Calculate your SIP ReturnsExplore

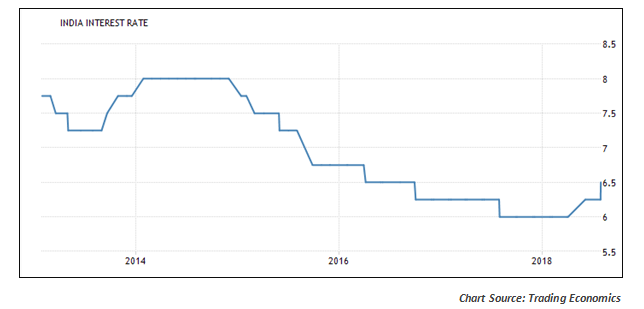

While the bond markets had factored another rate hike during calendar year 2018, they had really not bargained for two rate hikes in succession. But, that is exactly what the Monetary Policy Committee (MPC) did on August 01st. After a 2-day meeting, the MPC decided to effect the second 25 basis point hike in the repo rate in less than 2 months. This effectively takes the rate to 6.50%.

Broadly there were five reasons for the MPC to push through the rate hike in August itself, instead of waiting for more data points in the next few months.

While the June rate hike was a unanimous vote among the 6 members of the Monetary Policy Committee, August MPC meet had one dissenting voice in the form of Dr. Ravindra Dholakia who called for status quo on rates in the August policy. However, there could be 5 indications that the policy rate hikes may have been front-ended on the side of caution.

In a nutshell, the decision to front-end the rate hike may be a bet by the RBI that the impact of fuel and food may not be too steep on overall inflation. The current rate scenario prepares for up to 5% inflation by next year. The signal is that unless inflation threatens to go above that level, the RBI will not be too keen on further rate hikes. That may be the key takeaway for the financial markets in India!

Enjoy Zero Brokerage on Equity Delivery

Join our 2 Cr+ happy customers

Get the link to download the App

Enjoy Zero Brokerage on

Equity Delivery