IPO Note | Pharmaceuticals

April 26, 2016

Thyrocare Technologies

NEUTRAL

Issue Open: April 27, 2016

IPO Note - Not much upside

Issue Close: April 29, 2016

Thyrocare Technologies is one of the leading diagnostic chains in India with

Issue Details

market share of ~3% amongst organised players. The core business of the

Face Value: `10

company is diagnostic testing (~97.1% of sales as on 9MFY2016) while the

company through its wholly owned subsidiary also operates imaging centres.

Present Eq. Paid up Capital: `53.7cr

Fresh Issue**: NA

A differentiated model enables higher margins: Unlike other organized players,

which operate more on a B2C model, Thyrocare is more of a B2B player with

Offer for sale: 1.07cr Shares

~85% of its revenues coming through the channel (as against 30-40% for its

Post Eq. Paid up Capital: `53.1cr

peers). This enables the company to keep its other expenditure lower vis-a-vis its

Market Lot: 33 Shares

peers, which spend higher on promotional expenses. In terms of services, the

company is more focused on the preventive & wellness, and the non-preventive

Issue (amount): `451-479cr

segments, while its peers follow a portfolio model of providing a full range of tests

Price Band: `420-446

and services, which entail higher manpower costs. The company’s operations are

Post-issue implied mkt. cap `2,256cr*-

relatively more automated in nature, thereby requiring less manpower

2,396cr**

intervention, unlike its peers which need to employ qualified manpower like Phds

Note:*at Lower price band and **Upper price band

and doctors. As a result, employee costs for Thyrocare account for 10% of sales

V/s 20% of sales for its peers. This contributes towards the company enjoying

Book Building

better margins compared to the industry (~41% for Thyrocare’s diagnostic

QIBs

50%

business V/s ~26% for Dr Lal Pathlabs). We believe, over the medium term the

company would be able to sustain its margins and also scale up its business,

Non-Institutional

15%

given the opportunities in the industry. This coupled with the low capex

Retail

35%

requirement for the diagnostic segment makes its diagnostic business a high

ROIC business.

Post Issue Shareholding Pattern(%)

Outlook and Valuation: The company is valued at a P/E multiple of 42.3-44.9x its

Promoters Group

64.0

FY2016E annualised EPS at the lower and upper end of the issue price band. This

MF/Banks/Indian

compares with a P/E multiple of 61.9x FY2016E EPS for Dr Lal Pathlabs. Although

FIs/FIIs/Public & Others

36.0

the issue seems to be priced at a discount to Dr Lal Pathlabs, we believe that

Thyocare’s consolidated ROIC will come under pressure in the near term as it has

entered the molecular imaging space by acquiring Nuclear Healthcare Ltd (NHL).

According to the company, this business will take 3-4 years to attain peak

profitability while it accounts for almost 40% of its fixed assets of the company (as

on 9MFY2016). Thus, though Thyrocare could potentially provide listing gains, the

pressure on its ROIC in the near term and the not-so cheap valuation demanded by

it will keep the upside in the stock limited. We are Neutral on the issue.

Key Financials

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

Net Sales

109

134

150

183

% chg

44.2

23.1

11.7

22.0

Net Profit

35

45

46

44

Sarabjit Kour Nangra

% chg

53.5

28.3

3.0

(3.7)

+91 22 3935 7800 Ext: 6806

EPS (`)

6.5

8.3

8.6

8.3

EBITDA Margin (%)

42.6

44.7

43.3

34.7

Milan Desai

RoE (%)

41.1

34.1

25.2

18.5

+91 22 4000 3600 Ext: 6846

RoCE (%)

33.3

29.4

24.5

15.8

Source: Company, Angel Research; Note: FY2015 numbers are consolidated and rest standalone

Please refer to important disclosures at the end of this report

1

Thyrocare Technologies | IPO Note

Company background

Thyrocare is among the leading diagnostic chains. It conducts an array of medical

diagnostic tests that center on early detection and management of disorders and

diseases. The company operates its testing services through a fully-automated

central processing laboratory (CPL) in Navi Mumbai, which acts as a hub to

branches. The company has recently expanded its operations to include a network

of five regional processing laboratories (RPLs). Out of these, four RPLs were set up

in 2015 (one each in New Delhi, Coimbatore, Hyderabad, and Kolkata) while it

set up one in Bhopal in 2016.

