IPO Note | E-commerce

March 19, 2016

Infibeam Incorporation

NEUTRAL

Issue Open: March 21, 2016

IPO Note

Issue Close: March 23, 2016

Infibeam Incorporation Ltd (Infibeam) is an e-commerce company focused on

Issue Details

developing integrated and synergistic e-commerce business models. Its

operations can be broadly categorized as BuildaBazaar (BaB) e-commerce

Face Value: `10

marketplace and E-retail website Infibeam.com. BaB provides cloud-based,

Present Eq. Paid up Capital: `42.7cr

modular and customizable digital solutions and other value added services to enable

merchants to set up online storefronts. Infibeam.com is a multi-category E-retailer where

Fresh Issue**: 1.04cr Shares

it has more than 5,000 registered merchants while it sells its own products as well.

Offer for sale: NIL

E-retail posting strong growth, Infibeam lags: At the moment, the penetration of

Post Eq. Paid up Capital: `53.1cr

internet users in India is at 19%, which is lower compared to countries like the US

(87%) and China (46%). With an expected improvement in the number of internet

Market Lot: 34 Shares

users in the country, the on-line shopper base is expected to improve from the

Fresh Issue (amount): `450cr

present 35mn to 180mn by 2020. As a result, the E-retail market size in India is

expected to grow from US$7bn in 2015 (1.2% of total retail) to US$44bn (4.0% of

Price Band: `360-432

total retail) in 2020. This positive outlook for the E-retail industry augurs well for

Post-issue implied mkt. cap `1,986cr*-

e-commerce players. Despite such strong anticipated growth rate of the industry,

2,294cr**

Infibeam suffers from having smaller scale, absence of funding and lacks the customer

Note:*at Lower price band and **Upper price band

mindshare that the other larger players like Flipkart have garnered. In the past, it (CAGR

of 22% over FY2012-15 to `221) has not been able to match the revenue growth of

bigger players like Flipkart India (CAGR of 260% over FY2012-15 to `9,537).

Book Building

Higher focus on the profitable BaB marketplace business: The BuildaBazaar

QIBs

75%

business of the company has grown at a CAGR of ~119% over FY2011-15 to

Non-Institutional

15%

`67cr. As a result, its contribution to the company’s overall top-line has increased

from negligible levels in FY2011 to 28.3% in 1HFY2016. The business’ operating

Retail

10%

margin stood at 58.0% for 1HFY2016. Thus, the BaB business is totally mitigating

the E-retail business’ losses. Going forward, the company intends to use part of

IPO proceeds to scale up its BaB business. However, the BaB business is in the

Post Issue Shareholding Pattern(%)

nascent stage and considering that technological landscape being dynamic, this

Promoters Group

45.5

makes BaB a high risk reward venture.

MF/Banks/Indian

Outlook Valuation: Infibeam’s E-retail business has a similar model as Flipkart

FIs/FIIs/Public & Others

54.5

and Snapdeal, but is significantly smaller than the two dominant players which

have strong PE backup. Its other business, i.e. BaB, in revenue terms is also

smaller (`67cr FY2015) compared to global players like Shopify.com (US$205mn

CY2015). Moreover, even if BaB business does gain dominant position in India, it

is insufficient to justify the valuation. Considering this, we believe that the EV/Sales

multiple of 4.3x-5.2x demanded by the company is steep. Given that the

company is still evolving, has an unproven profitability track record and the

expensive valuation, we have a Neutral recommendation on the issue.

