4QFY2017 Result Update | Pharmaceutical

June 12, 2017

Lupin

BUY

CMP

`1,161

Performance Highlights

Target Price

`1,526

Y/E March

% chg

Investment Period

12 months

4QFY2017

3QFY2017

% chg qoq

4QFY2016

(`cr)

yoy

Net sales

4,162

4,410

(5.6)

4,109

1.3

Sector

Pharmaceutical

Other income

137

182

(24.7)

123

10.9

Market Cap (` cr)

52,424

Operating

690

1,143

(39.6)

1,226

(43.7)

Net Debt (` cr)

8,165

profit

Interest

41

46

(11.6)

31

30.8

Beta

0.7

Net profit

380

633

(40.0)

748

(49.2)

52 Week High / Low

1,750 / 1,080

Source: Company, Angel Research

Avg. Daily Volume

97,284

Face Value (`)

2

For 4QFY2017, Lupin posted results which were much below expectations mainly

BSE Sensex

31,262

on OPM and the net profit front. The revenues came in at `4,162cr v/s.

`4,338cr, a yoy growth of 1.3%. On the OPM front, the EBDITA margins came in

Nifty

9,668

at 16.6% (v/s. 25.7% expected) v/s. 31.2% in 4QFY2016. Thus, the Adj. PAT

Reuters Code

LUPN.BO

during the quarter came in at `380.3cr v/s. `748cr expected a yoy dip of 49.2%.

Bloomberg Code

LPC@IN

Given the valuations, we maintain our Buy rating on the stock.

Numbers lower than expectations: The revenues came in at `4,162cr v/s.

Shareholding Pattern (%)

`4,338cr, a yoy growth of 1.3%. The sales were impacted on the back of the

Promoters

46.7

USA (`1901cr), a yoy dip of 13.2%. On the OPM front, the EBDITA margins

MF / Banks / Indian Fls

10.5

came in at 16.6% (v/s. 25.7% expected) v/s. 31.2% in 4QFY2016. While the

FII / NRIs / OCBs

32.6

Gross margins came in at 71.5% v/s. 73.8%, a yoy rise of 24.4%, 31.3% and

Indian Public / Others

10.3

37.7% in the employee, R&D and other expenses respectively lead to the higher

than expected contraction in the OPM. Net impact of foreign exchange

fluctuation on EBITDA was a loss of `168cr during 4QFY2017 as compared to a

Abs. (%)

3m 1yr 3yr

gain of `26.7cr during 4QFY2016 and a gain of `27.6cr during 3QFY2017.

Sensex

8.1

16.8

22.2

Also, the company made a provision for liability towards its Australian subsidiary

Lupin

(19.9)

(18.7)

21.3

amounting to `155.9cr, in respect of compensation for patent litigation towards

its Isabelle generic launch in Australia. Thus, the Adj. PAT during the quarter

came in at `380.3cr v/s. `748cr expected, a yoy dip of 49.2%.

