Calculate your SIP ReturnsExplore

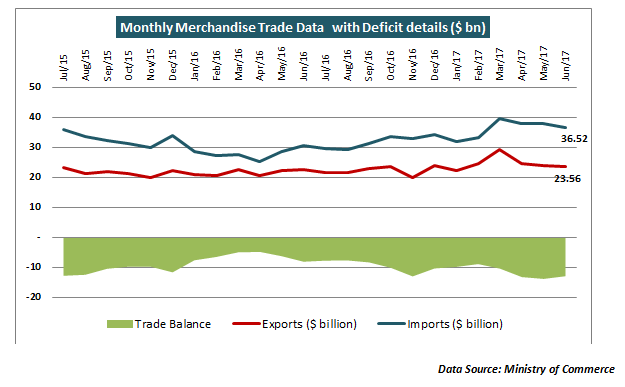

The trade data for the first four months of fiscal year 2017-18 has followed a standard pattern. Exports have been on an uptrend but imports in each of the months have been growing much faster. In fact, the average monthly trade deficit has also settled at a much higher plane compared to what we had seen in the previous fiscal year. Above all the net trade deficit combining the merchandise trade deficit and the services surplus has been on an uptick. Let us look at the chart below to get a grasp of how the trade data has patterned over the last year…

How the exports panned out for June 2017…

Exports for the month of June were up by 4.39% at $23.56 billion compared to the year-ago period. India showed a healthy growth in most of the key commodity exports for the month of June. While engineering goods and organic chemicals grew by over 14%, there was a 25% growth in rice exports and in the export of marine products. For the first 3 months of the current fiscal year (Apr-Jun), the total exports came in at $72.21 billion, a growth of 10.6% over the corresponding quarter last year. But that may not be a good comparison as in 2016 the world economy was just coming out of a mini-shock in the aftermath of the Fed hiking rates for the first time in 9 years in December 2015. On the exports front, the big worry continues to be the INR which has displayed strength. In fact, the INR was already overpriced to the extent of around 20% in REER terms when it was around the 68/$ level. That overvaluation would have only worsened with the INR settling closer to the 64.5/$ levels. That is something the RBI and the Commerce Ministry must be conscious about.

The worry is on the merchandise imports front…

Imports for the month of June at $36.52 billion were up by 19% on a YOY basis. For the first quarter of the fiscal year, imports were up by 33% at $112.26 billion. On a product-specific basis, the import growth in petroleum has petered down after the sharp growth seen in the previous months. With the Brent Crude staying around the $45/bbl mark, the petroleum import bill for the month of June grew at just about 12%. However, this still underscores the vulnerability of the import bill to sudden spikes in the price of crude. For example, a rise of 10-15% rise in the price of crude oil from current levels could sharply take India’s oil import bill up. That cannot be entirely ruled out as leading brokers like Goldman Sachs are already hinting that the OPEC may not have much of a choice other than a shock-and-awe cut in oil supply. Since India depends on imported crude for 80% of its fuel requirements, the oil import bill remains vulnerable to spikes in global crude oil prices.

But the bigger worry is on non-oil (gold imports)…

Non-oil imports for the month of June were up by 21.2% at over $28 billion with the oil import bill at a little above $8 billion. But within the gamut of non-oil imports, the real worry is on the gold front. For example imports of electrical goods were up by 24% while that of precious and semi-precious stones were up by 86%. However, both are not a worry as they have strong downstream production externalities. The worry is that gold imports for the month of June were up by 102%. This could be partially because of the base effect as last year gold demand was very low due to the jeweller’s strike across India. Combined with festival demand this year, the gold imports have been on a run this year. The problem is that gold does not have productive downstream externalities. Gold is consumption expenditure and the RBI has constantly warned against using up precious forex resources to fund the imports of gold.

Trade deficit is settling at a higher plane…

A quick look at the trade chart shows the merchandise trade deficit settling at around the $13 billion mark on a monthly basis. That means India may end the year with an overall merchandise trade deficit of nearly $160 billion. With monthly imports getting closer to $38 billion, India may end the year with a total import bill of $460 billion. That means the forex reserves, which currently stand at $391 billion, will be sufficient to cover just 10 months of imports. This is a clear weakening compared to 13 months import cover that India enjoyed in the previous fiscal year 2016-17.

Last, but not the least, the services surplus (at $5 billion) has been on a constant downward journey as software exports have been under pressure. That leaves a net trade deficit of close to $8 billion ($13 billion merchandise deficit – $5 billion services surplus) each month after considering the positive impact of the services surplus. That means two key things for the government. Firstly, it needs to urgently move in and curb the gold imports as they are adding to the trade deficit without any concomitant productivity benefits. Secondly, the RBI has been maintaining a strong INR for too long and that is taking a toll on the exports. The sooner a course correction is adopted on both these parameters, the better it will be for India’s external competitiveness.

Enjoy Zero Brokerage on Equity Delivery

Join our 2 Cr+ happy customers

Get the link to download the App

Enjoy Zero Brokerage on

Equity Delivery