3QFY2018 Result Update | IT

January 15, 2018

Tata Consultancy Services (TCS)

REDUCE

CMP

`2,773

Performance highlights

Target Price

`2,493

(` cr)

3QFY18

2QFY18

% chg (qoq) 3QFY17

% chg (yoy)

Investment Period

12 Months

Net revenue

30,904

30,541

1.2

29,735

3.9

Adj. EBITDA

7,065

8,164

(13.5)

8,088

(12.6)

Adj. EBITDA margin (%)

26.8

26.7

8.4bps

27.2

(87.3)bps

Adj. PAT

6,531

6,446

1.3

6,778

(3.6)

Source: Company, Angel Research

Stock Info

TCS posted a

1.0% sequential growth in USD revenues to US$4,787mn v/s

Sector

IT

US$4,801mn expected. In rupee terms, revenues came in at `30,904cr V/s `31,049cr, up

Market Cap (` cr)

530,813

Net Debt (` cr)

(45,288)

1.2% QoQ. In Constant Currency (CC) terms, the company posted a 1.3% QoQ growth

Beta

0.3

with volume growth coming in at 1.6% QoQ (highest growth in three years for the

52 Week High / Low

2,820/2,154

December quarter). On profitability front, EBIT margin showed an upside of ~12bps

Avg. Daily Volum e

42,762

QoQ to 25.2%. Consequently, PAT came in at 6,531cr v/s `6,509cr expected, up of 1.3%

Face Value (`)

1

BSE Sensex

32,507

QoQ. We maintain our Reduce rating on the stock, with a price target of `2,493.

Nifty

110,681

Quarterly highlights: TCS posted a 1.0% sequential growth in USD revenues to

Reuters Code

TCS.BO

Bloomberg Code

TCS@IN

US$4,787mn v/s US$4,801mn expected. In Constant Currency (CC) terms, the

company posted a 1.3% QoQ growth with volume growth coming in at 1.6% QoQ

Shareholding Pattern (%)

(highest growth in since three years for the December quarter). Geography wise, USA

Promoters

73.6

was key driver, with North America & Latin America registering a QoQ CC growth of

MF / Banks / Indian Fls

6.1

1.5% and 5.0% respectively. In Europe, it was Continental Europe registering a QoQ

FII / NRIs / OCBs

16.4

CC growth of 2.6%. In terms of Industries, Retail & CPG registered a QoQ CC growth

Indian Public / Others

4.0

of 6.4%, Energy & Utilities grew 8.5% and Life Sciences & Healthcare posted 2.5%. On

profitability front, EBIT margin showed an upside of ~12bps QoQ to 25.2%.

Abs .(%)

3m

1yr

3yr

Consequently, PAT came in at 6,531cr V/s `6,509cr expected, up 1.3% QoQ.

Sensex

6.0

27.0

25.4

TCS

7.3

18.3

10.4

Outlook and valuation: The Company has been cautiously optimistic regarding its

outlook for FY2018, with key verticals like BFSI and Hi-Tech expected to post a

recovery. During 3QFY2018, it signed a multiyear Digital contract, the highest value

digital contract for the company so far. We expect TCS to post revenue CAGR of 9.3%

