2QFY2018 Result Update | Pharmaceutical

November 20, 2017

GlaxoSmithKline Pharmaceuticals

SELL

Performance Highlights

CMP

`2,511

Target Price

`2,000

Y/E Mar (` cr)

2QFY2018

1QFY2018

% chg (QoQ) 2QFY2017

% chg (YoY)

Net Sales

Investment Period

12 months

836

607

37.7

799

4.6

Other income

15

34

(56.5)

18

(19.0)

Stock Info

Gross profit

460

316

45.6

438

5.0

Sector

Pharmaceutical

Operating profit

192

(1)

-

141

36.5

Market Cap (` cr)

21,272

Net Debt (` cr)

(936)

Adj. PAT

127

18

615.6

99

28.5

Beta

0.2

Source: Company, Angel Research

52 Week High / Low

3,343/2,309

A vg. Daily V olum e

2,050

GlaxoSmithKline Pharmaceuticals (GSK) posted better than expected results on

Face Value (`)

10

sales and OPM fronts for 2QFY2018. The revenues came in at `836cr v/s. `800r

BSE Sensex

33,343

Nifty

10,284

expected, registering a yoy growth of 4.6%, mainly on the back of GST

Reuters Code

GLAX.BO

implementation. On the OPM front, the EBDITA margins came in at 23.0% (v/s.

Bloomberg Code

GLXO@IN

15.3% expected) as compared to 17.6% in 2QFY2017, mainly driven by lower

expenses during the quarter. The Adj. PAT came in at `127cr v/s. `99cr in

Shareholding Pattern (%)

2QFY2017, a yoy growth of 28.5%. We recommend a Sell.

Promoters

75.0

MF / Banks / Indian Fls

10.9

F II / NRIs / OCB s

2.1

Results better than expectations: GlaxoSmithKline Pharmaceuticals (GSK)

Indian P ublic / Others

12.0

posted better than expected results on sales and OPM fronts for 2QFY2018. The

revenues came in at `836cr v/s. `800r expected, registering a yoy growth of 4.6%,

Abs. (%)

3m 1yr

3yr

mainly on the back of GST implementation. On the OPM front, the EBDITA

Sensex

4.2

24.2

15.6

Glaxo

(0.2)

(11.5)

(16.6)

margins came in at 23.0% (v/s. 15.3% expected) as compared to 17.6% in

2QFY2017, mainly driven by lower expenses during the quarter. The Adj. PAT

came in at `127cr v/s. `99cr in 2QFY2017, a yoy growth of 28.5%.

Outlook and valuation: On the operational front, we expect the company’s net sales

to post a CAGR of 6.6% to `3,324cr, while the EPS is expected to post a CAGR of 16.1%

