Calculate your SIP ReturnsExplore

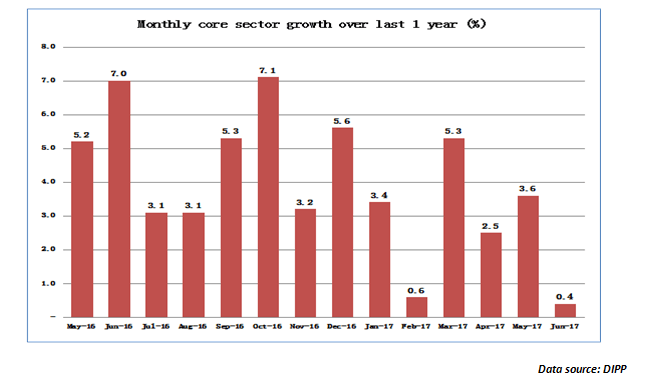

The core sector update for the month of June 2017 came in below expectations at a level of just 0.4%. As is well known, core sector accounts for 40.27% of the constituents of the IIP and hence a positive trend in the core sector is very important for a proper revival in the IIP numbers. The core sector essentially consists of 8 sectors viz. Coal, Crude oil, natural gas, refinery products, fertilizers, steel, cement and electricity. These eight segments represent the core of the economy and have strong externalities. For example, a pick-up in the demand for coal and natural gas has strong implications for power generation in the economy. Similarly, a pick-up in the demand for steel and cement has strong positive cues for the pick-up in construction demand in the economy. The chart below represents how the core sector numbers have panned out over the last one year…

GST actually took its toll on core sector growth…

As the trend-line suggests, the core sector number has been on a clear downtrend over the last 1 year. Two data points stand out. In the month of February 2017, we saw the lag effect of demonetization. In fact, demonetization had resulted in a resource crunch in industry forcing many manufacturers to operate at sub-optimal levels to conserve cash. The second is June 2017. The pressure on the core sector growth is clearly due to the caution among manufacturers regarding the implementation of GST. Most industries across the board focused more on getting rid of the existing inventory rather than on fresh production.

Which sectors contributed positively to the core sector numbers?

Natural gas was the major contributor to higher core sector growth in the month of June at 6.4%. However, this is on a much smaller base and with a much smaller weightage. There is a greater governmental thrust on natural gas considering its environmental friendliness. Also, more capacity is coming on stream and this should show further growth in the coming months. Crude oil production, on the hand, grew by just about 0.6% for the month of June with India still relying heavily on imports of crude to meet its regular requirements. The lower crude prices are also working as a disincentive for oil companies to operate at full capacity. Steel also saw a smart growth in production by 5.8%. Even on a first quarter basis, steel production is up by 6.2%. The government has adopted a pro-industry approach to steel by imposing countervailing duties and MIP on steel imports to curb dumping of steel by China and Russia. This has been a major incentive for Indian steel and that is reflected in the core sector numbers.

Which sectors contributed negatively in the month of June?

Coal production was the big disappointment with a decline of (-6.7%) for the month of June 2017. As Coal India Ltd, India’s largest coal producer has admitted it has serious issues over sustaining output levels. This also has implications for thermal electricity generation as we shall see later. While refinery products were almost flat, fertilizers production was down by (-3.6%). A clear-cut policy on fertilizers is on the cards and the sooner the government moves on it the better it will be for the fertilizer sector. Cement was a big disappointment with negative growth of (-5.8%). This was more due to tepid demand from the construction sector which has not exactly picked up after the impact of demonetization. However, this could change with the big focus on low-cost housing. Electricity production was up by 0.7% which we still consider disappointing as this looks more due to the impact of inclusion of renewable energy in the calculation. With key power plants operating at below capacity, the thermal power output is actually in the negative zone. Of course, the weak coal production has also been responsible for the same.

Getting a slightly broader picture of core sector growth…

When it comes to core sector growth measurement, the base effect has an inordinate impact. Hence, it may be useful to compare on a longer time basis. For the first quarter of Apr-Jun 2017, the core sector growth was at 2.4%, almost 450 basis points lower than the 6.9% core sector growth recorded in the first quarter of the previous fiscal. The message appears to be that sectors where a clear government thrust is visible as in the case of steel and natural gas, the core sector performance is actually commendable. That may be the key take-away from the core sector numbers!

Enjoy Zero Brokerage on Equity Delivery

Join our 2 Cr+ happy customers

Get the link to download the App

Enjoy Zero Brokerage on

Equity Delivery