Key Financial

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

1HFY2016

Net Sales

128

151

207

288

171

% chg

-

18.2

37.2

39.0

-

Net Profit

(11)

(25)

(26)

(10)

7

% chg

-

-

-

-

-

OPM (%)

(7.7)

(14.6)

(9.8)

(0.8)

6.8

Amarjeet S Maurya

EPS (`)

(2.5)

(5.8)

(6.1)

(2.3)

1.5

+91 22 4000 3600 Ext: 6831

P/E (x)

-

-

-

-

-

P/BV (x)

213.6

76.5

22.3

8.7

-

RoE (%)

-

-

-

-

-

Milan Desai

RoCE (%)

-

-

-

-

-

EV/Sales (x)

14.8

12.5

8.9

6.2

-

+91 22 4000 3600 Ext: 6846

EV/EBITDA (x)

-

-

-

-

-

Source: Company, Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end of price band

Please refer to important disclosures at the end of this report

1

Infibeam Incorporation | IPO Note

Company background

Infibeam is an e-commerce company focused on developing an integrated and

synergistic e-commerce business model. The company owns and operates

Infibeam BuildaBazaar (BaB) e-commerce marketplace and E-retail website

Infibeam.com. It has also launched its .ooo top level domain registry service which

helps attract merchants to its e-commerce platform.

BaB provides cloud-based, modular and customizable digital solutions and other

value added services to enable merchants to set up online storefronts. BaB has

features that include comprehensive catalog management system that enables

businesses to manage their products and enables merchants to manage/fulfill/ship

orders. BaB also provides cost-effective marketing solutions and access payment

gateways amongst other features. Infibeam’s registered merchant base on BaB

marketplace as of December 2015 stood at 48,274.

The company’s E-retail website Infibeam.com is a multi-category E-retailer with

more than

15mn SKUs of products across

40 product categories (as on

31st December 2015). The company directly sells a wide range of products on

Infibeam.com, particularly focused on fast moving product categories. Apart from

selling its products, Infibeam had more than 5,000 registered merchants on its

E-retail website and more than 7.8mn active users as of December 31, 2015.

As of December 31, 2015, it had six warehouses and 12 logistics centers across

11 cities in India. It also had more than 900 employees which include a large

number of software engineers and IT experts.

Exhibit 1: Buildabazaar pricing and plans

Source: Company, Angel Research

March 19, 2016

2

Infibeam Incorporation | IPO Note

Issue details

The company is raising `450cr through fresh issue of equity shares in the price

band of `360-432. The fresh issue will constitute 19.6% of the post-issue paid-up

equity share capital of the company assuming the issue is subscribed at the upper

end of the price band.

Exhibit 2: Shareholding pattern

Particulars

Pre-Issue

Post-Issue

No. of shares

(%)

No. of shares

(%)

Promoters

2,41,65,455

56.6

2,41,65,455

45.5

Others

1,85,09,200

43.4

2,89,25,867

54.5

Total

4,26,74,655

100.0

5,30,91,322

100.0

Source: Company, Angel Research

Objects of the offer

Setting up of cloud data center and purchase of property for shifting of the

registered and corporate office of the company. The company estimates to

deploy `235cr for the said purpose.

~`38cr will be utilized for setting up 75 logistics centers.

`67cr is proposed to be used for purchase of software.

The balance will be used for general corporate purposes.