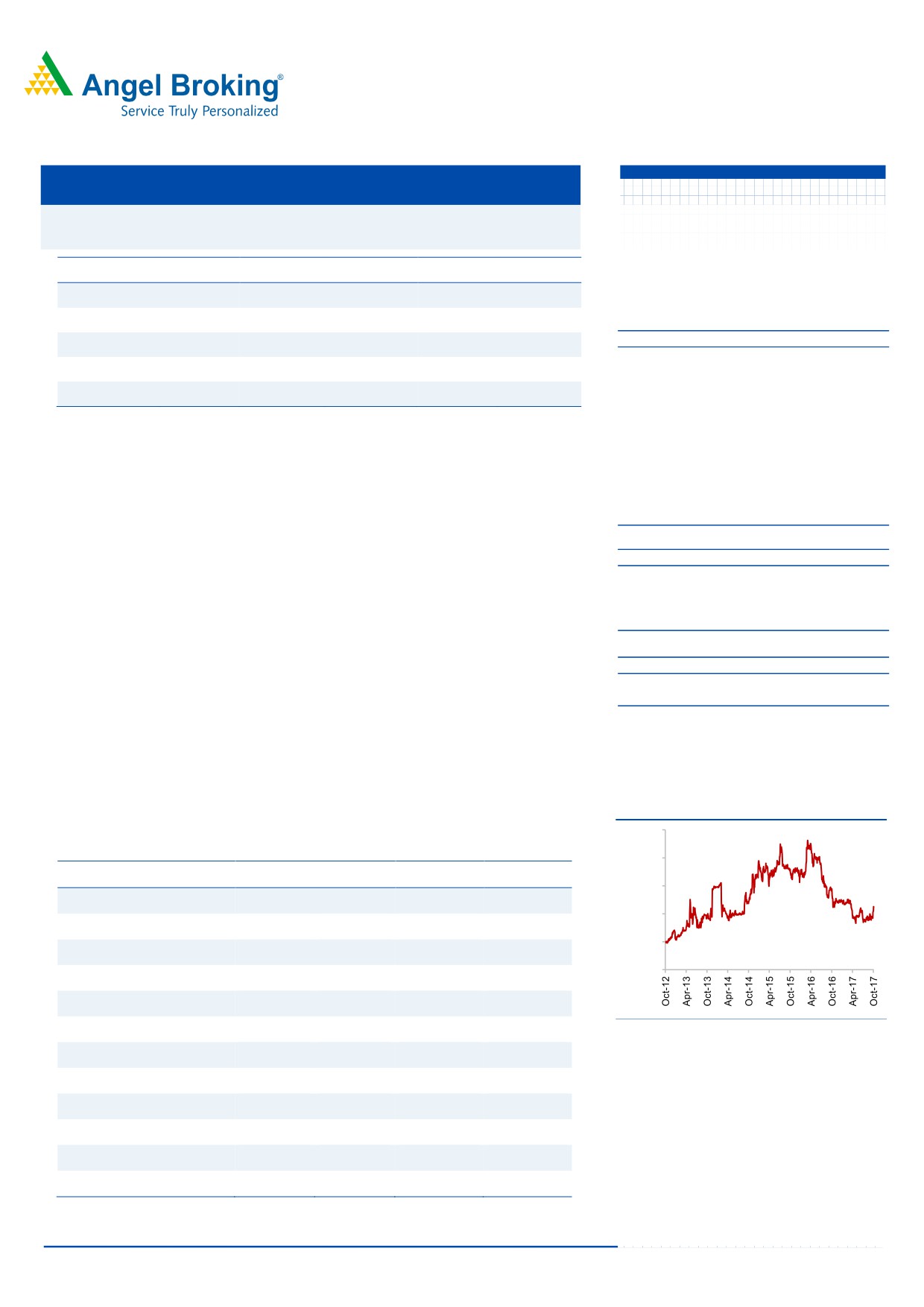

3-year price chart

over FY2017-19E. We recommend a Sell on the stock.

4,000

Key financials (Consolidated)

3,500

Y/E Mar (` cr)

FY2016

FY2017

FY2018E

FY2019E

3,000

2,741

2,927

2,968

3,324

Net sales

2,500

(16.2)

6.8

1.4

12.0

% chg

2,000

374

291

320

414

Net profit

1,500

(26.5)

(22.2)

9.9

29.5

% chg

44.2

34.4

37.8

48.9

EPS (`)

16.5

11.8

13.8

16.9

EBITDA (%)

Source: Company, Angel Research

56.8

73.1

66.5

51.4

P/E (x)

18.7

13.9

16.7

23.5

RoE (%)

Sarabjit Kour Nangra

19.4

14.0

17.0

25.8

RoCE (%)

+91 22 39357800 Ext: 6806

9.7

10.6

11.6

12.6

P/BV (x)

7.3

7.0

7.0

6.4

EV/Sales (x)

44.0

58.9

50.5

37.7

EV/EBITDA (x)

Source: Company, Angel Research; Note: CMP as of November 17, 2017

Please refer to important disclosures at the end of this report

1

Glaxo Pharma | 2QFY2018 Result Update

Exhibit 1: 2QFY2018 - Standalone performance

Y/E March (` cr)

2QFY2018

1QFY2018

% chg (QoQ)

2QFY2017

% chg (YoY) 1HFY2018 1HFY2017

% chg

Net Sales

836

587

42.5

799

4.6

1,423

1,468

(3.1)

Other income

15

34

(56.5)

18

(19.0)

49

78

(37.5)

Total Income

851

621

37.1

817

4.1

1,472

1,546

(4.8)

Gross profit

460

316

45.6

438

5.0

776

792

(2.1)

Gross margin

55.0

53.8

54.8

54.5

54.0

Operating profit

192

(1)

141

36.5

191

195

(1.8)

Operating margin (%)

23.0

(0.1)