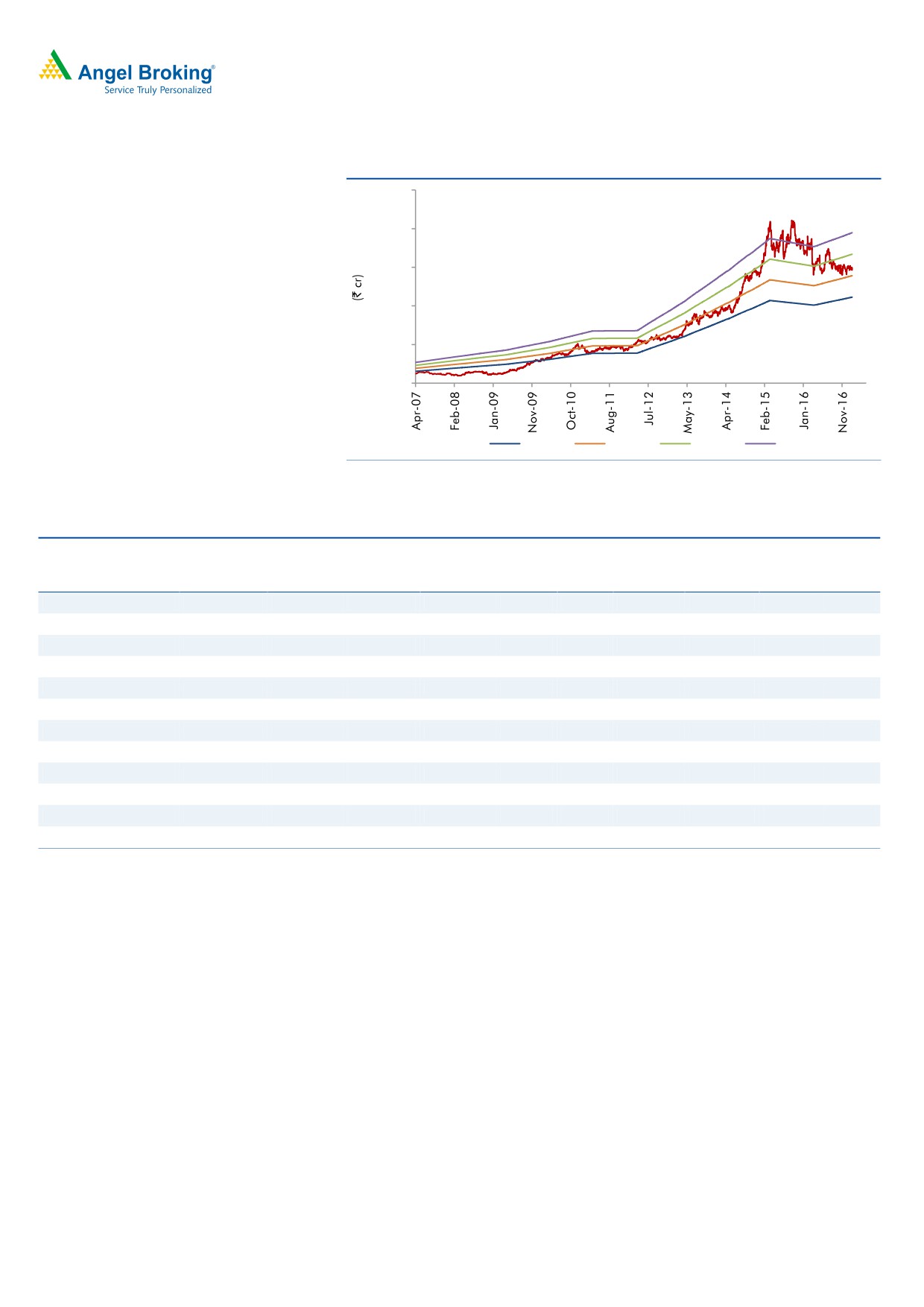

3-year price chart

2,300

Outlook and valuation: We expect Lupin to post a net sales CAGR of 11.5% to

2,100

`21,289cr and earnings CAGR of 10.4% to `69.3/share over FY2017-19E.

1,900

Currently, the stock is trading at 16.7x its FY2019E earnings respectively. We

1,700

1,500

recommend a Buy rating on the stock.

1,300

1,100

Key financials (Consolidated)

900

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

700

Net sales

13,702

17,120

18,657

21,289

500

% chg

8.7

24.9

9.0

14.1

Net profit

2,271

2,557

2,748

3,117

% chg

-5.5

12.6

7.4

13.4

Source: Company, Angel Research

EPS (`)

50.5

56.9

61.1

69.3

EBITDA margin (%)

23.7

24.1

24.1

24.1

P/E (x)

23.0

20.4

19.0

16.7

RoE (%)

22.7

20.7

18.6

17.8

Sarabjit Kour Nangra

RoCE (%)

19.4

15.5

17.1

20.6

+91 22 3935 7600 Ext: 6806

P/BV (x)

4.7

3.9

3.2

2.7

EV/sales (x)

4.2

3.5

2.8

2.3

EV/EBITDA (x)

17.9

14.4

11.8

9.8

Source: Company, Angel Research; Note: CMP as of June 9, 2017

Please refer to important disclosures at the end of this report

1

Lupin | 4QFY2017 Result Update

Exhibit 1: 4QFY2017 - Consolidated performance

Y/E March (` cr)

4QFY2017

3QFY2017

% chg (qoq)

4QFY2016

% chg (yoy)

FY2017

FY2016

% chg (yoy)

Net sales

4,162

4,410

(5.6)

4,109

1.3

17,120

13,758

24.4

Other income

137

182

(24.7)

123

10.9

481

683

(29.6)

Total income

4,232

4,591

(7.8)

4,232

0.0

17,601

14,441

21.9

Gross profit

2,977

3,108

(4.2)

3,008

12,118

9,425

28.6

Gross margin

71.5

70.5

73.2

70.8

68.5

Operating profit

690.0

1,142.7

(39.6)

1,226.3

(43.7)