The company as of February 29, 2016, had a network of 1,041 authorized service

providers (ASPs), comprising of 687 Thyrocare Aggregators (TAGs) and

354

Thyrocare Service Providers (TSPs) spread across 466 cities, 24 states and one

union territory. These ASPs operate under a franchise agreement with the company

and deliver samples directly to one of the RPLs or to one of the 22 hub locations if

the sample is to be processed at the CPL.

As of February 29, 2016, it offered 198 tests and 59 profiles of tests to detect a

number of disorders. Its profiles of tests include 16 tests administered under its

“Aarogyam” brand, which offers patients a suite of wellness and preventive health

care tests. In terms of revenue, Wellness & Preventive Healthcare tests account for

~50% of the revenue (of which thyroid tests account for 20% and the balance 30%

are accounted by non-thyroid tests).

The company’s wholly owned subsidiary, NHL, operates a network of molecular

imaging centers in New Delhi, Navi Mumbai and Hyderabad which focus on early

and effective cancer monitoring.

Issue details

The issue is an offer for sale by Promoters and Non-Promoters of 1.07cr equity

shares aggregating to `479cr at the upper end of the price band. The issue

constitutes 20% of the paid-up equity share capital of the company. Since it is an

offer for sale, the company will not receive any proceeds from the sale of shares.

Exhibit 1: Shareholding pattern

Particulars

Pre-Issue

Post-Issue

No. of shares

(%)

No. of shares

(%)

Promoter group

34,898,981

65.0

34,361,745

64.0

Others

18,824,552

35.0

19,361,788

36.0

Total

53,723,533

100.0

53,723,533

100.0

Source: Company, Angel Research

April 26, 2016

2

Thyrocare Technologies | IPO Note

Industry

The domestic diagnostic market is highly fragmented and has a current size

of ~US$6.2bn. The industry is expected to grow at

16-18% CAGR to

~US$9.3-$9.8bn by FY2018 as per CRISIL estimates.

Diagnostic centres in India can be classified as hospital-based, diagnostic chains

and standalone centres. Standalone centres form the majority share

(48%)

followed by hospital based (37%) centres, while diagnostic chains account for the

balance (15%). The absence of stringent regulations and low entry barriers has led

to the evolution of standalone centres, while hospitals tend to have their own

pathology labs. Within diagnostic chains, large pan-India chains form 35-40% and

regional chains form 60-65%.

Specialized tests require expensive infrastructure, which has led to the formation of

diagnostic chains in India. These follow the hub and spoke model and enable

economies of scale. However, the fragmented nature of the industry indicates low

pricing power for service providers in the near term.

The key drivers for the industry are- increase in evidence-based treatments, huge

demand-supply gap, increase in health insurance coverage, need for greater

health coverage as population and life expectancy increase, rising income levels

making quality healthcare services affordable, and growing demand for lifestyle

diseases-related healthcare services.