17.6

13.5

13.3

Interest

0

0

-

0

-

0

0

-

Depreciation & Amortization

8

8

2.8

7

17.5

15

12

27.1

PBT & Exceptional Items

199

26

671.2

152

30.7

225

261

(13.8)

Less : Exceptional Items

0

13

-

0

-

13

3

Profit before tax

199

38

417.8

153

30.6

238

265

(10.3)

Provision for taxation

69

12

496.8

54

28.5

80

92

(12.7)

Reported PAT

130

26

393.3

99

31.7

157

171

(8.4)

Adj. Net profit

127

18

615.6

99

28.5

145

170

(14.6)

EPS (`)

15.0

2.1

11.7

17.1

20.1

Source: Company, Angel Research,

Exhibit 2: 2QFY2018 - Actual v/s. Angel estimates

(` cr)

Actual

Estimates

Variation (%)

Net sales

836

800

4.5

Other income

15

15

0.0

Operating profit

192

122

56.9

Tax

69

8

793.6

Adj. net profit

127

86

47.7

Source: Company, Angel Research

Revenue grew by 4.6% yoy

GlaxoSmithKline Pharmaceuticals (GSK) posted lower than expected results on sales

and OPM fronts for 2QFY2018. The revenues came in at `836cr v/s. `800cr expected,

registering a yoy growth of 4.6%, mainly on the back of GST implementation.

Furthermore, the deflation in revenue by estimated 6% during the quarter was

predominately profit neutral, and was a result of the impact of the newly

implemented GST rates.

