic Pharma | 2QFY2017 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY2014 FY2015 FY2016

FY2017E

FY2018E

Profit before tax

308

360

936

596

743

Depreciation

40

44

72

99

120

(Inc)/Dec in Working Capital

(84)

66

191

(358)

169

Less: Other income

-

-

-

-

-

Direct taxes paid

75

76

216

137

171

Cash Flow from Operations

190

393

982

199

861

(Inc.)/Dec.in Fixed Assets

(81)

(222)

(301)

(400)

(200)

(Inc.)/Dec. in Investments

-

-

-

-

-

Other income

-

-

-

-

-

Cash Flow from Investing

(81)

(222)

(301)

(400)

(200)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

(109)

164

(87)

(2)

-

Dividend Paid (Incl. Tax)

(55)

(55)

(55)

(55)

(55)

Others

(34)

184

160

51

51

Cash Flow from Financing

(197)

293

19

(6)

(4)

Inc./(Dec.) in Cash

8

31

396

(53)

331

Opening Cash balances

16

24

55

451

398

Closing Cash balances

24

55

451

398

729

November 7, 2016

8

Alembic Pharma | 2QFY2017 Result Update

Key Ratios

Y/E March

FY2014

FY2015

FY2016

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

52.4

43.7

17.2

26.9

21.6

P/CEPS

44.7

37.7

15.6

22.2

17.9

P/BV

18.3

14.0

7.7

6.2

4.9

Dividend yield (%)

0.4

0.4

0.4

0.4

0.4

EV/Sales

6.7

6.1

3.8

3.5

2.9

EV/EBITDA

34.7

31.2

12.0

17.1

13.4

EV / Total Assets

15.6

10.6

6.6

5.4

4.3

Per Share Data (`)

EPS (Basic)

12.5

15.0

38.2

24.3

30.4

EPS (fully diluted)

12.5

15.0

38.2

24.3

30.4

Cash EPS

14.7

17.4

42.0

29.6

36.7

DPS

2.5

2.5

2.5

2.5

2.5

Book Value

35.8

46.9

84.9

106.4

133.8

Dupont Analysis

EBIT margin

17.0

17.3

29.6

17.4

18.5

Tax retention ratio

75.6

78.8

76.9

77.0

77.0

Asset turnover (x)

2.5

2.2

2.5

2.2

2.1

ROIC (Post-tax)

32.5

29.6

57.4

29.2

30.2

Cost of Debt (Post Tax)

5.6

0.9

1.5

5.4

5.4

Leverage (x)

0.2

0.1

0.0

0.0

0.0

Operating ROE

38.2

33.8

57.6

29.2

30.2

Returns (%)

ROCE (Pre-tax)

39.9

30.2

51.0

27.2

27.5

Angel ROIC (Pre-tax)

44.5

38.7

77.0

38.4

39.2

ROE

40.0

36.3

57.9

25.5

25.3

Turnover ratios (x)

Asset Turnover (Gross Block)

3.0

2.6

3.0

2.5

2.4

Inventory / Sales (days)

56.5

61.5

54.1

70.5

78.4

Receivables (days)

49.5

56.3

43.5

56.3

62.3

Payables (days)

79.8

79.3

37.8

41.7

46.9

WC cycle (ex-cash) (days)

58.6

60.3

45.9

54.3

59.8

Solvency ratios (x)

Net debt to equity

0.1

0.2

(0.2)

(0.1)

(0.2)

Net debt to EBITDA

0.2

0.5

(0.3)

(0.4)

(0.7)

Interest Coverage (EBIT / Int.)

32.3

199.5

252.8

61.3

71.8

November 7, 2016

9

Alembic Pharma | 2QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Alembic Pharma

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 7, 2016

10