4,119

3,188

29.2

OPM (%)

16.6

25.9

29.8

24.1

23.2

Interest

41

46

(11.6)

31

30.8

153

59

156.5

Dep. & amortization

267

231

15.8

149

79.8

912

487

87.3

PBT

519

1,047

(50.5)

1,170

(55.7)

3,535

3,324

6.3

Provision for taxation

137

409

(66.6)

419

(67.4)

979

1,059

(7.6)

Reported net profit

382

638

(40.1)

751

(49.1)

2,556

2,265

12.9

Less : exceptional items

-

-

-

-

-

MI & share in associates

2

5

(54.0)

3

(33.1)

(1)

4

-

PAT after exceptional

380

633

(40.0)

748

(49.2)

2,557

2,261

13.1

items

EPS (`)

16.7

14.1

57.0

57.0

50.5

Source: Company, Angel Research

Exhibit 2: 4QFY2017 - Actual Vs Angel estimates

` cr

Actual

Estimates

Variation

Net Sales

4,162

4,000

4.0

Other Income

137

106

28.5

Operating Profit

690

895

(22.9)

Deprecation

267

202

32.4

Tax

137

153

(10.4)

Net Profit

380

637

(40.4)

Source: Company, Angel Research

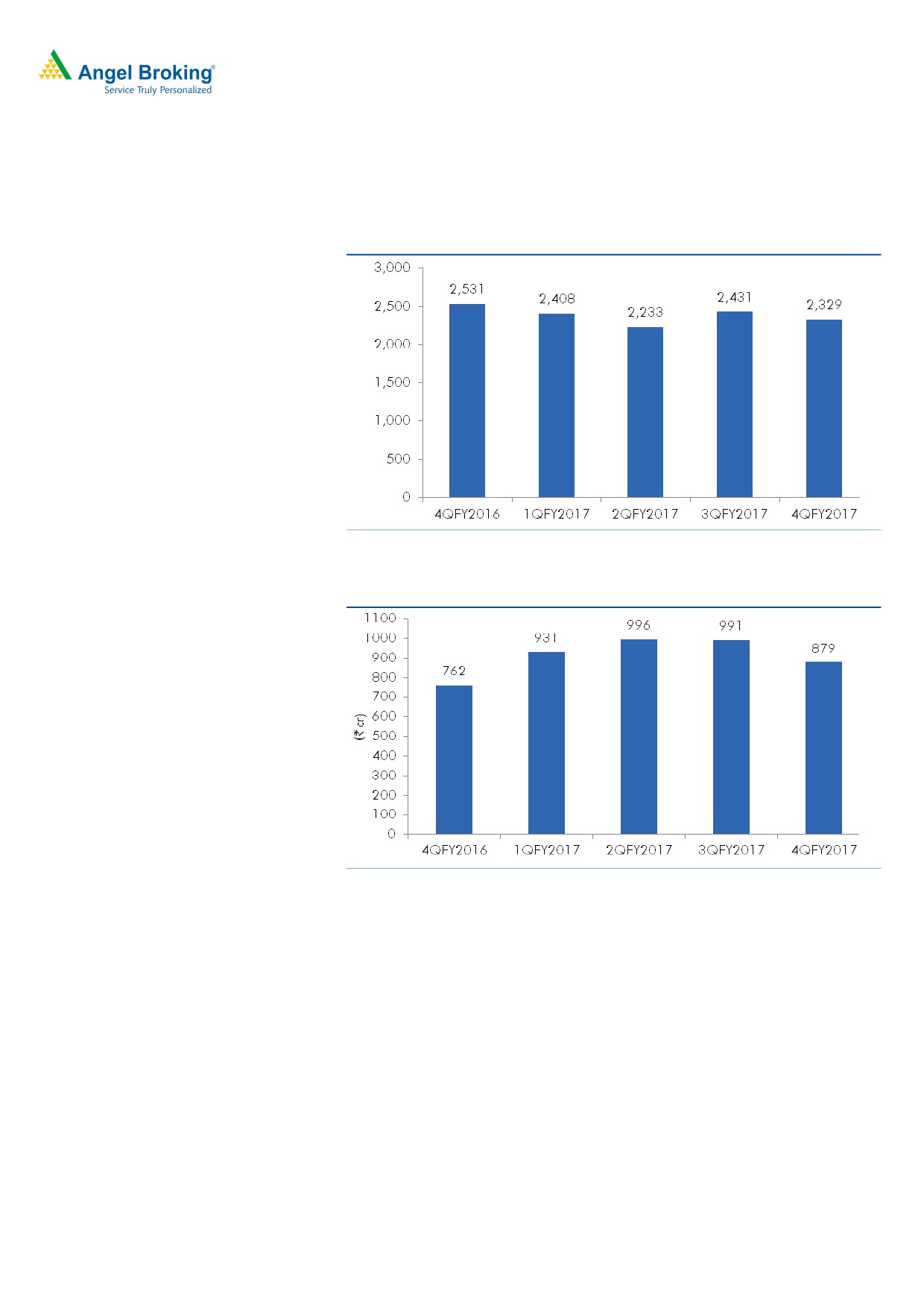

Revenue grows 1.3% yoy: The revenues came in at `4,162cr v/s. `4,338cr, a yoy

growth of 1.3%. The sales were impacted on the back of the USA (`1901cr), a yoy