November 20, 2017

2

Glaxo Pharma | 2QFY2018 Result Update

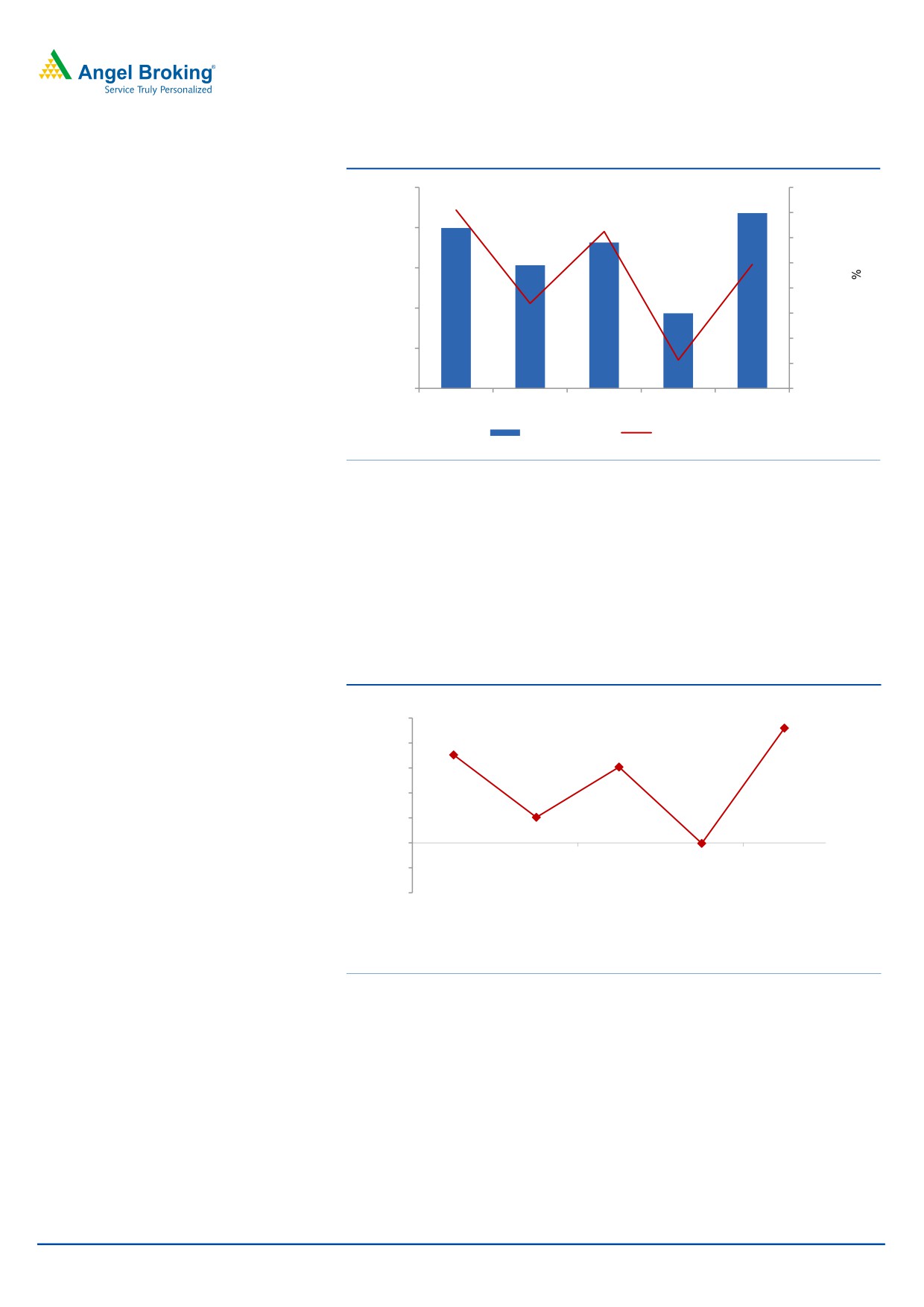

Exhibit 3: Sales trend

900

20.0

836

799

15.0

800

763

10.0

706

5.0

700

0.0

587

600

(5.0)

(10.0)

500

(15.0)

400

(20.0)

2QFY2017

3QFY2017

4QFY2017

1QFY2018

2QFY2018

Sales

Growth (YoY)

Source: Company, Angel Research

OPM better than expected on the back of lower other expenses

On the OPM front, the EBDITA margins came in at 23.0% (v/s. 15.3% expected) as

compared to 17.6% in 2QFY2017. This was mainly driven by sales growth during

the quarter. The Gross margins were almost flat at 55.0% in 2QFY2018 v/s. 54.8% in

2QFY2017. Employee expenses and other expenses grew by 6.8% and

-22.3%

respectively.

Exhibit 4: OPM trend(%)

25.0

17.6

23.0

20.0

15.2

15.0

10.0

5.1

5.0

(0.1)

0.0

(5.0)

(10.0)

2QFY2017

3QFY2017

4QFY2017

1QFY2018

2QFY2018

Source: Company, Angel Research

Net profit much higher than estimated

The Adj. PAT during the quarter came in at `127cr v/s. `99cr in 2QFY2017, a yoy

growth of 28.5%. The reported profit came in at `130cr v/s. `99cr, a yoy growth of

31.7%. Also, during the quarter, the company posted other income of `15cr v/s.

`18cr in 2QFY2017.

November 20, 2017

3

Glaxo Pharma | 2QFY2018 Result Update

Exhibit 5: Adjusted net profit trend(`cr)

150

127

99

100

87

50

41

18

0

2QFY2017

3QFY2017

4QFY2017

1QFY2018

2QFY2018

Source: Company, Angel Research

November 20, 2017

4

Glaxo Pharma | 2QFY2018 Result Update

Recommendation rationale

Renewed focus on the Indian market: GSK is among the top ten players in the

Indian pharmaceutical market, having a market share of 3.7%. Unlike other MNCs,

the company has been amongst the few which have taken initiatives to grow their

businesses in the Indian market with consistent launch of new products.

Over the last six years, the company has strategically decided to expand its

presence in the Specialty segment. The Specialty segment’s contribution to sales

has reached 23% (as of 2013). Another segment which is strong for the company is

the area of vaccines, where GSK Vaccines has become the leading company in the

private market for vaccines in India. The recently introduced vaccine for

pneumococcal conjugate disease, Synflorix, has become the biggest brand in the

vaccine portfolio of the company in the second year of its launch. The efforts of the

company in raising awareness about vaccines and preventable diseases continue

with increasing fervor. Also, in FY2015, GlaxoSmithKline Plc (Glaxo), London, UK,

entered into three inter-conditional agreements with Novartis AG (Novartis), Basel,

Switzerland. In one such agreement, Glaxo agreed to acquire Novartis’ vaccines

business (excluding influenza vaccine) and its manufacturing capabilities and

facilities, and in the second agreement, Glaxo agreed to sell the rights of its

Marketed Oncology Portfolio, related R&D activities and AKT Inhibitors currently in

development to Novartis. Globally, these transactions with Novartis were

completed on March 2, 2015.