March 19, 2016

3

Infibeam Incorporation | IPO Note

Investment rationale

E-retail posting strong growth, Infibeam lags

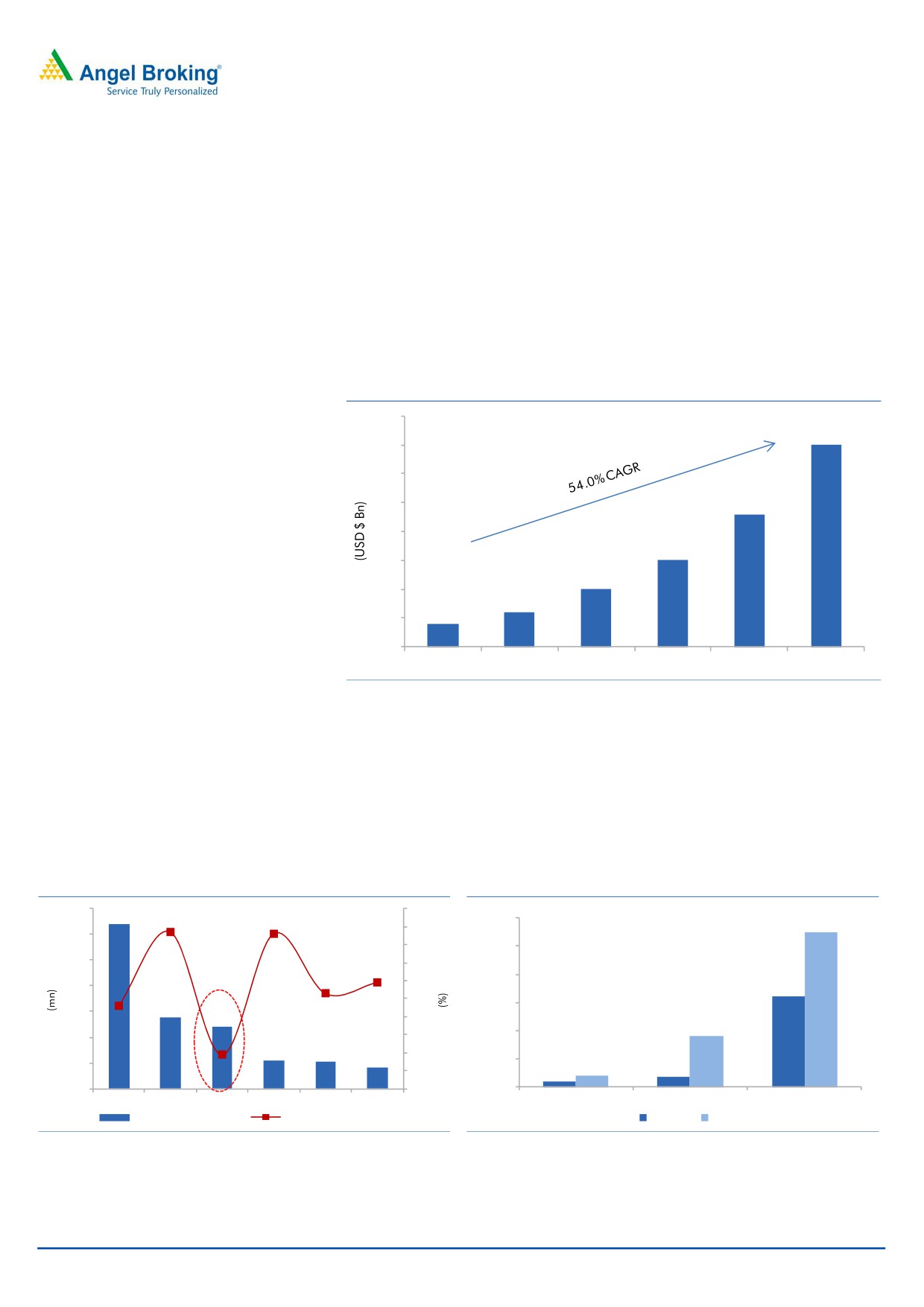

The E-retail market is among the fastest growing markets in India which is

estimated to have posted a CAGR of ~54.0% over CY2009-14 as per industry

reports. This has been on the back of factors such as improved internet

connectivity, discounted prices, convenient payment options, and customer friendly

return policies. Going forward, E-retail is expected to continue to grow on the back

of rising number of internet users and online buyers.

Exhibit 3: India E-retail growth

4.0

3.5

3.5

3.0

2.5

2.3

2.0

1.5

1.5

1

1.0

0.6

0.4

0.5

-

2009

2010

2011

2012

2013

2014

Source: IAMAI, CRISIL, Gartner, PwC

As per industry reports, there were an estimated 243mn internet users in India

(data as of 2014) in comparison to 279mn in the US and 641mn in China.