dip of 13.2%. Other significant markets like India posted (`878.8cr), a yoy growth

of 13.8%, APAC (`612cr), a yoy growth of 35%, EMEA (‘301.2cr), a yoy growth of

22.8%, LATAM (`126.9cr), a yoy growth of 37.3%.

The USA (which contributed around 46%), registered a yoy de-growth of 13.2%.

India at `878.8cr, posted yoy growth of 13.8%, APAC at `612cr, posted a yoy

growth of 35%, EMEA at `301cr, posted a yoy growth of 22.8%, LATAM at

`126.9cr, posted a yoy growth of 37.3% and ROW at `61.0cr posted, a yoy

growth of 0.7%.

Lupin’s USA sales de-grew by

13.2% to

`1900.7cr during 4QFY2017,

contributing 46% of Lupin’s global sales. The Company launched 9 products in the

US market during the quarter. The Company now has 139 products in the US

generics market. Lupin is now the leader in 45 products marketed in the US

generics market and amongst the top 3 in 83 of its marketed products (market

share by prescriptions, IMS Health, March 2017).

June 12, 2017

2

Lupin | 4QFY2017 Result Update

Lupin’s India formulation sales grew by 13.8% to `878.8cr during 4QFY2017, as

compared to `772.2cr during 4QFY2016, contributing 21% of Lupin’s global

sales. API sales (`281.5cr) posted a dip of 4.7% yoy.