On the other hand, its other key segments like mass markets and mass specialty,

which contribute 60% of its sales, de-grew by 12% in CY2013. This was as a result

of a number of products of the company having come under the DPCO 2013 ruling,

resulting in reduction in prices of its drugs, which impacted its sales in CY2013.

Along with this, the supply constraints, mainly from local supplies during FY2015,

have been impacting its performance. FY2017 was another year, where the

company’s, sales got impacted on the back of the government’s pricing cuts.

Overall, for FY2017-19E, we expect the domestic formulation business of the

company to grow at a CAGR of 6.6%.

Significant capex plans ahead indicate revival in growth: Global pharmaceutical

major Glaxo announced

`864cr investment in India to set up a medicine

manufacturing unit. The new facility will substantially increase the company’s

manufacturing base. The drug maker is proactively building capacity in the country

as it delivers its portfolio of products in areas such as gastroenterology and anti-

inflammatory medicines. When complete, the factory will make pharmaceutical

products for the Indian market at a rate of up to 8bn tablets and 1bn capsules a

year. The facility will include a warehouse, site infrastructure, and utilities to support

the manufacturing and packing of medicines. It showcases GSK's latest

commitment to its manufacturing network in India where the company has invested

`1,017cr over the last decade. The development is positive and comes after a long

lull in terms of investments.

November 20, 2017

5

Glaxo Pharma | 2QFY2018 Result Update

Outlook and valuation

GSK has a strong balance sheet with cash of ~`900cr, which could be used for future

acquisitions or higher dividend payouts. The company’s parent company Glaxo

increased stake in it through a voluntary open offer, after which Glaxo holds 75%

stake in the Indian subsidiary. The buy-back of shares is a strong indicator from the

Management towards the performance of its listed Indian entity, especially as it

comes after the recent `864cr investment plan announced by the company to

further its growth prospects in the Indian pharmaceuticals market. The said

investments are expected to fructify by 2018.

On the operational front, we expect the company’s net sales to post a CAGR of 6.6%

to `3,324cr and EPS to register a CAGR of 19.3% to `48.9 over FY2017-19E. At the

current level, the stock is trading at 66.5x and 51.4x its FY2018E and FY2019E

earnings respectively. We recommend a Sell on the stock.

Exhibit 6: Key assumptions

FY2018E

FY2019E

Sales growth (%)

1.4

12.0

Growth in employee expenses (%)

11.0

9.0

Operating margin (%)

13.8

15.9

Capex (` cr)

