Calculate your SIP ReturnsExplore

The IIP numbers for the month of March 2017 came in slightly better than expected. Remember, IIP numbers are normally announced with a 1-month lag as compared to CPI and WPI numbers. Here are some of the key takeaways from the IIP numbers that were announced for the month of March 2017…

Key Takeaways from the IIP announcement for March 2017…

Impact of the changed methodology on annual IIP figure…

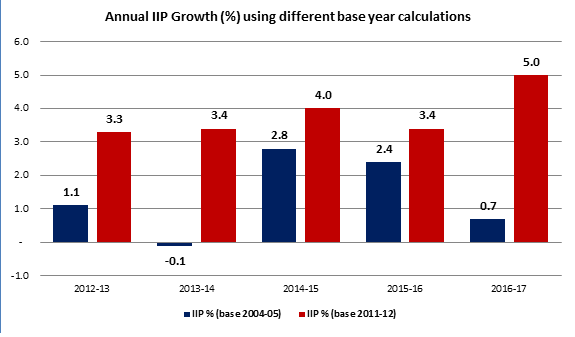

The monthly IIP numbers that we normally analyse have a big drawback in that they are too much influenced by the base effect. If the corresponding period last year was a high IIP month or a low IIP month, then it distorts the picture. A better way to look at the IIIP will be to look at the IIP on annual terms; more so with the completion of the fiscal year 2017-18…

The above chart captures the difference in the IIP growth figure changed retrospectively with a shift in the base year. It is clear for the last 5 years, changing the base for IIP calculation to 2011-12 is resulting in a distinct improvement in the IIP. The RBI may interpret this as a signal that the growth green-shoots are already visible and hence rate cuts may not be required to prop up growth. That is something that will be evident only in the next monetary policy in June.

When one takes a combined view of the recent CPI inflation, WPI inflation, IIP growth and the PMI data, it is clear that there appears to be traction as far as the pick-up in the economy is concerned. How far it translates into GDP growth remains to be seen!

Enjoy Zero Brokerage on Equity Delivery

Join our 2 Cr+ happy customers

Get the link to download the App

Enjoy Zero Brokerage on

Equity Delivery