Exhibit 3: Advanced markets - Sales trend

Source: Company, Angel Research

Exhibit 4: Domestic Formulation Market

Source: Company

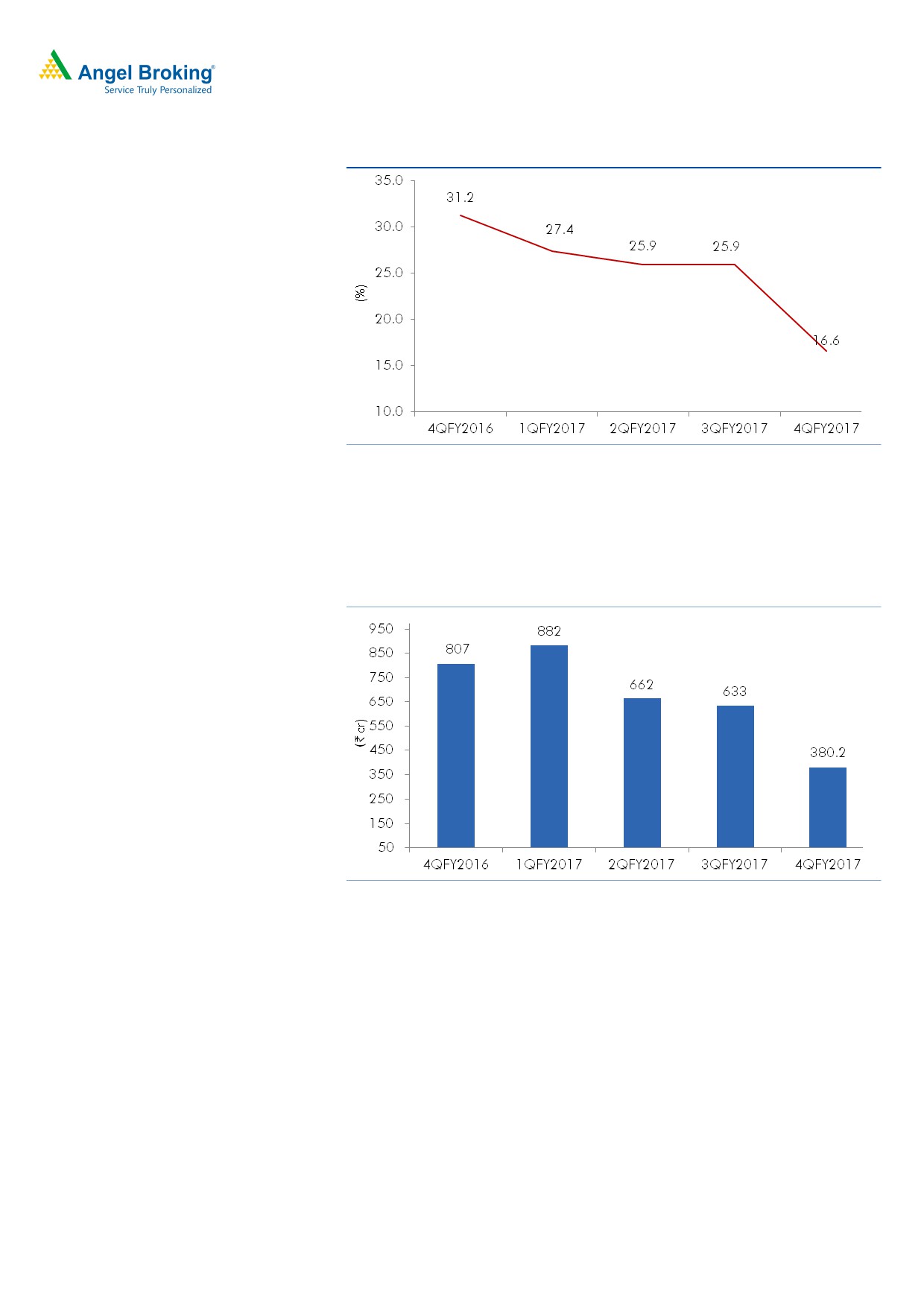

OPM at 16.6%, lower than expected: On the OPM front, the EBDITA margins

came in at 16.6% (v/s. 25.7% expected) v/s. 31.2% in 4QFY2016. While the Gross

margins came in at 71.5% v/s. 73.8%, a yoy rise of 24.4%, 31.3% and 37.7% in

the employee, R&D and other expenses lead to the higher than expected

contraction in the OPM. Net Impact of foreign exchange fluctuation on EBITDA

was a loss of `1,68cr during 4QFY2017 as compared to a gain of `26.7cr during

4QFY2016 and a gain of `27.6cr during 3QFY2017.

Also, the company made a provision for liability towards its Australian subsidiary

amounting to `155.9cr, in respect of compensation for patent litigation towards its

Isabelle generic launch in Australia. These aided the contraction in the OPM. R&D

expense stood at 16% of sales, higher than the normalized rate of 12-13%. Thus,

normalized EBDITA margins came in at ~25%.

June 12, 2017

3

Lupin | 4QFY2017 Result Update

Exhibit 5: OPM trend

Source: Company, Angel Research

Net profit growth lower than estimate: The Adj. PAT during the quarter came in at

`380.3cr v/s. `710.6cr expected, a yoy dip of 49.2%. Contraction in OPM along

with higher deprecation aided the Adj. net profit to de-grow by 49.2% yoy.

Exhibit 6: Net profit trends

Source: Company, Angel Research

Conference call takeaways

Management has guided for 30+ ANDA launches in FY2018.

R&D expense as % of sales to be in-line with FY2017.

14 FTF launches expected over the next five years.

US Branded business sales at US$78m in FY2017.

Management has guided for muted growth in FY18E due to pricing pressure.

With the company having huge pipeline of products to be launched in

FY2019E onwards, it expects growth to bounce back to double digits in

FY2019E and targeted revenues of US$3.5bn FY2020E onwards.

EBDITA Margins are expected to be in the range of 26-28%.

June 12, 2017

4

Lupin | 4QFY2017 Result Update

Recommendation rationale

US market - the key driver: The high-margin branded generic business has

been the key differentiator for Lupin in the Indian pharmaceuticals space. On

the generic turf, Lupin is currently the fifth largest generic player in the US,

with 5.3% market share in prescription. Lupin is now the market leader in 45

products marketed in the US generics market and is amongst the top 3 by

market share in 83 products. Currently, the company’s cumulative filings stand

at 368, of which 214 have been approved, with 23 exclusive FTFs. Lupin plans

to launch 25-30 products in the US in FY2018. We expect the region to post a

CAGR of 9.9% over FY2017-19E on the back of new product launches.