and 7.6% in USD & INR terms respectively over FY2017-19E. Hence, we maintain our

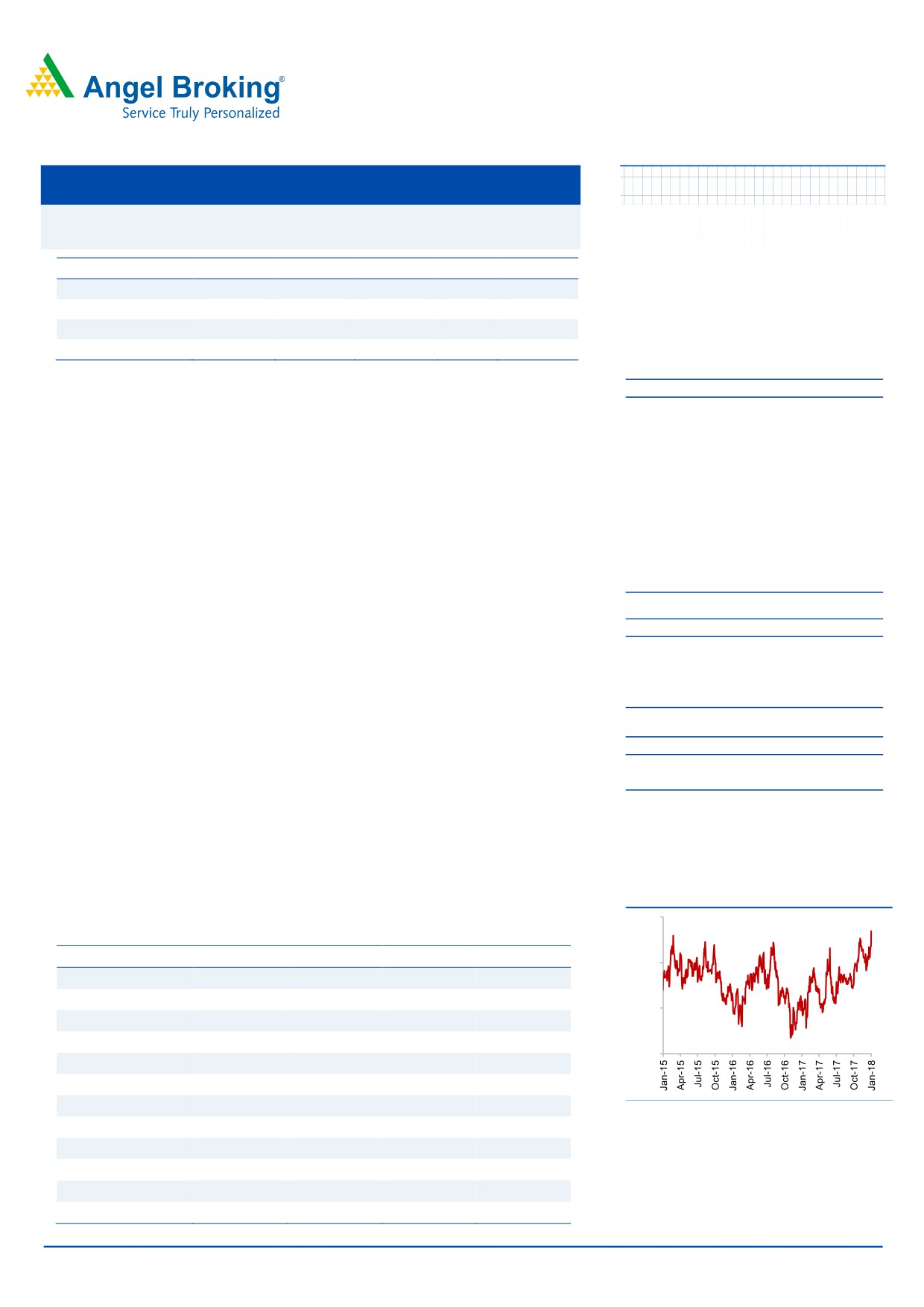

3-Year Daily Price Chart

Reduce recommendation.

2,900

Key financials (Consolidated, IFRS)

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

2,600

Net sales

108,646

117,966

123,384

136,504

% chg

14.8

8.6

4.6

10.6

2,300

Net profit

24,215

26,289

26,346

28,700

% chg

11.6

8.6

0.2

8.9

2,000

EBITDA margin (%)

28.3

27.5

26.4

26.3

EPS (`)

123.7

134.3

134.6

146.6

P/E (x)

22.4

20.6

20.6

18.9

Source: Company, Angel Research

P/BV (x)

7.4

6.1

5.7

5.3

RoE (%)

33.1

29.8

27.8

28.3

RoCE (%)

31.6

28.8

27.0

27.6

Sarabjit kour Nangra

EV/Sales (x)

4.6

4.1

4.0

3.5

+91 22 3935 7800 Ext: 6806

EV/EBITDA (x)

16.3

15.0

15.0

13.4

sarabjit @angelbroking.com

Source: Company, Angel Research; Note: CMP as of January 12, 2018

Please refer to important disclosures at the end of this report

1

TCS | 3QFY2018 Result Update

Exhibit 1: 3QFY2018 performance (Consolidated, IFRS)

(` cr)

3QFY2018

2QFY2018

% chg (qoq)

3QFY2017

% chg (yoy) 9MFY2018 9MFY2017

% chg(yoy)

Net revenue

30,904

30,541

1.2

29,735

3.9

91,029

88,324

3.1

Cost of revenue

17,356

16,572

4.7

16,378

6.0

51,255

48,732

5.2

Gross profit

13,548

13,969

(3.0)

13,357

1.4

39,774

39,592

0.5

SG&A expense

5,261

5,805

(9.4)

5,124

2.7

15,910

15,413

3.2

EBITDA

8,287

8,164

1.5

8,233

0.7

23,864

24,179

(1.3)

Dep. and Amortization

506

504

0.4

500

1.2

1,509

1,482

1.8

EBIT

7,781

7,660

1.6

7,733

0.6

22,355

22,697

(1.5)

Other income

864

812

6.4

1,185

(27.1)

2,608

3,200

(18.5)

PBT

8,645

8,472

2.0

8,918

(3.1)

24,963

25,897

(3.6)

Income tax

2,100

2,012

4.4

2,104

(0.2)

6,008

6,162

(2.5)

PAT

6,545

6,460

1.3

6,814

(3.9)

18,955

19,735

(4.0)

Earnings in affiliates

-

-

-

-

-

-

-

Minority interest

14

14

36

-

33

54

Reported PAT

6,531

6,446

1.3

6,778

(3.6)

