Calculate your SIP ReturnsExplore

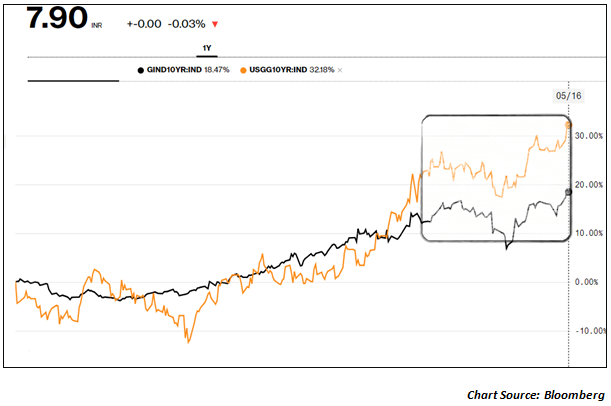

From the time the minutes of the last monetary policy were announced in the third week of April 2018, the bond yields on the 10-year benchmark have gone up sharply and are now inching closer to the 8% mark. There are two explanations for this sharp rise in bond yields. Firstly, the higher inflation implication due to higher Kharif prices and higher crude oil prices is one trigger for the rising yields. Secondly, the US 10-year benchmark has already crossed the 3% mark and it is expected that the RBI may hike rates to keep the yield differential intact. That will prevent rapid capital outflows of the kind we saw in 2013 at the peak of the currency crisis. Check the chart below:

Obviously, the bond yields in the US are rising much faster than in India in the last 1 year. Even other economies like Germany have seen a rise in 10-year bond yields at a rate faster than India. This has opened up the possibility that the RBI could also hike rates by 25-50 basis points in this calendar year. What would be its implications?

There is a conservative target of the RBI hiking rates by 25 basis points during the year and a worst case scenario of rates hiked by 50 basis points. What will be the implications of such a rate hike by the RBI?

All is not so bad if rates are actually hiked. A study in the US has proved that if the rate hikes are a reaction to higher inflation and growth, then rate hikes can actually be value accretive or the economic over the next 3-5 years. Here is hoping it really works out in practice!

Enjoy Zero Brokerage on Equity Delivery

Join our 2 Cr+ happy customers

Get the link to download the App

Enjoy Zero Brokerage on

Equity Delivery