Key investment rational

One of the leading players in the high growth market with

strong drivers in place

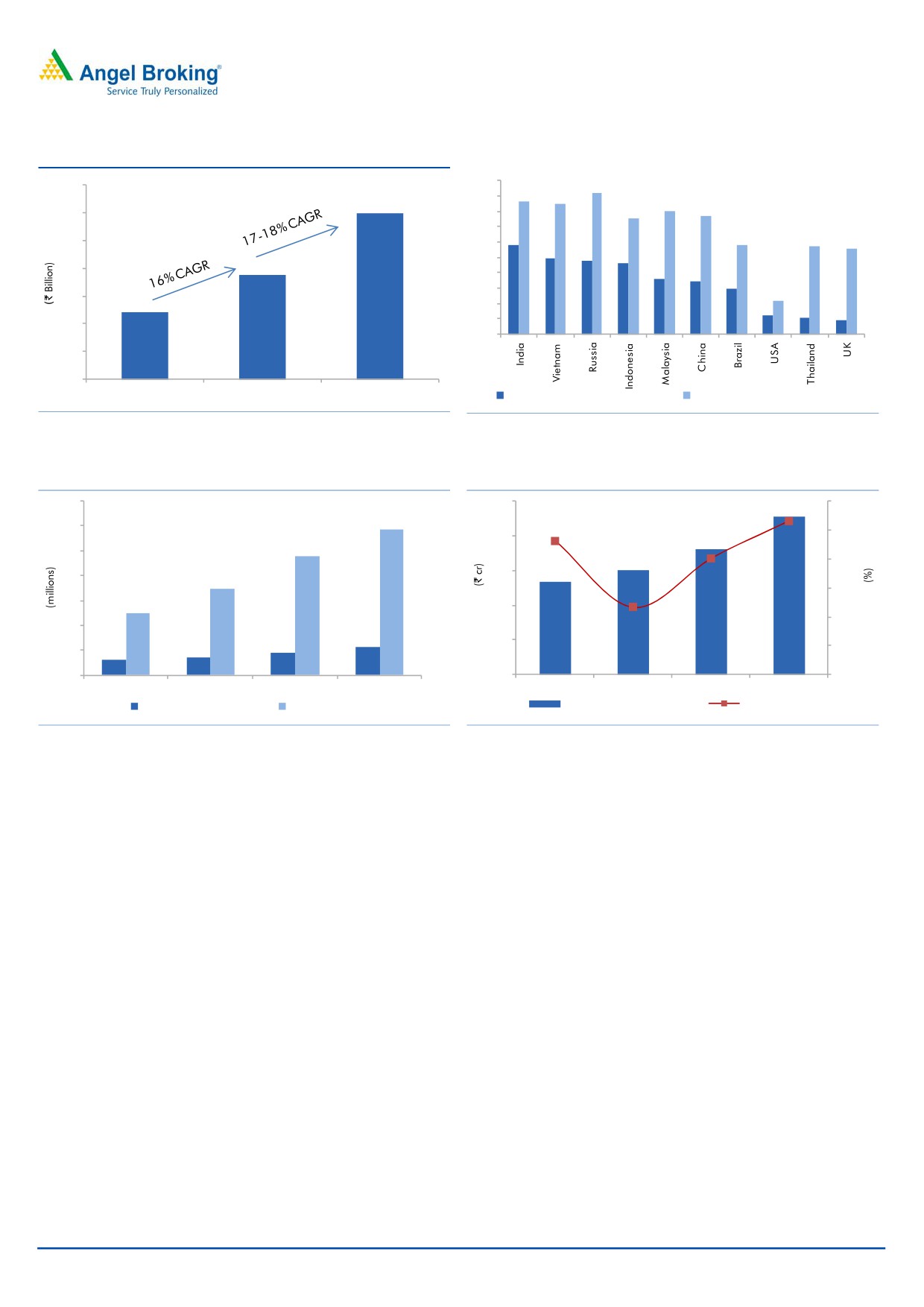

As per CRISIL, the Indian diagnostic industry which has grown at a CAGR of ~16%

over FY2012-2015 to `37,700cr, is expected to maintain its momentum and grow

at 16-18% CAGR to reach the ~`60,000cr mark by FY2018E. This growth is likely

to be supported by rising awareness towards wellness and a higher tendency

among the population to take preventive actions against diseases. Changing

lifestyle is perpetuating higher chronic diseases and with rising income levels,

demand for diagnostic testing in India is on the rise. Further, the health insurance

penetration level in India is currently low with ~17% of the population availing to

it. Moreover, ~86% of the healthcare related expenses are borne directly by

consumers in case of private healthcare services. Increase in penetration levels of

health insurance is expected to indirectly increase demand for diagnostic services.

Of the diagnostic market large pan-India chains account for 35-40% and regional

chains cover the balance 60-65%. Also, they can eat into unorganised sectors

market share which stands at 48%. This leaves a lot of room for organised players

like Dr Lal Pathlabs, Thyocare and SRL amongst others to grow faster than the

industry. Thyocare has posted a CAGR of 23.0% over FY2011-2015. Going

forward, given the cash rich balance sheet of the company, it can easily grow at

30% over the medium term.