200

200

Source: Company, Angel Research

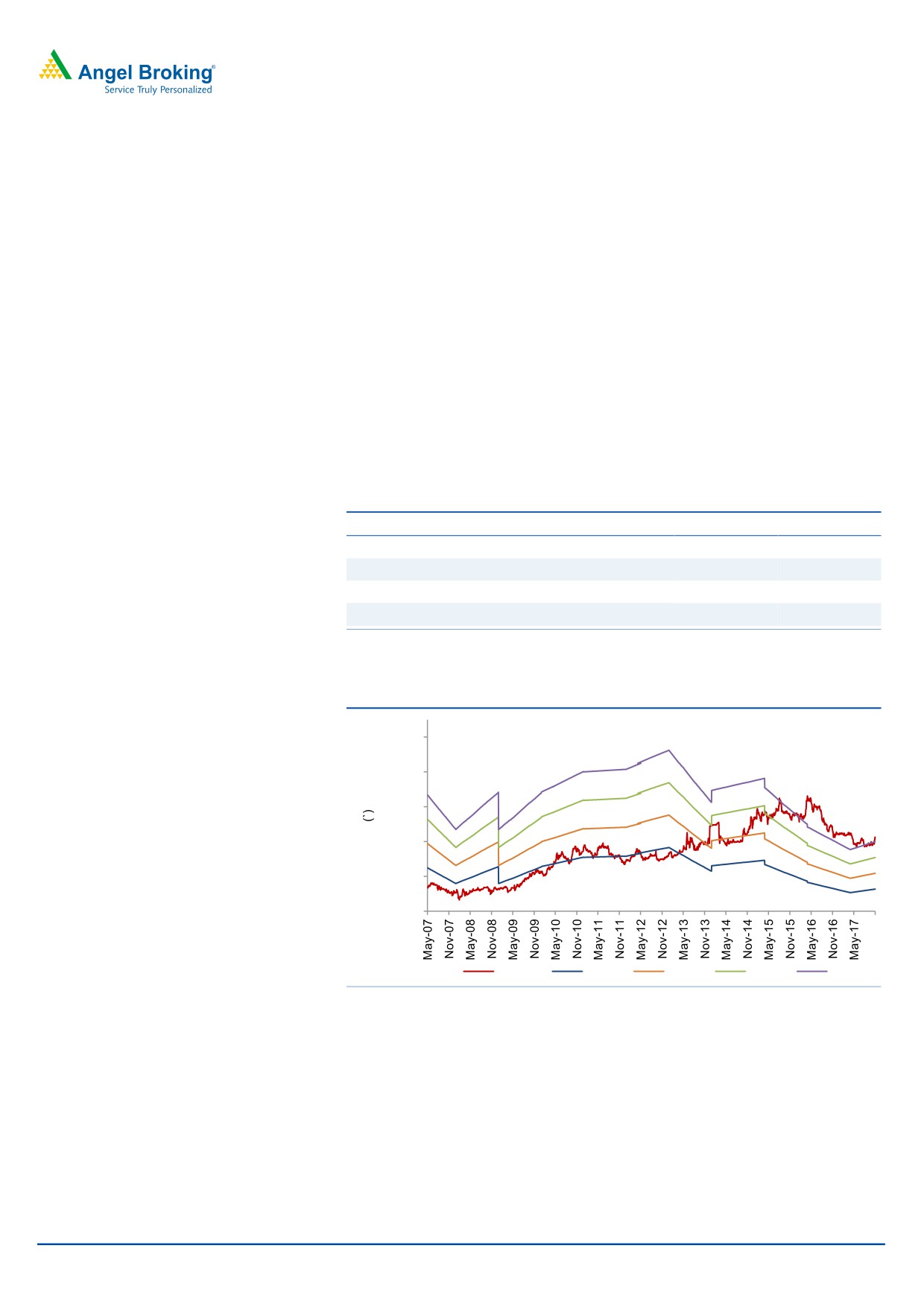

Exhibit 7: One-year forward PE

5,500

4,500

3,500

2,500

1,500

500

Price

18x

30x

42x

54x

Source: Company, Angel Research

November 20, 2017

6

Glaxo Pharma | 2QFY2018 Result Update

Exhibit 8: Recommendation summary

Company

Reco

CMP Tgt. price Upside

FY2019E

FY17-19E

FY2019E

PE

EV/Sales

EV/EBITDA

RoCE

RoE

(`)

(`)

%

CAGR in EPS (%)

(x)

(x)

(x)

(%)

(%)

Alembic Pharma

Buy

514

600

16.8

21.5

2.5

12.9

5.7

20.6

18.4

Aurobindo Pharma

Buy

708

823

16.3

13.8

2.1

9.6

14.2

25.3

22.7

Cadila Healthcare

Reduce

446

411

(7.9)

21.7

3.5

17.3

18.9

16.5

22.2

Cipla

Sell

609

426

(24.1)

25.0

2.7

16.0

39.3

10.9

13.1

Dr Reddy's

Reduce

2,325

2,040

(12.3)

22.8

2.8

13.7

18.5

10.8

12.4

Dishman Pharma

Under Review

301

-

-

19.3

2.7

11.5

23.3

4.5

4.4

GSK Pharma

Sell

2,511

2000

(20.4)

51.4

6.4

37.7

19.3

25.8

23.5

Indoco Remedies

Sell

267

153

(42.8)

16.7

2.1

14.9

16.2

10.1

14.5

Ipca labs

Neutral

529

-

-

22.1

1.7

11.2

24.7

12.4

11.0

Lupin

Buy

829

1,091

31.6

16.7

2.1

9.7

(6.6)

13.7

13.7

Sanofi India*

Neutral

4,485

-

-

27.4

3.2

17.1

12.8

25.8

27.5

Sun Pharma

Accumulate

517

558

7.9

20.9

3.5

15.4

(12.9)

12.3

15.2

Source: Company, Angel Research; Note: * December year ending;

November 20, 2017

7

Glaxo Pharma | 2QFY2018 Result Update

Company Background

GlaxoSmithKline Pharmaceuticals (GSK) is the sixth largest pharmaceutical player in

the Indian market with a market share of ~3.7%. The company’s product portfolio

includes both, prescription medicines and vaccines. GSK sells prescription

medicines across therapeutic areas such as anti-infectives, dermatology,

gynecology, diabetes, oncology, cardiovascular diseases and respiratory diseases.