18,922

19,681

(3.9)

Adj. PAT

6,531

6,446

1.3

6,778

(3.6)

18,922

19,681

(3.9)

EPS

34.1

33.7

1.3

34.4

(0.8)

96.6

100.5

(3.9)

Gross margin (%)

43.8

45.7

(190)bps

44.9

(108)bps

43.7

44.8

(113)bps

EBITDA margin (%)

26.8

26.7

8bps

27.7

(87)bps

26.2

27.4

(116)bps

EBIT margin (%)

25.2

25.1

12bps

26.0

(81)bps

24.6

25.7

(114)bps

Source: Company, Angel Research

Exhibit 2: Actual v/s Angel estimates

(` cr)

Actual

Estimate

Var. (%)

Net revenue

30,904

31,049

(0.5)

EBIT margin (%)

25.2

24.9

30

Adj. PAT

6,531

6,509

0.3

Source: Company, Angel Research

Numbers lower than expectations

TCS posted a 1.0% sequential growth in USD revenues to US$4,787mn v/s US$4,801mn

expected. In rupee terms, revenues came in at `30,904cr V/s `31,049cr, up 1.2% qoq. In

Constant Currency (CC) terms, the company posted a 1.3% qoq growth with volume

growth coming in at 1.6% qoq growth (highest growth in three years for the December

quarter). Geography wise, USA was key driver, with North America & Latin America

registering a qoq CC growth of 1.5% and 5.0% respectively. In Europe, it was Continental

Europe registering a qoq CC growth of 2.6%. In terms of Industries, Retail & CPG

registered a qoq CC growth of 6.4%, Energy & Utilities grew 8.5% and Life Sciences &

Healthcare posted 2.5%.

In terms of verticals, on CC basis, the growth registered by the company in respective

segments was mixed with BFSI down marginally (1.5% qoq), Energy Utilities (8.5% qoq)

and Retail & CPG (6.4% qoq) up significantly, and remaining segments performing well

including Communication & Media (2.2% qoq), Manufacturing (2.1% qoq), Life Sciences

& Healthcare (2.5% qoq), and Travel & Hospitality (0.1% qoq).

In terms of geography, on CC basis, qoq growth was North America (1.5%), Latin

America (5.0%), UK (0.8%), Continental Europe (2.6%), India (0.5%), Asia Pacific (0.0%),

MEA (-0.2%).