April 26, 2016

3

Thyrocare Technologies | IPO Note

Exhibit 2: Indian diagnostic sector

Exhibit 3: Out-of-pocket spending on healthcare (2013)

700

100

92

86

85

90

80

75

77

600

80

600

70

58

58

57

56

500

60

49

48

46

50

400

36

34

40

30

377

30

22

300

20

12

11

9

10

200

240

0

100

-

FY12E

FY15E

FY18E

OOP % of Total Healthcare Expend. OOP % of Pvt. Healthcare Expend.

Source: RHP, Angel Research

Source: WHO Global Healthcare Expenditure Database, Angel Research

Exhibit 4: Strong growth in Samples and Tests

Exhibit 5: Standalone top-line growth

70

250

30.0

26.5

58.60

60

228

25.0

200

20.1

47.84

23.1

50

20.0

180

150

40

34.90

150

15.0

134

30

25.03

100

11.7

10.0

20

11.36

9.09

50

6.28

7.01

5.0

10

-

-

-

FY2013

FY2014

FY2015

FY2016E

FY2013

FY2014

FY2015

FY2016*

No of samples processed

No of tests conducted

Standalone Revenue (LHS)

yoy growth (RHS)

Source: Company, Angel Research

Source: Company, Angel Research; note*9M annualised

A differentiated model enables higher margins

Thyrocare’s business model differs from that of its competitors in a couple of ways.

One of the striking difference is that unlike other organized players, which mostly

follow a B2C model, Thyrocare is more of a B2B player with ~85% of its revenues

coming through the channel (as against 30-40% for its peers). This enables the

company to keep its other expenditure lower vis-a-vis its peers, which spend higher

on promotional expenses. In terms of services, the company is more focused on

the preventive & wellness, and the non-preventive segments, while its peers follow

a portfolio model of providing a full range of tests and services, which entail

higher manpower costs. The company’s operations are relatively more automated

in nature, thereby requiring less manpower intervention, unlike its peers which

need to employ qualified manpower like Phds and doctors. As a result, employee

costs for Thyrocare account for 10% of sales V/s 20% of sales for its peers. This

contributes towards the company enjoying better margins compared to the industry

(~41% for Thyrocare’s diagnostic business V/s ~26% for Dr Lal Pathlabs). We

believe, over the medium term the company would be able to sustain its margins

and also scale up its business, given the opportunities in the industry. This coupled

with the low capex requirement for the diagnostic segment makes it a high ROIC

business.

April 26, 2016

4

Thyrocare Technologies | IPO Note

The company’s standalone business derived ~51% of its FY2015 revenues from

wellness and preventive healthcare tests segment. This segment grew at a CAGR of

~29% over FY2013-15E while the overall top-line posted a growth of ~16% over

the same period. Going forward, CRISIL estimates that this segment is expected to

grow at 25% over the next three years which augurs well for the company as the

company is keen on growing its wellness and preventive offerings.

Core business asset light in nature, debt free status

The company’s volumes and strong ties with its vendors has enabled it to develop

an equipment leasing model for the CPL that has resulted in minimal capex for its

otherwise expensive diagnostic equipments. The model entails leasing of

equipments and instruments for the CPL in exchange for a commitment to

purchase reagents and consumables from these vendors for a specified period of

time. The RPLs conduct routine tests which do not require complex equipments;

hence, the capex required for equipments is minimal and the same are purchased

outright by the company. Additionally, the premises required to set up these RPLs

are leased, thus resulting in lower capital outlay to set up these RPLs (`2-3cr

required for set up a RPL). As a result, the company has been able to expand its

operations without relying on debt. The company as of 9MFY2016 has no debt on

its books.

Low capex requirements and high asset turnover along with high margins enable

the company to generate high ROIC on the core diagnostic business, which is

around ~40%. This will enable the company to fund its growth with ease and

warrant it to make a high dividend payout. In fact it has cash and bank and

investments of `91cr as of FY2015 on a consolidated basis. The net cash flow

from operating activities is around `40-45cr/year and will be used to fund the next

phase of growth.