Domestic formulations on a strong footing: Lupin continues to make strides in

the Indian market. Currently, Lupin ranks No 3, and is the fastest growing

company among the top five companies in the domestic formulation space,

registering a strong CAGR of 20% over the last few years. Six of Lupin's

products are among the top 300 brands in the country. Lupin has a strong

field force of ~6,000MRs (as of FY2016). We expect the domestic formulation

market to grow at a CAGR of 16.0% over FY2017-19E.

First-mover advantage in Japan: Lupin figures among the few Indian

companies with a formidable presence in Japan, the world’s second largest

pharma market (Lupin was ranked as the 8th largest as per IMS MAT March

2014). The Management believes that there will be patent expiries (US$14-

16bn) in the next two years in the Japanese market, which along with

increased generic penetration would drive growth in the market. The

Management expects improvement in growth in the next 3-4 years. On a

conservative basis, we expect the Japan market to post a CAGR of 20% over

FY2017-19E.

Valuation

We expect Lupin to post a net sales CAGR of 11.5% to `21,284cr and earnings

CAGR of 10.4% to `69.3/share over FY2017-19E. Currently, the stock is trading

at 16.7x its FY2019E earnings, respectively. We recommend a Buy rating on the

stock.

Exhibit 7: Key Assumptions

FY2018E

FY2019E

Sales growth (%)

9.0

14.1

Domestic growth (%)

16.0

16.0

Exports growth (%)

7.8

13.5

Operating margins (%)

24.1

24.1

R&D Exp ( % of sales)

12.0

12.0

Capex (` cr)

1000

1000

Source: Company, Angel Research

June 12, 2017

5

Lupin | 4QFY2017 Result Update

Exhibit 8: One-year forward PE

2,500

2,000

1,500

1,000

500

-

20x

25x

30x

35x

Source: Company, Angel Research

Exhibit 9: Recommendation summary

Company

Reco

CMP

Tgt. price

Upside

FY2018E

FY16-18E

FY2018E

EV/Sale

EV/EBITDA

CAGR in

RoCE

(`)

(`)

(%)

PE (x)

RoE (%)

(x)

(x)

EPS (%)

(%)

Alembic Pharma

Buy

552

648

17.3

21.7

2.5

12.0

(10.8)

27.5

25.3

Aurobindo Pharma

Buy

609

823

35.2

13.6

2.2

9.9

18.1

22.5

26.1

Cadila Healthcare

Sell

541

450

(16.8)

28.4

4.8

23.8

(0.5)

16.2

24.6

Cipla

Sell

550

465

(15.5)

22.4

2.5

15.2

14.2

12.2

13.9

Dr Reddy's

Neutral

2,631

-

-

24.8

2.9

15.8

(13.7)

10.8

13.6

Dishman Pharma

Under Review

301

-

-

26.6

2.9

12.7

16.3

13.0

13.5

GSK Pharma*

Neutral

2,463

-

-

49.7

6.2

38.4

6.0

22.3

21.3

Indoco Remedies

Sell

193

153

(20.7)

17.1

1.7

11.7

6.3

10.1

15.0

Ipca labs

Buy

501

710

41.7

25.8

1.8

12.6

13.9

10.4

9.5

Lupin

Buy

1,161

1,526

31.5

19.0

2.7

11.4

10.0

20.6

17.8

Sanofi India

Neutral

4,051

-

-

29.0

3.3

19.8

16.8

22.5

26.4

Sun Pharma

Buy

525

712

35.7

16.6

3.5

12.9

1.2

16.9

18.7

Source: Company, Angel Research; Note: * December year ending

June 12, 2017

6

Lupin | 4QFY2017 Result Update

Company Background

Lupin, established in 1968, is primarily engaged in the manufacture and global

distribution of active pharmaceutical ingredients (APIs) and finished dosages. Over

the years, the company forayed into the US markets through a differentiated export

strategy of tapping branded generics and consequently gaining a large share of

the US prescription market. Further, to expand its footprint in the global markets,

Lupin has prudently adopted the inorganic growth route. In-line with this, over the

last two years, the company made small acquisitions across geographies,

prominent among these being the acquisition of Kyowa in the growing Japanese

market. In the US, the company has acquired privately held Gavis Pharmaceuticals

LLC and Novel Laboratories Inc. The acquisitions have enhanced Lupin’s scale in

the US generic market and have also broadened its pipeline in dermatology,

controlled substance products and other high-value and niche generics.