January 15, 2018

2

TCS | 3QFY2018 Result Update

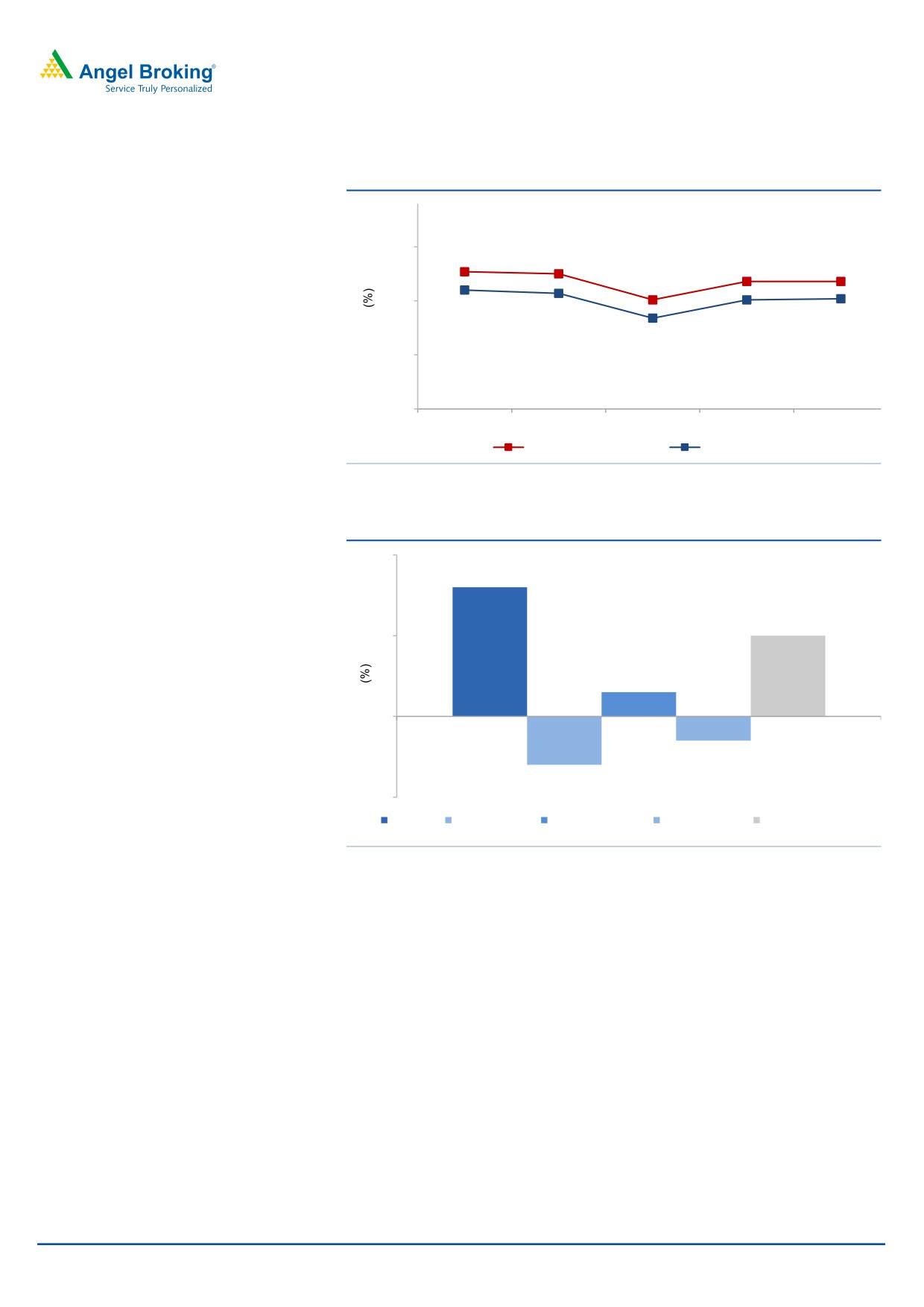

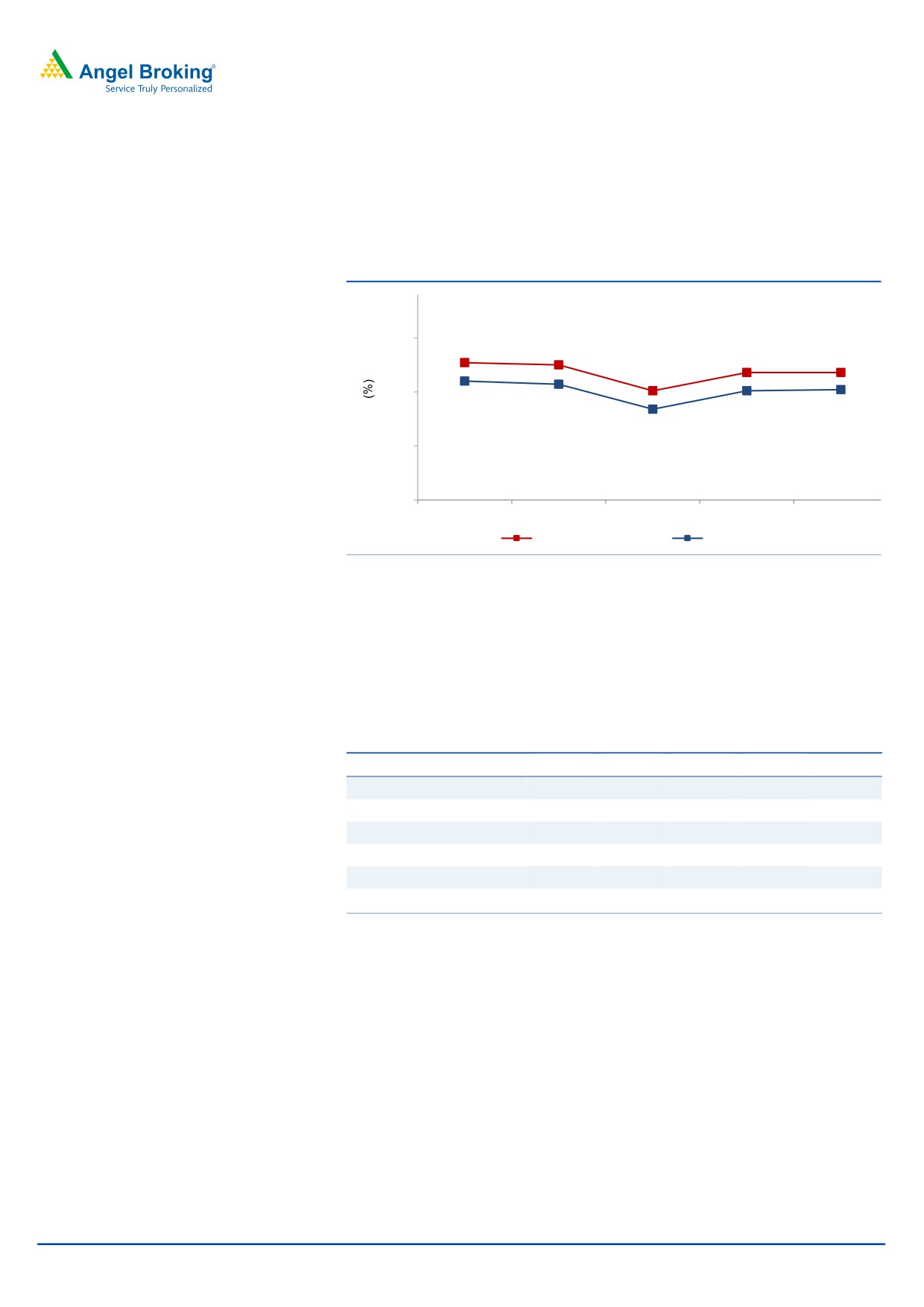

Exhibit 3: Trend in volume and revenue growth (QoQ)

