Calculate your SIP ReturnsExplore

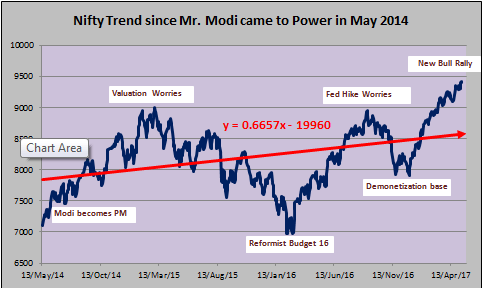

The equity market has been an interesting indicator of the way the Modi government has performed in the last 3 years. The market, being what it is, has always given more weightage to hope and expectations. Typically, markets have bought into hope, enhanced positions into expectations and sold into performance. The rally in the Nifty started well before the elections and actually peaked out in March 2015 after Arun Jaitley announced his maiden budget. From that point, it was a one-way journey downwards on the back of valuation concerns as well as rate tightening by the US Fed. The Nifty did manage to make a bottom on Budget day 2016 and showed a secular rally from then on, except for a minor hiccup in the form of the liquidity fears created by demonetization. The last round of market rally that begin around mid-November 2016 is actually in anticipation of the long term changes that a lot of government moves could bring about. That is why it is expected to be a lot more fundamental and a lot more decisive from here on.

The chart above clearly indicates that notwithstanding the fluctuations in the Nifty over the last 3 years they have still kept the market in an uptrend. The positive slope of the trend line as depicted by the equation clearly indicates that the future trend continues to remain positive. There is something interesting to note here. Most of the Nifty tops were created in the last 3 years either due to global events or due to FII concerns over valuations. The bottoms have been created by conscious government initiatives like a reformist budget or the demonetization drive.

As one looks back at the 3 years of the NDA rule, the stock market alone may not be a veritable indicator. The Nifty has given a compounded annual return (CAGR) of just 9.7% over the last 3 years. Also, the markets are virtually static between March 2015 and March 2017. However, there are a lot of positives from a macroeconomic standpoint. Let us look at a few of them…

CPI inflation is lower and WPI inflation is back in positive territory…

Retail inflation had been the big worry during the two years of drought in 2014 and 2015. But that seems to be finally coming under control. The inflation number has not only benefited from lower food and fuel prices, but also due to decongestion of supply side bottlenecks by the government. Heavy investments in infrastructure in rural areas, focus on post-harvest infrastructure and better buffer stock management have gone a long way. Especially, the way the government managed pulses inflation is creditable. The WPI inflation had gone into negative territory due to weak oil prices. That is back in positive territory obviating the risk of deflation. Also the WPI number is under control. That also gives leeway to the RBI on its rates stance.

Reform focus on GST and land reforms…

Notwithstanding the minority in the Rajya Sabha, the government has managed to push key legislations pertaining to GST, land reforms and RERA model code through. GST is likely to create a common market and make the cost of doing business lower. A single rate and efficiencies in logistics will add about 2% to the annual GDP growth. The shift from 7.5% to 9.5% real GDP growth will be a quantum shift for India’s growth trajectory. The central RERA model code has been passed and the state level acts are being implemented. The RERA is likely to put the onus of greater transparency on builders and will protect the interest of buyers. This was long called for to give a boost to real estate sales.

A focus on fiscal responsibility, despite the challenges…

The government has focused on fiscal responsibility despite constant pressure from industry to pump prime the economy. This debate is as old as the hills as to whether your fiscal policy should be static or counter cyclical. Most economists and industry bodies were recommending a counter-cyclical fiscal policy. Also known as pump priming, this involves getting lax on fiscal targets to boost growth through greater borrowings. However, the government has preferred to stick to its rigid framework laid out by the FRBM Act to reduce the fiscal deficit to 3.5%. This discipline has been largely responsible for the INR appreciating from the Rs.69/$ levels to the Rs.64/$ levels. Fiscal responsibility is also positive from the point of view of India’s external responsibility.

An attack on black money and the big shift to digital…

Many people over the last few months have focused on the painful impact of demonetization. Undoubtedly, there has been pain and stress but if the subsequent state elections are anything to go by the people at large have welcomed the demonetization move. For starters, demonetization was the starting point for an attack on black money. By forcing nearly Rs.4 trillion of currency to be routed through the banking system, it has forced black money out of the closets. Secondly, it has given a big push to digital India. Look at the sharp increase in the number of e-transactions and the number of e-wallets for digital payments. India has surely changed for the better!

Focus on the bottom of the pyramid…

The recent farm loan waivers by the government were criticised by many detractors as being too populist. However, the government has also initiated silent reforms to better the lot of the rural and semi-urban population in India. The big focus on rural infrastructure and roads is going to be income accretive to the poorer sections. The last two budgets have also focused on crop insurance and rural employment guarantee programs promising to increase the income levels of rural pockets. The big thrust on low-cost housing is also going to be a boon for the lower and middle classes. So, even without straining the fiscal deficit too much, there has been a definite focus on the bottom of the pyramid. And if the government succeeds in doubling farm incomes over the next 5 years, then it would be a big boost to rural incomes and rural demand.

More business with ease of doing business…

One of the underlying themes of the government has been ease of doing business. In the last two years, the “Make in India” program of the government has gone a long way in attracting foreign investments. In fact, the Foreign Direct Investment (FDI) flows over the last 2 years have surpassed that of China, making India the most preferred choice for global investors. India has already moved up in the “Ease of Doing Business” rankings and that is being combined with simpler regulations and easier business environment. All these promise to be value accretive for India.

Has this government been a tad too lucky?

There have been concerns that the government has been a tad too lucky. Here are a few arguments that are normally offered…

While most of these points are, prima facie, true many of them are simply beyond the control of the government. Oil, at the current demand / supply scenario looks unlikely to shoot up sharply in the near future, at least with the volume of US shale in the market. Jobs generation has reduced but that is also partially a result of lower investments and automation. For that the investment cycle needs to pick up which is just about showing green-shoots. While it is true that China’s trade has been affected, the reason India has been growing is its vast domestic market and the ability of domestic demand to sustain. Also the lower trade has helped the forex reserve to cover nearly 12 months of imports, a situation that India has never experienced before.

What is the good news for markets from 3 years of Modi Sarkar?

The good news is that a combination of cheap oil, weak commodity prices, aggressive reforms and a strong rupee could position the Indian markets in a sweet spot. As macro and micro factors combine to spur growth in corporate profits, the valuations could be revised upwards. That is when the P/E re-rating could start all over again. The stage may have been set for a long term rally in equities. The government may have just set the base in the first 3 years of Modi Sarkar.

Enjoy Zero Brokerage on Equity Delivery

Join our 2 Cr+ happy customers

Get the link to download the App

Enjoy Zero Brokerage on

Equity Delivery