June 12, 2017

7

Lupin | 4QFY2017 Result Update

Profit & Loss Statement (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

FY2018E

FY2019E

Gross sales

11,167

12,684

13,797

17,224

18,770

21,417

Less: Excise duty

80

84

96

104

113

129

Net sales

11,087

12,600

13,702

17,120

18,657

21,289

Other operating income

200

170

507

375

375

375

Total operating income

11,287

12,770

14,208

17,494

19,032

21,663

% chg

17.1

13.1

11.3

23.1

8.8

13.8

Total expenditure

8,284

9,150

10,455

13,001

14,169

16,167

Net raw materials

3,817

4,157

4,309

5,001

5,451

6,219

Other mfg costs

847

963

1,047

1,308

1,426

1,627

Personnel

1,465

1,747

2,108

2,850

3,105

3,543

Other

2,155

2,283

2,580

3,842

4,187

4,778

EBITDA

2,803

3,449

3,247

4,119

4,488

5,122

% chg

34.1

23.1

-5.9

26.9

9.0

14.1

(% of Net Sales)

25.3

27.4

23.7

24.1

24.1

24.1

Dep. & Amortization

261

435

464

912

1,002

1,122

EBIT

2,542

3,015

2,783

3,206

3,486

3,999

% chg

44.6

18.6

-7.7

15.2

8.7

14.7

(% of Net Sales)

22.9

23.9

20.3

18.7

18.7

18.8

Interest & other charges

27

10

45

153

153

153

Other Income

116

240

188

107

107

107

(% of PBT)

4

7

5

3

3

2

Share in profit of asso.

Recurring PBT

2,832

3,415

3,433

3,535

3,815

4,328

% chg

47.1

20.6

0.5

3.0

7.9

13.4

Extraordinary exp./(Inc.)

-

-

-

-

-

-

PBT (reported)

2,832

3,415

3,433

3,535

3,815

4,328

Tax

962

970

1,154

979

1,068

1,212

(% of PBT)

34.0

28.4

33.6

27.7

28.0

28.0

PAT (reported)

1,870

2,444

2,279

2,556

2,747

3,116

Add: Share of earnings of asso.

-

-

-

-

-

-

Less: Minority interest (MI)

33

41

9

(1)

(1)

(1)

Prior period items

-

-

-

-

-

-

PAT after MI (reported)

1,836

2,403

2,271

2,557

2,748

3,117

ADJ. PAT

1,836

2,403

2,271

2,557

2,748

3,117

% chg

39.7

30.9

-5.5

12.6

7.4

13.4

(% of Net Sales)

16.6

19.1

16.6

14.9

14.7

14.6

Basic EPS (`)

41.0

53.5

50.5

56.9

61.1

69.3

Fully Diluted EPS (`)

41.0

53.5

50.5

56.9

61.1

69.3

% chg

39.5

30.5

-5.5

12.6

7.4

13.4

June 12, 2017

8

Lupin | 4QFY2017 Result Update

Balance Sheet (Consolidated)

Y/E March

FY2014

FY2015

FY2016

FY2017

FY2018E

FY2019E

SOURCES OF FUNDS

Equity share capital

90

90

90

90

90

90

Reserves & surplus

6,842

8,784

11,073

13,407

15,987

18,935

Shareholders funds

6,932

8,874

11,163

13,497

16,076

19,025

Minority interest

67

24

32

35

33

32

Total loans

553

471

7,119

7,952

1,500

500

Other Long-Term

46

74

75

76

77

78

Liabilities

Long-Term Provisions

132

132

592

836

836

836

Deferred tax liability

178

118

(9)

(113)

(113)

(113)

Total liabilities

7,908

9,693

18,973

22,283

18,410

20,359

APPLICATION OF

FUNDS

Gross block

4,564

5,355

6,853

7,853

8,853

9,853

Less: Acc. Depreciation

1,928

2,363

2,827

3,739

4,741

5,863

Net block

2,635

2,992

4,026

5,047

4,112

3,989

Capital work-in-

304

304

304

304

304

304

progress

Goodwill

720

1,648

7,089

7,815

7,815

7,815

Investments

178

1,658

16

2,136

2,136

2,136

Long-Term Loans and

373

275

968

957

1,318

1,504

Adv.