30

27.7

27.5

26.8

26.8

25.1

25

26.0

25.7

25.1

25.2

23.4

20

15

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

EBITDA margin

EBIT margin

Source: Company, Angel Research

Exhibit 4: Revenue drivers for 3QFY2018

2

1.6

1.0

1

0.3

0

(0.3)

(0.6)

(1)

Volume Offshore shift

Currency impact

CC realization

Total revenue growth

Source: Company, Angel Research

BFSI in 3QFY2018 saw a decline of 1.5% qoq, led by softened demand trends. Retail,

which has been a troubled area in recent quarters, saw a decline in 2QFY2018 when it

bottomed out. In 3QFY2018, the vertical grew by 6.4% qoq CC staging a comeback.

Digital, now 22.1% of total revenues continued exhibiting strength having grown by

13.9% qoq CC. TCS won a US$50mn+ deal in digital this quarter.

January 15, 2018

3

TCS | 3QFY2018 Result Update

Exhibit 5: Revenue growth (Industry wise on CC basis)

% to revenue

% chg (CC qoq)

% chg (yoy)

BFSI

32.1

(1.5)

0.2

Manufacturing

7.6

2.1

9.5

Communication & Media

7.4

2.2

16.5

Life sciences and healthcare

7.3

2.5

13.5

Retail and CPG

12.5

6.4

3.0

Transportation & Hospitality

3.8

2.9

24.1

Energy and utilities

4.5

8.5

29.4

Technology & Services

8.0

0.1

9.6

Regional Markets & Others

16.8

0.5

2.2

Source: Company, Angel Research

Geography wise, qoq growth in INR sales in key geographies on CC basis was as follows:

USA (1.5%), Latin America (5.0%), UK (0.8%), India (0.5%), and MEA (-0.2%). However,

Continental Europe and Asia Pacific posted qoq growth of 2.6% and 0.0% on CC basis

respectively.

Exhibit 6: Revenue growth (Geography wise in INR terms)

% of revenue

% chg (CC qoq)

% chg (yoy)

U.S.

52.0

1.5

2.8

Latin America

2.2

5.0

5.4

U.K.

14.1

0.8

8.2

Continental Europe

13.5

2.6

22.3

India

6.3

0.5

4.1

Asia Pacific

9.5

0.0

6.2

MEA

2.4

(0.2)

3.7

Source: Company, Angel Research

Attrition rate expands

In 3QFY2018, TCS witnessed a gross addition of 12,534 employees and net addition of

1,667 employees, taking its total employee base to 3,90,880. During the quarter, the

attrition rate (last twelve-month [LTM] basis) for the company increased to 11.9% from

11.3% in 2QFY2018.

Exhibit 7: Hiring and attrition trend

Particulars

3QFY17 4QFY17

1QFY18

2QFY18

3QFY18

Gross addition

18,362

20,093

11,202

15,868

12,534

Net addition

6,978

8,726

(1,414)

3,404

1,667

Total employee base

3,78,497

3,87,223

3,85,809

3,89,213

3,90,880

Attrition (%) - LTM basis

12.2

11.5

12.4

11.3

11.9

Source: Company, Angel Research

January 15, 2018

4

TCS | 3QFY2018 Result Update

Margin expands

On the operating front, the company reported EBITDA and EBIT margins at 26.8%

and 25.2%, i.e. an expansion of 5ps and 6bps qoq respectively. The company has

maintained an EBIT margin Target of 26-28%.

Exhibit 8: Adj. Margin profile

30

27.7

27.5

26.8

26.8

25.1

25

26.0

25.7

25.1

25.2

23.4

20

15

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

EBITDA margin

EBIT margin

Source: Company, Angel Research

Client metrics

The client pyramid during the quarter witnessed a qualitative improvement with

client additions seen in the higher revenue brackets. The clients in US$20mn+

revenue band increased by 7 and in US$50mn+ revenue band increased by 3.