Internet penetration level in the country is lower at 19% compared to 46% in China

and 87% in the US, thus signaling significant scope of improvement. Of the

present ~318mn (estimated as of 2015 on basis of RHP data) internet users in

India, ~11% or 35mn are estimated to be shopping on-line.

Exhibit 4: Internet user base and Penetration (2014)

Exhibit 5: Projected user base and Penetration

700

100.0

600.0

550

90.0

600

87.0

86.0

80.0

500.0

500

70.0

59.0

53.0

400.0

400

60.0

320

46.0

50.0

300.0

300

19.0

40.0

180

200.0

200

30.0

20.0

100.0

100

40.0

35

10.0

19.0

641

279

243

109

107

84

-

-

-

China

US

India

Japan

Brazil

Russia

Internet Penetration

(%) On-line Shoppers (mn) Internet User Base (mn)

Internet User Base (LHS)

Internet Penetration (RHS)

Current

2020E

Source: PwC, Angel Research

Source: Company, Angel Research

March 19, 2016

4

Infibeam Incorporation | IPO Note

Driven by increasing penetration of smart phones and roll out of 4G internet

services, the internet user base is expected to grow to 550mn and the penetration

level is expected to reach ~40% by 2020. Consequently, the on-line shopper base

is estimated to grow from 35mn currently to 180mn over the same period. Led by

increasing internet users and on-line shopper base, the E-retail market size is

expected to grow from US$7bn in 2015 (1.2% of total retail) to US$44bn (4.0% of

total retail) in 2020.

Despite such strong anticipated growth rate of the industry, Infibeam suffers from

having smaller scale, absence of funding and lacks the customer mindshare that

the other larger players like Flipkart have garnered. In the past, it (CAGR of 22%

over FY2012-15 to `221) has not been able to match the revenue growth of

bigger players like Flipkart India (CAGR of 260% over FY2012-15 to `9,537).

Exhibit 6: E-retail and future prospects

2015

2020

Total Retail (USD bn)

585

1,100

Organized Retail (USD bn)

53

190

E-tail (% Total Retail)

1.2%

4.0%

E-tail (% Organized Retail)

13.0%

24.0%

Source: Company, Angel Research

Focus on profitable BaB market business

Apart from significant portion (~72% as on 1HFY2016) of the revenues derived

from the sale of products via its E-retail website Infibeam.com, the company also

generates revenue from solutions provided through BaB market place. The revenue

from sale of software and e-commerce related ancillary services has grown at a

CAGR of 118.7% over FY2011-15 to `67cr and the segment has posted revenue

of `48cr for 1HFY2016. The BaB business is profitable compared to products

business with margins at 58% for 1HFY2016. Going forward, the company intends

to scale up its BaB business by boosting its IT infrastructure and logistics

capabilities, strengthening merchant acquisitions, and increasing value added

offerings. The company has steadily increased the share of the non-products

business to

28.3% of total revenues as of 1HFY2016 and its increasing

contribution will support the overall profitability of the company. However, the BaB

business is in the nascent stage and considering that technological landscape being

dynamic, this makes BaB a high risk reward venture.

March 19, 2016

5

Infibeam Incorporation | IPO Note

Exhibit 7: Segmental break up

Particulars

FY2012

FY2013

FY2014

FY2015

1HFY2016

Revenue

Sale of products

123

139

177

221

123

change yoy (%)

140.3

13.2

26.9

25.4

% of total

96.1

92.0

85.1

76.8

71.7

Sale of software and e-commerce related ancillary services

5

12

31

67

48

change yoy (%)

71.2

140.8

155.7

117.2

% of total

3.9

8.0

14.9

23.2

28.3

Total net sales

128

151

207

288

171

Profit

Sale of products

(5)

(13)

(19)

(23)

(5)

% of sales

(3.9)

(9.1)

(10.7)

(10.4)

(3.9)

Sale of software and e-commerce related ancillary services

2

6

19

40

28

% of sales

35.5

49.4

62.6

59.8

58.0

Unallocated Expenses

7

17

27

29

19

Total

(10)

(24)

(26)

(12)

4

Source: Company, Angel Research

Valuation

Infibeam’s E-retail business has a similar model as Flipkart and Snapdeal, but is

significantly smaller than the two dominant players which have strong PE backup.