Valuation

The company is valued at a P/E multiple of 42.3-44.9x its FY2016E annualised

EPS at the lower and upper end of the issue price band. This compares with a P/E

multiple of 61.9x FY2016E EPS for Dr Lal Pathlabs. Although the issue seems to be

priced at a discount to Dr Lal Pathlabs, we believe that Thyocare’s profitability will

come under pressure in the near term as it has entered the molecular imaging

space by acquiring Nuclear Healthcare Ltd (NHL). According to the company, this

business will take 3-4 years to attain peak profitability while it accounts for almost

40% of the fixed assets of the company (as on 9MFY2015). Thus, though

Thyrocare could potentially provide listing gains, the pressure on its ROIC in the

near term and the not-so cheap valuation demanded by it will keep the upside in

the stock limited. We are Neutral on the issue.

April 26, 2016

5

Thyrocare Technologies | IPO Note

Risks to upside

Highly fragmented market with intense local competition (standalone centers

are 48% of the industry).

High dependence on preventive wellness which accounts for almost 51% of its

sales with thyroid tests accounting for 20% of the overall sales.

High investments in the imaging business with high gestation periods would

keep the profitability in check.

Margins could be under pressure in case the company moves higher in the

value chain.

April 26, 2016

6

Thyrocare Technologies | IPO Note

Consolidated Profit & Loss Statement

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

9MFY2016

Gross sales

107

131

146

175

169

Less: Excise duty

-

-

-

-

-

Net sales

107

131

146

175

169

Other operating income

2.5

3.5

3.7

8.3

6.9

Total operating income

109

134

150

183

176

% chg

40.1

23.1

11.7

22.0

(3.9)

Total expenditure

60

71

81

111

104

Net raw materials

29

36

43

56

51

Personnel

7

9

12

18

17

Other

24

26

27

38

37

EBITDA

47

60

65

63

65

% chg

37.6

28.9

8.4

(2.3)

2.1

(% of Net Sales)

43.6

45.9

44.4

36.3

38.3

Depreciation& amortisation

2

3

6

13

13

Interest & other charges

-

-

-

-

-

Other income

5

6

7

7

5

(% of PBT)

-

9

-

11

7

Share in profit of Associates

-

-

-

-

-

Recurring PBT

52

62

69

66

63

% chg

Extraordinary expense/(Inc.)

-

(12)

-

-

-

PBT (reported)

52

74

69

66

63

Tax

17.07

21.06

22.74

23.07

22.98

(% of PBT)

30.6

32.7

32.0

34.8

36.5

PAT (reported)

35

57

46

43

40

Add: Share of earnings of asso.

-

-

-

-

-

Less: Minority interest (MI)

-

-

-

(1)

-

Prior period items

-

-

-

-

-

PAT after MI (reported)

35

57

46

44

40

ADJ. PAT

35

45

46

44

40

% chg

40.8

28.3

3.0

(3.7)

(9.9)

(% of Net Sales)

32.8

43.5

31.6

25.4

23.7

Note: Consolidated for FY2015 and 9MFY2016

April 26, 2016

7

Thyrocare Technologies | IPO Note

Consolidated Balance Sheet

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

9MFY2016

SOURCES OF FUNDS

Equity share capital

11

11

11

51

54

Preference Capital

-

-

-

-

-

Reserves & surplus

92

149

195

224

314

Shareholders funds

102

160

206

274

367

Minority Interest

-

-

-

36.0

-

Total loans

31

32

32

12

11

Deferred tax liability

(0)

0

1

(1)

(2)

Total liabilities

133

193

239

321

377

APPLICATION OF FUNDS

Net block

20

75

87

151

152

Capital work-in-progress

-

10

6

6

3

Goodwill

-

-

-

45

107

Long Term Loans and Adv.

3

5

6

14

10

Investments

24.0

77.2

119.0

85.9

81.6

Current assets

90

28

27

26

37

Cash

59

18

12

5

7

Loans & advances

22

2

4

9

14

Other

9

9

11

12

16

Current liabilities

3

4

6

7

14

Net current assets

86

24

21

19

23

Mis. Exp. not written off

-

-

-

-

-

Total assets

133

193

239

321

377

Note- Consolidated for FY2015 and 9MFY2016

April 26, 2016

8

Thyrocare Technologies | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

April 26, 2016

9