Exhibit 9: Client pyramid

3QFY17 4QFY17 1QFY18 2QFY18 3QFY18

US$1mn-5mn

426

438

441

463

456

US$5mn-10mn

154

149

142

142

148

US$10mn-20mn

114

120

132

132

134

US$20mn-50mn

106

106

105

105

109

US$50mn-100mn

46

49

49

54

57

US$100mn plus

34

35

36

37

37

Source: Company, Angel Research

January 15, 2018

5

TCS | 3QFY2018 Result Update

Investment Argument

Guidance - Stability visible: While management has not given any guidance for

FY2018, it expects its key verticals like BFSI, Communications and Hi-Tech to

stabilize as we move forward. Digital also continues to see good traction,

constituting 22.1% of total revenue, and having grown by 13.9% qoq CC and 39.6%

yoy. Overall, the volume growth has been robust according to us for the 1HFY2018,

in spite of the challenges. On EBIT front, the company expects to manage its

margins in 26-28% range over medium term. For FY2018, we have estimated the

EBIT margins of 24.5% V/s 24.6% in 9MFY2018. On sales front, we expect the

company to post a US$ revenue CAGR of 9.3% over FY2017-19E.

Management Rejig: With Mr. Natarajan Chandrasekaran being the Chairman of

Tata Sons since February 21, 2017, CFO Mr. Rajesh Gopinathan has taken charge as

the CEO of the company. He started his professional career with TCS in 2001 and

was appointed as the CFO in February 2013. TCS also announced N G Subramanian

as the COO of the company. Thus, the new targets under the new CEO will have a

bearing on the performance of the company.

Outlook and valuation

Over FY2017-19E, we expect TCS to post revenue CAGR of 9.3% and 7.6% in

USD and INR terms, respectively. The company highlighted that it stands

comfortable in sustaining the EBIT margin in the range of 26-28%. On the EBIT and

PAT fronts, we expect the company to post 5.0% and 4.5% CAGR over FY2017-19E

respectively. The stock is trading at 18.9x FY2019E EPS of `146.6. We maintain our

Reduce recommendation.

Exhibit 10: Key assumptions

FY2018E

FY2019E

Revenue growth (USD)

8.0

11.0

USD-INR rate (realized)

65.0

65.0

Revenue growth (`)

4.6

10.6

EBITDA margin (%)

26.4

26.3

Tax rate (%)

23.5

23.5

EPS growth (%)