Its other business, i.e. BaB, in revenue terms is also smaller (`67cr FY2015)

compared to global players like Shopify.com (US$205mn CY2015). Moreover,

even if BaB business does gain dominant position in India, it is insufficient to justify

the valuation. Considering this, we believe that the EV/Sales multiple of 4.3x-5.2x

demanded by the company is steep. Given that the company is still evolving, has

an unproven profitability track record and the expensive valuation, we have a

Neutral recommendation on the issue.

Risks

Intense competition: The company faces intense competition from players like

Flipkart, Snapdeal, etc for its E-retail business which entails heavier discounting to

gain market share, thus resulting in higher operating losses for the business.

Unproven track record for profitability: The company has reported continuous

losses from `18cr in FY2011 to `10cr in FY2015. Although, it has reported

maiden profits amounting to `6cr in 1FY2016 there lacks a proven track record in

terms of profitability.

Government regulatory issues: Any unfavourable regulations for internet and

ecommerce industry can have a negative impact on the company’s business

growth.

March 19, 2016

6

Infibeam Incorporation | IPO Note

Profit & Loss (consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

1HFY16

Total operating income

128

151

207

288

171

% chg

-

18.2

37.2

39.0

-

Total Expenditure

138

173

228

291

160

Raw Material

120

134

168

223

118

Employee Cost

7

11

22

21

13

Other Expenses

11

29

37

47

29

EBITDA

(10)

(22)

(20)

(2)

12

% chg

-

-

-

-

-

(% of Net Sales)

(7.7)

(14.6)

(9.8)

(0.8)

6.8

Depreciation& Amortisation

1

3

7

13

8

EBIT

(11)

(25)

(28)

(15)

3

% chg

-

-

-

-

-

(% of Net Sales)

(8.7)

(16.6)

(13.4)

(5.3)

2.0

Interest & other Charges

1

1

1

1

1

Other Income

1

1

2

7

3

(% of PBT)

(12.1)

(5.7)

(6.4)

(71.0)

54.0

Recurring PBT

(11)

(25)

(27)

(10)

6

% chg

-

-

-

-

-

Prior Period & Extra. Exp/(Inc.)

-

-

-

-

-

PBT (reported)

(11)

(25)

(27)

(10)

6

Tax

-

-

0

0

-

(% of PBT)

-

-

(0.0)

(0.1)

-

PAT before MI & Adj. (reported)

(11)

(25)

(27)

(10)

6

Extraordinary Items

-

-

-

-

-

Less: Minority interest (MI)

-

0

1

1

0

Less: Share of Associates

(0)

0

(0)

(1)

(0)

ADJ. PAT

(11)

(25)

(26)

(10)

7

% chg

-

-

-

-

-

(% of Net Sales)

(8.5)

(16.5)

(12.5)

(3.4)

3.8

Basic EPS (`)

(2.5)

(5.8)

(6.1)

(2.3)

1.5

Fully Diluted EPS (`)

(2.5)

(5.8)

(6.1)

(2.3)

1.5

% chg

-

-

-

-

-

March 19, 2016

7

Infibeam Incorporation | IPO Note

Balance Sheet (consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

1HFY16

SOURCES OF FUNDS

Equity Share Capital

30

38

40

43

43

Reserves& Surplus

(29)

(14)