A large portion of the company’s revenue comes from the acute therapeutic

portfolio. However, the company is now scouting for opportunities in high-growth

therapeutic areas such as CVS, CNS, diabetes and oncology. Further, with a strong

parentage, the company plans to increase its product portfolio through patented

launches and vaccines. To fructify the same, the company plans to enhance its

manufacturing assets with its parent company investing `864cr in it; the capacity

expansion is expected to fructify in 2017.

November 20, 2017

8

Glaxo Pharma | 2QFY2018 Result Update

Profit & loss statement

Y/E March (` cr)

CY2013

FY2015

FY2016

FY2017 FY2018E FY2019E

Gross sales

2,589

3,328

2,800

2,999

3,029

3,392

Less: Excise duty

51

56

59

72

61

68

Net sales

2,538

3,272

2,741

2,927

2,968

3,324

Other operating income

24

32

27

28

28

28

Total operating income

2,563

3,305

2,768

2,954

2,996

3,352

% chg

(3.3)

28.9

(16.2)

6.7

1.4

11.9

Total expenditure

2,034

2,690

2,289

2,581

2,559

2,763

Net raw materials

1,164

1,510

1,233

1,398

1,336

1,463

Other Mfg costs

89

115

99

107

111

115

Personnel

362

493

443

483

490

532

Other

420

572

514

593

623

654

EBITDA

504

582

452

346

409

561

% chg

(33.6)

15.5

(22.4)

(23.5)

18.4

37.1

(% of Net Sales)

19.9

17.8

16.5

11.8

13.8

16.9

Depreciation& amortization

20

25

25

26

52

60

EBIT

484

557

427

319

357

501

% chg

(34.7)

15.0

(23.3)

(25.2)

11.8

40.3

(% of Net Sales)

19.1

17.0

15.6

10.9

12.0

15.1

Interest & other charges

-

-

-

-

-

1

Other income

177

200

125

119

100

100

(% of PBT)

Share in profit of Associates

-

-

-

-

-

-

Recurring PBT

685

789

579

465

485

627

% chg

(27.5)

15.1

(26.5)

(19.7)

4.1

29.5

Extraordinary expense/(Inc.)

(26)

33

(3)

(46)

-

-

PBT (reported)

711

756

582

511

485

627

Tax

230

279

203

174

165

213

(% of PBT)

32.3

36.9

34.8

34.1

34.0

34.0

PAT (reported)

482

477

377

337

320

414

Add: Share of earnings

-

-

-

-

-

-

of asso.

Less: Minority interest (MI)

-

-

-

-

-

-

Prior period items

-

-

-

-

-

-

Exceptional items

PAT after MI (reported)

482

477

377

337

320

414

ADJ. PAT

464

509

374

291

320

414

% chg

(29.4)

9.8

(26.5)

(22.2)

9.9

29.5

(% of Net Sales)

18.3

15.6

13.7

9.9

10.8

12.5

Basic EPS (`)

55

60

44

34

38

49

Fully diluted EPS (`)

55

60

44

34

38

49

% chg

(29.4)

9.8

(26.5)

(22.2)

9.9

29.5

November 20, 2017

9

Glaxo Pharma | 2QFY2018 Result Update

Balance Sheet

Y/E March (` cr)

CY2013

FY2015

FY2016

FY2017

FY2018E FY2019E

SOURCES OF FUNDS

Equity share capital

85

85

85

85

85

85

Preference Capital

-

-

-

-

-

-

Reserves& surplus

1,905

1,744

2,099

1,922

1,747

1,606

Shareholders funds

1,990

1,829

2,183

2,007

1,831

1,690

Minority Interest

Total loans

4

3

1

2

-

-

Other long-term liabilities

5

5

-

-

-

-

Long-term provisions

242

273

291

276

276

276

Deferred tax liability

(92)

(83)

(101)

(92)

(92)

(92)

Total liabilities

2,148

2,026

2,374

2,193

2,015

1,875

APPLICATION OF FUNDS

Gross block

323

467

725

1,105

1,305

1,505

Less: Acc. Depreciation

247

272

297

323

375

436

Net block

76

195

428

782

930

1,070

Capital work-in-progress

44

44

44

44

44

44

Goodwill

42

-

-

32

32

32

Other non-current assets

14

-

-

-

-

-

Long-term loans and adv.