0.2

8.9

Source: Company, Angel Research

January 15, 2018

6

TCS | 3QFY2018 Result Update

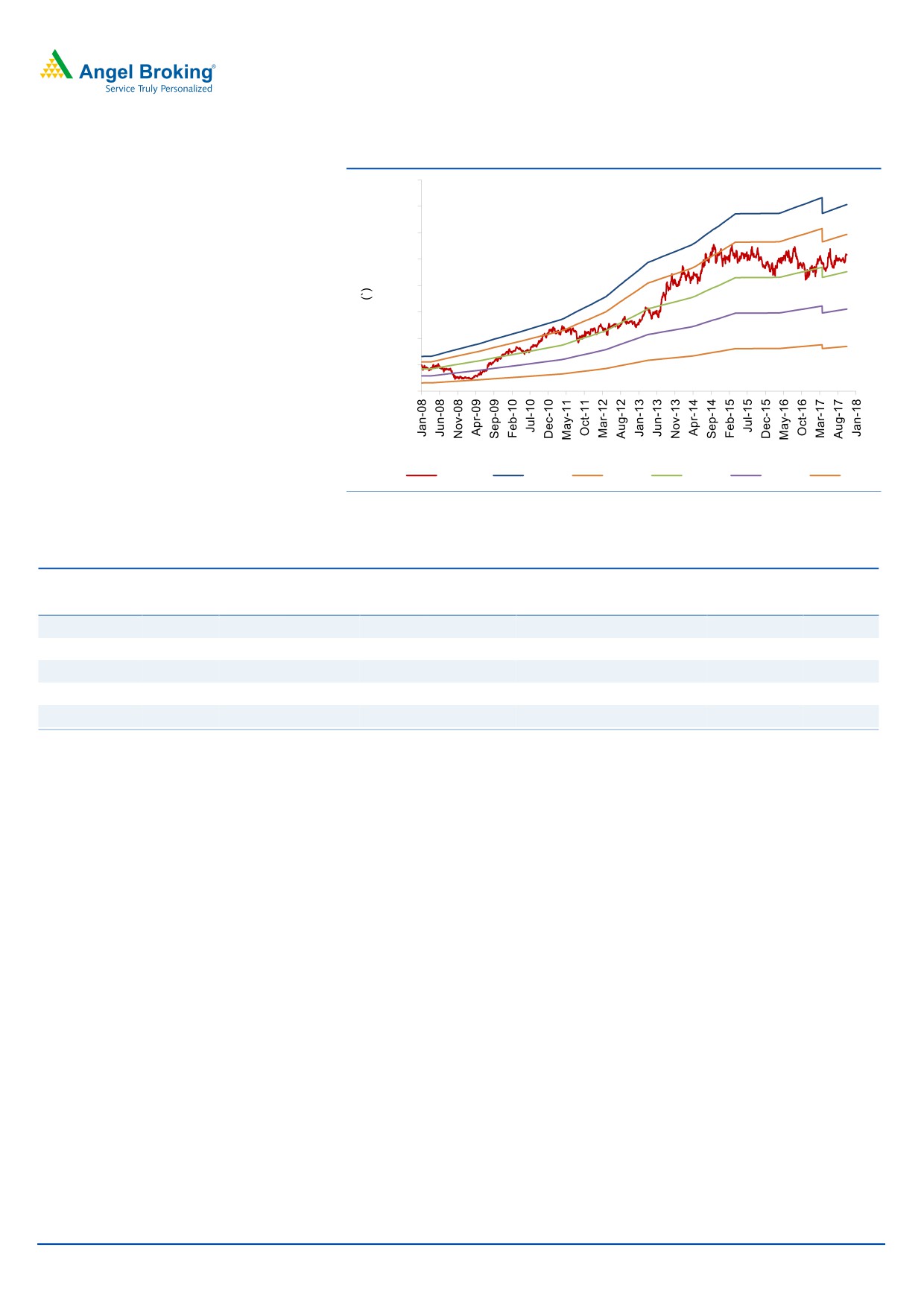

Exhibit 11: One-year forward PE chart

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

Price

25x

21x

16x

11x

6x

Source: Company, Angel Research

Exhibit 12: Recommendation summary

Company

Reco

CMP Tgt. price Upside

FY2019E FY2019E

FY2017-19E

FY2019E FY2019E

(`)

(`)

(%) EBITDA (%)

P/E (x)

EPS CAGR (%) EV/Sales (x)

RoE (%)

HCL Tech

Accumulate

926

1,014

9.6

20.9

13.7

6.2

1.8

20.6

Infosys

Neutral

1,078

-

-

26.0

16.4

5.3

2.1

19.6

TCS

Reduce

2,773

2,493

(10.1)

26.3

18.9

4.5

3.5

28.3

Tech Mahindra Neutral

550

-

-

15.0

14.6

8.6

1.3

16.3

Wipro

Reduce

319

280

(12.2)

20.3

16.3

4.4

1.5

13.4

Source: Company, Angel Research

January 15, 2018

7

TCS | 3QFY2018 Result Update

Company background

TCS is Asia's largest IT services provider and is amongst the top 10 technology firms

in the world. The company has a global footprint with an employee base of over

3lakh professionals, offering services to more than 1,000 clients across various

industry segments. The company has one of the widest portfolios of service

offerings, spanning across the entire IT service value chain - from traditional

application development and maintenance to consulting and package

implementation to products and platforms.

January 15, 2018

8

TCS | 3QFY2018 Result Update

Profit & Loss statement (Consolidated, IFRS)

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E FY2019E

Net sales

94,648

108,646

117,966

123,384

136,504

Cost of revenue

50,599

58,952

64,764

68,478

75,760

Gross profit

44,049

49,695

53,202

54,906

60,744

% of net sales

46.5

45.7

45.1

44.5

44.5

SGA expenses

17,353

18,956

20,755

22,332

24,844

% of net sales

18.3

17.4

17.6

18.1

18.2

EBITDA

26,696

30,738

32,447

32,573

35,901

% of net sales

28.2

28.3

27.5

26.4

26.3

Dep. and amortization

1272

1948

2123

2221

2457

% of net sales

1.3

1.8

1.8

1.8

1.8

EBIT

25,424

28,790

30,324

30,352

33,444

% of net sales

26.9

26.5

25.7

24.6

24.5

Other income, net

3140

3050

4189

4189

4189

Profit before tax

28,564

31,840

34,513

34,541

37,633

Provision for tax

6,083

7,503

8,156

8,117

8,844

% of PBT

21.3

23.6

23.6

23.5

23.5

PAT

22,481

24,338

26,357

26,424

28,789

Minority interest

205

123

68

78

89

Extra-ordinary (Exp.)/ Inc.

-2627.9

Reported PAT

19,648

24,215

26,289

26,346

28,700

Adj. PAT

21,696

24,215

26,289

26,346

28,700

Diluted EPS (`)

110.9

123.7

134.3

134.6

146.6

January 15, 2018

9

TCS | 3QFY2018 Result Update

Balance sheet (Consolidated, IFRS)

Y/E March (` cr)

FY2015 FY2016

FY2017 FY2018E FY2019E

Assets

Cash and cash equivalents

1,862

1,862

3,597.0

3,477.2

3,356.1

Other current financial assets

16,383

4,833

-

-

-

Accounts receivable

20,440

24,073

22,684

31,762

31,812

Unbilled revenues

3,827

3,992

5,351

5,348

5,349

Other current assets

6,414

5,975

7,258

7,258

7,258

Property and equipment

11,572

11,790

11,741

12,741

13,741

Intangible assets and goodwill

3,931

3,946

3,768

3,768

3,768

Investments

9,619

22,822

41,980

39,267

47,133

Other non current assets

906

11,919

8,974

8,974

8,974

Total assets

74,954

91,212

105,353

112,595

121,391

Liabilities

Current liabilities

14,428

15,407

14,294

14,806

16,381

Short term borrowings

243

162

218

218

218

Redeemable preference shares

-

(0)