Current assets

5,924

6,176

9,885

9,840

7,701

10,288

Cash

798

1,306

822

699

489

2,059

Loans & advances

302

671

737

912

994

1,134

Other

4,825

4,199

8,326

8,229

6,218

7,095

Current liabilities

2,227

3,360

3,316

3,816

4,975

5,677

Net current assets

3,697

2,816

6,570

6,024

2,726

4,611

Mis. Exp. not written off

-

-

-

-

-

-

Total assets

7,908

9,693

18,973

22,283

18,410

20,359

June 12, 2017

9

Lupin | 4QFY2017 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

FY2018E

FY2019E

Profit before tax

2,832

3,415

3,433

3,535

3,815

4,328

Depreciation

261

435

464

912

1,002

1,122

(Inc)/Dec in working

(1,481)

1,487

(4,931)

434

2,727

(501)

capital

Direct taxes paid

(962)

(970)

(1,154)

(979)

(1,068)

(1,212)

Cash Flow from

649

4,367

(2,188)

3,903

6,476

3,737

Operations

(Inc.)/Dec.in Fixed Assets

(443)

(791)

(1,498)

(1,000)

(1,000)

(1,000)

(Inc.)/Dec. in Investments

-

-

-

-

-

-

Cash Flow from Investing

(443)

(791)

(1,498)

(1,000)

(1,000)

(1,000)

Issue of equity

-

-

-

-

-

-

Inc./(Dec.) in loans

(611)

(82)

6,648

833

(6,452)

(1,000)

Dividend Paid (Incl. Tax)

(157)

(168)

(168)

(168)

(168)

(168)

Others

926

(2,816)

(3,278)

(3,689)

935

-

Cash Flow from Financing

157

(3,067)

3,202

(3,024)

(5,685)

(1,168)

Inc./(Dec.) in Cash

363

509

(484)

(122)

(209)

1,569

Opening Cash balances

435

798

1,306

822

699

489

Closing Cash balances

798

1,306

822

699

489

2,059

June 12, 2017

10

Lupin | 4QFY2017 Result Update

Key Ratios

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

FY2018E

FY2019E

Valuation Ratio (x)

P/E (on FDEPS)

28.3

21.7

23.0

20.4

19.0

16.7

P/CEPS

24.8

18.4

19.1

15.0

13.9

12.3

P/BV

7.5

5.9

4.7

3.9

3.2

2.7

Dividend yield (%)

0.5

0.7

0.7

0.7

0.7

0.7

EV/Sales

4.7

4.1

4.2

3.5

2.8

2.3

EV/EBITDA

18.4

14.9

17.9

14.4

11.8

9.8

EV / Total Assets

6.5

5.3

3.1

2.7

2.9

2.5

Per Share Data (`)

EPS (Basic)

41.0

53.5

50.5

56.9

61.1

69.3

EPS (fully diluted)

41.0

53.5

50.5

56.9

61.1

69.3

Cash EPS

46.8

63.1

60.8

77.2

83.4

94.3

DPS

6.0

8.0

8.0

8.0

8.0

8.0

Book Value

154.6

197.4

248.3

300.3

357.7

423.3

Dupont Analysis

EBIT margin

22.9

23.9

20.3

18.7

18.7

18.8

Tax retention ratio

66.0

71.6

66.4

72.3

72.0

72.0

Asset turnover (x)

1.7

1.6

1.1

0.9

1.0

1.2

ROIC (Post-tax)

25.4

28.2

14.4

11.9

13.0

16.2

Cost of Debt (Post

2.0

1.4

0.8

1.5

2.3

11.0

Tax)

Leverage (x)

0.0

0.0

0.0

0.4

0.1

-0.1

Operating ROE

25.4

28.2

14.4

16.4

14.0

15.9

Returns (%)

ROCE (Pre-tax)

34.7

34.3

19.4

15.5

17.1

20.6

Angel ROIC (Pre-tax)

44.1

48.2

32.4

26.5

30.0

40.0

ROE

30.3

30.4

22.7

20.7

18.6

17.8

Turnover ratios (x)

Asset Turnover (Gross

2.6

2.6

2.3

2.4

2.3

2.3

Block)

Inventory / Sales

66

62

74

74

61

55

(days)

Receivables (days)

75

66

79

79

64

58

Payables (days)

84

78

82

70

80

85

WC cycle (ex-cash)

89

63

93

116

73

40

(days)

Solvency ratios (x)

Net debt to equity

(0.0)

(0.1)

0.6

0.5

0.1

(0.1)

Net debt to EBITDA

(0.1)

(0.2)

1.9

1.8

0.2

(0.3)

Interest Coverage

95.4

307.3

62.4

21.0

22.9

26.2

June 12, 2017

11

Lupin | 4QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

June 12, 2017

12