238

307

302

374

386

432

Investments

10

0

5

6

6

6

Current assets

2,614

2,587

2,174

1,674

1,348

1,109

Cash

2,042

1,911

1,392

932

596

112

Loans & advances

238

122

123

132

134

150

Other

335

554

658

610

619

848

Current liabilities

889

1,107

579

720

731

819

Net current assets

1,725

1,480

1,595

954

617

290

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

2,148

2,026

2,374

2,193

2,015

1,875

November 20, 2017

10

Glaxo Pharma | 2QFY2018 Result Update

Cash flow statement

Y/E March (` cr)

CY2013

FY2015

FY2016

FY2017 FY2018E FY2019E

Profit before tax and exceptional

711

756

582

511

485

627

Depreciation

20

25

25

26

52

60

(Inc)/Dec in working capital

15

114

(633)

181

1

(157)

Direct taxes paid

230

279

203

174

165

213

Cash Flow from Operations

517

616

(229)

544

373

317

(Inc.)/Dec.in fixed assets

(49)

(144)

(258)

(381)

(200)

(200)

(Inc.)/Dec. in investments

(45)

(10)

5

1

-

-

Cash Flow from Investing

(93)

(154)

(253)

(380)

(200)

(200)

Issue of equity

-

-

-

-

-

-

Inc./(Dec.) in loans

-

-

-

-

-

-

Dividend paid (Incl. Tax)

(495)

(624)

(495)

(297)

(495)

(555)

Others

47

32

459

-

-

-

Cash Flow from Financing

(448)

(593)

(37)

(297)

(495)

(555)

Inc./(Dec.) in cash

(25)

(131)

(519)

(460)

(336)

(484)

Opening cash balances

2,067

2,042

1,911

1,392

932

596

Closing cash balances

2,042

1,911

1,392

932

596

112

November 20, 2017

11

Glaxo Pharma | 2QFY2018 Result Update

Key ratio

Y/E March

CY2013

FY2015

FY2016

FY2017

FY2018E FY2019E

Valuation Ratio (x)

P/E (on FDEPS)

45.8

41.8

56.8

73.1

66.5

51.4

P/CEPS

42.4

42.4

53.0

58.6

57.2

44.8

P/BV

10.7

11.6

9.7

10.6

11.6

12.6

Dividend yield (%)

2.0

2.0

2.0

1.2

2.0

2.3

EV/Sales

7.6

5.9

7.3

7.0

7.0

6.4

EV/EBITDA

38.2

33.3

44.0

58.9

50.5

37.7

EV / Total Assets

9.0

9.6

8.4

9.3

10.3

11.3

Per Share Data (`)

EPS (Basic)

54.8

60.1

44.2

34.4

37.8

48.9

EPS (fully diluted)

54.8

60.1

44.2

34.4

37.8

48.9

Cash EPS

59.2

59.3

47.4

42.9

43.9

56.0

DPS

50.0

50.0

50.0

30.0

50.8

56.8

Book Value

234.9

215.9

257.8

236.9

216.2

199.6

Returns (%)

RoCE (Pre-tax)

22.4

26.7

19.4

14.0

17.0

25.8

Angel ROIC (Pre-tax)

22.4

26.7

19.4

14.0

17.0

25.8

RoE

23.2

26.7

18.7

13.9

16.7

23.5

Turnover ratios (x)

Asset Turnover (Gross Block)

8.6

8.4

4.6

3.2

2.5

2.4

Inventory / Sales (days)

48

40

59

52

41

29

Receivables (days)

15

11

15

14

11

8

Payables (days)

54

55

77

43

49

48

WC cycle (ex-cash) (days)

79

69

96

94

91

95

Solvency ratios (x)

Net debt to equity

(1.0)

(1.0)

(0.6)

(0.5)

(0.3)

(0.1)

Net debt to EBITDA

(4.0)

(3.3)

(3.1)

(2.7)

(1.5)

(0.2)

Interest Coverage (EBIT / Int.)

-

-

-

-

-

-

November 20, 2017

12

Glaxo Pharma | 2QFY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits

and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Glaxo Pharma

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 20, 2017

13