-

1

2

Long term debt

114

83

71

71

71

Other non current liabilities

1,778

2,017

2,089

2,431

2,689

Minority interest

914

354

366

444

533

Shareholders funds

57,477

73,190

88,315

94,625

101,498

Total liabilities

74,954

91,212

105,353

112,595

121,391

January 15, 2018

10

TCS | 3QFY2018 Result Update

Cash flow statement (Consolidated, IFRS)

Y/E March (` cr)

FY2015 FY2016 FY2017 FY2018E FY2019E

Pre-tax profit from oper.

22,481

24,338

26,357

26,424

28,789

Depreciation

1,272

1,948

2,123

2,221

2,457

Exp. (deferred)/written off

160

174

-

-

-

Pre tax cash from oper

23,913

26,460

28,480

28,645

31,246

Other inc./prior period ad

1,272

1,948

2,123

2,221

2,457

Net cash from operations

25,185

28,408

30,604

30,866

33,703

Tax

6,083

7,503

8,156

8,117

8,844

Cash profits

19,102

20,905

22,448

22,749

24,859

(Inc)/dec in acc. recv.

(2,210)

(3,633)

1,389

(9,078)

(50)

(Inc)/dec in unbilled rev.

179

(165)

(1,359)

3

(1)

(Inc)/dec in oth. current asst.

(6,414)

439

(1,283)

-

-

Inc/(dec) in current liab.

(1,207)

(218)

49

(1,000)

(1,000)

Net trade working capital

(9,652)

(3,577)

(1,204)

(10,074)

(1,051)

Cash flow from opert. actv.

9,450

17,328

21,243

12,674

23,808

(Inc)/dec in fixed assets

(1,207)

(218)

49

(1,000)

(1,000)

(Inc)/dec in investments

(4,446)

(1,653)

(14,325)

2,713

(7,866)

(Inc)/dec in intangible asst.

(226)

16

(178)

-

-

(Inc)/dec in non-cur.asst.

(906)

(11,013)

2,945

-

-

Cash flow from invt. actv.

(6,786)

(12,869)

(11,509)

1,713

(8,866)

Inc/(dec) in debt

61

(113)

44

-

-

Inc/(dec) in minority int.

223

(559)

12

78

89

Dividends

(19,923)

(18,415)

(19,993)

(20,036)

(21,826)

Others

16,976

14,629

10,202

5,571

6,794

Cash flow from finan. actv.

(2,664)

(4,459)

(9,735)

(14,387)

(14,943)

Cash generated/(utilized)

393

-

1,735

(120)

(121)

Cash at start of the year

1,469

1,862

1,862

3,597

3,477

Cash at end of the year

1,862

1,862

3,597

3,477

3,356

January 15, 2018

11

TCS | 3QFY2018 Result Update

Key ratios

Y/E March

FY2015 FY2016 FY2017 FY2018E FY2019E

Valuation ratio(x)

P/E (on FDEPS)

25.0

22.4

20.6

20.6

18.9

P/CEPS

26.0

20.8

19.1

19.0

17.4

P/BVPS

9.4

7.4

6.1

5.7

5.3

Dividend yield (%)

1.6

1.4

1.6

1.6

1.7

EV/Sales

5.3

4.6

4.1

4.0

3.5

EV/EBITDA

18.8

16.3

15.0

15.0

13.4

EV/Total assets

6.7

5.5

4.6

4.3

4.0

Per share data (`)

EPS

110.9

123.7

134.3

134.6

146.6

Cash EPS

106.8

133.6

145.1

145.8

159.1

Dividend

43.5

40.2

43.6

43.7

47.6

Book value

294

374

451

483

519

DuPont analysis

Tax retention ratio (PAT/PBT)

0.8

0.8

0.8

0.8

0.8

Cost of debt (PBT/EBIT)

1.1

1.1

1.1

1.1

1.1

EBIT margin (EBIT/Sales)

0.3

0.3

0.3

0.2

0.2

Asset turnover ratio (Sales/Assets)

1.3

1.2

1.1

1.1

1.1

Leverage ratio (Assets/Equity)

1.3

1.2

1.2

1.2

1.2

Operating ROE

39.1

33.3

29.8

27.9

28.4

Return ratios (%)

RoCE (pre-tax)

33.9

31.6

28.8

27.0

27.6

Angel RoIC

54.0

46.7

50.7

43.5

47.2

RoE

34.2

33.1

29.8

27.8

28.3

Turnover ratios(x)

Asset turnover (fixed assets)

8.2

9.2

10.0

9.7

9.9

Receivables days

79

81

70

94

85

January 15, 2018

12

TCS | 3QFY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits

and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

TCS

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

January 15, 2018

13