43

170

183

Equity Application Money

8

-

-

-

-

Shareholders’ Funds

9

24

83

213

225

Minority Interest

2

2

1

0

-

Total Loans

55

43

9

5

5

Long-term provisions

1

0

1

1

1

Other long term liabilities

-

-

-

-

0

Total Liabilities

66

69

93

219

232

APPLICATION OF FUNDS

Gross Block

17

31

56

75

92

Less: Acc. Depreciation

8

11

17

30

39

Net Block

9

20

39

45

54

Capital Work in Progress

4

6

8

26

24

Goodwill

5

5

6

6

6

Investments

0

0

-

-

-

Current Assets

15

51

37

121

148

Inventories

2

5

9

12

18

Sundry Debtors

7

36

17

33

43

Cash

1

4

4

60

70

Loans & Advances

4

6

5

11

11

Other Assets

0

1

1

5

6

Current liabilities

8

51

42

49

52

Net Current Assets

6

0

(5)

72

96

Long term loans and advances

41

38

44

69

52

Other Non Current Assets

0

0

1

0

0

Mis. Exp. not written off

-

-

-

-

-

Total Assets

66

69

93

219

232

March 19, 2016

8

Infibeam Incorporation | IPO Note

Cash Flow Statement (consolidated)

Y/E March (`cr)

FY2012

FY2013

FY2014

FY2015

1HFY16

Profit before tax

(11)

(25)

(27)

(10)

6

Depreciation

1

3

7

13

8

Change in Working Capital

(31)

9

(2)

(18)

(17)

Interest / Dividend (Net)

1

1

0

(3)

(3)

Direct taxes paid

0

(0)

(1)

(5)

(1)

Others

(1)

2

12

2

2

Cash Flow from Operations

(40)

(11)

(11)

(21)

(3)

(Inc.)/ Dec. in Fixed Assets

(5)

(16)

(15)

(50)

9

(Inc.)/ Dec. in Investments

(0)

(1)

(2)

(41)

10

Cash Flow from Investing

(6)

(17)

(17)

(91)

19

Issue of Equity

-

7

65

123

-

Inc./(Dec.) in loans

48

24

(37)

45

(6)

Dividend Paid (Incl. Tax)

-

-

-

-

-

Interest / Dividend (Net)

(1)

(1)

(0)

(1)

(0)

Cash Flow from Financing

47

30

28

168

(6)

Inc./(Dec.) in Cash

1

3

1

56

10

Opening Cash balances

0

1

4

4

60

Acquisition / (sale) of business

-

(0)

0

-

-

Closing Cash balances

1

4

4

60

70

March 19, 2016

9

Infibeam Incorporation | IPO Note

Key Ratios

Y/E March

FY2012

FY2013

FY2014

FY2015

Valuation Ratio (x)

P/E (on FDEPS)

-

-

-

-

P/CEPS

-

-

-

557.1

P/BV

213.6

76.5

22.3

8.7

Dividend yield (%)

0.0

0.0

0.0

0.0

EV/Sales

14.8

12.5

8.9

6.2

EV/EBITDA

-

-

-

-

EV / Total Assets

25.5

15.8

13.7

6.7

Per Share Data (`)

EPS (Basic)

(2.5)

(5.8)

(6.1)

(2.3)

EPS (fully diluted)

(2.5)

(5.8)

(6.1)

(2.3)

Cash EPS

(2.2)

(5.1)

(4.3)

0.8

DPS

0.0

0.0

0.0

0.0

Book Value

2.0

5.6

19.3

49.8

Returns (%)

ROCE

-

-

-

-

Angel ROIC (Pre-tax)

-

-

-

-

ROE

-

-

-

-

Turnover ratios (x)

Asset Turnover (Gross Block)

7.5

4.9

3.7

3.8

Inventory / Sales (days)

5

13

15

16

Receivables (days)

21

86

30

42

Payables (days)

14

92

44

26

Wc cycle (ex-cash) (days)

12

7

2

31

Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

March 19, 2016

10

Infibeam Incorporation | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

March 19, 2016

11